base metals and bulk commodities marking prices to market ...€¦ · base metals stocks are cheap,...

TRANSCRIPT

Please see Disclosures and Disclaimers at the end of this report. A division of Dundee Securities Ltd.

Dundee Capital Markets is a registered trademark of Dundee Corporation, used under license.

Base Metals and Bulk Commodities

January 8, 2015

David Charles, CFA / (514) 396-0320 [email protected]

Patrick Racicot, CFA / (514) 395-0296 [email protected]

Joseph Gallucci, MBA / (514) 396-0330 [email protected]

Sean Bracken / (514) 396-0325 [email protected]

Marking Prices to Market Again as Sector faces New Reality of Deflation and Commodity Volatility, Patience to be tested

We are updating our commodity price forecast by marking-to-market our short-term and medium term prices. The most meaningful changes were for copper, nickel and molybdenum in 2015/16 and thermal/HCC coal throughout the whole forecast period and long term. DCM's commodity preferences are Zn>Ni>Cu>coal (bulks). The new reality driving the adjustment to our forecast prices is the on-going strength of the US$, the slowdown in the global economy (deficient demand), and lack of supply discipline. The lessons learned from oil's price collapse, is that there needs to be a significant reduction in supply before prices can rebound. Copper prices may suffer a similar examination in 2015. Given the recent flow of funds, we do not expect Base Metal stocks to outperform until the US dollar peaks (first US rate hike?). So investor patience will be tested. We expect strong trading rallies in 2015 as Risk/Reward attractive, especially if the US$ corrects.

New DCM Base Metals and Bulk Commodity Price Forecast

Annual Quarterly

Sources: Dundee Capital Markets

We present the new target prices for our DCM base metals universe. Our new target prices for producers are based on anticipated 2015 EV/EBITDA multiples roughly ranging from 6x to 9x, levels last seen in 2008/2001. The total impact on our EBITDA, EPS, CFPS and NAV estimates for our coverage universe are shown on page 2 and 3. Our preferred equities (risk/reward) include:

Lundin Mining (Top Pick) Trevali Mining (Top Pick) Nevsun Resources (Top Pick)

Rating changes: Removed CS as Top Pick, changed NSU to Top Pick; downgraded TCM, IVN to Neutral from Buy.

2015 2016

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2.90 2.90 2.95 3.05 3.05 3.05 3.00 3.10(6.5%) (7.9%) (7.8%) (4.7%) (12.9%) (12.9%) (14.3%) (11.4%)

1.05 1.10 1.07 1.15 1.15 1.15 1.10 1.20(4.5%) (8.3%) (7.0%) (4.2%) 9.5% 9.5% 4.8% 14.3%

0.92 0.97 0.96 1.02 1.04 1.06 1.06 1.08(12.4%) (7.6%) (8.6%) (2.9%) (1.0%) 1.0% 1.0% 2.9%

8.10 8.80 8.40 9.70 9.75 9.75 9.25 9.25(4.7%) (5.4%) (9.7%) (0.5%) (2.5%) (2.5%) (7.5%) (7.5%)

14.50 14.75 14.50 15.25 15.00 15.00 15.00 15.00(1.4%) (1.7%) (4.6%) (1.6%) 3.4% 3.4% 3.4% 3.4%

9.50 10.00 10.00 10.50 11.50 11.50 11.50 11.50(20.8%) (16.7%) (16.7%) (12.5%) (4.2%) (4.2%) (4.2%) (4.2%)

120 120 130 140 150 150 150 150- - - - - - - -

65 70 75 79 80 75 70 75(13.3%) (12.5%) (11.8%) (12.2%)

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 2

End of an Era- Ratio of TSX Metals & Mining Sub Index OVER the S&P/TSX back to Pre-"Super Cycle" Levels!

Sources: FactSet, Dundee Capital Markets

Base Metals Stocks are cheap, multiples in-line with bottom of cycle seen last year (relative to TSX)

Sources: FactSet Consensus, Dundee Capital Markets

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

Ja

n-1

3

Ja

n-1

4

Ratio of "TSX Mining Index" over S&P/TSX(last 10 years)

TSX Capped Dvr Mtl&Mng / S&P/TSX

Linear (TSX Capped Dvr Mtl&Mng / S&P/TSX)

10 yeartrend line

Valuation Metrics: Now vs BottomCurrent (Jan 2015) Sector Bottom (July 2013)

EV/EBTIDA

(NTM)

P/E

(NTM)P/NAV

EV/EBTIDA

(NTM)

P/E

(NTM)P/NAV

TSE Metals & Mining 5.7x 11.4x 0.57x 5.8x 11.1x 0.67x

S&P/TSX 9.1x 15.2x n/a 8.1x 14.8x n/a

Discount 63% 75% n/a 72% 75% n/a

The ratio of the TSX M+M vs. the S&P/TSX is still well below its 10-year trend line and has broken below GFC (2008/9) levels.

But the ratio could be set to decline further as the Base Metals "Super Cycle" appears to be at an end.

With a 12% downside risk to post-GFC lows, but >30% upside potential, we believe risk/reward is attractive.

In an environment where the outlook for the global economy and base metal prices is weak, valuations are key. Current Valuation is cheap and below the bottom established in July 2013. Multiples could expand if the outlook does not improve in 2015 (commodities weaken further). Weak domestic currencies/energy will help.

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 3

Changes to DCM Earnings and Cashflow Estimates Post-Commodity Price Update (alphabetical order)

Source: Dundee Capital Markets

(7%) (11%) (12%) (14%)(19%) (20%) (21%) (22%) (22%)

(30%)(34%) (36%)(45%)

(35%)

(25%)

(15%)

(5%)

5%

TCK

.B

NSU

-T

TCM

-T

CU

M-T

ATY

-T

LUN

-T

CS-

T

HB

M-T

TKO

-T

TV-T

FM-T

IVW

-T

LGO

-T

Changes in 2015 EBITDA (%)

Sources: Dundee Capital MarketsEBITDA ($M) EPS CFPS NAV

2015 %∆ 2016 %∆ 2015 %∆ 2016 %∆ 2015 %∆ 2016 %∆ ($/sh) %∆

Major Producers

Firs t Quantum FM-T $1,728 (34%) $2,430 (39%) $0.92 (38%) $1.58 (39%) $2.69 (21%) $4.49 (23%) $22.98 (9%)

Teck Resources TCK.B $2,713 (7%) $2,964 15% $0.97 (18%) $1.24 42% $2.96 (7%) $3.19 13% $29.04 (18%)

Producers

Atico Mining ATY-T $14 (19%) $15 (23%) $0.04 (39%) $0.03 (47%) $0.10 (20%) $0.10 (24%) $0.72 (8%)

Capstone Mining CS-T $235 (21%) $274 (27%) $0.20 (45%) $0.35 (35%) $0.40 (27%) $0.51 (26%) $3.75 (22%)

