bank mandiri (europe) ltd annual report 2008 annual report 2008.pdf · chairman’s statement i am...

TRANSCRIPT

Bank Mandir i (Europe) Ltd

Annual Repor t 2008

Contents

Financial Highlights

Directors’ Report

Management

Auditor’s Report

Profit and Loss Account

Notes to the Financial Statements

Board of Directors and Management

Chairman’s Statement

Board of Directors

Statement of Directors’ Responsibilities

Corporate Profile and Services

Balance Sheet

Bank Mandiri Network

04

07

10

12

17

19

03

05

08

11

13

18

Inside Back Cover

Professionalism

Trust

Excellence

Customer focus

Integrity

Board of Directors and Management

Directors Gatut Subadio Chairman 10/11/05 –

Ken Widjajanto Chief Executive 16/09/05 –

Mansyur Nasution Non-Executive Director 09/11/07 –

Patrick Quinn Non-Executive Director 31/05/07 –

John Williams Non-Executive Director 02/07/07 –

Management Ken Widjajanto Chief Executive

Gordon Turpin General Manager

Rudy Hutagalung General Manager

Ajay Joshi Deputy General Manager

Steve Wansell Deputy General Manager

Brendan Battle Deputy General Manager

Company Secretary Ajay Joshi Deputy General Manager and Company Secretary

Auditors Ernst & Young LLP 1 More London Place London SE1 2AF

Registered Office Cardinal Court 23 Thomas More Street London E1W 1YY

Registration Number: 3793679

Appointed Resigned

03

Restated

2008US$ 000

2007US$ 000

2006US$ 000

2005US$ 000

2004US$ 000

Fee–Based Income (US$ 000’s) Operating Income (US$ 000’s)Net Interest Income (US$ 000’s)

3,571 3,3233,700

4,8675,133

FY04 FY05 FY06 FY07 FY08

4,0194,924

6,298

7,6928,455

FY04 FY05 FY06 FY07 FY08

7,590 8,265

9,998

12,55913,588

FY04 FY05 FY06 FY07 FY08

Financial Highlights

Income Statement

Net interest incomeFees & commissions receivableOperating incomeOverhead expenses (1)Profit before tax & provisionsProvisions for bad debtsProvisions for commitments & contingenciesProfit/(Loss) before taxationTaxationProfit/(Loss) after taxation

Balance Sheet

Loans and advances to banksLoans and advances to customers (2)Debt securities (3)Total assets Deposits from banksCustomer accountsDebt securities in issueShareholder’s funds (4)

Ratios

Capital adequacy ratioTotal equity to total assetsReturn on average equityReturn on average assets (5)

8,4555,133

13,5887,4826,106

(82)-

6,188(1,822)

4,366

12,618196,421

50,779296,728171,348

49,561-

71,264

32.5%24.0%

9.2%1.9%

7,6924,867

12,5596,3996,160(662)

-6,822

(1,997)4,825

57,311158,467

52,829274,635141,938

60,981-

67,244

29.9%24.5%10.4%

2.7%

6,2983,7009,9986,4883,510

(2,032)-

5,542873

6,415

18,415115,371

74,731218,570104,913

37,28310,00062,827

36.3%28.4%10.7%

1.8%

4,9423,323 8,265 7,380

8853,2031,499

(3,817)-

(3,817)

32,63868,92972,377

179,694 73,00739,708

8,51455,457

51.9%31.0%-8.2%0.5%

4,0193,5717,5905,3752,215

718 -

1,497 -

1,497

46,88057,37963,508

172,69168,13835,616

8,94059,172

62.8%34.3%

2.7%1.4%

In US$ 000’s

(1) 2005 Includes exceptional costs in respect of: (a) Staff restructuring costs US$154k (b) Premises move costs of US$528k (c) Exceptional client administration and legal costs relating to a borrower in default US$377k(2) Net of specific provisions(3) Comparative after adoption of FRS26 to 2005(4) Shareholder’s funds restated for 2005 to include reserves of available–for–sale & hedge accounting(5) Excluding tax and bad debt provisions

Basis for Calculation of the Ratios

Capital Adequacy Ratio – Capital adequacy ratio is calculated in line with the format prescribed by the Financial Services Authority

Total Equity to Total Assets – The total equity to total assets ratio is calculated by dividing the shareholders funds (see note 19) by the total assets after deducting specific provisions for bad debts.

Return on Average Equity – The return on average equity is calculated by dividing profit before tax by the average equity during the year.

Return on Average Assets – The return on average assets is calculated by dividing profit before tax and provisions for bad debts by the average total assets during the year.

04

Chairman’s Statement

I am pleased to present the Report and Accounts of Bank Mandiri (Europe) Limited

for its ninth year as a wholly owned subsidiary of PT Bank Mandiri (Persero) Tbk,

Indonesia.

Notwithstanding the worldwide economic turmoil prevailing throughout 2008,

the Bank performed well and we recorded operating income of US$13.6 million for

the year, which was 8.2% higher than in 2007. Operating profits before provision

adjustments and taxes of US$6.1 million were marginally (0.3%) lower than in 2007 due

to a larger proportionate increase in overheads of 17% to US$7.4 million. The higher

overheads were attributable to increased business volumes and the unfavourable

GBP/US$ exchange rate used for conversion of our GBP expenses to US$ for much of

2008 compared to the prior year. Net profits, after taxes and provision adjustments,

were US$4.4 million in 2008.

I am pleased to confirm that the Bank has no sub-prime mortgage exposure in its

balance sheet and has never been involved in the sub-prime mortgage or securitisation

market either directly or indirectly. Nor, as yet, has the quality of the Bank’s credit

portfolio been significantly affected by the bow wave from the “credit crunch” and, in

view of the foregoing, it was not considered necessary to take any new provisions for

bad debts in the reporting period ended 31st December 2008.

As at 31st December 2008 our total balance sheet footings were US$296.7 million,

which was 8.2% higher than at the end of 2007. Growth was slower than in prior years,

as, given the difficult market conditions, we took a conservative approach to business

and new lending activity was focused primarily on self liquidating trade finance

business. Total loans and advances to banks and customers (including cash held by

banks) grew by 9.9% to US$240.6 million; of this amount US$54.1 million was secured

by cash collateral.

The Bank actively manages its assets and liabilities to ensure that business growth is

supported by the appropriate level of funding and liquidity resources; more details as

to the Bank’s liquidity management are contained in note 23 to the accounts.

Pre–Tax Profit (US$ millions) Total Assets (US$ millions) Net Interest Income (US$ millions)

-3.817

1.497

5.542

6.8226.188

FY04 FY05 FY06 FY07 FY08

172.69 179.69

218.57

274.63 296.72

FY04 FY05 FY06 FY07 FY08

4.024.9

6.3

7.78.5

FY04 FY05 FY06 FY07 FY08

05

Notwithstanding the strong growth in assets, the Bank maintained adequate capital

resources to support its business activities and our capital adequacy ratio measured

in accordance with Basel 2 guidelines was 32.4%. This ratio is well above accepted

industry norms and gives the Bank ample scope to further expand its business and

profitability.

With effect from 1st January 2008 the Bank did all things necessary to comply with the

requirements of Basel 2 and the Capital Requirements Directive; further information is

contained in the Pillar 3 disclosures that are published on the Bank’s website.

We start 2009 against the backdrop of a very uncertain economic environment and

with many of the major economies in recession, however, I am confident that BMEL has

the right business model to weather the storm and will be able to sustain continued

business growth and profitability in the year ahead.

Finally, I should like to express my gratitude to our customers and business

counterparts for their continued support and custom over the past year and to my

fellow directors, the executive management and, not least to the staff for their hard

work and dedication.

