bank bukopin · •bank bukopin also assists bulog with logistics information and accounting system...

TRANSCRIPT

BANK BUKOPIN

OVERVIEW

As of December 2012

BANK BUKOPIN

Disclaimer

IMPORTANT: The following forms part of, and should be read in conjunction with, this presentation.

This report is prepared by PT. Bank Bukopin Tbk independently and is circulated for the purpose of general information only. It is not intended to the specific person who may receive this report. No warranty (expressed or implied) is made to the accuracy or completeness of the information. Some of the statements contained in this document contain “forward looking” statements with respect to the financial conditions, results of operations and businesses, and related plans and objectives. These Statements do not directly or exclusively relate to historical facts and reflect the Company’s current intentions, plans, expectations, assumptions and beliefs about future events. The Statements involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those in the statements as originally made. Such statements are not, and should not be construed as a representation to future performance of the Company. Readers are urged to view all forward-looking statements contained herein with caution.

2

Table of Contents

Overview

Business Activity

Competitive Strengths

Financial Summary

Strategic Plan

3

Overview

4

Financial Highlight

2012 2011

Time Deposit Savings Current Account

40.7

2012 2011

R:250 G:250 B:0

R:0 G:111 B:192

R:63 G:173 B:92

Total Assets (Rp. Tn)

Total Loans (Rp. Tn)

Total Third Party Deposits (Rp. Tn)

Earning (Rp. Bn)

