best practices for plan fiduciaries - vanguard€¦ · · 2013-12-16to be effective in today’s...

TRANSCRIPT

Best practices for plan fiduciaries

> ContentsIntroduction

A brief history of pension law 1

Fundamentals of fiduciary responsibilities 5

Fiduciary best practices

Organization of committees 11

Investment selection and monitoring 17

Administrative oversight 25

Plan costs 31

Legally, the fiduciary standard of ERISA

is one of the highest the law recognizes.

Plan fiduciaries are held to an exceptional

level of duty and care under the law,

including the assumption of personal

liability for fiduciary decision-making.

All fiduciary responsibilities must be

discharged solely in the interest of the

plan’s participants and beneficiaries.

Additional fiduciary considerations

DB funding 39

Section 404(c) compliance and additional fiduciary protections 45

Participant education and advice 49

Company stock 53

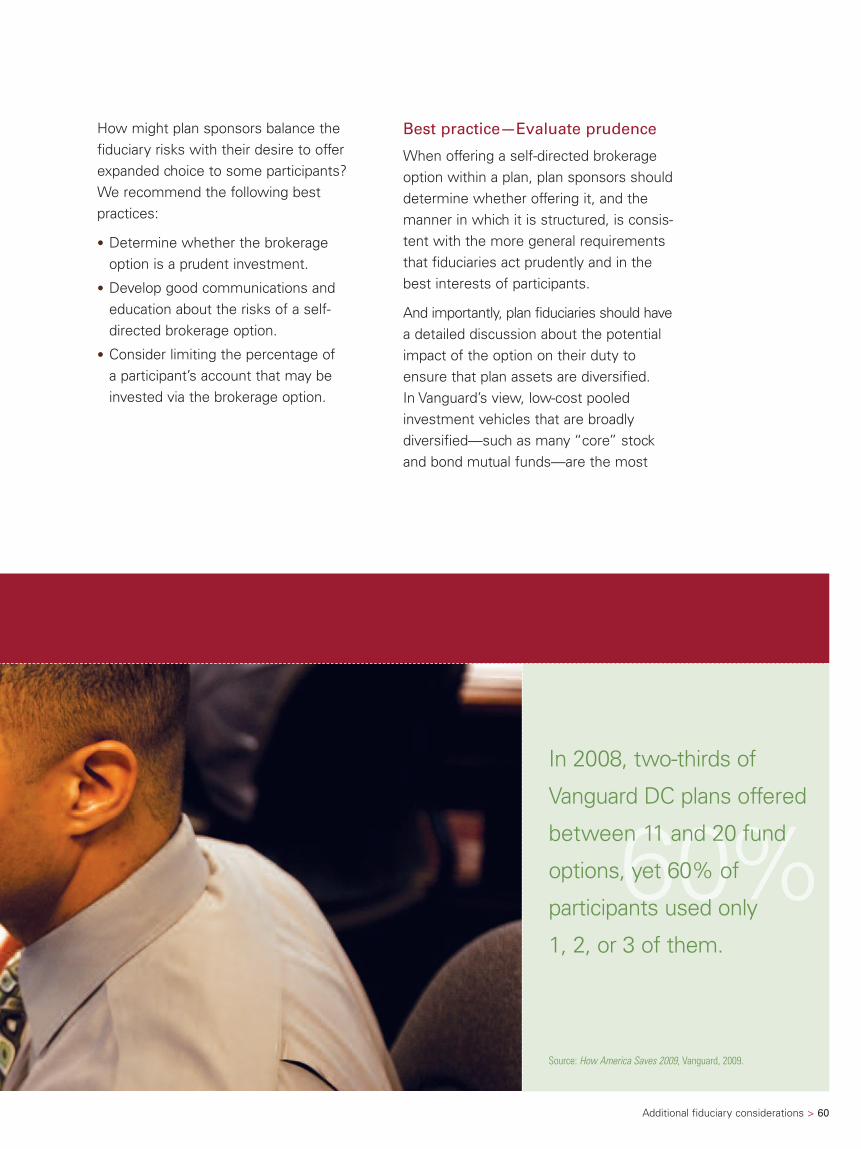

Brokerage accounts 59

To be effective in today’s ever-changing fiduciary environment, you need an experiencedpartner for knowledge, insight, and support. As head of Vanguard Strategic RetirementConsulting (SRC), I can assure you that our team of actuaries, attorneys, and benefitsprofessionals can help you fulfill your fiduciary responsibilities.

In this booklet, SRC provides a perspective on fiduciary duties and recommends bestpractices you should consider implementing to minimize risk and achieve positive resultswith your retirement plans. This guide to best practices will serve as a road map to yourfiduciary duties. We hope to clarify—and simplify—what it means to take on ERISA fiduciary responsibility.

While Vanguard provides many services to help clients satisfy ERISA duties, there arecertain steps employers need to take on their own. These steps are presented in thisguide, as well as in a companion piece that provides a concise checklist to best practices.Vanguard and SRC’s team of strategic consultants are available to help you and your fiduciary committees understand and execute these requirements.

The guide and checklist also summarize many ways Vanguard helps you satisfy your fiduciary responsibilities. Beyond the list of specific services, Vanguard’s unique corporatestructure, which helps us avoid conflicts of interest and maintains our singular focus onmeeting the needs of our shareholders, is a tremendous advantage for employers.

In short, this Fiduciary Best Practices booklet is designed to educate you and your retirement-plan committee on the key fiduciary duties related to the investment management and administration of your retirement plans.

We hope you find this guide useful. Please contact your relationship manager to discuss any questions.

Sincerely,

Ann L. Combs, PrincipalVanguard Strategic Retirement Consulting

> Introduction

1 > Introduction

Congress enacted theEmployee Retirement Income SecurityAct (ERISA). At the time, 80% of plan participants in private-sector retirementplans were covered by defined benefit(DB) programs, and the legislation wasdesigned to strengthen the DB systemwith a national standard of fiduciary conduct. The fiduciary sections of ERISAset a new, nationwide standard for themanagement and oversight of private pension plans, including broad fiduciaryprinciples and specific rules prohibitingconflicts of interest (referred to as prohibited transactions). Additionally, anew federal agency, the Pension BenefitGuaranty Corporation (PBGC), was created

to provide federal financial backing to privatepension benefits if a plan failed. ERISA wasenacted in an effort to address weaknessesin the DB system, including inadequateplan funding and overconcentration of planinvestments in employer securities.

The shift from DB to DC plans

ERISA was designed with a specific modelof pension-plan governance in mind. Atthe core of the decision-making process is a fiduciary, overseeing DB plan assetsfor an essentially passive and uninvolvedgroup of plan participants. Pension planswere employer-funded and invested, witha committee making all decisions, assistedas needed by various professional

In 1974,

> A brief history of pension law

Introduction > 2

80%

advisors and service providers. While therewere defined contribution (DC) plans inexistence at the time of ERISA’s adoption,most were also employer-funded andemployer-invested. These DC plans wereoften intended as supplemental benefitprograms, not as the core retirement benefit.

Today the world of private pension planshas been transformed. More than 80% of all private-sector workers with employerretirement plans have DC accounts. Insuch plans, participant contributionsaccount for the majority of plan funding(through elective salary deferrals), and participants are responsible for most saving and investment decisions.

Over the years, regulations have evolvedto accommodate the growth of individualaccount plans. In 2006, Congress enactedthe Pension Protection Act (PPA), the mostcomprehensive retirement legislation sinceERISA. A principal purpose of PPA was to improve the overall funded status of DB plans. The PPA changes represent acomplete overhaul of existing fundingrequirements. Additionally, PPA reflectsthe evolution of the participant as activedecision-maker and provides much-neededprotections for plan fiduciaries and participants in DC plans.

More than 80% of all

private-sector workers

with employer retirement

plans have defined

contribution accounts.

3 > Introduction

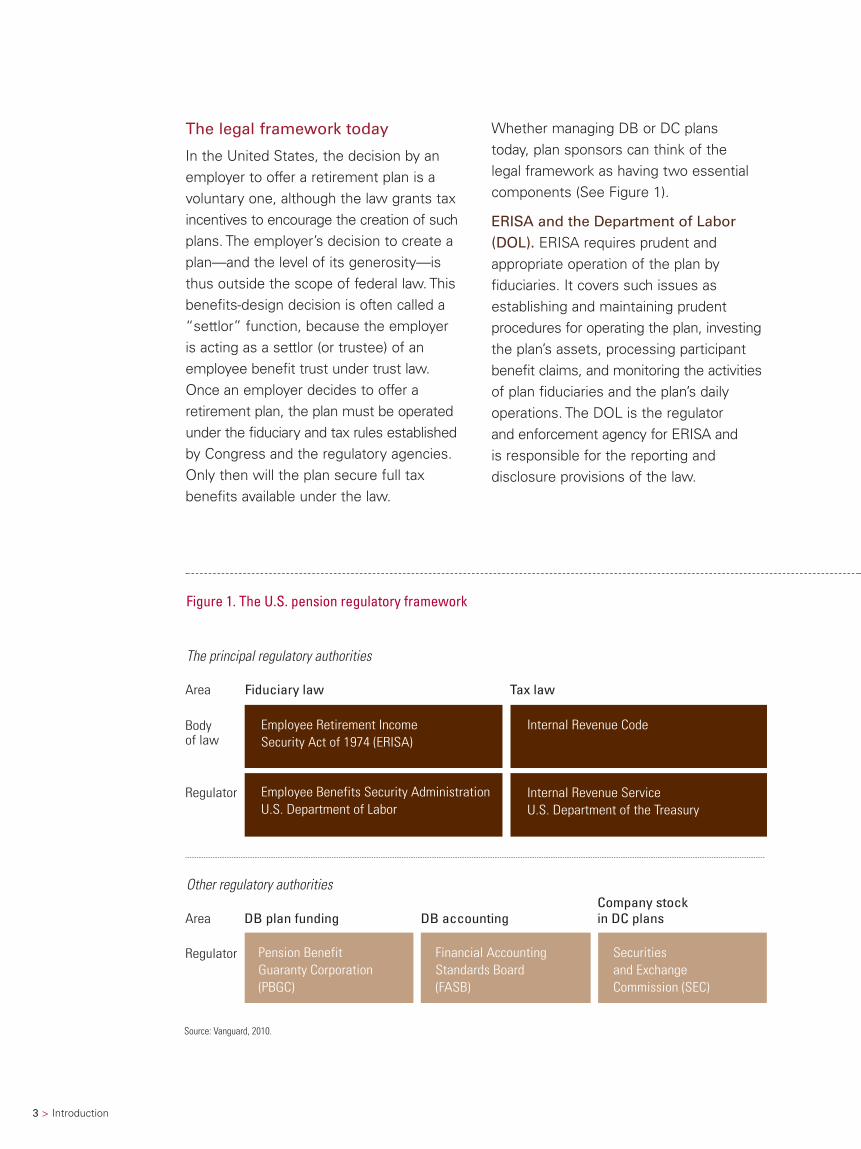

The legal framework today

In the United States, the decision by anemployer to offer a retirement plan is avoluntary one, although the law grants taxincentives to encourage the creation of suchplans. The employer’s decision to create aplan—and the level of its generosity—isthus outside the scope of federal law. Thisbenefits-design decision is often called a“settlor” function, because the employeris acting as a settlor (or trustee) of anemployee benefit trust under trust law.Once an employer decides to offer aretirement plan, the plan must be operatedunder the fiduciary and tax rules establishedby Congress and the regulatory agencies.Only then will the plan secure full tax benefits available under the law.