Copper Mountain CUM-T $90 (14%) $113 (21%) $0.26 (18%) $0.30 (41%) $0.80 (15%) $0.95 (24%) $1.79 (14%)

Hudbay Minera ls HBM-T $369 (22%) $805 (28%) $0.53 (43%) $1.67 (48%) $1.52 (21%) $3.19 (33%) $13.28 (7%)

Ivernia Inc. IVW-T $46 (36%) $56 (13%) $0.02 (53%) $0.05 (18%) $0.03 (46%) $0.06 (17%) $0.41 13%

Largo Resources LGO-T $35 (53%) $75 (23%) ($0.10) (160%) $0.20 (40%) $0.07 (78%) $0.36 (25%) $2.88 (8%)

Lundin Mining LUN-T $876 (20%) $887 (18%) $0.48 (36%) $0.41 (34%) $1.11 (20%) $1.07 (17%) $6.61 (13%)

Nevsun Resources NSU-T $207 (11%) $98 (15%) $0.25 (10%) $0.13 (13%) $0.63 (10%) $0.33 (14%) $4.10 (11%)

Taseko Mines TKO-T $70 (22%) $99 (45%) $0.06 (52%) $0.16 (57%) $0.25 (20%) $0.35 (38%) $2.78 (21%)

Thompson Creek TCM-T $195 (12%) $236 (18%) ($0.04) (249%) $0.02 ($0.92) $0.54 (19%) $0.72 (25%) $3.33 (15%)

Treval i Mining TV-T $67 (30%) $107 (15%) $0.08 (46%) $0.16 (23%) $0.19 (31%) $0.28 (14%) $1.79 (6.2%)

Name Symbol

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 4

DCM Base Metals and Bulk Commodities Updated Ratings and Recommendations

Source: Dundee Capital Markets

NEW PREVIOUSPrice MCap Implied Price Target 2015 2015 Implied Target

7-Jan-15 (US$M) Return /NAV /NAV EBITDA EPS return /NAV

BASE METALS - Major ProducersFirs t Quantum FM-T C$16.13 $8,416 BUY -- $20.00 ▼ 25% C$22.98 ▼ 0.70x 0.87x US$1,728 $0.92 BUY $25.00 56% $25.15 0.99x DC

Teck Resources TCK.B C$15.56 $9,095 NEUTRAL -- $19.00 ▼ 28% C$29.04 ▼ 0.54x 0.65x $2,713 $0.97 NEUTRAL $24.00 60% $35.50 0.68x DC

Major Producers Average 0.62x 0.76x 0.84x

BASE METALS - ProducersAtico Mining ATY-T C$0.59 $62 BUY -- $0.75 ▼ 27% C$0.72 ▼ 0.81x 1.04x US$14 $0.04 BUY $1.00 69% $0.79 1.27x DC

Capstone Mining CS-T C$2.01 $700 BUY -- $3.25 ▼ 62% C$3.75 ▼ 0.54x 0.87x US$235 $0.20 BUY $4.25 111% $4.84 0.88x JG

Copper Mountain CUM-T C$1.58 $165 NEUTRAL -- $1.90 ▼ 20% C$1.79 ▼ 0.88x 1.06x US$90 $0.26 NEUTRAL $2.80 77% $2.10 1.33x JG

Hudbay Minera ls HBM-T C$9.74 $2,281 BUY -- $11.50 ▼ 18% C$13.28 ▼ 0.73x 0.87x US$369 $0.53 BUY $13.00 34% $14.24 0.91x DC

Ivernia Inc. IVW-T C$0.05 $31 NEUTRAL ▼ $0.20 ▼ 344% C$0.41 ▲ 0.11x 0.48x US$46 $0.02 BUY $0.30 567% $0.36 0.82x JG

Katanga Mining KAT-T C$0.36 $595 NEUTRAL -- $0.40 -- 11% C$0.68 ▼ 0.53x 0.59x US$493 $0.09 NEUTRAL $0.40 11% $0.75 0.53x DC

Largo Resources LGO-T C$1.64 $227 BUY -- $3.00 ▼ 83% C$2.88 ▼ 0.57x 1.04x US$35 ($0.10) BUY $4.50 174% $3.12 1.44x JG

Lundin Mining LUN-T C$5.47 $3,437 BUY -- $7.00 ▼ 28% C$6.61 ▼ 0.83x 1.06x US$876 $0.48 BUY $8.00 46% $7.62 1.05x DC

Nevsun Resources NSU-T C$4.53 $824 BUY -- $6.00 -- 36% C$4.10 ▼ 1.11x 1.47x US$207 $0.25 BUY $6.00 36% $4.59 1.31x JG

Taseko Mines TKO-T C$1.26 $288 NEUTRAL -- $1.50 ▼ 19% C$2.78 ▼ 0.45x 0.54x $70 $0.06 NEUTRAL $2.00 59% $3.53 0.57x JG

Thompson Creek TCM-T C$1.91 $355 NEUTRAL ▼ $2.15 ▼ 13% C$3.33 ▼ 0.57x 0.65x $195 ($0.04) BUY $3.00 57% $3.93 0.76x DC

Treval i Mining TV-T C$1.07 $315 BUY -- $2.00 -- 87% C$1.79 ▼ 0.60x 1.12x $67 $0.08 BUY $2.00 87% $1.91 1.05x JG

Producers Average 0.64x 0.90x 0.99x

BASE METALS - DevelopersCanadian Zinc CZN-T C$0.21 $50 BUY -- $0.60 ▼ 186% C$0.78 ▼ 0.27x 0.77x NM NM BUY $0.75 257% $0.81 0.93x JG

Candente Copper DNT-T C$0.09 $9 SELL -- $0.10 ▼ 11% C$1.79 ▼ 0.05x 0.06x NM NM SELL $0.15 67% $2.33 0.06x DC

Excels ior Mining MIN-T C$0.25 $30 BUY -- $0.90 ▼ 260% C$2.96 ▼ 0.08x 0.30x $0 NM BUY $1.00 300% $3.04 0.33x JG

Heron Resources HER-T C$0.11 $43 BUY -- $0.20 ▼ 82% C$0.34 ▼ 0.32x 0.58x $0 $0.00 BUY $0.30 173% $0.50 0.60x JG

Ivanhoe Mines IVN-T C$1.10 $776 NEUTRAL ▼ $1.60 ▼ 45% C$3.85 ▲ 0.29x 0.42x NM NM BUY $2.50 127% $3.63 0.69x DC

Marengo Mining MRN-T C$0.01 $25 NEUTRAL -- NA NA C$0.21 -- 0.05x NM NM NM NEUTRAL NA $0.21 JG

Nevada Copper NCU-T C$1.72 $150 BUY -- $3.00 ▼ 74% C$3.72 ▼ 0.46x 0.81x $0 ($0.67) BUY $5.00 191% $6.15 0.81x JG

NGEx Resources NGQ-T C$1.15 $215 BUY -- $2.50 117% C$3.37 0.34x 0.74x ($20) ($0.11) BUY $3.40 $3.37 DC