Gatut SubadioChairman

5th February, 2009

Capital Adequacy Ratio (US$ 000’s)

Type of Loans (US$ 000’s)

62.8%

51.9%

36.3%

29.9 % 32.4%

FY04 FY05 FY06 FY07 FY08

2006 2007 2008

Trade Finance Trade Finance Trade Finance Secondary Markets Secondary Markets Secondary Markets Ship Finance Ship Finance Ship Finance

36,562

63,851

11,132

13,856

67,67780,760

55,325

14,645

126,451

06

Directors’ Report

The Directors present their Report and the Financial Statements for the year ended

31st December 2008.

Results and DividendsThe trading profit after tax for the year amounted to US$4,366,377

The Directors do not recommend the payment of a dividend.

Principal Activities and Review of BusinessThe Bank is an authorised UK Bank under the Banking Act 1987 and carries on

international corporate and institutional banking business, which includes the

following activities:

(1) Trade Finance.

(2) Ship Finance.

(3) Inter-bank Deposits.

(4) Current and Deposit Accounts.

(5) Purchase of Investment Securities, Marketable Securities and Secondary

Market Debt.

Details of the Review of Business have been covered in the Chairman’s Statement.

Principal Risks and UncertaintiesThe Board, in conjunction with Senior Management of the Bank, has established

comprehensive policies and procedures in order to manage and mitigate the risks and

uncertainties facing the Bank and the on-going implementation of such is monitored

by management and through a robust and independent internal audit function. More

detail as to the principal risks and uncertainties facing the Bank and the mitigation

thereof is contained in Note 23 to the Financial Statements.

Fixed AssetsDetails of the Bank’s fixed assets are shown in Note 12 to the financial statements.

Future DevelopmentsThe Directors aim is to maintain the management policies which have resulted in the

Bank’s growth in recent years. As per the Chairman’s statement, the Bank will be able

to sustain continued growth and profitability in the year ahead. The details of the

directors who served during 2008 can be seen on page 3 of this report.

Disclosure of InformationSo far as each Director is aware, there is no relevant audit information of which the

Bank’s auditors are unaware; and each Director has taken all steps that they ought

to have taken as a Director in order to make themselves aware of any relevant audit

information and to establish that the Bank’s auditors are aware of that information.

AuditorsErnst & Young LLP have expressed their willingness to continue in office as auditors. A

resolution proposing their re-appointment and giving authority to the directors to fix

their remuneration will be tabled at the next Annual General Meeting.

By order of the Board

Ajay JoshiCompany Secretary

5th February 2009

07

Board of Directors

In accordance with the best principles of corporate governance the Bank’s activities are directed by a Board which is comprised of three appointees from our parent bank and two non-executive directors, as follows:

Gatut SubadioChairman

Graduated with a Bachelor Degree in Industrial Engineering from Bandung Institute of Technology in 1984 and obtained an MBA in International Business and Finance from the University of Miami in 1992. He is a seasoned international banker who started his banking career in 1984 as an analyst at Bank Bumi Daya in Indonesia. In 1999 he joined Bank Mandiri where he has held a number of senior international banking positions. Since 2005 he has been Head of International Banking and Capital Market Services at Bank Mandiri, Jakarta Indonesia.

Appointed as Chairman of Bank Mandiri (Europe) Limited in 2005.

Ken WidjajantoChief Executive

Graduated with a Bachelor Degree in Economics from the University of Indonesia in 1983 and obtained an MBA degree from the Cleveland State University (Ohio, USA) in 1995.

He began his banking career in 1993 at Bank Dagang Negara, Indonesia where he gained a broad experience in both plantation finance and corporate lending.

In 1999 he joined Bank Mandiri as a senior manager in the loan recovery and debt work

out unit and was subsequently responsible for setting up and managing Bank Mandiri’s

international branch in Timor Leste.

Appointed as Chief Executive of Bank Mandiri (Europe) Limited in 2005.

Patrick QuinnNon–Executive Director

Associate member of the Chartered Institute of Bankers and an Associate member of the British Institute of Management.

During a long banking career, which started at National Westminster Bank in 1960, he has held a number of senior positions both in London and overseas, including directorships at AMEX Bank Limited, Chartered West LB and as a Director & General Manager of Yamaichi Bank Plc.

In addition to his non-executive directorship at Bank Mandiri (Europe) Ltd, since 2000 he has held a position as a Non-Executive Director of Habibsons Bank Ltd.

Appointed as a Non Executive Director of Bank Mandiri (Europe) Ltd in 2007 and is Chairman of the Audit Committee.

08

09

John WilliamsNon–Executive Director

Fellow of the Institute of Chartered Accountants of England and Wales; qualified as a chartered accountant in 1968. Worked for three years with Price Waterhouse and Co in Nassau, Bahamas before joining The Deltec Banking Corporation Limited in 1973 where, after working in several group companies, in 1977 he became General Manager of the Nassau operation before leaving in 1980.

He returned to England to work with Trade Development Bank and joined American Express Bank Limited, upon its purchase of Trade Development Bank, as Chief Financial Officer for Europe, Middle East and Africa until his retirement from full time employment in 2000. Since then he has been working as a consultant to companies in the financial sector.

Appointed as a Non-Executive Director of Bank Mandiri (Europe) Ltd in 2007 and is Chairman

of the Remuneration Review Committee.

Mansyur Syamsuri NasutionNon–Executive Director

Graduated from the Institute of Agronomy Bogor (Indonesia) in 1981 and completed his Master

Degree in Agronomy in University of Colorado (USA) in 1991.

In 1983, he began his career in banking by joining Bank Bumi Daya, Jakarta, Indonesia. In 1999 he joined Bank Mandiri, as a division head in the loan recovery and debt work-out unit.

He is currently Head of the Corporate Secretary Group of Bank Mandiri, Jakarta, Indonesia.

Appointed as a Non-Executive Director of Bank Mandiri (Europe) Limited in November 2007.

Management

The management of BMEL comprises six members, consisting of the Chief Executive, two General Managers and three Deputy

General Managers.

10

Ken WidjajantoChief Executive

Brendan BattleDeputy General Manager

Operations

Ajay JoshiDeputy General Manager

MIS & IT

Steve WansellDeputy General Manager Corporate

Gordon TurpinGeneral Manager Risk & Operations

Rudy HutagalungGeneral Manager Corporate &

Treasury

Statement of Directors’ Responsibilities

The Directors are responsible for preparing the Annual Report and the Financial

Statements in accordance with applicable law and regulations.

Company Law requires the Directors to prepare financial statements for each financial

year. Under that law the Directors have elected to prepare the financial statements in

accordance with United Kingdom Generally Accepted Accounting Practice (United

Kingdom Accounting Standards and applicable law). The financial statements are

required by law to give a true and fair view of the state of affairs of the Bank and of the

profit or loss of the Bank for that period. In preparing those financial statements, the

Directors are required to:

• Selectsuitableaccountingpoliciesandthenapplythemconsistently; • Makejudgmentsandestimatesthatarereasonableandprudent;and • Preparethefinancialstatementsonthegoingconcernbasis,unlessitis inappropriate to presume that the Bank will continue in business.

The Directors are responsible for keeping proper accounting records which disclose

with reasonable accuracy at any time the financial position of the Bank and to enable

them to ensure that the financial statements comply with the Companies Act 1985.

They are also responsible for safeguarding the assets of the Bank and hence for taking

reasonable steps for the prevention and detection of fraud and other irregularities.

11

•

••

Selectsuitableaccountingpoliciesandthenapplythemconsistently;Makejudgmentsandestimatesthatarereasonableandprudent;andPrepare the financial statements on the going concern basis, unless it is inappropriate to presume that the Bank will continue in business.

Auditor’s Report

Independent Auditor’s report to the members of Bank Mandiri (Europe) Limited

We have audited the Company’s financial statements for the

year ended 31 December 2008 which comprise the Profit and

Loss Account, the Statement of Total Recognised Gains and

Losses and the Balance Sheet and the related note 1 to 26.

These financial statements have been prepared under the

accounting policies set out therein.

