bench marking the it industry competitiveness index

TRANSCRIPT

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 1/32

I v stm t or th F t rBenchmarking IT IndustryCompetitiveness 2011

Developed by

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 2/32

C

BSA CEO Letter

Pre ace

Introduction

Innovation Leaders

People or Technology

Upholding the Law

Policy and In rastructure

Conclusion: Many Centers o

Competitiveness BSA Blueprint or Global ITCompetitiveness

Appendix 1: Index Methodologyand Defnitions

Appendix 2: Index Scores by Region 25

Appendix 3: Index Scores by Category 27

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 3/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

1Business so tware allianCe

Bsa Ceo letter

But the eld o competition is becoming morecrowded as new players rise steadily to meet thestandards that the leaders have set. India, orexample, has leapt 10 spots in the overall rankingsby posting strong scores on indicators o humancapital and research and development. Others,such as Singapore, Mexico and Poland, haveclimbed in the rankings by showing new levels o strength across the board, proving that investment begets advantage, too.

Meanwhile, countries that are treading water ordri ting o course o er cautionary tales about theconsequences o cutting corners or neglectingthe undamentals o IT competitiveness. China,

or example, a ter making impressive headwayin previous years, has seen its momentum slowconsiderably in large part because o its poorrecord o protecting intellectual property rights.

Canada, too, has dropped down the overallrankings because it has allowed its IP standardsto all.

How will this story have changed two years hence?It depends on decisions countries are makingtoday.

Robert HolleymanPresident and CEOBusiness So tware Alliance

Technology innovation boosts productivityand spurs economic growth, economistshave long understood, because it allows

companies to get more out o the investmentsthey make in labor and capital. In the industrialera, this happened as new machines automatedthe actory foor. Today, or our globally connecteddigital economy, we have in ormation andcommunications technologies.

But how do we keep the engine o IT innovationhumming? The ormula is here in the IT Industry Competitiveness Index . In short, a country musthave a healthy business environment plus a rst-rate IT in rastructure, dynamic human capital,robust research and development, a strong legalenvironment, and adequate public support orindustry development.

With support rom the Business So tware Alliance,the Economist Intelligence Unit benchmarks 66countries every two years on a series o indicatorsin each o those six categories. In this latest editiono the Index , we see the continuation o a distincttrend: The competitive environment in the ITsector is heating up globally.

As the overall rankings attest, established ITpowerhouses like the United States are holdingtheir leadership positions — even in the ace o the recent economic turmoil — because o the

solid competitive oundations they have built upthrough years o investment. “Advantage begetsadvantage,” notes Pro essor David Hsu o theWharton Business School in one o the interviewsthe Economist Intelligence Unit has conducted orthis year’s study.

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 4/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

2 Business so tware allianCe

Pre aCeThis report is published by BSA and written by theEconomist Intelligence Unit, with the exception o the BSACEO Letter and BSA commentary appearing on pages18–20. The views expressed by the Economist IntelligenceUnit do not necessarily refect those o BSA.

The Economist Intelligence Unit research drew on two maininitiatives:

> Updating o the IT Industry Competitiveness Index,

which compares 66 countries on the extent to whichthey support the competitiveness o in ormationtechnology (IT) rms. The Index was created in 2007.

> The conduct o in-depth interviews with nine IT industryexecutives and independent experts, all with uniqueperspectives on the drivers o IT competitiveness.

Sincere thanks go to the interviewees or sharing theirinsights on this topic. The ollowing individuals wereinterviewed or the study:

> Walter Deppeler, President EMEA, Acer > Brett Dawson, Chief Executive, Dimension Data > Karen Geary, Group Director of Human Resources and

Corporate Communications , Sage > Antony Gold, Head of Contentious Intellectual Property ,

Eversheds > David Hsu, Associate Professor of Management ,

Wharton Business School > Ian Ing, Analyst , Gleacher & Company > Phaneesh Murthy, Chief Executive, iGATE Patni

> Charlotte Walker Osborn, Head of Telecommunications,

Media and Technology , Eversheds > Mike Shove, President , CSC Asia Group

September 2011

introDuCtion

Maintaining investment levels during aneconomic downturn is no easy eat,but business leaders know the bene t:

the ability to compete at a higher level whenmarkets recover. The same may be said o thein ormation technology (IT) industry and nationalgovernments, as continued attention to actorssuch as education, research and development(R&D), high-speed communications networks, andaccess to nance is needed to ensure the sector’sglobal competitiveness in the longer term.

The virtue o sustained investment in the enablerso sector competitiveness is borne out in the 2011IT Industry Competitiveness Index. The two years

since the last study have been the leanest nancialtimes IT producers have known in a decade, andor many governments — in at least a generation.

But countries that have seen continued investmentin key competitiveness enablers such as the R&Denvironment, talent and skills are notable gainersin the 2011 Index.

For example, despite its obvious economicproblems, or perhaps because o them, Irelandappears to have redoubled e orts to cultivate oneo the world’s most competitive environments or

IT producers. Private-sector R&D spending was upin the early part o the downturn (as was enrolment

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 5/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

3Business so tware allianCe

The US is probably the world’s best example o thevirtues o long-term investment in the enablers o IT sector competitiveness. The US tops the Indexonce again, its high scores across all categoriesrefecting not only the historical strength o its ITindustry but also the high quality o its educationand talent environments, its strong encouragemento innovation and entrepreneurialism, and itswell developed legal system. Recent economicand scal problems have not dented its clear ITindustry strengths.

The importance o competitive IT industryenvironments extends, o course, beyond thesector and its players to impact on national

economic competitiveness overall. There is ahigh degree o correlation, or example (0.88),between the results o this year’s IT IndustryCompetitiveness Index and those o the WorldEconomic Forum’s Global Competitiveness Index2010–2011.

This report, beyond highlighting selectedcountries’ per ormance in the 2011 Index, exploreshow companies and governments are addressingmajor trends a ecting the industry. The examplesand expert insights provided will underscore

the critical importance o innovation, people,transparency (o laws and rules) and balance (o industry policy), not only to the competitivenesso industry environments, but to IT producersthemselves.

in science and engineering programs). With ITpatent generation also increasing, the e ect isto boost Ireland’s score or the R&D environmentand advance the country to joint 8th positionthis year (with Australia) rom 11th in 2009. Asimilar improvement in the R&D environment,with higher private-sector spending, along withincreased patent activity, li ts Israel rom 13th to

joint 10th (with the Netherlands). And signi cantimprovement across all R&D environmentindicators, as well as in higher educationenrolment, has boosted India ten places to joint34th this year (tied with Lithuania).

There are other noteworthy upward shi ts in 2011.

Singapore, advancing to 3rd position in the table,has bene ted rom a vastly improved score in thehuman capital environment. Its northern neighbourMalaysia has jumped to 31st place thanks tomuch improved per ormance in its R&D indicators— and especially in IT patent activity. Germany,Austria, Poland and Turkey are other countriesregistering signi cant gains due to improvement inone or both o these Index categories. Conversely,Lithuania (41st) and Russia (46th) have allen backseveral places due mainly to a decline in scores inthe key R&D category. The other BRIC countries,China and Brazil, have maintained slow but steadyimprovement in Index per ormance, with bothadvancing one place this year, to 38th and 39threspectively.