57.2

2012 2011

65.7

45.5

47.9

11.1

8.0

28.8

13.8

54.0

8.4

31.8

Earning After Tax

2012 2011

940.4

738.2

*

* Audited, Consolidated

** Unaudited

*

*

*

5

Earning Before Tax 1,059.4

830.5

Shareholders Structure as of 31 December 2012

Koperasi Pegawai Bulog Seluruh

Indonesia (KOPELINDO)/ Cooperative of

Bulog Employees

Public

Koperasi Perkayuan

APKINDO MPI (KOPKAPINDO)/ Cooperative of

Indonesia Timber

Government of

Republic of Indonesia

PT Bank Syariah Bukopin PT Bukopin Finance

31.73% 13.04% 9.40% 5.05% 40.78%

88.26% 77.57%

Yayasan Bina Sejahtera Warga

Bulog (YABINSTRA)/ Foundation of

Bulog Employees

6

Industry Position

In billion Rp

Source: Bank’s Publication as of Sept 2012, Bank Only 7

Deposit Rank 13th

Asset Rank 15th

Loan Rank 13th

50,277

56,483

57,899

58,626

58,646

59,193

63,161

65,107

71,436

98,756

101,018

115,053

127,609

133,714

186,743

299,705

421,093

469,018

519,572

STANCHART

BTPN

CITIBANK

UOB INDONESIA

BUKOPIN

MEGA

HSBC

BANK JABAR BANTEN

OCBC NISP

BTN

BII

PERMATA

DANAMON

PANIN

NIAGA

BNI

BCA

BRI

MANDIRI

26,120

39,787

42,583

42,785

46,938

47,166

47,756

50,485

53,618

69,331

79,940

88,531

92,328

99,632

140,723

231,516

357,822

373,137

386,335

STANCHART

CITIBANK

BTPN

HSBC

UOB INDONESIA

MEGA

BUKOPIN

BANK JABAR BANTEN

OCBC NISP

BTN

BII

DANAMON

PERMATA

PANIN

NIAGA

BNI

BCA

BRI

MANDIRI

29,278

30,628

32,525

32,790

36,620

37,085

39,460

43,722

50,365

71,355

76,566

88,307

89,559

92,192

129,238

177,844

237,653

318,007

319,154

MEGA

CITIBANK

STANCHART

BANK JABAR BANTEN

HSBC

BTPN

BUKOPIN

UOB INDONESIA

OCBC NISP

BII

BTN

PANIN

PERMATA

DANAMON

NIAGA

BNI

BCA

BRI

MANDIRI

History and Key Milestone

1989 1993 2003 2006 2008 2009 2011 1970 2012

8

Business Activity

9

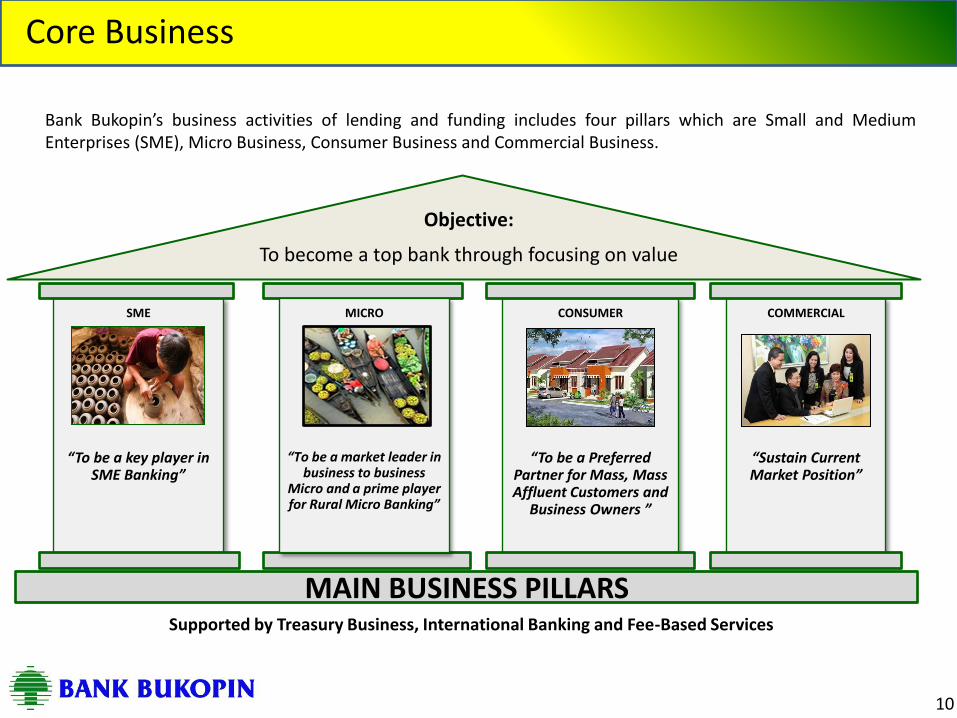

Core Business

Supported by Treasury Business, International Banking and Fee-Based Services

Objective:

To become a top bank through focusing on value

CONSUMER

“To be a Preferred Partner for Mass, Mass Affluent Customers and

Business Owners ”

SME

“To be a key player in SME Banking”

COMMERCIAL

“Sustain Current Market Position”

MAIN BUSINESS PILLARS

MICRO

“To be a market leader in business to business

Micro and a prime player for Rural Micro Banking”

Bank Bukopin’s business activities of lending and funding includes four pillars which are Small and Medium Enterprises (SME), Micro Business, Consumer Business and Commercial Business.

10

Competitive Strenghts

11

Positioned for Growth

Leading Sophisticated

Mid-Sized Bank

Experienced and

Competent in SMEs and

Micro Business

Strategic Partnerships

Satisfying and Compatible

Services

Extensive Branch and Electronic Network

Established Control and

Risk Management

Experienced Management

12

Strategic Partnerships

Bukopin’s Strategic Partners

BULOG

• National Food Logistic Agency

Perusahaan Listrik Negara (PLN)

• Indonesia state-owned electricity company

Swamitra

• Community-based cooperative

Jamsostek

• State-owned social security company for private sector workers

Pertamina

• Indonesia state-owned oil extraction company

Taspen

• State-owned pension company for civil servants

13

• Responsible for the maintenance of rice security, rice distribution and price control.

