bank marketing paper

TRANSCRIPT

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 1/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 1

Bank & Fi nanci al I nst i t ut i on Mar ket i ng

J oseph Kul wi cki

FI N 509: Bank and Fi nanci al I nst i t ut i on Management

Wal sh Col l ege- Spr i ng 2013

J une 3, 2013

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 2/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 2

Abst r act

As banks and f i nanci al i nst i t ut i ons begi n t o shi f t out of t he

most r ecent f i nanci al cr i s i s, i t i s cr i t i cal t hey r emai n

compet i t i ve t o mai nt ai n cur r ent cl i ent s and mor e i mpor t ant l y

devel op new cl i ent s. Al most dai l y we hear about new market i ng

pl ans by l ar ge r et ai l and r est aur ant chai ns and t he aut omot i ve

i ndust r y; never do we hear f r om compani es about t hei r new

mar ket i ng i n t he f i nanci al sector . I t i s cr i t i cal f or compani es

such as Bank of Amer i ca, GE Capi t al , and ot her banks and

f i nanci al i nst i t ut i ons t o i ncrease t hei r mar ket i ng t o obt ai n

mar ket shar e f or bot h t hei r r et ai l and commer ci al oper at i ons.

Banks and f i nanci al i nst i t ut i ons must under st and who t hei r

l ar gest cur r ent and f ut ur e audi ences ar e. Fur t her , t hey must

devel op st r at egi es f ocused on at t r act i ng and r et ai ni ng t hese

t arget market s.

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 3/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 3

Bank & Fi nanci al I nst i t ut i on Mar ket i ng

Andr ew Needham and Phi l i p McNaught on once sai d, “Consumers'

desi r e to be l i st ened t o and i nvol ved mor e di r ect l y i n what a

brand does and says means t hat now, more t han ever , t her e i s a

gr eat opport uni t y t o market wi t h consumer s r ather t han at t hem. ”

I n order f or any company t o set t hemsel ves apart t hey ar e i n

need of a market i ng team whi ch knows who t hei r cl i ent i s and how

t o r each t hem. Thi s i s t r ue f or a company l i ke McDonal d’ s and

even mor e i mpor t ant f or banks and f i nanci al i nst i t ut i ons. Banks

have l arge mar ket i ng budget s, but t hey ar e not spendi ng i t i n

t he manner t hat br i ngs t hem t he same amount of exposur e. I t i s

t r ue banks ar e not as f un or as sexy as t he new Camaro, however ,

t hey account f or a si gni f i cant por t i on of t he US GDP and al l

consumers i nt er act wi t h banks on a weekl y basi s. “As t he wor l d

emer ges f r om t he gl obal f i nanci al cr i si s, banks f i nd t hemsel ves

i n a chal l engi ng envi r onment . Low i nt er est r at es are maki ng i t

di f f i cul t t o gener at e r evenue i n t r adi t i onal ways, whi l e r ai si ng

capi t al and r educi ng r i sk have become t he new pr i or i t i es ( Far ah,

Macaul ay & Er i csson) . ” Market i ng i s key t o maki ng t hi s change.

“J ust do i t ” ( Ni ke) , “Di amonds ar e For ever ” ( DeBeer s) ,

“They’ r e G- r - r - r - eat ” ( Fr ost ed Fl akes) ; t hese ar e t hr ee of t he

t op 20 mar ket i ng sl ogans of al l t i me ( "The t op 20, " 2011) . Onl y

one Fi nanci al I nst i t ut i on made t hi s pr est i gi ous l i st , Amer i can

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 4/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 4

Expr ess. “Don’ t Leave Home Wi t hout I t ”- The hi st or y of t hi s

campai gn began i n, “1975 when Amer i can Expr ess f i r st advi sed t o

consumers t hat t hey shoul dn' t l eave home wi t hout t hei r AMEX

card. These sl ogans at t empt ed t o est abl i sh Amer i can Expr ess as

t he t op pr ovi der of t r avel er ' s checks and car ds t hat coul d be

used i n ever y- day l i f e. Amer i can Expr ess al so used cel ebr i t y

endorsement s t o hel p cement t hi s phr ase i nto t he mi nds of

consumers. The f i r st commerci al s f eat ured Academy Award wi nner

Kar l Mal den. Ot her cel ebr i t i es t hat pr ovi ded endor sement s, over

t he years, i ncl uded St ephen Ki ng and J er r y Sei nf el d.

