benefits of direct and securitized real estate allocations

TRANSCRIPT

Bene�ts of Direct and Securitized RealEstate Allocations within a Mixed-Asset

PortfolioKaren Mitchell Smith*

INTRODUCTION

It has been found through numerous stud-ies that real estate is an important componentof a well-diversi�ed portfolio. With the adventof ERISA in 1974, pension funds have beeninvesting in real estate through variousvehicles, though most notably through directproperty acquisitions and securitized RealEstate Investment Trusts (REITS).

Modern portfolio theory, developed byHarry Markowitz in 1952, outlines the ben-e�ts of diversi�cation in a manner thatminimizes the variance of a portfolio withoutnecessarily sacri�cing total returns. As anasset class, real estate plays an integral rolein reducing risk in pension funds that focuspredominantly on the mean and variance ofportfolio returns.

Ciochetti, Craft and Shilling1 have shownthat private real estate investment by pen-sion funds has little in�uence over whethersaid fund also participates in securitized REITownership. Thus, the fact that a pension fundmay currently be invested in a single form ofreal estate does not necessarily mean that itwill invest exclusively in that speci�c realestate vehicle.

Hence, is there a fundamental di�erencebetween owning securitized and non-securitized real estate in such a portfolio? Isowning both types of assets in a singleportfolio a form of naive diversi�cation, orcan the argument be made that both types ofreal estate should have a place in an “opti-mal” portfolio allocation? These are twoquestions which will be explored in thispaper.

Indeed, there is a debate in the academicliterature and among practitioners whetherthere is a bene�t derived from direct realestate ownership and securitized real estatesuch as REITs.

Direct real estate is considered to haveadvantageous attributes, such as the abilityto invest in individual properties that aredistinctive in terms of �nancial performance,the potential to provide favorable tax advan-tages, and the fact that direct real estate hasa low, even negative, correlation with the se-curities markets, including that of securitizedreal estate, which makes it an attractivediversi�er to these markets. Disadvantagesinherent in direct real estate are noted as

*Karen Mitchell Smith is a doctoral candidate at the Henley Business School, University of Reading. In additionto attending the Henley Business School, Ms. Smith is a Managing Partner with Graham Mitchell Consultants,specializing in compliance for Investment Management Firms and Hedge Funds. Previously, Karen was employed asthe Head Securities Trader for European Investors, Inc. and Robert E. Torray & Co., Inc.

Editor's Note: Special thanks to Dr. Tom G. Geurts for his editorial comments and encouragement.

Real Estate Review E No. 2© Thomson Reuters

45

Bene�ts of Direct and Securitized RealEstate Allocations within a Mixed-Asset

PortfolioKaren Mitchell Smith*

INTRODUCTION

It has been found through numerous stud-ies that real estate is an important componentof a well-diversi�ed portfolio. With the adventof ERISA in 1974, pension funds have beeninvesting in real estate through variousvehicles, though most notably through directproperty acquisitions and securitized RealEstate Investment Trusts (REITS).

Modern portfolio theory, developed byHarry Markowitz in 1952, outlines the ben-e�ts of diversi�cation in a manner thatminimizes the variance of a portfolio withoutnecessarily sacri�cing total returns. As anasset class, real estate plays an integral rolein reducing risk in pension funds that focuspredominantly on the mean and variance ofportfolio returns.

Ciochetti, Craft and Shilling1 have shownthat private real estate investment by pen-sion funds has little in�uence over whethersaid fund also participates in securitized REITownership. Thus, the fact that a pension fundmay currently be invested in a single form ofreal estate does not necessarily mean that itwill invest exclusively in that speci�c realestate vehicle.

Hence, is there a fundamental di�erencebetween owning securitized and non-securitized real estate in such a portfolio? Isowning both types of assets in a singleportfolio a form of naive diversi�cation, orcan the argument be made that both types ofreal estate should have a place in an “opti-mal” portfolio allocation? These are twoquestions which will be explored in thispaper.

Indeed, there is a debate in the academicliterature and among practitioners whetherthere is a bene�t derived from direct realestate ownership and securitized real estatesuch as REITs.