This report is made solely to the Company’s members, as

a body, in accordance with Section 235 of the Companies

Act 1985. Our audit work has been undertaken so that we

might state to the Company’s members those matters we

are required to state to them in an auditors’ report and for

no other purpose. To the fullest extent permitted by law, we

do not accept or assume responsibility to anyone other than

the Company and the Company’s members as a body, for

our audit work, for this report, or for the opinions we have

formed.

Respective responsibilities of Directors and auditors

The Directors’ responsibilities for preparing the Annual Report

and the financial statements in accordance with applicable

United Kingdom law and Accounting Standards (United

Kingdom Generally Accepted Accounting Practice) are set

out in the Statement of Directors’ Responsibilities.

Our responsibility is to audit the financial statements in

accordance with relevant legal and regulatory requirements

and International Standards on Auditing (UK and Ireland).

We report to you our opinion as to whether the financial

statements give a true and fair view are properly prepared

in accordance with the Companies Act 1985. We also report

to you whether in our opinion the information given in the

Directors’ Report is consistent with the financial statements.

In addition we report to you if, in our opinion, the Company

has not kept proper accounting records, if we have not

received all the information and explanations we require for

our audit, or if information specified by law regarding directors’

remuneration and other transactions is not disclosed.

We read the Directors’ Report and consider the implications

for our report if we become aware of any apparent

misstatements within it.

Basis of audit opinion

We conducted our audit in accordance with International

Standards on Auditing (UK and Ireland) issued by the Auditing

Practices Board. An audit includes examination, on a test basis,

of evidence relevant to the amounts and disclosures in the

financial statements. It also includes an assessment of the

significant estimates and judgments made by the directors in

the preparation of the financial statements, and of whether

the accounting policies are appropriated to the Company’s

circumstances, consistently applied and adequately

disclosed.

We planed and performed our audit so as to obtain all the

information and explanations which we considered necessary

in order to provide us with sufficient evidence to give

reasonable assurance that the financial statements are free

from material misstatement, whether caused by fraud or other

irregularity or error. In forming our opinion we also evaluated

the overall adequacy of the presentation of information in the

financial statements.

Opinion

In our opinion

The financial statements give a true and fair view in

accordance with United Kingdom Generally Accepted

Accounting Practice of the Company‘s affairs as at 31st

December 2008 and of its profit for the year then ended.

•

•

•

The financial statements have been properly prepared in

accordance with the Companies Act 1985; andThe information given in the Director’s Report is consistent

with the financial statements.

Ernst & Young LLPRegistered Auditor

London

11th February 2009

12

BMEL’s Services

Some of the principal products and

services we provide are listed below:

Import letter of credit and documentary collection

services;

Supplier credit financing;

Short-term refinancing loans under import letters

of credit;

Export letter of credit services (advising,

confirmation, negotiation, etc);

Bill discounting and forfaiting;

Contract bonding and guarantee facilities;

Ship financing;

Syndications.

Corporate Profile and Services

The bank that delivers Trade Finance and Shipping Solutions Worldwide“

BMEL’s Profile

Bank Mandiri (Europe) Limited (“BMEL”) was established on the 2nd August 1999 and is

a wholly owned subsidiary of Bank Mandiri, Indonesia.

When BMEL was established it took over the banking business of PT Bank Ekspor Impor

Indonesia (Persero), London Branch which had been based in London since 1992; and

previously since 1983 as a representative office.

BMEL is incorporated and licensed in the United Kingdom and is a British bank under

the regulation of the UK Financial Service Authority (FSA) and has a complement of

29 staff.

By virtue of its Indonesian ownership, BMEL can offer a more informed and pro-active

service in Indonesian related business than many of its competitors.

Although BMEL is Indonesian owned, its business activities are not restricted to

Indonesia and we like to consider BMEL, as the bank that delivers Trade Finance and

Shipping Solutions Worldwide.

BMEL’s primary business activities are trade finance and ship finance. BMEL is staffed

by a team of experienced banking professionals who are committed to providing an

efficient, informed and personal service.

The Bank has a wide network of correspondent banking contacts developed over

many years of servicing its customers’ needs throughout the World.

BMEL provides tailored financial solutions specific to individual client requirements

which assist in the timely settlement of transactions and can substantially benefit the

cash flow of our customers.

•

•

•

•

•••

•

”

13

Financial Statements

Profit and Loss Account

Statement of total recognised gains and losses

Bank Mandiri (Europe) Limited

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

for the year ended 31st December 2008

Profit for the financial year

Change in fair value of investment available for sale

Change in fair value of forward exchange contracts

Realised to profit and loss

Total recognised gains relating to the year

Total recognised gains since last annual report

The profit above is achieved from continued operations.

The accompanying notes are an integral part of these financial statements.

2008US$ 000

2008US$ 000

2007US$ 000

2007US$ 000

NotesIn US$ 000’s

[3]

[5]

[6]

[12]

[10]

[4]

[8]

18,773

(10,318)

8,455

4,961

172

13,588

(7,274)

(208)

82

6,188

(1,822)

4,366

17,044

(9,352)

7,692

4,749

118

12,559

(6,195)

(204)

662

6,822

(1,997)

4,825

4,366

(354)

(771)

19

3,260

3,260

4,825

(19)

-

-

4,806

17

Interest receivable

Interest payable

Net interest income

Fees and commissions receivable

Other operating Income

Total operating income

Administrative expenses

Depreciation and amortisation

Provision for bad and doubtful debts

Profit on ordinary activities before tax

Tax charge

Profit on ordinary activities after tax

Balance SheetBank Mandiri (Europe) Limited

as at 31st December 2008

Cash and money at call and deposits with central banks

Loans and advances to banks

Loans and advances to customers

Debt securities

Tangible fixed assets

Other assets prepayments and accrued income

Total assets

Deposits from banks

Customer accounts

Other liabilities, accruals and deferred income

Total liabilities excluding capital and other reserves

Contingent Liabilities:

Guarantees and assets pledged as collateral security

The financial statements on pages 17 to 39 were approved by the Board of

Directors on 5th February 2009 and are signed on its behalf by:

Ken Widjajanto,Chief Executive

The accompanying notes are an integral part of these financial statements.

Called up share capital

Cash flow hedge reserve

Available-for-sale reserve

Profit and loss account

Total shareholder’s funds - equity interests

Total liabilities and shareholder’s funds

[18]

[24]

[19]

[19]

49,000

(771)

(354)

22,629

70,504

296,728

49,000

-

(19)

18,263

67,244

274,635

[9]

[10]

[11]

[12]

[13]

[14]

[15]

[16]

[17]

[14]

[22]

Notes

3,231

57,311

158,467

52,829

457

2,340

274,635

141,938

60,981

4,472

207,391

20,139

2007US$ 000

31,598

12,618

196,421

50,779

318

4,994

296,728

171,348

49,561

5,315

226,224

8,545

2008US$ 000ASSETS

LIABILITIES

MEMORANDUM ITEMS

SHAREHOLDER’S FUNDS

18

Notes to the Financial StatementsBank Mandiri (Europe) Limited

for the year ended 31st December 2008

ACCOUNTING POLICIES1

The financial statements have been prepared under the

historical cost basis of accounting except for available-for-

sale investments and derivative financial instruments that

have been measured at fair value and in accordance with

the special provision of Part VII of the Companies Act 1985,

relating to banking companies, and in accordance with

applicable accounting standards and with the Statements

of Recommended Accounting Practice issued by the British

Bankers’ Association.

The financial statements have been prepared in US Dollars,

as this is the primary currency of the economic environment

in which the Bank operates.

Changes in Accounting PolicesAs from 1st January 2007, the Bank adopted FRS29 Financial

Instruments: Disclosures. As a result, additional disclosures

are made providing information on impairment of loans

& advances, interest on impaired loans & advances and

additional disclosures on Risk Management. The change

has no recognition or measurement effect for the year

ended 31st December 2008.

Under Financial Reporting Standard 1 (revised 1996) the

Bank is exempt from the requirement to prepare a cash

flow statement on the grounds that it is a wholly owned

subsidiary of a parent undertaking that includes the Bank in

its own published consolidated financial statements, which

include a consolidated cashflow report.