( I nvest opedi a) ” Al most 40 years l ater , we have not had a

mar ket i ng campai gn f r om a bank or f i nanci al i nst i t ut i on t hat has

been as preval ent as Amer i can Express.

Banks, i n a br oad sense, t ar get t wo t ypes of cl i ent s-

consumer and commer ci al . These cl i ent s ar e served vi a a r etai l

br anch, onl i ne, and di r ect sal es f r om banker s. Consumer s ar e

t ypi cal l y i nt er act i ng wi t h t he banks t hr ough t he f ol l owi ng

ser vi ces:

i . Savi ngs Account - A deposi t account hel d at a bank

or ot her f i nanci al i nst i t ut i on t hat pr ovi des

pr i nci pal secur i t y and a modest i nt er est r at e.

( I nvest opedi a)

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 5/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 5

i i . Checki ng Account - A t r ansact i onal deposi t account

hel d at a f i nanci al i nst i t ut i on t hat al l ows f or

wi t hdr awal s and deposi t s. Money hel d i n a

checki ng account i s ver y l i qui d, and can be

wi t hdr awn usi ng checks, aut omat ed cash machi nes

and el ect r oni c debi t s, among ot her methods.

( I nvest opedi a)

i i i . Mort gage- A debt i nst r ument t hat i s secur ed by

t he col l at er al of speci f i ed r eal est at e pr oper t y

and t hat t he bor r ower i s obl i ged t o pay back wi t h

a pr edet er mi ned set of payment s. ( I nvest opedi a)

i v. Loans ( Home Equi t y, Aut o) - The act of gi vi ng

money, pr oper t y or other mat er i al goods t o a

another par t y i n exchange f or f ut ur e repayment of

t he pr i nci pal amount al ong wi t h i nt er est or ot her

f i nance char ges. ( I nvest opedi a)

v. Ref i nanci ng debt - Consol i dat i on of debt i nt o one

mont hl y payment .

vi . Cer t i f i cat e of Deposi t - A savi ngs cer t i f i cat e

ent i t l i ng t he bear er t o r ecei ve i nt er est . A CD

bear s a mat ur i t y dat e, a speci f i ed f i xed i nt er est

r at e and can be i ssued i n any denomi nat i on. CDs

are general l y i ssued by commerci al banks and ar e

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 6/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 6

i nsur ed by t he FDI C. The t er m of a CD gener al l y

r anges f r om one mont h t o f i ve years.

( I nvest opedi a)

Busi nesses i nt er act wi t h banks t hr ough t he f ol l owi ng f i nanci al

servi ces and i nst r ument s:

i . Busi ness Capi t al - Pr ovi di ng ongoi ng capi t al

l i nes i n or der t o meet shor t t er m and l ong t er m

obl i gat i ons. ( I nvest opedi a)

i i . Cash Management - assi st i ng i n t he pr ocess of

col l ect i ng, managi ng and ( shor t - t er m) i nvest i ng

cash. A key component of ensur i ng a company' s

f i nanci al st abi l i t y and sol vency

i i i . Cl ear i ng and Fi nanci ng Sol ut i ons- consi st i ng of

hedge f unds, pr of essi onal t r ader s i ncl udi ng

market maker s and pr opr i et ary t r adi ng f i r ms,

ECNs/ AT Ss, r esear ch sal es and t r adi ng f i r ms,

advi sors, and i nvest ment banks ( "Cl ear i ng and

f i nanci ng: , " 2013)

i v. Asset Based Lendi ng- A busi ness l oan secured by

col l at er al ( asset s) . The l oan, or l i ne of

credi t , i s secur ed by i nvent or y, account s

r ecei vabl e and/ or ot her bal ance- sheet asset s.