Whether managing DB or DC plans today, plan sponsors can think of the legal framework as having two essentialcomponents (See Figure 1).

ERISA and the Department of Labor(DOL). ERISA requires prudent and appropriate operation of the plan by fiduciaries. It covers such issues as establishing and maintaining prudent procedures for operating the plan, investingthe plan’s assets, processing participantbenefit claims, and monitoring the activitiesof plan fiduciaries and the plan’s dailyoperations. The DOL is the regulator and enforcement agency for ERISA and is responsible for the reporting and disclosure provisions of the law.

Figure 1. The U.S. pension regulatory framework

The principal regulatory authorities

Other regulatory authorities

Source: Vanguard, 2010.

Fiduciary law Tax law

Employee Retirement Income Security Act of 1974 (ERISA)

Body of law

Regulator

Regulator

Area

DB plan funding DB accountingCompany stock in DC plansArea

Internal Revenue Code

Employee Benefits Security Administration U.S. Department of Labor

Pension Benefit Guaranty Corporation (PBGC)

Financial AccountingStandards Board (FASB)

Securities and Exchange Commission (SEC)

Internal Revenue ServiceU.S. Department of the Treasury

Introduction > 4

to PBGC’s rules. Publicly held companiesalso must report DB funding status totheir shareholders, according to rules ofthe main accounting oversight authority,the FASB. DC plan sponsors that permitemployee dollars to be invested in companystock within their plan must comply withrules governing public securities, which areregulated by the SEC.

Internal Revenue Code and the IRS.The Internal Revenue Code (IRC) governsthe tax benefits offered by “qualified”retirement plans.1 Rules for funding theplan, whether with employer or employeecontributions, and taking distributions,withdrawals, or loans, are provided in the IRC. The IRS, under the authority ofthe U.S. Department of the Treasury, is theregulator and enforcement agency for the tax rules.

Other agencies are involved as well. DB plan sponsors must comply with therules of the DB plan insurance agency, the PBGC, including paying premiums and reporting funding status according

1 The IRC also contains rules for certain “nonqualified” arrangements; however these plans are generally outside the scope of this guide.

5 > Introduction

and what does it mean to be a good plan fiduciary? In addition to a specific person(or title) being named in the plan document,a fiduciary is defined in ERISA as someonewho: 1) exercises discretion over the management of the plan or authority overplan assets; 2) renders investment advicefor a fee—or other compensation, directlyor indirectly; or, 3) has discretion over plan administrative issues.

Fiduciary duties

Underlying the conduct of fiduciaries in private pension plans are the core fiduciary duties drawn from ERISA:

Exclusive benefit. Fiduciaries must actfor the exclusive purpose of providing benefits to participants and beneficiariesand defraying reasonable expenses ofadministering the plan.

Prudence. Fiduciaries have a duty to actwith the care, skill, prudence, and diligenceunder the circumstances then prevailingthat a prudent person acting in like capacityand familiar with such matters would act,including ensuring investments remainprudent investments. Fiduciaries must follow the “prudent expert” rule—actingas an experienced or knowledgeableexpert might.

> Fundamentals of fiduciary responsibilities

Who is a fiduciary

Introduction > 6

Diversification. Fiduciaries have a duty to ensure that plan assets are well-diversified in an effort to “avoid large losses.” (There is an exception to thisdiversification requirement for companystock in DC plans. See the company stock section.)

Documents. Fiduciaries must follow the terms of the plan document and other documents governing the planunless inconsistent with ERISA.

Courts also shape the definition of what it means to be a good fiduciary. In casesagainst plan fiduciaries related to companystock or plan expenses, the courts are not judging fiduciaries against a standard

of perfection but rather a standard of prudence in decision-making. The prudencestandard is measured in a normative manner(e.g., customary fund lineup, range offund choices, relevant disclosure, and procedural due diligence). Procedural duediligence is generally more important thanthe results attributable to fiduciary decisions.

In Vanguard’s view, it is critical for fiduciariesto apply personal experience, judgment,and knowledge to maximize the welfareof the plan’s participants. Above all, fiduciaries must bring the highest levels of ethical conduct and fiduciary care tothe operation and ongoing managementof a retirement program.

In Vanguard’s view, it is

critical for fiduciaries to

apply personal experience,

judgment, and knowledge

to maximize the welfare

of the plan’s participants.

7 > Introduction

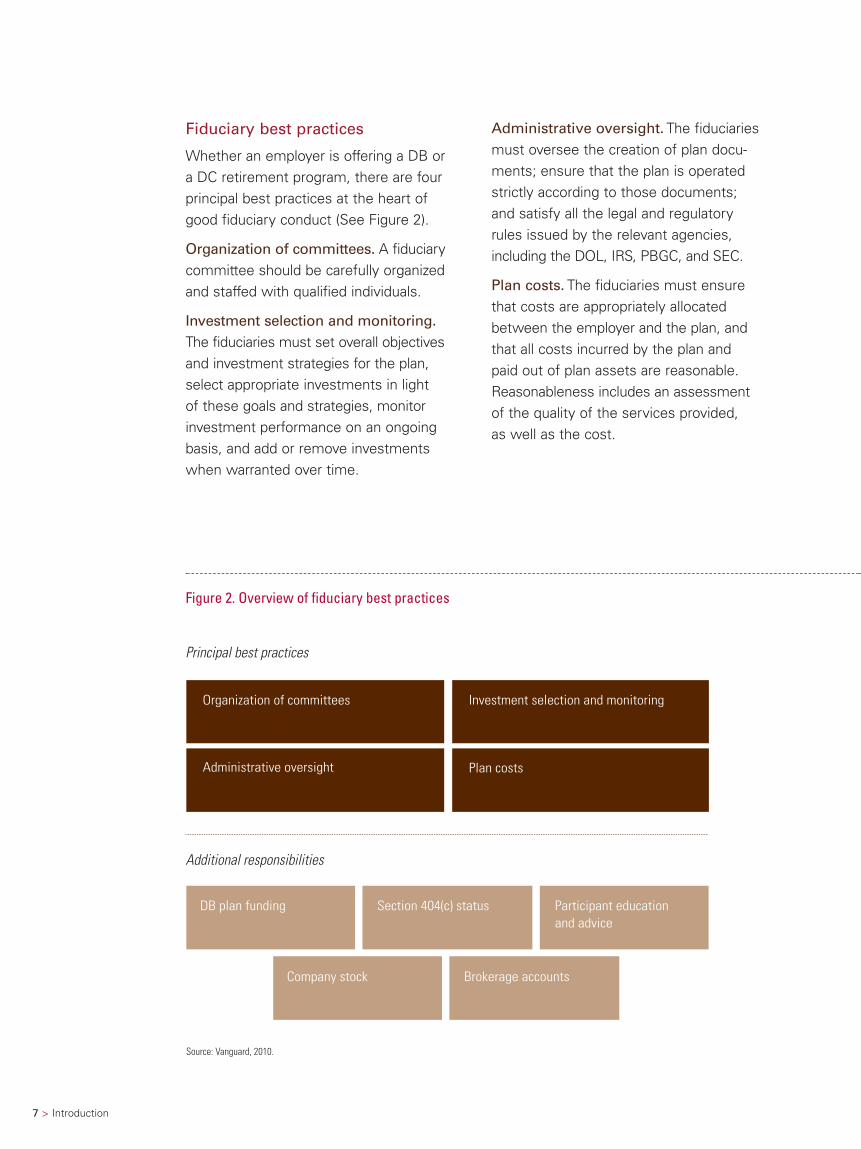

Fiduciary best practices

Whether an employer is offering a DB or a DC retirement program, there are fourprincipal best practices at the heart ofgood fiduciary conduct (See Figure 2).

Organization of committees. A fiduciarycommittee should be carefully organizedand staffed with qualified individuals.

Investment selection and monitoring.The fiduciaries must set overall objectivesand investment strategies for the plan,select appropriate investments in light of these goals and strategies, monitorinvestment performance on an ongoingbasis, and add or remove investmentswhen warranted over time.

Administrative oversight. The fiduciariesmust oversee the creation of plan docu-ments; ensure that the plan is operatedstrictly according to those documents;and satisfy all the legal and regulatoryrules issued by the relevant agencies,including the DOL, IRS, PBGC, and SEC.

Plan costs. The fiduciaries must ensurethat costs are appropriately allocatedbetween the employer and the plan, andthat all costs incurred by the plan and paid out of plan assets are reasonable.Reasonableness includes an assessmentof the quality of the services provided, as well as the cost.

Figure 2. Overview of fiduciary best practices

Principal best practices

Additional responsibilities

Organization of committees Investment selection and monitoring

Administrative oversight

DB plan funding Section 404(c) status Participant education and advice

Source: Vanguard, 2010.

Company stock Brokerage accounts

Plan costs

Introduction > 8

Collectively, these four best practices constitute the essential elements of good retirement plan governance. Theyare addressed in the second section ofthis guide.

Additional fiduciary considerations

In addition, there are other best practice considerations that arise depending onthe type of retirement plan the fiduciariesare overseeing. An explanation of respon-sibilities in this area is detailed in the thirdsection of this guide. These include:

DB funding. For DB plan sponsors, a critical duty is to oversee the plan’s funding and its compliance with IRS and the PBGC rules.

Section 404(c) status. Regulations underSection 404(c) of ERISA provide importantfiduciary protections for DC plan sponsors.Sponsors should seek to comply with therules, even though they are technically anoptional provision of the law that providesprotection in the event the plan fiduciaryis sued.

Education and advice. In participant-directed plans, effective plan design aswell as ongoing education and advice are essential if participants are to makewell-informed decisions. Offering suchprograms is a way of minimizing the plansponsor’s fiduciary risk, while increasingthe likelihood of adequate retirement savings for plan participants.

Company stock. When ERISA was adopted,Congress continued to allow employers toutilize company stock in DC plans as anemployee-ownership vehicle. But thepresence of company stock in the planposes one of the largest sources of fiduciary risk for sponsors. This guide discusses steps that can be taken to mitigate this risk.

Brokerage accounts. How do plan sponsors fulfill their duty to select andmonitor investments—while providing participants an option to invest in tens of thousands of securities in a brokerageaccount? Some simple steps can help mitigate these risks.

> Fiduciary best

practices

fiduciary responsibility for the plan in thesponsoring organization and we will focuson their responsibilities in our guide.

