banking regulations - citibank regulations ... (snap) 2013 . greece ... do not consider short term...

TRANSCRIPT

The Financial Professionals Forum 2012

Banking Regulations

Ruth Wandhofer, Global Head of Regulatory & Market Strategy, Citi

Implications for Corporate Clients

The Financial Professionals Forum 2012

Table of Contents

1. Global Regulatory Environment 4

2. Basel III 9

3. OTC Derivatives Legislation 16

4. SEPA in Europe 21

5. Considerations for Corporate Treasurers 25

1. Global Regulatory Environment

The Financial Professionals Forum 2012

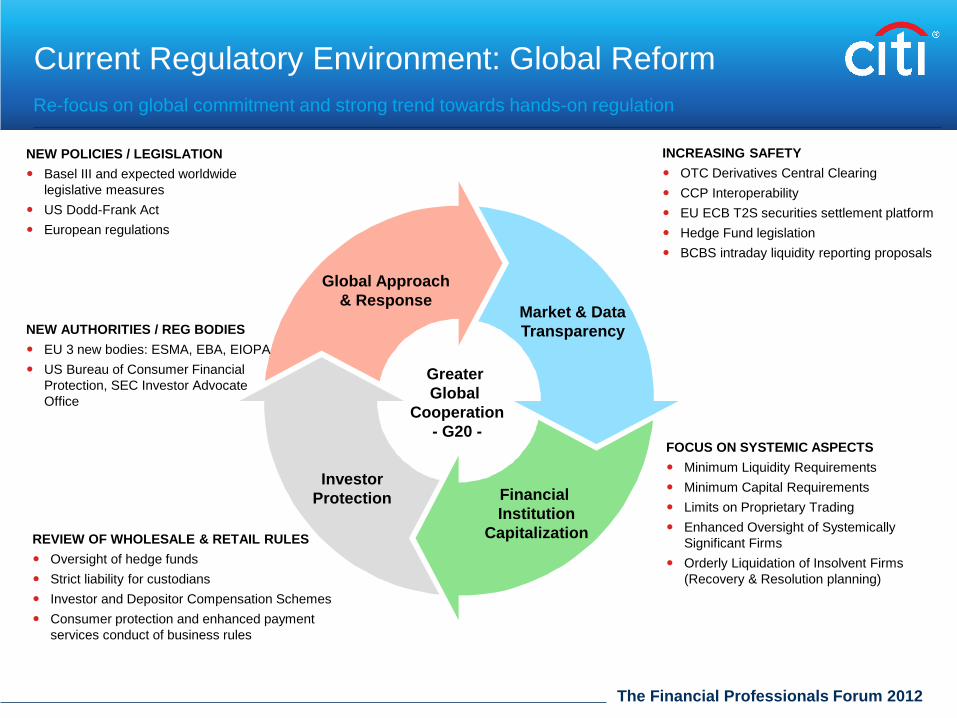

Current Regulatory Environment: Global Reform Re-focus on global commitment and strong trend towards hands-on regulation

Market & Data Transparency

Financial Institution

Capitalization

Investor Protection

Global Approach & Response

NEW POLICIES / LEGISLATION Basel III and expected worldwide

legislative measures US Dodd-Frank Act European regulations

NEW AUTHORITIES / REG BODIES EU 3 new bodies: ESMA, EBA, EIOPA US Bureau of Consumer Financial

Protection, SEC Investor Advocate Office

INCREASING SAFETY OTC Derivatives Central Clearing CCP Interoperability EU ECB T2S securities settlement platform Hedge Fund legislation BCBS intraday liquidity reporting proposals

REVIEW OF WHOLESALE & RETAIL RULES Oversight of hedge funds Strict liability for custodians Investor and Depositor Compensation Schemes Consumer protection and enhanced payment

services conduct of business rules

FOCUS ON SYSTEMIC ASPECTS Minimum Liquidity Requirements Minimum Capital Requirements Limits on Proprietary Trading Enhanced Oversight of Systemically

Significant Firms Orderly Liquidation of Insolvent Firms

(Recovery & Resolution planning)

Greater Global

Cooperation - G20 -

The Financial Professionals Forum 2012

Elections timeline 2012

Finland

Russia

France

Czech Rep.

