bayesian estimation with dynare · pdf fileintroduction likelihood posterior mcmc estimating...

TRANSCRIPT

Introduction Likelihood Posterior MCMC Estimating in Dynare

Bayesian Estimation with Dynare

Colin Caines

UBC

March 4, 2016

Introduction Likelihood Posterior MCMC Estimating in Dynare

Overview

• Can we use information in model solution to estimate parameters?

• Does the data tell us about more than just the mode?

• Can we compute P(q |X ), the distribution of parameters q given data?

Introduction Likelihood Posterior MCMC Estimating in Dynare

Bayes Law for Posterior

• Given P(q) and data X

P(q |X ) =P(X |q) ·P(q)R

P(X |q 0)P(q 0)dq 0

- P(q |X ) is posterior distribution- P(q) is prior distribution, this is a choice- P(X |q) is likelihood function, comes from model solution-

RP(X |q 0)P(q 0)dq 0 is normalization constant

=) P(q |X ) µ L(X |q) ·P(q)

Introduction Likelihood Posterior MCMC Estimating in Dynare

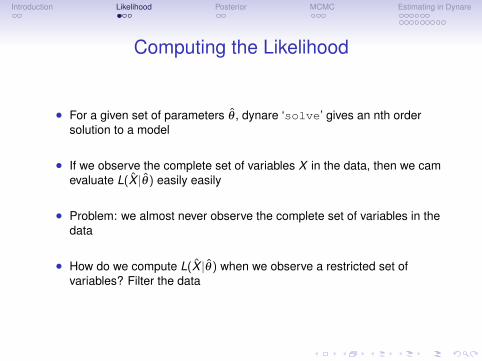

Computing the Likelihood

• For a given set of parameters q , dynare ‘solve’ gives an nth ordersolution to a model

• If we observe the complete set of variables X in the data, then we camevaluate L(X |q) easily easily

• Problem: we almost never observe the complete set of variables in thedata

• How do we compute L(X |q) when we observe a restricted set ofvariables? Filter the data

Introduction Likelihood Posterior MCMC Estimating in Dynare

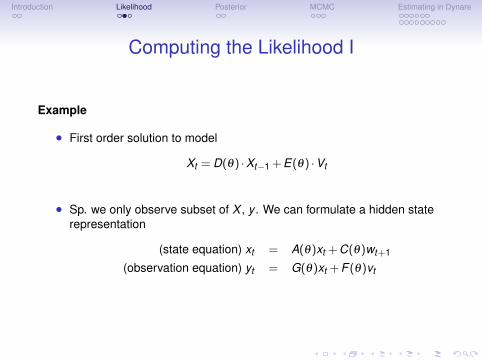

Computing the Likelihood I

Example

• First order solution to model

X

t

= D(q) ·Xt�1 +E(q) ·V

t

• Sp. we only observe subset of X , y . We can formulate a hidden staterepresentation

(state equation) x

t

= A(q)xt

+C(q)wt+1

(observation equation) y

t

= G(q)xt

+F (q)vt

Introduction Likelihood Posterior MCMC Estimating in Dynare

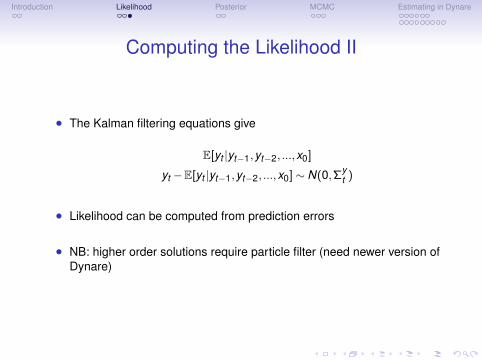

Computing the Likelihood II

• The Kalman filtering equations give

E[yt

|yt�1,yt�2, ...,x0]

y

t

�E[yt

|yt�1,yt�2, ...,x0]⇠ N(0,⌃y

t

)