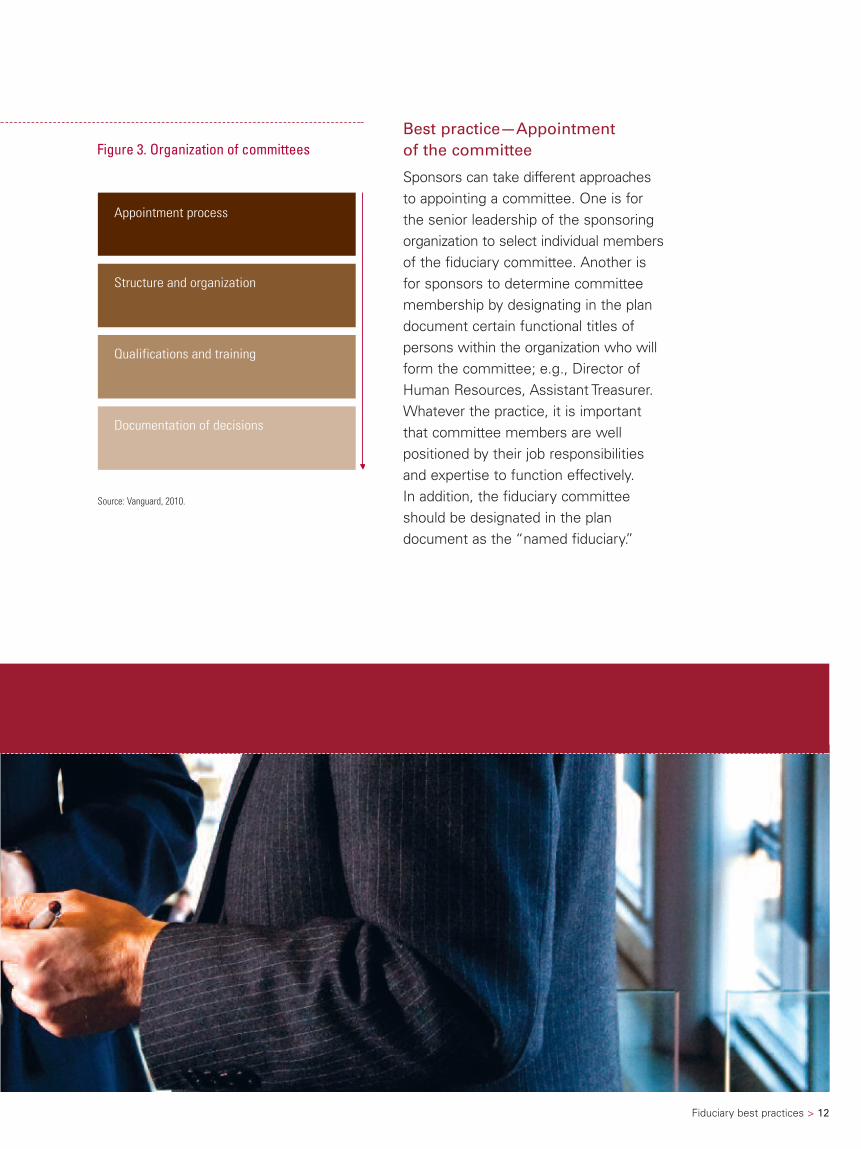

Employers should think carefully about theorganization of the fiduciary committeeand incorporate the following best practices(See Figure 3):

• Have a clear appointment process ofone or more committees, and specifythe relationship to the company’s boardof directors and executive managementteam or officers.

• Determine the structure of the committeeincluding appropriate size, membership,designated responsibilities, and frequencyof meetings.

• Appoint qualified committee membersand ensure appropriate ongoing training.

• Document all committee actions anddecisions.

11 > Fiduciary best practices

at the heart of the fiduciary role includehaving a well-organized and effective committee, selecting and monitoring planinvestments regularly, overseeing planadministration, and monitoring plan costsfor reasonableness.

Under ERISA, many types of individuals or entities—employers, service providers,investment advisors, and consultants—can be plan fiduciaries. But in this guide,we take the perspective of the typicalemployer, who has chosen to sponsor an IRS tax-qualified DB or DC retirementplan. The employer’s senior managementteam appoints individuals to oversee operation of the plan or plans and to be theemployer’s designated ERISA fiduciaries.These individuals may delegate their dutiesfrom time to time to others. However,these appointed individuals maintain the

> Organization of committees

Four best practices

Fiduciary best practices > 12

Best practice—Appointment of the committee

Sponsors can take different approaches to appointing a committee. One is for the senior leadership of the sponsoringorganization to select individual membersof the fiduciary committee. Another is for sponsors to determine committeemembership by designating in the plandocument certain functional titles of persons within the organization who willform the committee; e.g., Director ofHuman Resources, Assistant Treasurer.Whatever the practice, it is important that committee members are well positioned by their job responsibilities and expertise to function effectively. In addition, the fiduciary committeeshould be designated in the plan document as the “named fiduciary.”

Figure 3. Organization of committees

Appointment process

Structure and organization

Qualifications and training

Documentation of decisions

Source: Vanguard, 2010.

13 > Fiduciary best practices

In addition to appointing a committee, the sponsoring employer should have amechanism for overseeing the committee.Typically, the committee reports on a regular basis to a senior managementteam or the sponsoring organization’sboard of directors. Increasingly, the trend is to report to the senior managementteam, on the theory that the board is notas well-positioned to focus on the level of detail that effective oversight entails.

Under ERISA, the members of the fiduciary committee are personally liablefor their fiduciary decisions. Fiduciaryinsurance can help mitigate some of therisk, yet even fiduciary insurance has itslimits and exclusions. Many insurance policies have clauses that relieve the insurerof any responsibility in the event of a willfulbreach of duty by plan fiduciaries. Whileimportant, fiduciary insurance can offeronly limited protection in certain circumstances. In addition, ERISA alsorequires that plan fiduciaries maintainbonding to protect the plan against losses due to fraud or dishonesty.

As a result, to limit personal liability, it iscritical that fiduciaries conduct themselveswith an exceptional level of care—and thatsenior management provide appropriateoversight to their deliberations and decisions.

Best practice—Structure of thecommittee and regular meetings

In small organizations, it is a commonpractice to have a single committee ofplan fiduciaries responsible for overseeingall aspects of the plan. Large organizationsoften have such complex plans that theycreate two committees: an administrativecommittee responsible for daily operationsof the plan and an investment committeeresponsible for investment selection andmonitoring.

A committee might be as small as two orthree individuals in a small firm, or as largeas ten in a big company. In Vanguard’sexperience, committees with ten or moremembers often become unwieldy from agroup-decision-making perspective. Often,their sense of responsibility can be too diffuse.

It is a better idea to have a smaller, well-identified committee with a clearsense of “who is a fiduciary,” rather thanplacing everyone involved with the plan on the committee. Committee meetingscan be expanded to include other individualsas needed. But there should be a clear,focused, and small group of qualified individuals who know they are the plan’sfiduciaries—and are legally responsible for its operation and for making criticaldecisions.

Fiduciary best practices > 14

In large organizations with two committees, an important question is the reporting relationship between thosetwo groups. It is a fairly common practicefor plan sponsors to have two committeesorganized in a parallel fashion, with certaincore treasury and human resources (HR)individuals participating on both committees.In such cases, coordination and cooperationis essential. Each committee should begoverned by a charter that clearly delineatesrespective duties.

Frequency of meetings is important. Large organizations with complex plansmay meet monthly or every other month,depending on the length of agendas andthe complexity of the investment andadministrative issues. A good discipline isto meet quarterly. In addition, committeesshould call off-schedule meetings whennecessary (e.g., in cases of extraordinarymarket or plan events).

Many small organizations may find quarterly meetings unnecessary if planadministration is relatively simple and the investment program is operating well; instead, they may decide to meetsemiannually or annually. However, if thecommittee meets infrequently, at leastone of the plan fiduciaries should beresponsible for more regular oversight of investment or administrative issues.

Committee members should understandthe importance of their role and should be expected to attend meetings regularly.Plan fiduciaries are collectively responsiblefor the plan’s oversight. In the event of aproblem, committee members cannot distance themselves from responsibilityby maintaining that they did not participatein the committee’s decision-making.

Best practice—Qualification andtraining of fiduciaries

Individuals chosen for the committeeshould have relevant experience, either in investments, plan administration, orboth. They should be familiar with theirduties and responsibilities under the law.Committee members should be chosenfor the variety of perspectives they canprovide on administrative and investmentissues, and the committee should generallynot rely on a single individual as thesource of expertise.

Appointments to the committee should befor a specific time, and the period shouldbe relatively long (e.g., five years) to allowfor continuity of thinking and oversight.Some positions will be permanent and by position (e.g., senior vice president of HR), while others may rotate and be based on current knowledge and experience.

15 > Fiduciary best practices

If an organization lacks individuals withappropriate qualifications, the committeemembers should pursue relevant knowledgethrough training programs or professionalcounsel. Plan professionals such as attorneys, accountants, plan consultants,service providers, and investment managerscan provide professional and technicalassistance. However, the ultimate responsibility and decision-making alwayslie with the fiduciary unless this authorityhas been specifically delegated.

Best practice—Documentation

Using a committee charter or incorporatingrelevant language into the plan document isa best practice for plan sponsors. The plandocument or charter should define thecommittee structure and its responsibilities.Documentation should include the numberof members, the required presence ofsenior officers, the reporting relationship tosenior management (or board, if applicable),the selection and removal process ofmembers, the purpose and frequency of meetings, voting procedures and guidelines, as well as the procedure forgenerating minutes for each meeting.

The level of detail in these governing documents will vary. More is not necessarilybetter. What’s essential is the framework. Ifthe committee finds it helpful to be guidedby more details, that is fine, but it’s criticalto ensure that the committee is actuallyoperating as the documentation describes.

Written documentation extends to com-mittee meetings. Each meeting should bedocumented with minutes to be reviewedand approved by the committee. Onceagain, copious detail is not required. Whatis important is to have a clear and conciserecord of who attended the meeting, high-level descriptions of issues discussed, andaction items agreed upon.

Vanguard encourages plan sponsors totake documentation seriously. Litigants,courts, and regulators will look at meetingminutes when assessing cases of potentialfiduciary breach. Careful documentation is critical in establishing procedural duediligence—a key factor in demonstratinggood fiduciary practices. By maintainingcareful minutes and holding regular meetings, plan fiduciaries can keep their focus on their duties as well as help minimize personal liability.

