benefit strategies and compliance in a health reform era · 2016-07-18 · p agenda i. recap of...

TRANSCRIPT

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

CLAconnect.com

Benefit Strategies and Compliance in a Health Reform Era

Nicole Otto Fallon Director/Consultant Aging Services of MN Institute February 5, 2014

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Agenda

I. Recap of Affordable Care Act Basics

II. Compliance Issues for employers/plan sponsors in 2014 and 2015

III. Evaluating your benefit strategy in a reforming environment – A Panel and Audience Discussion

2

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

3

Recap

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

•The definition of “large employer” varies depending upon the section of the law one is referring to:

Defining Small and Large Employers

For employer penalties:

50 or more full-time

employees plus full-time

equivalents.

FT employee: avg. 30 or more hours of service per week

FT equivalents = Hours worked in a month by all PT employees divided by 120

Eligibility for premium

tax credits:

25 or fewer employees

earning < an avg. of

$50,000

Employer who must auto-enroll: 200 + employees

Eligibility for the SHOP: •Fewer than 50 OR •Fewer than 100

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

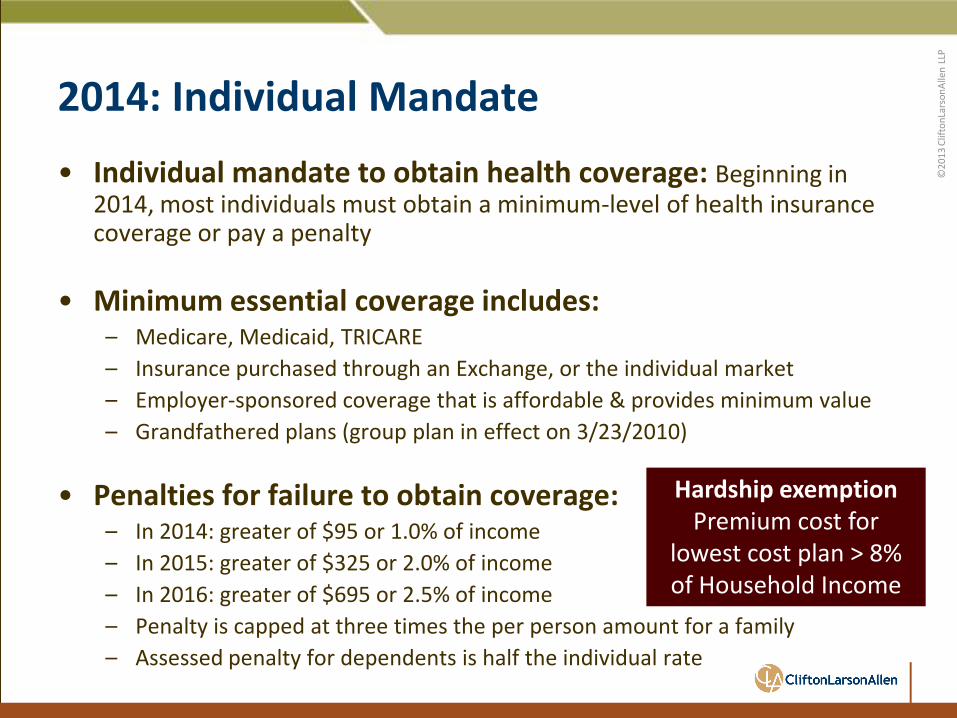

2014: Individual Mandate

• Individual mandate to obtain health coverage: Beginning in 2014, most individuals must obtain a minimum-level of health insurance coverage or pay a penalty

• Minimum essential coverage includes: – Medicare, Medicaid, TRICARE

– Insurance purchased through an Exchange, or the individual market

– Employer-sponsored coverage that is affordable & provides minimum value

– Grandfathered plans (group plan in effect on 3/23/2010)

• Penalties for failure to obtain coverage: – In 2014: greater of $95 or 1.0% of income

– In 2015: greater of $325 or 2.0% of income

– In 2016: greater of $695 or 2.5% of income

– Penalty is capped at three times the per person amount for a family

– Assessed penalty for dependents is half the individual rate

Hardship exemption Premium cost for

lowest cost plan > 8% of Household Income

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

2014: Government Assistance to Help Some Individuals Obtain Coverage • Medicaid expansion: Expands eligibility to

individuals and families up to 133 % of the federal poverty level (FPL) or Modified Adjusted Gross Income(MAGI) of 138% of FPL

– If cost effective, states can opt to subsidize employer-sponsored premiums for this group

• Premium tax credit assistance: Individuals and families with household income of 100 - 400 % FPL may be eligible for sliding-scale

assistance to help pay premiums; • Cost sharing assistance: Those earning

between 100-250% FPL are also eligible for out-of-pocket reductions to help with cost sharing (e.g., maximum out-of-pocket, deductibles, co-payments) if enrolled in a silver plan 6

