bbc all radio reportdownloads.bbc.co.uk/radio/commissioning/bbc_radio_rajar_summ… · contents bbc...

TRANSCRIPT

BBC All Radio Report Quarter 3 2017

Alison Winter

Head of Audiences, BBC Radio & Education

26th October 2017

Contents

BBC RADIO

13.3 13 13.7

15.6 15.5 15.3

UK Radio Q3 2017: At a glance

2

Reach (000’s)

9,697 15,357 1,963 11,217 5,067 2,430 1,082 1,643 2,153 662 1,492 35,559 5,433 2,926 4,501

Key metrics against All Radio, BBC Radio & Commercial Radio

Share Key metrics for digital platforms at an all radio level

90.1% All radio 100%

71.9% AM/FM 51.2%

61.1% All digital 48.8%

48.1% DAB 35.9%

14.6% DTV 4.9%

18.3% Online \ apps 8%

Weekly reach (%) Share (%)

ALL RADIO

49,076 90.1% 21.3 1,046m

Reach

(000’s)

Reach

%)

Avg hours

per listener

Total hours

(m)

Weekly Hours

ALL BBC

34,853 64% 15.6 545m

Reach

(000’s)

Reach

%)

Avg hours

per listener

Total hours

(m)

Weekly Hours

ALL COMMERCIAL

35,559 65.3% 13.3 474m

Reach

(000’s)

Reach

%)

Avg hours

per listener

Total hours

(m)

Weekly Hours

AHPL

51.5% Sept16 45.8%

52.3% Jun1

7 45.0%

52.1% Sept17 45.3%

BBC Share All Commercial Share

Sept 17 June 17 Sept 16

BBC AHPL

Commercial

AHPL

All

Comm-

ercial

Contents

BBC RADIO

A statistically flat quarter sees strong reach figures maintained across both sides of the industry

3

Source: RAJAR / Ipsos MORI / RSMB

Last quarter’s highest ever (000s) reach for UK

Radio is more or less maintained this time

round, with only a (directional) dip down on

the quarter to 49.1m, or 90.1% of the 15+

population. This represents a statistically

significant rise on the year of 911k/2%. On top

of which, average hours increase slightly on

the quarter, adding 19mins QoQ to 21h19m

per week per listener. All of which means total

live radio hours consumed every week remain

in excess of 1 billion.

BBC Radio has a statistically steady quarter –

shifting no more than 0.3% on either period, to

reach just shy of 35m at 34.85m/64% (versus a

1718 target of 35m/65%). AHPL nudge up on

both periods to exceed (just!) the divisional

target of 15h36m per listener, at 15h38m.

Commercial Radio, too, sees no significant

shifts this quarter so stays above BBC in terms

of reach – but slight movements on both sides

mean the reach gap narrows from 936k to

706k. Q2 saw a highest ever reach for Comm

Radio and this quarter’s figure of 35.56m is

their 3rd highest. AHPL are up 23m QoQ but

down 21mins YoY to 13h20m per listener.