• Likelihood can be computed from prediction errors

• NB: higher order solutions require particle filter (need newer version ofDynare)

Introduction Likelihood Posterior MCMC Estimating in Dynare

Computing the Posterior

=) P(q |X ) µ L(X |q) ·P(q)

• Given a choice of q we can easliy calculate P(q |X )

• We can (usually) find maxq P(q |X ) via numerical methods withoutmuch difficulty

- NB: P(q) smoothes the posterior, makes maximization easier

• In general P(q |X ) is an extremely complex object

Introduction Likelihood Posterior MCMC Estimating in Dynare

Drawing from the Posterior

• We are usually interested in calculating objects like

E[g(q)] =R

g(q)P(q |X )dqRP(q |X )dq

- ie. mean, standard deviation, condifence intervals

• Problem: P(q |X ) is too complex to draw from

- Solution: draw from a simple distribution that looks like P(q |X )

Introduction Likelihood Posterior MCMC Estimating in Dynare

Markov Chain Monte Carlo (MCMC) Method

Metropolis-Hastings Algorithm

• Use a simple heuristic to generate a Markov chain q such that thedistribution of q converges to P(q |X )

Algorithm

1. Choose initial draw q0

2. For each iteration t

- Generate candidate draw q⇤ by drawing from N(qt�1,s

mh

)

- Calculate acception ratio a = P(q⇤|X )/P(qt�1|X )

- If a � 1 set qt

= q⇤

- If a < 1 set qt

= q⇤ with probability a (generate new draw if notaccepted)

Introduction Likelihood Posterior MCMC Estimating in Dynare

MCMC, MH Algorithm

• Choice of smh

will determine the overall acception ratio

• Brooks & Gellman (1997): optimum acception ratio 0.234

• Should generate multiple sequences

• Sequences should behave as if drawn from P(q |X ), at a minimum thedistribution:

- Should be the same for different parts of same sequence- Should be the same for same parts of different sequences

Introduction Likelihood Posterior MCMC Estimating in Dynare

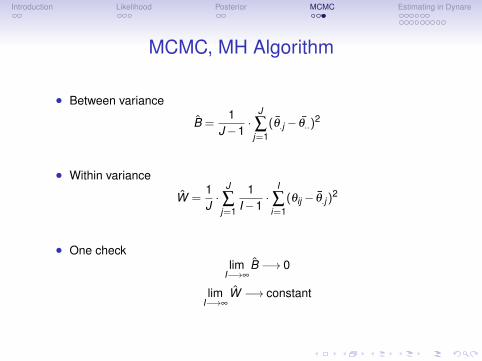

MCMC, MH Algorithm

• Between variance

B =1

J �1·

J

Âj=1

(q.j � q..)2

• Within variance

W =1J

·J

Âj=1

1I �1

·I

Âi=1

(qij

� q.j )2

• One checklim

I�!•B �! 0

limI�!•

W �! constant

Introduction Likelihood Posterior MCMC Estimating in Dynare

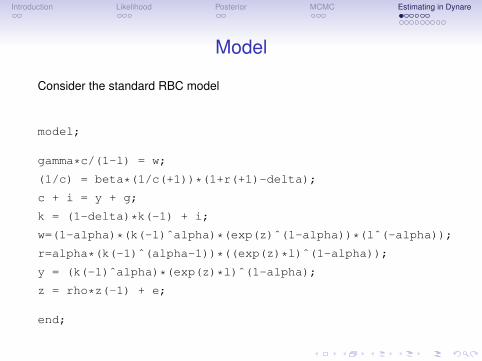

Model

Consider the standard RBC model

model;

gamma*c/(1-l) = w;