( I nvest opedi a)

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 7/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 7

v. Gl obal Mar ket s- access t o gl obal mar ket s,

equi t i es, f unds, and cur r enci es

The above l i st ed ser vi ces ar e st andar ds pr oduct and ser vi ces

most commerci al banks pr ovi de. Bank of Amer i ca, Wel l s Far go,

and J P Mor gan Chase pr ovi de al l of t hese ser vi ces i n ver y

si mi l ar manner s. I t i s up t o t he i ndi vi dual mar ket i ng

depar t ment s wi t hi n t hese banks t o set t hemsel ves apar t f r om t he

compet i t i on.

Market i ng t o consumers i s much di f f er ent t han market i ng t o

commerci al busi nesses. When market i ng t o consumers, banks

l ever age t he l ocal r et ai l l ocat i on, i nt er net , and l ocal medi a.

The quest i on mar ket i ng t eams need t o ask t hemsel ves i s “what

makes our pr oduct s di f f er ent ?” I n t he past f ew year s, mar ket i ng

t eams have been get t i ng bet t er at answer i ng t hi s quest i on. The

si mpl e answer i s t hr ough cust omer ser vi ce and ease of doi ng

busi ness. Rene Domi ngo t al ks about t he concept s wi t hi n t he

banki ng communi t y usi ng a t er m cal l ed r esponsi ve banki ng, “The

obj ect i ves of r esponsi ve banki ng ar e t o cut cust omer wai t i ng

t i me, r educe t r ansact i on t i me, and cut cost s and wast es t hr ough

r educt i on i n i dl e t i me, wast es, and ot her i nef f i ci enci es i n bot h

t he f r ont - l i ne and back r ooms. Responsi ve banki ng pr event s t he

l oss of cust omer s by el i mi nat i ng t he causes of sl ow and

i nsensi t i ve bur eaucrati c ser vi ce. I t addr esses t hi s concer n wi t h

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 8/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 8

syst em changes t hat r esul t i n paper l ess and queue- l ess banki ng.

Ci t i bank' s Gl obal Br anch concept el i mi nat es queues by shi f t i ng

cust omer ser vi ce f r om t he t el l er ar ea ( wi ndows) t o t he sal es and

ser vi ce sect i on ( desks) , wher e cust omer r el at i onshi ps ar e

‘ opened, servi ced, deepened, and br oadened. ’ Gl obal Br anches

l ook exact l y t he same - f ur ni t ur e, l i ght s, ser vi ce st andar ds,

f aci l i t i es, al a McDonal d' s, wi t h no sur pr i ses. Usi ng t he

machi nes i n t hese br anches, cust omer s can pr i nt up- t o- t he- mi nut e

st atement s wi t h a push of a but t on. They can al so enj oy t he

conveni ence of paper l ess, f orml ess deposi t and wi t hdr awal

t r ansacti ons. ”

I n r ecent years, banks have underst ood t he i mpor t ance of

begi nni ng t o i ncr ease t hei r spend wi t hi n mar ket i ng and

adver t i si ng. Accor di ng t o t he ABA Bank Marketing Survey Report,

“Some of t he sur vey’ s f i ndi ngs i ncl ude adver t i si ng expendi t ur es

account ed f or 53 percent of 2005 market i ng expendi t ur es. Ot her

maj or expendi t ur es i ncl ude publ i c r el at i ons ( 23 per cent ) and

sal es pr omot i ons ( 16 per cent ) ; Banks i ncr eased spendi ng f or

newspaper adver t i si ng t o 31 per cent of t ot al adver t i si ng dol l ar s

spent , compared to 26 per cent i n 2003. Spendi ng f or r adi o

commerci al s decreased f r om 15 percent i n 2003 to 12 i n 2005.