Sept 16 June 17 Sept 17 QoQ YoY

ALL

RA

DIO

Weekly reach (000s) 48,165 49,206 49,076

p

Weekly reach (%) 89.1 90.3 90.1

p

Average hours per listener 21.54 21 21.32

Total hours (millions) 1,038 1,033 1,046

ALL

BB

C

Weekly reach (000s) 34,823 34,945 34,853

Weekly reach (%) 64.5 64.2 64

Average hours per listener 15.34 15.45 15.64

Total hours (millions) 534 540 545

ALL

CO

MM

ER

CIA

L

Weekly reach (000s) 34,762 35,881 35,559

Weekly reach (%) 64.3 65.9 65.3

Average hours per listener 13.68 12.95 13.34

Total hours (millions) 476 465 474

Contents

BBC RADIO

4

Q3 2016 Q2 2017 Q3 2017 Q3 2016 Q2 2017 Q3 2017

BBC Reach 4258.5 4241.7 4232.6 Reach 4831.4 4927.9 4913

Reach (%) 53.2 53.4 53.3 Reach (%) 54.1 54.5 54.4

Share 31.4 33.7 33.4 Share 34.7 37.6 34.2

AHPL 7.2 7.3 7.4 AHPL 10.1 10.4 9.9

CR Reach 5640.5 5783.2 5550.9 Reach 6318.1 6520.5 6607.8

Reach (%) 70.5 72.8 69.9 Reach (%) 70.8 72.2 73.1

Share 65.4 63 61.9 Share 61.9 58.5 62.1

AHPL 11.3 10 10.4 AHPL 13.8 12.2 13.3

BBC Reach 14247.9 14249 14101.9 Reach 20575.2 20695.9 20750.7

Reach (%) 56.4 56.2 55.7 Reach (%) 71.5 71 71.2

Share 36.7 38 35.9 Share 60.7 60.6 61.5

AHPL 10.3 10.2 9.8 AHPL 18.9 19.1 19.6

CR Reach 18096.1 18510 18366.6 Reach 16665.6 17370.6 17192.6

Reach (%) 71.6 73.1 72.5 Reach (%) 57.9 59.6 59

Share 59.8 58.3 60.5 Share 37.1 37.2 36.5

AHPL 13.2 12 12.7 AHPL 14.2 14 14

15-24 25-34

15-44 45+

15-44 reach is just shy of the 1718 target: 55.7%

listen every week, versus 55.9%; and they listen

for an average of 9.8 hours which, again, is

short of the 10.2 1718 target. This is also the first

time AHPL among this age-group have slipped

below 10, and contributes to a record low

share for BBC Radio of 35.9%, versus a new

high for Commercial Radio of 60.5% (their first

time over 60%).

And almost all BBC stations have contributed

to this shift: Radio 2 loses 35-44s but posts

record reach among 55+s; Radio 4 sees its

lowest reach among ABC1 35-54s since 2009,

while posting the joint highest reach among

65+s; and 6 Music sees growth across the

board but it’s more marked among 45-54s

who see a record reach in Q3.

BBC Radio loses out among younger listeners at Q3 17, as AHPL among 15-44s slip below 10 for the first time ever

Contents

BBC RADIO Record share (just!) again for digital radio in Q3

Weekly Reach (%) Total Hour (millions) Share (%)

Sept 16 June 17 Sept 17 Sept 16 June 17 Sept 17 Sept 16 June 17 Sept 17

All radio 89.1 90.3 90.1 1,038 1,033 1,046 100 100 100

All digital 59 61.2 61.1 472 503 511 45.5 48.7 48.8

DAB 44.8 47.5 48.1 336 357 376 32.3 34.5 35.9

DTV 14.7 14.7 14.6 53 56 51 5.2 5.4 4.9

Online\apps 18.7 19.6 18.3 83 91 83 8 8.8 8

Digital unspecified* 0 0 0 0 0 0 0 0 0

5

Source: RAJAR / Ipsos MORI / RSMB

• On the back of last quarter’s 1.5%pt rise for digital share, this quarter sees a more modest increase of 0.1% which is nevertheless

enough to report a record digital radio share of 48.8% - only 1.2%pts away from the 50% threshold. Within that, DAB is the real driver,

up to 34.9%, while Online falls back once more (to 8% overall, but up to 18% among 16-24s vs. 2% for 65+s). 61.1% of adults listen to

the radio digitally every week, and over half a billion hours are digital. Demographically, 15-54s are now on, or over, 50% digital

share but among 65+s its a low 40.9%. There is also record share of digital listening in work at 53.3%; only in-car is now below the 50%

threshold at 30.9% digital hours.

• A steady 4.7m (8.6%) of UK adults listen to podcasts every week. There has also been a record among 25+s who claimed mobile

listening this quarter, up to 21% (vs 22.1% of all adults and 28.8% of 15-24s).