Transactions or accruals in foreign currencies are recorded

in the profit and loss account at the US Dollar rate of

exchange applicable to the related month-end, such that

all profits are ultimately booked in US dollars. Assets and

liabilities denominated in foreign currencies are translated

into US Dollars at the rates of exchange prevailing as at the

Balance Sheet date. Both realised and unrealised foreign

exchange gains and losses are recognised in the profit and

loss account.

Fixed assets are included at cost less accumulated

depreciation. Depreciation is provided at rates calculated

to write off the cost less estimated residual value of each

asset on a straight line basis from the date of use over its

estimated useful life as follows:-

The carrying values of the tangible fixed assets are reviewed

for impairment when events or changes in circumstances

indicate the carrying value may not be recoverable.

The Bank offers to its staff a money purchase arrangement.

The cost to the Bank is charged to the Profit and Loss

account as incurred.

Date of recognitionThe purchase or sale of financial assets, liabilities and

derivatives that require the delivery of assets within the

time frame generally established in the market place are

recognised on the trade date i.e. the date that the Bank

commits to purchase or sell the assets.

• LeaseholdImprovements 5years • ComputerHardware 3years • ComputerSoftware 3years • FurnitureandFixtures 5years • OfficeEquipment 3years • Motorvehicles 4years

The accounting policies, all of which, unless specifically stated, have been consistently applied throughout the year, are

detailed below:

A Basis of preparation

B Cashflows

C Foreign currencies

D Fixed assets

E Pensions

F Financial Instruments

19

Initial recognition of financial instrumentsThe classification of financial instruments at initial

recognition depends on the purpose for which the financial

instruments were acquired and their characteristics. All

financial instruments are measured initially at their fair

value less/plus any directly related costs

Notes to the Financial StatementsBank Mandiri (Europe) Limited

for the year ended 31st December 2008

ACCOUNTING POLICIES (Continued)1

Subsequent measurementThe subsequent measurement of financial instruments

depends on their classification as follows:

• Held-to-maturity financial investmentsHeld-to-maturity financial instruments are those which

carry fixed or determinable payments and have fixed

maturities and which the Bank has the intention and ability

to hold to maturity. After initial measurement, held-to-

maturity financial investments are subsequently measured

at amortised cost using the effective interest rate method

less allowance for impairment. A component of debt

securities is included in this category.

• Available-for-sale financial investmentsFinancial investments classified as available-for-sale are

measured at fair value. Unrealised gains and losses are

recognised directly in equity in the “Available-for-sale

reserve”. When the security is disposed of, the cumulative

gain or loss previously recognised in equity is recognised in

the profit and loss account. A component of debt securities

is included in this category.

• Loans and advancesAfter initial measurement, loans and advances are

subsequently measured at amortised cost using the

effective interest rate method, less allowances for

impairment. Amortised cost is calculated by taking into

account any discount or premium on acquisition and fees

and costs that are an integral part of the effective interest

rate. The amortisation is included in “interest income” in the

profit and loss account.

Derecognition of financial assets and financial liabilitiesA financial asset is derecognised where:

Determination of fair valueThe determination of fair values of financial instruments is

based upon quoted market prices or dealer price quotation

for financial instruments traded in active markets.

The rights to receive cash flows from the asset have

expired; or

The Bank has transferred its right to receive cash flows

from the asset or has assumed an obligation to pay the

received cash flows in full without material delay to a

third party; and

Either (a) the Bank has transferred substantially all the

risks and rewards of the asset, or (b) the Bank has neither

transferred nor retained substantially all the risks and

rewards of the asset, but has transferred control of the

asset.

A financial liability is derecognised when the obligation

under the liability is discharged or cancelled or expires.

The Bank assesses at each balance sheet date whether

there is any objective evidence that a financial asset is

impaired. A financial asset is deemed to be impaired if, and

only if, there is objective evidence of impairment as a result

of one or more events that has occurred after the initial

recognition of the asset and the loss event has an impact

on the estimated cash flows of the financial asset that can

be reliably estimated.

Loans and advancesFor loans and advances carried at amortised cost, the Bank

first assesses individually whether objective evidence of

impairment exists individually for financial assets that are

individually significant.

If there is objective evidence that an impairment loss has

been incurred, the amount of the loss is measured as the

difference between the asset’s carrying amount and the

present value of estimated future cash flows (excluding

future expected credit losses that have not yet been

incurred). The carrying amount of the asset is reduced

through the use of specific provision, and the amount of

the loss is recognised in the profit and loss account. Interest

income continues to be accrued on the reduced carrying

amount based on the original effective interest rate of the

asset. Loans together with the associated specific provision

are written-off when there is no realistic prospect of future

recovery and all collateral has been realised or has been

transferred to the Bank. If, in a subsequent year, the amount

if the estimated impairment loss increases or decreases

because of an event occurring after the impairment was

recognised, the previously recognised impairment loss is

increased or reduced by adjusting the specific provision. If

a write-off is later recovered, the recovery is recognised in

the profit and loss account.

G Impairment of financial assets

•

•

•

20

Notes to the Financial StatementsBank Mandiri (Europe) Limited

for the year ended 31st December 2008

ACCOUNTING POLICIES (Continued)1

Available-for-sale financial investmentsFor available-for-sale financial investments, the Bank

assesses at each balance sheet date whether there is

objective evidence that an investment or a group of

investments is impaired,

Debt instruments classified as available-for-sale, are

assessed for impairment based on the same criteria as

financial assets carried at amortised cost. Interest continues

to be accrued at the original effective interest rate on the

reduced carrying amount of the asset and is recorded as

part of ‘interest receivable’. If, in a subsequent year, the fair

value of the debt instrument increases and the increase

can be objectively related to an event occurring after the

impairment loss was recognised in the profit and loss

account, the impairment loss is reversed through the profit

and loss account.

Initial recognition and subsequent measurementThe Bank makes use of derivative financial instruments, i.e.

forward foreign exchange contracts, to manage exposures

to foreign currency risks, including exposures arising from

forecast transactions. The derivative financial instruments

are initially recognised at fair value on the date on which

a derivative contract is entered into and are subsequently

remeasured at fair value at market prices. Derivatives are

carried as financial assets when the fair value is positive and

as financial liabilities when the fair value is negative.

Any gains and losses arising from changes in fair value on

the derivatives during the year that do not qualify for hedge

accounting and the ineffective portion of an effective

hedge, are taken directly to the profit and loss account.

For the purpose of hedge accounting, the Bank uses forward

foreign exchange contracts to hedge highly probable

future sterling expenses. These hedges are classified as

cash flow hedges.

Cash flow hedges which meet the criteria for hedge

accounting are accounted as follows:

Cash flow hedgesThe effective portion of the gain or loss on the forward

foreign exchange contracts is recognised directly in equity

in the “Cash flow hedge reserve”, while any ineffective

portion is recognised immediately in the profit and loss

account. Cumulative gains or losses recognised in equity

are transferred to the profit and loss account when the

hedged future sterling expenses occur. If the forecast future

sterling expenses are no longer expected to occur, any

cumulative gain or loss previously recognised in the equity

is transferred to the profit and loss account. If a forward

foreign exchange contract is sold or terminated or if its

designation as a hedge is revoked, any cumulative gain or

loss previously recognised in equity remains in equity and

is transferred to the profit and loss account when future

sterling expenses occur.

Interest income is recognised in the profit and loss account

as it accrues. Once the recorded value of a financial asset has

been reduced due to an impairment loss, interest income

continues to be recognised using the effective interest rate

applied to the new carrying amount.

Interest expense is debited to the profit and loss account

on an accruals basis.

Corporation tax payable, where applicable, is provided on

taxable profits at the current UK tax rate.

Fees earned for the provision of services over a period

of time are accrued over that period. These fees include

commission income. Loan commitment fees for loans that

are likely to be drawn down and other credit related fees are

deferred and recognised as an adjustment to the effective

interest rate on the loan.