Quaterra Resources QTA-T C$0.05 $12 NEUTRAL -- $0.15 -- 200% C$0.34 ▼ 0.15x 0.44x $0 $0.00 NEUTRAL $0.15 200% $0.39 0.39x JG

Rathdowney ResourcesRTH-T C$0.26 $28 NEUTRAL -- NA NA C$0.36 ▲ 0.73x NM NM NM NEUTRAL NA $0.32 JG

Reservoir Minera ls* RMC-T C$3.82 $198 BUY -- NA NA NA NM NM NM NM BUY NA NA DC

Zazu Metals ZAZ-T C$0.33 $13 NEUTRAL -- NA NA C$1.95 ▼ 0.17x NM NM NM NEUTRAL NA $2.80 JG

Copper Developers Average 0.20x 0.46x 0.46x

AGGREGATES Zinc Developers Average 0.37x 0.68x 0.76x

Polaris Minera ls PLS-T C$2.14 $171 BUY -- $3.00 40% C$2.59 ▲ 0.83x 1.16x $9 $0.04 BUY $3.00 40% $2.42 1.24x DC

COALCardero Resource CDU-T C$0.03 $5 UR UR UR UR UR UR UR UR NEUTRAL $0.15 400% $0.38 0.40x JG

Coalspur Mines CPT-T C$0.01 $7 NEUTRAL -- $0.10 -- 900% C$0.24 ▼ 0.04x 0.41x NM NM NEUTRAL $0.10 900% $1.09 0.09x DC

Xinergy Ltd XRG-T C$0.09 $4 UR UR UR UR UR UR UR UR UR UR UR DC

*Ideas of Interest: Dundee Capital Markets has not initiated formal continuing cov erage of Idea of Interest companies. All opinions and estimates contained in an Idea of Interest report are subject to change w ithout notice and are

prov ided in good faith but w ithout the legal responsibility that w ould accompany formal continuous research cov erage.

AnalystRating TargetNAV

($/sh)

NAV

($/sh)Name Symbol Rating Target

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 5

SECTOR VALUATION IS ATTRACTIVE

Book Value - Canadian Metals & Minerals Sector now back to GFC and 2001 levels

Sources: Factset

Copper Producers Discounting $2.65/lb copper prices, a 6% discount to spot

Sources: Dundee Capital Markets

$2.11

$2.18

$2.31

$2.53

$2.56

$2.72

$2.73

$2.74

$2.78

$2.79

$2.83

$2.88

$2.97

$3.02

$0.00 $1.00 $2.00 $3.00

Excelsior Mining

Ivanhoe Mines

Quaterra Resources

Thompson Creek

Capstone Mining

Taseko Mines

First Quantum

Hudbay Minerals

Candente Copper

Lundin Mining

Atico Mining

Nevada Copper

Copper Mountain

NGEx Resources

ProducersDevelopers

*Ivanhoe's NAV is supported by its zinc and platinum assets.

*Average $2.65

Copper Price Required for NAV = Current Stock Price

Price/Book Value (Canada: Metals/Minerals)

This chart shows the price to book value ratio for the industry since 2001.

We can see that the P/BV ratio has come down steadily since the end of 2010 and now trades at their lowest level since the Global Financial Crisis and 2001. The DCM universe is trading at a P/BV of 0.81X, the bottom in 2008 and 2001.

This is after the Mining industry wrote down over $80B in 2013. Teck Resources could be forced to write down its oil sands projects if oil prices stay low.

The following chart shows the copper price being discounted by the copper producers is $2.61/lb., a 6% discount to the current spot copper price.

In October when we last calculated this discounted copper price it was $2.51/lb. or a 17% discount to the spot price. Since then we have rolled forward our NAV's to reflect only value for 2015 and beyond.

This analysis might suggest a further 10% downside to the copper producers or our price forecasts.

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 6

SHORT/MEDIUM TERM DRIVERS

Waiting for US$ to Peak-Could get short term correction in 2015

Sources: IMF, DCM Economics.

Lower Energy Prices A Positive For Base Metals Miners

Sources: FactSet.

Mining margins-At 2008 levels, offering fundamental support for shares

Sources: FactSet Consensus, Dundee Capital Markets

Medium term - US monetary reflation ending while Europe, Japan, China easing. This should support the US$ in 2015.

But with US$ at a 9-year high, it could be ripe for a short term technical correction.

Potential positive: US$ could peak at first US rate increase.

Oil prices have collapsed recently on worries of oversupply despite uncertainties in the Middle East and Ukraine. Weaker energy (oil futures in contango) prices would be a positive for miners.

Futures Curve

Based on consensus estimates, EBITDA margins appear to have bottomed in Q2-Q3/2014 at 2008 levels.

Weaker domestic currencies/energy prices should help margins going forward.

Adding fundamental support for consolidating share prices.

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 7

FUNDAMENTAL BACKDROP

Adjusting our Metal prices to allow for US$ strength/weak economic growth - Zn/Co forecasts up, but rest flat to down

Sources: Dundee Capital Markets

Global Growth vs. Commodity Prices - 2015 Global Growth could be revised down further

Source: IMF, Federal Reserve and DCM Economics.

US $ Strength has dominated TSX Diversified Metals & Mining (commodity) performance

Source: Thomson Reuters Datastream, WSJ, DCM Economics.

This chart shows the impact of 3 factors on the 12-month percent change of the TSX Diversified Metals & Mining Index, namely the US dollar, the cost/profitability and the global demand factors. We can see that the US dollar (in blue) has been the most influential factor in recent period.

We are updating our commodity price forecasts by marking-to-market our short term forecasts, leaving our long term view unchanged, except for coal. We have raised the zinc/lead/cobalt price forecast for 2016.

Global growth below 4% is a major headwind for commodities; IMF forecasts 2014/2015 growth of 3.3%/3.8%.

2015's forecast could be revised down further, closer to 2014 levels, although US growth is expected to be strong.

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 8

Metals & Mining Sub-Index performance enters into the "improving" zone - Beginning of a rotation into Base Metals?

Sources: Bloomberg, Dundee Capital Markets

Global Economy (PMI) Struggling- Chinese economy weakened, US economy looks to be strengthening

Sources: Bloomberg, Dundee Capital Markets

Using Bloomberg's Relative Rotation metric we show that the Materials universe (STMATR, in purple) has recently moved from the "lagging" to the "improving" zone of sector performance.

The M+M index will first look to stabilize, and will not benefit from sector rotation until the US$ peaks.

US economy is expanding nicely. The Chinese economy has weakened and the Japan appears to be stagnating. Europe should benefit from cheap oil.

Chinese GDP appears to be growing at <7.0% Y/Y. More stimulus is needed to offset weakness in the construction sector and worries over shadow banking defaults.

Other Risks: Geopolitical uncertainty increasing in Ukraine, Middle East, HK.

