basic bookkeeping student handouts - dcc-moodle

TRANSCRIPT

Discovery Community College Basic Bookkeeping, 8th Edition Page 1 of 60

Basic

Bookkeeping

Student Handouts

Chapter Note Pages, Cheat Sheets

and Other Working Papers for

Basic Bookkeeping, An Office Simulation, 8th Edition

Brooke C. W. Baker

Discovery Community College Basic Bookkeeping, 8th Edition Page 2 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 3 of 60

BASIC BOOKKEEPING

Curriculum Guide

PURPOSE This course is designed to provide the learner with the basic skills and knowledge required to

perform manual bookkeeping functions. Essential bookkeeping concepts will be reviewed and

applied. Considerable time will be spent applying these skills and knowledge by completing

practice exercises and assignments.

The skills and knowledge required to carry out manual payroll calculations and remittances will

also be presented.

GOALS Upon successful completion of this course, the participant will have the knowledge and skills

to:

Identify three forms of business organizations

Define each of the five categories of accounts

Classify accounts according to the five categories

Define the terms “debit” and “credit”

Record bookkeeping transactions in a general journal

Assign account numbers

Post transactions from the general journal to the general ledger

Prepare a trial balance from the general ledger

Record transactions in the purchase and sales journals

Set-up accounts payable and accounts receivable subsidiary ledgers

Post purchase and sales journal entries to the subsidiary ledgers

Allocate GST and PST for purchases and sales

Record transactions in the cash receipt and cash payment journals

Reconcile the bank account with the bank statement

Prepare a bank reconciliation statement and accompanying journal entries

Discuss and apply the regulations of the Employment Standards Act

Review and apply Canada Revenue Agency’s (CRA) payroll guide

Use a Payroll Remittance Form (RC104)

Calculate gross earnings and use CRA’s deduction tables

Make payroll calculations and record payroll transactions in the general journal

Record payments to employees and remittances to CRA

Identify and complete various payroll forms

Review Workers Compensation Board (WCB) regulations

ADMISSION REQUIREMENTS and/or PREREQUISITES Applicants must satisfy the admissions requirements for the AF Program.

RECOMMENDED STUDENT CHARACTERISTICS This course assumes an interest in keeping books with a high standard of accuracy. Students

should be willing to work independently and cooperatively, to think and to problem solve.

Discovery Community College Basic Bookkeeping, 8th Edition Page 4 of 60

COURSE DESIGN AND ACTIVITIES This course will be offered over five weeks, Monday to Friday, in either the morning or the

afternoon. All activities will take place in a classroom or computer classroom. Occasional

homework may be required.

The instructor will use various strategies including lectures, group discussion, and student

practice.

Information contained in this curriculum guide is correct at the time of publication. Content of

courses and programs are revised on an ongoing basis to ensure relevance to changing

educational, employment, and marketing needs. The instructor will endeavour to provide notice

of any changes to students as soon as possible.

RESOURCES The required text for this course is Basic Bookkeeping 8th/e, (2019), by Brooke C.W. Barker. A

set of blank working papers comes with the text. Students have access to an online Moodle

course, which includes mini-lectures, practice exercise solutions and chapter multiple choice and

true/false quizzes. The instructor may supply additional resources.

ASSESSMENT AND EVALUATION Student progress and success will be assessed regularly throughout the course. This will be

accomplished using three major practice assignments; two smaller practice assignments (these all

simulate actual bookkeeping activities), Moodle chapter quizzes, and a final simulated

bookkeeping activity project.

The assignments and quizzes are checked for accuracy during the class, and each of the

assignments is valued as per the attached marking schedule. Solutions to practice exercises are

available on Moodle for students to consult.

The final distribution of marks is:

o Major assignments (KBC Company & Moodle Chapter Quizzes) 50%

Smaller assignments 20% (Bank Reconciliation – Payroll Ex. #3)

o Quizzes (Payroll – Assign. #1 & #2, ROE, T4) 10%

Final project (Bookkeeping & Payroll Exams) 20%

Final percent grades for this course will be posted, according to student number, three working

days after the course end date.

INSTRUCTOR CONTACT INFORMATION

Name:

DCC Telephone:

DCC email:

Discovery Community College Basic Bookkeeping, 8th Edition Page 5 of 60

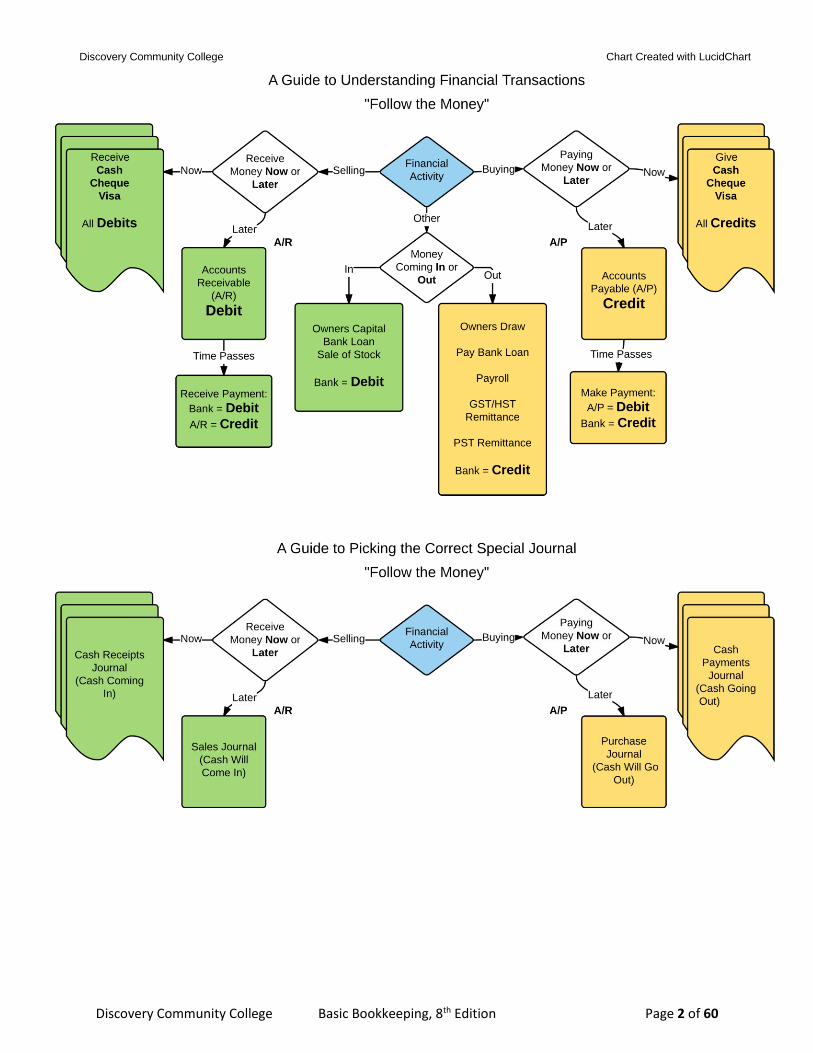

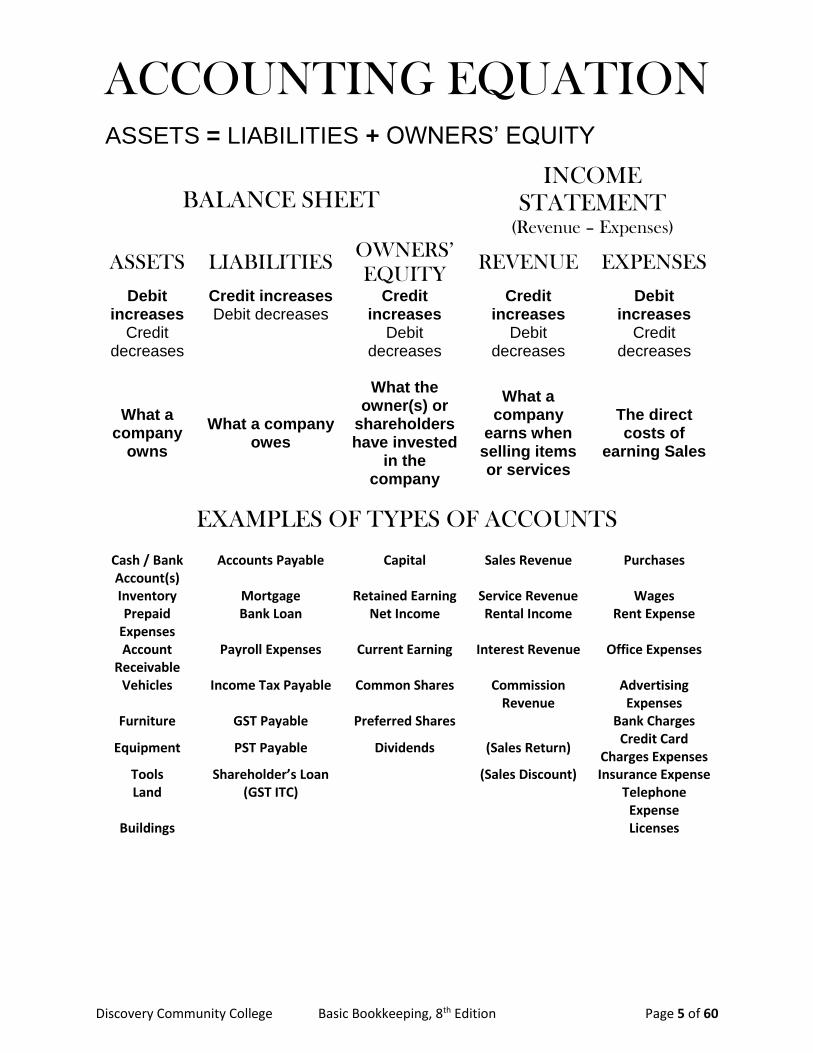

ACCOUNTING EQUATION ASSETS = LIABILITIES + OWNERS’ EQUITY

BALANCE SHEET INCOME

STATEMENT (Revenue – Expenses)

ASSETS LIABILITIES OWNERS’

