basic economic concepts

TRANSCRIPT

Some fundamental principles

Microeconomics versus Macroeconomics

• Microeconomics is concerned with the economic decisions made by individuals, e.g. consumers, occupational groups, industries, markets.

• Micro is focused on the particular.

• Macroeconomics is concerned with the economy as a whole.

• “The whole” is typically interpreted as the nation.

Micro vs. Macro

Micro categories and examples

• Prices of particular goods.

• Theory of individualconsumer behavior.

• Employment in particularoccupations and industries.

• Choice of technology by particular firms.

• Policies that affect particular industries and markets.

Macro categories and examples

• The general level of prices.

• The general level of employment and unemployment.

• The general level of economic activity, e.g. GrossDomestic Product.

• Aggregate demand, aggregate supply.

Definition of economics.

• The definition of economics found in most textbooks is stated as a problem.

• Economics is the study of how people (individuals, nations) attempt to satisfy apparently unlimited wants, needs and desires given that they possess limited (scarce) resources.

Does this definition (problem) apply to everyone?

• Does it apply to you?

• Does it apply to the richest person in the world? Bill Gates?

• Can Bill Gates have everything? Do everything?

• Is Bill Gates constrained in any way in his allocation of resources?

• Does he face any resource constraints? Time?

Key concepts

• Scarcity

• Opportunity cost

• Allocation

– The fact that resources are scarce implies that every economic choice entails a cost.

– The fact that costs are incurred when a choice is made implies that rational decision makers require an allocation rule or mechanism to guide their decision making.

Opportunity Cost

• The opportunity cost of any economic choice is the highest-valued alternative foregone when a choice is made.

• Opportunity cost is not the sum total of allgoods and services foregone.

• Out of the menu of all alternatives foregone, the opportunity cost of a particular choice is what the choice-maker most otherwise would have preferred to have had.

What is the opportunity cost to you of taking this course?

• What do you give up when you take this course?

• Do you have alternative uses for the time and other resources you allocate to this course?

• Out of the menu of alternatives available to you to which you might dedicate these resources, which would you most otherwise prefer?

• This most-preferred alternative is your opportunity cost of this course.

• Study hard!

Allocation mechanisms.

• An allocation mechanism is a device that enables an economic decision maker to rationally allocate scarce resources to achieve some desired end or outcome.

• Economic systems are typically characterized by the nature of their allocation mechanisms.