• Bank Bukopin is the major bank (60%) in financing Bulog and the other banks are BRI (35%) and Mandiri (5%).

• Bank Bukopin has a long-standing partnership with Bulog. Around 33.7 % of Bank Bukopin’s SME loan portfolio comprises loans to Bulog.

• Bank Bukopin provides financing to Bulog’s food distribution supply chain from end-to-end.

• Bank Bukopin also assists Bulog with logistics information and accounting system management

• Bank Bukopin provides full serviced financing to 6 areas of regional division of Perum Bulog : West Java, East Java, DKI Jakarta, Bali, South Sulawesi & South Kalimantan

• Since the late 1990s, Bank Bukopin has developed Swamitra model. We provide Management Assistance, System and Procedure and IT System.

• Today, Bank Bukopin partners with around 625 Swamitra with more than 457.000 members across Indonesia. Cooperative members are mostly in the micro-business segment.

• Bank Bukopin provides loans to Swamitra, which then channels the loan to its members (two step loan).

• In Swamitra lending, members of the cooperative keep an eye on one another, to ensure repayments so as to protect the profitability of the cooperative. This leads to a low NPL ratio for Swamitra loans.

Savings and loan cooperative

Strategic Partnership

Bulog’s network:

26 Regional Divisions

101 Sub-Regional Divisions

30 Logistic Offices

463 Warehouses

14

• Jamsostek manages social security for over 40 million private sector workers, of which over 11 million are active members, with total assets of over Rp. 137 trillion (US$ 14.1 Tn).

• Bank Bukopin has 34 outlets co-located at Jamsostek’s offices. These outlets enable the deposit of contributions by and payment of Jamsostek claims to its members.

• Jamsostek owns a 6.14% stake in PT Bank Syariah Bukopin, in which Bank Bukopin controls 77.57% (the remaining shareholders are local funds).

• In line with Jamsostek’s ongoing transformation – from providing merely financial benefit to “total benefit” for its members (including housing and health benefits) – Bank Bukopin is collaborating with Jamsostek to provide financing and cash management for the housing.

Social security for private sector workers

Pension scheme for civil servants

• Appointed as one of 16 institutions as pension fund payment agent.

• Bank Bukopin implemented personal financing to Taspen pensioners in 2Q 2010, under its micro financing segment.

• Repayments are through deduction from pension payments.

• Outstanding loans under the Taspen program have grown, to around Rp.1.54 trillion by December 2012.

Strategic Partnership

15

• Bank Bukopin is one of 5 banks given exclusive right by Pertamina to receive payment for Pertamina’s products (fuel and non-fuel). This arrangement commenced in April 2009.

• Bank Bukopin provides banking facilities (letters-of-credit/trade financing) and cash management services for Pertamina’s operations.

• Pertamina-related transactions via Bank Bukopin currently average Rp.2.3 trillion per month.

State-owned oil extraction company

Strategic Partnership

• Bank Bukopin currently serves 13 million out of 42 million PLN customers who pay their bills through around 56 banks.

• Bank Bukopin was the first commercial bank in Indonesia to establish the Payment Point On-line Bukopin (PPOB) over 3 years ago. It now has more than 15.000 PPOBs across Indonesia.

• PPOBs can provide services to PLN customers such as billing payment, new PLN installation and PLN prepaid card for electricity.

• The PLN partnership has provided a boost to Bank Bukopin’s fee-based income, cash management services, CASA accumulation and loan portfolio (note: As of 31 Dec 2012 fee-based income contributes around 8.11 % of Bank Bukopin’s total income).