(1/c) = beta*(1/c(+1))*(1+r(+1)-delta);

c + i = y + g;

k = (1-delta)*k(-1) + i;

w=(1-alpha)*(k(-1)ˆalpha)*(exp(z)ˆ(1-alpha))*(lˆ(-alpha));

r=alpha*(k(-1)ˆ(alpha-1))*((exp(z)*l)ˆ(1-alpha));

y = (k(-1)ˆalpha)*(exp(z)*l)ˆ(1-alpha);

z = rho*z(-1) + e;

end;

Introduction Likelihood Posterior MCMC Estimating in Dynare

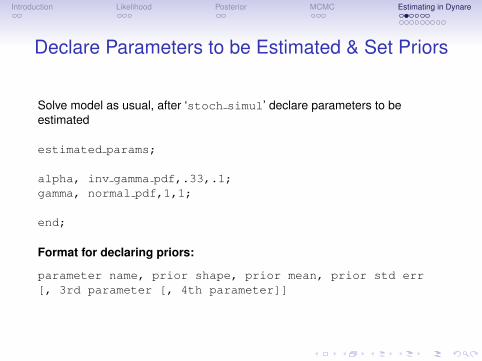

Declare Parameters to be Estimated & Set Priors

Solve model as usual, after ‘stoch simul’ declare parameters to beestimated

estimated params;

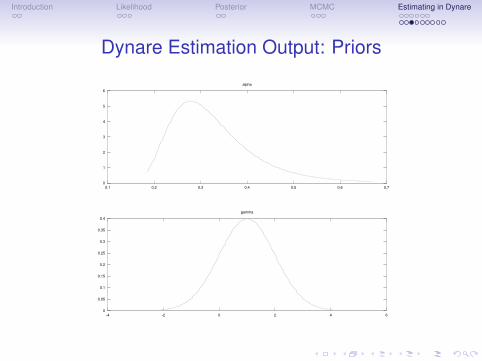

alpha, inv gamma pdf,.33,.1;gamma, normal pdf,1,1;

end;

Format for declaring priors:

parameter name, prior shape, prior mean, prior std err[, 3rd parameter [, 4th parameter]]

Introduction Likelihood Posterior MCMC Estimating in Dynare

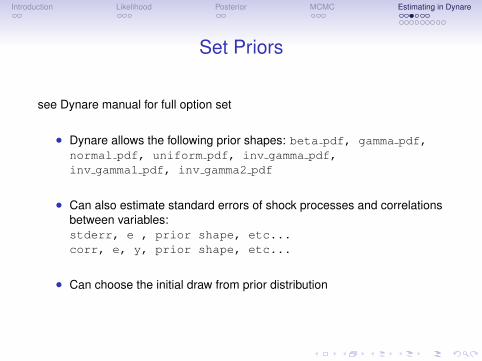

Set Priors

see Dynare manual for full option set

• Dynare allows the following prior shapes: beta pdf, gamma pdf,normal pdf, uniform pdf, inv gamma pdf,inv gamma1 pdf, inv gamma2 pdf

• Can also estimate standard errors of shock processes and correlationsbetween variables:stderr, e , prior shape, etc...corr, e, y, prior shape, etc...

• Can choose the initial draw from prior distribution

Introduction Likelihood Posterior MCMC Estimating in Dynare

Set observable variables

After estimated params block set variables that are observable:

varobs y;

• Cannot have more observed variables than shocks in your model

• Can estimate more parameters than observed variables, butidentification tends to be difficult

• Should try to avoid using data series that are highly correlated

Introduction Likelihood Posterior MCMC Estimating in Dynare

Estimation

Estimation command:

estimation(datafile=z ycildata,mh nblocks=5,mh replic=10000,mh jscale=.5);

You must have data file in the search path

• Dynare can read .m, .mat, or .xls files• File must have variable names at the begining of columns, names must

match variable names in mod file• Dynare can filter data before estimation (‘prefilter=1’)