138% FPL Individual = $16,105 Family of 4 = $32,913

400% FPL: Individual= $46,680 Family of 4= $95,400

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

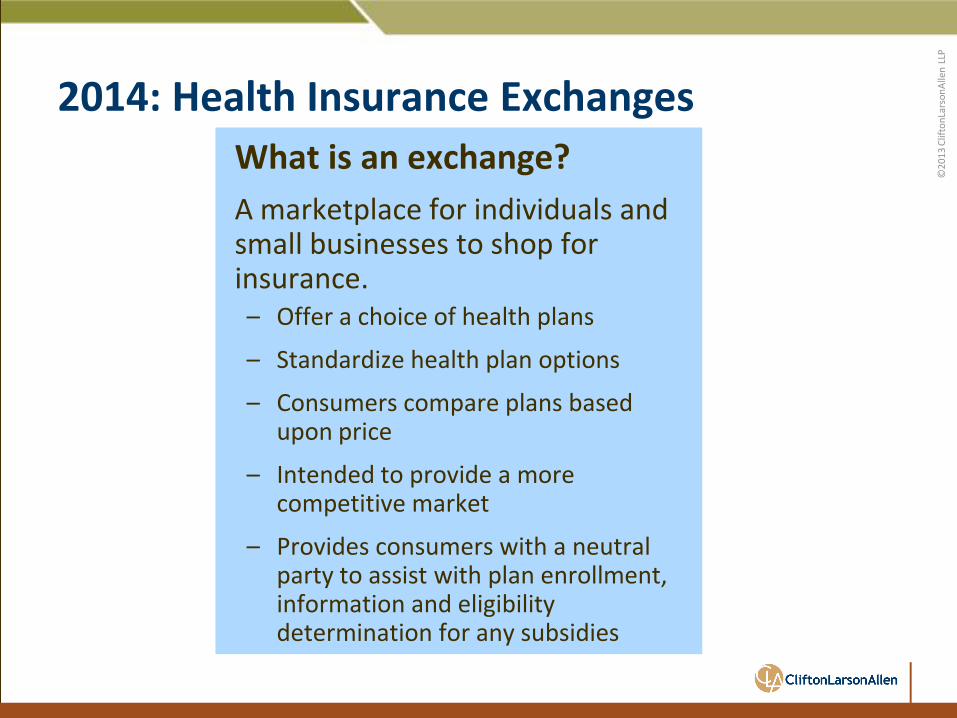

2014: Health Insurance Exchanges

What is an exchange?

A marketplace for individuals and small businesses to shop for insurance. – Offer a choice of health plans

– Standardize health plan options

– Consumers compare plans based upon price

– Intended to provide a more competitive market

– Provides consumers with a neutral party to assist with plan enrollment, information and eligibility determination for any subsidies

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

2014: Exchange Plans

Types of exchange plans to be offered by insurers

– Bronze = 60% actuarial value

– Silver = 70% actuarial value

– Gold = 80% actuarial value

– Platinum = 90% actuarial value

– Catastrophic plan

◊ Only available to individuals < 30 years old, or those exempted from the individual mandate due to unaffordability or hardship.

◊ Plan must cover:

• “minimum essential benefits”

• a minimum of three primary care visits per year

– All exchange “metal” plans must cover essential health benefits, limit cost-sharing and have a specified actuarial value

8

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

9

2015: Potential Large Employer Penalties

•Large employers subject to one of two “shared responsibility” penalties if any FT employee receives Exchange subsidies

–For employers that own multiple companies, the 50 + employees is determined by control group or affiliated service group

Large employer = 50 or more full-time employee + FTEs

FT employee = avg. 30 or more hours of service per week

FT equivalents = Hours worked in a month by all PT employees divided by 120

Law does NOT require employers to offer health insurance

For “minimum essential coverage”, see IRS Notice 2012-31 at: http://www.irs.gov/pub/irs-drop/n-12-31.pdf

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

No Insurance Coverage Penalty • Also applies if coverage not offered to at least 95% of FT

employees and their dependent children under age 26.

Amount = $2000 x each full-time employee (after first 30 employees)

Unaffordable Employer Coverage Penalty If employer fails to offer coverage that is:

1. Minimum essential coverage and minimum 60% actuarial value offered to employees and their children under age 26.

2. Affordable = Employee premium cost for single coverage < 9.5% of household income.

Amount = $3000 x # of full-time employees who receive exchange subsidies

Employer “Shared Responsibility” Penalties

Penalty only assessed if a FT employee receives Exchange subsidies. Employees ineligible for subsidies if employer coverage affordable.

“Affordable” = the employee premium contribution for single coverage is less than 9.5% of their MAGI household income, or one of three employer safe harbor options exist. (e.g., W-2 wages) Maximum penalty = no insurance penalty

Inflationary adjustments to penalties begin in 2015

Employer pays no penalty for Medicaid eligible employees

10

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

2015: Other Employer Requirements

• Beginning in 2015, “large” employers (50 or more FT employees + FTEs) will be required to submit an information return to the IRS, including at least the following: – Names of FT employees on the health plan – Employer contribution levels to employee coverage – Plan waiting period length – Whether employer-sponsored plan meets “minimum essential

coverage” requirements

• Large employers to auto-enroll: Employers with 200+ FT

employees will be required to auto-enroll employees into their employer-sponsored health plan

– Employees can opt out

– Won’t be effective until U.S. Dept. of Labor issues rules. No sooner than 2015.

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

12

Compliance Issues

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

2014

• Payment of ACA-related fees

• 90-day waiting period

• Pre-tax reimbursement limitations

• FSA Carryover Option

• Individual mandate

• Track hours for look-back measurement safe harbor

2015

• Information Return filing

• Large employer pay or play – Affordability

– Minimum Value

– 95% offer

• Non-discrimination rules?

• Documenting safe harbors

• Large employer auto-enroll?

• Smaller employer W-2 health care cost reporting?