State-owned electricity company

16

Satisfying and Compatible Services

Providing arrays of products and services to fulfill customer needs

Using technology as a strategic means to deliver services

Improving human resources competencies as a key factor

17

Extensive Branch and Electronic Network

Lampung

Nanggroe Aceh Darussalam

Riau

Jambi

South Sumatera

West Sumatera

West Kalimantan

East Kalimantan

South Kalimantan

Banten

North Sulawesi

South Sulawesi

Bali

West Nusa Tenggara

East Nusa Tenggara

East Java

West Java

D.I.Yogyakarta

DKI Jakarta

Central Java

North Sumatera

Riau Island

As of Dec 31, 2012

Branches 36

Sub Branches 107

Cash Offices 140

Micro-Service Offices 87

Payment Point 42

Pickup Service 8

Total outlet 420

ATMs 381

Mini ATMs 923

• Bank Bukopin’s network is in 22 out of 33 provinces in Indonesia.

• Bank Bukopin’s ATM card gives its holder access to all major ATM networks in Indonesia (including ATM BCA Prima, ATM Bersama and ATM Plus), comprising more than 30.000 ATMs.

• Bank Bukopin’s 15.000 PPOB outlets across Indonesia reaches out to the urban and rural population.

• Our IT system provides real-time monitoring of each branch’s transactions and positions.

18

Established Controls and Risk Management

• Implementation of risk management in Bank Bukopin covered 8 main risks

* credit risk * legal risk

* market risk * reputational risk

* liquidity risk * strategic risk

* operational risk * compliance risk

• Bank Bukopin has developed models and systems for risk management

• Bank Bukopin also regularly conduct stress testing, to forecast the impact of any external shock to the Bank’s performance

• The Risk Management Division is independent from risk taking units

• Beside the internal audit activity, there’s also internal control units embedded to the risk taking units and an independent unit of compliance, all to establish comprehensive internal control system

Active observation by Boards through

Committee

• Risk Management Systems is executed

according to internal and external rules

• All transactional execution had to go through checker and approval system.

• There’s also clear segregation between business and operational units

Risk management executed by each related

unit (risk taking units)

Bank-wide risk management by Risk

Management Division

Internal control process

• Bank Bukopin has set and continously

review various internal policies and guidance for controlling all risks faced

19

Experienced Management Glen Glenardi,

President Director

Agus Hernawan, Services & Distribution Director

Tri Joko Prihanto, Finance & Planning Director

Sunaryono, Risk Management, Compliance and Human Resources Development Director

Sulistyohadi DS, SME and Cooperatives Director

Lamira S. Parwedi, Consumer Director

Mikrowa Kirana, Commercial Director

26 years of experience Past experience includes: - Director of Micro and SME (2000-2005) - Director of Cooperatives and Small Enterprises (1999) - Head of Credit for Cooperatives and Small Enterprises (1992-1999) - Head of Cirebon Branch (1989-1992)

26 years of experience Past experience includes: - Director of Operations (2000-2006) - Corporate Secretary (1996-2000) - Group Business Head (1995-1996) - Head of Human Resources (1993-1995) - Head of Business Development for Cooperatives (1991-1993)

26 years of experience Past experience includes: - Director of Consumer Banking (2000-2006) - Group Business Head (1997-2000) - Head of Bukopin branches (1988-1997

24 years of experience Past experience includes: - Director of Risk Management and Compliance (2003-2006) - Head of Business Development for Cooperatives and Small Enterprises (2000-2003) - Group Head of Central Java Province (1997-2000) - Head of Commercial Branches Supervision (1996-1997)

24 years of experience Past experience includes: - Group Head for Institutional Business (1999-2005) - Some positions within Bank Bukopin since 1988

26 years of experience Past experience includes: - Group Head for Commercial Business (2000-2006) - Group Business Head (1995-2000) - Head of Commercial Business Segment (1993-1995)

26 years of experience Past experience includes: - Group Head for Commercial Business (2001-2006) - Group Head for Commercial Business in West and Central Java (2000-2001) - Group Business Head (1997-2000) - Head of Kupang and Denpasar Branches (1992-1996)