H Derivative financial instruments and hedge accounting

I Income recognition

J Taxation

21

The present value of the estimated future cash flows is

discounted at the financial asset’s original effective interest

rate. If a loan has variable interest rate, the discount rate for

measuring any impairment loss is the effective interest rate

at the date at which the impairment occurs.

Notes to the Financial StatementsBank Mandiri (Europe) Limited

for the year ended 31st December 2008

ACCOUNTING POLICIES (Continued)1

Assets held under finance leases, which are leases where

substantially all the risk and rewards of ownership of

the asset have passed to the Bank, are capitalised in the

balance sheet and depreciated over their useful lives. The

capital elements of future obligations under the leases

are included as liabilities in the balance sheet. The interest

elements of the rental obligations are charged in the

profit and loss account over the periods of the leases and

represent a constant proportion of the balance of capital

repayments outstanding.

Rentals payable under operating leases are charged in the

profit and loss account on a straight line basis over the

lease term.

M Leasing

Deferred taxation is recognised in respect of all timing

differences that have originated but not reversed at the

balance sheet date where transactions or events that result

in an obligation to pay more, or a right to pay less, tax in the

future have occurred at the balance sheet date. Deferred

tax is measured on an undiscounted basis at the tax rates

that are expected to apply in the periods in which timing

differences reverse, based on tax rates and laws enacted or

substantively enacted at the balance sheet date. Deferred

tax assets are recognised only to the extent that the

Directors consider it more likely than not that there will be

suitable taxable profits from which the future reversal of

the underlying timing difference can be deducted.

The Bank has taken advantage of the exemption in

paragraph 3 (c) of FRS8, from disclosing transactions with

related parties that are part of the Bank Mandiri Group, as

consolidated financial statements are publicly available.

K Deferred Taxation

L Related Parties

22

Notes to the Financial StatementsBank Mandiri (Europe) Limited

for the year ended 31st December 2008

SEGMENTAL ANALYSIS

Segmental Information - By Class of BusinessThe Directors consider that the Bank does not have more than one class of business namely Corporate & Institutional Banking,

and therefore a disclosure by class of business has been deemed unneccessary.

Segmental Information - By Geographic Segment

Notes:(i) Geographic segments are based on the ultimate market risk to which the Bank is exposed.

(ii) Operating expenses have been allocated to each geographic segment based on the percentage of income attributed to

that segment.

(iii) The Bank’s Capital is not directly attributed to business lines but its benefit is evenly distributed on the basis of assets

employed within each respective segment.

2

UK & Europe Asia Others Intra-group TotalRegion:

Interest receivable

Interest payable

Net interest income

Fees & commissions receivable

Net revenue

Operating expenses

Operating (loss)/profit before provisions

Provisions for bad debts

Provisions for commitments & contingencies

Profit/(Loss) before taxation

Total assets employed

Total net assets/(liabilities)

7,906

(6,852)

1,054

2,850

3,904

(3,366)

537

-

-

537

92,167

(30,110)

6,313

(6,699)

(386)

2,986

2,600

(2,716)

(116)

-

-

(116)

120,313

(18,617)

9,979

(1,259)

8,720

2,172

10,892

(3,803)

7,089

82

-

7,171

173,300

101,192

9,424

(1,572)

7,852

1,791

9,643

(3,275)

6,368

662

-

7,030

121,312

95,437

673

(1,757)

(1,084)

48

(1,036)

(226)

(1,261)

-

-

(1,261)

31,230

14,633

215

(450)

(235)

63

(172)

(87)

(259)

-

-

(259)

31

(15,210)

1,061

(829)

232

4

236

(311)

(75)

-

-

(75)

10,136

(7,666)

18,773

(10,318)

8,455

5,133

13,588

(7,482)

6,106

82

-

6,188

296,728

70,504

17,044

(9,352)

7,692

4,867

12,559

(6,399)

6,160

662

-

6,822

274,635

67,244

246

(252)

(6)

86

80

(97)

(17)

-

-

(17)

22,874

(1,910)

2008US$000

2008US$000

2008US$000

2008US$000

2008US$000

2007US$000

2007US$000

2007US$000

2007US$000

2007US$000

Due from banks

Debt Securities (inc AFS)

Loans and Advances to customers

Interest accrued on impaired Loans & Advances to customers

Other

1,902

3,946

10,749

177

270

17,044

2007

US$ 000

964

3,369

12,894

715

831

18,773

2008

US$ 000INTEREST RECEIVABLE3

23

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

Is stated after charging:

Depreciation of owned fixed assets

Operating lease rentals - Buildings

Operating lease rentals - Office Equipment

Auditors’ remuneration for audit work

Other fee to Auditors’ - taxation sevices

Gains from sale of available-for-sale financial instruments

Foreign exchange profit

Staff Costs:

Wages and salaries

Social security costs

Pension costs [Note 21]

Other staff costs

Other administrative expenses

204

389

46

134

17

25

93

118

2,594

303

309

1,012

1,977

6,195

208

324

60

147

18

-

172

172

2,850

301

295

1,027

2,801

7,274

PROFIT ON ORDINARY ACTIVITIES BEFORE TAX

OTHER OPERATING INCOME

ADMINISTRATIVE EXPENSES

Notes to the Financial Statements

4

5

6

The average weekly number of employees during the year ended 31st December 2008 was 28 (2007-27).

2007

US$ 000

2008

US$ 000

Directors’ remuneration and other emoluments were:

Directors’ emoluments 835837

EMOLUMENTS OF DIRECTORS7

The emoluments of the highest paid director were US$ 748,000 - 12 month period, (2007 US$ 659,000). No director received

benefits in the form of pension contributions during 2008 or 2007.

24

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

1,825

3

1,828

(5)

(1)

(6)

1,822

6,188

-

1,763

52

10

-

-

-

3

1,828

1,180

–

1,180

852

(35)

817

1,997

6,822

2,047

-

47

(3)

(48)

(66)

(797)

-

1,180

TAX ON PROFIT ON ORDINARY ACTIVITIES

Notes to the Financial Statements

8

(a) Analysis of charge for the year:

Current Tax

Current year

Adjustment in respect of prior periods

Total current tax charge

Deferred Tax

Current year

Adjustment in respect of prior periods

Total deferred tax (credit)/charge

(b) Factors affecting tax charge for the year:

Profit on ordinary activities before tax

Corporation tax at 30% to 31st March 2008

Corporation tax at 28% to 31st December 2008

Effects of:-

Expenses not deductible for tax purposes

Capital allowances less than / (in excess) of depreciation

Other Short term timing differences

Foreign Exchange movements on tax balances

Utilisation of tax losses brought forward

Adjustment in respect of prior periods

Current tax charge for the year

(c) Factors that may affect future tax charges:

At the year end, the Bank has a deferred tax asset of $62,154 (2007: $56,260). The asset arises in respect of capital allowances in excess of depreciation.

2007

US$ 000

2008

US$ 000

25

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

2007

US$ 000

2008

US$ 000

TAX ON PROFIT ON ORDINARY ACTIVITIES (Continued)

Notes to the Financial Statements

8

Loans and advances

Remaining maturity:

Repayable on demand

Other loans and advances:

Between 3 months and 1 year

Between 1 year and 5 years

Remaining maturity:

Repayable on demand or short notice

3 months or less (excluding demand or at short notice)

Between 3 months and 1 year

Between 1 year and 5 years

Over 5 years

Less specific bad and doubtful debt provisions

Non-performing loans and advances to customers:

Loans and advances before provisions

Loans and advances after provisions

LOANS AND ADVANCES TO BANKS

LOANS AND ADVANCES TO CUSTOMERS

9

10

24,846

83,986

56,869

19,427

11,801

(508)

196,421

4,918

4,410

981

47,602

73,139

33,712

3,744

(711)

158,467

13,202

12,491

(d) Deferred Tax

The deferred tax asset included in the balance sheet and changes recorded in the income tax gain are as follows:-

Provision at start of the yearPrior period adjustmentEffect of change in tax rateOther temporary differencesUtilisation of tax losses

561-5-

62

87335(4)

(51)(797)

56

52,311

-

5,000

57,311

7,618

5,000

-

12,618

The Bank derives and manages its loan portfolio in a risk averse manner. The Directors have agreed that the customer portfolio will comprise principally of short-term self-liquidating trade finance exposures and medium term asset backed ship financing loans.