Fiduciary best practices > 16

17 > Fiduciary best practices

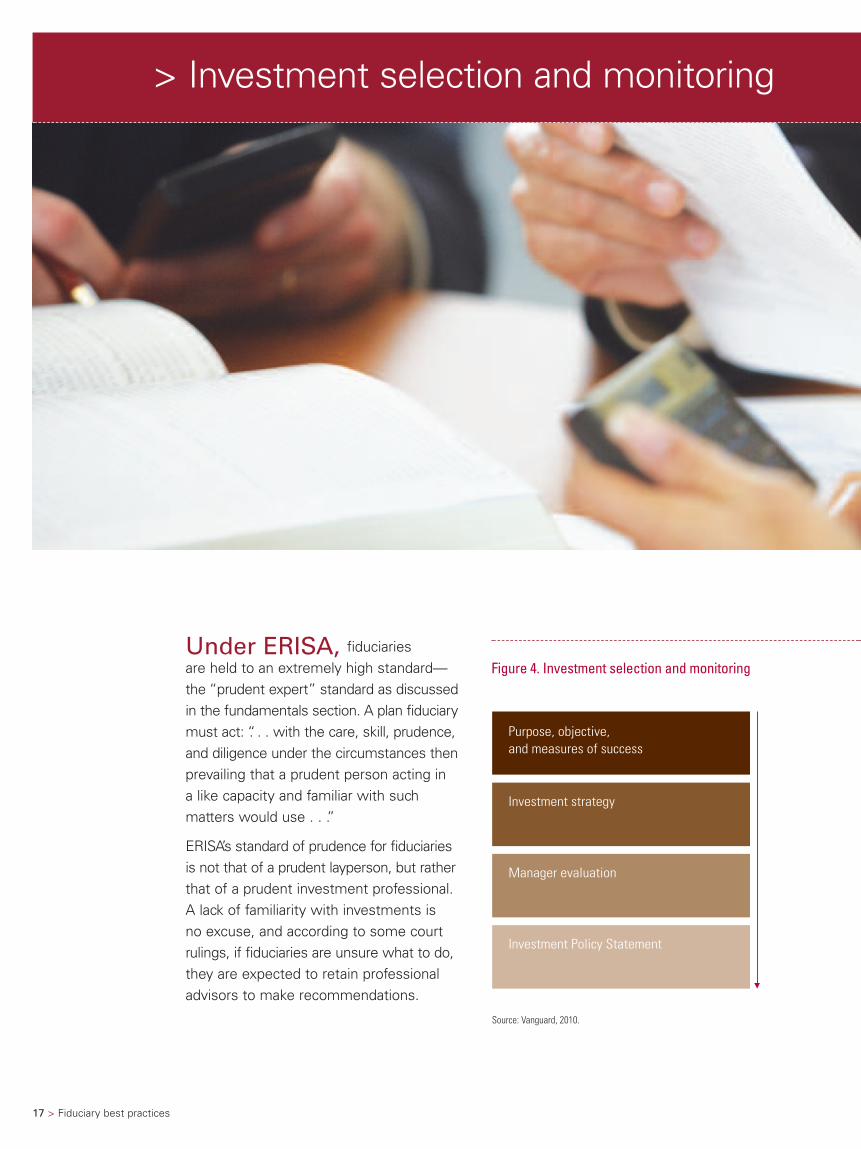

fiduciaries are held to an extremely high standard—the “prudent expert” standard as discussedin the fundamentals section. A plan fiduciarymust act: “. . . with the care, skill, prudence,and diligence under the circumstances thenprevailing that a prudent person acting in a like capacity and familiar with such matters would use . . .”

ERISA’s standard of prudence for fiduciariesis not that of a prudent layperson, but ratherthat of a prudent investment professional.A lack of familiarity with investments is no excuse, and according to some courtrulings, if fiduciaries are unsure what to do,they are expected to retain professionaladvisors to make recommendations.

> Investment selection and monitoring

Figure 4. Investment selection and monitoring

Purpose, objective, and measures of success

Investment strategy

Manager evaluation

Investment Policy Statement

Source: Vanguard, 2010.

Under ERISA,

Fiduciary best practices > 18

In this section, we summarize best practices around investment selection and monitoring (See Figure 4):

• Ensure an understanding of your investment portfolio’s purpose andobjective, with a clear definition of success.

• Adopt an investment strategy withexpectations for both risk and return,including selecting a default fund in a DC plan.

• Create a well-defined process for hiring, evaluating, and terminatinginvestment managers.

• Adhere to an Investment PolicyStatement (IPS).

Best practice—Investment purpose,objective, and measures of success

Investment committees should have awell-articulated view of the goals andobjectives for the plan assets they areoverseeing, and well-defined metrics forsuccess. This concept is incorporated in theregulations issued under ERISA, writtenoriginally in the context of DB plans. Planfiduciaries should select investments: “. . . reasonably designed . . . to further the purposes of the plan, taking into consideration the risk of loss and theopportunity for gain (or other return) . . .”

Investment committees

should have a

well-articulated view

of the goals and objectives

for the plan assets they

are overseeing.

19 > Fiduciary best practices

The DOL goes on to say that plan fiduciaries should take into account thediversification of plan assets, the plan’s liquidity and current income needs, aswell as the projected rate of return on the portfolio relative to the plan’s fundingobjectives. In other words, plan investmentsshould be based on the program’s goalsand objectives—to fund the obligationspromised to participants under the plan—while factors such as liquidity, risk, return,and funding status should be metrics of success.

Although these regulations were drafted inthe context of managing a DB trust, theyalso provide a helpful framework for DCplan sponsors. In the end, each DC planparticipant’s savings objective is to accumulate adequate savings for retirement, and fiduciary decisions shouldbe made with this goal in mind. Sponsorscan assess participants’ progress towardthis goal by using a variety of metrics: participation rates for plans with voluntarydeferrals; combined participant andemployer contribution rates; and, on the investment side, both asset allocationand contribution-allocation decisions.

At one level, all DB and DC plans havesimilar objectives—the provision of collective (DB) or individual (DC) assets for retirement. At another level, however,there will be differences among the plans.For example, DB plans will have differingneeds for liquidity and current incomedepending on the ratio of retirees toemployees. While DC plans are used primarily for retirement, some plans may have secondary objectives—such aspromoting employee ownership throughcompany stock. Vanguard works with plan

sponsors to develop plan objectives andmeasures of success that reflect theunique needs and goals of each specificretirement program.

Best practice—Investment strategy

Under ERISA, plan fiduciaries are givenwide latitude in their investment discretion,as Congress did not want to create a setof authorized or government-approvedinvestments for pension plans. Instead itopted for a decentralized approach, relyingon the experience and judgment of theindividuals serving as fiduciaries in eachemployer-sponsored plan. Still, the lawand regulations provide guideposts to helpfiduciaries select appropriate investments.

ERISA embraces a modern portfolio view and recognizes the benefits of diversification. What matters is not theindividual risk of a specific investment, but how the entire portfolio seeks to manage risk and return. Thus plan fiduciaries are not prohibited from offeringor investing in high-risk assets—such asvolatile common stocks, illiquid privateequity, or real estate investments—if in the fiduciaries’ judgment the portfolio in its entirety presents a prudent level of risk and return.

In addition, Congress recently providedguidance affording plan sponsors fiduciaryprotection for the selection of a QualifiedDefault Investment Alternative (QDIA).This is discussed later in this section.

Most fiduciaries will structure their investment program around diversifiedpools of publicly traded, marketable securities or mutual funds in the threemajor asset classes: common stocks(equities), bonds, and short-term reserves.

Fiduciary best practices > 20

DB investment strategies typically willcarefully weigh bond investments—whichmatch the nature of the pension liability—against equity investments—which mayoffer higher returns in the long run. Menusof options offered by DC plans often contain many different equity funds.

Because DC plans receive regular payrollcontributions and must be able to pay outaccounts when participants change jobs,retire, or exercise withdrawal options inthe plan, it is more difficult for DC plans to hold illiquid assets. Mutual funds arehighly regulated under the InvestmentCompany Act of 1940 and are often desirable in DC plans for a variety of reasons. Participants appreciate thedaily pricing of mutual fund shares, whichare published and widely available. Also,mutual funds enhance diversificationbecause the funds invest in a variety of underlying securities. In addition todiversification, another benefit of mutualfund investing is the oversight provided bymutual fund providers and their regulator,the SEC. Mutual funds are required to setforth a well-defined investment objectivein a formal prospectus so that investorsknow the kind of investment they arechoosing and the risks involved. In addition,the mutual fund’s board of directors has a fiduciary duty to ensure that the fund isoperated in accordance with the fund’sprospectus. Plan fiduciaries should reviewthe prospectus and the fund’s performanceas they select and monitor plan investments.

DB plans will often have the flexibility toinvest in a range of less-liquid investments—subject to the proviso that they are part ofa prudent and diversified portfolio. Liquidityrequirements need to be considered iflarge amounts of benefits payments may

need to be made in a short time frame.Again, mutual funds can play a role in aprudent investment structure to enablecertain DB plans to diversify holdings andmeet their investment objectives.

Whatever investments are chosen, it isfairly clear what plan fiduciaries should notdo—they should not choose investmentasset classes or money managers basedon “hot” past performance. Instead, they should examine risk-and-return characteristics with a long-term view of performance.

Because risk-and-return characteristics arestrongly influenced by a portfolio’s assetallocation, an important decision for planfiduciaries is to determine an overall assetallocation for the plan’s investments. Riskfor a DB plan is related to the funded status, so the asset allocation policyshould consider the pension obligationbeing covered. In the case of a DB plan,there is a single asset allocation policy,although the policy may be designed tochange the asset allocation upon theoccurrence of designated events, such as when funded status reaches a certainlevel. In the case of participant-directedDC plans, plan fiduciaries should offer educational programs or tools—for example,a worksheet or an online calculator—to help participants establish their ownasset allocation appropriate to their age,risk tolerance, and time horizon. To helpsimplify the decision-making process, plansponsors offer participants professionally managed, diversified portfolios by offeringone target-date fund. Fiduciaries also canoffer advice services, which provide bothpersonalized asset allocation strategies and specific investment recommendations to participants.

21 > Fiduciary best practices

Developing an investment strategy for a DCplan involves several other aspects. First,sponsors have wide latitude about thenumber of investment options offered toparticipants. Technically, to comply with404(c) regulations, a sponsor need onlyoffer a minimum of three diversifiedoptions designed to enable the participantsto create an investment portfolio based onrisk and return characteristics appropriatefor them. However, most plan sponsorsoffer an average of 18 funds in a balancedarray of investment options covering fourmajor investment categories: equities,bond funds, balanced or life-cycle funds,and money market or stable value options.A small number of plan sponsors mayoffer even more choices, perhaps througha mutual fund window or brokerage option.

Second, plan sponsors should evaluate thecomplexity of the plan investment menu inlight of the demographics and investmentexperience of the participant population. A less experienced population more likelycalls for a simple menu and easy-to-understand choices, such as a target-datefund. For a more knowledgeable and experienced employee population, a widerarray of choices may make sense. At thesame time, plan fiduciaries are not underany obligation to satisfy every investmentdesire of the most sophisticated employees in the plan.

DC plan sponsors should also design theirinvestment menus in concert with theiremployee education and advice programs.It does little good for a committee to addinvestment options that participants donot understand. We return to this topic of education and advice in the last sectionof this guide.

Best practice—Qualified DefaultInvestment Alternative

In an individual account DC plan, plan fiduciaries should select a default fund.The default fund is used when a plan participant fails to make an investmentselection for his or her elective contributionsor for an employer contribution, or in caseswhere participants are automaticallyenrolled in the plan.