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 6/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

4 Business so tware allianCe

Ov r ll Scor s d R sIT I d stry Comp titiv ss I d x 2011

Countries are scored on a scale of 1–100.

s c :Economist Intelligence Unit

Rank SCORe / 1002011 YoY 2011 YoY

1 - United States 80.5 +1.6

2 - Finland 72.0 -1.6

3 +6 Singapore 69.8 +1.6

4 -1 Sweden 69.4 -2.1

5 +1 United Kingdom 68.1 -2.1

6 +2 Denmark 67.9 -0.7

7 -3 Canada 67.6 -3.7

=8 +3 Ireland 67.5 +0.6

=8 -1 Australia 67.5 -1.2

=10 -5 Netherlands 65.8 -4.9

=10 +3 Israel 65.8 +1.5

12 +2 Switzerland 65.4 +1.9

13 +2 Taiwan 64.4 +1.0

14 -4 Norway 64.3 -2.8

15 +5 Germany 64.1 +6.0

16 -4 Japan 63.4 -1.7

17 +5 Austria 61.4 +4.418 +1 New Zealand 61.3 +2.5

=19 -3 South Korea 60.8 -1.9

=19 +2 Hong Kong 60.8 +3.3

21 -4 France 59.3 +0.1

22 -5 Belgium 57.7 -1.5

23 +1 Italy 50.7 +2.2

24 +1 Spain 50.4 +3.0

25 +4 Slovenia 48.8 +3.5

26 +3 Portugal 47.1 +1.8

27 -1 Czech Republic 46.1 -0.9

28 -1 Hungary 45.4 -0.7

29 -6 Estonia 45.0 -10.6

30 +5 Poland 44.6 +3.8

31 +11 Malaysia 44.1 +8.5

32 -5 Chile 43.2 -2.9

33 +1 Slovakia 42.1 +0.7

Rank SCORe / 1002011 YoY 2011 YoY

=34 -1 Latvia 41.6 -1.0

=34 +10 India 41.6 +7.5

36 -4 Greece 40.7 -2.3

37 -1 Romania 40.4 +0.8

38 +1 China 39.8 +3.1

39 +1 Brazil 39.5 +2.9

40 -3 Croatia 39.0 +0.7

=41 +5 Turkey 38.7 +4.9

=41 -10 Lithuania 38.7 -4.6

43 +4 Bulgaria 38.1 +4.5

44 +4 Mexico 37.0 +5.0

45 -4 Argentina 36.2 -0.3

46 -8 Russia 35.2 -1.6

47 -4 South A rica 35.0 -0.3

48 -3 Saudi Arabia 34.1 +0.2

49 +3 Colombia 33.7 +5.3

50 -1 Thailand 30.5 -1.351 -1 Ukraine 28.9 -2.5

52 -1 Philippines 28.4 -0.1

53 +3 Vietnam 27.1 +2.1

54 -1 Egypt 26.3 -0.5

55 - Peru 25.5 -0.5

56 +2 Sri Lanka 25.0 +1.1

57 +2 Indonesia 24.8 +2.0

58 -1 Venezuela 24.5 +0.1

59 +1 Ecuador 23.1 +0.4

60 -6 Kazakhstan 22.8 -3.6

61 +2 Pakistan 22.3 +2.3

62 +3 Nigeria 21.4 +2.6

63 -1 Bangladesh 20.6 -0.5

64 -3 Azerbaijan 20.3 -1.0

65 -1 Algeria 19.5 -0.3

66 - Iran 18.8 +1.7

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 7/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

5Business so tware allianCe

innoVation leaDers

The other great advantage enjoyed by the USis what Pro essor Hsu calls the “incestuous”relationships ostered by Silicon Valley: thetechnology community is perpetually regeneratingitsel as individuals leave one organization tobegin another, and angel investors ollow. Intoday’s environment, such start-ups could quicklybecome pricey acquisition targets, uelling evenmore entrepreneurial interest. “A big motivation isbeing taken over by the Oracles and Microso ts o the world,” says Mike Shove, Asia Group Presidento CSC, an IT services rm.

When it comes to innovation, is the USlosing its edge? Walter Deppeler,EMEA President o Acer, a Taiwanese

computer maker, believes the IT industry’s centero gravity is “shi ting rom West to East”. BrettDawson, Chie Executive o Dimension Data, aSouth A rica-based provider o IT so tware andservices, also notes the “material gains o Asia-based technology companies against those inthe US and Europe”. Yet the companies seen asthe real game-changers, attracting the lo tiestvaluations, still have US roots. Think Apple,Google, Amazon, and — even more recently —Facebook.

For Pro essor David Hsu o Wharton BusinessSchool, the US is not about to slip behind itsemerging-market rivals anytime soon. Besideshaving all the vital ingredients needed or

entrepreneurs to thrive, including world-classeducational institutions, a developed venture-capital community and a business- riendly politicalsystem, the US also has a deep-seated culture o encouraging experimentation. “Around 75% o American venture-capital investments result in anexit value o zero, but without this tolerance o

ailure there would be ewer successes,” he says.

It may thus come as no surprise that the USis the top-ranked country in 2011 in the R&Denvironment category o the Index, which

considers such indicators as IT patent generationand public and private R&D spending. Israel,Taiwan, Finland and Singapore round out the top

ve in this category.

United States

Israel

Taiwan

Finland

Singapore

Japan

Ireland

Sweden

Germany

Canada

74.3

71.3

69.9

67.3

67.2

56.9

55.9

54.9

52.6

47.6

R&D e viro m tTop 10 Co tri sCountries are scored on a scale of 1–100.

s c : Economist Intelligence Unit

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 8/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

6 Business so tware allianCe

Yet wider developments could boost innovation inother parts o the world. For a start, as extendingworking visas or the US becomes more di cult,Asian expatriates may return home and exploittheir knowledge o local market conditions,combined with their experiences and contactsin the US, to come up with new IT products andservices. The lessening wage disparity betweenthe US and some Far Eastern emerging markets islikely to work in avor o this trend.

Rising labor costs are already orcing change in

countries where hardware production is o criticalimportance. Ian Ing, an analyst at New York-basedGleacher & Company, says it is un air to continueaccusing Chinese technology giants Huawei andZTE o simply producing low-cost versions o goods rst developed in the US or Europe. “Theyare still ocused on low-cost solutions but nowhave leading-edge products and are open to newways o improving value- or-per ormance,” hesays. “Innovative component start-ups or smallercompanies, indeed, have a much better chance

o selling to Huawei and ZTE than to Ericsson andCisco, which only want to deal with large, publiclytraded companies. Optichron (now Netlogic) andLattice Semiconductor are examples in the area o wireless base stations.”

M v g p

The gradual ebbing away o the low-costadvantage will bring about more pro ound shi ts.For Taiwanese companies, which have moved

a lot o their hardware production to China, astrategic priority is developing expertise in themore pro table area o so tware and services,according to Mr. Deppeler o Acer. As it tries to

build a reputation or quality and innovation, Acerhas been success ul at turning itsel into a globalbrand and cultivating relationships with others,including Google. “The challenge or some o these companies is making the transition rombeing a small part o a supply chain to being at the

ore ront o a given category,” says Pro essor Hsu.

But that is not the only di culty. In manyemerging markets, IT companies are not as closeto consumers as they are in the West, and soinnovations in areas such as social networking

— where there is the potential to develop a“plat orm” and become a global phenomenon— are much harder to realize. “The US has beenvery innovative because it has this large domesticmarket that accounts or [a large share] o globaltechnology spending,” says Phaneesh Murthy,Chie Executive o Indian IT services companyiGATE Patni. “Being based in that market, youhave an understanding o the usage culture.”

By contrast, in small but relatively wealthy Israel,the IT sector is largely export-driven. Whilesuccess ul, its companies tend to be importantcogs rather than instantly recognizable brandsin their own right. And because the addressablemarket or sophisticated technology is limited inthe BRICs, their IT companies struggle to appealto consumers in developed economies. “Once youhave developed the most cutting-edge products,you can dumb them down or di erent incomecategories,” says Pro essor Hsu. “It’s much harderto do the reverse.”

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 9/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

7Business so tware allianCe

PeoPle or teCHnoloGY

markets i their workers are being lured to theWest. But the growing availability and quality o ITworkers rom Asia, in particular, must be a long-term worry or more developed economies. “Thereare enormous talent pools across the Asian region,with China alone set to churn out about 400,000 ITgraduates this year,” says CSC’s Mr. Shove. “Andthe quality is there on a number o levels.”

Sheer numbers such as these, when combinedwith lower costs and increasing quality, meansomething to IT producers in any part o the worldworried about uture talent shortages. Chinaemploys by ar the largest number o IT workers

AGerman executive interviewed in 2009 orthe last iteration o this study expressed aconcern that jobs would begin migrating

rom Europe to less heavily regulated marketspost recession. But infexible labor markets arenot the most serious issue con ronting Europe’sIT employers today. Sage, a UK-based providero business-management so tware and services,bemoans the poor quality and availability o ITworkers in Europe. Unless the situation improves,the company is likely to ll more roles withindividuals rom emerging markets in the uture(see case study, “A Technology Talent Crunch”).

Pro essor Hsu o Wharton Business Schoolsays that European countries have most o theingredients needed or a competitive IT industry— including the physical in rastructure, stablepolitical systems and good en orcement o

intellectual property rights — but marks themdown on what he calls “labor rigidity”. “I youhave government policy or a business culture thatinduces this rigid labor market, it will work to thedetriment o innovation,” he says.

The contrast, clearly, is with the US, where bothrecruiting and laying o sta are perceived to beless cumbersome processes, suiting the cultureo experimentation discussed earlier. Yet workers

rom neither Europe nor the US can competewith those rom emerging markets on cost. “I I

start thinking about countries where the talent isavailable at a more a ordable price range, thenIndia clearly has signi cant advantages,” says Mr.Murthy o iGATE Patni. “In terms o a value ormoney, it remains the world number one.”