EQUITY REVENUE EXPENSES

Debit increases

Credit decreases

Credit increases Debit decreases

Credit increases

Debit decreases

Credit increases

Debit decreases

Debit increases

Credit decreases

What a company

owns

What a company owes

What the owner(s) or

shareholders have invested

in the company

What a company

earns when selling items or services

The direct costs of

earning Sales

EXAMPLES OF TYPES OF ACCOUNTS

Cash / Bank Account(s)

Accounts Payable Capital Sales Revenue Purchases

Inventory Mortgage Retained Earning Service Revenue Wages Prepaid

Expenses Bank Loan Net Income Rental Income Rent Expense

Account Receivable

Payroll Expenses Current Earning Interest Revenue Office Expenses

Vehicles Income Tax Payable Common Shares Commission Revenue

Advertising Expenses

Furniture GST Payable Preferred Shares Bank Charges

Equipment PST Payable Dividends (Sales Return) Credit Card

Charges Expenses Tools Shareholder’s Loan (Sales Discount) Insurance Expense Land (GST ITC) Telephone

Expense Buildings Licenses

Discovery Community College Basic Bookkeeping, 8th Edition Page 6 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 7 of 60

Reading Questions – Chapter 1 – An Intro to Bookkeeping – 8th Edition

1. Bookkeeping can be defined as the process of

2. How can keeping detailed financial records aid a business?

3. Define Balance Sheet: and Income Statement:

4. Look at Figure 1.4 to determine the relationship between Assets, Liabilities and Owner’s Equity.

5. The three types of business are: ___________________________________________________________________________________________________________________________________________________________________

6. Give one positive and one negative aspect for each type of business: Prop – Positive: ________________________________________________________________________________ Prop – Negative: ________________________________________________________________________________ Part – Positive: ________________________________________________________________________________ Part – Negative: ________________________________________________________________________________ Corp – Positive: ________________________________________________________________________________ Corp – Negative: ________________________________________________________________________________

7. Define each of the following terms and give one or more examples of each: Assets: Accounts Receivable: Liabilities: Accounts Payable: Owner’s Equity:

Discovery Community College Basic Bookkeeping, 8th Edition Page 8 of 60

Capital: Revenue: Expenses:

8. What is the major difference between assets and expenses?

9. List the 11 GAAP principles?

Practice Exercises:

Do exercises 1, 2 and 3 – All are available on Moodle as Drag and Drop Questions.

Think about It: Check out this section and look back for answers to any questions you are unable to answer.

Discovery Community College Basic Bookkeeping, 8th Edition Page 9 of 60

Reading Questions – Chapter 2 – Recording the Transaction

1. In bookkeeping what does balancing refer to?

2. What is the accounting equation?

3. In bookkeeping what do the terms “Debit” and “Credit” refer? What is the abbreviation for each? Debit: Credit:

4. Which categories of accounts normally increase on the debit side and hold debit balances?

5. Which categories of accounts normally increase on the credit side and hold credit balances?

6. What is meant by a “double entry” system of bookkeeping?

7. What is the difference between a simple journal entry and a compound journal entry?

8. What are the six steps in analyzing a transaction? 1. 2. 3. 4. 5. 6.

9. Define “General Journal” and detail what pieces of information each line contains.

10. Complete the following “rules” for constructing the General Journal. The ____________ side of each transaction must be recorded before the __________side. The ____________ and _____________ are recorded at the top of each page of the General Journal. All financial records must be kept for a period of at least _________ years. If an entry has no cents you may use a ____________ instead. Please do, it is so much easier to read. Entries in the GJ should fill approximately _________ the space provided on the line. This allows room to make ___________________. Credit entries should be ______________ to distinguish them visually from ________ entries.

Discovery Community College Basic Bookkeeping, 8th Edition Page 10 of 60

Transaction explanations should include details such as: __________________________________ Leave a _______________ line between transactions. A transaction should not be ___________________________________________________ General Journal pages should be numbered __________________. Example: ___________ Do not include _________ signs when recording dollar amounts. All numbers in money columns should be written the ________ size. All entries in the General Journal should be made with a/an ________________ to maintain the integrity of the information.

Exercises: 1-8 over several days. Do “Think About It” before moving on.

Discovery Community College Basic Bookkeeping, 8th Edition Page 11 of 60

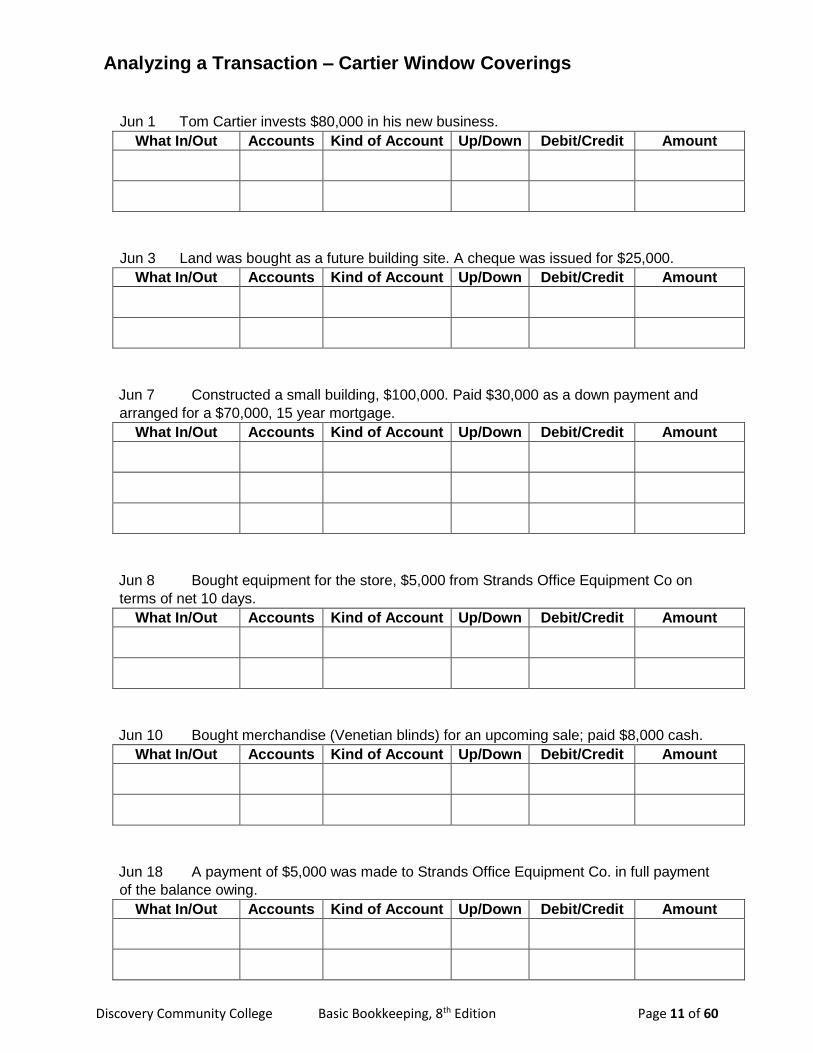

Analyzing a Transaction – Cartier Window Coverings

Jun 1 Tom Cartier invests $80,000 in his new business.

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Jun 3 Land was bought as a future building site. A cheque was issued for $25,000.

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Jun 7 Constructed a small building, $100,000. Paid $30,000 as a down payment and

arranged for a $70,000, 15 year mortgage.

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Jun 8 Bought equipment for the store, $5,000 from Strands Office Equipment Co on

terms of net 10 days.

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Jun 10 Bought merchandise (Venetian blinds) for an upcoming sale; paid $8,000 cash.

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Jun 18 A payment of $5,000 was made to Strands Office Equipment Co. in full payment

of the balance owing.

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 12 of 60

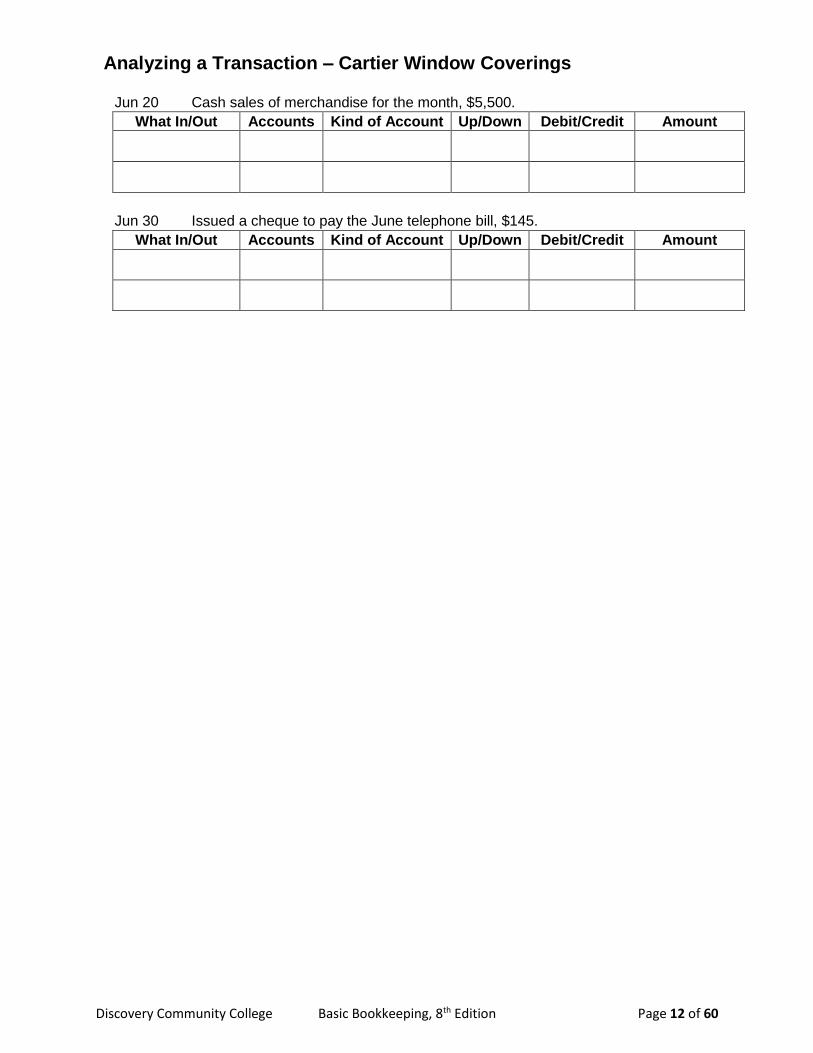

Analyzing a Transaction – Cartier Window Coverings

Jun 20 Cash sales of merchandise for the month, $5,500.