13

2014 Compliance Issues

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

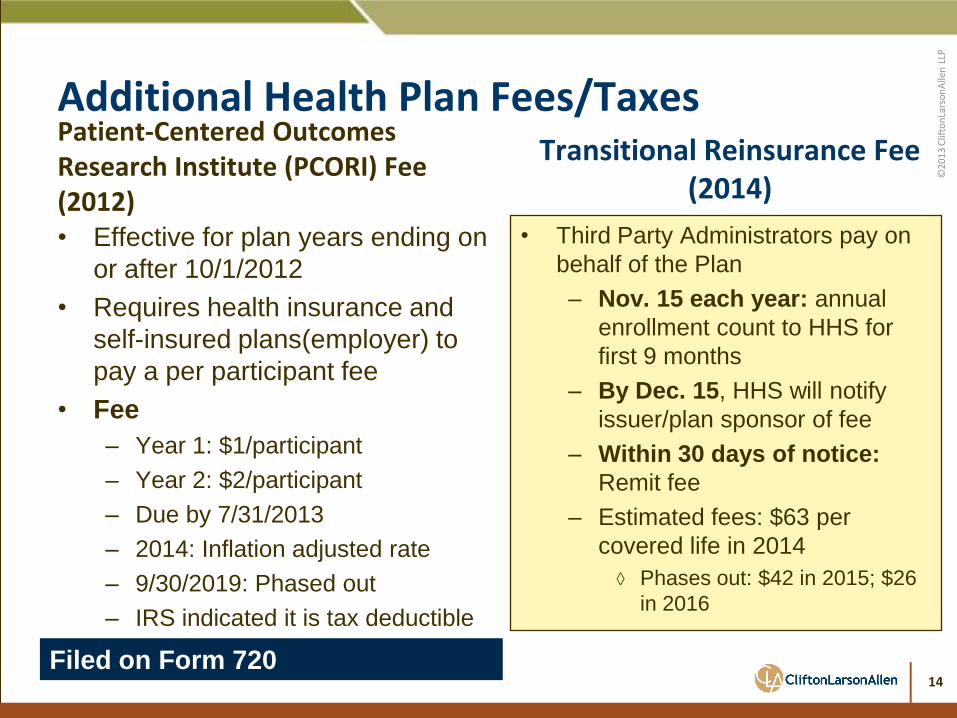

Additional Health Plan Fees/Taxes Patient-Centered Outcomes Research Institute (PCORI) Fee (2012) • Effective for plan years ending on

or after 10/1/2012

• Requires health insurance and

self-insured plans(employer) to

pay a per participant fee

• Fee

– Year 1: $1/participant

– Year 2: $2/participant

– Due by 7/31/2013

– 2014: Inflation adjusted rate

– 9/30/2019: Phased out

– IRS indicated it is tax deductible

Transitional Reinsurance Fee (2014)

• Third Party Administrators pay on

behalf of the Plan

– Nov. 15 each year: annual

enrollment count to HHS for

first 9 months

– By Dec. 15, HHS will notify

issuer/plan sponsor of fee

– Within 30 days of notice:

Remit fee

– Estimated fees: $63 per

covered life in 2014

◊ Phases out: $42 in 2015; $26

in 2016

Filed on Form 720

14

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

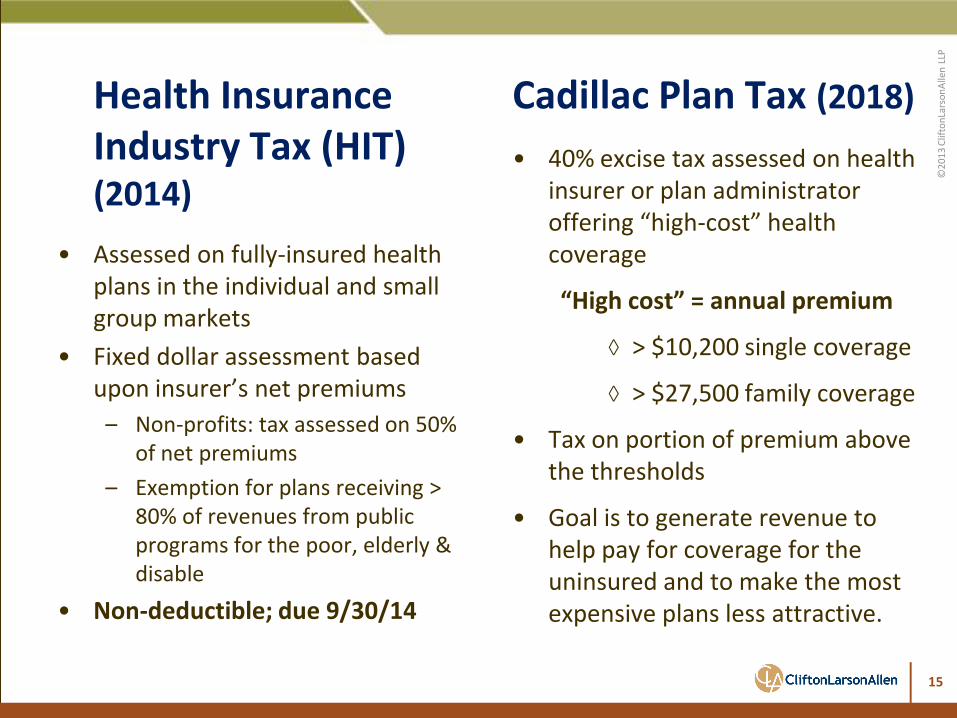

Cadillac Plan Tax (2018)

• 40% excise tax assessed on health insurer or plan administrator offering “high-cost” health coverage

“High cost” = annual premium

◊ > $10,200 single coverage

◊ > $27,500 family coverage

• Tax on portion of premium above the thresholds

• Goal is to generate revenue to help pay for coverage for the uninsured and to make the most expensive plans less attractive.