Contents

BBC RADIO Record reach for 6 Music, closing in on 2.5m ….

6

Source: RAJAR / Ipsos MORI / RSMB

Sept 16 June 17 Sept 17

34,823 34,945 34,853

64.5 64.2 64

All BBC Network radio

32,107 32,136 32,110

59.4 59 59

9,873 9,586 9,697

18.3 17.6 17.8

15,144 14,884 15,357

28 27.3 28.2

1,977 2,062 1,963

3.7 3.8 3.6

11,227 11,551 11,217

20.8 21.2 20.6

5,502 5,317 5,067

10.2 9.8 9.3

5,975 5,631 5,578

11.1 10.3 10.2

8,429 8,632 8,249

15.6 15.8 15.1

11,632 11,923 11,656

21.5 21.9 21.4

Weekly Reach (000s)

(%) Sept 16 June 17 Sept 17

1,601 1,246 1,643

3 2.3 3

2,342 2,235 2,430

4.3 4.1 4.5

1,026 1,031 1,082

1.9 1.9 2

2,043 2,093 2,153

3.8 3.8 4

1,537 1,593 1,492

2.8 2.9 2.7

662 646 662

1.2 1.2 1.2

An unremarkable quarter, at a station level. The star, though, is 6 Music, which delivers a record, on the back of a slight dip last time round, to 2.4m. This consolidates its position as the UK’s biggest digital-only brand, despite 4Extra’s rise on both periods to 2.15m, and alongside period on period rises for ARIA National Station of the Year 1Xtra (1.1m, its highest since Q414) and 5live sports extra (second highest reach of 1.6m, driven by a statistical shift upwards, thanks to a LOT of cricket). Asian Network, too, is directionally up QoQ and rock-solid YoY at 662k. Apart from that, its pretty steady – Radio 1 sees a second directional rise, but is down on the year, to 9.7m; Radio 2 is up on both periods and – crucially- recovers from its sub 15m dip to 15.4m; Radio 3 is down on both periods – somewhat disappointingly in a Proms quarter; and Radio 4 is steady to stay above 11m for the 6th quarter in a row. In fact the only significant shift down is for 5 live, which edged closer to 5m, at 5.1m (losing 435k/8.6% on the year). ELR sees directional declines on both periods to 8.2m, as does World Service to 1.5m

QoQ YoY

q

q

QoQ YoY

p

Contents

BBC RADIO Narrowing of share gap between BBC and Commercial once more to 6.8%pts

7

Source: RAJAR / Ipsos MORI / RSMB

Overall, the BBC and Commercial share

gap narrows once more - as the BBC

nudges down on the quarter (0.2%points) to

52.1% and Commercial nudges up (0.3%

points) to 45.3% – to 6.8% points, which is the

narrowest since Q3 last year.

Within this, Radio 2 share is at its highest

level since Q4 15, at 17.5%, while all others

are broadly steady.

(%) Sept 16 June 17 Sept 17 QoQ YoY

51.5 52.3 52.1

All BBC Network

radio 44.4 45.0 45.2

6.0 6.2 5.9

16.7 16.8 17.5 p

1.2 1.2 1.1

11.8 12.3 11.8

3.5 3.4 3.4

4.1 3.7 4.1 p

7.1 7.3 6.8

12.9 13.5 13.0

Contents

BBC RADIO BBC AHPL (just!) ahead of target (15h36m) at 15h38m

8

Source: RAJAR / Ipsos MORI / RSMB

Overall BBC Radio AHPL nudge up to 15h38m, 2m ahead of the

1718 target (15h36m) and up by 11m on last quarter, and 18m on

the year. Beneath this, it’s a mixed bag. We see some

directional increases for our digital services: 1Xtra (4h57, highest

since Q116), 4Extra (6h04m, highest since Q2 16) and 5 live sports

extra which sees significant increases on both periods to 5h02m –

its highest figure since Q3 13. Meanwhile, sister station 5 live can

offset its drop in reach somewhat with period-on-period rises in

timespent to 6h55m. Meanwhile Radio 2 remains the most

listened to UK station with AHPL of 12, versus Radio 4’s equally

impressive 11h.

