beyond fico: default prediction and optimal lending

TRANSCRIPT

Beyond FICO: Default Predictionand Optimal Lending Strategies

in Online P2P InvestingThe Harvard community has made this

article openly available. Please share howthis access benefits you. Your story matters

Citable link http://nrs.harvard.edu/urn-3:HUL.InstRepos:38811439

Terms of Use This article was downloaded from Harvard University’s DASHrepository, and is made available under the terms and conditionsapplicable to Other Posted Material, as set forth at http://nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of-use#LAA

Acknowledgements

I would first like to thank my adviser Yaron Singer for all of his help through this process. From

iterating through what seemed like a dozen ideas to providing the inspiration for what would

eventually become this thesis to reviewing my analyses and writing, his assistance has been

invaluable. I would also like to thank John Campbell for agreeing to read my paper without

hesitation and helping me work through the theoretical foundations for the economic analysis of

investment strategies that has become the cornerstone of this project. I am especially thankful

for him because without his class Economics 1723, I would have never had the insight to turn

what was initially a project about predicting defaults to a much more interesting project about

investment optimization. Additional thanks go to LendingClub for making their data public and

thereby facilitating such endeavors. I am especially indebted to my friends and family for their

warmth and support.

Special thanks go to late night pizza deliveries from the Dominos Pizza in Harvard Square,

without which this thesis realistically would never have been completed.

2

Contents

1 Introduction 6

2 Preliminaries 9

2.1 LendingClub: A Primer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.2 Literature Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.2.1 On Borrowers and Default Risk . . . . . . . . . . . . . . . . . . . . . . . . 13

2.2.2 On Online P2P Investing . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

3 Dataset 18

3.1 Features . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3.2 Variable Sets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