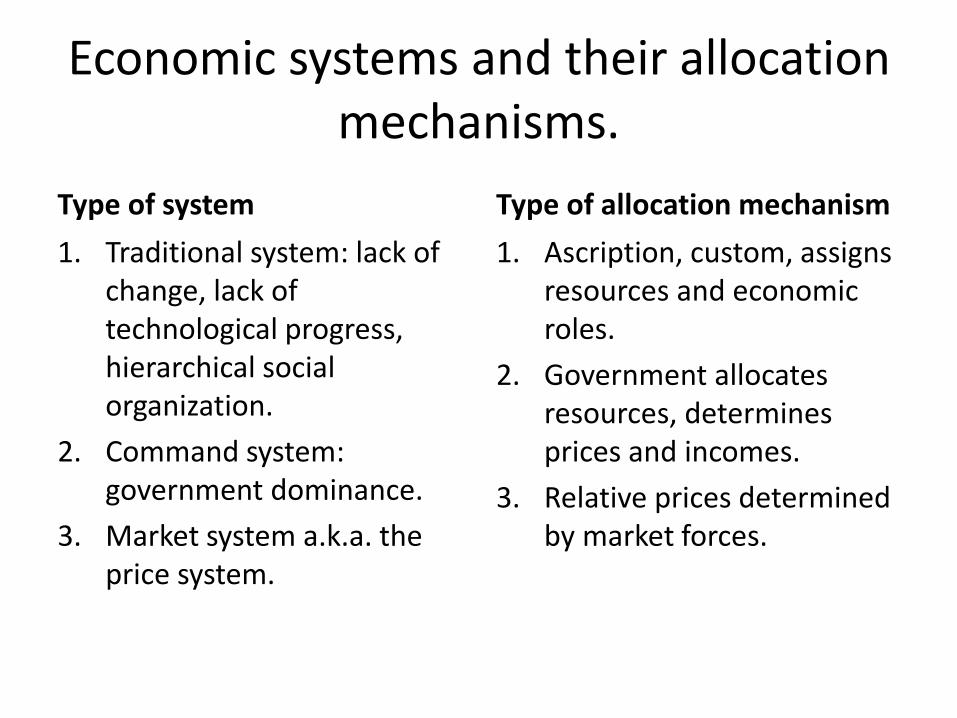

Economic systems and their allocation mechanisms.

Type of system

1. Traditional system: lack of change, lack of technological progress, hierarchical social organization.

2. Command system: government dominance.

3. Market system a.k.a. the price system.

Type of allocation mechanism

1. Ascription, custom, assigns resources and economic roles.

2. Government allocates resources, determines prices and incomes.

3. Relative prices determined by market forces.

How would you characterized the economic system of the U.S.?

• Does the U.S. have any elements of the traditional system?

• Does government play any role in the allocation of goods and services in the U.S.?

• While the U.S. is probably a “mixed” system, it is by far dominated by the market system of resource allocation.

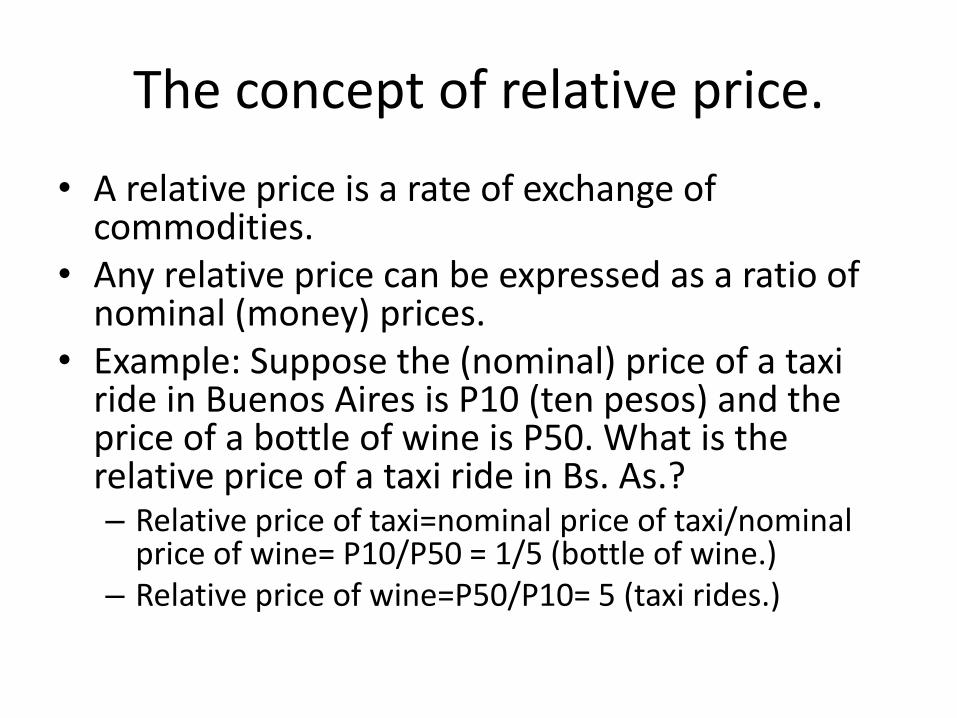

The concept of relative price.

• A relative price is a rate of exchange of commodities.

• Any relative price can be expressed as a ratio of nominal (money) prices.