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 9

Base Metal Prices - Zinc and Nickel up, Copper prices down (just like Chinese economy), Bulk commodities down

Sources: FactSet, Dundee Capital Markets

LME Inventories- Total Inventories declining, led by zinc and copper, looks like we will have to wait for Nickel

Sources: Bloomberg, Dundee Capital Markets

23-Dec-13 10-Feb-14 31-Mar-14 19-May-14 07-Jul-14 25-Aug-14 13-Oct-14 01-Dec-14

-10

0

10

20

30

40

50%

-15.2 Pb

-12.2 Cu

4.0 Zn

7.5 Ni

Commodities performance over 1 yearCopper (LME Cash $/t) Zinc (LME Cash $/t) Lead (LME Cash $/t) Nickel (LME Cash $/t)

Prices

Base Metals US$/tonne US$/lb 1M 3M 1Y

LME Cobalt $31,000 $14.06 3.3% (1.6%) 8.8%

LME Nickel $15,148 $6.87 (6.9%) (9.0%) 8.6%

LME Zinc $2,177 $0.99 (1.5%) (4.0%) 6.1%

LME Aluminum $1,856 $0.84 (6.0%) (3.0%) 3.1%

LME Molybdenum $19,996 $9.07 (0.3%) (8.4%) (7.0%)

LME Copper $6,285 $2.85 (2.1%) (5.4%) (14.8%)

LME Tin $18,910 $8.58 (7.1%) (6.9%) (15.5%)

LME Lead $1,857 $0.84 (8.6%) (10.7%) (16.2%)

Change

5.00

6.00

7.00

8.00

9.00

10.00

200

240

280

320

360

400

440

De

c-1

3

Ja

n-1

4

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oc

t-1

4

No

v-1

4

De

c-1

4

US

$/lb

Th

ou

sa

nd

s t

on

ne

s

Nickel - 1Yr Inventory & Price

Price

0.80

0.90

1.00

1.10

500

700

900

1100

De

c-1

3

Ja

n-1

4

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oc

t-1

4

No

v-1

4

De

c-1

4

US

$/lb

Th

ou

sa

nd

s t

on

ne

s

Zinc - One Year Inventory & Price

Price

2.80

3.00

3.20

3.40

3.60

100

300

500

700

900

De

c-1

3

Ja

n-1

4

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oc

t-1

4

No

v-1

4

De

c-1

4

US

$/lb

Th

ou

sa

nd

s t

on

ne

s

Copper - 1Yr Inventory & Price

Price

0.0

0.5

1.0

1.5

2.0

2.5

Se

p-0

3

Au

g-0

4

Au

g-0

5

Au

g-0

6

Au

g-0

7

Se

p-0

8

Se

p-0

9

Se

p-1

0

Se

p-1

1

Se

p-1

2

Se

p-1

3

Se

p-1

4

Mil

lio

ns

to

nn

es

10 Yr Total Inventories (ex aluminium)

Nickel inventory

Lead inventory

Zinc inventory

Copper inventory

Inventories

Base Metals tonnes 1W chg 1M 3M 1Y 2Y

LME Nickel 405,294 -2,076 4.1% 21.0% 58.9% 194.1%

LME Tin 11,270 -245 9.7% 13.7% 8.7% (4.2%)

LME Lead 220,200 -6,575 1.6% (2.5%) (0.9%) (36.5%)

LME Aluminum 4,292,450 -25,750 (2.3% ) (8.9%) (20.5%) (17.0%)

LME Zinc 690,825 11,900 0.5% (8.5%) (24.8%) (43.7%)

LME Copper* 283,808 5,999 2.8% 7.5% (48.7%) (47.9%)

*Copper inventory includes LME, COMEX and Shanghai

Total LME Inventories rolled over in late 2013, but increased again in mid-2014.

With copper and zinc inventories down 49% and 25% each over the last 12 months, total base metals inventories (ex-aluminum) are back down to 2010 levels.

Nickel inventories are still high (up 59% over the last 12 months), but are expected to peak in 2015.

Chinese NPI production is falling. As laterite stockpiles are used up, expect NPI production to fall further. This will help send nickel market into deficit.

However with supply coming from Philippines deficit may be less than expected.

From the bottom in July 2013, Base metal prices are mixed, led by nickel and zinc.

Nickel/Zinc are responding to supply curtailments. Indonesian regulations (Ni) and closure of western mines (Zn).

Copper is below $3/lb due to worries over Chinese (global) economy, collateralized financing deals and strong US$. Copper looks to test $2.50/lb. in H1/15, but supply surplus rapidly disappearing and fundamental outlook should be better in second half.

HCC and Iron ore markets needs to deal with oversupply, curtailments needed soon.

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 10

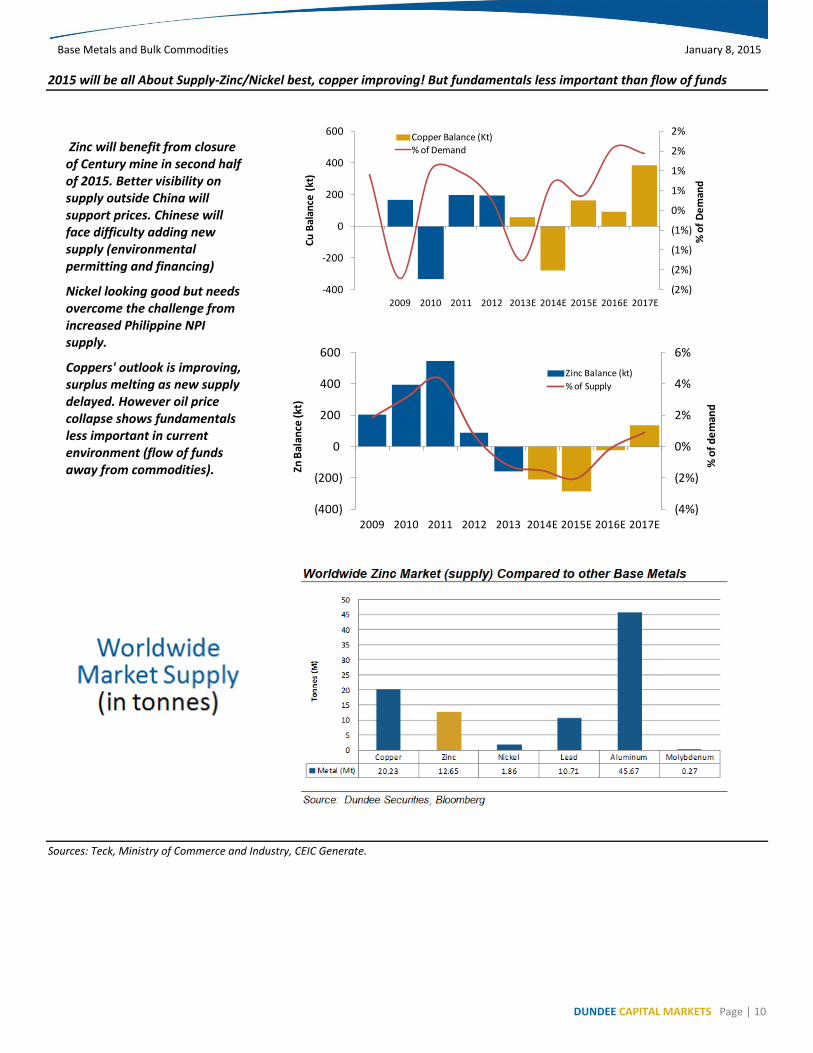

2015 will be all About Supply-Zinc/Nickel best, copper improving! But fundamentals less important than flow of funds

Sources: Teck, Ministry of Commerce and Industry, CEIC Generate.