4 Default Prediction 28

4.1 Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

4.1.1 Balancing the Dataset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

4.1.2 Ranked Optimal Subset Algorithm . . . . . . . . . . . . . . . . . . . . . . 31

4.2 Overview of Classification Methods . . . . . . . . . . . . . . . . . . . . . . . . . . 32

4.2.1 K-Nearest Neighbors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

4.2.2 Decision Tree . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

4.2.3 Linear Regression . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

4.2.4 Logistic Regression . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

4.3 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

4.3.1 Overall Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

3

4.3.2 Variable Set Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

4.4 Marginal Value of FICO Score . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

4.5 Default Probability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

5 Investment Strategy Analysis 49

5.1 Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

5.1.1 Mean-Variance Analysis of a Loan . . . . . . . . . . . . . . . . . . . . . . 50

5.1.2 Mean-Variance Analysis of a Portfolio of Loans . . . . . . . . . . . . . . . 52

5.2 Calculating the Loan Correlation . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

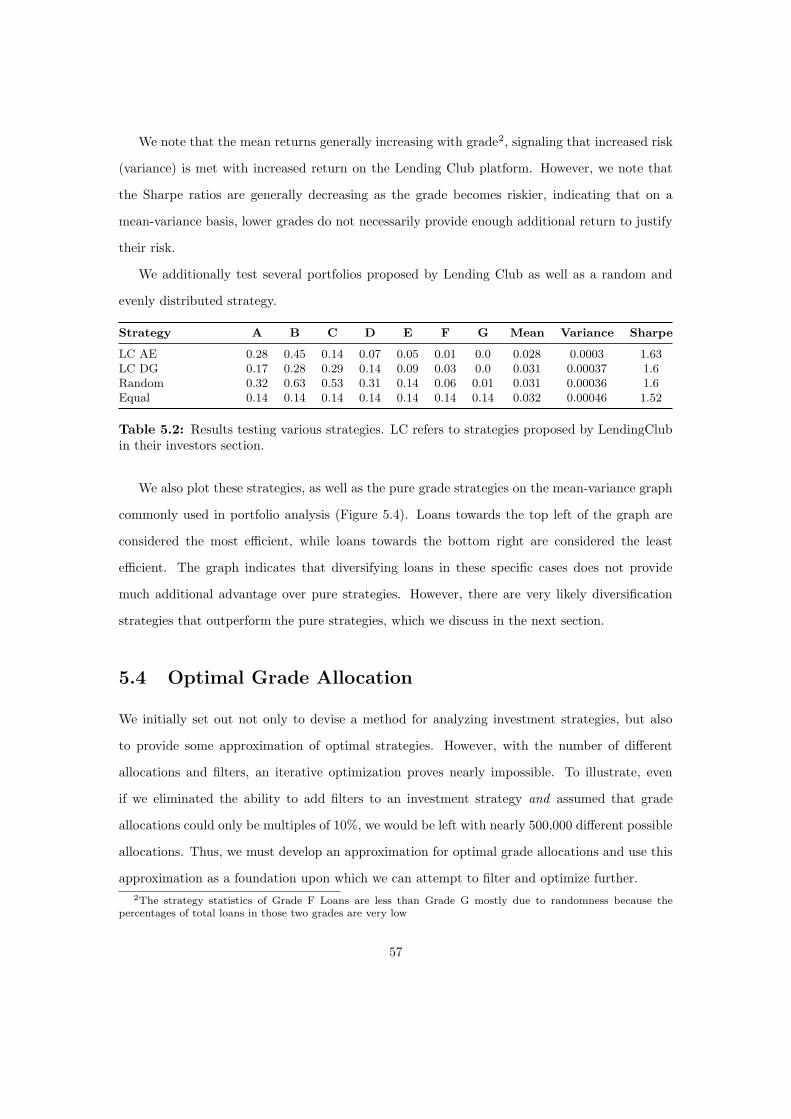

5.3 Analysis of Grade Allocation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

5.4 Optimal Grade Allocation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

5.5 Analysis of Filtering Strategies . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

5.6 Optimal Filters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

5.7 Introduction of Novel Analysis Tool . . . . . . . . . . . . . . . . . . . . . . . . . 67

6 Conclusion 68

Appendices 72

A Additional Information 73

A.1 Application Screenshots . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

A.2 LendingClub Screenshots . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