Slovenia

Lithuania

USA

Romania Portugal (tbc)

Malta (Mar)

Cyprus (Feb)

Germany (Sep)

Italy (Apr)

Mexico

India

China (Autumn)

South Korea

Greece

Iceland

Ireland (referendum)

Czech Rep. (tbc)

Bulgaria (tbc)

Netherlands (snap)

2013

Greece

Turkey

jan feb mar apr may jun jul aug sep oct nov dec

The Financial Professionals Forum 2012

Hot Topics on Treasurers’ Agendas Today Increased uncertainty and a wide range of possible economic, financial, and business outcomes are shaping Treasurers’ agendas

Managing the fallout from ongoing market crisis – Driving initiatives on bank counterparty risks, supply chain risks, commercial policy, and cash

management structures

Reassessing balance sheet structures – While high cash levels are a drag on b/s ratios, market events are highlighting need for strategic

approach to defining liquidity risks

Refining Emerging Market strategies – “EM dependence” is rising…Citi now expects fully 30% of 2012 global GDP growth to be generated

solely by China

Extending treasury role in working capital management – Continuing to work with businesses on procurement and customer terms, ROIC targets for initiatives,

sponsoring supply chain financing tools

Talent management for attracting and retaining people – A key imperative – and a challenge – to manage the business shift to EMs

The Financial Professionals Forum 2012

While Regulation Is Keeping Banks Busy… The financial services industry is busy implementing a host of new regulations

A few examples… – Basel III (Global) – Dodd-Frank (US) – FATCA (US) – Repeal of Regulation Q (US) – Financial Transaction Tax (EU) – MiFiD II (EU) – Solvency II (EU) – Securities Law Directive (EU) – Single Euro Payments Area

(EU)

– Independent Commission on Banking (UK)

– FSA liquidity regulation (UK) – CBRC new

capital adequacy ratios (China) – APRA accelerated Basel III

timeline (Australia) – And more

2. Basel III

The Financial Professionals Forum 2012

Basel III introduces radical changes in capital rules and a one-size fits all set of liquidity ratios.

The Move to Basel III

4

Basel I: 1988 Basel II: 2005 Basel III: 2010

Established minimum Total Capital ratio

Simplistic credit-risk model focused on solvency risk

Prescribed risk-weights applied to counterparty categories

Standardized or VAR model for market risk added in 1996

Retained minimum capital requirement, but…

Enhanced sensitivity of credit risk measurement

Expanded scope of risks, including operational risk

Still primarily focused on solvency risk

Live in EU (2008) and many countries, exc. U.S. (thus far)

Significantly increases quality and quantity of capital

Adds new measures for liquidity and leverage

Differentiates global systemically important banks

Still a work in progress

To be phased-in over six years, starting 2013

Key Precepts

Important to keep in mind that Basel is a global initiative, with recommendations ratified by the G20 and affecting banks worldwide

The Financial Professionals Forum 2012

Basel III: in a nutshell

Liquidity coverage ratio – Banks have to examine likely net cash outflow over a 30-day period, and hold highly-liquid assets to

sell to meet such outflow – Some facilities and deposits are assumed to be more likely to be drawn/withdrawn

Net stable funding ratio – Same idea but this looks at stickiness of deposits – amount of stable funding must exceed amount

needed – Amount needed calculated by reference to assets and off-balance-sheet items

Leverage ratio – Crude comparison of capital and assets (no risk weighting here)

CCP clearing – G20 agenda – Requirement for collateral or capital – Banks’ exposures to CCPs cease to be zero-weighted

And – Inter-bank risk weights increase – Lending is more expensive than holding debt securities – Additional capital buffers e.g. “counter-cyclical”