Health Insurance Industry Tax (HIT) (2014)

• Assessed on fully-insured health plans in the individual and small group markets

• Fixed dollar assessment based upon insurer’s net premiums

– Non-profits: tax assessed on 50% of net premiums

– Exemption for plans receiving > 80% of revenues from public programs for the poor, elderly & disable

• Non-deductible; due 9/30/14

15

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

90 Day Waiting Period: Newly Hired, Full-Time Employees • Beginning January 1, 2014, an employer’s waiting

period for insurance generally cannot exceed 90 calendar days – IRS Notice 2012-59 provided guidance on 90-day waiting limitation

(Public Health Service Act § 2708)

• Newly Hired, Full-Time Employees: If employee is reasonably expected to be full-time, then must be eligible to enroll within 90 days of start date

◊ Not permitted to wait until the 1st of the month after 90 days

◊ May require employers to allow mid-month enrollment or participate well before 90 days have passed

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

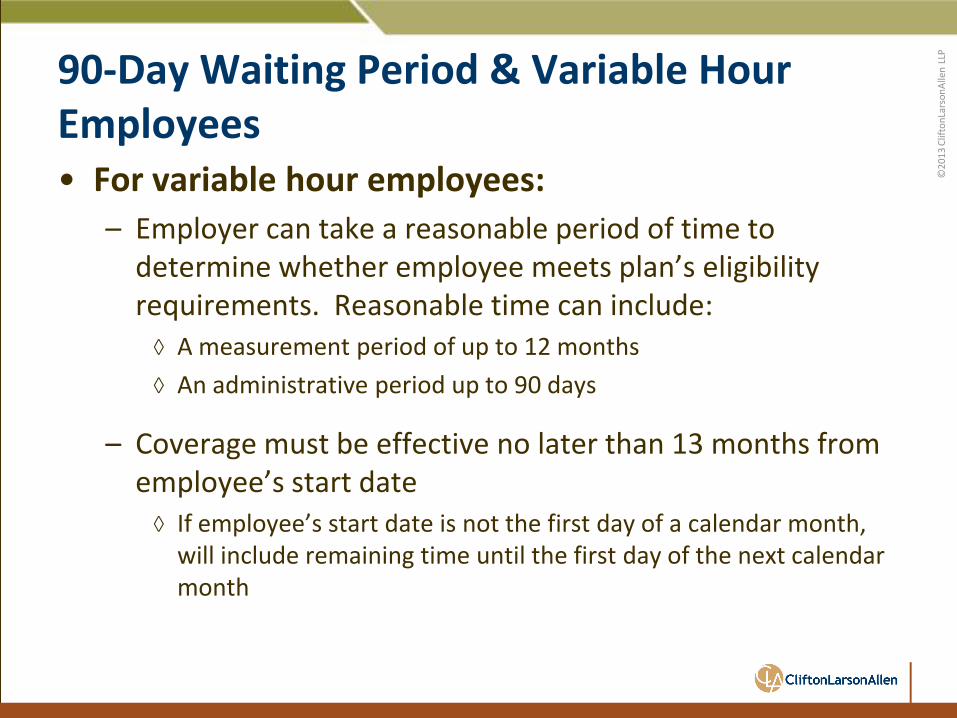

90-Day Waiting Period & Variable Hour Employees • For variable hour employees:

– Employer can take a reasonable period of time to determine whether employee meets plan’s eligibility requirements. Reasonable time can include:

◊ A measurement period of up to 12 months

◊ An administrative period up to 90 days

– Coverage must be effective no later than 13 months from employee’s start date

◊ If employee’s start date is not the first day of a calendar month, will include remaining time until the first day of the next calendar month

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Allowed

• HRAs integrated with Group Health Plan

• Ancillaries – dental, vision, LTC

Prohibited

• HRA + Individual Health Plan

• Pre-tax reimbursement of individual plan premiums

18

Pre-Tax Reimbursement Changes for 2014

•If individual has Minimum Essential Coverage, NOT eligible for Exchange subsidies such as premium tax credits

Minimum essential coverage includes: medical coverage provided through Sec. 125 plans, employer payment plans, health Flexible Spending Accounts, and HRAs

•Pre-2014 HRA contributions, can be used in 2014 and beyond if: •Contribution made before January 1, 2013 •Contributions credited in 2013 to an HRA in effect on 1/1/2013

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

New Carryover Provision for Healthcare Flexible Spending Accounts

• New IRS rules permit plan sponsors to adopt policy allowing employees to carryover up to $500 of their FSA contributions to the next plan year without penalty [IRS Notice

2013-71]

– Effective immediately, but employers decide timing: Can be effective for plan years beginning in 2013, if amendments completed on or before last day of the plan year that begins in 2014.

– Must amend health FSA and Section 125 plan documents to permit carryover option.

– No grace period if carryover option elected

– Carryover amount not subject to $2500 annual contribution limit and can carry forward multiple years 19

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Pending Implementation: Fully-Insured Plans Can No Longer Discriminate • Expands the nondiscrimination rules to cover

fully-insured group health plans (IRS Code Section 105(h), which already applies to self-insured)

– Also includes HRAs or stand-alone Medical Reimbursement Plans (MRPs)

– Affects non-grandfathered plans for plan years beginning on or after 9/23/10

• Penalties – An employer who sponsors a discriminatory

insured group health plan will be subject to an excise tax liability of $100 per day per employee or $36,500 per employee/year

UPDATE: As of 1/18/2014, Obama Administration said they won’t enforce the provision in 2014 because they have not yet issued regulations.