Sept 16 June 17 Sept 17 QoQ YoY

15.3 15.5 15.6

All BBC Network

radio 14.4 14.5 14.7

6.3 6.7 6.4

11.4 11.7 12.0

6.2 6.1 5.7

10.9 11.0 11.0

6.5 6.6 6.9

7.1 6.8 7.8 p

8.7 8.7 8.7

11.5 11.7 11.7

Sept 16 June 17 Sept 17 QoQ YoY

3.85 2.65 5.03 p p

9.34 8.67 8.62

4.50 4.52 4.82

5.36 5.72 6.06

4.82 5.97 5.14

6.43 4.90 5.40

Contents

BBC RADIO Record reach for National Commercial Radio, now over 20m.

9

Source: RAJAR / Ipsos MORI / RSMB

Commercial Radio reach, like that of

BBC, is statistically flat on both periods

at 35.56m/65.3%, which sees them stay

ahead but the gap narrows by c200k to

706k.

Within this, ILR is more or less stable at

just shy of 50% of the population

listening every week but INR is up on

both periods to a record 20.2m/37.1%

listening every week.

Both talkSPORT (2.9m) and Total

Absolute Radio Network (4.5m) have

seen their highest reach this year.

Weekly Reach (000s) Sept 16 June 17 Sept 17

All Commercial 34,762 35,881 35,559

64.3 65.9 65.3

All Local Commercial 26,781 27,277 26,952

49.6 50.1 49.5

All National Commercial 19,503 19,905 20,231

36.1 36.5 37.1

Classic FM 5,281 5,781 5,433

9.8 10.6 10

talkSPORT 2,857 2,622 2,926

5.3 4.8 5.4

Total Absolute Radio Network 4,471 4,297 4,501

8.3 7.9 8.3

QoQ YoY

Contents

BBC RADIO

Record results for several UK-wide CR brands – such as LBC, Kiss, Radio X, Smooth, Virgin, Kisstory, Capital Xtra, Absolute 90s and Heart 80s.

10

Source: RAJAR / Ipsos MORI / RSMB

(000s) Sept

16

June

17

Sept

17 QoQ

YoY

Gold Network UK 1,154 1,168 1,108

Heart Network UK* 9,101 8,712 8,644 q

Kerrang! UK 769 526 615 q

Kiss 5,425 5,393 5,686 p

Total LBC UK 1,801 2,038 2,084 p

Smooth Radio UK 4,749 5,091 5,104 p

Radio X UK 1,265 1,391 1,523 p

Capital Network UK 8,055 8,055 7,760 q

Capital Xtra (UK) 1,324 1,194 1,464 p

(000s) Sept

16

June

17

Sept

17 QoQ YoY

Jazz FM 556 556 570

Heat 841 591 616 q

The Hits 738 586 600 q

Planet Rock 1,060 1,075 1,050

Kiss Fresh (was Smash Hits) 611 526 519 q

Kisstory 1,611 1,734 1,823

Absolute Radio Classic Rock 646 644 637

Absolute 80s 1,458 1,512 1,532

Absolute 90s 703 651 756

Among the Commercial Radio brands now available UK-wide, there are more statistically significant shifts this time round. And all of Kiss, LBC, Smooth, Radio X, Capital Xtra, Jazz, Kisstory, Absolute 80s and Absolute 90s show increases across both periods. In particular, LBC builds on a Q2 record to report a new record reach of 2.1m, as does Kiss (5.7m), Smooth (5.1m) Radio X (1.5m), Capital Xtra (1.5m), Kisstory (1.8m) and Absolute 90s (756k). Among the stations that came on air last year within the new D2 multiplex, there are records for Magic Chilled (270k), talkSPORT2 (342k) and Virgin (556k); and the second report card for Heart 80s sees it leap up from 852k to 1.1m, versus Absolute 80s 1.5m.