As emerging-market wages rise, this advantagewill slowly ade away. Nor does it necessarily boostthe competitiveness o IT industries in emerging

United States

China

Australia

South Korea

United Kingdom

New Zealand

Ireland

Taiwan

Canada

India

74.1

60.4

60.4

58.7

57.5

56.0

54.8

53.7

53.4

52.8

H m C pit lTop 10 Co tri sCountries are scored on a scale of 1–100.

s c : Economist Intelligence Unit

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 10/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

8 Business so tware allianCe

in the world (over 5m according to EconomistIntelligence Unit estimates), and is just behindRussia and India when it comes to studentsenrolled in tertiary-level science and engineeringcourses. These are reasons why China occupies2nd position globally, behind the US, in the Index’shuman capital category. (India and Russia rank arelatively high 10th and 11th, respectively.)

a ch

Perhaps the biggest change taking place in Asiais the improvement in so-called “so t skills” that

all outside the traditional remit o the IT worker.While Mr. Shove says there is still some immaturityin the area o project management, which isimportant to CSC as an IT services company,Pro essor Hsu observes a “huge move” in businesseducation that will have ar-reaching implications.“We [Wharton Business School] helped set upthe Indian School o Business and we have a

partnership in China with Beijing University,” hesays. “The development o local managerial talentis going to be a big disruptor by helping thesecountries to break through.”

O course, the US can still boast probably theworld’s best environment or business education.Along with the UK, Ireland and Australia, theUS gets top marks in the Index’s “quality o technology skills” indicator, which assesses theeducational system’s ability to train technologistswith business skills. Mr. Ing o Gleacher &

Company suggests that business acumen couldin orm the decisions o traditional IT educatorsabout where to ocus resources. “My graduateengineering school, Georgia Tech, now produces

ewer semiconductor designers, because a lot o those jobs have moved to Asia, but it has lots o expertise in search-engine optimization,” he says.“You have to be nimble in terms o where you areinvesting and play to your strengths.”

Case stuDY

a teCHnoloGY talent CrunCH

The hunt or IT talent in Western Europe is growing ever more di cult, according to Sage. Asone o the region’s largest providers o business-management so tware and services, the UK-based company employs about 13,500 employees globally, with around 20% in research anddevelopment and 15% in technical support roles. Employee turnover runs at about 15% annually,and so the company needs to ll some 2,000 jobs a year even be ore it considers any growthinitiatives.

For Karen Geary, Group Director o Human Resources and Corporate Communications, the lowavailability o skills is a particular concern. In the UK, or instance, relatively ewer youngstersnow choose IT/technology-based courses at the higher-education level. (According to data romUNESCO, the number o students enrolled in tertiary science courses in the UK declined by morethan 7% between 2005 and 2008.)

continued on next page

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 11/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

9Business so tware allianCe

The contrast with other parts o the world is stark. “The availability o IT talent is much greater insome o the Asian economies because that is what they are churning out in schools,” says Ms.Geary. “I think IT is seen as a more acceptable discipline to pursue. This is especially so whengender is added to the mix, as Asian emales are well represented in technology, in contrast toWestern Europe. So on pure numbers alone Europe’s available talent pool is probably smaller.”

But it is not just low availability that worries Ms. Geary. The quality o the skills on o er is o tenmuch poorer in Western European economies than elsewhere, she says. While graduates tend tobe more IT-savvy these days, they o ten lack the business acumen and training that a customer-

acing organization like Sage increasingly values. “Universities are still producing candidates withprimarily technical skills, whereas other skills are also required o ten in equal measure,” observesMs. Geary.

Her criticisms may surprise those who think Asia is the true laggard in this area, but Ms. Gearybelieves the region has made big improvements in recent years. “I know that certain parts o Asiahave a reputation or being too ocused on the technology part, but the students I have met area lot more rounded than they used to be,” she says.

Although Sage is involved at the educational level — with senior sta taking advisory boardroles at universities and providing input to curricula — the slower pace o academic li e makes itdi cult to embed new skills within courses. The company still spends a considerable amount o time getting new recruits up to speed, with technical-support sta requiring three-to-six monthso initial on-the-job training and so tware developers as much as a year.

Long term, the implications o Europe’s perceived shortcomings could be dramatic. Sage isalready starting to ll roles in the US and Europe with IT pro essionals rom emerging markets.Ms. Geary says that trend will accelerate over the next ew years unless more youngsters can bepersuaded to choose science-based degrees. “We need to make technology more attractive interms o placements, scholarships and nancial incentives,” she says.

O shoring could also become more appealing i skills shortages persist. Owing to its emphasison customer support, Sage has no plans to shi t its human capital to other parts o the world. Butother companies will eel di erently. Cost used to be the main reason or o shoring. Could talenttake its place?

continued from previous page

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 12/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

10 Business so tware allianCe

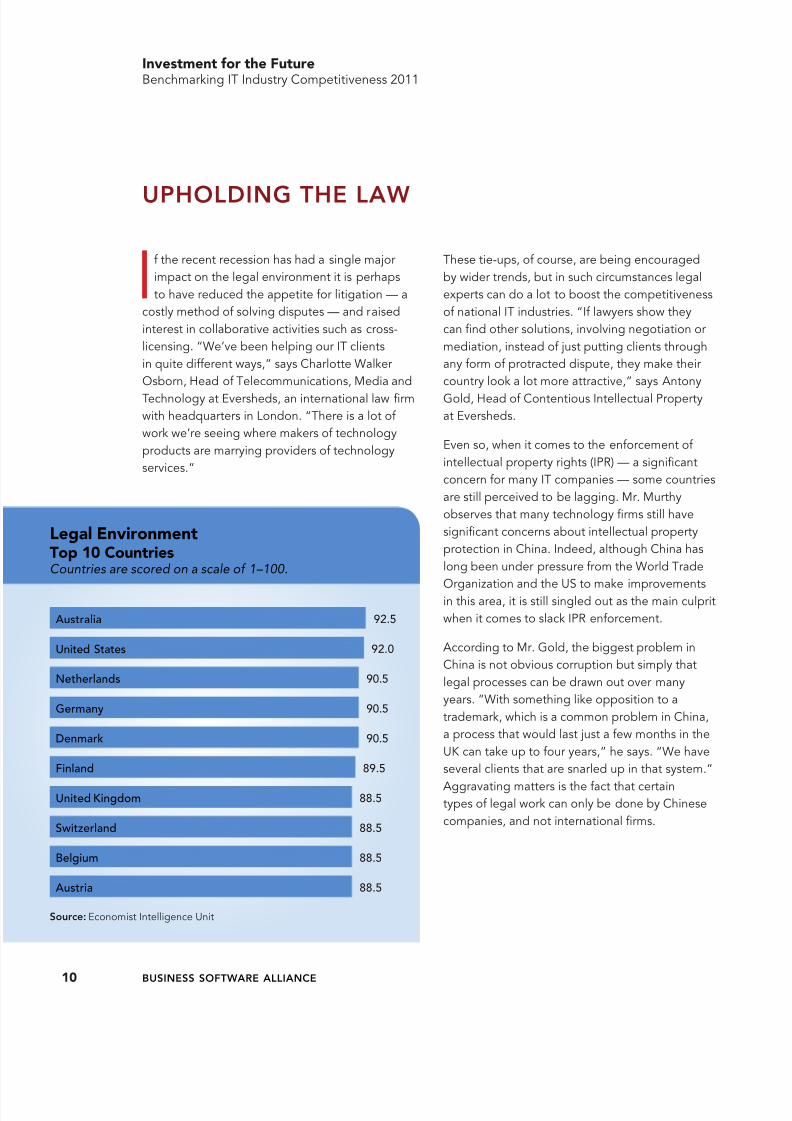

uPHolDinG tHe law

These tie-ups, o course, are being encouragedby wider trends, but in such circumstances legalexperts can do a lot to boost the competitivenesso national IT industries. “I lawyers show theycan nd other solutions, involving negotiation ormediation, instead o just putting clients throughany orm o protracted dispute, they make theircountry look a lot more attractive,” says AntonyGold, Head o Contentious Intellectual Propertyat Eversheds.