•U. S. Chamber has suggested establishing a single set of non-discrimination rules for self-insured and fully-insured plans

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

21

Evaluating Your Benefit Strategy in a Reforming Environment

A panel and audience discussion

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Factors in Evaluating Health Benefits

• Size of employer: do you have to pay or play?

• Number of full-time employees: what if they all enroll?

• Premium cost: – What can you afford to pay? Can you make it affordable for your

employees?

– How does what employee pays for employer coverage compare to what they would pay for a plan through the Exchange?

• Employer benefit philosophy

• Employee recruitment and retention

• Wages vs. health care benefits: which drives your employees more?

• What will your competitors do?

22

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

What can increase costs?

• Guarantee issue

• No pre-existing conditions

• No annual or lifetime dollar limits on essential benefits

• First dollar coverage for preventive benefits.

• Deductibles and maximum out of pockets Limits

• Broader benefit package

• Claims experience

• ACA fees on insurers

What Can reduce costs?

• Narrow provider networks

• Steep provider discounts on what plans pay

• Higher actuarial value plans

• Skinny benefit set

• Higher deductibles and co-pays

23

What Impacts Premium Costs?

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Health Insurance Premium Tax Credit

Eligibility: Household Income between 100- 400% FPL and NOT eligible for minimum essential coverage

Credit calculation = Premium cost for benchmark plan (second lowest silver plan) – taxpayer’s applicable percentage

24 *Using 2014 Federal Poverty Levels

Household Income

as a % of Federal

Poverty (FPL)

Annual

Income

(Low)

Annual

Income

(High)

Affordable

monthly

premium

for top of

range

Initial

Exchange

Contribution

(% of Income)

Initial

Monthly

Exchange

Premium

Cost

Final

Exchange

Contribution

(% of Income)

Final

Monthly

Exchange

Premium

Cost

Less than 133% FPL $15,521 $15,521 $122.87 2.00% $25.87 2.00% $25.87

133-150% FPL $15,522 $17,505 $138.58 3.00% $38.81 4.00% $58.35

150-200% FPL $17,505 $23,340 $184.78 4.00% $58.35 6.30% $122.54

200-250% FPL $23,340 $29,175 $230.97 6.30% $122.54 8.05% $195.72

250-300% FPL $29,175 $35,010 $277.16 8.05% $195.72 9.50% $277.16

300-400%FPL $35,010 $46,680 $369.55 9.50% $277.16 9.50% $369.55

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Individual Example for Minnesota: Calculating Premium Assistance Tax Credit

•40 year old individual

•Household Income (MAGI) = $28,725 (250% FPL/individual)

•Applicable % = 8.05%

MN Area 1 – SE MN

MN Area 8 - Metro

Benchmark plan $3,588 $1,748

Expected taxpayer contribution

$2,349 $2,349

Credit amount $1,239 $0

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Cost Sharing Subsidies

•Federal government will pay insurers to reduce the cost sharing for individuals:

–Enrolled in a silver-level plan through an Exchange and

–Whose household income is between 100-250% FPL

• Reductions don’t apply to benefits not included in the federal definition of “essential health benefits”

Household income as % of FPL

Cost sharing Reduction

100-200% FPL Two-thirds

200-250% FPL 50%

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Lowest Cost Premiums in Country: MNsure Individual Premiums

27

Anoka, Benton, Carver,

Dakota, Hennepin, Ramsey,

Scott, sherburne, Stearns,

Washington, Wright

Dodge, Fillmore, Freeborn,

Goodhue, Houston, Mower,

Olmstead, Steele, Wabasha,

Winona

Area 8 25 year 40 year 60 year Family

Catastrophic 77 N/A N/A N/A

Bronze 91 115 245 380

Silver 121 154 327 565

Gold 141 180 382 594

Platinum 151 192 408 634

Area 1 25 year 40 year 60 year Family

Catastrophic 126 N/A N/A N/A

Bronze 184 238 512 760

Silver 231 299 644 956

Gold 256 331 713 1058

Platinum 290 375 808 1200

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Identifying Full-Time Employees: 2013 & Beyond • Employee engaged in average of 30 “hours of service” per

week or 130 hours in a month. – Uses common law definition of employee

◊ Does not include: leased employees, sole proprietors, partners in partnership, 2% S-corp shareholder

– Hours of service = hours worked and hours paid but for which no work was performed (e.g., PTO, FMLA, deployment leaves, disability, etc.)

– Salaried workers use actual hours, or 8 hours/day or 40 hours per week standard.

– Special rules for employees of educational institutions

– Seasonal workers: If 120 days or fewer; or 4 calendar months of work, then excluded from calculation of large employer

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Defining which employees are full time

• Why is this important? – Employers must offer to full-time

employees and their children under age 26 health insurance coverage or pay a penalty.

– Penalties are assessed for full-time employees only

– Current FT employees who waive coverage may enroll in ESI in 2014 adding bottom line, non-penalty costs to employers.

– Now is the time to make strategic decisions to limit penalty risk

Strategies •Select measurement and corresponding stability period to capture fewest number of full-time employees.

•Limit employee hours of service to less than 30 hours/week or 130 hours per month.

•If not offering ESI, limit full-time status to 30 or fewer employees across businesses

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Safe Harbor: Look-Back Measurement to Define Full-Time Employee • IRS Notice 2012-58 and Dec. 2012 IRS/HHS proposed

regulations explain a method employers may use to determine full-time status for ongoing employees, new employees, and variable hour and seasonal workers.