• Example: Suppose the (nominal) price of a taxi ride in Buenos Aires is P10 (ten pesos) and the price of a bottle of wine is P50. What is the relative price of a taxi ride in Bs. As.?– Relative price of taxi=nominal price of taxi/nominal

price of wine= P10/P50 = 1/5 (bottle of wine.)– Relative price of wine=P50/P10= 5 (taxi rides.)

Why do economists insist on the concept of relative price?

• Relative price is the notion most akin to opportunity cost.

• What is the opportunity cost of a taxi ride in the above example? 1/5 bottle of wine.

• Relative price is the operative notion of price even in a context where we are accustomed to the currency.

• When you evaluate the price of a good priced in U.S. dollars, don’t you consider what those dollars would otherwise purchase?

3 functions of relative price.

• Incentive function.

• Signaling function.

• Rationing function.

Incentive function.

• The incentive function of price relates to the fundamental incentive associated with the market system, a.k.a. private property capitalism, to wit, PROFIT.

• Profit (π) = Total revenue (TR) – Total costs (TC).

• Total revenue = Price of output (P) x Quantity of output sold (Q).

• Total cost= Prices of productive factors (PF) x Quantity of production factors (QF).

Productive factors (an aside)

• Productive factors, a.k.a., productive resources, a.k.a., productive inputs, include the following:

– Labor or human resources, i.e. mental and physical productive abilities of people.

– Capital, i.e. physical plant, equipment, machinery, tools, etc.

– Land or natural resources, e.g. land, forests, minerals.

– Entrepreneurship, i.e. willingness and ability to combine productive enterprise in the pursuit of profit.

Incentive function (cont.)

• Write profit as π = (PxQ) – (PFxQF).

• As price increases, ceteris paribus*, profit increases, and there is a greater incentive to produce this good. Productive resources then will be allocated towards the production of this good.

• “Profit makes the world go round in private property capitalism.”

Signaling function of relative price.

• Relative prices provide decision makers with the information they need to make rational decisions.

• Suppose you were told that the average starting salary for college grads with majors in economics was $43,419 while that for finance majors was $38,024.*

• Would the relative price (wage rate) have an influence on how you allocate your scarce time and tuition dollars? Would it provide you with a “signal” as to how to decide?

Rationing function.

• The rationing function of relative price refers to the ability of price to allocate a scarce food to those most willing and able to pay.

• Suppose there are more people who want to see the Super Bowl than there is available seating in the stadium at the face value price for a ticket?

• A rising price for the ticket in the “secondary” (“black”) market for the tickets will reduce the number of people who want to pay and increase the number of people who are willing to sell.

• When the price increases to a high enough level, the number of buyers will equal the number of sellers and the good will be perfectly rationed (allocated) to those most willing to pay.

3 fundamental questions.

• Every economic system(traditional, command, market) must address itself to 3 fundamental questions that allocation issues.

• The market system addresses these questions via the relative price mechanism.

• The questions are:– What to produce?

– How to produce?

– How to distribute (allocate) output/income?

What to produce?

• What should be the composition of output? How should it be divided between consumption goods versus capital goods? How should it be divided between necessary goods and luxury goods?

• In private property capitalism the answer to these questions is provided by relative prices, which in turn determine relative profitability.

• Why does our pharmaceutical industry provide several treatments for male pattern baldness, but very no effective treatment for malaria?

How to produce?

• This question asks which productive technique, i.e. combination of productive factors, should be used to produce a particular output.

• The answer involves relative prices of productive factors.

• If firms wish to increase profits, they must minimize costs of production. (Recall the profit equation!)

• To minimize total costs firms will those techniques that involve relatively cheap productive inputs.

How to distribute output/income?

• Why does Peyton Manning have so much more stuff than I do?!

• (Because his income is higher, dummy!)

• Why is his income higher?!

• (Because the relative wage for elite football talent is much greater that that for mediocre economics teaching talent, idiot!)

• Oh, right! It comes down to relative price, again.