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Jun 30 Issued a cheque to pay the June telephone bill, $145.

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 13 of 60

Analyzing Transactions

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 14 of 60

Analyzing Transactions

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 15 of 60

Analyzing Transactions

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 16 of 60

Analyzing Transactions

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 17 of 60

Analyzing Transactions

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 18 of 60

Analyzing Transactions

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 19 of 60

Analyzing Transactions

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 20 of 60

Analyzing Transactions

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

What In/Out Accounts Kind of Account Up/Down Debit/Credit Amount

Discovery Community College Basic Bookkeeping, 8th Edition Page 21 of 60

Reading Questions – Chapter 3 – The Ledger

1. Define General Ledger.

2. What do ledger accounts show?

3. Memo fields are ________ always necessary in the GL but are particularly helpful in the ___________________ and ________________ ledgers.

4. The Folio, or ______________________________ contains the journal page reference from where the entry was copied.

5. Amounts recorded in the Debit column of the General Journal are recorded in the ___________ column of the General Ledger. Likewise with Credit entries.

6. It is recommended that the balance for each entry be recorded .

7. The DR/CR. Column shows the ____________ of the account balance.

8. Define “Chart of Accounts”

9. What is posting?

10. How do you decide if a DR. or CR goes in the DR./CR. column

11. What is the final step in transferring each transaction from the General Journal to the General Ledger accounts? Why is this step important?

12. What is a Trail Balance and what is the objective in creating the Trial Balance?

13. The titles above the Trial Balance always show what information?

Discovery Community College Basic Bookkeeping, 8th Edition Page 22 of 60

14. What are the five types of errors that can be made in GJ GL Trial Balance Process? 1. 2. 3. 4. 5.

Practice Exercises: Do Exercises 1, 3, 5, 6, and 7. #2 and #4 are Extra Practice.

Do: Think About It Exercises.

KBC Company Project:

Complete the January transactions for the KBC decorating Company introduced on the Chapter 3 KBC Project Handout which you will find in your student handout package or online in Moodle. The KBC Project in your text book is Ontario based and will use HST taxation. The KBC in these project sheets is Manitoba based and uses GST and PST as in BC.

There is a special set of General Ledger sheets for this KBC project in your student forms package. You should place these forms in a separate binder/folder to pass in to your instructor for marking. Shuffle the following forms into this KBC package as directed in the Shuffle List below.

Shuffle List:

1) Please the Marking Sheet (page 23) at the front of your KBC binder.

2) Please the exercise instructions for chapters 3, 4, 5 and 6 (page 25 - 36) after the Marking Sheet.

3) Replace the HST Payable (Account #206) to HST-ITC (Account #207) with pages 37 & 38.

4) Replace the ledger sheet with account numbers 402 – 501 with pages 39 & 40.

5) Remove all the Trial Balance sheets and replace them with pages 41 - 48.

Discovery Community College Basic Bookkeeping, 8th Edition Page 23 of 60

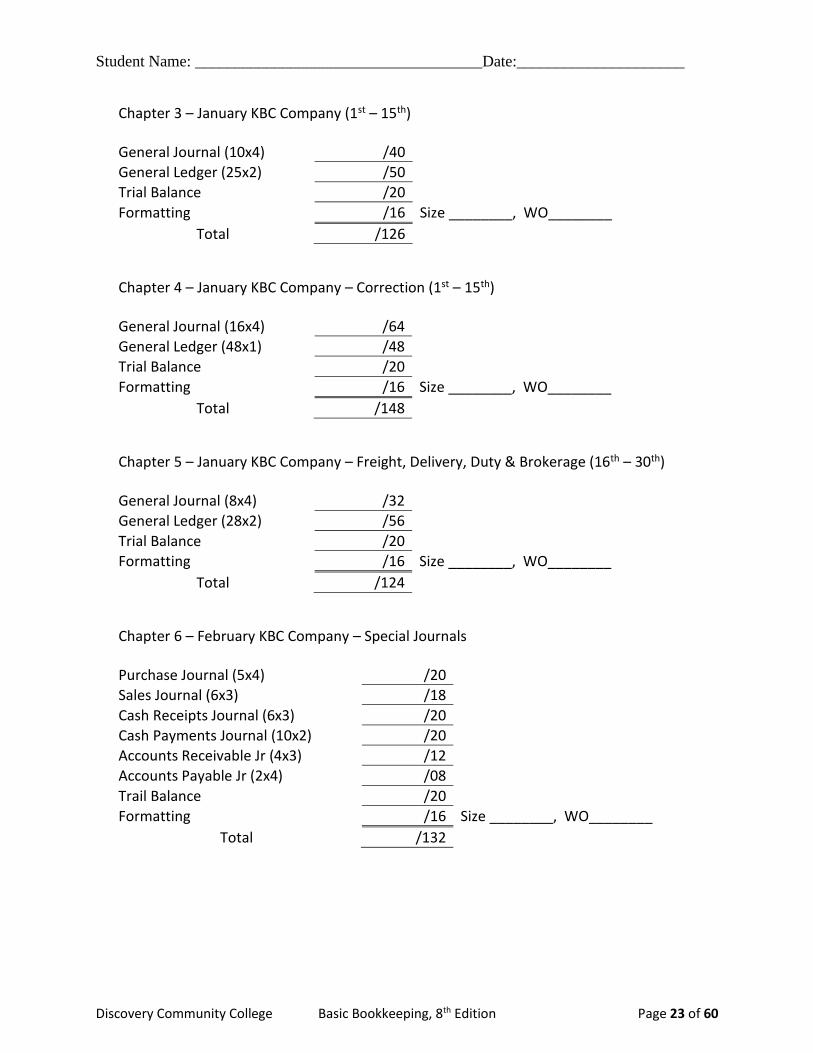

Student Name: ____________________________________Date:_____________________

Chapter 3 – January KBC Company (1st – 15th) General Journal (10x4) /40

General Ledger (25x2) /50

Trial Balance /20

Formatting /16 Size ________, WO________

Total /126

Chapter 4 – January KBC Company – Correction (1st – 15th) General Journal (16x4) /64

General Ledger (48x1) /48

Trial Balance /20

Formatting /16 Size ________, WO________

Total /148

Chapter 5 – January KBC Company – Freight, Delivery, Duty & Brokerage (16th – 30th) General Journal (8x4) /32

General Ledger (28x2) /56

Trial Balance /20

Formatting /16 Size ________, WO________

Total /124

Chapter 6 – February KBC Company – Special Journals Purchase Journal (5x4) /20

Sales Journal (6x3) /18

Cash Receipts Journal (6x3) /20

Cash Payments Journal (10x2) /20

Accounts Receivable Jr (4x3) /12

Accounts Payable Jr (2x4) /08

Trail Balance /20

Formatting /16 Size ________, WO________

Total /132

Discovery Community College Basic Bookkeeping, 8th Edition Page 24 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 25 of 60

Discovery Community College Chapter 3 KBC Exercise – GST and PST

INTRODUCING THE CASE STUDY: KBC DECORATING CO.

Henri Martin and Wes Corbett have decided to go into business together and have

chosen the name KBC Decorating Co. Their business will be two main divisions: a retail

department that will sell paint, wallpaper, and related supplies; and a service department that

will do painting and decorating of office buildings, apartment blocks, and private homes.

Martin and Corbett were previously in this same type of work but operated separate

businesses.

KBC Decorating Co. is located in Winnipeg, Manitoba. Martin and Corbett found a suitable

location from which to operate their business, renting half of a warehouse building owned by

Frank Bailes. Their space includes an office, retail space, and warehouse space.

Your job is to keep the books for KBC Decorating Co. for the first calendar year (January

to December). As you progress through these chapters, you will learn and do. Each chapter will

introduce new concepts that you will incorporate into the regular bookkeeping activities of KBC

Decorating Co. Just as in any new job, each step will be explained and practised before you are

asked to apply it to KBC's activities. You will be learning on the job.

All the supplies necessary for keeping the books for KBC Decorating Co. are found in

the package of working papers available with this textbook. All ledger accounts are

preprinted with the appropriate account names and account numbers. The KBC exercise as

shown in your textbook uses HST taxation. Since BC still uses GST and PST we want you

to practice using this tax scheme. In your student package you will find two ledger pages

that you should use to replace the corresponding sheets in the KBC Decorating Co working

papers ledger. Once reintroduces GST, GST-ITC and PST Payable. The other reintroduces

Commission Revenue. Also in your student package you find pre-printed Trial Balance

sheets that you will use with the KBC exercise instead of the ones you find in your working

papers.

Be sure that the accounts remain in the order given. This will ensure that the ledger is

organized and that the accounts are easy to locate. The chart of accounts for this ledger has been

printed at the end of the textbook for easy reference (see Appendix C).

To record the transactions for the first half of January, select a General Journal sheet from

your supplies and give it GJ1 as the page number. Continue numbering the journal pages as

you start each new page (GJ2, GJ3, etc.). All entries should be recorded in proper format with

suitable explanations. As you proceed further with this case study in later chapters, you will

be referring to this first journal page again, so keep it handy.

Remember to use the Trial Balance sheets from your student package that have GST Payable, GST‐ITC and PST Payable.

Discovery Community College Basic Bookkeeping, 8th Edition Page 26 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 27 of 60

Discovery Community College Chapter 3 KBC Exercise – GST and PST

CASE STUDY: KBC DECORATING

(a) Begin now by recording these transactions in the General Journal: 20—

Jan. 2 The owners started their new business by investing the assets shown here. Notice

from the chart of accounts that each owner has his own Capital account. (You will record

two compound entries for these investments, one for each owner.)