Direct real estate is considered to haveadvantageous attributes, such as the abilityto invest in individual properties that aredistinctive in terms of �nancial performance,the potential to provide favorable tax advan-tages, and the fact that direct real estate hasa low, even negative, correlation with the se-curities markets, including that of securitizedreal estate, which makes it an attractivediversi�er to these markets. Disadvantagesinherent in direct real estate are noted as

*Karen Mitchell Smith is a doctoral candidate at the Henley Business School, University of Reading. In additionto attending the Henley Business School, Ms. Smith is a Managing Partner with Graham Mitchell Consultants,specializing in compliance for Investment Management Firms and Hedge Funds. Previously, Karen was employed asthe Head Securities Trader for European Investors, Inc. and Robert E. Torray & Co., Inc.

Editor's Note: Special thanks to Dr. Tom G. Geurts for his editorial comments and encouragement.

Real Estate Review E No. 2© Thomson Reuters

45

increased transaction costs, and the illiquid-ity and lack of transparency in this market.

The advantages of the securitized realestate market are that this asset class has apre-established management team that ispresumably knowledgeable within each mar-ket, thus reducing management and searchcosts at the individual pension fund level.Moreover, there is the ability to attain owner-ship positions in a portfolio of properties withless capital outlay through the purchase ofshares of one or multiple REITs. And, Finally,REITs are considered to be a liquid proxy fordirect real estate.

Indeed, Ciochetti, et al2 identi�ed liquidity-constrained pension funds as having thestrongest preference for REITs, thus an es-sential argument involves volatility risk versusilliquidity risk. To illustrate this point, whilethe REIT market is much more liquid thandirect real estate, the NAREIT CompositeIndex, the widely accepted proxy for securi-tized real estate, exhibits the strongest cor-relations to small-cap stocks in the Russell2000 Index (Exhibit I).

The variance of the Russell 2000 Index is10.54%. One of the reasons that the Russell2000 is more volatile than most other classesof equity is because securities with smallermarket capitalization are less liquid, thus thespread between the price bid and the priceo�ered can be much greater than a more liq-uid security.

However, though the historic variance ofthe NAREIT Composite has been substantiallylower than the Russell 2000 at 7.15% (Ex-

hibit I), and though there has been an increasein the average market cap of the REIT mar-ket overall, many of the NAREIT CompositeIndex's constituents either qualify as, orbehave like, small cap stocks. This indicatesthat like direct real estate ownership, there isalso inherent liquidity risk in the REIT marketas well.

As noted by the volatility in the Russell2000, if a security or an index has a smallergeneral market capitalization, a sell-o� of any

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

46

given security, sector, or market may havemuch the same e�ect on liquidity as in directreal estate. Thus, those pension funds invest-ing in securitized real estate for the sole ben-e�t of increased liquidity may experience thesame problems encountered by direct realestate holders during a market downturn: il-liquidity, a lack of transparency, and the saleof shares below what would be consideredreasonable given the value of the underlyingassets.

REAL ESTATE MARKETS AND PENSION

ALLOCATIONS

Following the �ndings of Chun, Chiochetti,and Shilling3 that the inclusion of real estatein a stock-and-bond portfolio improves apension plan's overall returns in a mean-variance space, a ‘typical’ pension portfoliowould consist of large, mid, and small-capequities, bonds, and real estate. Thoughprevious studies suggest that an optimal realestate allocation for an institutional portfoliois roughly 30–35%4, pension funds have al-locations of only 2–3% in this asset class5.

The commercial real estate market isvalued at an estimated at $4.6 trillion andpension funds account for approximately23.3% of the investment in this sector6. Asnoted above, actual real estate allocationswithin pension funds are far below what theyshould be for optimal performance. However,given the size of the overall real estate mar-ket, it is ever more possible to satisfy inincrease in real estate allocations within pen-sion funds without sacri�cing the bene�ts ofthe asset class itself.

INDICES

In looking at the question of direct andsecuritized real estate and their place in apension fund, a number of indices were used

in this paper's analysis to represent theaforementioned ‘typical’ pension fund's do-mestic allocation choices: Large-cap, mid-cap, and small-cap stocks represented bythe Dow Jones Industrial Average (INDU), theStandard & Poor's 500 (SPX), and the Rus-sell 2000 (RTY) indices respectively.

The bond allocation is represented by theSmith Barney Broad Investment Grade BondIndex (SBBIG), and securitized real estate bythe FTSE NAREIT Composite Index(FNCOTR).