Even so, when it comes to the en orcement o intellectual property rights (IPR) — a signi cantconcern or many IT companies — some countriesare still perceived to be lagging. Mr. Murthyobserves that many technology rms still havesigni cant concerns about intellectual propertyprotection in China. Indeed, although China haslong been under pressure rom the World Trade

Organization and the US to make improvementsin this area, it is still singled out as the main culpritwhen it comes to slack IPR en orcement.

According to Mr. Gold, the biggest problem inChina is not obvious corruption but simply thatlegal processes can be drawn out over manyyears. “With something like opposition to atrademark, which is a common problem in China,a process that would last just a ew months in theUK can take up to our years,” he says. “We haveseveral clients that are snarled up in that system.”

Aggravating matters is the act that certaintypes o legal work can only be done by Chinesecompanies, and not international rms.

I the recent recession has had a single majorimpact on the legal environment it is perhapsto have reduced the appetite or litigation — a

costly method o solving disputes — and raisedinterest in collaborative activities such as cross-licensing. “We’ve been helping our IT clientsin quite di erent ways,” says Charlotte WalkerOsborn, Head o Telecommunications, Media andTechnology at Eversheds, an international law rmwith headquarters in London. “There is a lot o work we’re seeing where makers o technologyproducts are marrying providers o technologyservices.”

Australia

United States

Netherlands

Germany

Denmark

Finland

United Kingdom

Switzerland

Belgium

Austria

92.5

92.0

90.5

90.5

90.5

89.5

88.5

88.5

88.5

88.5

L g l e viro m tTop 10 Co tri sCountries are scored on a scale of 1–100.

s c :Economist Intelligence Unit

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 13/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

11Business so tware allianCe

A groundswell o innovation, and the need orChinese IT companies to diversi y away rommanu acturing and into so tware development,could provide the impetus or change. “Asinnovation happens, interest in intellectual-property protection will come rom inside thecountry instead o rom a US multinationalcomplaining about the system,” says Mr. Shove o CSC. “In other words, as Chinese companies startto develop their own so tware products, they willwant to be protected.”

The spotlight on China should not, o course,distract attention rom shortcomings elsewhere.While Mr. Gold lauds Germany and Austria orhaving justice systems that are both speedy andcheap or litigants, he says the French system isvery slow, while that in the UK is perceived to bequite costly. “We have been trying hard to improvethat, partly through the Patents County Court [setup to provide a less costly and complex alternativeto the High Court], and you do get a relativelygood system o justice in the UK,” he says.

th v c

While rigorous patenting systems are sometimesseen as a barrier to innovation, the lack o legal protection or social-networking sites andapps could be just as troubling. Because thesenewer developments are usually protectedonly by copyright law, and not by the stricterlaws on patents designed or more substantiveinnovations, they are much easier to replicate

without ear o legal reprisal, according to Ms.Walker Osborn. “It puts pressure on innovationin this area,” she says. “You don’t want to riskspending lots o money i someone else can copyyour idea.”

By contrast, there have been some encouragingdevelopments in the area o cross-bordercollaboration on cyber crime. Since the last updateo our study a number o countries — includingAustria, Germany, Portugal, Spain and Azerbaijan— have rati ed their governments’ adherence tothe Council o Europe Convention on Cybercrime.And July 2011 saw the launch o the non-pro tInternational Cyber Security Protection Alliance(ICSPA), whose stated aim is “to channel unding,expertise and assistance directly to assist law-en orcement cyber crime units.” Ms. WalkerOsborn, a member o the British Computer SocietyIn ormation Security Specialist Group (BCS-ISSG),sees the establishment o the ICSPA as a positivemove. “A lot o technical understanding is neededto deal with these crimes, and police have beenstretched just dealing with local issues,” she says.

Although based in the UK, and backed by UKpoliticians, it is a primary goal o the ICSPA toprovide assistance to other countries. Those thatare most serious about IT industry competitiveness

are likely to welcome its appearance.“Governments that want success or theirtechnology businesses know they must tackle thecyber crime problem,” says Ms. Walker Osborn.“Because o its borderless nature, the best way todo that is through alliance.”

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 14/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

12 Business so tware allianCe

PoliCY anD in rastruCture

top per ormer when it comes to the strength o itslegal environment or IT producers, although it’syielded the pole position in 2011 to Australia.

Even during the recession, so tware companySAP had complained about Germany’s car-scrapping scheme or the same reason,arguing that policymakers would do better

supporting technologies designed to improvethe competitiveness o various industries. TheEconomist Intelligence Unit doubts the wisdomo government support or speci c technologiesbut agrees that, as the global economy starts torecover, the need or governments to take a long-term view o IT industry development appearsstronger than ever.

“Much like venture capitalists, policymakerscannot just look at something on an annual basis,”says Pro essor Hsu o Wharton Business School.“In terms o their investments, they have to thinkabout the next seven to nine years i they aregoing to make substantive changes with regard tocountry competitiveness.”

While governments in China andSouth Korea announced some boldinitiatives around green technology

and smart grids during the downturn, many inthe recession-struck West were more ocused onshort-term stimulus. In the US, or instance, thistook the orm o public-works projects to createtemporary jobs. “It’s a little bit disappointing therewasn’t more oresight,” says Mr. Ing o Gleacher& Company. “The US taxpayers were willing tostep up in 2009, and in today’s environment theyprobably aren’t.” All the same, the US remains a

S pport or IT I d stry D v lopm tTop 10 Co tri sCountries are scored on a scale of 1–100.

United States

Canada

Ireland

Singapore

Norway

Australia

Sweden

New Zealand

Hong Kong

United Kingdom

87.2

85.4

83.9

82.3

82.1

82.1

81.6

80.7

80.4

80.0

s c :Economist Intelligence Unit

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 15/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

13Business so tware allianCe

Case stuDY

tHe PaYo s anD Perils o it inDustrY PoliCY

Policymakers are widely credited with making South Korea an IT powerhouse and one o theworld’s most connected countries. It ranks a respectable 19th in the 2011 IT Industry CompetitiveIndex. But government e orts to oster a competitive IT sector have come in or plenty o criticism, too.

No doubt, the IT industry is the driver o South Korea’s economic success. The Asian countryis today the world’s biggest producer o memory semiconductors and display panels and thesecond-biggest maker o mobile phones. According to the Ministry o the Knowledge Economy(MKE), IT exports increased rom US$5m in 1970 to US$154bn in 2010 and now represent 33% o total exports. The IT sector accounts or about 11% o GDP, compared with just 0.01% 40 yearsago.

MKE o cials stress that the key to this success is e ective collaboration between the governmentand the private sector. A good example is in the rollout o super- ast broadband networks, whichwill be crucial in the era o cloud computing. By establishing rm targets or speed and coverage,and providing incentives such as a avourabletax regime, the government has encouragedthe private sector to invest the bulk o the

unds needed while ensuring competitiondoes not su er.

The government’s e orts in the educationalarea are also laudable. One initiative is topromote cooperation between businesses,universities and research institutions. An“IT mentoring” program gives studentsthe opportunity to gain experience in acommercial environment. At the sametime, the government tries to ensure thatbusinesspeople are involved in shapinguniversity curricula. All o this is aimed atmatching the needs o the IT sector with the

educational system.

Nevertheless, South Korea has acquired areputation over the years or protectionistpolicies that avour chaebols, like Samsung,and discourage oreign direct investment. In2009 — the last year or which actual data

continued on next page

Hong Kong 25.04

9.17

8.16

India : 2.61

Singapore

Vietnam

Indonesia : 0.90

Taiwan : 0.74

Malaysia : 0.72

South Korea : 0.27

Japan : 0.24

I w rd For ig Dir ct I v stm ts % o GDP, 2009

s c : Economist Intelligence Unit

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 16/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

14 Business so tware allianCe

were available — South Korea ranked lower than any regional peer apart rom Japan in termso inward direct investment as a percentage o GDP (see chart; although not industry-speci c,this statistic is almost certainly refective o oreign investment in the technology industry, whichin South Korea accounts or a large share o economic output). The MKE puts its hand up or“causing controversy over discrimination against oreign enterprises”, but insists it has recentlyexpanded the scope o sectors open to oreign investment and is trying to create an environmento air competition or oreign companies.

A related criticism is that policymakers have promoted technologies with limited commercialappeal simply to bolster the chaebols. The classic example — albeit rom the telecoms industry— is o WiBro, a mobile broadband technology developed largely by Samsung. The governmentessentially orced Korea Telecom and SK Telecom, the country’s two biggest operators, to launchWiBro despite their own pre erence or more established 3G standards. As both operators nowstart migrating rom 3G to LTE, a so-called ‘4G’ technology, the money spent on WiBro appearslargely to have been wasted.