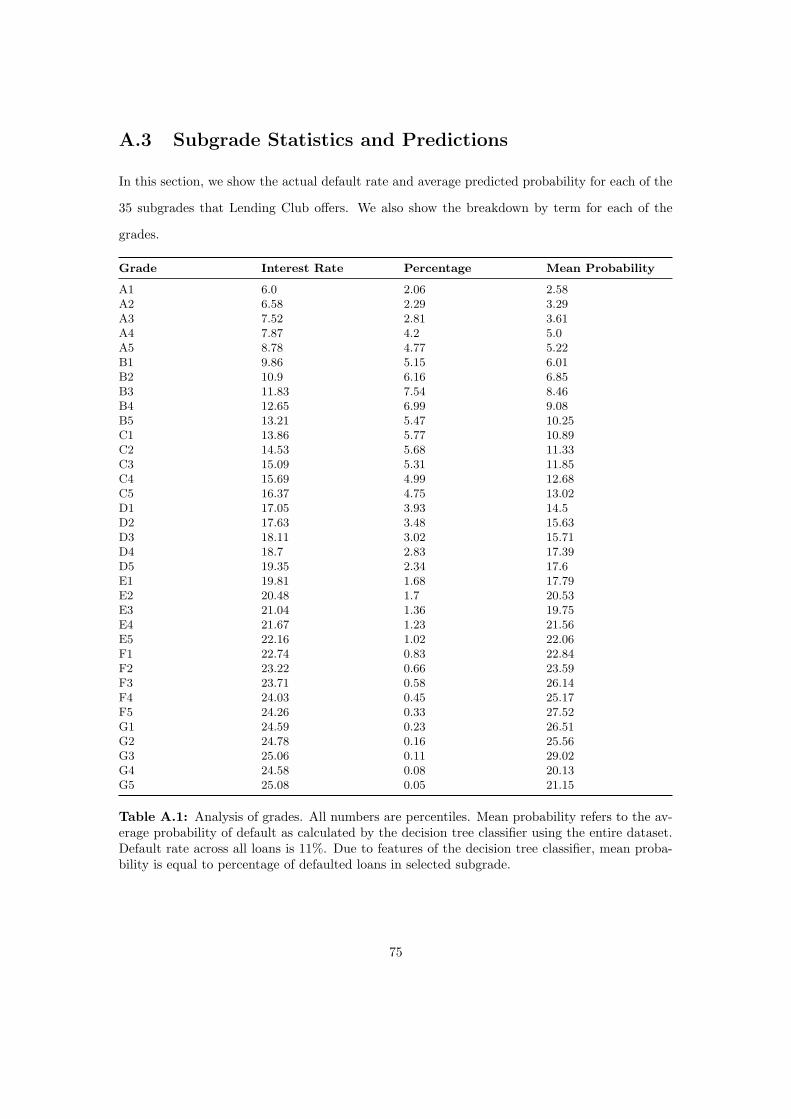

A.3 Subgrade Statistics and Predictions . . . . . . . . . . . . . . . . . . . . . . . . . . 75

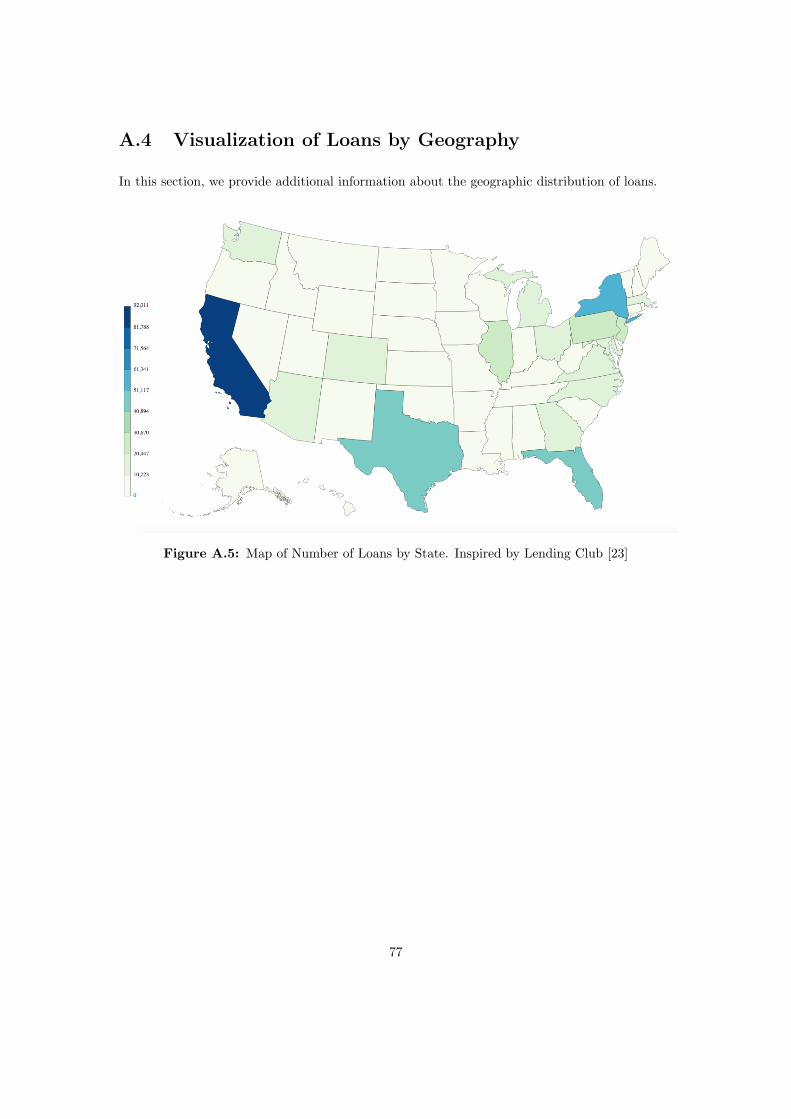

A.4 Visualization of Loans by Geography . . . . . . . . . . . . . . . . . . . . . . . . . 77