For direct real estate, there are two indi-ces; the appraisal based NCREIF Index (NPI)and the MIT Transactions-Based Index (TBI).7

The rationale for including two direct realestate indices is the following: The NPI Indexis based on appraised values, not historicalcost. This gives rise to two major issues withcomparing it to securitized indices.

First, there is the potential for an arti�cial‘smoothing’ of data that is inherent in the ap-praisal process that arti�cially lowers thevariance of the NPI.8 There have been stud-ies, such as the one done by Salama9 who‘unsmoothed’ the NPI data and the result wasa much higher risk rate than the NPI indicates.However, there have also been studies thatshow that the long term low variance of theNPI is more of a result of the lease structurethat provides a more stable income streamthan that of stocks and bonds.10 Second, theinfrequency of the appraisals in the NPImeans that the index lags changes in theactual value of real estate.11 This means thatthough the index is reported quarterly, theentire index is only updated partially eachquarter as opposed to the securities indiceswhich are updated daily to re�ect changes totheir constituents.

To strengthen our analysis and following

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

47

the idea presented by Geltner and Gatzla�12

regarding a transactions-based index thatwould address the issues with the NPI, thedata of the MIT Transactions-Based Index(TBI) was added to our data set. The TBI isan index that uses the recent appraisedvalues of properties in the NPI as a compos-ite hedonic variable and represents transac-tion prices that re�ect variable liquidity in thereal estate marketplace over time by apply-ing the methodology outlined in Fischer, etal.13 Additionally, the NPI Index reports thepre-tax, unlevered total returns (incomereturn and capital value return) that are grossof management fees of institutional-gradecommercial properties. As noted by Pagliariand Webb14, the NPI Index does not take intoaccount “dividends”15 paid by reportingproperties.

Dividends and dividend yields play a largerole in the performance of the securitized in-dices as well, so rather than employ Pagliariet al's process of creating a dividend seriesby subtracting capital improvements from theNOI, all of the returns used in this paper'sanalysis of the indices are calculated on ahistorical price-traded basis, non-inclusive ofdividends, so as to provide a more uniformcomparison. The assumption is made that alldividends have been paid out and there is noreinvestment of income.

Another index-related consideration in-volved in this paper's methodology was the

disparity between the levered FNCOTRindex, and the unlevered NPI and TBI indices.However, the author of this paper is examin-ing securitized and direct real estate bothseparately and together in relation to optimalportfolio allocations rather than comparingthe two for similarity. They are then evalu-ated as to how each performs as its own as-set class and what then the optimal alloca-tion would be for each class.

Finally, the author does not separate fundsby liquidity or by examining the timeframesfor pension liability16 as these factors are dif-�cult to standardize over multiple timeperiods. Rather, the focus is on investigatingallocations strictly in relationship to Markow-itz's e�cient frontier.

RETURNS, VOLATILITY, AND CORRELA-

TIONS

The average returns over 10-, 15-, and20-year annual time frames are shown in Ex-hibit II. Note that for all of the time-frames, ona price-traded basis, real estate outper-formed all of the asset classes. The FNCOTRwas �rst in the 15- and 20-year time frameswith the TBI �rst in the 10-year time frame.The 20-year time frame does include thestock market crash of 1987, as well as theperiod between 1987 and 1993 marked bythe RTC. Thus, this period incorporatesperiods marked by volatility and illiquidity forall asset classes.

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

48

Volatility during the same time periodsnoted above, as represented by standarddeviations in Exhibit III, shows that the Rus-

sell 2000 Index possesses the greatest vari-ance in all noted periods.

Examining the volatility of both direct realestate indices and the bond index, the great-est period of volatility is the 20-year periodwith each successive period examined il-lustrating a progressive decline in volatility,with the 10-year period being least volatile.However, each of the securities indices,including the FNCOTR, exhibits the greatestvolatility over the 10-year period, followed bythe 20-year period that is inclusive of thestock market crash. It appears that the stockmarket crash had more of an e�ect on thevolatility of the equity markets than did theperiod marked by the RTC for the direct realestate markets.

The NPI consistently exhibits the lowestvolatility in all time periods, followed by thebond index, though this may be a result ofthe previously noted data smoothing relativeto the appraisal process.