5 areas of key changes proposed

The Financial Professionals Forum 2012

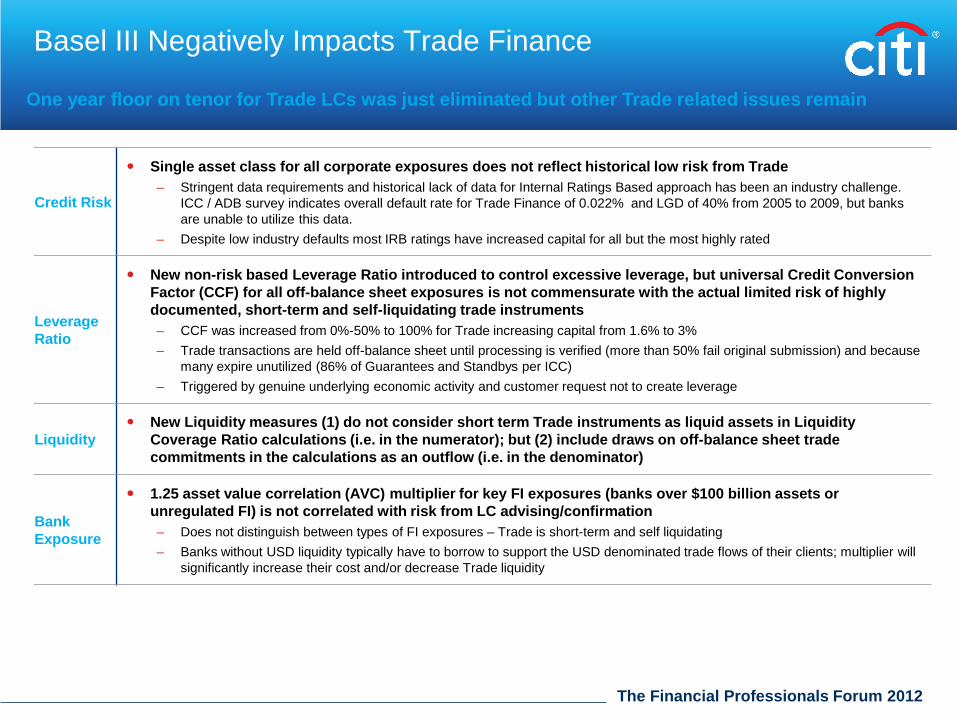

Basel III Negatively Impacts Trade Finance

Credit Risk

Single asset class for all corporate exposures does not reflect historical low risk from Trade – Stringent data requirements and historical lack of data for Internal Ratings Based approach has been an industry challenge.

ICC / ADB survey indicates overall default rate for Trade Finance of 0.022% and LGD of 40% from 2005 to 2009, but banks are unable to utilize this data.

– Despite low industry defaults most IRB ratings have increased capital for all but the most highly rated

Leverage Ratio

New non-risk based Leverage Ratio introduced to control excessive leverage, but universal Credit Conversion Factor (CCF) for all off-balance sheet exposures is not commensurate with the actual limited risk of highly documented, short-term and self-liquidating trade instruments – CCF was increased from 0%-50% to 100% for Trade increasing capital from 1.6% to 3% – Trade transactions are held off-balance sheet until processing is verified (more than 50% fail original submission) and because

many expire unutilized (86% of Guarantees and Standbys per ICC) – Triggered by genuine underlying economic activity and customer request not to create leverage

Liquidity New Liquidity measures (1) do not consider short term Trade instruments as liquid assets in Liquidity

Coverage Ratio calculations (i.e. in the numerator); but (2) include draws on off-balance sheet trade commitments in the calculations as an outflow (i.e. in the denominator)

Bank Exposure

1.25 asset value correlation (AVC) multiplier for key FI exposures (banks over $100 billion assets or unregulated FI) is not correlated with risk from LC advising/confirmation – Does not distinguish between types of FI exposures – Trade is short-term and self liquidating – Banks without USD liquidity typically have to borrow to support the USD denominated trade flows of their clients; multiplier will

significantly increase their cost and/or decrease Trade liquidity

One year floor on tenor for Trade LCs was just eliminated but other Trade related issues remain