Henri Martin:

Cash $22,000

Furniture & Equipment

Wes Corbett:

8,000

$30,000

Cash $15,000

Vehicle (used van) 15,000

$30,000

2 Issued Cheque #1 for the January rent, $2,500.

2 Issued Cheque #2 for advertising in the newspaper, $565. (Debit Advertising Expense)

4 Bought office supplies, $282.50. Issued Cheque #3. (Debit Office Supplies Expense)

4 Issued Cheque #4 for the installation of our new phone line, $165. (Telephone

Expense)

5 Bought merchandise as follows: paint and supplies, $10,000; wallpaper, $5,000.

Issued Cheque #5. (Notice on the chart of accounts that there are separate Purchases

accounts for these goods.)

9 Bought a paint mixer and color dispenser from Rainbow Supplies Co., $1,695. Issued

Cheque #6. (Tools & Equipment)

10 Cash sales: paint and supplies, $3,000; wallpaper, $1,000. (Notice that there are

separate Sales accounts for these goods.)

15 Cash sales: paint-and supplies, $6,000; wallpaper, $2,000.

(b) Post the journal entries to the ledger accounts. (All ledger accounts for KBC Decorating

Co. should be kept separate from your practice exercise material and should be neatly

arranged in a binder or file so you can access them easily and pass them in for

marking.)

(c) After all posting is complete; prepare a trial balance on January 15. If your trial balance

does not balance on the first attempt, use the steps for locating errors as described in this

chapter.

Discovery Community College Basic Bookkeeping, 8th Edition Page 28 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 29 of 60

Discovery Community College Chapter 4 KBC - Corrections

CASE STUDY: KBC DECORATING.

In this chapter, you learned how to correct writing and recording errors, as well as how to

calculate and record GST/HST and PST. You will now apply these concepts to the entries

that have already been recorded in the General Journal; therefore, you will need to refer to

the journal entries that you recorded in Chapter 3.

KBC Decorating Co. is located in Winnipeg, Manitoba. Most goods and services bought

and sold in MA are subject to GST and PST. (For the purposes of this exercise we will

calculate GST at 5% and PST at 8%).

We will assume that a number of errors were recorded in January. For each of the following

transactions, record a reversing entry, then record the correct entry based on the new

information available.

20—

Jan. 2 Cheque #1 issued for rent was actually $2,500 plus GST.

2 Cheque #2 for advertising should have been $500+GST+PST

4 Cheque #3 for office supplies should have been $250+GST+PST

4 Cheque #4 for the new phone line should have been $165+GST+PST

5 The purchase of merchandise on the 5th, was recorded without GST.

Add GST to the values given.

9 Cheque #6 for the paint mixer and color dispenser should have been

$1,695 (including $75 GST)

10 GST and PST were not charged on the sales recorded on the 10th.

Add GST and PST to the amounts given.

15 GST and PST were not charged on the sales recorded on the 15th.

Add GST and PST to the amounts given.

After all posting is complete; prepare a trial balance on January 15

Remember to use the Trial Balance sheets from your student package that have GST Payable, GST‐ITC and PST Payable.

Discovery Community College Basic Bookkeeping, 8th Edition Page 30 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 31 of 60

Discovery Community College Chapter 5 – KBC Freight, Delivery, Duty & Brokerage

CASE STUDY: KBC DECORATING

These transactions occurred during the second half of January. Record these in the

General Journal. Be sure to account for taxes as indicated. (Remember GST=5% and PST=8%)

20—

Jan 16 Bought advertising space in the local community newspaper, $125 plus taxes. Issued Cheque #7.

16 Paid shipping costs on the merchandise bought on the 5th, $85 plus taxes. Issued Cheque #8.

17 Paid transportation cost for new paint mixer and color dispenser bought on the 9th and delivered from Toronto. Issued Cheque #9 for $81.36 (includes $3.60 GST).

20 Cash sales: paint and supplies, $2,500; wallpaper, $2,000; plus taxes.

21 Paid delivery costs for paint and supplies delivered to customer, $60 plus taxes. Cheque #10.

26 Bought paint and supplies, $8,500 plus GST. Cheque #11.

26 Paid for delivery of the paint and supplies bought today, $45 plus taxes. Cheque #12.

30 Cash sales: paint and supplies, $3,000; wallpaper, $1,000; plus taxes.

Post these entries to the ledger accounts and prepare a trial balance on January 31, 20—

Remember to use the Trial Balance sheets from your student package that have GST Payable, GST‐ITC and PST Payable.

Discovery Community College Basic Bookkeeping, 8th Edition Page 32 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 33 of 60

Discovery Community College Chapter 6 KBC – Special Journals

CASE STUDY: KBC DECORATING

February Entries

In this chapter, you learned how to use special journals to record transactions and how to post from

these special journals to the ledger accounts. KBC Decorating Co. will now begin to use special

journals: Sales Journal, Purchase Journal, Cash Receipts Journal, and Cash Payments Journal. The

company also has ledger accounts for its regular customers (Accounts Receivable Ledger) and its

suppliers (Accounts Payable Ledger). These ledger accounts are located immediately after the

General Ledger accounts that you have already been using.

Set up the Sales Journal (page SJ1) with these headings: Date, Account Dr., Invoice No., Terms,

Folio, Accounts Receivable Dr., Sales Paint & Supplies Cr., Sales Wallpaper Cr., GST Payable

Cr., and PST Payable Cr.

Set up the Purchase Journal (page PJ1) with these headings: Invoice Date, Account Cr., Invoice No.,

Terms, Folio, Accounts Payable Cr., Purchases Paint & Supplies Dr., Purchases Wallpaper Dr.,

GST-ITC Dr., and Other Accounts Dr. (with subheadings of Account Dr., Folio, and Amount).

Set up a Cash Receipts Journal with these headings: Date, Account Cr., Memo, Folio, Accounts

Receivable Cr., Sales Discounts Dr., Sales Paint & Supplies Cr., Sales Wallpaper Cr., GST

Payable Cr., PST Payable Cr., General Ledger Cr., and Bank Dr.

Set up a Cash Payments Journal with these headings: Date, Account Dr., Memo,

Folio, Accounts Payable Dr., Purchase Discounts Cr., GST-ITC Dr., General Ledger

Dr., Bank Ct., and Cheque No. (All payments will be by cheque unless otherwise stated.)

Record each of the following transactions in the appropriate special journal. Be sure each

transaction is recorded as a balanced entry. Post immediately any transaction affecting a customer's

or a supplier's account.

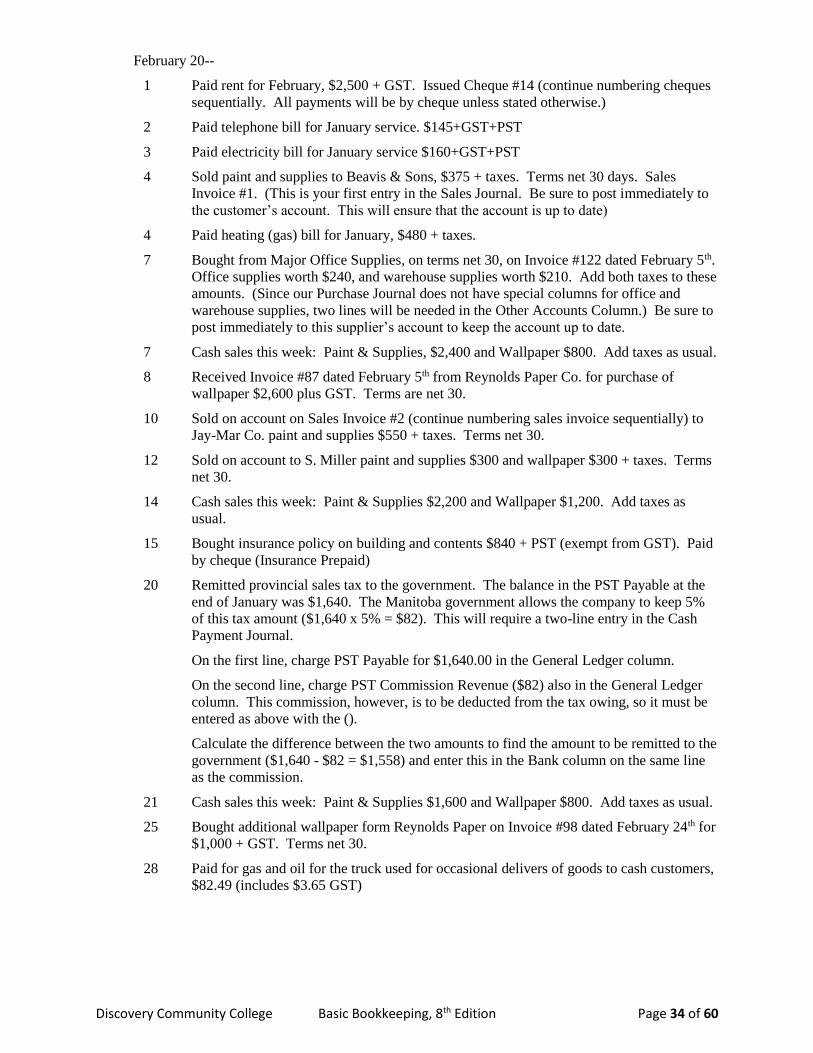

Discovery Community College Basic Bookkeeping, 8th Edition Page 34 of 60

February 20--

1 Paid rent for February, $2,500 + GST. Issued Cheque #14 (continue numbering cheques

sequentially. All payments will be by cheque unless stated otherwise.)

2 Paid telephone bill for January service. $145+GST+PST

3 Paid electricity bill for January service $160+GST+PST

4 Sold paint and supplies to Beavis & Sons, $375 + taxes. Terms net 30 days. Sales

Invoice #1. (This is your first entry in the Sales Journal. Be sure to post immediately to

the customer’s account. This will ensure that the account is up to date)

4 Paid heating (gas) bill for January, $480 + taxes.

7 Bought from Major Office Supplies, on terms net 30, on Invoice #122 dated February 5th.

Office supplies worth $240, and warehouse supplies worth $210. Add both taxes to these

amounts. (Since our Purchase Journal does not have special columns for office and

warehouse supplies, two lines will be needed in the Other Accounts Column.) Be sure to

post immediately to this supplier’s account to keep the account up to date.