In fact, within the 20-year time period of

March 1987 through March 2007, the NPIonly reported below average quarterly returnsin the years 1991, 1992, and 1993. Althoughthe volatility of the FNCOTR is greater thaneither the NPI or the TBI, when looking atsecuritized real estate, it is still lower than allof the other securities indices. Hence, pen-sion funds, with their need to limit downsiderisk, should �nd a combination of both directreal estate and securitized real estate a bet-ter investment option over the long term inrelationship to either stocks or bonds inregards to both the returns noted above andthe lower risk variables noted here.

Correlations for the di�erent time periodsare shown in Exhibit IV. This con�rms earlier�ndings17 as the NPI exhibits the lowest rela-tionship to any of the other indices. TheFNCOTR had the least correlation to the NPIand TBI indices than with any of the securi-tized indices, with the highest correlation be-ing with that of small cap stocks. These cor-

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

49

relations, or lack of correlations, give strengthto the argument that there is a place for bothsecuritized and non-securitized real estate ina mixed-asset portfolio.

In addition; looking at the NPI and the TBI,we see that they are becoming more posi-tively correlated with the securities marketswhile the FNCOTR is becoming less so. Thus,

the relative weightings for portfolios holdingboth forms of real estate may shift substan-tially as direct real estate becomes more cor-related to the securities markets includingsecuritized real estate as direct real estateloses some of the diversi�cation bene�tssought by pension funds.

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

50

OPTIMAL PORTFOLIOS

The data that is being used is historical innature, thus any interpretations of the data

should not be inferred as a guarantee offuture performance. All portfolios were runincorporating some form of real estate based

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

51

on the assertion that real estate should bean integral part of a well-diversi�ed pensionportfolio.

Examining the optimization results usingthe appraisal based NPI and the securitizedFNCOTR for the 20-year period (Exhibit V), itwas found that direct real estate accountsfor the sole allocation to real estate when theexpected return rates are in the higherranges of 8%-10%. The variances for these

portfolios are also higher than the combinedreal estate allocations exhibited in the lowerexpected return range, at 1.23% to 5.75%,though they are considerably lower than theequity-only return and variance of 11% and9.62% respectively.

Thus, a portfolio that does not include realestate may expect an additional 1% in returnover one that includes real estate, but this istempered by an additional 3.87% in variance.

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

52

It is also at the 10% expected rate of returnthat an allocation is made to real estate, andsaid allocation is made in the form of directreal estate rather than securitized real estate.As the expected returns drop, it is found thatthe overall allocation to real estate increases.Hence, any allocation to real estate lowers

the overall risk in a portfolio, and for thosefunds looking for returns of 7% or less, thebest way to achieve those goals is throughinvestment in both direct and securitized realestate.

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

53

The same phenomenon is found in thetransactions-based TBI over the same period(Exhibit VI), though the overall allocation toreal estate drops considerably for the sameexpected rates of return with an increase ininvestment to bonds to make up thedi�erence. The allocations to the FNCOTRfor both indices, given the expected returnsof 6–7%, are within 200bp of each other,though the direct real estate allocations varyby half in each case.

Thus, despite the fact that both direct realestate indices show the closest correlationto each other relative to the other indicesused in the analysis and that the TBI is onlynominally correlated to the SBBIG, on acomparative basis there is a marked di�er-ence between the appraisal-based andtransaction-based direct real estateallocations.