26

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

TradeFinance

2008US$ 000

TradeFinance

2007US$ 000

ShippingPortfolio

2008US$ 000

ShippingPortfolio

2007US$ 000

Total2008

US$ 000

Total2007

US$ 000

LOANS AND ADVANCES TO CUSTOMERS (Continued)

Notes to the Financial Statements

710

-

-

-

-

-

-

-

4,094

-

(1,373)

(1,373)

(2,721)

-

-

711

-

(82)

(82)

(121)

508

508

-

711

-

711

-

711

711

711

-

(82)

(82)

(121)

508

508

4,094

711

(1,373)

(662)

(2,721)

711

711

A reconciliation of the allowance for impairment losses for loans and advances by class is as follows:

As at 1st January 2008

Charges for the year

Recoveries

Amounts written off

As at 31st December 2008

Individual Impairment

As at 1st January 2007

Charges for the year

Recoveries

Amounts written off

As at 31st December 2007

Individual Impairment

The factors considered during impairment valuation of the loans and advances included future cash flows and collateral consisting of cash deposits and mortgaged / charged assets.

27

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

Investment securities:

Public sector securities

Other debt securities – banks

Investment securities:

Listed

Unlisted

Remaining maturity:

3 months or less

Between 3 months and 1 year

Between 1 year and 5 years

Over 5 years

Floating rate notes & fixed rate notes

Commercial bills discounted

Amounts Include:

Issued by group undertakings

22,249

30,580

52,829

40,235

12,594

52,829

4,527

21,089

27,214

-

52,829

40,229

12,600

52,829

clear

10,018

22,249

13,017

35,266

35,266

-

35,266

-

13,017

22,249

-

35,266

40,262

12,600

52,862

clear

10,018

-

17,563

17,563

4,969

12,594

17,563

4,527

8,072

4,965

-

17,563

32,174

18,605

50,779

-

22,162

28,617

50,779

32,174

18,605

50,779

14,834

8,744

27,201

-

50,779

32,573

18,605

51,178

-

22,162

-

22,162

22,162

-

22,162

-

-

22,162

-

22,162

-

28,617

28,617

10,012

18,605

28,617

14,834

8,744

5,039

-

28,617

Total

2007

US$ 000

2007

US$ 000

Fair value

Held–to–

maturity

2007

US$ 000

2007

US$ 000

Original cost

Available–

for–sale

2007

US$ 000

2008

US$ 000

Fair value

Total

2008

US$ 000

2008

US$ 000

Original cost

Held–to–

maturity

2008

US$ 000

Available–

for–sale

2008

US$ 000

Notes to the Financial Statements

DEBT SECURITIES711

Valuation:

Securities are purchased with the dual purpose of complying with the necessary statutory liquidity requirements, and to provide

an even flow of floating rate interest receipts. Bills are purchased primarily as a result of the Bank’s involvement in the discounting

of letters of credit. Although some paper may be traded prior to maturity, it is not the Bank’s original intention to sell these

assets and they are therefore funded accordingly. The Directors consider that the book value of commercial bills is not materially

different from fair value, since this is intrinsically linked to a Libor plus margin pricing regime which is reasonably consistent

throughout this market. The Bank intends to hold the securities listed under held-to-maturity until their final maturity.

28

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

Cost:

Balance as at 31st December 2007

Additions

Disposals

At 31st December 2008

Accumulated Depreciation:

Balance as at 31st December 2007

Charge for the year

Disposals

At 31st December 2008

Net book value at 31st December 2008

Net book value at 31st December 2007

Accrued interest receivable (net of suspended interest)

Prepaid expenses

Deferred tax asset (Note 8D)

Other receivables

Assets and liabilities denominated in foreign currencies:

Denominated in US dollars

Denominated in currencies other than US dollars

Total assets

Denominated in US dollars

Denominated in currencies other than US dollars

Total liabilities excluding capital and other reserves

2,33469

(41)

2,362

1,877208(41)

2,044318

457

1,722

287

56

275

2,340

243,423

31,212

274,635

184,850

22,541

207,391

304

6

(3)

307

234

24

(3)

255

52

70

2,203

245

62

2,484

4,994

clear

267,252

29,476

296,728

196,348

29,876

226,224

1,410

13

-

1,423

1,330

54

-

1,384

39

80

481

50

-

531

197

107

-

304

227

284

139

-

(38)

101

116

23

(38)

101

-

23

2008

Total

US$ 000

2007

US$ 000

Furniture,

fixtures and

fittings

US$ 000

2008

US$ 000

* Computer

and other

equipment

US$ 000

Leasehold

improve–

ments

US$ 000

Motor

vehicles

owned

US$ 000

Notes to the Financial Statements

TANGIBLE FIXED ASSETS12

OTHER ASSETS, PREPAYMENTS AND ACCRUED INCOME13

ASSETS AND LIABILITIES14

*Included in the above is the telephone system under finance lease which had a NBV of Nil (2007: $16,684)

29

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

Notes to the Financial Statements

Repayable on demand

3 months or less

Between 3 months and 1 year

Between 1 year and 5 years

Amounts include:

Due to group undertakings

Repayable on demand

3 months or less

1 year or less but over 3 months

Accrued interest and expenses payable

UK corporation tax

Forward foreign exchange contracts - fair value

Other

Obligations under finance leases payable:

1 year or less

Between 1 year and 5 years

Less: future finance charges

Current Obligations

Non Current Obligations

With agreed maturity dates or periods of notice, by remaining maturity of:

With agreed maturity dates or periods of notice, by remaining maturity of:

A total of US$4.07 million ( 2007 - US$10.4 million) of deposits are frozen and held as collateral against trade finance loan facilities.

3,908

64,030

34,000

40,000

141,938

14,000

38,597

11,950

10,434

60,981

2,882

1,180

-

383

4,445

16

14

(3)

27

12

15

27

4,472

1,344

95,000

35,004

40,000

171,348

14,000

49,561

-

-

49,561

2,685

1,352

771

493

5,301

15

-

(1)