7 Cash sales this week: Paint & Supplies, $2,400 and Wallpaper $800. Add taxes as usual.

8 Received Invoice #87 dated February 5th from Reynolds Paper Co. for purchase of

wallpaper $2,600 plus GST. Terms are net 30.

10 Sold on account on Sales Invoice #2 (continue numbering sales invoice sequentially) to

Jay-Mar Co. paint and supplies $550 + taxes. Terms net 30.

12 Sold on account to S. Miller paint and supplies $300 and wallpaper $300 + taxes. Terms

net 30.

14 Cash sales this week: Paint & Supplies $2,200 and Wallpaper $1,200. Add taxes as

usual.

15 Bought insurance policy on building and contents $840 + PST (exempt from GST). Paid

by cheque (Insurance Prepaid)

20 Remitted provincial sales tax to the government. The balance in the PST Payable at the

end of January was $1,640. The Manitoba government allows the company to keep 5%

of this tax amount ($1,640 x 5% = $82). This will require a two-line entry in the Cash

Payment Journal.

On the first line, charge PST Payable for $1,640.00 in the General Ledger column.

On the second line, charge PST Commission Revenue ($82) also in the General Ledger

column. This commission, however, is to be deducted from the tax owing, so it must be

entered as above with the ().

Calculate the difference between the two amounts to find the amount to be remitted to the

government ($1,640 - $82 = $1,558) and enter this in the Bank column on the same line

as the commission.

21 Cash sales this week: Paint & Supplies $1,600 and Wallpaper $800. Add taxes as usual.

25 Bought additional wallpaper form Reynolds Paper on Invoice #98 dated February 24th for

$1,000 + GST. Terms net 30.

28 Paid for gas and oil for the truck used for occasional delivers of goods to cash customers,

$82.49 (includes $3.65 GST)

Discovery Community College Basic Bookkeeping, 8th Edition Page 35 of 60

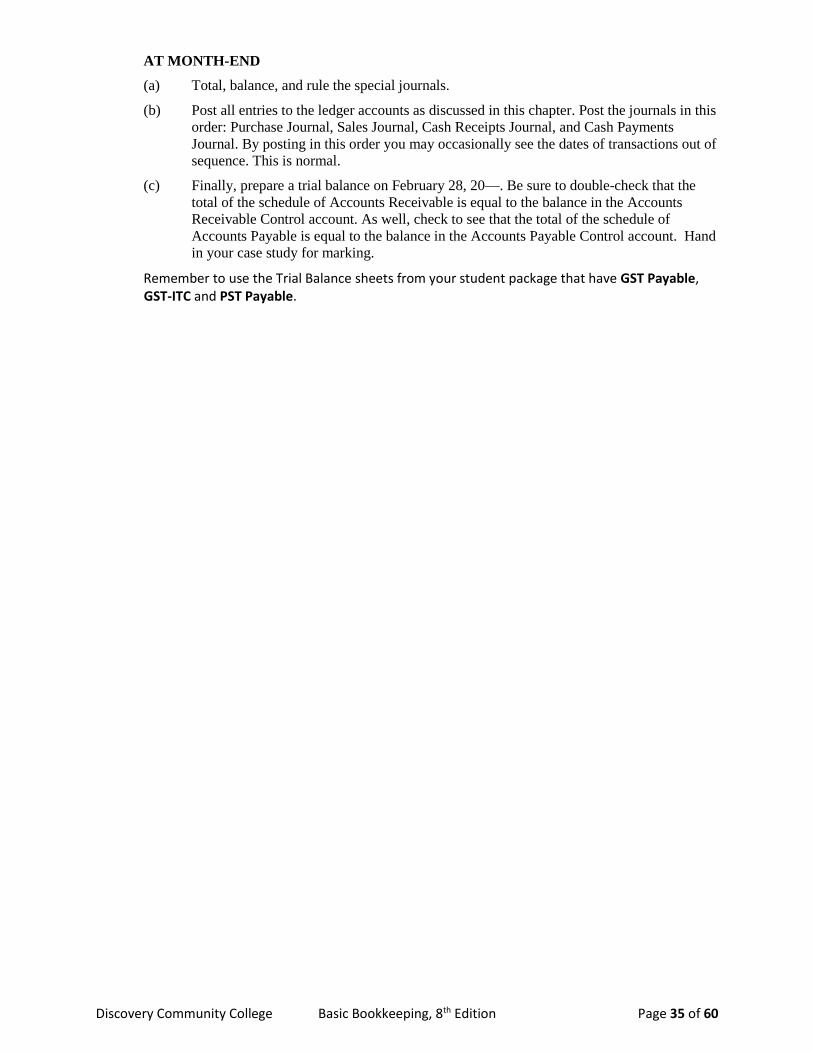

AT MONTH-END

(a) Total, balance, and rule the special journals.

(b) Post all entries to the ledger accounts as discussed in this chapter. Post the journals in this

order: Purchase Journal, Sales Journal, Cash Receipts Journal, and Cash Payments

Journal. By posting in this order you may occasionally see the dates of transactions out of

sequence. This is normal.

(c) Finally, prepare a trial balance on February 28, 20—. Be sure to double-check that the

total of the schedule of Accounts Receivable is equal to the balance in the Accounts

Receivable Control account. As well, check to see that the total of the schedule of

Accounts Payable is equal to the balance in the Accounts Payable Control account. Hand

in your case study for marking.

Remember to use the Trial Balance sheets from your student package that have GST Payable, GST‐ITC and PST Payable.

Discovery Community College Basic Bookkeeping, 8th Edition Page 36 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 37 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 38 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 39 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 40 of 60