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

54

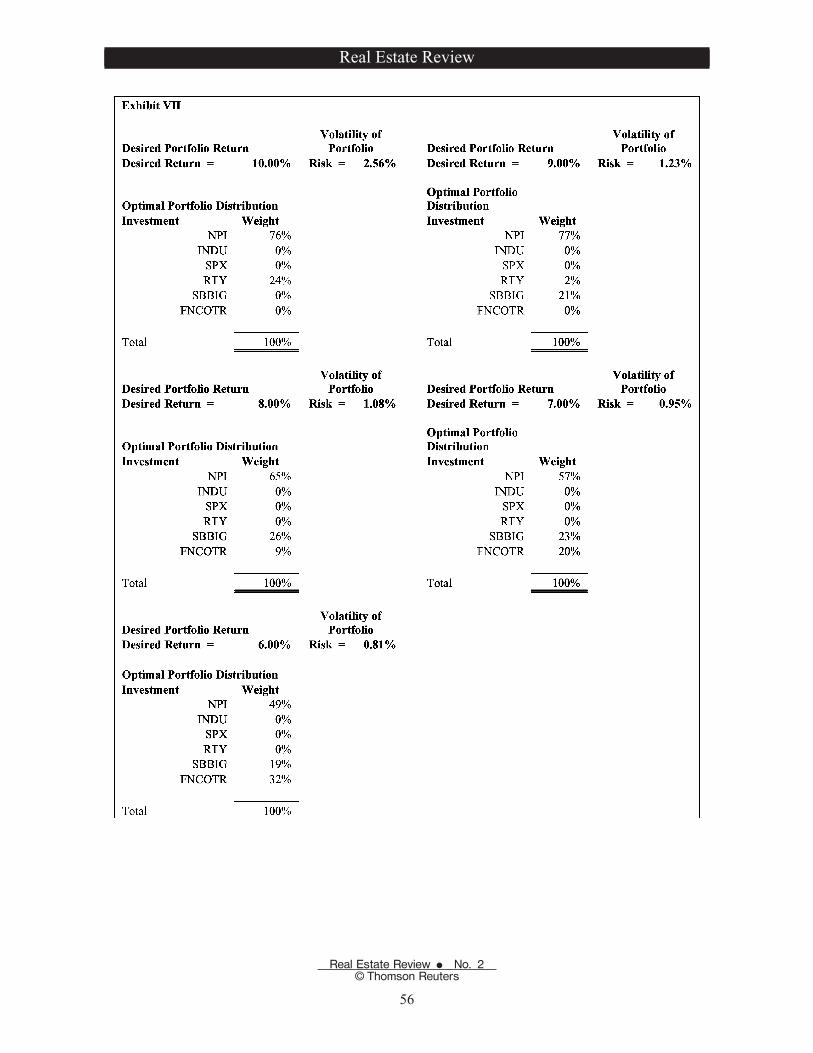

Over the 15-year period, the results re�ectthose of the 20-year period (Exhibit VII & Ex-hibit VIII), though the combination of realestate products does not come into play untilthe portfolio has an expected 8% annual rateof return. The largest total allocation to real

estate is seen in a portfolio with a 6% ex-pected rate of return and is found to decreasewith each percentage increase in expectedreturn, though real estate in some form isfound to be a part of each allocation.

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

55

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

56

In examining the 10-year period, the samegeneral pattern is found as noted in the 15-and 20-year time frames. However, the al-

location to real estate overall is higher forthis period with the highest percentage being

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

57

found in the portfolio with a 6% expectedreturn.