A.5 Pseudocode for Ranked Optimal Subset Algorithm . . . . . . . . . . . . . . . . . 78

A.6 Additional Classification Methods . . . . . . . . . . . . . . . . . . . . . . . . . . 79

A.6.1 Perceptron Algorithm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

A.6.2 Support Vector Machine . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

A.6.3 Boosted Decision Tree . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

B Additional Data 82

B.1 Additional Default Prediction Results . . . . . . . . . . . . . . . . . . . . . . . . 82

4

B.2 FICO Comparison Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

B.3 Grade Allocations for Filtering Strategies . . . . . . . . . . . . . . . . . . . . . . 87

Bibliography 89

5

Chapter 1

Introduction

Over the last decade, against the backdrop of the financial recession, a radical new form of

lending known as online P2P (Peer-to-Peer or People-to-People) lending has grown tremendously,

disrupting traditional financial intermediation and changing the landscape of the credit markets.

The fundamental premise behind this new form of lending is that borrowers can apply online

for loans and other individuals can fund these loans and receive interest payments, potentially

making substantial returns. Dominated by U.S. based LendingClub and Prosper and U.K. based

Zopa, these companies have suceeded not only due to their ability to provide credit at lower rates

than borrowers other might receive, but also by introducing a lucrative, alternative asset class

for investors [48]. Indeed, this ability of investors to potentially outperform the market with

these loans has spawned a huge community of investors (see LendAcademy, LendingMemo), as

well as automatic investing services (LendingRobot), a secondary market (Folio) and retirement

accounts on several platforms.

An effect of this is a huge variety of information as to the best strategies to utilize P2P

lending platforms. A cursory glance at these investment communities yields vastly different

optimal strategies, largely based on anecdotal evidence of high returns. Some investors believe

in only investing in low-risk loans while others believe the opposite. Still more believe in investing

in a variety of risk levels, but disagree on the specific allocation. It is in this conflict of opinions

that our motivating problem emerges.

6

Our thesis has two main goals:

1. Using publicly available data from LendingClub to develop a framework for analyzing

lending strategies on Online P2P Marketplaces and, in doing so, develop a set of optimal

investment strategies.

2. Analyze the features that affect default in Online P2P Loans, specifically focusing on

determining predictive value of the FICO Score, which has had its effectiveness questioned

in recent times, and the Lending Club assigned subgrade of the loan [44].

The framework we introduce, based largely on modern portfolio theory and the ideas of ex-

pected value, fundamentally consists of viewing an lending strategy as the purchase of a portfolio

of loans, each of which has a mean and variance [33]. Thus, the default prediction question fol-

lows naturally from that of determining optimal lending strategies, as a determination of the

probability of default is essential to calculating the mean and variance of a loan. To investigate

default, we first use several machine learning methods to classify the loans into ”default” and

”paid off”, in an extension of a fairly common machine learning problem. In our analysis of the

causes of default, we noticed that the subset of features used in classification has a large effect on

the predictive accuracy of a loan classifier. Furthermore, though a few studies have shown which

features in the Lending Club dataset are most predictive of default, hardly any have separated

features into subsets in an attempt to determine the effect of including or excluding a certain

feature from the classifier [44]. We seek to extend these analyses of the LendingClub dataset by

doing just that. By ascertaining and quantifying the effects of each feature on default, we hope

to provide insights into the drivers of default not only in LendingClub but in personal credit

markets more generally. In doing so, we hope to inform both borrowers and investors, for, as

we will discuss throughout this work, default is the single most important determinant of the

success of an investment strategy and minimizing perceived likelihood of default is paramount

to obtaining lower rates for borrowers.