Introduction Likelihood Posterior MCMC Estimating in Dynare

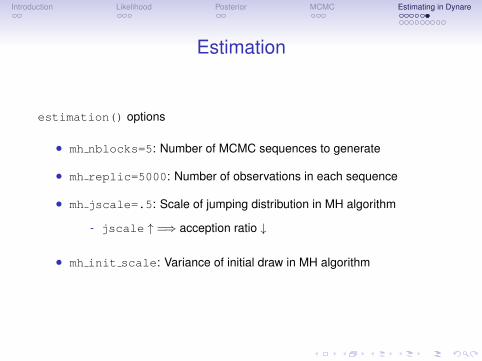

Estimation

estimation() options

• mh nblocks=5: Number of MCMC sequences to generate

• mh replic=5000: Number of observations in each sequence

• mh jscale=.5: Scale of jumping distribution in MH algorithm

- jscale " =) acception ratio #

• mh init scale: Variance of initial draw in MH algorithm

Introduction Likelihood Posterior MCMC Estimating in Dynare

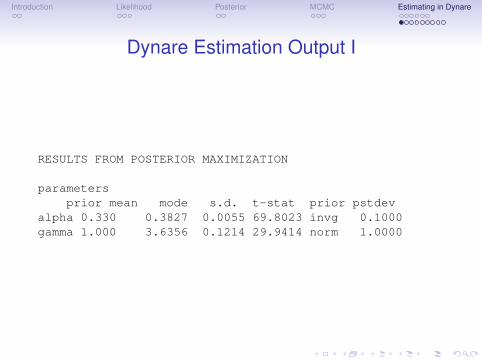

Dynare Estimation Output I

RESULTS FROM POSTERIOR MAXIMIZATION

parametersprior mean mode s.d. t-stat prior pstdev

alpha 0.330 0.3827 0.0055 69.8023 invg 0.1000gamma 1.000 3.6356 0.1214 29.9414 norm 1.0000

Introduction Likelihood Posterior MCMC Estimating in Dynare

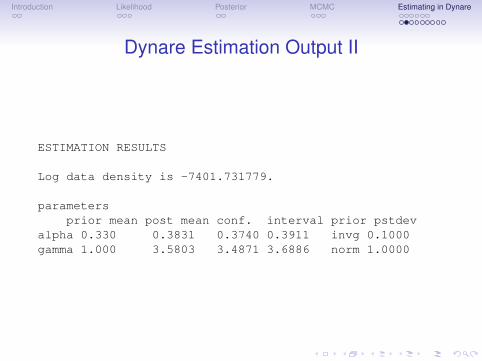

Dynare Estimation Output II

ESTIMATION RESULTS

Log data density is -7401.731779.

parametersprior mean post mean conf. interval prior pstdev

alpha 0.330 0.3831 0.3740 0.3911 invg 0.1000gamma 1.000 3.5803 3.4871 3.6886 norm 1.0000

Introduction Likelihood Posterior MCMC Estimating in Dynare

Dynare Estimation Output: Priors

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

-4 -2 0 2 4 6

gamma

0

1

2

3

4

5

6

0.1 0.2 0.3 0.4 0.5 0.6 0.7

alpha

Introduction Likelihood Posterior MCMC Estimating in Dynare

Dynare Estimation Output: Posterior

• Want to see some evidence that your estimater posterior is not beingdriven by your choice of prior