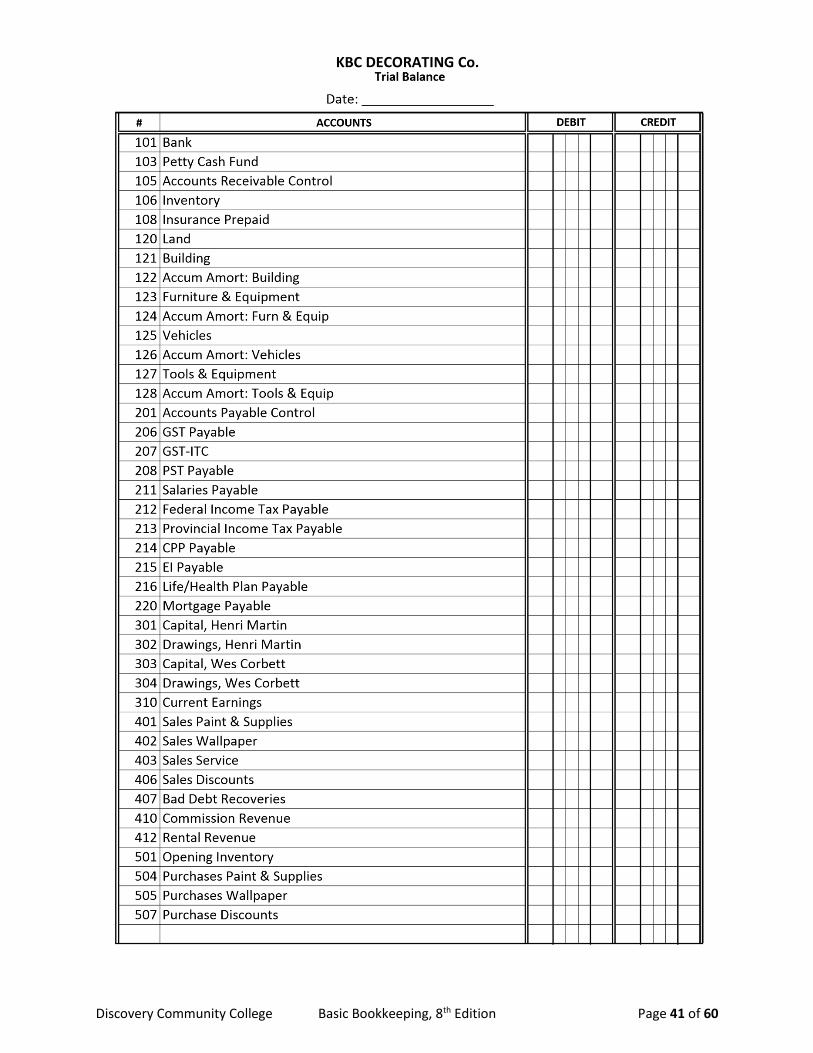

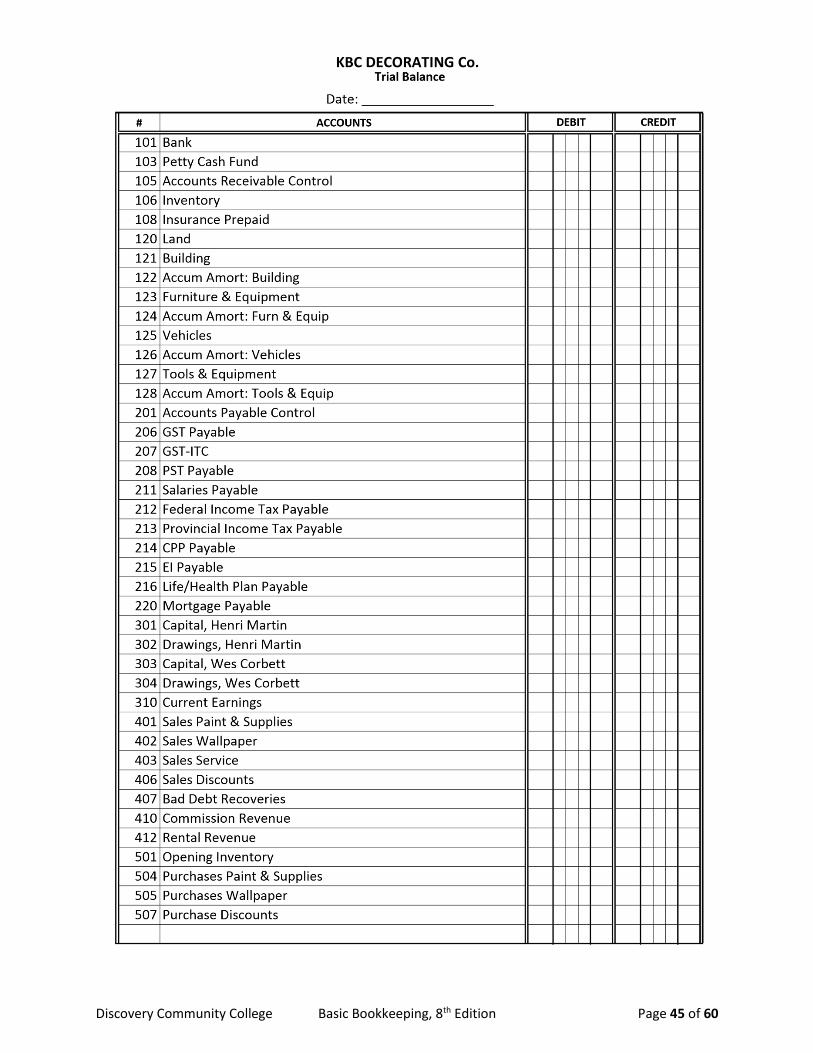

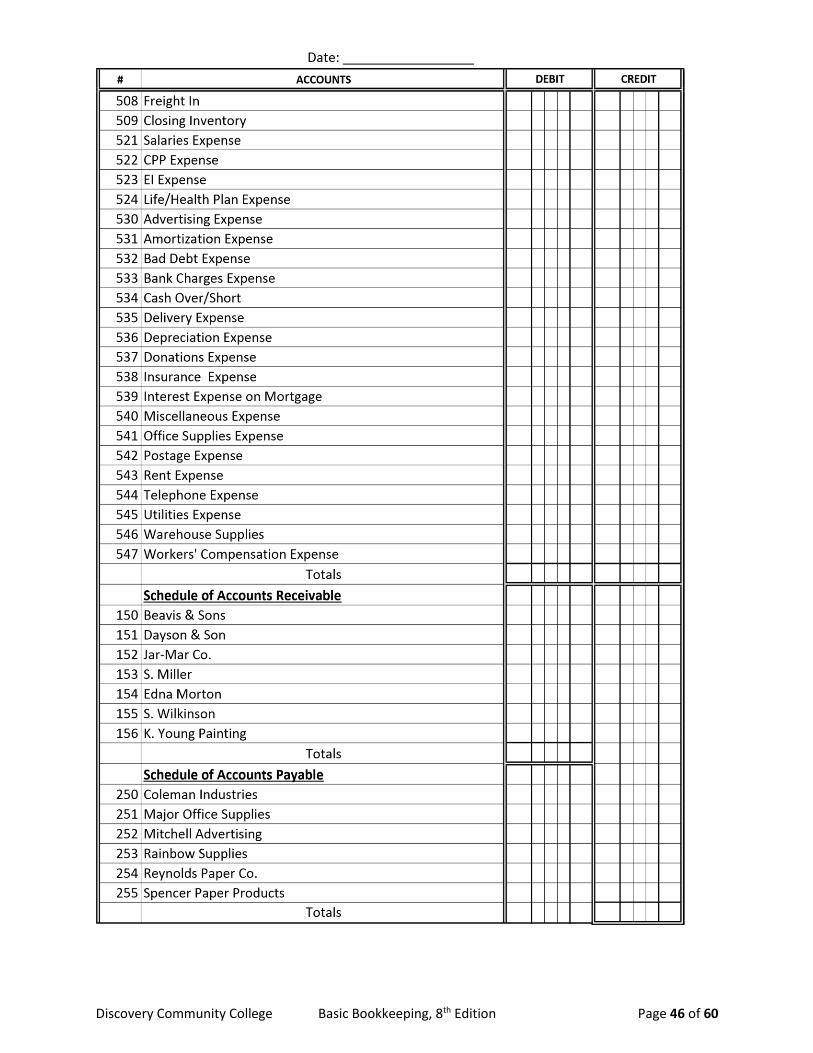

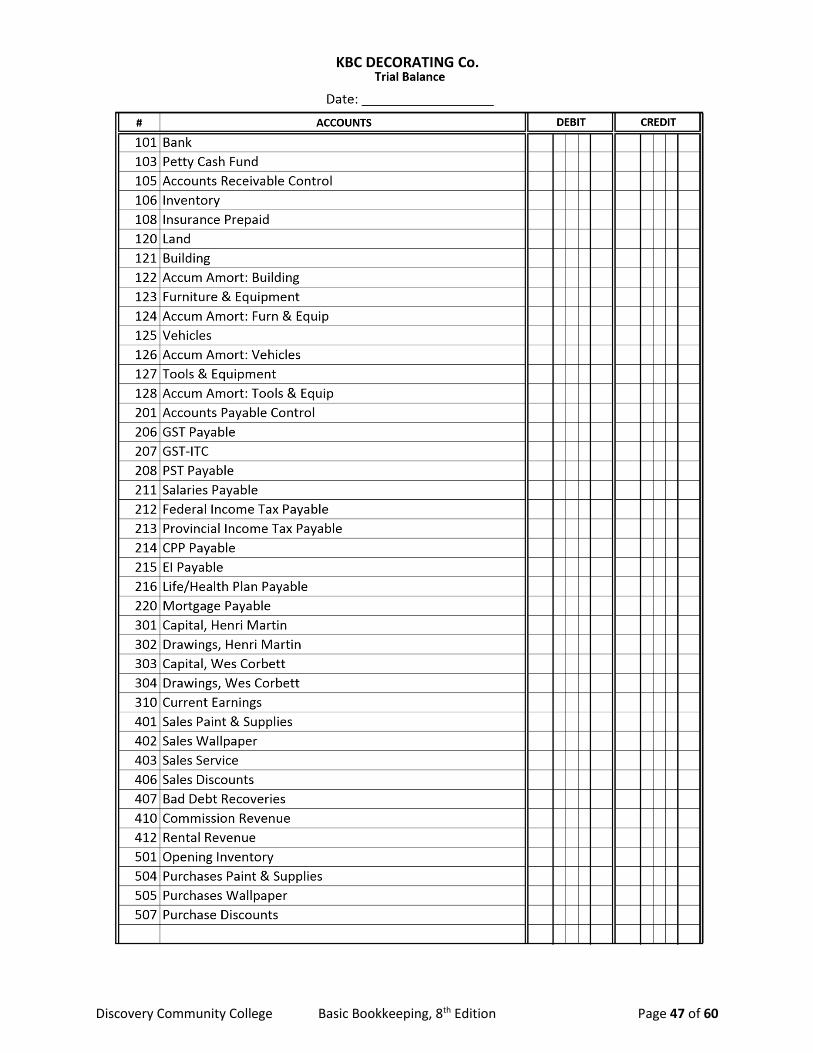

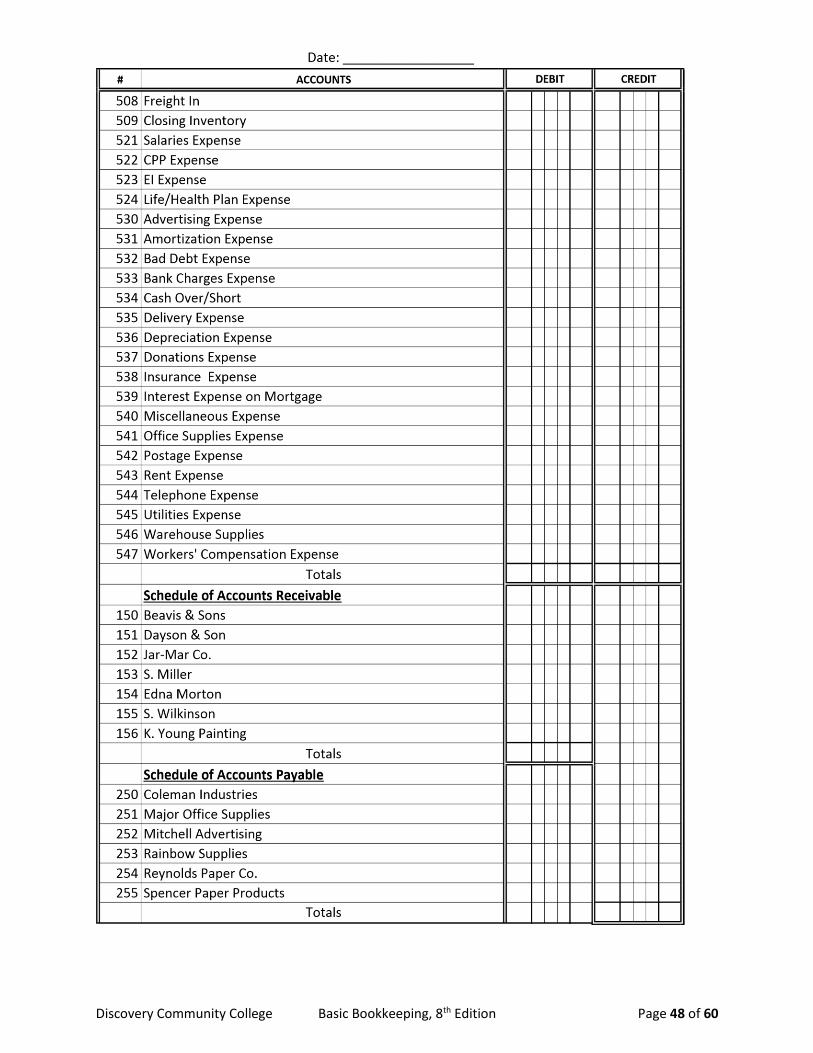

Discovery Community College Basic Bookkeeping, 8th Edition Page 41 of 60

KBC DECORATING Co.