Perhaps the biggest problem the government has created is a cultural one. Chaebols likeSamsung have become so power ul that smaller domestic rms have been squeezed out o thepicture almost entirely. As a result, South Korea’s brightest students have seen little incentive inbecoming entrepreneurs. The government now says it is pursuing policies to nurture creativeIT talent and provide greater support to small and medium-sized rms. Supporting alternativesources o innovation to ageing technology giants seems eminently sensible.

O particular importance here is recognizing andresponding to the big shi t currently taking placein IT. As more so tware and applications move

rom desktops and locally hosted servers intothe “cloud”, policymakers can take various stepsto ensure their own consumers and producersdo not miss out. Yet Mr. Dawson o DimensionData suggests they could be more ambitious intheir approaches. “There are many governmentagencies using aspects o the cloud but not manythat have come up with bold approaches,” hesays. “There is a dearth o centralized medicalin ormation and government nancial systems,

or example. Governments must trans orm theirown ICT plat orms to drive widespread cloudadoption.”

European policymakers are attempting to addresssome o the cross-border issues raised by thecloud. By 2012, European Commission Vice-President Neelie Kroes wants to have a plandeveloped or an EU-wide cloud-computingstrategy that would also tackle other issues,such as interoperability and allocation o undsto urther research and development o cloudsolutions. In a speech given last January at theWorld Economic Forum’s annual meeting in Davos,she cited three key areas or this strategy: thelegal ramework; the technical and commercial

undamentals; and the market. Clearly, the rsto these alone poses some big questions. Which

continued from previous page

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 17/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

15Business so tware allianCe

country’s laws, or instance, would apply i acompany’s headquarters, back-o ce systemsand customers were each located in a di erentcountry?

Another, critical way in which governments canacilitate a move towards cloud computing is by

ensuring the underlying in rastructure is in place.“I we’re going to create cloud centers that canbe used across the Asia-Paci c region then weneed strong telecommunications links,” says CSC’sMr. Shove. As Mr. Dawson notes, government

involvement in broadband rollout has taken manydi erent orms, rom public-sector unding inAustralia and South Korea to light-touch regulationin the US. But getting a scheme wrong couldhamper deployment or competition. In parts o Western Europe, authorities have already comeunder re or exempting high-speed networks

rom regulations applied to older broadbandinvestments.

Switzerland is the Index leader this year in theIT in rastructure category, with Denmark, theNetherlands, Sweden and Australia also extremelycompetitive. Beyond having one o the world’shighest rates o broadband penetration, itsper ormance improved since 2009 across all otherin rastructure indicators — and especially so whenit comes to Internet security, which is also centralto the success o cloud computing.

Policymakers have stoked other concerns besidesin rastructure. A lack o transparency aroundbusiness proceedings in some Asian markets is

a cause or considerable “nervousness” on thepart o a large US-based multinational, says Mr.

Shove. He also cautions against dependency ongovernment incentives or tax breaks to make abusiness viable. “I that changes you suddenlyhave a less-than-competitive center.”

A lacklustre economic recovery, or the need tomaintain a ast pace o growth, could also uelsubtle orms o protectionism, such as sovereign-backed vendor nancing. Mr. Ing notes that not allUS companies have the balance sheets or vendor

nancing today, but that the Chinese governmentcan help national champions like Huawei and

ZTE. “As a result,” he says, “it’s not truly an openmarket.”

IT I r str ct rTop 10 Co tri sCountries are scored on a scale of 1–100.

Switzerland

Denmark

Netherlands

Sweden

Australia

Norway

Hong Kong

Canada

United States

United Kingdom

89.9

87.2

84.3

83.3

82.4

80.2

79.7

76.9

76.5

74.0

s c : Economist Intelligence Unit

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 18/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

16 Business so tware allianCe

Case stuDY

ClouD CoMPutinG: tHe JourneY Yet to BeGin

Cloud computing is arguably the most important innovation the IT industry has seen or many years —comparable to the move rom main rames to personal computers. The bene ts to enterprise users o cloud-based services are potentially signi cant, including cost savings rom the reduction o xed in rastructurecosts and greater fexibility to scale IT resources up or down as circumstances dictate. Yet the path to a cloud-computing uture is littered with obstacles, according to Dimension Data, a South A rica-based provider o ITso tware and services.

In developed markets, and particularly the enterprise sector, IT customers still have many reservations aboutthe cloud. “Some o our clients have major security concerns and are not prepared to give up their coreapplications at this stage,” says Brett Dawson, Dimension Data’s chie executive. Many large corporationsare also burdened with ageing, bespoke IT systems and have made little progress on standardization andvirtualization o their applications. “These companies need to adopt a lot o the cloud architecture principles

internally be ore they can move to the public cloud,” he says.Mr. Dawson reckons most big enterprises, as well as public-sector organizations and governments, will need tospend at least another year on consolidating their IT activities be ore the journey to the cloud can truly begin.

High-pro le security breaches at Sony and downtime at Amazon earlier this year will no doubt cause evenmore “head-scratching” at already apprehensive organizations, says Mr. Dawson. In response to that, hebelieves, a new class o cloud provider will appear over the next couple o years, o ering guaranteed levels o service with the enterprise sector speci cally in mind. Until then, enterprises may continue to avour the use o so-called private clouds, which are operated or a single organisation. These promise some o the economicbene ts o the more open public cloud but entail less o the risk.

By contrast, in emerging markets, and among small and medium-sized organizations, there is greaterenthusiasm or the cloud. “It allows these companies to deploy IT systems without the same degree o costand complexity as more traditional solutions,” says Mr. Dawson. O course, cost savings are a big incentive

or the enterprise sector as well, but many start-ups and younger organizations do not have to make such adi cult transition rom those older systems in the rst place.

The major constraint in emerging markets is likely to be the basic communications in rastructure — or ratherthe lack o it. Mr. Dawson applauds the installation o new submarine capacity o the coast o A rica, sayingthis will help to lower the cost o Internet access and spur take-up o cloud services. But he thinks a lot o emerging markets still need more telecoms deregulation and investment in xed-line and mobile networks.

Mr. Dawson said he would like to see more countries adopting bold approaches like Europe and the USwhich would acilitate the move to cloud computing. There are some notable examples: in Brazil, or instance,the government is promoting the cloud as part o its modernization initiative. Yet there has been limitedinternational progress on creating a legislative environment in which cloud computing can fourish. Lawsprohibiting the storage o nancial data in another jurisdiction, or example, could be seen as a urther brakeon the rollout o cloud computing.

In the meantime, cloud innovators will continue to nd answers. “Because o these laws, providers serving theenterprise sector will need in rastructure in multiple geographies, which is a challenge in terms o complexityand management,” says Mr. Dawson. “It’s another reason why I think an enterprise-grade service provider willemerge in the near uture.”

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 19/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

17Business so tware allianCe

ConClusion: ManY Centers oCoMPetitiVeness

businesses move to other emerging markets. Yetseveral industry experts interviewed or this studynoted improvements in the quality o IT talent inthese markets. With the emergence o a morebusiness-savvy managerial class, and the impetusprovided by recent economic developments,

China and India are being taken more seriouslyrom an entrepreneurial perspective. As innovation

gathers pace, the en orcement o intellectualproperty rights — which has always been viewedas a problem in this part o the world — is likely toimprove as well.

Europe, meanwhile, still looks attractive in termso IT in rastructure and the legal environment,among other actors. But the continent is arguably

ailing to keep pace with other regions when itcomes to human capital, while rigid labor-marketregulations and a poor climate or investment innext-generation broadband networks could stymiethe development o the IT sector in the uture.Maintaining their high rankings in the Index maybe a tough challenge or these countries in yearsto come.

Despite the impact o the recent recessionon the developed world, North Americanand Western European nations still

per orm strongly in our Index. For many o these, not least the US, the bene ts o long-termvision and sustained investment in the enablers

o IT industry competitiveness are bearing ruit.Indeed, the continued dominance o the USis hardly surprising given the country’s long-standing reputation or innovation, academicexcellence, business acumen and political stability.In combination, those actors have producedan environment in which, to quote Pro essorHsu o Wharton Business School, “advantagebegets advantage”. For the IT industries o othercountries, struggling to raise capital or againstgovernment bureaucracy, the US might sometimes

appear to be disappearing even urther into thedistance.