Tel evi si on commer ci al s' share of adver t i si ng expendi t ures

r emai ned at 6 per cent ; Fi f t y- ei ght per cent of publ i c rel at i ons

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 9/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 9

expendi t ur es went t owar ds communi t y r el at i ons act i vi t i es, up

f r om 49 per cent i n 2003. Banks wi t h $5 bi l l i on t o $24. 9 bi l l i on

i n asset s spent 19 per cent of t hei r publ i c r el at i ons dol l ar s on

shar ehol der r el at i ons, however t hose wi t h $25 bi l l i on or mor e i n

assets spent a comparabl e pr oport i on on medi a rel at i ons; Banks

wi t h l ess t han $5 bi l l i on i n asset s spent t he l ar gest shar e of

t hei r sal es promot i on budget on gi ve- away i t ems ( 32 per cent ) .

Banks wi t h $5 bi l l i on or mor e i n asset s spent al most hal f ( 48

per cent ) on poi nt - of - sal e mat er i al s, such as di spl ays, banner s

and br ochur es. ”

Al t hough compani es ar e i ncr easi ng thei r market i ng budget s

t hey ar e qui ckl y l osi ng mar ket shar e ( see char t bel ow) .

Accor di ng t o Frankl i n Edwar ds, “I n t he Uni t ed St at es, t he

i mpor t ance of commerci al banks as a sour ce of f unds t o

nonf i nanci al bor r ower s has shr unk dr amat i cal l y. I n l 974 banks

pr ovi ded 35 per cent of t hese f unds; t oday t hey pr ovi de ar ound 22

per cent . Thr i f t i nst i t ut i ons ( savi ngs and l oans, mut ual savi ngs

banks, and cr edi t uni ons) , whi ch can be vi ewed as speci al i zed

banki ng i nst i t ut i ons, have al so suf f er ed a decl i ne i n mar ket

shar e, f r om more t han 20 per cent i n t he l at e 1970s t o bel ow 10

per cent i n the 1990s. ”

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 10/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 10

When banks are market i ng t o t hei r commerci al cl i ent s, we

see a much more di r ect appr oach. Of t en f or t hese cl i ent s who

have si gni f i cant deposi t s, a banker i s assi gned t o handl e t he

r el at i onshi p bet ween t he bank and t he cl i ent . The t ypi cal r ol e

f or a banker i s t o be a sal esman and advi ser t o t he cl i ent . The

banker opens t he door t o al l t he servi ces we l i st ed above and

mor e. They pr ovi de a one poi nt of cont act t o t he cl i ent .

I compl et ed a t wo week st udy wher e I kept t r ack of how many

t i mes I hear d or saw an adver t i sement f r om a bank or f i nanci al

i nst i t ut i on ver sus f ast f ood chai ns. My st udy di d not i ncl ude

any onl i ne adver t i sement s. These are my f i ndi ngs:

Advertising During 2 Week Period

Banks/ Fi nanci al I nst i t ut i onFastFood

Tel evi si on Commer ci al s 6 15

Pr i nt ( Newspaper s, Magazi nes) 5 12

Bi l l boar ds 12 8

Radi o 14 4

Ot her 1 4

Tot al 38 43

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 11/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 11

Col l ect i vel y, f ast f ood r est aur ant s ( pr i mar i l y McDonal ds and

Bur ger Ki ng) had more poi nt s of exposur e t han banks and

f i nanci al i nst i t ut i ons. Fast f ood r est aur ant s had al most t hr ee

t i mes t he amount of t el evi si on commerci al s and more t han doubl e

t he amount of pr i nt adver t i si ng t han t he banks. I was exposed

t o mor e bi l l boar ds and r adi o spot s f ocusi ng on banks t han f ast

f ood r est aur ant s. The most uni que campai gn was by Hunt i ngt on

Bank. Accor di ng t o Ml i ve, “I nst ead of adver t i si ng i t s r at es or

pr oduct s, Hunt i ngt on Bank East Mi chi gan Regi on Presi dent Mi chael

Fezzey i nt er vi ews busi ness l eader s and t hen f eat ur es t hem on t he

“Best i n Busi ness” spot on WJ R r adi o. ” The ar t i cl e quot es Rhan

Rampt on, a market i ng execut i ve f or Hunt i ngt on Bank, “The i dea i s

t hat we don’ t adver t i se anyt hi ng about Hunt i ngt on, we don’ t make

an of f er , we don’ t quot e a r at e, we don’ t hi ghl i ght

product s…When you t hi nk about i t , what a bank does on a day- t o-

day basi s i s eval uat e compani es, so why not hi ghl i ght t hem f or

bei ng good cust omer s, f or bei ng good busi nesses. ” Hunt i ngt on

Bank i s at t empt i ng t o t r y somet hi ng new t o at t r act new cl i ent s.