The thesis is structured in the following way. Chapter 2 provides background information

on Lending Club, including previous studies on the subject, to better understand the envi-

ronment in which our analyses take place. In Chapter 3, we provide a brief outline and ex-

ploratory investigation of the LendingClub dataset that we used for our analysis to better

7

understand the features and terminology used throughout the remainder of the work. After

these preliminaries, we dive into the issue of default prediction in Chapter 4, discussing the

various methods and statistical learning techniques used in the analysis as well as their re-

sults. We devote Chapter 5 to the discussion of the two major investment decisions all Lend-

ingClub investors must make: determining the allocation of their portfolio and determining

which (if any) filters to use in the dataset. Finally, we provide concluding remarks in Chap-

ter 6. As we will show, while various methods can approximate optimal strategies, with mil-

lions of allocation-filter combinations, finding optimal points can be quite complex. To aid in

this process, we introduce an online application to simultaneously test allocations and filter-

ing strategies using the framework developed in the rest of the work. This application can be

found at http://kunalmehta-thesis-dev.us-west-2.elasticbeanstalk.com and

screenshots can be seen in Appendix A.1.

8

Chapter 2

Preliminaries

In this section, we seek to ground this thesis in its larger context. Because we focus on Lending-

Club exclusively in the analyses to come, we first provide an extensive overview of the platform

itself, as well as the terminology and mechanisms that the platform uses. In addition, we also

review some of the existing literature on default prediction and investment optimization on

LendingClub and online lending more generally.

2.1 LendingClub: A Primer

LendingClub describes itself in the following way:

”We are the world’s largest online credit marketplace, facilitating personal loans,

business loans, and financing for elective medical procedures. Borrowers access lower

interest rate loans through a fast and easy online or mobile interface. Investors

provide the capital to enable many of the loans in exchange for earning interest [13].”

For our purposes, this description is succinct and quite apt. Indeed, LendingClub can be

summarized as having two main functions: (1) providing borrowers with a way to apply for and

access loans and (2) allowing investors to fund those same loans. We will discuss each of these

functions in depth by way of a look at the life of a loan.

9

Directly from LendingClub’s home page, borrowers can check their rates by entering their

FICO Credit Range, the purpose of their loan and their required amount (up to $25,000) [7].

Following this preliminary questionnaire, they then fill out a simple form with basic personal

information as well as annual income. Once they submit this form, they allow LendingClub to

verify their income and additionally agree to various legally binding documents. LendingClub

will then instantly provide them with an assigned grade (A-G) and subgrade (1-5) and a cor-

responding interest rate and a term length for various loans that they qualify for depending on

their credit characteristics [10]. Loans classified as A1 are considered the safest and have the

lowest corresponding interest rates and those in grade G5 the most risky and therefore require

the highest interest rate. Appendix A.3 provides a detailed breakdown of the grades and cor-

responding interest rates for the loans. Once borrowers choose a loan and term, they fill out

additional employment and bank account information and, a few hours later, after additional

verification, the loan is listed on the LendingClub online marketplace.

For the borrower, paying back the loan is simple. They are given an amortized payment

schedule relating to their loan amount and interest rate and must make the required monthly

payment until the loan matures (either 36 or 60 months). For more information on this process,

please see LendingClub and SocialLendingNetwork [7, 10]. For an example of a loan payment

schedule please see LendingMemo [35].

Investors, upon signing in to LendingClub, see a marketplace of available loans as well as an

interface to view the status of their invested loans (see Appendix A.2 for visualizations of these

interfaces) [13]. Upon deciding on investing in a loan, an investor can fund as little as $25 of the

loan, allowing for significant diversification across loans. Let’s say our investor decides to lend

$25 in the loan from above. Then, over the next few days (LendingClub’s average funding time

is approximately seven days, according to their website), other investors will purchase portions

of the loan until the full amount has been funded [8]. At this point, the borrower receives the

amount of the loan in their bank account and must make required payments each month. They

may additionally prepay the amount of the principal at any time.

Investors face two primary risks to their returns: (1) default risk and (2) prepayment risk.

Default risk naturally refers to the likelihood that a borrower does not pay back the loan, thereby

preventing the investor from earning the agreed-upon return. Traditional financial intermediaries,

10

as well as LendingClub investors, are most concerned with this risk as it poses the highest risk

to their returns, often even causing large losses to the investor. Prepayment risk refers to ther

likelihood that a borrower pays the principal off early, thereby preventing the investor from

earning the entirety of the interest paid over the full term of the loan. While prepayment risk

is difficult to classify, LendingClub provides a number of labels that inform the investor as to

the current default status of the loan. We have summarized these in Table 2.1 and additionally

provided the number of loans in our dataset that fit each label.