30

Measurement Period Admin-istrative Period

Stability Period

3-12 months (employer

determined)

Up to 90 days

Greater of 6 months or

measurement period length

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

The Look Back Measurement Safe Harbor

• This method can be used for ongoing employees, and for new variable hour or seasonal employees

• An “ongoing” employee is someone employed for at least one standard measurement period

• Method cannot be used for new employees who are not variable hour or seasonal

31

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Types of Employees

• Full-time: one who has an average of 30 hours of service per week or

130 hours per month.

• On-going: an employee who has been employed by the employer for at

least one complete standard measurement period.

• Newly hired – Expected to work full time: Up to 90-day waiting period permitted if

full-time. No penalty during waiting period

– Variable Hour: Up to 13 months to determine full-time status and offer coverage before penalty

• Variable hour: An employee for which it is unclear whether they will

average of 30 hours of service/week for an entire measurement period.

• Seasonal: Not been defined for the purposes of this safe harbor, only

for determining if count toward whether an employer is a large employer. Good faith effort is standard for 2014.

32

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Measurement/Stability Periods Can Vary

• May use different measurement/stability periods by classification of employee, including:

1. Collectively bargained employees and non-collectively bargained employees;

2. Salaried employees and hourly employees;

3. Employees of different entities; and

4. Employees located in different states.

• For new variable or seasonal employees, combined measurement and administrative period cannot exceed 13 months after employee’s start date.

33

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

34

Picking a Measurement period

Three-month measurement period, 90-day administrative period

When must employee be covered?

J F M A M J J A S O N D J F M A M J J A S O N D J F M

3 month 125 150 142 139 Coverage required

115 150 100 122 No coverage required

125 153 130 136 Coverage required

115 140 125 127

125 150 142 139

2015 2016 2017

Measurement

Administrative

Stability period - where must offer coverage

Stability period - where no coverage required

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

35

Same Employee Data: 6 & 12 Month Measurement Periods

6 month J F M A M J J A S O N D J F M A M J J A S O N D J F M

125 150 142 115 150 100 130 Coverage Required

125 153 130 115 140 125 131 Coverage required

J F M A M J J A S O N D J F M A M J J A S O N D J F M

12 month 125 150 142 115 150 100 125 153 130 115 140 125 131 Coverage required

2015 2016 2017

2015 2016 2017

Measurement

Administrative

Stability period - where must offer coverage

Stability period - where no coverage required

In both cases, covered for 12 months but in 12-month example, coverage starts in February 2016 instead of October 2015.

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

36

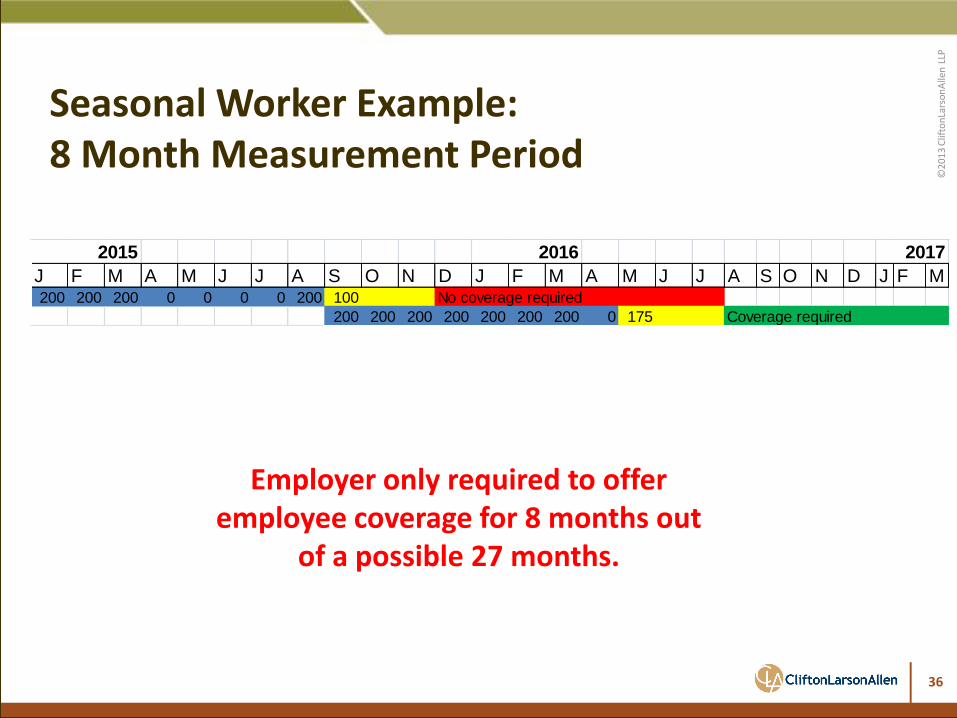

Seasonal Worker Example: 8 Month Measurement Period

8 month measurement period

J F M A M J J A S O N D J F M A M J J A S O N D J F M200 200 200 0 0 0 0 200 100 No coverage required

200 200 200 200 200 200 200 0 175 Coverage required

2015 2016 2017

Employer only required to offer employee coverage for 8 months out

of a possible 27 months.

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Three Employer Affordability Safe Harbors: W-2 Safe Harbor IRS Notice 2012-58

Form W-2 Safe Harbor: If employee’s premium cost for self-only coverage is less than 9.5% of their W-2 wages for the employer, the health insurance is considered affordable AND

– The employer will not pay a penalty for that employee

– The employee may still be eligible for premium tax credits in the Exchange based upon Modified Adjusted Gross Income of Household.

– Employer is not subject to penalty if employee receives tax credit but later employer-sponsored insurance is determined to be affordable.