Ordinarily, when the plan participant failsto exercise a choice, the plan fiduciariesare responsible for the investment of planassets in the plan’s default investmentalternative. As an exception to this generalrule, plan sponsors are afforded fiduciaryprotection of ERISA Section 404(c) by utilizing a QDIA as the plan default fund.Generally, a default fund will qualify as aQDIA if it is a target-date fund, a balancedfund, or a managed account option—andif notice requirements are satisfied.

When selecting the type of fund to bedesignated as a QDIA, a plan sponsor isafforded fiduciary relief regardless of thetype selected. This means, for example,that a sponsor cannot be second-guessedon whether a balanced fund would havebeen a “better” choice than a target-datefund. However, plan fiduciaries continue to have responsibility for the selection andmonitoring of the investments offeredunder the plan as well as the selectionand monitoring of the QDIA to be used as the plan’s default investment.

Fiduciary best practices > 22

In practice, the vast majority of plan sponsors select a target-date fund as aQDIA. Below are four key considerationsin evaluating and implementing a target-date fund as the QDIA.2

Asset allocation glide path. The chosenfunds’ asset allocation shift through timeshould match the investment committee’sview of the appropriate risk/return trade-off for participants at each stage of life, as well as include exposure toasset classes the committee believes can add value.

Passive versus active management.The costs and benefits of an index (passive) versus active approach should be carefully considered, keeping in mindexpected performance, risks, and fiduciary responsibilities.

Packaged or customized solution.Sponsors considering a customizedapproach should be convinced that either(1) the approach offers a significantexpected performance advantage—net of costs—versus a packaged solution or (2) their participants differ both systematically and significantly from typical plan participants in such a way that a unique approach at a fund leveladds value.

Impact on participant portfolios.Research shows that sponsor decisionsplay a critical role in influencing target-datefund adoption rates. Our research alsoshows that participants use target-datefunds in a variety of ways, and that individual participant decisions throughtime drive the overall impact of target-datefunds on plan asset allocations.

Best practice—Manager evaluation

A fundamental responsibility of plan fiduciaries is to hire, evaluate, and as necessary, terminate money managers for the plan. This means having in place adisciplined process for manager selectionand evaluation. Without such a strategy,plan fiduciaries risk overreacting to the latest performance trends, either positive or negative.

Evaluation of investment managers incorporates four key elements:

• Evaluating the manager’s team andorganization.

• Understanding the philosophy thatguides the manager’s firm.

• Understanding the firm’s process and its consistency over time.

• Analyzing performance over time in lightof the firm’s philosophy and process.

No single qualitative or quantitative factorwill determine whether an investmentoption should be added, retained, or eliminated; however, certain factors maycarry more weight in the final analysis.When evaluating investment managers,other considerations include changes in thefund manager’s investment philosophy andchanges within the manager’s organization.

On an ongoing basis, investment committees should evaluate whetherinvestment managers are achieving thegoals set for them within the plan’s investment strategy. Committees shouldexamine performance relative to indexesand peers, as well as look at style consistency.

2 For a complete discussion on target-date fund construction, see the Vanguard Investment Counseling & Research publication Evaluating and implementingtarget-date portfolios: Four key considerations.

23 > Fiduciary best practices

Investment performance should bereviewed quarterly, or at the very leastannually, on a benchmark and peer-groupbasis. Monitoring the plan’s investments isfundamentally the fiduciary’s responsibility.Even in cases where an ERISA investmentmanager is appointed, the plan fiduciaryretains ultimate responsibility for monitoringthe investment manager. Vanguard assistsfiduciaries by providing detailed perform-ance and portfolio information on theplan’s investments.

Having Vanguard as your investment providergives you an additional level of scrutiny andprotection. Vanguard meets regularly withall of our investment managers, monitorsthem carefully for consistency with portfoliostrategies and style, and negotiatesaggressively on fees. Our portfolio reviewteam is highly qualified to assist plan fiduciaries with their duty to monitorinvestments. Our use of independentmoney managers for many funds alsoallows us to negotiate portfolio and feerelationships at arm’s length.

Best practice—Investment PolicyStatement

A simple best practice is to documentyour investment decision-making in yourplan’s Investment Policy Statement (IPS).The IPS defines the purpose, objectives,and measures of success for the plan; it summarizes the plan’s investment strategy; and it describes the process for evaluating money managers. The IPSshould detail performance measurementand the frequency of reviews. Parametersalso should be established to determinewhen the committee should considereliminating investments or managers.

Committees should review the IPS annuallyto ensure that it continues to reflect theplan’s objectives and meet the needs ofthe plan’s participants. While changes to theIPS are expected to be infrequent, possiblecauses for change may include major shiftsin workforce demographics, significantgrowth of the plan, and the performanceof existing investment options.

Fiduciary best practices > 24

Vanguard recommends

all plan sponsors use

an Investment Policy

Statement and can assist

in the development and

review of this document.

25 > Fiduciary best practices

it is theduty of plan fiduciaries to maintain planand employee records, adjudicate benefitsclaims and appeals of claims’ denials fromparticipants, and file all reports, notices,and statements required by law.

The cornerstone of effective plan administration is the plan document, whichstipulates how fiduciaries will handleadministrative features of the plan. There arefour best practices in this area (See Figure 5):

• Ensure that the administration of the planconforms to the written plan documentand any administrative policies and procedures for the plan.

• Maintain an up-to-date plan documentand conduct a periodic compliance review.

• Comply with nondiscrimination testingand other compliance rules.

• Ensure the timely investment ofemployee contributions, recognize theimportance of participant notifications,and implement a well-defined claimsappeal process.

> Administrative oversight

Broadly speaking,

Fiduciary best practices > 26

Best practice—Plan documents and the management process

Plan fiduciaries should ensure that theprocesses used to administer the planconform to the written plan document,unless the plan does not comply withERISA or unless following the documentwould otherwise conflict with the fiduciaryduties imposed by ERISA. In the rareinstance where the plan document conflictswith ERISA's fiduciary duties, the planfiduciary may need to deviate from theplan document provided they take stepsto memorialize the reason the plan wasnot followed, and then either amend theplan or change the procedure.

Figure 5. Administrative oversight

Consistency of documents and process

Compliance review of documents

Nondiscrimination and compliance testing

Contributions, claims, and notifications

Source: Vanguard, 2010.

27 > Fiduciary best practices

One of the simplest measures of qualityfor plan fiduciaries is the extent to whichthere is alignment between proceduresand the plan document. To ensure that the plan document and procedures arealigned, a good practice is for employers to review plan transactions periodically—for example, employee contributions,employer contributions, withdrawals, ter-minations, loans (if offered), DB pensioncalculations, qualified domestic relationsorders (QDROs), and so forth. Workingwith their recordkeeper, plan fiduciariescan ensure that transaction processingconforms to the plan document language.

At Vanguard, an independent accountingfirm audits the internal controls of ourrecordkeeping system annually. Reports on the Processing Transactions by ServiceOrganizations is a report prepared inaccordance with the American Institute of Certified Public Accountants (AICPA)Statement on Auditing Standards No. 70(SAS70). The report, provided to plansponsors annually, offers a description of the procedures designed for achievingthe control objectives and ensuring effective operations.

Best practice—Current documentsand compliance reviews

Plan fiduciaries should review and maintaintheir plan document in compliance withcurrent regulations. This means updatingor amending documents as necessary in a disciplined fashion and making sure thatthe plan document and the summary plandescription (SPD) are current.

Congress and the regulatory agenciesperiodically update and modify plan rules.Plan fiduciaries are responsible for ensuringthat the plan document continues to conform to all laws and regulations. Mostnotably, these include tax rules from the

IRS and fiduciary and disclosure rules fromthe DOL. As we have noted before, planfiduciaries should also ensure compliancewith PBGC rules (in the case of DB plans)and any SEC regulations (for mutual fundsand company stock). As a result, it isimportant that plan fiduciaries keepapprised of legislative and regulatorychanges and make modifications to thelanguage in the plan document and theadministration of their plan when warranted.

Vanguard has a strong presence inWashington, D.C. Vanguard clients canrely on our legislative and regulatoryupdates including our Regulatory Briefs,SRC bulletins, webcasts, and videos.These resources identify strategies tohelp plan sponsors respond to legal and regulatory changes.

Best practice—Nondiscriminationand compliance testing

For most plans that permit employee elective deferral rules, plan fiduciariesmust ensure the plan complies with federal nondiscrimination testing rules.Under such rules, highly compensatedemployees are not permitted to contributedisproportionately to the plan comparedwith nonhighly compensated employees.If highly compensated employees makecontributions at a significantly higher rate,the plan must refund their contributions,make additional contributions on behalf of the other employees, or risk losing the plan’s status as a tax-qualified retirement plan.

There are a variety of strategies that plansponsors can pursue to satisfy theserequirements. A simple approach is forplan sponsors to limit the highly paid to acontribution rate (e.g., 6% or 8% of pay)that will allow the plan to satisfy testingrequirements each year. In Vanguard’sview, this is the least attractive strategy, as

Fiduciary best practices > 28

it frustrates the retirement objectives ofhighly paid employees and accommodatesthe low savings rates of nonhighly paidemployees.

Plan fiduciaries who face testing issuescan pursue alternative approaches that will lead to better retirement outcomes for plan participants instead of “capping”the highly paid, including:

• Automatic plan design strategies, suchas automatic enrollment and automaticannual increases to raise participation andsavings rates among the nonhighly paid.

• Safe-harbor plan designs, where inexchange for meeting certain vesting,eligibility, and contribution requirements,a plan sponsor is able to avoid therequirement of nondiscrimination testing.

• Targeted education programs to boostparticipation among the nonhighly paid.

SRC is able to assist our clients in evaluating all of these strategies. OtherVanguard departments assist with ensuring

that plans are administered in compliancewith all other federal tax limits and restrictions.

Best practice—Contributions, notifications, and claims

Three other administrative responsibilitiesare worth highlighting: the timeliness ofremittance of employee contributions tothe plan, participant notifications, and theclaims appeal process.

Employee contributions. Employee contributions (including any applicable loan repayments) that are deducted from employee pay are plan assets, notemployer assets. The DOL requires timelyremittance of all contributions to the plan’strust as soon as they can be reasonablysegregated from the employer’s assets. In large organizations, timely remittancetypically means that contributions occuron payday or a few days later. However,the rule is that employee contributionsmust reach the trust no later than the 15th

The law requires that participant

contributions be deposited in

the plan trust as soon as they

can be reasonably segregated

from the employer’s assets.

29 > Fiduciary best practices

business day in the month after the monththe contributions were withheld. The 15business days of the following month set forth in current regulations is not a safe harbor, it is an outer limit. Recently,the DOL created a new safe-harbor periodfor plans with fewer than 100 participants.Specifically, participant contributions willbe deemed to comply with the law ifthose amounts are deposited to the trust within seven business days afterthe date the amounts were withheld.Timely remittance of contributions is animportant priority for DOL enforcement,and all employers should do everythingpossible to remit employee contributionsas soon as reasonably possible.