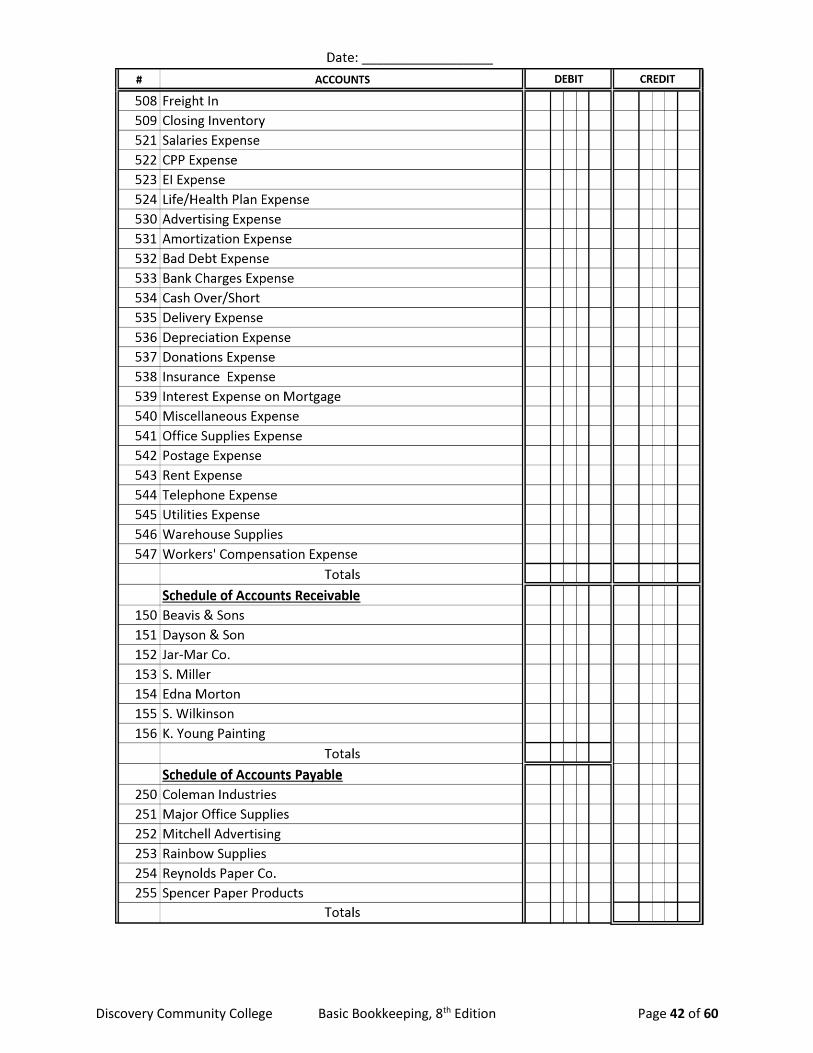

Discovery Community College Basic Bookkeeping, 8th Edition Page 42 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 43 of 60

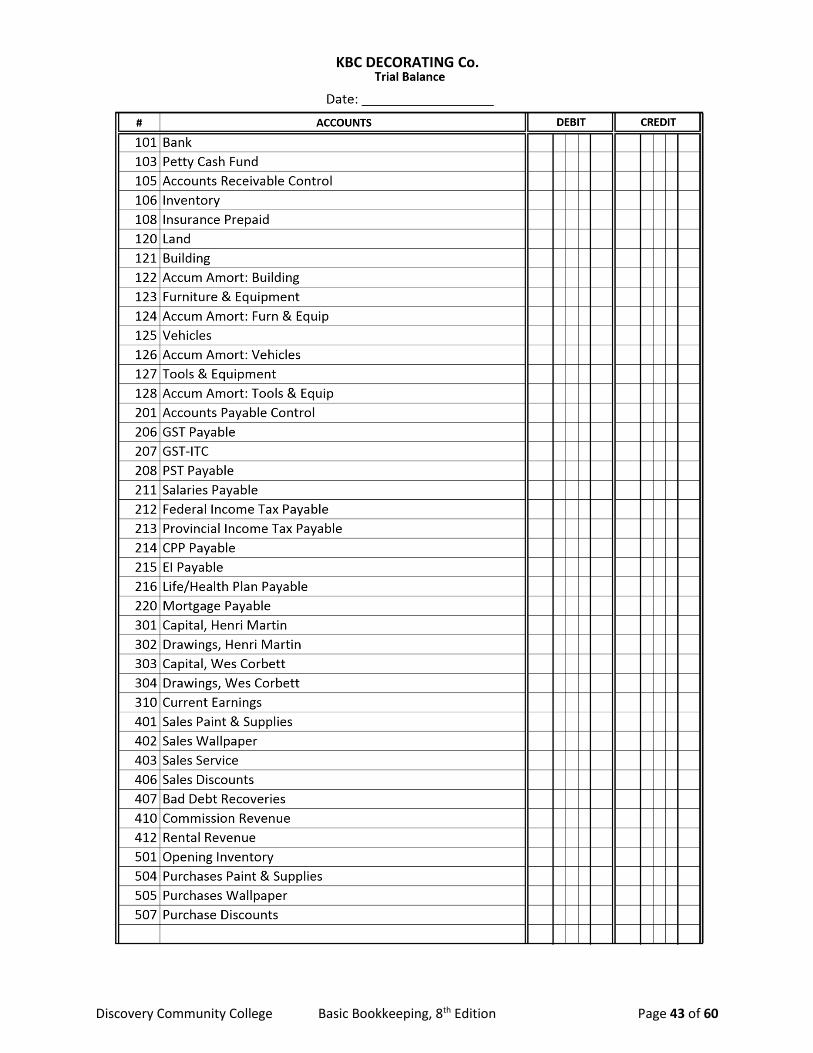

KBC DECORATING Co.

Discovery Community College Basic Bookkeeping, 8th Edition Page 44 of 60

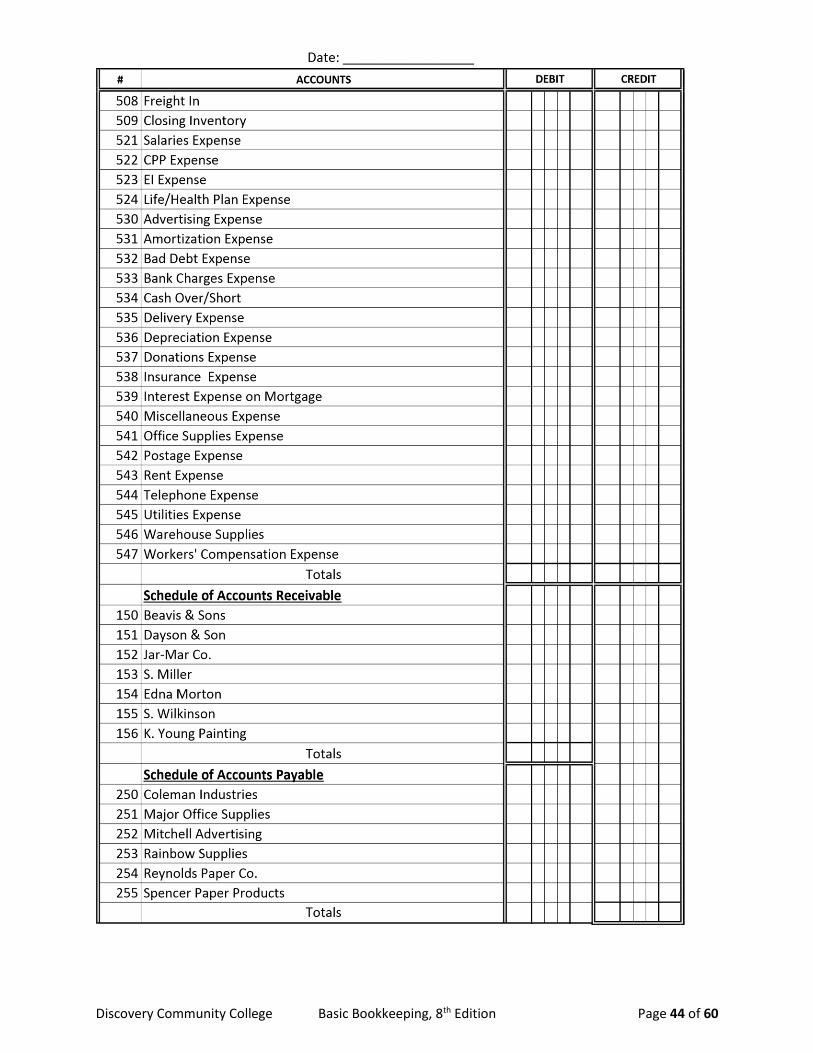

Discovery Community College Basic Bookkeeping, 8th Edition Page 45 of 60

KBC DECORATING Co.

Discovery Community College Basic Bookkeeping, 8th Edition Page 46 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 47 of 60

KBC DECORATING Co.

Discovery Community College Basic Bookkeeping, 8th Edition Page 48 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 49 of 60