– Affordability for related individuals: employers don’t need to make coverage affordable for dependents (e.g. family coverage, employee+1)

37

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Affordability Safe Harbors: W-2 (continued)

• Using total amount of wages = Box 1 of Form W-2

– Box 1 does not include employee elective deferrals

• Can include wages paid to employees by a third party that are reported on the W-2 and reflecting the 3rd party EIN

• Determined at the end of calendar year on per employee basis using the year’s W-2 reportable (e.g. compare 2014 premium cost to 2014 Box 1 W-2 wages)

• Could be used prospectively to set employee contribution level to < 9.5% of wages

38

IRS Notice 2012-58 December 2012 proposed regulations

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Affordability Safe Harbors: FPL December 2012 proposed regulations

• Coverage considered affordable for calendar month if employee’s required contribution for lowest-cost self-only coverage that provides minimum value under plan does not exceed 9.5% of Federal Poverty Level (FPL)

– Determined by calculating FPL for single individual (where individual is employed) for applicable calendar year

– Divided by 12

• 2014 FPL for single person = $11,670

– 9.5% of $11,670 = $1108.65/year or $92.38/month

39

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Affordability Safe Harbors: Rate of Pay December 2012 proposed regulations

• Coverage considered affordable for calendar month if employee’s required contribution for month for lowest cost, self-only coverage provides minimum value does not exceed 9.5% of a Rate of Pay Safe Harbor Amount

– Rate of Pay Safe Harbor Amount = 130 hours multiplied by employee’s hourly rate of pay as of the first day of the coverage period (generally first day of plan year)

– Salaried employees use monthly salary instead of hourly rate of pay

• Available as long as employer does not reduce hourly rate of pay or monthly wages during calendar year

40

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Applying the Affordability Safe Harbors: Employee Maximum Premium Payment

Hourly Wage = $8.25/hour

$10,500 W-2 wages

$15,000 $25,000 $35,000

W-2 Safe Harbor

$101.88 $83.12 $118.75 $197.91 $277.08

FPL Safe Harbor

$92.38 $92.38 $92.38 $92.38 $92.38

Rate of Pay Safe Harbor

$101.88

41

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

So, What Does This All Mean?

• Documentation, tracking will be required – Hours, wages, measurement & stability periods

• Forms, forms, and more forms – Fees

– Income taxes, income verification

– Proof of insurance

– W-2s reporting health care benefit costs

– Employers reporting benefit offerings and full-time employees on information returns

• Costs: deductible vs. non-deductible

• Pre-tax benefits narrowing: will it matter?

• Is the non-deductible penalty really a penalty for employers or individuals when compared with health insurance premium costs?

42

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

43

Where to Focus

• Determine and document full-time employees and equivalents

• Are you a large or small employer?

• Evaluate how your benefits compare to what is available in Exchange marketplace.

• If small employer: consider SHOP plan (plus possible tax credit) vs. plan premiums outside the Exchange with no credit.

• Are your employees likely eligible for subsidies through the Exchange?

• Compare non-deductible penalty cost vs. premium contributions (after deductibility, if for-profit)

• Develop processes and procedures for tracking/monitoring

• Hours of service; determine measurement period, if going to use this safe harbor

• Who must be offered coverage

• Waiting period eligibility

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

44

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

CLAconnect.com

twitter.com/ CLAconnect

facebook.com/ cliftonlarsonallen

linkedin.com/company/ cliftonlarsonallen

Nicole O. Fallon Health Care Director/ Consultant CliftonLarsonAllen LLP [email protected] 612-376-4843

Questions?

Thank you!

For more information on health reform: CLAconnect.com/healthreform

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

45

Case Studies: Health Reform in Action

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Senior Service Provider Case Studies

46

Case Study#1 Case Study #1a Case Study #2 Case Study #3

Facility type Non-profit SNF Non-profit SNF For-profit CCRC SNF + AL

Size 85 beds 85 beds 180 Bed SNF 77 Bed SNF

# of employees 79 FT employees 80 FT employees 1922 FT employees 284 FT Employees

Employer contribution to

single coverage (% of total) $7,632/year (85%) $4,534/year (60%) $4,030/year (81%) $5,090/year (66%)

Currently waived employees 34% (or 27 FT employees)

54% (or 43 FT

employees) 31.3% (or 603 FT employees) 57.7% (or 164 FT employees)

# of Medicaid eligible O FT employees 2 FT employees 10.7% (206 FT employees) 6% (17 FT employees)

# of Exchange subsidy eligible

26% of FT employees (21

of 79 FT employees),

many would pay less in

the Exchange vs. ESI

51.3% of FT employees

(41 of 80 FT employees)

3.1% of full-time employees (59 FT

employees), many would pay less in

the Exchange vs. ESI

74.3% of full-time employees (211

FT employees), most would pay

less in the Exchange vs. ESI

Impact of ACAEstimated to pay 11%

less

Estimated to pay 22%

more Estimated to pay 25% more Estimated to pay 12.7% more

Cost drivers

1. A pre-reform

reduction in employer

contribution, resulted

in higher number of

waived employees,

resulting in new costs

for employer post-

reform.

2. Pays "no coverage"

penalty because high

number of subsidy

eligible.

1. Number of waived employees

that will now enroll in ESI

2. Few subsidy eligible employees

(many of whom currently waive ESI)

because FT employee contribution

is affordable for most so most

employees would enroll in ESI

The increased cost is the result of

the fact that as a for-profit they

benefit from the deductibility of

health insurance premiums today

but because of the high number of

employees who would be eligible

to receive subsidies in the

Exchange, the company would

incur $508K in penalties that are

not deductible.