(2%)

(2%)

(1%)

(1%)

0%

1%

1%

2%

2%

-400

-200

0

200

400

600

2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

% o

f D

em

and

Cu

Bal

ance

(kt

)

Copper Balance (Kt)

% of Demand

(4%)

(2%)

0%

2%

4%

6%

(400)

(200)

0

200

400

600

2009 2010 2011 2012 2013 2014E 2015E 2016E 2017E

% o

f d

em

and

Zn B

alan

ce (k

t)

Zinc Balance (kt)

% of Supply

Zinc will benefit from closure of Century mine in second half of 2015. Better visibility on supply outside China will support prices. Chinese will face difficulty adding new supply (environmental permitting and financing)

Nickel looking good but needs overcome the challenge from increased Philippine NPI supply.

Coppers' outlook is improving, surplus melting as new supply delayed. However oil price collapse shows fundamentals less important in current environment (flow of funds away from commodities).

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 11

DCM Base Metals and Bulk Commodities Updated Ratings and Recommendations

Major Producers

First Quantum

FM

We are reiterating our BUY rating but are decreasing our target to $20.00/sh (from $25.00) using a 9.9x EV/EBITDA

multiple to our 2015 EBITDA of $1.7B (from $2.6B).

Why such a large reduction in EBITDA? The biggest impact on our EBTIDA came from the fact we are now assuming

the Zambian government will be successful in replacing the current corporate tax by a 20% royalty at both Kansanshi

and Sentinel (the royalty is taken out of gross profit).

We are also being cautious on Kansanshi's production due to incertainties related to the availability of the 2nd

power line and the reliability of the power grid in Zambia. This could slowdown the production coming out of

Sentinel, Kansanshi and the new copper smelter. As for nickel, we are being cautious regarding the leak in the

atmospheric leach tank at Ravensthorpe announced in December. As such we also lowered our copper and nickel

production expectation in 2015 and this had a negative impact on our EBITDA forecast.

We believe FM remains the premium copper growth play in the sector despite the short term political/fiscal

uncertainties in Zambia. By 2018 once Sentinel, Kansanshi's smelter and the high profile Cobre Panama projects are

on-line, FM could become the 4th biggest copper producer, ahead of big producers such as BHP Billiton, Southern

Copper and Rio Tinto (not covered).

Teck Resources

TCK.B

We are reiterating our NEUTRAL rating and are decreasing our 12-month target to $19.00/sh (from $24.00) based on a

6.4x EV/EBITDA multiple to our 2015 EBITDA of $2.7B (from $2.9B). While we previously had a $1.0B value (~$1.65/sh)

for the Energy Business (Fort Hills, Frontier & Equinox), we have set this value to zero given the current oil price and

poor visibility going forward.

Producers

Atico Mining

ATY

We are reiterating our BUY rating but are decreasing our target price to $0.75/share (from $1.00) based on a 6.7x

EV/EBITDA multiple to our 2015 EBITDA of $14M (from $17M). We like ATY for its FCF yield of ~15%.

Capstone Mining

CS

We are reiterating our BUY rating (previously BUY, TOP PICK) and are lowering our target price to $3.25/share (from

$4.25/share) based on a 6.0x EV/EBITDA multiple (unch.) to our 2015 EBITDA of $235M (from $299M).

Copper Mountain

CUM

We are reiterating our NEUTRAL rating but are decreasing our target price to $1.90/share (from $2.80) based on a 6.0x

EV/EBITDA multiple (unch.) to our 2015 EBITDA of $90M (from $105M).

Hudbay Minerals

HBM

We are reiterating our BUY rating but are decreasing our target price to $11.50/share (from $13.00) based on a 8.9x

EV/EBITDA multiple to our 2015 EBITDA of $369M (from $471M). HBM will finally see production growth in 2015 as

Constancia ramps up. 2016 should be even bigger with Constancia at full speed for the entire year.

Ivernia

IVW

We are reiterating our NEUTRAL rating but are lowering our target price to $0.20/share (from $0.30) based on a 0.5x

multiple (from 0.8x) to our NAV of $0.41/share (from $0.36/share). The lower lead price forecast is offset by the AUD.

Katanga Mining

KAT

We are reiterating our NEUTRAL rating and 12-month target price to $0.40/sh (no change) based on a 0.6x NAV

multiple to our NAV of $0.68/sh (from $0.76). KAT's parent company is Glencore (not rated) which owns 75.2% of KAT

shares.

Lundin Mining

LUN

We reiterate our BUY (Top Pick) rating but are decreasing our target to C$7.00/share (from $8.00) based on a 6.9x

EV/EBITDA multiple to our 2015 EBITDA of $876M (from $1,100M). We expect the new Candelaria mine plan will

smooth production going forward. However, until 2Q15 release we have production declining in 2016.

Largo Resources

LGO

We are reiterating our BUY rating but are lowering our target price to $3.00/share (from $4.25/share) based on a 8.0x

EV/EBITDA multiple (unch.) to our 2016 EBITDA of $75M (from $98M) due to lower vanadium prices and liquidity

concerns. We have lowered our V2O5 forecast in 2015 and 2016 to $5.25/lb V2O5 from $6.00/lb V2O5.

Nevsun Resources

NSU

We are upgrading our rating to BUY (TOP PICK) from BUY and are reiterating our target price of $6.00/share based on

a 3.5x EV/EBITDA multiple (from 3.3x) to our 2015 EBITDA of $207M (from $231M). Our TOP PICK rating is based on the

fact that NSU is a low cost copper producer, FCF-yielding, levered to zinc in 2016, has a strong balance sheet, and has

an annualized dividend of US$0.16/share (~4% dividend yield).

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 12

Polaris Materials

PLS

We are reiterating our BUY rating and target price of C$3.00/sh based on a 1.2x multiple to our NAV of C$2.59/sh (up

from $2.42). PLS is leveragedd to the US non-residential construction market which we expect to grow in 2015.

Taseko Mines

TKO

We are reiterating our NEUTRAL rating but are lowering our target price to $1.50/share (from $2.00) based on a 6.0x

EV/EBITDA multiple (unch.) to our 2015 EBITDA of $70M (from $90M) and 0.5x NPV multiple to the Florence ISR

copper project (from 0.4x). We are increasing the NPV multiple due to the successful permitting of Florence.