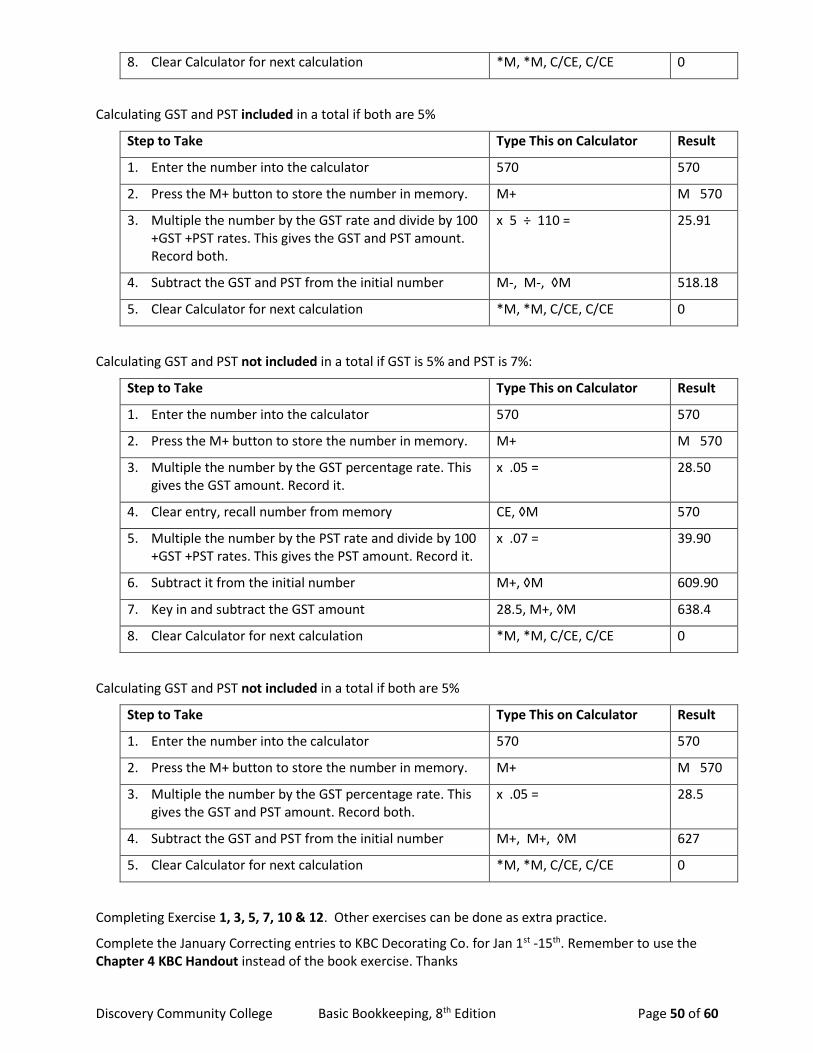

Reading Questions – Chapter 4 – Corrections Entries & Sales Taxes

1. What is the proper process for correcting a writing error in the General Journal?

2. What are the two steps in making a correcting Journal Entry after GL entries have been posted?

3. Define each of the following. Which one is not included when computing tax money returned to the business? GST: PST: HST: ITC:

4. What two accounts are used in this course to record the GST/HST paid on purchases and charged on sales?

5. How do you calculate the GST (5%) amount if there is no provincial sales tax included in the price of an item?

6. How do you calculate the GST (5%) amount if there is a provincial sales tax of 7% included in the price of an item?

Calculating GST and PST included in a total if GST is 5% and PST is 7%:

Step to Take Type This on Calculator Result

1. Enter the number into the calculator 570 570

2. Press the M+ button to store the number in memory. M+ M 570

3. Multiple the number by the PST rate and divide by 100 +GST +PST rate. This gives the PST amount. Record it.

x 7 ÷ 112 = 35.63

4. Clear entry, recall number from memory CE, ◊ M 570

5. Multiple the amount by the GST rate and divide by 100 +GST +PST rates. This gives the GST amount. Record it.

x 5 ÷ 112 = 25.45

6. Subtract it from the initial number M-, ◊M 544.55

7. Key in and subtract the PST amount 35.63, M-, ◊M 508.92

Discovery Community College Basic Bookkeeping, 8th Edition Page 50 of 60

8. Clear Calculator for next calculation *M, *M, C/CE, C/CE 0

Calculating GST and PST included in a total if both are 5%

Step to Take Type This on Calculator Result

1. Enter the number into the calculator 570 570

2. Press the M+ button to store the number in memory. M+ M 570

3. Multiple the number by the GST rate and divide by 100 +GST +PST rates. This gives the GST and PST amount. Record both.

x 5 ÷ 110 = 25.91

4. Subtract the GST and PST from the initial number M-, M-, ◊M 518.18

5. Clear Calculator for next calculation *M, *M, C/CE, C/CE 0

Calculating GST and PST not included in a total if GST is 5% and PST is 7%:

Step to Take Type This on Calculator Result

1. Enter the number into the calculator 570 570

2. Press the M+ button to store the number in memory. M+ M 570

3. Multiple the number by the GST percentage rate. This gives the GST amount. Record it.

x .05 = 28.50

4. Clear entry, recall number from memory CE, ◊M 570

5. Multiple the number by the PST rate and divide by 100 +GST +PST rates. This gives the PST amount. Record it.

x .07 = 39.90

6. Subtract it from the initial number M+, ◊M 609.90

7. Key in and subtract the GST amount 28.5, M+, ◊M 638.4

8. Clear Calculator for next calculation *M, *M, C/CE, C/CE 0

Calculating GST and PST not included in a total if both are 5%

Step to Take Type This on Calculator Result

1. Enter the number into the calculator 570 570

2. Press the M+ button to store the number in memory. M+ M 570

3. Multiple the number by the GST percentage rate. This gives the GST and PST amount. Record both.

x .05 = 28.5

4. Subtract the GST and PST from the initial number M+, M+, ◊M 627

5. Clear Calculator for next calculation *M, *M, C/CE, C/CE 0

Completing Exercise 1, 3, 5, 7, 10 & 12. Other exercises can be done as extra practice.

Complete the January Correcting entries to KBC Decorating Co. for Jan 1st -15th. Remember to use the Chapter 4 KBC Handout instead of the book exercise. Thanks

Discovery Community College Basic Bookkeeping, 8th Edition Page 51 of 60

Reading Questions – Chapter 5 – Freight In, Delivery, Brokerage

1. What is recorded in the Freight In account?

2. What is not recorded in the Freight In account?

3. Name the account used to record the cost of delivering merchandise to customers. ________________________________________________________________________________

4. What is recorded in the Duty and Brokerage account?

Complete Exercises 1 & 2.

Complete the January to KBC Decorating Co. for Jan 16th to 30th from the Ch. 5 KBC Handout Sheet in your student package and hand it in for marking.

Discovery Community College Basic Bookkeeping, 8th Edition Page 52 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 53 of 60

Reading Questions – Chapter 6 – Using Special Journals

1. What are three advantages of special journals?

2. What do each of the following journals record? Sales Journal: Cash Receipts Journal: Purchase Journal: Cash Payment Journal:

Sales Journal

3. Why are invoice numbers normally entered in numerical order in the Sales Journal?

4. What is meant by the word “Proof” with regard to a special journal and what does it prove?

5. What is an “Accounts Receivable Control” account and how is its value determined?

6. How often are the individual amounts in the Accounts Receivable Dr column posted to the individual customer ledgers?

7. How often are the totals from the four columns posted and to what accounts in the general ledger? Accounts Receivable: Sales : GST/HST Payable: Sales Tax :

Discovery Community College Basic Bookkeeping, 8th Edition Page 54 of 60

8. What is an “Accounts Payable Control” account and how is its value determined?

Cash Receipts Journal

9. What kinds of transactions are recorded in the Cash Receipts Journal?

10. Like the Purchase and Sales Journals the Cash Journal needs for each transaction and still remain balanced

11. What type of particulars should you put in the memo field?

12. What types of accounts are placed in the General Ledger Cr. column? Give two examples from Figure 6.5.

13. Entries in which column of the Cash Receipts Journal are daily posted to the customers’ accounts?

Exercises:

1. Compute the values of the two control accounts and record them below but don’t prepare a

new trial balance.

Accounts Receivable Control Value: ____________

Accounts Payable Control Value: _____________

Complete Practice #2

Discovery Community College Basic Bookkeeping, 8th Edition Page 55 of 60

14. Of all the accounts shown on the typical Cash Receipts Journal which on does not have it’s total posted to the ledger accounts? What is posted instead?

Purchase Journal

15. What is the Purchase Journal used for.?

16. What does the terms “3/10,1/20,n30” mean?

17. Entries from which two columns must be posted individually in the General Ledgers?

Cash Payments Journal

18. What kinds of transactions are recorded in the Cash Payments Journal? How should all payments be made?

19. What is recorded in the Account Dr. column?

20. Entries in which column are posted right away to the vendors ledger accounts?

Exercises:

Complete Practice #6

Exercises:

Complete Practice #15

Discovery Community College Basic Bookkeeping, 8th Edition Page 56 of 60

21. What is recorded in the Cheque No column when money is deducted directly from your bank account?

Do March Transactions for KBC – Remember to use the Ch 6-KBC handout and not the book version. This will end your work with KBC.

Exercises:

Complete Practice #18

Discovery Community College Basic Bookkeeping, 8th Edition Page 57 of 60

Reading Questions – Chapter 8 – Remitting GST/HST

1. What are the three categories at which GST/HST is charged? Give an example of each.

2. If you have annual sales of less than ____________ you are not required to collect GST/HST. If your income is ______________ or less you must file once a year. If annual sales are over the second threshold but _______________ or less you must file quarterly. Above the 3rd threshold you must file _______________.

3. Monthly and quarterly GST/HST filers have ________ month(s), while yearly filers have ___________________ month(s) to file their GST/HST returns.

4. Lines 104 and 107 of the GST/HST return deal with adjustments. What is the normal source of these adjustments?

5. What are the three ways that a GST/HST form can be remitted to the CRA?

6. What is the recommended way of handling GST-ITC remittance in the Cash Payments Journal? .

7. If you have no GST/HST to submit or refund to claim do you still have to file a return?

8. If a customer gets a discount for paying early is the GST/HST calculated on the original or the lowered price?____________________________________________________

Reading Exercise: Read over the section on the Quick Method and the Simplified Method of calculating GST/HST.

Practice Exercise: Do Exercises #1, 3 and 4 for practice and check it against the answer key.

Hand-In Exercise: Complete Exercise #2 and hand it in to your instructor for marking.

Discovery Community College Basic Bookkeeping, 8th Edition Page 58 of 60

Discovery Community College Basic Bookkeeping, 8th Edition Page 59 of 60

Reading Questions – Chapter 9 –Bank Reconciliation

1. When a company deposits all cash receipts daily and pays all accounts by cheques a double record is maintained. One record is in the bank statements where is the other?

2. What are cancelled cheques and what other information is returned with the cheques?

3. What are outstanding cheques and why are they important to the bookkeeper?

4. What is a NSF cheques and what accounting entries must we make because of a NSF cheques?

5. What is a credit memo? Give 3 examples.

6. What is a debit memo? Give 3 examples?

7. What are bank service charges? What is a Bank Reconciliation?

Discovery Community College Basic Bookkeeping, 8th Edition Page 60 of 60

8. What are the seven step one takes in doing a Bank Reconciliation? 1. 2.

3

4.

5.

6.

7.

Do Practice Exercise 6, 8 & 9

Do Exercise 10 to hand in for marks.

Please ask your instructor for your Practice Bookkeeping Final Exam.