14

14

-

14

5,315

2007

US$ 000

2008

US$ 000

DEPOSITS FROM BANKS

CUSTOMER ACCOUNTS

OTHER LIABILITIES, ACCRUALS AND DEFERRED INCOME

15

16

17

30

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

Notes to the Financial Statements

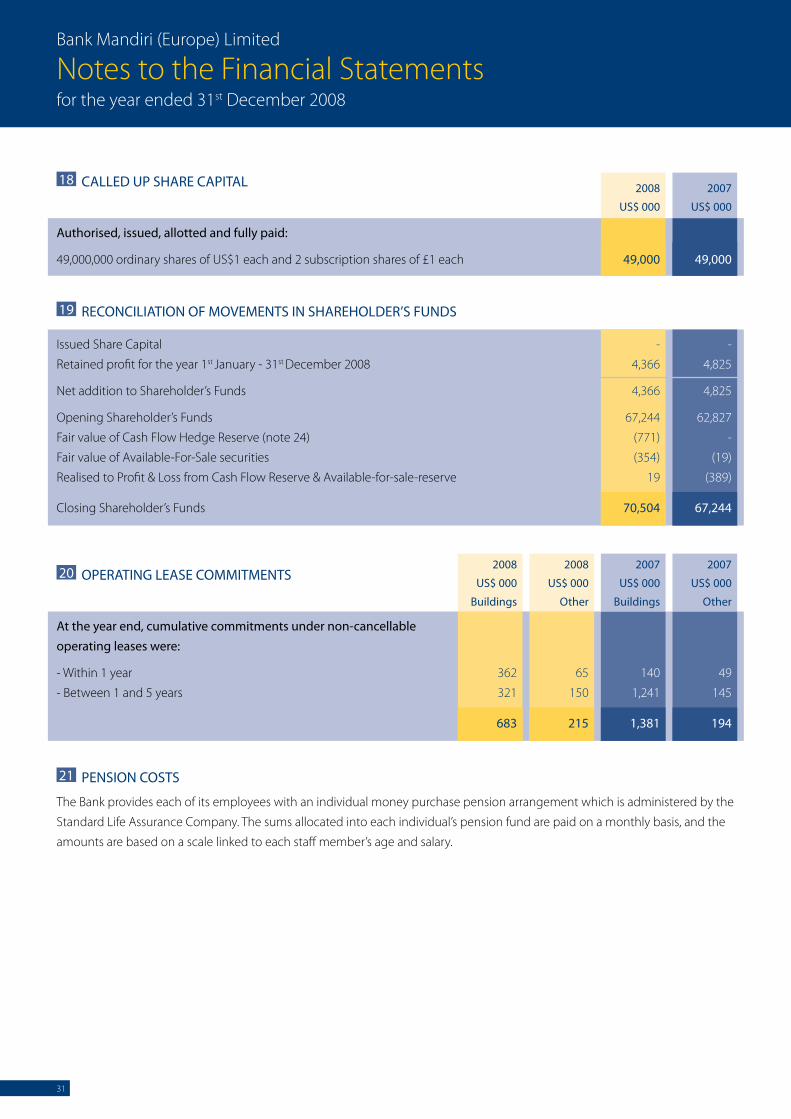

Authorised, issued, allotted and fully paid:

49,000,000 ordinary shares of US$1 each and 2 subscription shares of £1 each

Issued Share Capital

Retained profit for the year 1st January - 31st December 2008

Net addition to Shareholder’s Funds

Opening Shareholder’s Funds

Fair value of Cash Flow Hedge Reserve (note 24)

Fair value of Available-For-Sale securities

Realised to Profit & Loss from Cash Flow Reserve & Available-for-sale-reserve

Closing Shareholder’s Funds

At the year end, cumulative commitments under non-cancellableoperating leases were:

- Within 1 year

- Between 1 and 5 years

49,000

-

4,825

4,825

62,827

-

(19)

(389)

67,244

49

145

194

65

150

215

49,000

-

4,366

4,366

67,244

(771)

(354)

19

70,504

140

1,241

1,381

362

321

683

2007

US$ 000

2008

US$ 000

2007

US$ 000

Buildings

2008

US$ 000

Buildings

2007

US$ 000

Other

2008

US$ 000

Other

CALLED UP SHARE CAPITAL

RECONCILIATION OF MOVEMENTS IN SHAREHOLDER’S FUNDS

OPERATING LEASE COMMITMENTS

PENSION COSTS

18

19

20

21

The Bank provides each of its employees with an individual money purchase pension arrangement which is administered by the

Standard Life Assurance Company. The sums allocated into each individual’s pension fund are paid on a monthly basis, and the

amounts are based on a scale linked to each staff member’s age and salary.

31

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

1,526

1,526

7,019

7,019

8,545

1,526

1,526

7,019

7,019

8,545

681

681

19,458

19,458

20,139

681

681

19,458

19,458

20,139

2008

US$ 000

Book value

2008

US$ 000

Fair value

2007

US$ 000

Book value

2007

US$ 000

Fair value

Notes to the Financial Statements

MEMORANDUM ITEMS22

CONTINGENT LIABILITIES:

Transaction-related:

Guarantees pledged

Trade-related:

Letters of credit issued

RISK MANAGEMENT723

The identification, measurement and containment of risk is integral to the management of our business. Our risk policies and

procedures are regularly updated to meet changing business requirements, and to comply with best practice. Our parent

company, PT Bank Mandiri (Persero) Tbk, conducts an in-depth review at least once a year of our loan portfolio and also

conducts a review of our internal controls/procedures. Our Audit Committee is apprised of these and other developments

throughout the year to ensure adequate controls are in place to meet our changing business requirements.

The Bank is firmly committed to the management of risk, recognising that sound internal risk management is essential to its

prudent operation, particularly with the growing complexity, diversity and volatility of markets, facilitated by rapid advances

in technology and communications. Risk management is given high priority throughout the Bank.

Responsibility for risk management policies, limits, and the level of risk assumed, lies with the Board of Directors. The Board

charges Senior Management with developing, presenting and implementing these policies and limits. The structure is

designed to provide a reasonable degree of assurance that no single event, or contribution of events, will materially affect

the wellbeing of the Bank.

A Risk Committee comprised of Senior Management plays a key role in the identification, evaluation and management of all

risks. All credit and other new product decisions require direct Senior Management & Risk Committee approval. Management

is supported by a comprehensive structure of independent controls, analysis and reporting processes.

The Bank has strict controls and detailed procedures in place for the monitoring of the financial instruments employed in

its business. Before any new financial instrument is employed by the Bank approval must be sought from the Bank’s Senior

Management Committee and as part of this approval process the Senior Management Committee ensures that the Bank has

the relevant expertise, adequate controls and operating procedures in place before the new financial instrument is initiated.

Where it is deemed necessary product or sector limits are established and monitored such that excessive concentration risk

is minimised.

The Bank’s Board of Directors, Asset and Liability Committee, Risk Committee and Audit Committee, assist in appraising

market trends, economic and political developments, and providing strategic direction for all aspects of risk management.

A Risk Management and Control

32

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

Notes to the Financial Statements

The Bank has in place an extensive number of limit controls and management information systems to facilitate effective

management overview. All limits are approved by the Board of Directors and are reviewed at least annually. Limit breaches,

if any, are reported to the Chief Executive and Senior Management on a daily basis.

The following basic elements of sound risk management are applied to all financial risk instruments, including derivatives.

This includes where appropriate:

• ReviewbytheBoardofDirectorsandSeniorManagement. • Riskmanagementprocesseswithintegralproductrisklimits. • Measurementproceduresandinformationsystems. • Continuousriskmonitoringandfrequentmanagementreporting. • Segregationofduties,comprehensiveinternalcontrolsandauditprocedures.

In the opinion of the Directors, the period end numerical disclosures are not materially unrepresentative of the entity’s

position during the period or its agreed objectives, policies and strategies. In addition, the Directors have no plans, at the

current time, to make any significant changes either to the product base or to the methods employed in the management

and control of the above-mentioned risks.

Market risk refers to the uncertainty of future earnings, resulting from changes in interest rates, foreign exchange rates,

market prices and volatility thereof. Senior Management constantly monitors market risk by a combination of reports and

real time market information systems.

B Market Risk

Interest rate risk arises when there is a mis-match between positions which are subject to interest rate adjustments within

a specific period. In the Bank’s funding/lending activities, fluctuations in interest rates are reflected in interest margins and

earnings. Our interest rate risk profile is short term and liquid and the Directors therefore feel that risks have been minimised.

Hedging techniques can be applied on a limited basis should the need arise.

An interest rate gap is a common measure of interest rate sensitivity (note 25). A liability gap occurs when more liabilities

than assets are subject to rate changes during a prescribed future time period. Interest rate gaps are monitored by Senior

Management & Asset & Liability Committee regularly.

The Bank does not actively trade in the foreign exchange markets on its own account, and foreign exchange swaps and

forward foreign exchange contracts are committed for management of the Bank’s expenses and the Bank’s assets and

liabilities.

Where possible the Bank matches its currency transactions. The majority of the asset and liability positions are denominated

in US Dollars and therefore, in the opinion of the Directors, the level of currency risk is considered to be minimal.