The Financial Professionals Forum 2012

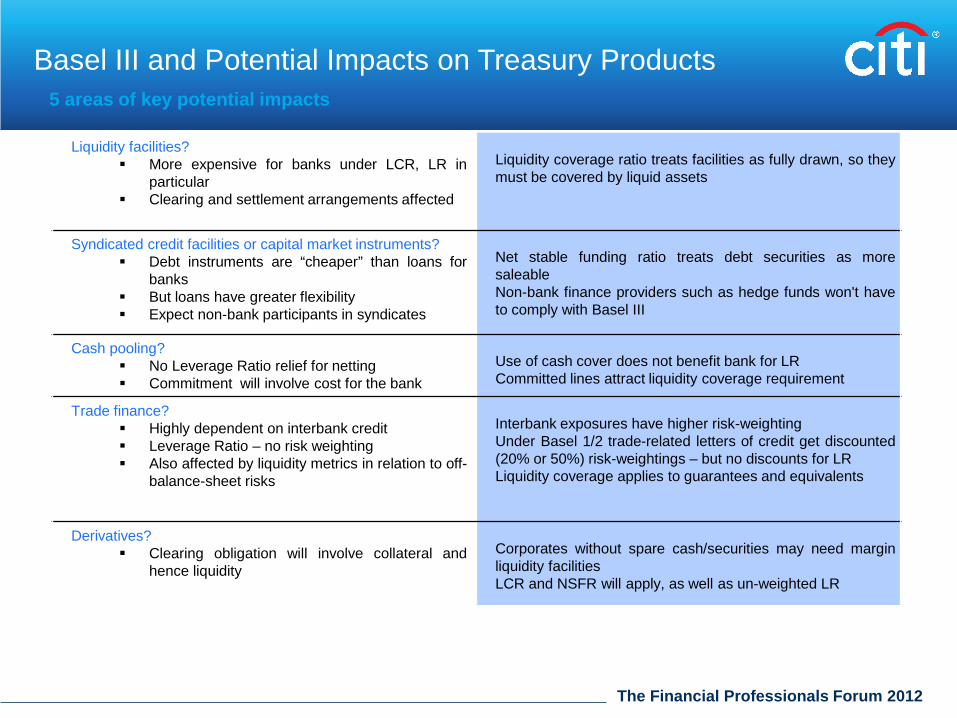

Basel III and Potential Impacts on Treasury Products 5 areas of key potential impacts

Liquidity facilities? More expensive for banks under LCR, LR in

particular Clearing and settlement arrangements affected

Liquidity coverage ratio treats facilities as fully drawn, so they must be covered by liquid assets

Syndicated credit facilities or capital market instruments? Debt instruments are “cheaper” than loans for

banks But loans have greater flexibility Expect non-bank participants in syndicates

Net stable funding ratio treats debt securities as more saleable Non-bank finance providers such as hedge funds won't have to comply with Basel III

Cash pooling? No Leverage Ratio relief for netting Commitment will involve cost for the bank

Use of cash cover does not benefit bank for LR Committed lines attract liquidity coverage requirement

Trade finance? Highly dependent on interbank credit Leverage Ratio – no risk weighting Also affected by liquidity metrics in relation to off-

balance-sheet risks

Interbank exposures have higher risk-weighting Under Basel 1/2 trade-related letters of credit get discounted (20% or 50%) risk-weightings – but no discounts for LR Liquidity coverage applies to guarantees and equivalents

Derivatives? Clearing obligation will involve collateral and

hence liquidity

Corporates without spare cash/securities may need margin liquidity facilities LCR and NSFR will apply, as well as un-weighted LR