Participant notifications. There are a variety of notice requirements imposed on plan sponsors under ERISA. Generally,changes in benefits must be communicatedin a disciplined fashion in accordance withregulations by updating the summary plandescription or providing separate notice.ERISA has specific rules indicating howthese changes should be incorporated inplan documents and communicated, sothat participants understand what rightsand features they have under the plan. The summary plan description is a criticaldocument for participant communication.Fiduciaries should focus on how the summary plan description is worded; making certain that it is accurate,

understandable, and clear. When there isa discrepancy between the plan documentand the SPD, courts have tended to relyon the language in the SPD. Additionally,fiduciaries should ensure that requiredannual notices are provided to participantsfor certain plan designs, including safe-harbor plan designs and plans with aQDIA. Vanguard can provide assistance to help plan sponsors satisfy these notice requirements.

Claims appeal process. Plan documents,and especially the SPD, should containdetailed information regarding how a participant files a claim for benefits and theappeal process for a denied claim. ERISAhas specific rules on the steps a sponsormust take to deny a claim, including thetiming of the notice of denial and the contents of the notice. Communicatingand following the claims process is important because participants may notpursue a lawsuit in the retirement-plancontext until the claim’s remedy proce-dures are exhausted.

Fiduciary best practices > 30

31 > Fiduciary best practices

oversight by planfiduciaries to ensure that plan assets areused exclusively for paying plan benefitsor defraying reasonable administrativeexpenses.

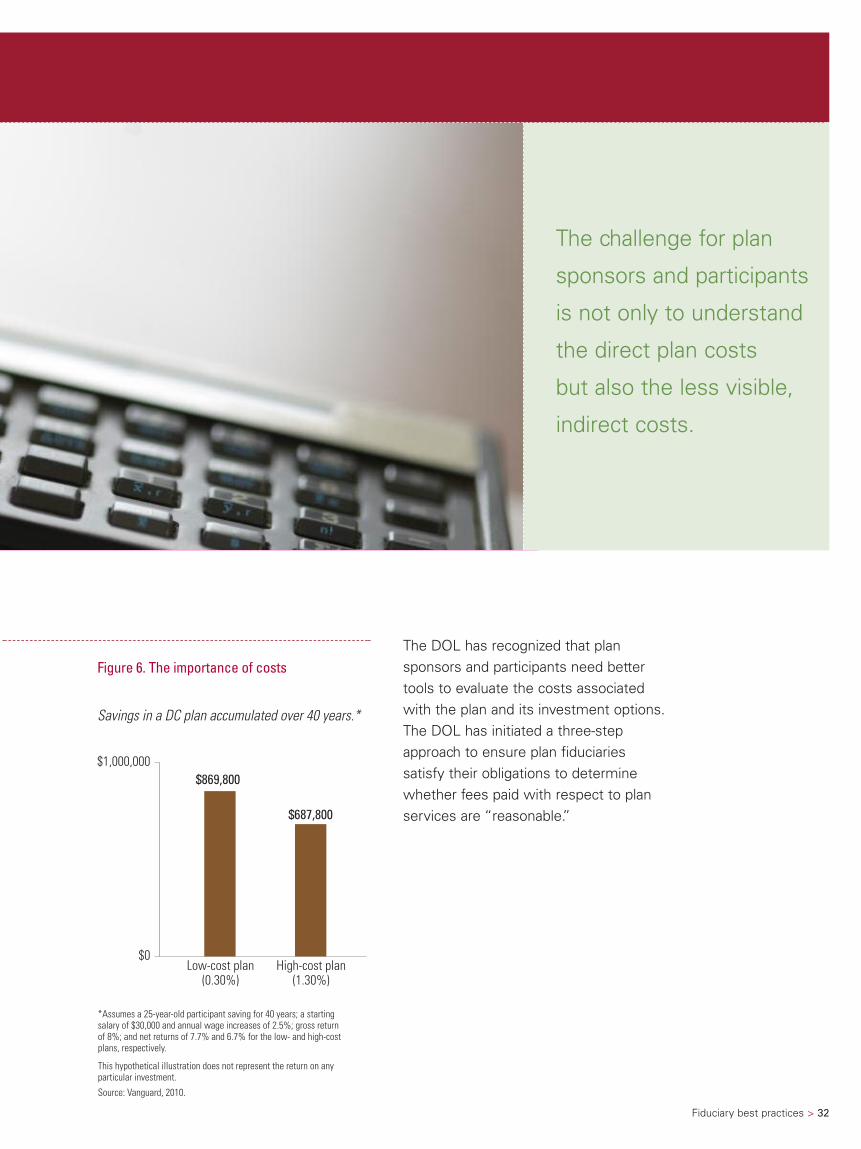

Costs of plan administration matter.Generally, lower costs will lead to higherafter-expense investment results. As aresult, for a DB plan, required employercontributions will be lower, and for a DCplan participant, retirement savings will behigher. Over a working career, the benefitsof a low-cost retirement program can besubstantial. As a hypothetical illustration, a participant in a DC plan will have anadditional $182,000 in retirement savings ifhis employer offers a low-cost rather thana high-cost retirement plan (See Figure 6).

Research suggests that investors tend tobe aware of direct costs, but not indirectfees. In the case of retirement plans, ourexperience is that plan sponsors who writea check for a service are often well aware ofthe fee they are paying. Similarly, participantsare well aware of fees that appear as directcharges on their statements. What somesponsors and many participants ignore,however, are the indirect fees deducted asinvestment charges against their plan assets.The challenge for plan sponsors and participants is not only to understand thedirect plan costs—but also to understandthe less visible, indirect costs.

> Plan costs

ERISA requires

Fiduciary best practices > 32

The DOL has recognized that plan sponsors and participants need bettertools to evaluate the costs associatedwith the plan and its investment options.The DOL has initiated a three-stepapproach to ensure plan fiduciaries satisfy their obligations to determinewhether fees paid with respect to planservices are “reasonable.”

The challenge for plan

sponsors and participants

is not only to understand

the direct plan costs

but also the less visible,

indirect costs.

Figure 6. The importance of costs

*Assumes a 25-year-old participant saving for 40 years; a starting salary of $30,000 and annual wage increases of 2.5%; gross return of 8%; and net returns of 7.7% and 6.7% for the low- and high-cost plans, respectively.

This hypothetical illustration does not represent the return on any particular investment.

Source: Vanguard, 2010.

$0

$1,000,000$869,800

Low-cost plan(0.30%)

$687,800

High-cost plan(1.30%)

Savings in a DC plan accumulated over 40 years.*

33 > Fiduciary best practices

The DOL’s regulatory approach involvesdisclosure to:

• The government through enhancedForm 5500 reporting that will requireplan sponsors to disclose additionalinformation about fees paid to service providers.

• Plan fiduciaries through greater transparency regarding fees and expenses–including disclosure to plan fiduciaries of revenue sharingreceived by service providers.

• Plan participants through detailed communications regarding fees andother investment-related information.

The DOL guidance serves as a basis forplan sponsors to use in evaluating the reasonableness of plan costs. It shouldalso be noted that, in addition to the DOL’s regulatory approach, there continuesto be significant legislative and regulatoryfocus on fee disclosure.

Regardless of legal and regulatorychanges, there are several fiduciary best practices to consider with respect to plan costs (See Figure 7):

• Ensure fees charged against the plan are a legitimate plan expense and not a business expense of the sponsoringemployer (i.e., settlor versus plan costs).

• Evaluate the fees being paid from trustassets and ensure they are reasonable.

• Review the disclosures made to participants to ensure complete andaccurate disclosure.

Best practice—Settlor versusadministrative costs

The law generally views plan costs in two broad categories: settlor versus planadministrative costs. Settlor functionsinclude discretionary activities that relate tothe establishment, design, and terminationof plans. Expenses incurred as a result of

Fiduciary best practices > 34

Figure 7. Plan costs

Plan versus business expenses

Reasonableness of fees

Participant disclosure

Source: Vanguard, 2010.

settlor functions ultimately benefit theemployer and cannot be paid from planassets. The plan sponsor, as a normalbusiness expense, must pay theseexpenses. Plan fiduciaries have a duty to ensure that no settlor costs are everpaid by the plan.

Costs relating to the administration of the plan and the investment of its assetscan be charged to the plan. Administrativecosts include: plan amendments to complywith tax-law changes; nondiscriminationand compliance testing; legal, accounting,and actuarial fees to maintain the plan’squalified status; and complying with ERISA’sreporting and disclosure requirements.Investment costs include fees paid toinvestment advisors, as well as expensesfor trustee and custodial services. Generally,if the expense relates to the administrativeor investment activities of the plan, it canbe paid from the plan’s assets. Paymentsmay be deducted from individual participantaccounts or the plan’s forfeiture account in a DC plan.

35 > Fiduciary best practices

Best practice—Determine fees are reasonable

ERISA is clear that plan fiduciaries have a duty to evaluate the fees incurred by the plan for reasonableness. Thus, planfiduciaries should benchmark their fees as a way to determine reasonableness. It isimportant for sponsors to remember that“reasonable” is not necessarily the lowestcost—it involves an evaluation of cost and value.

As part of the reasonableness analysis, it is imperative that plan fiduciaries have a clear understanding of all direct and indirect fees paid by the plan. These costsinclude not only those obvious costs relatedto plan administration and investments—but also all fees, reimbursements, rebates,subsidies, and other payments (includingrevenue sharing paid to third parties), whichmay be charged against plan assets.Because it is often easier to overlook fees paid indirectly, such as asset-basedinvestment management fees, a best

practice for the fiduciaries is to review all investment-based fees on at least anannual basis, as part of the review of overall all-in fees.

In benchmarking fees, it is important that plan fiduciaries make an “apples to apples” comparison. For example, it would not be appropriate to comparethe investment advisory fee for a DB planwith the expense ratio of a commingledfund or separate account in a DC plan. The latter is typically higher because itincludes a range of higher-cost activities—including payroll processing and individualrecordkeeping services, participant education and advice, individual statements,and telephone and Web account servicesfor participants. Such costs are not generallyincurred by DB plans.

To compare overall fees, some sponsors relyon averages published in surveys by planconsultants, professional associations, orpublications. Others will benchmark their

In benchmarking fees,

it is important that plan

fiduciaries make an

"apples to apples"

comparison.

Fiduciary best practices > 36

fees with other non-DC investment programs, such as DB investment feeschedules or mutual fund expense ratios,while making adjustments for the additionalcosts incurred by the DC plan for adminis-trative activities. Some sponsors solicit a “request for information” or a “request for proposal” in order to obtain current fee information from a list of competitivevendors.

Best practice—Participant disclosure

In DC plans, any participant charges—suchas an annual charge for recordkeeping or a fee for a loan—should be disclosed. Byand large, participants become fully awareof direct fees at the time they are incurred.However, participants may fail to considerasset-based investment fees chargedagainst their accounts. As noted, the DOLis concerned about the transparency ofparticipant fees and encourages full

disclosure to participants of both transaction-related fees (e.g., loan fees)and investment-related fees so that participants may make informed decisionsconcerning their individual accounts.