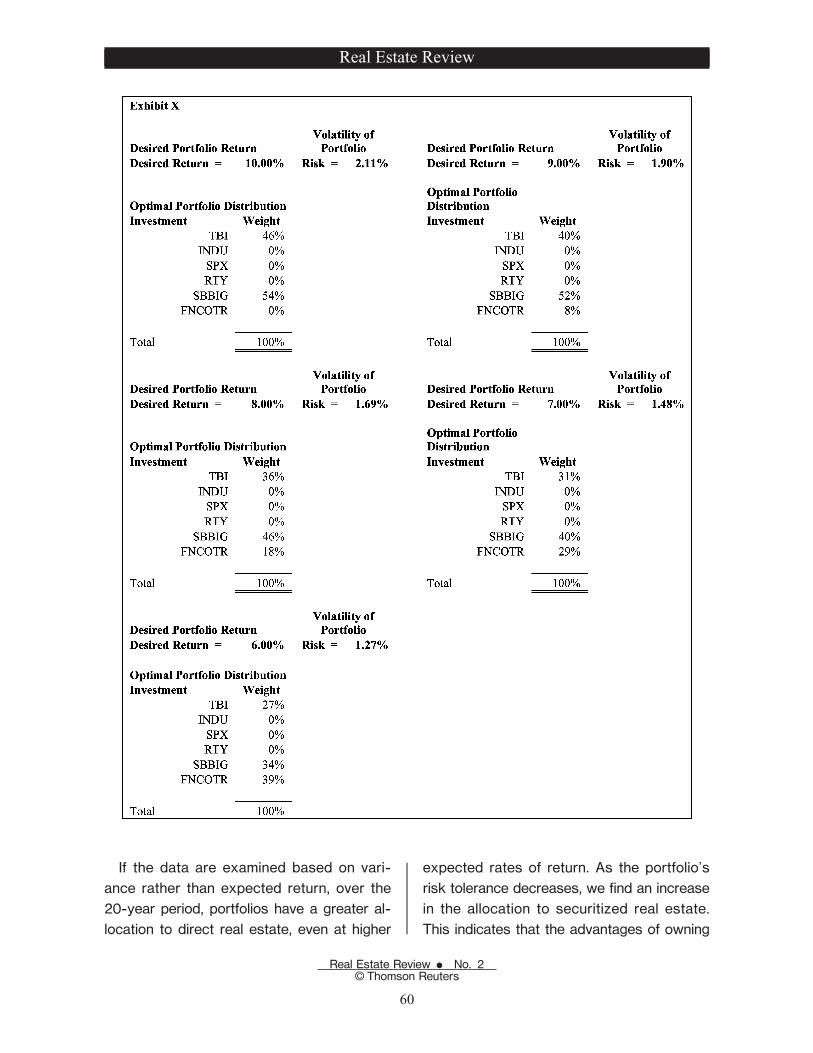

Though, as in the other time frames, theoverall allocation to real estate diminishes asthe expected rate of return increases, thecombination of securitized and direct realestate allocations begins at a much higherlevel of expected returns (Exhibit IX & ExhibitX). This can be explained by both the favor-

able rate of return of real estate relative tothe general securities markets during thistime period, and the lower risk attributed tothese investments.

Of note, the TBI index and the FNCOTRindex are not closely correlated until the 10-year timeframe, but the allocations to thepension portfolios are more similar than theNPI.

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

58

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

59

If the data are examined based on vari-ance rather than expected return, over the20-year period, portfolios have a greater al-location to direct real estate, even at higher

expected rates of return. As the portfolio'srisk tolerance decreases, we �nd an increasein the allocation to securitized real estate.This indicates that the advantages of owning

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

60

direct real estate outweigh the inherent dis-advantages, as re�ected in a mean-varianceportfolio.

The percentages of securitized real estateallocated to the portfolio increase as the al-locations to direct real estate decrease,though not in the same proportion (ExhibitXI). This pattern is even more pronounced in

the 15-year time horizon (Exhibit XII). How-ever, during the 10-year period, real estate,both securitized and direct, has heavy, andusually dual, weightings within the lower risk-tolerance portfolios (Exhibit XIII). This is,again, attributed to the superior performanceand lower variance as compared to the otherindices.

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

61

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

62

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

63

CONCLUSION

This study has examined the relationshipbetween direct real estate allocations andsecuritized real estate allocations in a mean

and variance of return-focused pensionportfolio. Any allocation to real estate lowersthe overall risk in a portfolio, though in thecase of funds looking for greater returns andthat have a higher risk tolerance, this study

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

64

has clearly shown that an allocation to directreal estate is more favorable than an alloca-tion to securitized real estate.

When looking at direct real estate, thereare signi�cant di�erences to both overall al-locations to real estate and the speci�c directreal estate allocation when incorporating thetransactions-based index v. the appraisal-based index into a portfolio using the identi-cal parameters. Funds with a lower risk tol-erance bene�t from a greater weight in realestate in either form, or in combination, as apercentage of their overall portfolio.

A portfolio with expected returns of 8% orlower bene�t the most from an allocation toboth direct and securitized real estate, withsecuritized real estate becoming more heavilyweighted as expected returns decrease.Finally, funds with a time horizon in the rangeof 10-years would have been the greatestbene�ciaries of both an increased allocationto real estate overall, and a dual allocation ofdirect and securitized real estate.

Though the allocation levels outlined in thisstudy are unlikely objectives for all pensionfunds, it is clearly shown that not only arepension fund target allocations below whatthey should be for optimal performance18 butthe author has also shown that direct realestate and securitized real estate both havea place within the asset allocation framework.The data also have shown that the relativeweightings for portfolios holding both formsof real estate may shift substantially if directreal estate continues to become more closelycorrelated to the securities markets.