20

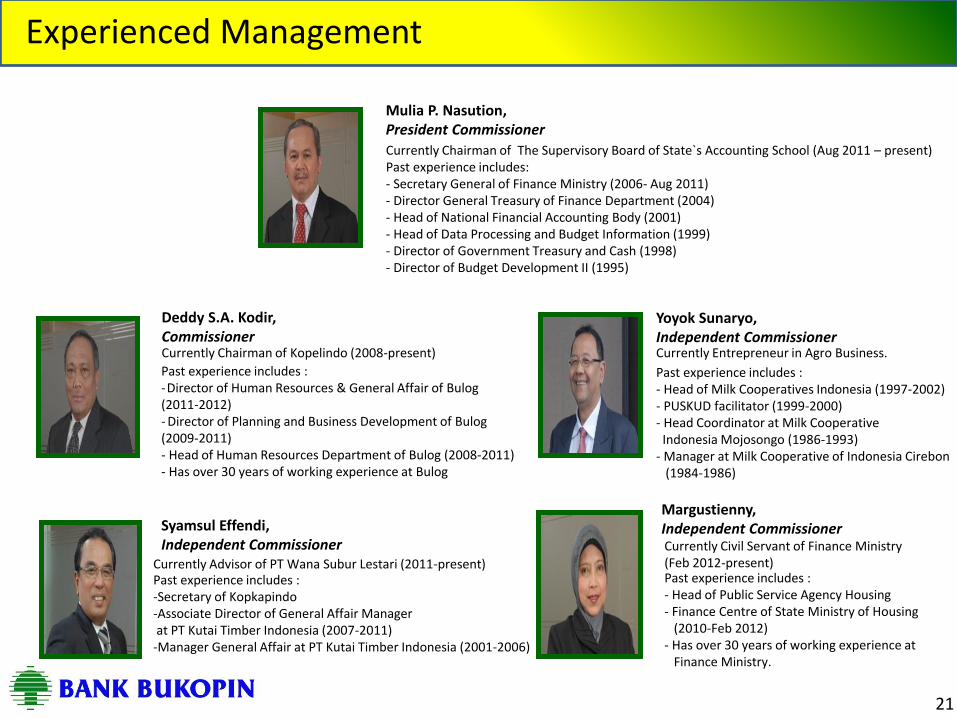

Experienced Management

Mulia P. Nasution, President Commissioner

Deddy S.A. Kodir, Commissioner

Syamsul Effendi, Independent Commissioner

Yoyok Sunaryo, Independent Commissioner

Margustienny, Independent Commissioner

Currently Chairman of The Supervisory Board of State`s Accounting School (Aug 2011 – present) Past experience includes: - Secretary General of Finance Ministry (2006- Aug 2011) - Director General Treasury of Finance Department (2004) - Head of National Financial Accounting Body (2001) - Head of Data Processing and Budget Information (1999) - Director of Government Treasury and Cash (1998) - Director of Budget Development II (1995)

Currently Chairman of Kopelindo (2008-present) Past experience includes : -Director of Human Resources & General Affair of Bulog (2011-2012) - Director of Planning and Business Development of Bulog (2009-2011) - Head of Human Resources Department of Bulog (2008-2011) - Has over 30 years of working experience at Bulog

Currently Advisor of PT Wana Subur Lestari (2011-present) Past experience includes : -Secretary of Kopkapindo -Associate Director of General Affair Manager at PT Kutai Timber Indonesia (2007-2011) -Manager General Affair at PT Kutai Timber Indonesia (2001-2006)

Currently Entrepreneur in Agro Business. Past experience includes : - Head of Milk Cooperatives Indonesia (1997-2002) - PUSKUD facilitator (1999-2000) - Head Coordinator at Milk Cooperative Indonesia Mojosongo (1986-1993) - Manager at Milk Cooperative of Indonesia Cirebon (1984-1986)

Currently Civil Servant of Finance Ministry (Feb 2012-present) Past experience includes : - Head of Public Service Agency Housing - Finance Centre of State Ministry of Housing (2010-Feb 2012) - Has over 30 years of working experience at Finance Ministry.