The Financial Professionals Forum 2012

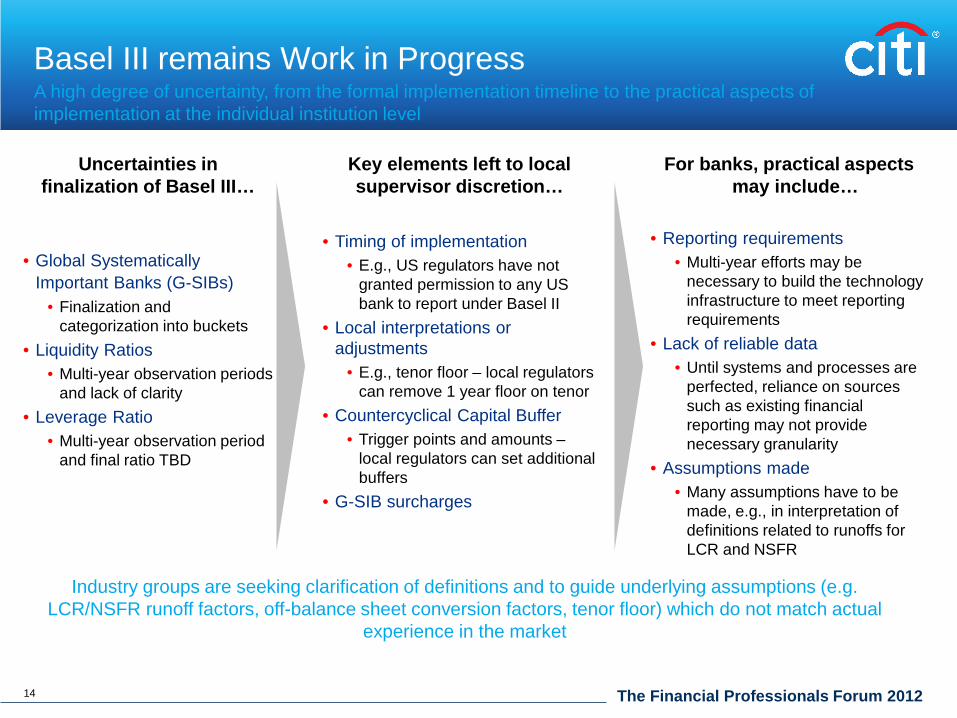

Basel III remains Work in Progress A high degree of uncertainty, from the formal implementation timeline to the practical aspects of implementation at the individual institution level

Uncertainties in finalization of Basel III…

• Global Systematically Important Banks (G-SIBs)

• Finalization and categorization into buckets

• Liquidity Ratios • Multi-year observation periods

and lack of clarity • Leverage Ratio

• Multi-year observation period and final ratio TBD

Key elements left to local supervisor discretion…

• Timing of implementation

• E.g., US regulators have not granted permission to any US bank to report under Basel II

• Local interpretations or adjustments

• E.g., tenor floor – local regulators can remove 1 year floor on tenor

• Countercyclical Capital Buffer • Trigger points and amounts –

local regulators can set additional buffers

• G-SIB surcharges

For banks, practical aspects may include…

• Reporting requirements

• Multi-year efforts may be necessary to build the technology infrastructure to meet reporting requirements

• Lack of reliable data • Until systems and processes are

perfected, reliance on sources such as existing financial reporting may not provide necessary granularity

• Assumptions made • Many assumptions have to be

made, e.g., in interpretation of definitions related to runoffs for LCR and NSFR

Industry groups are seeking clarification of definitions and to guide underlying assumptions (e.g. LCR/NSFR runoff factors, off-balance sheet conversion factors, tenor floor) which do not match actual

experience in the market

14

The Financial Professionals Forum 2012

Summary of Potential Impacts of Basel III on Corporates

The leverage ratio adds additional capital to high quality lending over the Basel II charge. This will effect good quality mortgage business and lending to high quality corporates, encouraging securitisation of mortgages and corporates to use public markets.

The LCR and NSFR regime treat corporate balances less favourably, which could result in lower remuneration on the deposit side as well as less willingness of certain banks to lend.

Overall the NSFR is considered to have a potentially significant impact on economic growth.

In relation to trade, the Loan Loss Reserves introduced already by Basel II continue to impact the cost of letters of credit (LCs) in particular where the seller has a low rating, leading to higher confirmation costs for LCs.