For a pension fund looking to minimize theprobability of not realizing anticipated returns,both securitized real estate and direct realestate have been shown to be important con-stituents in portfolios across a wide range of

expected risk and returns. More importantly,one should consider each form of real estateto be a separate allocation category, eachable to act in a complimentary fashion withinthe framework of a fully optimized pensionportfolio.

NOTES:

1Ciochetti, B. A., Craft, T. M., & Shilling, J. D.(2002). Institutional Investors' Preferences for REITStocks. Real Estate Economics, 30 (4), 567–593.

2Ciochetti, B. A., Craft, T. M., & Shilling, J. D.(2002). Institutional Investors' Preferences for REITStocks. Real Estate Economics, 30 (4), 567–593.

3Chun, G. H., Ciochetti, B. A., & Shilling, J. D.(2000). Pension-Plan Real Estate Investment in anAsset-Laibility Framework. Real Estate Economics, 28(3), 467–491.

4Geltner, D., Rodriguez, J., & O'Connor, D. (1995).The similar genetics of public and private real estateand the optimal long-horizon portfolio mix. Real EstateFinance, 12 (3), 13–26.

5Ciochetti, B. A., Craft, T. M., & Shilling, J. D.(2002). Institutional Investors' Preferences for REITStocks. Real Estate Economics, 30 (4), 567–593.

6Ibbotson Associates Global Real Estate Study:Optimizing Portfolios With Global Listed Real EstateAllocations. (2007, May). Retrieved June 2007, fromNational Association of Real Estate Investment TrustsWeb Site: www.investinreits.com/webinar/IbbotsonSummary.pdf

7All quarterly data for the range March 1987–March 2007 was sourced through Bloomberg FinanceL.P. and the MIT Center for Real Estate (Transactions-Based Index (TBI). (n.d.). Retrieved June 2007, fromMIT Center for Real Estate Commercial RE Data Labo-ratory all-QuarterlyIndex.csv: http://web.mit.edu/CRE/research/credl/tbi.html)

8Geltner, D. M. (1993). Estimating Market Valuesfrom Appriased Values without Assuming an E�cientMarket. Journal of Real Estate Research, 8 (3), 325–345.

9Salama, K. (1995). Measuring Risk in CommercialRea lEstate Investments, Real Estate Investing in the1990's. ICFA Continuing Education. Charlottesville, VA,:AIMR.

10Linneman, P. (1989, September). Limitations ofthe FRC Index. Baring Investment Property Bulletin, 1(2), 1–4.

11Gyourko, J., & Keim, D. B. (1993). Risk andReturn in Real Estate: Evidence from a Real EstateStock Index. Financial Analysts Journal, 49 (5), 39–46.

12Gatzla�, D., & Geltner, D. (1998, Spring). ATransaction-Based Index of Commercial Property and

Bene�ts of Direct and Securitized Real Estate Allocations within a Mixed-AssetPortfolio

Real Estate Review E No. 2© Thomson Reuters

65

its Comparison to the NCREIF Index. Real EstateFinance, 7–22.

13Fisher, J., Gatzla�, D., Geltner, D., & Haurin, D.(n.d.). Controlling for the Impact of Variable Liquidity inCommercial Real Estate Price Indices. Retrieved June2007, from MIT Transactions-Based Index (TBI):http://web.mit.edu/CRE/research/credl/pfd/FGGH�Variable�Liq�RRE.pdf

14Pagliari, J. J., & Webb, J. R. (1995). A FundamentalExamination of Securitized and Unsecuritized RealEstate. The Journal of Real Estate Research, 10, 381–425.

15As typically reported, the NACREIF PropertyIndex publishes income, based on net operating income,

and appreciation returns. Pagliari and Webb were ableto obtain additional data outlining capital improvements,partial sales, and beginning and ending asset values.The authors then accounted for a separate “dividendseries” that they approximated by subtracting capitalimprovements from net operating income.

16Ciochetti, B. A., Craft, T. M., & Shilling, J. D.(2002). Institutional Investors' Preferences for REITStocks. Real Estate Economics, 30 (4), 567–593.

17Mueller, A. G., & Mueller, G. R. (2003). Public andPrivate Real Estate in a Mixed-Asset Portfolio. Journalof Real Estate Portfolio Management, 9 (3), 193–203.

18The results of which are in line with previousstudies.

Real Estate Review

Real Estate Review E No. 2© Thomson Reuters

66