21

Financial Summaries

22

Key Financial – Balance Sheet

23

40.7

2012 2011

45.5

Total Assets (Rp. Tn)

Asset increased year-on-year by

14.9% from Rp57.2Tn to

Rp65.7Tn, which was supported

by loan growth.

Total Loans (Rp. Tn)

Period Percentage

% Y o Y 14.9%

Period Percentage

% Y o Y 11.8%

57.2

2012 2011

65.7

Key Financial – Balance Sheet

24

2012 2011

47.9

11.1

8.0

28.8

54.0

13.8

8.4

31.8

Total Third Party Deposits (Rp. Tn)

Total Shareholders’ Equity (Rp. Tn)

Deposits increased year-on-year by 12.7% from Rp47.9Tn to Rp54.0Tn. The largest increases came from time deposit and savings

Period Percentage

% Y o Y 12.7%

Period Percentage

% Y o Y 11.4% 4.4

4.9

2012 2011

Savings Currenct Account Time Deposit

Overview of Loan Portofolio

25

Consumer

Commercial

Micro

Small and Medium Enterprise (SME), including Bulog

Loan segment Loan size

Micro < Rp.500 M

SME Rp.500 M – Rp.25 Bn

Commercial > Rp.25 Bn

Bulog 40.4% Bulog 33.7%

Rp.40.7 Tn Rp.45.5 Tn

9.1%

5.7%

51.6% 54.3%

9.9%

30.0%

2011 2012

*)

*)

* From SME Loan

33.6%

5.8%

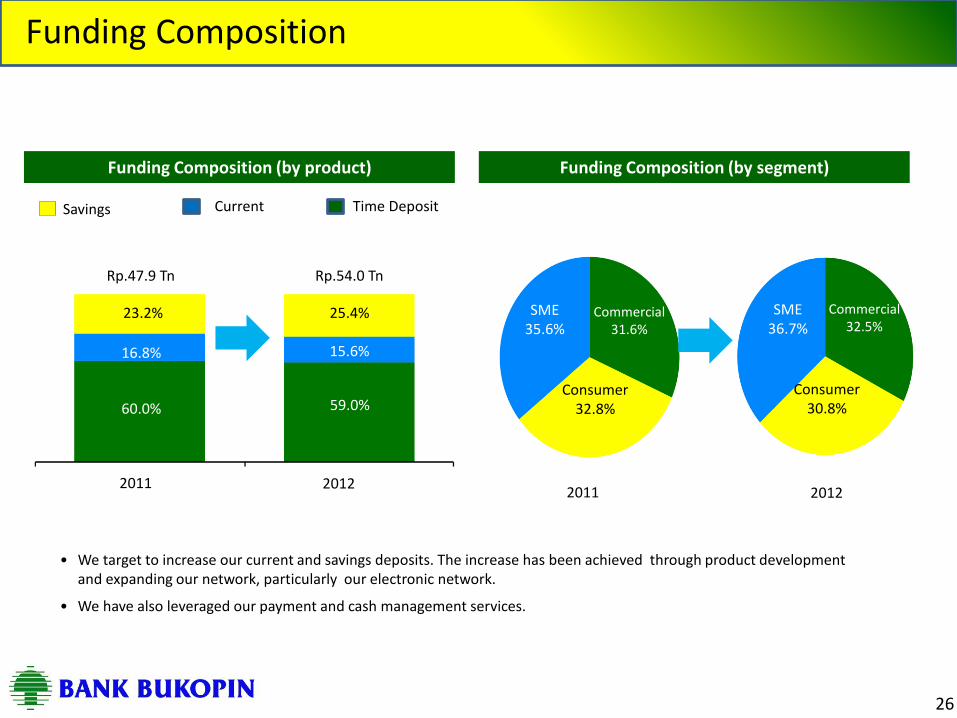

Funding Composition

26

Funding Composition (by product) Funding Composition (by segment)