Tangible change is to be expected in the context of OTC derivatives trading due to the clearing requirement as well as the extra capital requirements for uncleared transactions.

Additionally, there is a second order cost effect stemming from the formal reporting requirement on trade repositories imposed by the new regulations; depending on the outcome this could also apply to intra-group transactions under the European legislation.

3. OTC Derivatives Legislation

The Financial Professionals Forum 2012

OTC Derivatives Clearing: Where Is the Regulatory Pressure Coming From?

Short answer: the Lehman Default Problem with bilateral framework: – As shown in Lehman case, counterparties to swaps were unable to access or even recover collateral posted /

exiting trade positions needed to be replaced in dislocated trading conditions – Buy-side collateral management was done on spread sheets prepared by part-timers with limited derivatives

knowledge…

And…the market is systemically large! BIS estimate: notional amount of OTC derivatives outstanding in June 2010 was $583 trillion

Hence…In September 2009 the G-20 leaders agreed that:

“All standardised OTC derivative contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties by end 2012 at the latest. OTC derivative contracts should be reported to trade repositories. Non centrally cleared contracts should be subject to higher capital requirements”

• A Regulation proposal on OTC derivatives, central counterparties and trade repositories (‘EMIR’) was published by the EU Commission on 15th September 2010 & US Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 Act also covers this area

Both (European and US) regulatory approaches set out new rules in relation to mandatory central counterparty (CCP) clearing and risk mitigation in respect of certain standardised OTC derivative contracts

The Financial Professionals Forum 2012

Requirements for non-financial entities

• Every OTC Derivatives trade, whether cleared or not, has to be reported to a trade repository.

• Non-financial entities are out of scope of the clearing requirement under the US legislation. In Europe they are also out of scope if their OTC Derivative activities fall under the threshold that ESMA will define (use of OTC Derivatives for the pure purpose of risk hedging exempted).

• A trade off between collateralization and capital charge has to be made.

• In July 2012 the BCBS and IOSCO issued a consultation paper that seeks to establish global minimum standards for margin requirements for non-centrally-cleared derivatives. The proposal is expected to create significant liquidity demands and substantially increase trading cost: 1) each derivative counterparty will have to post to the other the full amount of initial margin on a gross basis and 2) initial margin must be segregated and must not be re-hypothecated or re-used.

• A quantitative impact study is being conducted in parallel to the consultation and will hopefully provide further clarity.

The European OTC Derivative rules will also impact the corporate space.

The Financial Professionals Forum 2012

Collateral Management Considerations for Corporates

Challenges

Liquidity: Need to have sufficient eligible assets on hand to meet daily margin calls

Operational: Margin movements follow strict processes (e.g. ISDA CSA) and rely on daily valuation of open OTC positions

Documentation: Negotiation of necessary collateral agreements can be complex and time consuming

Benefits

Reduces Counterparty Risk: Exposure to counterparty insolvency is offset by collateral held

Frees up Credit Lines: Enabling other transactions

Broadens Scope of OTC Trade Types and Counterparties: Some trade types typically require collateralisation; lower-rated counterparties become acceptable

Supports Access to OTC Clearing: Collateral is a core requirement for use of OTC clearing

Reduces Cost of Trading: Regulatory capital and CVA charges from brokers can be reduced resulting in improved prices on trades

Liquidity and operational concerns deter most corporates from collateralizing their OTC derivatives. However the arrival of OTC legislation and Basel III will tip the scales in favor of CSAs for many entities.

The Financial Professionals Forum 2012

Checklist for Implementing Collateral Management

Establishing collateral management capabilities imposes significant additional burdens on corporate treasurers. However daily operational tasks are easily outsourced to a services provider.