Even so, big changes are taking place that couldultimately lead to a reshaping o the globalmarket. Although India and China currently liemid-rankings, both countries have gained groundin the Index since its inception, and it would notbe surprising to see urther gains in the yearsahead. Having built competitive IT industries inthe services and manu acturing sectors, bothcountries ace a threat to their low-cost-labor

advantage as wages rise and commoditizing

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 20/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

18 Business so tware allianCe

Bsa BluePrint or GloBal itCoMPetitiVeness

> Vigorously en orce copyright and trademarklaws — and ensure they keep pace with newinnovations such as cloud computing.

> Institute civil and criminal penalties to combatIP in ringement, especially in the world’s astest-

growing markets or in ormation technology,such as China, India, Brazil, and Russia.

w d-c p y m

> Devote adequate resources to patent o ces toensure they can review applications e cientlyand award high-quality patents while weedingout those that are undeserving.

> Do not discriminate among technologies ortypes o inventions.

t ch gy y

> Promote technology-neutral principles ingovernment procurement and other policyinitiatives.

Technology innovation drives economicgrowth and improves people’s daily lives,but countries cannot take innovation

or granted. They must actively promote it withpublic policies that oster development o newtechnologies. As the leading advocate or the

global so tware industry, the Business So twareAlliance (BSA) champions national policy

rameworks that protect intellectual property,attract and welcome talent rom around the world,invest in basic science, create exceptional schools,promote open markets, ensure air competition,and build trust and con dence in technology.

The blueprint outlined here is broadly applicableor all countries aspiring to thrive in today’s

globally integrated digital economy.

P m J b C by gC v y d i v

Robust intellectual property protections —including copyright, patent and trademark laws —provide the very oundation or creative enterpriseto fourish.

BSA recommends the ollowing:

s g c p p y c m> Raise awareness among the public about the

roles that intellectual property rights play inostering innovation and driving wage and job

growth.

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 21/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

19Business so tware allianCe

sp h D g ec my byi p g o C fd c dt

BSA calls or policies that oster a vibrant onlinemarketplace in which government, citizensand businesses can use in ormation tools withcon dence and trust — regardless o whether thetools are mobile, installed on a desktop or servedthrough a cloud. This is a shared responsibility ortechnology industry, governments, businesses andconsumers.

BSA recommends the ollowing:

C m p v cy d d c y

> Support development o sound data-stewardship practices to protect consumers’privacy; bolster security practices to addressconstantly evolving threats; and promoteresponsible habits among Internet users.

> Ensure that privacy policies leave ampleroom or technological innovation and thedevelopment o new services such as cloudcomputing.

> Streamline compliance or businesses andreduce con usion or consumers by establishinguni orm national standards and requiringthat consumers be noti ed when a breach o their personal in ormation puts them at risk o identity the t, raud or unlaw ul activity.

C -b d d > Forge bilateral or multilateral agreements that

harmonize the increasingly inconsistent web o rules governing the movement o data acrossborders.

s pp y-ch c y> Promote international standards or supply-

chain audits and security assurance — withintellectual property rights honored andrespected by manu acturers and serviceproviders at every stage.

C c c

> Strengthen cybersecurity with voluntarystandards that ocus on risks in a fexible, non-

burdensome manner, so technology companiescan innovate aster than threats develop.

Cyb c m

> Enact strong laws to deter and punishcybercrime, such as those prescribed in theCouncil o Europe Cybercrime Convention.

> Create specialized cybercrime authorities,including investigators, prosecutors and judgeswho are well equipped and adequately trained.

> Overcome the borderless nature o cybercrimeby building networks o relationships amonglaw en orcement agencies around the world.

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 22/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

20 Business so tware allianCe

op G b M k d CB opp

BSA believes that international trade creates jobs and boosts economic growth. This entailseliminating market barriers and discouragingdiscriminatory procurement practices in the publicsector. This is especially important in rapidlygrowing economies such as Brazil, Russia, Indiaand China.

BSA recommends the ollowing:

M k - p g d g m

> Support trade agreements that open marketsto all manner o legitimate goods and services,including cloud computing solutions.

> Redouble e orts to ensure that trading partnersadopt and vigorously en orce modern, e ectivelaws against intellectual property the t.

i v h d hD g ec my

BSA calls or policies to promote investment innext-generation technologies, including smartin rastructure. This spurs growth and innovationnot just in the technology industry but in thebroader economy.

BSA recommends the ollowing:

ed c d pp ch dd v pm

> Promote educational opportunities in science,technology, engineering and mathematics.

> Boost unding or basic and applied research atuniversities and government institutions.

e-g v m

> Expand e-government programs that allowcitizens to interact with government and accesspublic services.

> Work toward comprehensive government ITplans that are fexible and technology-neutral,and that protect citizens’ privacy and security.

> Lead by example in adopting cloud computingsolutions where appropriate.

t x p cy

> Ensure tax laws promote investment in newtechnologies and provide a level playing eld

or domestic and multinational companies.

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 23/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

21Business so tware allianCe

aPPenDiX 1: inDeX MetHoDoloGY anDDe initions

The purpose o the IT IndustryCompetitiveness Index is to comparecountries in di erent regions o the world

on the extent to which they possess the conditionsnecessary to support a strong IT industry. Toachieve this, the Economist Intelligence Unit

maintains a benchmarking model which scoresindividual countries on the key attributes o acompetitive IT sector.

There are six categories o indicator used in theIndex; these are set out in the table below, alongwith their weights in the Index, and that o eachindicator in the category. The main data sources

or each indicator are also provided, along withan indication o whether the score is basedon quantitative data ( or example, US$ spend,number o students) or on a qualitative assessmentmade by Economist Intelligence Unit analysts.

Qualitative indicators are scored on a 1–5 basis.Quantitative indicators are normalized through thepopulation set so that each country is measured

rom 0 to 1 by applying a ormula (Yij=[xij-minij]/[maxij-minij]) to each data point. Each indicator isthen converted into a score o 0–100 by applyingthe appropriate multiplier (20 or the qualitativeindicators, 100 or the quantitative indicators).As the weights sum to 1, the composite score or

each country is also based on an Index range o 0to 100 (with 100 representing the highest and bestpossible score).

When employing a normalization method o scoring as we have, there occurs some scoredistortion in selected indicators at both thehighest and lowest ends o the score range. Thisoccurs when indicator scores are based solelyon quantitative data, and explains why some

countries’ scores in certain categories shownare below 1 while others exceed 80 in the samecategory.

Normalization is also the reason why somecountries’ scores in individual categories, or theoverall Index, may be lower than in the previousyear even though their actual per ormance maynot have deteriorated. I the score o the globalleader in a quantitative indicator is lower than thato the previous year’s leader, the scores o othercountries in that indicator will be a ected, possiblyirrespective o their actual per ormance.

No changes have been made to the indicators orscoring methodology in 2011, and the previousweights remain unaltered. We have, however,changed the source o data used in scoring oneimportant indicator — IT patents. Statistics on IT-speci c patent applications collected by the WorldIntellectual Property Organization (WIPO) are nowused or this indicator. (The European Patent O cewas the source used in 2009).

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 24/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

22 Business so tware allianCe

B chm r i g Mod l

InDICaTOR WeIGHTMaIn DaTa

SOuRCeS YeaR TYPe OF SCORe

C t gory 1: Ov r ll b si ss viro m t 10%

Foreign investment policy:Government policy towards oreign capital; culturalreceptivity to oreign infuence; risk o expropriation;investment protection

20% EconomistIntelligence

Unit: BusinessEnvironment

Rankings

2006–10 Qualitative:assigned byEconomistIntelligenceUnit analysts

Private property protection:Degree to which private property rights are guaranteed

and protected

35% EconomistIntelligence

Unit: BusinessEnvironmentRankings

2006–10 Qualitative:assigned by

EconomistIntelligenceUnit analysts

Government regulation:Level o government regulation (mainly licensingprocedures) on setting up new private businesses

25% EconomistIntelligence

Unit: BusinessEnvironment

Rankings

2006–10 Qualitative:assigned byEconomistIntelligenceUnit analysts

Freedom to compete:Freedom o existing businesses to compete in domesticmarkets

20% EconomistIntelligence

Unit: BusinessEnvironment

Rankings

2006–10 Qualitative:assigned byEconomistIntelligenceUnit analysts

C t gory 2: IT i r str ct r 20%

IT investment:Market spending on hardware, so tware and IT services(US$ per 100 people)

15% IDC 2010 Quantitative

PC ownership:Desktop and laptop computers per 100 people

35% PyramidResearch, ITU

2010 Quantitative

Broadband penetration:Broadband connections (xDSL, ISDN PRI, FWB, cable,FTTx) per 100 people