Through t he use of t hese r adi o spot s, Hunt i ngt on Bank i s l et t i ng

pot ent i al cl i ent s know t hey ar e i n t he busi ness of l endi ng.

Fur t her , peopl e have an i mmedi ate comf ort l evel wi t h Hunt i ngt on

Bank si nce t hey ar e wi t h l ocal smal l busi nesses.

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 12/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 12

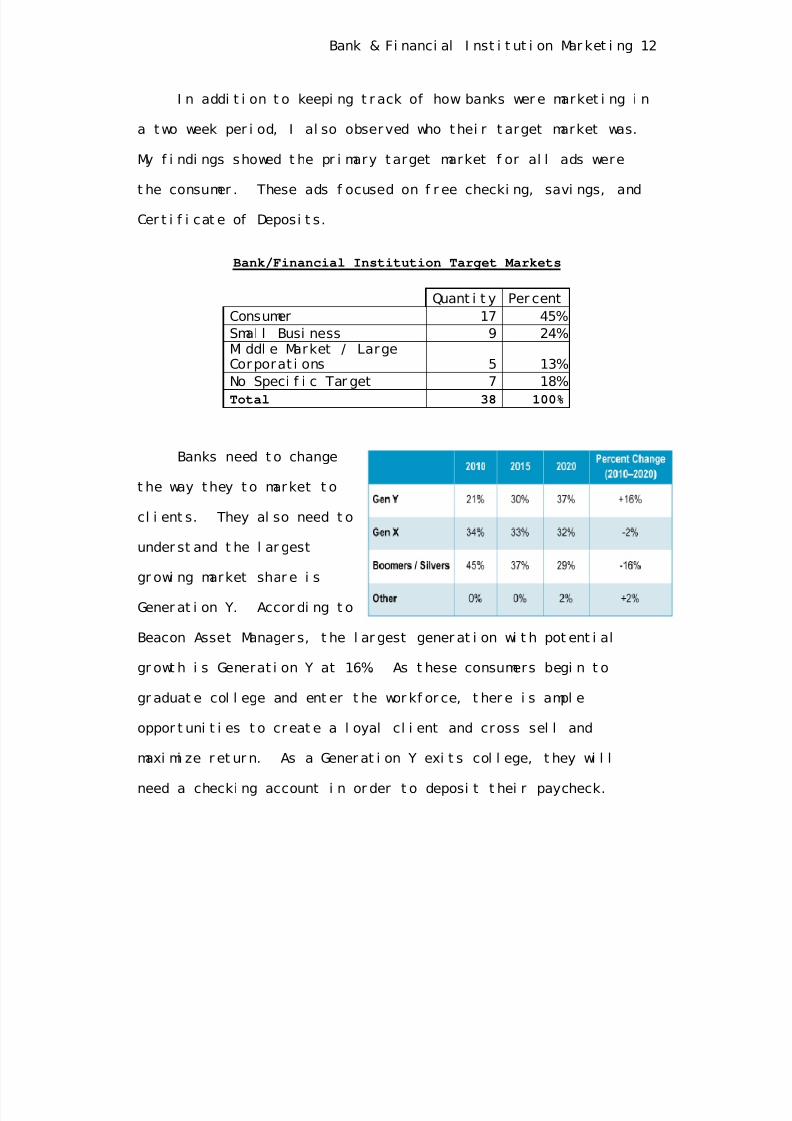

I n addi t i on t o keepi ng t r ack of how banks wer e market i ng i n

a two week per i od, I al so obser ved who thei r t arget market was.