C Interest Rate Risk

D Currency Risk

RISK MANAGEMENT (Continued)723

33

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

Notes to the Financial Statements

Liquidity risk arises from fluctuations in cash flows. The liquidity risk management process ensures that the Bank is able to

honour all of its financial commitments as they fall due. Liquidity is monitored daily through specialised reports provided to

Senior Management against appropriate limits set by the Board of Directors and with reference to statutory requirements. In

addition the Asset and Liability Committee and the Risk Committee review the liquidity position periodically. The Bank has

access to a variety of funding sources including bank deposits, loan facilities, customer deposits and corporate trade finance

deposits. Regular weekly reviews are conducted, via meetings of the Asset and Liability Committee, of these sources and

requirements for perusal by Senior Management. In practice, the Bank operates well within its prescribed liquidity levels.

In the light of market conditions, at the present time, the Bank does not generally offer medium-term advances. As existing

medium-term advances run off, they are being replaced by shorter-term advances. Management forecasts for the year

ahead, even on the assumption that all bank lines that fall due are not replaced, demonstrate that, taking into account

reasonably possible changes in market conditions, the Bank can meet all repayment obligations through its existing cash

resources, scheduled repayment of advances and/or the sale of assets. There is no reliance on facilities being granted by the

parent bank, although in practice such facilities are likely to be available if required

RISK MANAGEMENT (Continued)723

E Liquidity Risk

As at 31st December 2008

Due to Banks

Customer Accounts

Other financial

Total financial liabilities

As at 31st December 2007

Due to Banks

Customer Accounts

Other financial

Total financial liabilities

171,348

49,561

5,315

226,224

141,938

60,981

4,472

207,391

40,000

-

471

40,471

-

-

-

-

40,000

-

1,385

41,385

-

-

-

-

35,004

-

4,844

39,848

34,000

10,435

3,087

47,522

95,000 *

-

-

95,000

64,030

3,500

-

67,530

1,344

49,561

-

50,905

3,908

47,046

-

50,954

Total

US$ 000

1 to 5

years

US$ 000

Over5 years

US$ 000

3 to 12

months

US$ 000

Less than

3 months

US$ 000

On

Demand

US$ 000

Analysis of financial liabilities by remaining contractual maturities

The table below summarises the maturity profile of the Bank’s financial liabilities as at 31 December 2008 based on contractual

undiscounted repayment obligations. Repayments which are subject to notice are treated as if notice were to be given immediately.

However, the Bank expects that many customers will not request repayment on the earliest date the Bank could be required to

pay and the table does not reflect the expected cash flows indicated by the Bank’s deposit retention history.

* This amount includes cash collateral deposits of US$50 million

34

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

Notes to the Financial Statements

As at 31st December 2008

Guarantees

Letters of credit issued

Total financial liabilities

As at 31st December 2007

Guarantees

Letters of credit issued

Total financial liabilities

1,526

7,019

8,545

681

19,458

20,139

-

-

-

-

-

-

-

-

-

-

-

-

1,526

7,019

8,545

681

19,458

20,139

-

-

-

-

-

-

-

-

-

-

-

-

Ageing for Contingent liabilities TotalUS$ 000

Over5 years

US$ 000

1 to 5years

US$ 000

3 to 12 monthsUS$ 000

Less than3 months

US$ 000

OnDemandUS$ 000

RISK MANAGEMENT (Continued)723

Operational Risk is the risk that deficiencies in information systems or internal controls result in unexpected business, financial

and operating losses. Operational Risk is ultimately managed by the Board of Directors and is given the highest priority.

Senior Management are charged with applying stringent procedures to mitigate risk of error, fraud, money laundering, and

other irregularities. In addition, strong disaster recovery procedures have been formulated and are tested on at least a yearly

basis. Internal Audit reviews the risk mitigation processes to ensure that these meet the organisation’s current needs and are

being properly implemented and controlled.

Controls are in place to constantly monitor the level of capital to ensure the Bank is able to meet its regulatory obligation

on a daily basis. In doing so the Board of Directors believe that the interest of all stakeholders including customers and

shareholders are fully protected. Account is taken of all potential events that could have an impact on capital.

Management have stress tested the Bank’s capital requirements. This stress testing takes into account reasonably likely

developments in all of the above risks, the Board’s balance sheet management strategy and the deteriorating market

conditions. This stress testing has demonstrated that the Bank is adequately capitalised to support the existing business

and future plans.

The Bank uses a formal credit process to quantify and evaluate the risk of proposed credits, and to ensure appropriate

returns for assuming risks. Relationship Managers undertake a full financial review of each client at least annually, so that the

Bank remains aware of counterparties’ risk profiles. This analysis includes a review of previous historical financial data, future

projections, industry reviews, broker reports and credit analysis techniques.

Securities, Letters of Credit, Guarantees and Off-Balance Sheet instruments are managed by the same process. Settlement

and any other credit risks are restricted through product limits and counterparty netting agreements.

From time to time the Bank takes collateral to mitigate credit or transactional risks. The taking of collateral as security is

governed by detailed policies and procedures and where necessary the security is registered and perfected in the relevant

jurisdictions using legal counsel.

F Operational Risk

G Capital Adequacy Risk

H Credit Risk

35

Bank Mandiri (Europe) Limited

for the year ended 31st December 2008

Notes to the Financial Statements

RISK MANAGEMENT (Continued)723

The table below shows the maximum exposure to credit risk for the components of the balance sheet, including derivatives. The

maximum exposure is shown gross, before the effect of mitigation through use of master netting and collateral agreements.

Risk concentrations of the maximum exposure to credit risk

Concentration of risk is managed by client/counterparty, by geographical region and industry sector. The maximum credit

exposure to any non-bank client during has been within our prescribed LECB by the FSA of US$16.8 million before talking account

of collateral or other credit enhancements.

The Bank’s financial assets, before talking into account any collateral held or other credit enhancements can be analysed by the

following geographical regions:

Cash and money at call and deposits with central banks

Loans and advances to banks

Loans and advances to customers

Debt securities

Other assets prepayments and accrued income

Total

Contingent Liabilities

3,231

57,311

158,467

52,829

2,340

274,178

20,139

31,598

12,618

146,421

50,779

4,994

246,410

8,545

3,231

57,311

159,178

52,829

2,340

274,889

20,139

31,598

12,618

196,929

50,779

4,994

296,918

8,545

[09]

[10]

[11]

[13]

[22]

GrossMaximum exposure

2008US$ 000

Notes

GrossMaximum exposure

2007US$ 000

NetMaximum exposure

2008US$ 000

NetMaximum exposure

2007US$ 000

United Kingdom

Europe

Asia

North America

Total

99,110

10,427

146,503

18,850

274,889

126,152

13,880

132,500

24,386

296,918

2007

US$ 000

2008

US$ 000

36

TotalLossDoubtfulSub

Standard

Special

MentionCurrent

Neither past

due nor

impaired

Past due or individually impaired

Bank Mandiri (Europe) Limited

for the year ended 31 December 2008

Notes to the Financial Statements

RISK MANAGEMENT (Continued)723

An industry sector analysis of the Bank’s financial assets, before taking into account collateral held or other credit enhancements,

is as follows:

Bank

Intergroup

Corporate Finance

Foodstuffs

Metals

Other

Pharmaceutical

Shipping

Sovereign debt

Total

81,137

10,018

22,245

22,824

18,996

32,338

8,913

64,562

13,856

274,889

72,833

-

22,162

28,075

66,783

28,511

8,537

55,325

14,692

296,918

2007

US$ 000

2008

US$ 000

As at 31st December 2008

Due from Banks

Loans and Advances

Intergroup

Total

As at 31st December 2007

Due from Banks

Loans and Advances

Other

Total

72,833

224,085

-

296,918

81,137

183,734

10,018

274,889

-

47

-

47

-

230

-

230

-

-

-

-

-

850

-

850

-

4,279

-

4,279

-

-

-

-

-

593

-

593

-

12,122

-

12,122

Credit Quality per class of financial assets:

72,833

219,166

-

291,999

81,137

170,532