25% Pyramid Research 2010 Quantitative

Internet security:Secure Internet servers per 100,000 people

10% World Bank,Netcra t

2010 Quantitative

Mobile penetration:Mobile phone subscriptions per 100 people

15% Pyramid Research 2010 Quantitative

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 25/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

23Business so tware allianCe

InDICaTOR WeIGHTMaIn DaTa

SOuRCeS YeaR TYPe OF SCORe

C t gory 3: H m c pit l 20%

Enrolment in higher education:Total number o students in higher education, as % o gross university-age population

25% UNESCO 2009 Quantitative

Enrolment in science:Enrolment in tertiary-level science programmes (numbero people)

15% UNESCO 2009 Quantitative

Employment in IT:

Employment in technology sector (number o people)

20% OECD;

EconomistIntelligence Unitestimates

2010 Quantitative

Quality of technology skills:The education system’s capacity to train technologistswith business skills (project management, customer-

acing application and web development, etc)

40% EconomistIntelligence Unit

2010 Qualitative:assigned byEconomistIntelligenceUnit analysts

C t gory 4: R&D viro m t 25%

Public sector R&D:Gross government expenditure on R&D (US$ atpurchasing power parity-PPP, per capita)

15% UNESCO;World Bank

2008 Quantitative

Private sector R&D:Gross private-sector expenditure on R&D (US$ at PPP,per capita)

15% UNESCO;World Bank 2008 Quantitative

Patents:Number o new domestic IT patent applications led byresidents each year, as % o total patent applications

50% WIPO; EconomistIntelligence Unit

estimates

2007 Quantitative

Royalty and license fees:Receipts rom royalty and license ees (US$ per 100people)

20% World Bank, IMF 2009 Quantitative

C t gory 5: L g l viro m t 10%

Intellectual property protection:Comprehensiveness, transparency o IP legislation;adherence to treaties

35% EconomistIntelligence

Unit: BusinessEnvironment

Rankings;national sources

2006–10 Qualitative:assigned byEconomist

Intelligence Unitanalysts

Enforcement of IP rights:En orcement o IP legislation by government authoritiesand courts

35% EconomistIntelligence Unit;USTR; national

sources

2010 Qualitative:assigned byEconomist

Intelligence Unitanalysts

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 26/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

24 Business so tware allianCe

InDICaTOR WeIGHTMaIn DaTa

SOuRCeS YeaR TYPe OF SCORe

C t gory 5: L g l viro m t (continued) 10%

Electronic signature:Status o electronic signature legislation

10% National sources 2010 Qualitative:assigned byEconomist

Intelligence Unitanalysts

Data privacy and spam:Status o data privacy and anti-spam laws

10% National sources 2010 Qualitative:assigned byEconomist

Intelligence Unit

analystsCybercrime:Status o cybercrime laws

10% National sources 2010 Qualitative:assigned byEconomist

Intelligence Unitanalysts

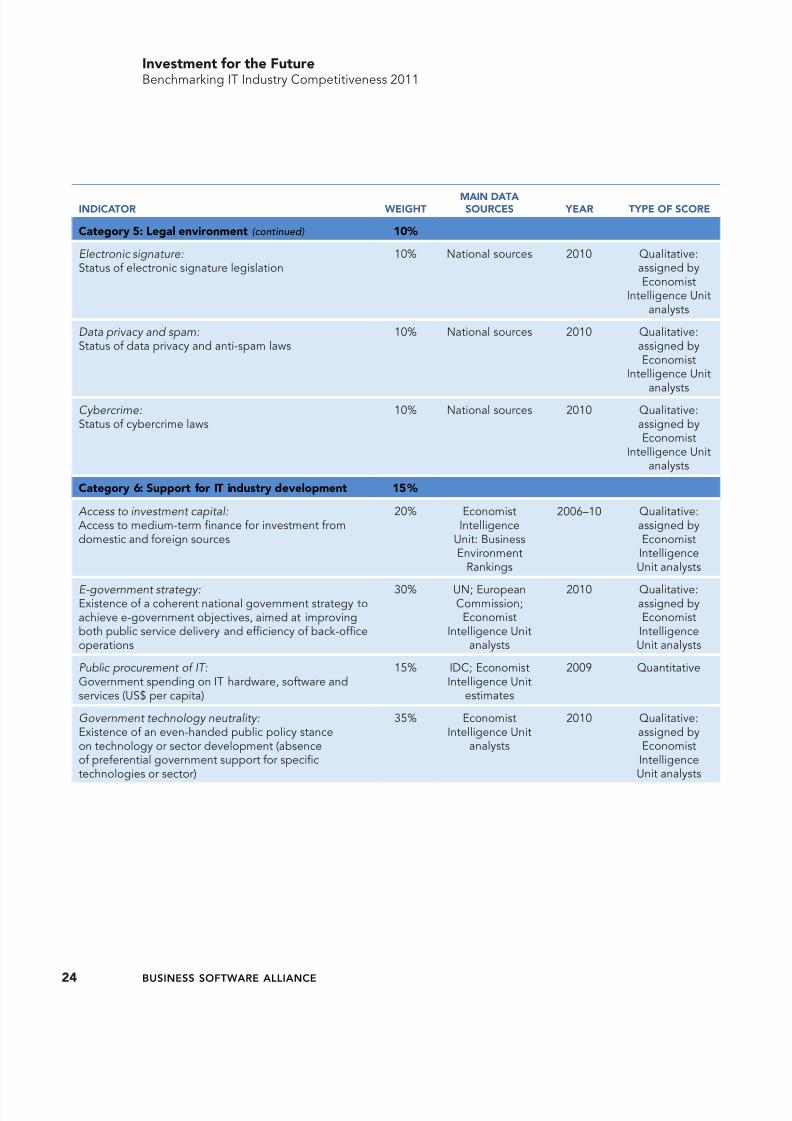

C t gory 6: S pport or IT i d stry d v lopm t 15%

Access to investment capital:Access to medium-term nance or investment romdomestic and oreign sources

20% EconomistIntelligence

Unit: BusinessEnvironment

Rankings

2006–10 Qualitative:assigned byEconomistIntelligenceUnit analysts

E-government strategy:Existence o a coherent national government strategy toachieve e-government objectives, aimed at improvingboth public service delivery and e ciency o back-o ceoperations

30% UN; EuropeanCommission;

EconomistIntelligence Unit

analysts

2010 Qualitative:assigned byEconomistIntelligenceUnit analysts

Public procurement of IT:Government spending on IT hardware, so tware andservices (US$ per capita)

15% IDC; EconomistIntelligence Unit

estimates

2009 Quantitative

Government technology neutrality:Existence o an even-handed public policy stanceon technology or sector development (absenceo pre erential government support or speci ctechnologies or sector)

35% EconomistIntelligence Unit

analysts

2010 Qualitative:assigned byEconomistIntelligenceUnit analysts

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 27/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

25Business so tware allianCe

Rank COunTRY SCORe YoY CHanGe

Th am ric s

1 United States 80.5 +1.6

2 Canada 67.6 -3.7

3 Chile 43.2 -2.9

4 Brazil 39.5 +2.9

5 Mexico 37.0 +4.9

6 Argentina 36.2 -0.2

7 Colombia 33.7 +5.3

8 Peru 25.5 -0.6

9 Venezuela 24.5 +0.1

10 Ecuador 23.1 +0.3 W st r e rop

1 Finland 72.0 -1.6

2 Sweden 69.4 -2.1

3 United Kingdom 68.1 -2.1

4 Denmark 67.9 -0.7

5 Ireland 67.5 +0.6

6 Netherlands 65.8 -4.9

7 Switzerland 65.4 +1.88 Norway 64.3 -2.8

9 Germany 64.1 +6.0

10 Austria 61.4 +4.4

11 France 59.3 +0.1

12 Belgium 57.7 -1.5

13 Italy 50.7 +2.2

14 Spain 50.4 +3.1

15 Portugal 47.1 +1.9

16 Greece 40.7 -2.3

e st r e rop

1 Slovenia 48.8 +3.5

2 Czech Republic 46.1 -0.9

3 Hungary 45.4 -0.7

4 Estonia 45.0 -10.5

5 Poland 44.6 +3.9

6 Slovakia 42.1 +0.7

7 Latvia 41.6 -0.9

app dix 2: I d x Scor s by R gio

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 28/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

26 Business so tware allianCe

Rank COunTRY SCORe YoY CHanGe

e st r e rop (continued)