SME 35.6%

Consumer 32.8%

Commercial 31.6%

SME 36.7%

Consumer 30.8%

Commercial 32.5%

60.0%

2012 2011

Rp.47.9 Tn Rp.54.0 Tn

2012 2011

23.2%

16.8%

25.4%

15.6%

59.0%

Savings Current Time Deposit

• We target to increase our current and savings deposits. The increase has been achieved through product development and expanding our network, particularly our electronic network.

• We have also leveraged our payment and cash management services.

Core & Supplementary Capital

27

An increase in CAR in Dec 2012 due to the issuance of subordinated bonds in the first quarter of 2012 and increase of net profit.

2012 2011

12.16%

0.54%

12.09%

4.25%

Core Capital

Supplementary Capital

CAR 12.71%

CAR 16.34%

Key Financial – Earning

28

Earning Before Tax Earning After Tax

Periode % EBT % EAT

%Y o Y 12.7% 12.5%

Earning Before and After Tax (Rp. Bn)

Net profit year-on-year increased by 12.5%

from Rp738.2 billion to Rp830.5 billion. This

was due to an increase of net interest income

and fee based income

738.2

940.4 1,059.4

830.5

2012 2011

Key Financial – Balance Sheet

29

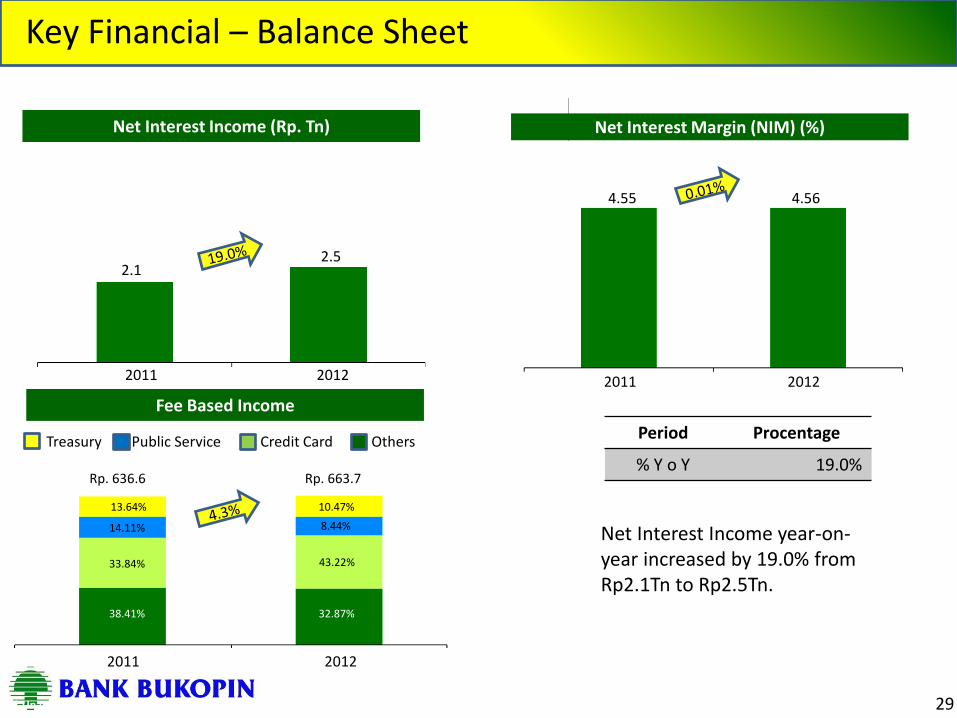

2012 2011 2011 2012

2.1 2.5

4.55 4.56

Net Interest Income (Rp. Tn) Net Interest Margin (NIM) (%)

Net Interest Income year-on-year increased by 19.0% from Rp2.1Tn to Rp2.5Tn.