Participant decisions should not be basedsolely on fees, and sponsors should seekto educate participants on risk and return.Vanguard believes that plan fiduciariesshould make an effort to encourageawareness of all plan fees, includingasset-based fees. Vanguard facilitates participant disclosure through the use of fund fact sheets, detailed informationregarding plan investments and fees onVanguard.com, and through quarterly benefit statements.

>Additional fiduciary c

considerations

39 > Additional fiduciary considerations

plans,there are other fiduciary responsibilities to consider. These include minimum contributions to DB plans as well asERISA Section 404(c) compliance and fiduciary protections, participant educationand advice, company stock, and brokerageaccounts in DC plans.

Maintaining a well-funded DB plan isimportant to both plan participants and the plan sponsor. Making required contributions and investing plan assetsappropriately is an important fiduciary duty.

The funded status of a pension plan isdetermined by comparing the assets withthe present value of benefits that have beenearned at any point in time (the obligationor liability). There is more than one way to

measure asset values and pension liabilitiesbecause there is more than one regulatoryframework used to assess the plan’s fundedstatus. One set of rules is based on the IRSdefinitions originally established in 1974 byERISA and amended several times, mostrecently by the PPA legislation in 2006.Other rules under the Financial AccountingStandards Board (FASB) are used to assessthe funded status for accounting purposes,which is of interest to investors, and governed ultimately by the SEC. There arealso rules used by the PBGC to determinefunded status for their purposes, forexample, when a plan terminates.

Our discussion of funding status looks at thequestion from four distinct perspectives—the three regulatory frameworks and the

> DB funding

For both DB and DC

Additional fiduciary considerations > 40

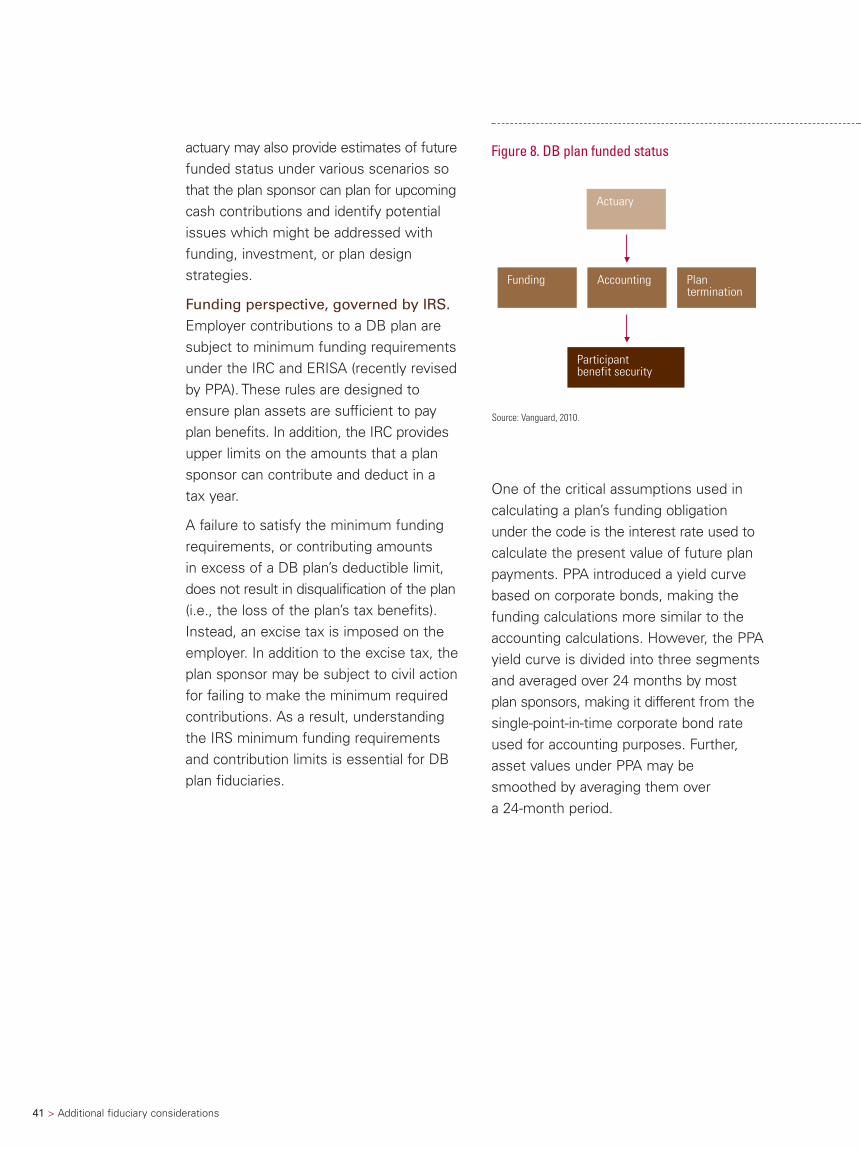

plan actuary. Understanding these perspectives is important for the employerto appropriately discharge fiduciary responsibilities on behalf of plan participants.These perspectives include (See Figure 8on page 41):

• The actuary.

• Funding—governed by IRS.

• Company accounting—governed byFASB and SEC.

• Plan termination—governed by PBGC.

Actuary’s role. A plan actuary will ordinarilyconduct an actuarial valuation on an annualbasis. The actuarial report(s) contains information on funded status for fundingand accounting purposes, as well as possible information for the PBGC.

The actuary’s report provides details aboutthe plan’s liabilities and its funding status.A best practice is for plan sponsors tomeet with the plan’s actuaries and reviewthe numbers, assumptions, and findingsin the annual actuarial report. The actuarycan help the plan sponsor assess howwell the plan is funded by interpreting thenumbers and explaining the differencesbetween the regulatory frameworks. The

Green DB™ is Vanguard’s

approach to creating

sustainable DB pension plans

through low-risk plan design

that provides appropriate

levels of guarantees and

liability-driven investing.

41 > Additional fiduciary considerations

Figure 8. DB plan funded status

Actuary

Accounting

Participant benefit security

Plantermination

Funding

Source: Vanguard, 2010.

actuary may also provide estimates of futurefunded status under various scenarios sothat the plan sponsor can plan for upcomingcash contributions and identify potentialissues which might be addressed withfunding, investment, or plan design strategies.

Funding perspective, governed by IRS.Employer contributions to a DB plan aresubject to minimum funding requirementsunder the IRC and ERISA (recently revisedby PPA). These rules are designed toensure plan assets are sufficient to payplan benefits. In addition, the IRC providesupper limits on the amounts that a plansponsor can contribute and deduct in atax year.

A failure to satisfy the minimum fundingrequirements, or contributing amounts in excess of a DB plan’s deductible limit,does not result in disqualification of the plan(i.e., the loss of the plan’s tax benefits).Instead, an excise tax is imposed on theemployer. In addition to the excise tax, theplan sponsor may be subject to civil actionfor failing to make the minimum requiredcontributions. As a result, understandingthe IRS minimum funding requirementsand contribution limits is essential for DB plan fiduciaries.

One of the critical assumptions used incalculating a plan’s funding obligationunder the code is the interest rate used tocalculate the present value of future planpayments. PPA introduced a yield curvebased on corporate bonds, making thefunding calculations more similar to theaccounting calculations. However, the PPAyield curve is divided into three segmentsand averaged over 24 months by mostplan sponsors, making it different from thesingle-point-in-time corporate bond rateused for accounting purposes. Further,asset values under PPA may be smoothed by averaging them over a 24-month period.

Additional fiduciary considerations > 42

Information related to minimum fundingrequirements is reported to the IRS andDOL on Schedules SB and MB of Form5500. Participants also receive basic information on the funded status eachyear in a Funding Notice.

Accounting perspective, governed by FASB and SEC. A different set of standards applies in reporting the fundingstatus of a DB plan to a public company’sshareholders.

Employer pension accounting determinesthe proper pension expense that is part of the employer’s income statement andthe asset or liability reflected on the plansponsor’s balance sheet. FAS 87 governshow pension accounting calculations areperformed and how results are included inthe income statement and balance sheet.FAS 158 modified FAS 87 to fully reflectthe funded status of each plan as a component of the company’s assets andliabilities. FAS 132R describes informationthat must be shown in footnotes to thecompany financial statements. Pensionaccounting rules are likely to be revisedfurther in coming years and there is aneffort under way to harmonize the UnitedStates with international standards.

For public companies, understanding thepension accounting information and how it impacts the overall corporate financialsituation has become increasingly importantas pension plans have grown. Keeping theplan well-funded and the sponsoring company healthy are both significantaspects of ensuring the security of planbenefits for participants. External partiesinterested in the company’s financial sta-tus—such as investors, debt-rating agen-cies, equity analysts, and the SEC—mayall be interested in not just the results, but the assumptions underlying the pension accounting results.

FAS 87 requires that companies use a rate reflecting the yields on high-qualitycorporate bonds to discount the value offuture pension payments in calculating thepension accounting liability. The discountrate is selected on the day the plan liabilities are measured and is not averaged(unlike the discount rate used for funding,which is smoothed). Additionally, for pension expense calculations, but not the balance sheet, asset values may besmoothed by averaging them over a five-year period.

43 > Additional fiduciary considerations

Plan termination perspective, governedby PBGC. A plan termination by a companyin financial distress is the only way for participants to lose benefits in a tax-qualifiedpension plan. The PBGC provides insuranceprotection for participants and beneficiariesunder DB plans. It effectively offers a federal guarantee of most pension benefitsin the event that the plan sponsor goes outof business or otherwise must terminatethe plan without adequate assets.

Employers pay a premium to the PBGCfor the insurance provided and must alsoreport information on funded status sothat the PBGC can identify potential problems. Sponsors pay an annual insurance premium to the PBGC. Theamount of the required annual PBGC premium for 2010 is $35 per participant.For an underfunded plan, as measured

under the PBGC’s rules, additional premiums are required in the amount of $9 per $1,000 of unfunded vested benefits.(The rates are indexed for inflation.)Employers with plans that are underfundedmust provide information abou t all relatedcompanies and all of their pension plansto the PBGC by filing a Form 4010.

PBGC’s calculations are focused on identifying the funded status in the eventof a plan termination, but the calculationsused to report to the PBGC on an ongoingbasis are somewhat different from the calculations used in an actual plan termination. The ongoing calculations use a discount rate similar to the fundingdiscount rate, but it is not averaged over24 months. Asset values used for PBGCpurposes are not smoothed or averaged.

Additional fiduciary considerations > 44

45 > Additional fiduciary considerations

a plan’s fiduciariesassume all legal responsibility for a retirement plan’s investments. Yet, withthe growth of self-directed DC plans, it is clear that employers have effectivelydelegated investment control and discretionto plan participants. Plan sponsors have anindirect influence over a participant’sinvestment results, principally by selectingthe menu of options offered in the plan.