Operations can be outsourced to service provider

CSA parameters administration

Daily collateral valuation, eligibility testing

Daily OTC valuation (mark-to-market)

OTC reconciliation

Margin call calculation and issuance to counterparties

Margin call agreement with counterparties and dispute management

Selection of assets and instruction of settlement

Proactive collateral substitution

Generation of daily reports an transaction data feeds

Obligations for Corporate Treasury Confirm exemption from EMIR for

parent and all subsidiaries and affiliates

Negotiate CSA agreements and/or OTC clearing agreements

Manage liquidity for collateral purposes

Maintain general ledger / record keeping

Operational aspects of daily CSA management

o Necessary systems and expertise available?

o How to forecast capacity requirements?

4. SEPA in Europe

The Financial Professionals Forum 2012

SEPA in Europe: The original scope and objective

European Union (10 non-Euro) European Economic Area (3)

Switzerland and Monaco

European Union (17 Euro)

The Single Euro Payments Area currently spans 32 countries: – 27 EU Member States – 3 additional EEA Member States – Switzerland and Monaco

SEPA governs Euro payments only – Payments in other currencies are not impacted

SEPA is for payments within this geographical area – Payments to/from Europe are not impacted

SEPA will impact domestic + cross-border Euro credit transfers and direct debits

– No distinction between ‘national’ and ‘cross-border’ Euro payments within the 32 countries

Standardised Schemes for CT and DD – Mandatory use of BIC and IBAN – Single legal framework: Payment Services Directive

SEPA addresses non-urgent / retail / ACH payments – Urgent / same-day Euro Wire Transfers are already

integrated across the Single Market

SEPA is trying to complete the Single Market for Euro Payments in Europe

The Financial Professionals Forum 2012

Long-sought certainty for market participants – current migration for SEPA Credit Transfers at 22%, SEPA Direct Debits at 0.45%

Single end date for both SEPA CT and SEPA DD in Euro Member States

For non-Euro Member States the corresponding end date is 31 October 2016

Most countries Euro Member States expected to work towards Feb 2014 timeline. – Some might choose to migrate earlier; none have announced such decision currently

By end date indicates SEPA CT and DD will have to be executed in accordance with a set of prescribed “technical requirements” to be SEPA Compliant

1st February 2014

SEPA Regulatory Update : Implications of End Date Legislation

1 Feb 2014

1. Migration end-date for SEPA CT and SEPA DD in Euro Member States

2. End-date for grandfathering existing DD mandates to SEPA DD Core 3. Use of ISO 20022 XML standard when initiating and receiving SEPA

transactions; Member States have the option to defer to 1 Feb 2016. 4. Interoperability requirement for payment schemes in Euro Member

States 5. Elimination of the obligation for users to provide the BIC for national

payments, where necessary – Note: Member States have the option to defer application to 1 Feb 2016

1 Feb 2016

1. Elimination of the obligation for users to provide the BIC for cross-border payments

2. Expire of transitional arrangements for so called “niche products”

3. Expiry of transitional arrangements for one-off direct debits used at merchants (e.g. Germany’s ELV)

4. Expiry of Member State option to allow banks to provide conversion services from BBAN to IBAN.

5. Removal of settlement-based national reporting for balance of payment statistics (such as Central Bank Reporting)

31 Oct 2016

1. Migration end-date for SEPA CT and SEPA DD in non-Euro Member States 2. Reachability for SEPA CT and SEPA DD in non-Euro Member States 3. Interoperability requirement for payment schemes in non-Euro Member

States

1 Feb 2017

1. Prohibition of per-transaction Multilateral Interchange Fees for national DDs

1 Nov 2012

1. Prohibition of per-transaction Multilateral Interchange Fees for cross-border DD

Citi played a leading role in the EU-level negotiations and development of industry guidance as chair of European Bank Federation’s (EBF’s) Payment Regulatory Expert Group (PREG)

Immediately

1. Reachability for SEPA credit transfers and SEPA DD in Euro Member States

The Financial Professionals Forum 2012

Given the many ambiguous points in the Regulation the European Banking Federation (EBF) Payments Regulatory Expert Group, chaired by Citi, has drafted industry guidance, which can be found under the following link on the website of the European Payments Council: www.europeanpaymentscouncil.eu/knowledge_bank_detail.cfm?documents_id=580

Key clarifications include:

Bank readiness of ISO 2002 XML payment processing capability – conversion is not permitted after 2014

The big BIC issue: in a very late addition to the text the EU institutions politically felt that customers should not be required to provide the BIC for national transactions from 2014 and for cross-border transactions from 2016. BIC is a key necessity in terms of payment routing. At global level, BICs will remain a requirement. Corporates should continue focusing on both IBAN and BIC – liability of bank for payment executed via IBAN only is limited / not covered by this Regulation.