Introduction Likelihood Posterior MCMC Estimating in Dynare

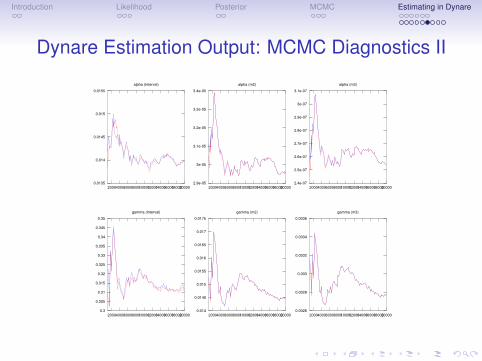

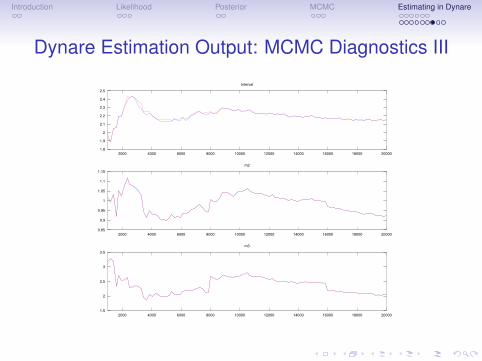

Dynare Estimation Output: MCMC Diagnostics I

Dynare computes 3 sets of MCMC statistics from Brooks & Gelman (1998)

1. Interval: Mean

2. M2: Variance

3. M3: Skewness

For each of these, dynare computes a statistic related to the within-sequencevalue of each of these (red) and essentially a sum of the within-sequencestatistic and a between-sequence variance (blue)

=) Want the red and blue to converge and to settle down

Also computes multivariate versions of these statistics

Introduction Likelihood Posterior MCMC Estimating in Dynare

Dynare Estimation Output: MCMC Diagnostics II

0.0026

0.0028

0.003

0.0032

0.0034

0.0036

2000400060008000100001200014000160001800020000

gamma (m3)

0.014

0.0145

0.015

0.0155

0.016

0.0165

0.017

0.0175

2000400060008000100001200014000160001800020000

gamma (m2)

0.3

0.305

0.31

0.315

0.32

0.325

0.33

0.335

0.34

0.345

0.35

2000400060008000100001200014000160001800020000

gamma (Interval)

2.4e-07

2.5e-07

2.6e-07

2.7e-07

2.8e-07

2.9e-07

3e-07

3.1e-07

2000400060008000100001200014000160001800020000

alpha (m3)

2.9e-05

3e-05

3.1e-05

3.2e-05

3.3e-05

3.4e-05

2000400060008000100001200014000160001800020000

alpha (m2)

0.0135

0.014

0.0145

0.015

0.0155

2000400060008000100001200014000160001800020000

alpha (Interval)

Introduction Likelihood Posterior MCMC Estimating in Dynare

Dynare Estimation Output: MCMC Diagnostics III

1.5

2

2.5

3

3.5

2000 4000 6000 8000 10000 12000 14000 16000 18000 20000

m3

0.85

0.9

0.95

1

1.05

1.1

1.15

2000 4000 6000 8000 10000 12000 14000 16000 18000 20000

m2

1.8

1.9

2

2.1

2.2

2.3

2.4

2.5

2000 4000 6000 8000 10000 12000 14000 16000 18000 20000

Interval

Introduction Likelihood Posterior MCMC Estimating in Dynare

Bayesian IRF

estimation(...,bayesian irf) varlist

• will compute the Bayesian IRFS of all variables in varlist

• results stored in structure oo .PosteriorIRF.dsge

Introduction Likelihood Posterior MCMC Estimating in Dynare

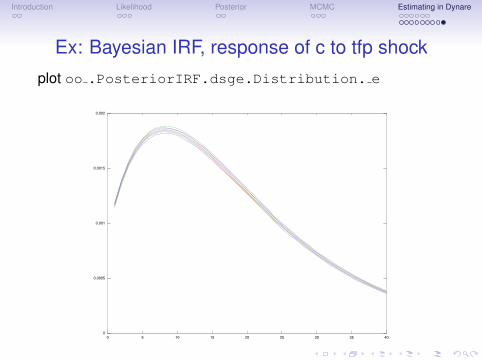

Ex: Bayesian IRF, response of c to tfp shockplot oo .PosteriorIRF.dsge.Distribution. e

0

0.0005

0.001

0.0015

0.002

0 5 10 15 20 25 30 35 40