Thompson Creek

TCM

We are downgrading our rating to NEUTRAL (from BUY) and are decreasing our target price to $2.15/share (from

$3.00) based on a 5.9x EV/EBITDA multiple to our 2015 EBITDA of $195M (from $221M). While we believe Mt.Milligan

is improving, TCM's ability to deal with its high debt level is constrained.

Trevali Mining

TV

We are reiterating our BUY (TOP PICK) rating and our target price of $2.00/share based on a 6.0x EV/EBITDA multiple

(unch.) to our 2016 EBITDA (from 2015) of $107M. Recall 2015 is a ramp-up year at Caribou, and TV is the best vehicle

for zinc leverage on the TSX. TV should have two producing operations online and fully ramped-up by the time we

expect improving zinc S&D fundamentals to buoy prices this year.

Developers

Cadente Copper

DNT

We are reiterating our SELL rating and are symbolicaly decreasing our target price to $0.10/sh (from $0.15) based on a

0.05x NAV multiple to our NAV of $1.79/sh (from $2.33). While the NAV is attractive, DNT will require financing or a

JV Partner and this will most likely dilute current shareholders. We also highlight that aside from financing, the

social license remains a key issue for DNT.

Canadian Zinc

CZN

We are reiterating our BUY rating but are lowering our target to $0.60/share (from $0.70/share) based on a 0.8x

multiple (from 0.9x) to our NAV of $0.78/share (from $0.81/share).

NGEx Resources

NGQ

We are reiterating our BUY recommendation but are decreasing our target to $2.50/sh based on an EV/lbs approach

(using ¢2.00/lb, down from ¢2.50) as it is still too early to reliably value NGQ using NPV. We decided to lower the

value per pound of resources given the lower pricing environment for copper. NGQ has capital to survive this

difficult period.

Ivanhoe Mines

IVN

We are downgrading our rating to NEUTRAL (from BUY) and are decreasing our target price to $1.50/share (from

$2.50) based on a 0.4x NAV multiple to our NAV of $3.85/sh (from $3.63). The NAV went up slightly given some sunk

capex and the fact that production projection occurs at our unchanged long term commodity prices. That said, we

lowered our multiple to account for the fact IVN will need to raise a lot of funds to build its 3 projects in a

challenging environment.

Marengo Mining

MRNWe are reiterating our NEUTRAL rating with no target price. MRN has a NAV of $0.21/share (unch.).

Nevada Copper

NCU

We are reiterating our BUY rating but are lowering our target price to $3.00/share (from $5.00/share) based on a 0.8x

mulitple (unch.) to our NAV of $3.72/share (from $6.15/share). NAV down due to increased cost of the new Red Kite

facility, lower copper price, delay in production of Stage 1 underground by 1 year, and delay of Stage 2 OP mine by

1.5 years.

Quaterra Res.

QTA

We are reiterating our NEUTRAL rating and our target of $0.15/share based on a 0.4x mulitple to our NAV of

$0.34/share (from $0.39/share).

Rathdowney Res.

RTHWe are reiterating our NEUTRAL rating with no target price. RTH has a NAV of $0.36/share (from $0.32/share).

Heron Resources

HER

We are reiterating our BUY rating but are lowering our target price to $0.20/share (from $0.30/share) based on a 0.6x

multiple (unch.) to our NAV of $0.34/share (from $0.50/share).

Zazu Metals

ZAZWe are reiterating our NEUTRAL rating with no target price. ZAZ has a NAV of $1.95/share (from $2.80/share).

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 13

Source: Dundee Capital Markets

Idea Of Interest*

Reservoir Minerals

RMC

No rating. No target. Reservoir continues to work towards a strategic agreement with FCX (not rated) on Cukaru Peki

which is taking longer than planned. In the meantime, the company is reporting interesting exploration results on its

100%-owned properties. One of the key element to the RMC story is that it already has a strategic partner (in FCX) to

help them finance and develop the Cukaru Peki Discovery and we believe this is key in the current market

environment where many juniors are simply unable to raise funds.*Dundee Capital Markets has not initiated formal continuing coverage of Idea of Interest companies. All opinions and estimates

contained in an Idea of Interest report are subject to change without notice and are provided in good faith but without the legal

responsibility that would accompany formal continuous research coverage.

Coal

Cardero Resources

CDU

We are downgrading our rating to UNDER REVIEW (from NEUTRAL) as the project is not economical at our new coal

price forecast.

Coalspur Mines

CPT

We are reiterating our NEUTRAL rating but are lowering our target to C$0.02/sh (from $0.10) based on a 0.1x multiple

to our NAV of C$0.24/sh (from $1.09). The company need much higher termal coal price in order for the project to be

viable. Aside from a good recovery in thermal coal prices, the two other pieces of the puzzle missing are the

construction permits and, more importantly, a strategic partner to finance the construction. CPT currently has a

negative working capital balance of ~$100M and needs financing to remain a going concern.