Customers using files for payments should initiate/receive in ISO 20022 XML – slight ambiguity in terms of what this really means. It was clarified with the Commission that banks can provide relevant conversion/mapping solutions to client to facilitate connectivity to SEPA (see SEPA guidance).

The potential prolonged co-existence of ‘niche schemes’ (only needing to be announced by Feb 2013) will mean that local clearing systems will continue operating with legacy standards in this space – complexity/cost.

The lifting of the EUR 50,000 limit with regard to pricing parity under Regulation 924/2009 will apply from date of entry into force of this Regulation (31 March 2012). Positive for users.

In terms of banks and customers located outside of SEPA, we clarified with the Commission that these can still benefit from SEPA payments if appropriate solutions are being used via SEPA compliant banks.

Key Challenges with the SEPA Regulation European industry guidance and collaboration will support clarifications

5. Considerations for Corporate Treasurers

The Financial Professionals Forum 2012

Evaluate options to free trapped cash

Tap into local knowledge and expertise in growth markets

Integrate treasury processes

Leverage technology to drive efficiency and de-risk processes

Develop firm-wide view of exposures

Implement policies and governance framework to monitor compliance

De-risk supply chain

Centralize decision-making

Plan ahead

Adjusting to Greater Global Complexity The role of the Treasurer has been re-defined as a strategic partner and “gatekeeper” of the balance sheet

Acting as gatekeeper of the balance sheet

Addressing treasury and funding implications of internal processes, policies and capital actions

Identifying appropriate level of liquidity to support operations vs. strategic cash available for investment and expansion

Extracting value from working capital / supply chain financing options to create in-house liquidity

Rationalize account structures, processes and technology

Centralize treasury operations and services, extend best practices

Release cash from working capital cycle

Improve cash forecasting

High proportion of expansion into EM countries and currencies; increasing importance of managing currency risk

Restrictive regulatory and operational environments

Proliferation of systems and data formats; insufficient global visibility into positions

Aggregating critical information for real-time decision support

15

Strategic Focus – Optimizing Capital Allocation & Funding Structure

Key Challenges – Increasing Complexity

Maximize Cash Efficiency Improve Risk Management Manage Growth

efficiency, renewable energy & mitigation

In January 2007, Citi released a Climate Change Position Statement, the first US financial institution to do so. As a sustainability leader in the financial sector, Citi has taken concrete steps to address this important issue of climate change by: (a) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of alternative energy, clean technology, and other carbon-emission reduction activities; (b) committing to reduce GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (c) purchasing more than 52,000 MWh of green (carbon neutral) power for our operations in 2006; (d) creating Sustainable Development Investments (SDI) that makes private equity investments in renewable energy and clean technologies; (e) providing lending and investing services to clients for renewable energy development and projects; (f) producing equity research related to climate issues that helps to inform investors on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the issue of climate change to help advance understanding and solutions.

Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

[TRADEMARK SIGNOFF: add the appropriate signoff for the relevant legal vehicle]

© 2012 Citibank, N.A. All rights reserved. Citi and Arc Design is a registered service mark of Citigroup Inc..

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby ("Transaction"). Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor.Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the information contained herein and the existence of and proposed terms for any Transaction.Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b) there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that from the commencement of discussions with respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction. We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also request corporate formation documents, or other forms of identification, to verify information provided.Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without any notice. We and/or our affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time.Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications between its investment banking and research personnel to specifically prescribed circumstances.