8 Romania 40.4 +0.8

9 Croatia 39.0 +0.7

10 Lithuania 38.7 -4.6

11 Bulgaria 38.1 +4.5

12 Russia 35.2 -1.5

13 Ukraine 28.9 -2.5

14 Kazakhstan 22.8 -3.6

15 Azerbaijan 20.3 -0.9

Middl e st & a ric1 Israel 65.8 +1.5

2 Turkey 38.7 +5.0

3 South A rica 35.0 -0.3

4 Saudi Arabia 34.1 +0.2

5 Egypt 26.3 -0.4

6 Nigeria 21.4 +2.7

7 Algeria 19.5 -0.3

8 Iran 18.8 +1.7asi -P cifc

1 Singapore 69.8 +1.62 Australia 67.5 -1.1

3 Taiwan 64.4 +1.0

4 Japan 63.4 -1.8

5 New Zealand 61.3 +2.5

6 Hong Kong 60.8 +3.3

7 South Korea 60.8 -1.9

8 Malaysia 44.1 +8.5

9 India 41.6 +7.5

10 China 39.8 +3.1

11 Thailand 30.5 -1.3

12 Philippines 28.4 -0.1

13 Vietnam 27.1 +2.1

14 Sri Lanka 25.0 +1.0

15 Indonesia 24.8 +2.0

16 Pakistan 22.3 +2.4

17 Bangladesh 20.6 -0.5

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 29/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

27Business so tware allianCe

OVeRaLLBuSIneSS

enVIROnMenTIT

InFRaSTRuCTuReHuManCaPITaL

R&DenVIROnMenT

LeGaLenVIROnMenT

SuPPORT FORIT InDuSTRY

DeVeLOPMenT

C t gory W ight 10.0% 20.0% 20.0% 25.0% 10.0% 15.0%

United States 80.5 95.3 76.5 74.1 74.3 92.0 87.2

Finland 72.0 98.2 71.0 52.1 67.3 89.5 78.6

Singapore 69.8 91.0 65.2 51.8 67.2 81.5 82.3

Sweden 69.4 90.1 83.3 46.4 54.9 85.0 81.6United Kingdom 68.1 93.2 74.0 57.5 46.7 88.5 80.0

Denmark 67.9 95.1 87.2 47.9 42.0 90.5 79.0

Canada 67.6 88.3 76.9 53.4 47.6 79.5 85.4

Australia 67.5 92.3 82.4 60.4 32.7 92.5 82.1

Ireland 67.5 96.0 59.3 54.8 55.9 85.0 83.9

Netherlands 65.8 90.1 84.3 43.8 43.8 90.5 74.6

Israel 65.8 81.3 64.4 47.2 71.3 73.0 68.1

Switzerland 65.4 88.3 89.9 40.7 41.3 88.5 75.0

Taiwan 64.4 86.5 54.1 53.7 69.9 74.5 61.4

Norway 64.3 87.4 80.2 46.6 36.8 87.0 82.1Germany 64.1 88.3 70.5 46.0 52.6 90.5 65.1

Japan 63.4 82.9 69.9 50.7 56.9 79.0 58.9

Austria 61.4 87.4 69.9 42.0 40.7 88.5 74.9

New Zealand 61.3 93.4 67.1 56.0 29.2 80.0 80.7

Hong Kong 60.8 97.3 79.7 46.4 23.0 81.0 80.4

South Korea 60.8 79.7 62.4 58.7 46.4 78.5 61.0

France 59.3 82.4 65.8 44.1 40.6 87.0 68.3

Belgium 57.7 89.2 60.1 44.1 34.5 88.5 69.8

Italy 50.7 74.7 50.0 47.0 25.4 80.0 63.2

Spain 50.4 84.4 44.6 47.1 24.4 76.5 66.1

Slovenia 48.8 67.8 41.2 45.9 29.1 73.0 66.7

Portugal 47.1 85.6 47.8 43.3 11.3 76.5 65.9

Czech Republic 46.1 77.3 45.8 43.0 20.4 71.0 56.4

Hungary 45.4 79.1 39.0 44.6 23.1 67.5 55.2

Estonia 45.0 88.3 45.9 44.0 4.3 73.0 65.7

Poland 44.6 76.5 42.8 42.6 18.1 70.0 55.9

app dix 3: I d x Scor s by C t gory

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 30/32

I v stm t or th F t rBenchmarking IT Industry Competitiveness 2011

28 Business so tware allianCe

OVeRaLLBuSIneSS

enVIROnMenTIT

InFRaSTRuCTuReHuManCaPITaL

R&DenVIROnMenT

LeGaLenVIROnMenT

SuPPORT FORIT InDuSTRY

DeVeLOPMenT

Malaysia 44.1 69.6 27.4 29.9 43.9 59.5 58.2

Chile 43.2 94.1 32.3 42.1 1.4 72.5 75.4

Slovakia 42.1 77.1 36.4 37.5 19.1 69.5 52.6

Latvia 41.6 78.6 28.1 45.4 20.1 62.0 52.5

India 41.6 61.8 5.8 52.8 42.9 53.5 51.0

Greece 40.7 72.7 29.0 47.3 11.3 71.0 54.9

Romania 40.4 70.4 31.0 32.9 31.8 56.0 46.7

China 39.8 54.5 18.1 60.4 25.6 59.5 42.2

Brazil 39.5 73.6 25.9 33.1 21.2 58.0 61.3

Croatia 39.0 60.8 36.6 36.4 18.2 59.5 52.0Turkey 38.7 75.9 20.8 38.9 19.4 62.0 54.2

Lithuania 38.7 73.7 34.7 43.5 2.3 67.5 55.5

Bulgaria 38.1 64.2 33.2 36.8 21.7 56.0 44.0

Mexico 37.0 72.5 19.5 33.1 16.3 65.5 57.4

Argentina 36.2 53.9 28.7 38.3 16.8 67.5 43.3

Russia 35.2 48.4 32.0 52.4 15.4 50.0 31.1

South A rica 35.0 57.5 17.5 32.1 18.4 64.5 55.2

Saudi Arabia 34.1 70.0 29.1 32.9 5.6 55.0 51.9

Colombia 33.7 68.5 17.8 25.8 15.1 62.0 54.3

Thailand 30.5 78.8 16.1 34.0 0.3 43.5 54.2Ukraine 28.9 40.3 22.2 37.0 10.8 51.5 34.5

Philippines 28.4 67.8 9.6 34.9 0.0 50.5 51.0

Vietnam 27.1 60.8 23.5 23.5 0.2 50.0 43.5

Egypt 26.3 66.5 10.9 29.9 0.6 42.0 47.9

Peru 25.5 61.5 13.2 21.9 0.2 52.0 47.0

Sri Lanka 25.0 64.5 8.6 20.9 0.1 53.5 48.0

Indonesia 24.8 52.7 7.2 30.1 0.1 48.0 48.0

Venezuela 24.5 46.6 18.0 36.8 0.5 37.0 33.9

Ecuador 23.1 49.9 12.9 22.8 0.3 53.0 37.0

Kazakhstan 22.8 47.3 16.6 23.4 0.7 42.0 38.0

Pakistan 22.3 58.4 2.9 22.8 0.4 41.5 47.5

Nigeria 21.4 42.1 4.4 23.3 3.3 36.5 48.1

Bangladesh 20.6 47.1 0.9 20.1 0.0 40.0 51.0

Azerbaijan 20.3 40.3 9.9 16.8 1.0 50.0 38.0

Algeria 19.5 49.0 8.6 20.2 0.2 35.0 34.9

Iran 18.8 32.9 12.4 23.0 7.6 34.0 20.9

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 31/32

8/3/2019 Bench Marking the IT Industry Competitiveness Index

http://slidepdf.com/reader/full/bench-marking-the-it-industry-competitiveness-index 32/32

BSA Worldwide Headquarters

1150 18th Street, NWSuite 700Washington, DC 20036T: +1.202.872.5500F: +1.202.872.5501

BSA Asia-Pacifc

300 Beach Road#25-08 The ConcourseSingapore 199555T: +65.6292.2072F: +65.6292.6369

BSA Europe, Middle East & A rica

2 Queen Anne’s Gate BuildingsDartmouth StreetLondon, SW1H 9BPUnited KingdomT: +44.207.340.6080F: +44.207.340.6090

Bangkok, Thailand Beijing, China Brussels, Belgium Hanoi, Vietnam Jakarta, Indonesia Kuala Lumpur, MalaysiaMünchen, Germany New Delhi, India São Paulo, Brazil Taipei, Taiwan Tokyo, Japan

www bsa org