Contents

BBC RADIO Record share for National Commercial Radio

11

Source: RAJAR / Ipsos MORI / RSMB

(%) Sept 16 June 17 Sept 17 QoQ YoY

All Commercial 45.8 45.0 45.3

All Local Commercial 28.7 28.3 28.1

All National Commercial 17.1 16.7 17.2

Classic FM 3.5 3.9 3.5 q

talkSPORT 2.0 1.5 1.9 p

Total Absolute Radio Network 3.0 3.2 3.2

Overall, the BBC and Commercial share

gap narrows once more this time round

as Commercial share nudges up on the

quarter (but is down on the year) to 45.3%

and BBC goes the opposite way to 52.1%

- a gap of 6.8%pts is the lowest since Q3

last year.

As with reach, its INR that is driving this

increase for Commercial – up to a high

17.2%, while ILR is down on both periods

to 28.1%.

Contents

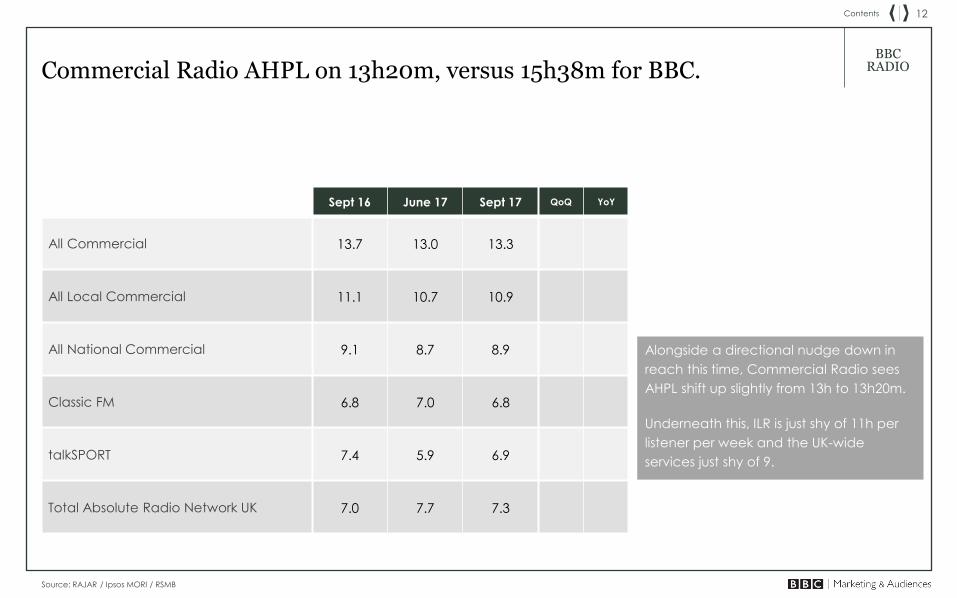

BBC RADIO Commercial Radio AHPL on 13h20m, versus 15h38m for BBC.

12

Source: RAJAR / Ipsos MORI / RSMB

Sept 16 June 17 Sept 17 QoQ YoY

All Commercial 13.7 13.0 13.3

All Local Commercial 11.1 10.7 10.9

All National Commercial 9.1 8.7 8.9

Classic FM 6.8 7.0 6.8

talkSPORT 7.4 5.9 6.9

Total Absolute Radio Network UK 7.0 7.7 7.3

Alongside a directional nudge down in

reach this time, Commercial Radio sees

AHPL shift up slightly from 13h to 13h20m.

Underneath this, ILR is just shy of 11h per

listener per week and the UK-wide

services just shy of 9.