Acknowledging this shift in investmentresponsibility, Section 404(c) of ERISA and DOL regulations limit an employer’sliability for the investment decisions made by plan participants if certainrequirements are met.

The 404(c) status is optional, but if anemployer chooses to follow the require-ments of 404(c), relief of some fiduciaryresponsibility for the investment decisionsmade by participants is available—animportant shift in legal liability for a plan’sinvestment holdings. The liability relief islimited—employers are still responsiblefor selecting prudent and diversifiedinvestment choices, as well as for monitoring the investment options andmanagers provided to participants. The404(c) relief applies when the participantassumes effective control of investmentsor when participant assets are invested ina QDIA. Employer contributions directedto company stock, or participant moneyinvested in a default fund other than aQDIA, remain the full responsibility ofplan fiduciaries.

> Section 404(c) compliance and additional

Under ERISA,

Additional fiduciary considerations > 46

Because 404(c) offers important fiduciaryprotections, Vanguard recommends all participant-directed DC plans follow thesebest practices:

• Seek to qualify as a 404(c) plan as wellas offer a QDIA as the default fund.

• Conduct a periodic analysis of 404(c) status.

• Satisfy the 404(c) rules for company stock.

Best practice—Qualify for 404(c)

Section 404(c) offers important benefits in the event of any participant litigationregarding plan investments. FromVanguard’s perspective, this potential benefit alone justifies the relatively small effort needed to comply with the regulation.

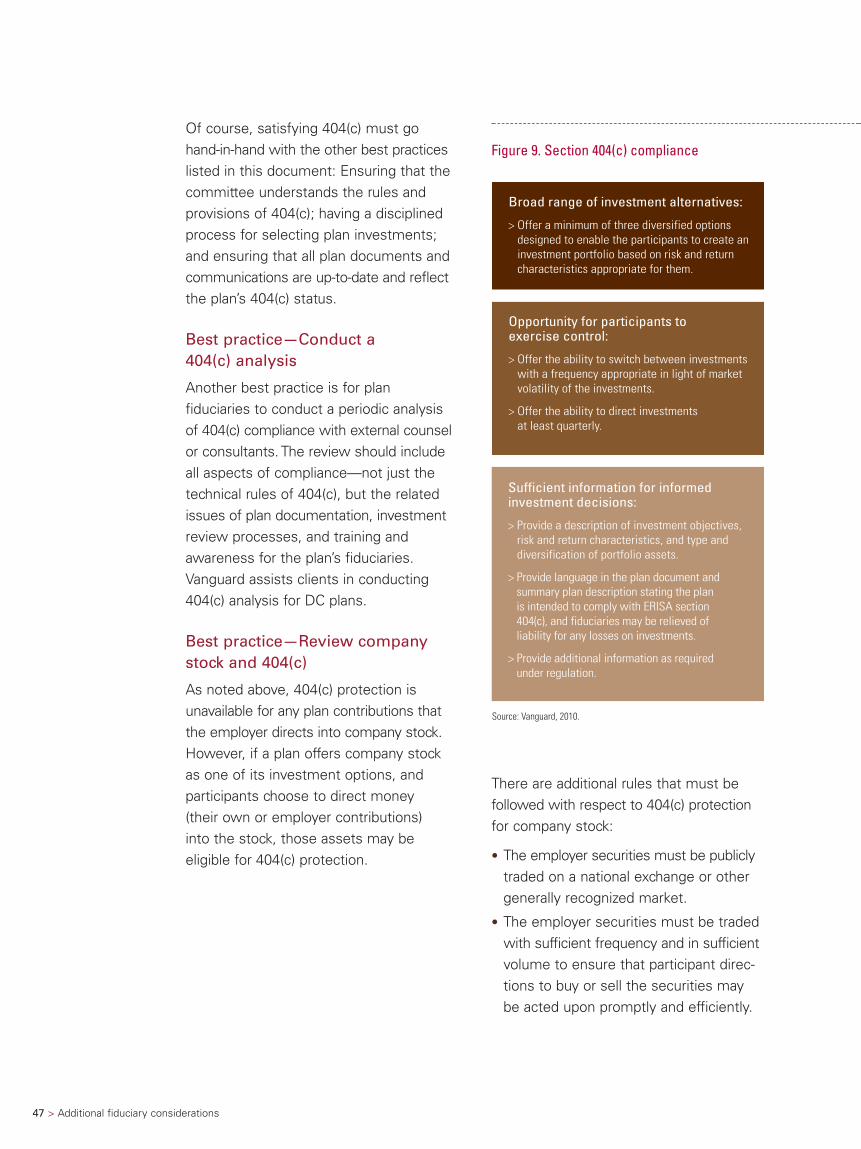

There are a number of well-known features of 404(c) (See Figure 9 on page47). The plan must offer a minimum ofthree diversified options designed toenable the participants to create aninvestment portfolio based on risk andreturn characteristics appropriate forthem. Participants must have the right to change investment instructions (i.e.,exchange investment funds or changecontribution allocations) at least quarterly.However, DC plan fiduciaries may findthat some participants abuse their dailytrading privileges by engaging in market-timing. The DOL has stated that imposingappropriate trading restrictions does notinterfere with 404(c) compliance.

404(c)

fiduciary protections

It is Vanguard’s view

that plan fiduciaries

should seek to qualify

as a 404(c) plan

as well as offer a QDIA

as the default fund.

47 > Additional fiduciary considerations

Of course, satisfying 404(c) must go hand-in-hand with the other best practiceslisted in this document: Ensuring that thecommittee understands the rules and provisions of 404(c); having a disciplinedprocess for selecting plan investments;and ensuring that all plan documents andcommunications are up-to-date and reflectthe plan’s 404(c) status.

Best practice—Conduct a 404(c) analysis

Another best practice is for plan fiduciaries to conduct a periodic analysisof 404(c) compliance with external counselor consultants. The review should includeall aspects of compliance—not just thetechnical rules of 404(c), but the relatedissues of plan documentation, investmentreview processes, and training and awareness for the plan’s fiduciaries.Vanguard assists clients in conducting404(c) analysis for DC plans.

Best practice—Review companystock and 404(c)

As noted above, 404(c) protection isunavailable for any plan contributions thatthe employer directs into company stock.However, if a plan offers company stockas one of its investment options, and participants choose to direct money (their own or employer contributions) into the stock, those assets may be eligible for 404(c) protection.

There are additional rules that must be followed with respect to 404(c) protectionfor company stock:

• The employer securities must be publiclytraded on a national exchange or othergenerally recognized market.

• The employer securities must be tradedwith sufficient frequency and in sufficientvolume to ensure that participant direc-tions to buy or sell the securities may be acted upon promptly and efficiently.

Figure 9. Section 404(c) compliance

Broad range of investment alternatives:

> Offer a minimum of three diversified options designed to enable the participants to create an investment portfolio based on risk and return characteristics appropriate for them.

Opportunity for participants to exercise control:

> Offer the ability to switch between investments with a frequency appropriate in light of market volatility of the investments.

> Offer the ability to direct investments at least quarterly.

Sufficient information for informed investment decisions:

> Provide a description of investment objectives, risk and return characteristics, and type and diversification of portfolio assets.

> Provide language in the plan document and summary plan description stating the plan is intended to comply with ERISA section 404(c), and fiduciaries may be relieved of liability for any losses on investments.

> Provide additional information as required under regulation.

Source: Vanguard, 2010.

Additional fiduciary considerations > 48

• Information provided to shareholders ofthe employer securities must be providedto participants whose plan accounts areinvested in employer securities.

• Voting, tendering, and similar rights withrespect to employer securities must bepassed through to participants.

In addition, a 404(c) plan must include procedures designed to safeguard theconfidentiality of information related toparticipant-directed transactions involvingthe plan’s employer securities. The planalso must designate a fiduciary to monitorcompliance with these procedures. If thedesignated fiduciary determines that aconflict exists (in the case of a tenderoffer or contested board election), an inde-pendent fiduciary must be appointed.

Additional fiduciary protections—QDIA, reenrollment, fund mapping

QDIA. Plan sponsors should select a QDIAas the default fund to shield plan fiduciariesfrom liability for investment losses whenparticipants do not make an affirmativeinvestment election. Additionally, a QDIA isimportant for sponsors who have alreadyadopted or are considering an automaticenrollment program for their DC plan. The “Investment Strategy” section of theguidebook provides additional informationregarding a QDIA and evaluating target-date funds.

Reenrollment3. As a result of the PPA,reenrollment has emerged as a new plan design strategy to improve portfoliodiversification. With reenrollment, currentparticipants are reenrolled and theiraccount balances in the plan are transferredinto the plan’s QDIA, with an opt-out right

for participants preferring to retain theirexisting asset allocations. This strategy hasthe dual benefit of improving diversificationof plan assets and assisting plan sponsorsin limiting fiduciary liability. Such a strategymight be used in a variety of settingsincluding conversions to a new record-keeper, or menu changes to a plan’sinvestment lineup. Importantly, if thesponsor follows this reenrollmentapproach, and adheres to the proceduralrequirements in the QDIA regulations, participants will be deemed to have exercised control over their accounts and plan fiduciaries will not be liable for investment losses incurred by these participants.

Fund mapping. The PPA extends the fiduciary protection of ERISA Section404(c) to plan sponsors who are mappingparticipants’ assets from one investmentoption to another, provided the mapping is a “qualified change in investment.” Aqualified change in investment occurs ifassets invested in the eliminated option arereallocated to a remaining or new optionin the plan that is “reasonably similar” tothe old option in terms of risk and return,and participants are notified of the changeat least 30 days—but no more than 60days—before the change. The notice mustprovide participants with an opportunity to make an affirmative election to movemoney to another investment option before the mapping.

3 For additional details on reenrollment, see Improving plan diversification through reenrollment in a QDIA, Vanguard Strategic Retirement Consulting, September 2008.

49 > Additional fiduciary considerations

contained noexplicit requirements regarding fiduciarystandards for participant education andadvice. However, over the years, with thegrowth of individual account plans, the DOLhas undertaken a number of efforts to promote participant education. For example,the DOL outlined the types of educational programs that would be appropriate forplan participants, issued regulations that encourage the use of personalizedadvice services, and affirmed the use ofindependent third-party advice for DC plan participants. Additionally, PPA providedprohibited transaction exemptions forservice providers who offer investmentadvice to DC plan participants.

Considerations

Clearly, many participants need investmenteducation or advice. They are not schooledin the complexities of investment management or the principles of assetallocation and diversification—yet they stillhave responsibility for making investmentdecisions. Others may be comfortablewith investment decision-making butstruggle with setting appropriate savingstargets for retirement.

In part because of participant inertia, plan sponsors are implementing designstrategies intended to improve participationand portfolio diversification in participant-directed DC plans. These design strategies

> Participant education and advice

ERISA originally

Additional fiduciary considerations > 50

include automatic enrollment plan featuresand QDIAs. Plan design is critical, but in considering their overall design strategy,plan fiduciaries should also take steps toensure that all participants have access to education and advice programs that willenable them to make informed choices.