My f i ndi ngs showed t he pr i mary t arget market f or al l ads were

t he consumer . These ads f ocused on f r ee checki ng, savi ngs, and

Cer t i f i cat e of Deposi t s.

Bank/Financial Institution Target Markets

Quant i t y Per cent

Consumer 17 45%

Smal l Busi ness 9 24%Mi ddl e Market / LargeCorporat i ons 5 13%

No Speci f i c Tar get 7 18%

Total 38 100%

Banks need t o change

t he way t hey t o market t o

cl i ent s. They al so need t o

under st and t he l argest

gr owi ng market shar e i s

Gener at i on Y. Accor di ng t o

Beacon Asset Manager s, t he l argest gener at i on wi t h potent i al

gr owt h i s Generat i on Y at 16%. As t hese consumers begi n t o

gr aduat e col l ege and ent er t he wor kf or ce, t her e i s ampl e

oppor t uni t i es t o creat e a l oyal cl i ent and cross sel l and

maxi mi ze r et ur n. As a Gener at i on Y exi t s col l ege, t hey wi l l

need a checki ng account i n order t o deposi t t hei r paycheck.

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 13/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 13

Next , t hey wi l l need aut o l oan t o r epl ace t he car t hey have been

dr i vi ng si nce t hei r sophomor e year of hi gh school 8 year s pr i or .

Four year s l at er , af t er get t i ng mar r i ed, t he cl i ent wi l l need a

mor t gage t o pur chase a house; t hi s l oyal cl i ent wi l l hopef ul l y

come t o t he bank. I n order t o i mpr ove t he home, t hey wi l l need

a home equi t y l i ne of cr edi t . Two year s l at er , t he mar r i ed

coupl e wi l l need t o st ar t t hi nki ng about r et i r ement . Hopef ul l y,

t he bank can pr ovi de a f i nanci al advi ser f or t hei r cl i ent . I t

i s i mpor t ant f or a bank t o cross sel l t hei r ser vi ces i n or der t o

maxi mi ze pr of i t . Most consumer s ar e at t r act ed t o a bank f or t he

f r ee checki ng and $100 whi ch wi l l be deposi t ed i nt o thei r

account af t er t hr ee mont hs of use. The hardest par t i s ensur i ng

t he cl i ent knows t o come t o you when they need a l oan or ot her

pr oduct / ser vi ce.

Mar ket i ng Depar t ment s need t o underst and what Generat i on X

i s l ooki ng f or i n a bank. Ci sco I BSG pr epar ed a st udy wi t h t he

f ol l owi ng r ecommendat i on t o bet t er penet r at e Generat i on X and Y.

These r ecommendat i ons i ncl ude:

• A mobi l e- enabl ed onl i ne PFM( Per sonal Fi nanci al Manager )

of f er i ng t hat emphasi zes a hol i st i c vi ew of cust omer s’

f i nanci al si t uat i ons and behavi or s

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 14/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 14

• A vi deo- cent r i c advi sor y model t o al l ow consumer s t o

i nt er act wi t h r emot e f i nanci al advi sor s vi a vi deo ki osks i n

t he br anch as wel l as f r om t he home

• A bank- moderat ed communi t y of i nterest and soci al

networki ng venue t o pr ovi de vi r t ual i zed advi ce on demand

The r esearch and r ecommendat i ons show t he i mpor t ance of

ut i l i zi ng t echnol ogy t o at t r act and obt ai n new cl i ent s. Chase

Bank i nt r oduced a mobi l e check deposi t as par t of t he smar t

phone app i n 2009. Robi n Si del wr i t es i n t he Wal l St r eet

J ournal , “The t r end i s t aki ng hol d wi t h younger consumer s who

i ncreasi ngl y rel y on smar t phones f or ever yday tasks. I t i s l ess

cl ear , however , whet her ol der bank cust omers—many of whom t ook a

whi l e t o embr ace onl i ne banki ng and who are among t he i ndust r y' s

most pr of i t abl e cust omer s—are wi l l i ng t o make another swi t ch.