Period Procentage

% Y o Y 19.0%

Fee Based Income

2012 2011

Public Service Credit Card Treasury Others

33.84%

38.41% 32.87%

14.11%

43.22%

13.64%

8.44%

10.47%

Rp. 636.6 Rp. 663.7

* Unaudited

2011 2012

4.56 4.55

Key Ratio

30

Cost-to-Income Ratio (CIR) (%) Loan-to-Deposit Ratio (LDR) (%)

• LDR year-on-year decreased by 1.2% from 85.01% to 83.81%

• We will maintain our LDR to be in-line with Bank Indonesia’s range at 78%-100%.

• We target to manage our Cost to Income Ratio around 60%.

2012 2011

83.81 85.01

2012 2011

60.50

59.94

Key Ratio

31

Gross Non-Performing Loan (NPL) (%)

• Our gross NPL stood at level 2.66% and net NPL at 1.56% in December 2012.

2012 2011

2.66 2.88

2012 2011

1.56

2.14

* Net Non-Performing Loan (NPL) (%)

Key Ratio

32

61.59

2012 2011

19.47 20.10

• We target to maintain ROE around 20% by

the end of 2012

• We target to maintain CAR above 12%

Return-on-Equity (ROE) (%) Return-on-Assets (ROA) (%)

Capital Adequacy Ratio (CAR) (%)

2012 2011

1.83 1.87

2012 2011

16.34

12.71

Award

“Indonesia Banking Award Best Performance Banking 2012”

Awarded for National Private Bank Category (Asset > 50 T)” from Tempo Magazine and Perbanas.

“First Bank ISO 20000” Awarded for being the first bank in Indonesia that received the Certification ISO 20000-1:2011 of Quality Management System.

“Certification of ISO 20000-1:2011” For providing the electric utility connection system and the core banking saving system from British Standards Institute.

“Infobank Platinum Trophy 2012” Awarded for Financial Performance Excellence Bank 2002-2011.

“Property & Bank Awards 2012” Awarded for The Best Overall Performance Banking.

“Infobank Platinum Awards 2011” Awarded for Financial Performance Excellence Bank 2002-2011.

33

Award

“1st The Best Bank 2012 in Compliance” Awarded for National Private Bank Category (Asset > 25 - 100 T ) from Business Review Magazine and Perbanas.

“ 2nd The Best Bank 2012 in Financial Aspect”

Awarded for National Private Bank Category (Asset > 25 - 100 T ) from Business Review Magazine and Perbanas.

“Indonesian Bank Loyalty Index (IBLI)” Awarded for Saving Account Conventional Banking (Asset > 75 T ) from Infobank Magazine and MarkPlus Insight.

“ 3rd The Best Bank 2012 in Corporate Social Responsibilty”

Awarded for National Private Bank Category (Asset > 25 - 100 T ) from Business Review Magazine and Perbanas.

“Certification of ISO 27001:2005” For providing for information security from Bureau Veritas Certification.

34

“ 2nd The Best Bank 2012 in Corporate Communication”

Awarded for National Private Bank Category (Asset > 25 - 100 T ) from Business Review Magazine and Perbanas.

“Indonesian Bank Loyalty Index (IBLI)” Awarded for Top 10 Credit Card for Loyalty Program from Infobank Magazine and MarkPlus Insight.

Strategic Plan

35

Strategic Plan

Become a Trusted Bank for Financial

Services

Strenghtening the Structure

of Capital Enlarge the

Composition of SME`s, Micro

and Consumer Business

Focus on Excelling in

Business Segments

Improvements of value chain

and cross selling

Enhances Strategic

Partnership

Inprovement of Information

Systems, Technology and

Procedures

Strenghtening of Corporate

Culture

Enhance the Role of Risk

Management and

Compliance Aspects

36

Thank You

37

Q & A

38