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 14

Disclosures & Disclaimers This research report (as defined in IIROC Rule 3400) is issued and approved for distribution in Canada by Dundee Securities Ltd. (“Dundee Capital Markets”), an investment dealer operating its business through its two divisions, Dundee Capital Markets and Dundee Goodman Private Wealth. Dundee Capital Markets is a member of the Canadian Investor Protection Fund, the Investment Industry Regulatory Organization of Canada and an investment fund manager registered with the securities commissions across Canada. Dundee Capital Markets is a subsidiary of Dundee Corporation. Research Analyst Certification: Each Research Analyst involved in the preparation of this research report hereby certifies that: (1) the views and recommendations expressed herein accurately reflect his/her personal views about any and all of the securities or issuers that are the subject matter of this research report; and (2) his/her compensation is not and will not be directly related to the specific recommendations or views expressed by the Research Analyst in this research report. The Research Analyst involved in the preparation of this research report does not have authority whatsoever (actual, implied or apparent) to act on behalf of any issuer mentioned in this research report. U.S. Residents: Dundee Securities Inc. is a U.S. registered broker-dealer, a member of FINRA and an affiliate of Dundee Capital Markets. Dundee Securities Inc. accepts responsibility for the contents of this research report, subject to the terms and limitations as set out above. U.S. residents seeking to effect a transaction in any security discussed herein should contact Dundee Securities Inc. directly. Research reports published by Dundee Capital Markets are intended for distribution in the United States only to Major Institutional Investors (as such term is defined in SEC 15a-6 and Section 15 of the Securities Exchange Act of 1934, as amended) and are not intended for the use of any person or entity. UK Residents: Dundee Securities Europe LLP, an affiliate of Dundee Capital Markets, is authorized and regulated by the United Kingdom’s Financial Conduct Authority (No 586295) for the purposes of security broking & asset management. Research prepared by UK-based analysts is under the supervision of and is issued by its affiliate, Dundee Capital Markets. Dundee Securities Europe LLP is responsible for compliance with applicable rules and regulations of the FCA, including Chapter 12 of the FCA’s Conduct of Business Sourcebook (the “FCA Rules”) in respect of any research recommendations (as defined in the FCA Rules) in reports prepared by UK-based analysts. Dundee Capital Markets and Dundee Securities Europe LLP have implemented written procedures designed to identify and manage potential conflicts of interest that arise in connection with the preparation and distribution of their research. Dundee Capital Markets is responsible (i) for ensuring that the research publications are compliant with IIROC Rule 3400 Research Restrictions and Disclosure Requirements. And (ii) including all required conflict of interest disclosures. General: This research report is provided, for informational purposes only, to institutional investor and retail clients of Dundee Capital Markets in Canada. This research report is not an offer to sell or the solicitation of an offer to buy any of the securities discussed herein. The information contained in this research report is prepared from publicly available information, internally developed data and other sources believed to be reliable, but has not been independently verified by Dundee Capital Markets and Dundee Capital Markets makes no representations or warranties with respect to the accuracy, correctness or completeness of such information and they should not be relied upon as such. All estimates, opinions and recommendations expressed herein constitute judgments as of the date of this research report and are subject to change without notice. Dundee Capital Markets does not accept any obligation to update, modify or amend this research report or to otherwise notify a recipient of this research report in the event that any estimates, opinions and recommendations contained herein change or subsequently becomes inaccurate or if this research report is subsequently withdrawn. Past performance is not a guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance of any security mentioned in this research report. The price of the securities mentioned in this research report and the income they produce may fluctuate and/or be adversely affected by market factors or exchange rates, and investors may realize losses on investments in such securities, including the loss of investment principal. Furthermore, the securities discussed in this research report may not be liquid investments, may have a high level of volatility or may be subject to additional and special risks associated with securities and investments in emerging markets and/or foreign countries that may give rise to substantial risk and are not suitable for all investors. Dundee Capital Markets accepts no liability whatsoever for any loss arising from any use or reliance on this research report or the information contained herein. The securities discussed in this research report may not be suitable for all types of investors and such reports do not take into account particular investment needs, objectives and financial circumstances of a particular investor. An investor should not rely solely on investment recommendations contained in this research report, if any, as a substitution for the exercise of their own independent judgment in making an investment decision and, prior to acting on any of contained in this research report, investors are advised to contact his or her investment adviser to discuss their particular circumstances.

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 15

Non-client recipients of this research report should consult with an independent financial advisor prior to making any investment decision based on this research report or for any necessary explanation of its contents. Dundee Capital Markets will not treat non-client recipients of this research report as its clients by virtue of such persons receiving this research report. Nothing in this research report constitutes legal, accounting or tax advice. Investors should consult with his or her own independent legal or tax adviser in this regard. Dundee Capital Markets Research is distributed by email, website or hard copy. Dissemination of initial research reports and any subsequent research reports is made simultaneously to a pre-determined list of Dundee Capital Markets' Institutional Sales and Trading representative clients and Dundee Goodman Private Wealth retail private client offices. The policy of Dundee Capital Markets with respect to Research reports is available on the Internet at www.dundeecapitalmarkets.com. Dundee Capital Markets has written procedures designed to identify and manage potential conflicts of interest that arise in connection with its research and other businesses. The compensation of each Research Analyst/Associate involved in the preparation of this research report is based competitively upon several criteria, including performance assessment criteria based on quality of research. The Research Analyst compensation pool includes revenues from several sources, including sales, trading and investment banking. Research analysts do not receive compensation based upon revenues from specific investment banking transactions. Dundee Capital Markets generally restricts any research analyst and any member of his or her household from executing trades in the securities of a company that such research analyst covers. Certain discretionary client portfolios are managed by portfolio managers and/or dealing representatives in its private client advisory division, Dundee Goodman Private Wealth. The aforementioned portfolio managers and/or dealing representatives are segregated from Research and they may trade in securities referenced in this research report both as principal and on behalf of clients (including managed accounts and investment funds). Furthermore, Dundee Capital Markets may have had, and may in the future have, long or short positions in the securities discussed in this research report and, from time to time, may have executed or may execute transactions on behalf of the issuer of such securities or its clients. Should this research report provide web addresses of, or contain hyperlinks to, third party web sites, Dundee has not reviewed the contents of such links and takes no responsibility whatsoever for the contents of such web sites. Web addresses and/or hyperlinks are provided solely for the recipient's convenience and information, and the content of third party web sites is not in any way incorporated into this research report. Recipients who choose to access such web addresses or use such hyperlinks do so at their own risk. Unless publications are specifically marked as research publications of Dundee Capital Markets, the views expressed therein (including recommendations) are those of the author and, if applicable, any named issuer or Investment dealer alone and they have not been approved by nor are they necessarily those of Dundee Capital Markets. Dundee Capital Markets. expressly disclaims any and all liability for the content of any publication that is not expressly marked as a research publication of Dundee Capital Markets. Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by the author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. © Dundee Securities Ltd. Any reproduction or distribution in whole or in part of this research report without permission is prohibited. Informal Comment: Informal Comments are analysts’ informal comments that are posted on the Dundee website. They generally pertain to news flow and do not contain any change in analysts' opinion, estimates, rating or target price. Any rating(s) and target price(s) in an Informal Comment are from prior formal published research reports. A link is provided in any Informal Comment to all company specific disclosures and analyst specific disclosures for companies under coverage, and general disclosures and disclaimers. Presentations do not include disclosures that are specific to analysts and specific to companies under coverage. Please refer to formal published research reports for company specific disclosures and analyst specific disclosures for companies under coverage. Please refer to formal published research reports for valuation methodologies used in determining target prices for companies under coverage. Idea of Interest: Dundee Capital Markets has not initiated formal continuing coverage of Idea of Interest companies. Dundee Capital Markets from time to time publishes reports on Idea of Interest securities for which it does not and may not choose to provide formal continuous research coverage. All opinions and estimates contained in an Idea of Interest report are subject to change without notice and are provided in good faith but without the legal responsibility that would accompany formal continuous research coverage. The companies may have recommendations and risk ratings as per our regular rating system and may have target prices, see Explanation of Recommendations and Risk Ratings for details. Any recommendations, ratings, target prices and/or comments expire 30 days from the published date, and once expired should no longer be relied upon as