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Employer Health Insurance & Penalty (HIP) Costs

47

Impact of Employer Health Insurance Reforms HEALTH REFORM SUBSIDIES IMPACT ON HEALTH COSTS

Full-Time Employees 80 (37 Insured / 43 Waived) Sample Today's 2015 Offer 2015 Drop/

Total Staffed 92 (0 PT Insured/12 PT No ESI) ($000s) Cost Coverage Don't Offer

2015 PPACA FTEs 89 Baseline Premium Cost 232$ 232$ 232$

HEALTH REFORM KEY DRIVERS 2013-2015 Premium Increase (9.0% / Yr) - 44 44

Single Coverage Employer Premium Cost Pre-Reform Projected Premium Cost 232 276 276

2015 Average Single Employer Cost 4,534$ Tax Adjusted Premium Costs 151 179 179

Current Employer Contribution % 60% PLUS: Additional Reform Impact

Medicaid Eligible Employees Previously Waived FT Employees - 195 -

Total FT Medicaid Enrollees 2 Penalty: Subsidy Eligibles & ESI - 100 -

Employer Estimated Cost Savings 9$ ($000s) Health Reform Increased Cost - 295 -

Employer Unaffordable Coverage Penalty

Subsidy Eligible Full-Time Employees 41 LESS: Previous Premium Liabilities

Subsidy ($3,000) 3$ Medicaid Employee ESI - (9) -

Estimated Subsidy Penalty 123$ ($000s) Subsidy Eligible FT Employees ESI - (224) -

% Total Full-Time Employees 51.3% Health Reform Decreased Cost - (233) -

Employer No ESI Insurance Penalty No Minimal Essential Coverage

Total Full-Time Employees 80 Less: 2015 Inflation Adjusted HC Cost - - (276)

Less: 30 Employees (30) Plus: Subsidy Eligible Penalty - - 100

Adjusted Full-Time Employees 50 Health Reform No ESI Cost - - (176)

No Insurance Penalty ($2,000) 2$ Post Reform HC Costs 232$ 338$ 100

Estimated Subsidy Penalty 100$ ($000s) HC Cost Change to 2015 Projected 62$ (176)$

2015 Pre Reform Projected HC Costs 276$ ($000s) % HC Cost Change to 2015 Projected 22% -64%

Estimated Net Savings 176$ ($000s) Tax Adjusted HC Costs 151$ 255$ 100

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

Employee Exchange Subsidy Eligibility Factors

Exchange Subsidy Eligibility =

ESI Affordability +

Income between

139-400% FPL

In 2015, employer pays penalty when a

FT employee is eligible for

Exchange Subsidy.

48

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

49

2015 Coverage Breakdown

We estimate 51% of your full-time employees will be eligible for Exchange subsidies, 3% employees eligible for Medicaid,

and the remaining 46% enrolled in ESI.

2 , 3%

41 , 51%

37 , 46%

Post Reform ESI FT Employee

Mix

Medicaid

EligibleSubsidy

EligibleESI Coverage

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

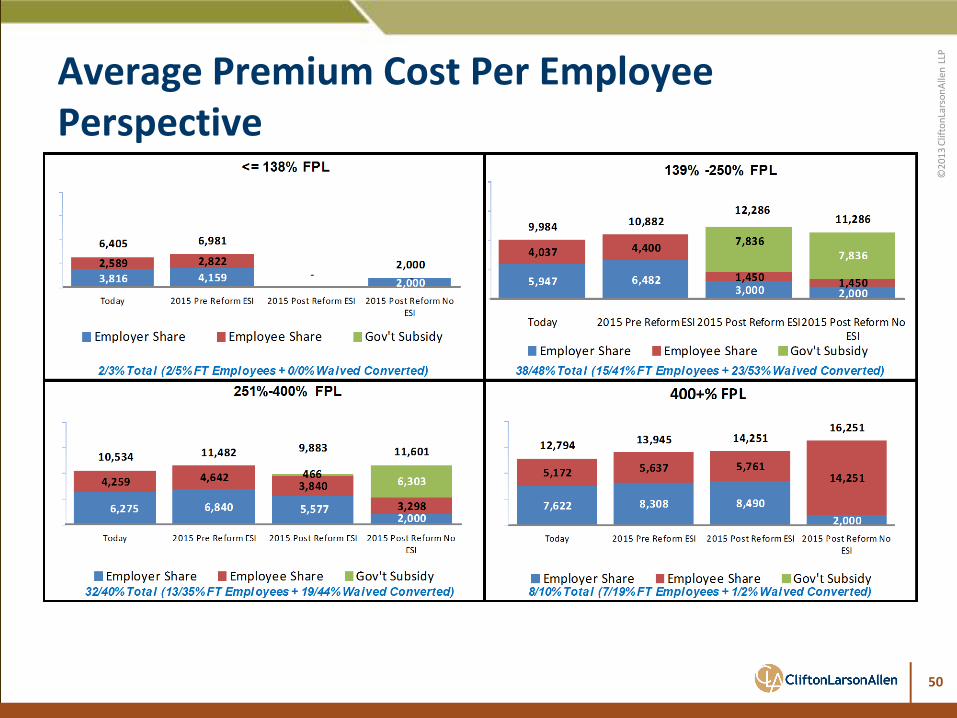

Average Premium Cost Per Employee Perspective

50

©2

01

3 C

lifto

nLa

rso

nA

llen

LLP

2014 Program Eligibility under MNsure & ACA

51

Federal

Poverty

Level Program

100-133% Medicaid

133-200% MinnesotaCare

200-400% MNSure Subsidies

400% + MNSure - full cost