The ef f or t s come as banks of al l si zes l ook f or new ways t o

at t r act cust omer s dur i ng a per i od of l ow i nt er est r at es, t epi d

l oan demand and t i ght prof i t margi ns. ” Lever agi ng t echnol ogy

l eads t o meet i ng cust omer demands, expandi ng pr of i t s, and

at t r act i ng new cust omer s.

I t shoul d be t he goal of ever y busi ness t o gr ow. Thi s i s

t r ue f or manuf actur i ng, r et ai l , hospi t al i t y, and j ust as

i mpor t ant f or banks and f i nanci al i nst i t ut i ons. I n or der f or

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 15/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 15

banks t o gr ow a gr eat er mar ket shar e wi t h i t s cl i ent s, i t needs

t o st ep back and bet t er under st and t hei r needs. Thi s paper has

demonst r ated t he i mport ance of banks t o target speci f i c market s

( Gener at i on X) i n or der t o t ur n a onet i me cl i ent i nt o a l i f el ong

cl i ent . Thi s wi l l r esul t i n banks gai ni ng a gr eat er mar ket

shar e r esul t i ng i n i ncreased pr of i t s. Addi t i onal l y, gai ni ng and

r et ai ni ng a new cl i ent i s possi bl e wi t h f ewer per sonnel t hr ough

t he l ever age of pr ovi di ng t echnol ogy whi ch al l ows cl i ent s t o

manage t hei r por t f ol i o wi t hout ent er i ng a r et ai l l ocat i on.

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 16/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 16

Ref erences

Beacon Asset Manager s. ( 2009, Oct ober 22) . The f ut ur e of u. s.

consumer spendi ng: I t ' s a gener at i onal t hi ng Seeki ngAl pha,

Cl ear i ng and f i nanci ng: Bank of amer i ca and mer r i l l l ynch.

( 2013, May 21) . Ret r i eved f r om

ht t p: / / cor p. bankof amer i ca. com/ busi ness/ ci / cl ear i ng- and-

f i nanci ng

Domi ngo, R. ( 2003) . From r eact i ve t o r esponsi ve, pr oact i ve

banki ng. I n Banki ng Servi ce Management Ret r i eved f r om

ht t p: / / www. r t donl i ne. com/ BMA/ BSM/ 9. ht ml

Edwar ds, F. R. , & Mi shki n, F. S. ( 1995) . The decl i ne of

t r adi t i onal banki ng: I mpl i cat i ons f or f i nanci al stabi l i t y

and regul at or y pol i cy. FRBNY ECONOMI C POLI CY REVI EW,

Ret r i eved f r om

ht t p: / / www2. econ. i ast ate. edu/ cl asses/ econ353/ ganco/ document

s/ Decl i neof Tr adi t i onal Banki ng. pdf

Far ah, P. , Macaul ay, J . , & Er i csson, J . ( n. d. ) . Ret r i eved f r om

ht t p: / / www. ci sco. com/ web/ about / ac79/ docs/ f s/ nextgr owt hoppor

t uni t yf or banks. pdf

7/27/2019 Bank Marketing Paper

http://slidepdf.com/reader/full/bank-marketing-paper 17/17

Bank & Fi nanci al I nst i t ut i on Mar ket i ng 17

Feder al r eser ve boar d: Dat a r el eases. ( n. d. ) . Ret r i eved f r om

ht t p: / / www. f eder al r eser ve. gov/ econr esdat a/ st at i st i csdat a. ht

m

I nvest opedi a. Ret r i eved f r om ht t p: / / www. i nvest opedi a. com/

Mul l er , D. ( 2013, J anuar y 31) . Hunt i ngt on bank cel ebr at es

i naugur al ' best i n busi ness' cl ass i n met r o det r oi t . Ml i ve

Si del , R. ( 2013) . Banks make smart phone connect i on. Wal l St r eet

J ournal , C1.

The t op 20 ad sl ogans of al l t i me. ( 2011, November 22) .

Ret r i eved f r om ht t p: / / www. spaci ouspl anet . com/ wor l d/ new/ t op-

20- ad- sl ogans- of - al l - t i me