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 16

no assurance can be given as to the accuracy or relevance going forward. Dundee does not accept any obligation to update, modify or amend any Idea of Interest report or to otherwise notify a recipient of an Idea of Interest report in the event that any estimates, opinions and recommendations contained in such report change or subsequently become inaccurate. Dundee clients should consult their investment advisor as to the appropriateness of an investment in the securities mentioned. IIROC Rule 3400 Disclosures and/or FCA COBS 12.4.10 Disclosures: A link is provided in all research reports delivered by electronic means to disclosures required under IIROC Rule 3400. Disclosures required under IIROC Rule 3400 for sector research reports covering six or more issuers can be found on the Dundee Capital Markets website at www.dundeecapitalmarkets.com in the Research Section. Other Services means the participation of Dundee in any institutional non-brokered private placement exceeding $5 million. Where Dundee Capital Markets and its affiliates collectively beneficially own 1% or more (or for the purpose of FCA disclosure 5% or more) of any class of the issuer’s equity securities, our calculations will exclude managed positions that are controlled, but not beneficially owned by Dundee Capital Markets. Explanation of Recommendations and Risk Ratings Dundee target: represents the price target as required under IIROC Rule 3400. Valuation methodologies used in determining the price target(s) for the issuer(s) mentioned in this research report are contained in current and/or prior research. Dundee target N/A: a price target and/or NAV is not available if the analyst deems there are limited financial metrics upon which to base a reasonable valuation. Recommendations: BUY: Total returns expected to be materially better than the overall market with higher return expectations needed for more risky securities. NEUTRAL: Total returns expected to be in line with the overall market. SELL: Total returns expected to be materially lower than the overall market. TENDER: The analyst recommends tendering shares to a formal tender offer. UNDER REVIEW: The analyst will place the rating and/or target price Under Review when there is a significant material event with further information pending; and/or when the analyst determines it is necessary to await adequate information that could potentially lead to a re-evaluation of the rating, target price or forecast; and/or when coverage of a particular security is transferred from one analyst to another to give the new analyst time to reconfirm the rating, target price or forecast. Risk Ratings: risk assessment is defined as Medium, High, Speculative or Venture. Medium: securities with reasonable liquidity and volatility similar to the market. High: securities with poor liquidity or high volatility. Speculative: where the company's business and/or financial risk is high and is difficult to value. Venture: an early stage company where the business and/or financial risk is high, and there are limited financial metrics upon which to base a reasonable valuation. Investors should not deem the risk ratings to be a comprehensive account of all of the risks of a security. Investors are directed to read Dundee Capital Markets Research reports that contain a discussion of risks which is not meant to be a comprehensive account of all the risks. Investors are directed to read issuer filings which contain a discussion of risk factors specific to the company’s business. Medium and High Risk Ratings Methodology: Medium and High risk ratings are derived using a predetermined methodology based on liquidity and volatility. Analysts will have the discretion to raise but not lower the risk rating if it is deemed a higher risk rating is warranted. Risk in relation to forecasted price volatility is only one method of assessing the risk of a security and actual risk ratings could differ. Securities with poor liquidity or high volatility are considered to be High risk. Liquidity and volatility are measured using the following methodology: a) Price Test: All securities with a price <= $3.00 per share are considered high risk for the purpose of this test. b) Liquidity Test: This is a two-tiered calculation that looks at the market capitalization and trading volumes of a company. Smaller capitalization stocks (<$300MM) are assumed to have less liquidity, and are, therefore, more subject to price volatility. In order to avoid discriminating against smaller cap equities that have higher trading volumes, the risk rating will consider 12 month average trading volumes and if a company has traded >70% of its total shares outstanding it will be considered a liquid stock for the purpose of this test. c) Volatility Test: In this two step process, a stock’s volatility and beta are compared against the diversified equity benchmark. Canadian equities are compared against the TSX while U.S. equities are compared against the S&P 500. Generally, if the volatility of a stock is 20% greater than its benchmark and the beta of the stock is higher than its sector beta, then the security will be considered a high risk security. Otherwise, the security will be deemed to be a medium risk security. Periodically, the equity risk ratings will be compared to downside risk metrics such as Value at Risk and Semi-Variance and appropriate adjustments may be made. All models used for assessing risk incorporate some element of subjectivity. SECURITY ABBREVIATIONS: NVS (non-voting shares); RVS (restricted voting shares); RS (restricted shares); SVS (subordinate voting shares).

Base Metals and Bulk Commodities January 8, 2015

DUNDEE CAPITAL MARKETS Page | 17

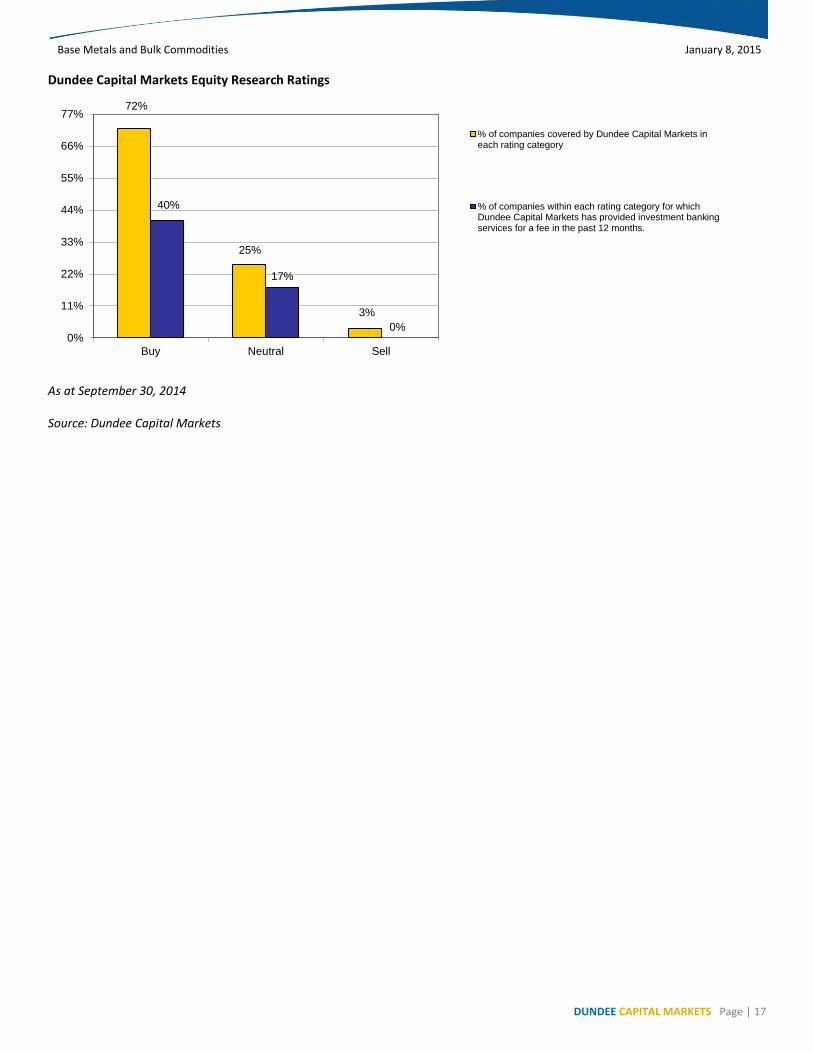

Dundee Capital Markets Equity Research Ratings

As at September 30, 2014 Source: Dundee Capital Markets

72%

25%

3%

40%

17%

0%0%

11%

22%

33%

44%

55%

66%

77%

Buy Neutral Sell

% of companies covered by Dundee Capital Markets ineach rating category

% of companies within each rating category for whichDundee Capital Markets has provided investment bankingservices for a fee in the past 12 months.