Status Description Number

Current The loan is currently being paid off on time. 428,294Fully Paid The loan was fully paid off. 163,412Grace Period Payments are late by 15 days or less on this loan. 5155Late (16-30 days) Payments are late by 16-30 days on this current loan. 1952Late (31-120 days) Payments are late by 31-120 days on this current loan. 9215Defaulted Payments are late by 31-120 days on this loan. 223Charged Off LendingClub believes that there further payments on this loan

are unlikely. Payments are 150 days past due date.35,389

Table 2.1: Loan Status Categories from LendingClub [12]

When a borrower misses a payment, LendingClub enacts a process that attempts to return

the loan to ”Current” status [7]. If after 150 days, the borrower has not restarted payments on

the loan, the loan is ”charged off”, which is essentially default beyond the point of recovery. At

this point, LendingClub believes any attempt to reacquire the value of the loan are fundamentally

futile. Nonetheless, LendingClub outsources collection of charged off loans to a third-party but

admits that any recoveries after the loan is charged off are ”infrequent” [7].

LendingClub profits off this process in several ways. First, investors are charged a 1% service

fee for each purchase. Additionally, LendingClub charges 30% of any collections made after the

loan is classified as late and 30% of attorney fees and costs in the case of litigation [7]. This

fee structure undoubtedly has been successful for the company, leading to a $400 million dollar

revenue in 2015 [22].

We have hitherto discussed the investment and payment process for a single loan. However,

hardly any investors purchase a single loan. In fact, most do not even manually select which

loans to purchase, instead utlizing LendingClub’s propietary ”Automated Investing” tool. Here

investors can use two tools to craft an investment strategy

11

1. Grade Allocation: Investors can select an allocation of grades A-G they would like to

invest their funds in. LendingClub also has some predefined allocations, which we will

discuss in Chapter 5.

2. Filters: Investors can filter based on the features discussed further in Chapter 3 by selecting

a variable and a cutoff amount. For example, investors can choose to invest only in loans

whose borrowers have an income of greater than $50,000 per year. When a filter conflicts

with a grade allocation, the automated investor notifies the borrower and ceases activity.

Investors can also sell loans through LendingClub’s Note Trading Platform (in partnership

with Folio Investing) [11]. Without this platform, however, investors must hold the loans through

maturity. LendingClub claims that 99.9% of investors with more than $2,500 invested in more

than 100 loans see positive returns on their investment, a claim that will be addressed in the next

few chapters [23]. Primarily due to the novelty of online lending, there seems to be a relative

dearth in academic discussion regarding issues of default prediction and investment optimization

in online lending, with much of the work in the field coming from informal sources, mostly

investment forums and the like. We review both types of research in the next section, as both

provide insights into the data.

2.2 Literature Review

We first look at works that provide an overview of the P2P Lending, often comparing it to

traditional intermediaries. Wang, Greiner and Anderson provide perhaps the most complete

overview of the concept of online peer lending, categorizing LendingClub, Prosper and Zopa

into Profit-Seeking Lending Models, one of the four quadrants of a matrix separated by what

they see as the two main factors that differentiate lending models: motive of lending (economic

or philanthropic) and degree of separation (friends or strangers) [48]. Furthermore, they note

that ”the value proposition of P2P lending for borrowers is that they are able to obtain loans

with lower interest rates than bank loan rates...[and the] value proposition for lenders is that

P2P loans offer an alternative investment option [48]”. Berger and Gleisner not only provide an

excellent overview of the history and existing literature on Online P2P Lending, but also discuss

12

the now-discontinued group dynamic on Prosper, in which ”screening of potential borrowers and

monitoring of loan repayment can be delegated to designated group leaders [24]”. They find that

these group leaders serve as financial intermediaries not dissimilar to banks in terms of their

ability to reduce information asymmetries, thereby improving credit conditions [24].

Wang, Chen, Zhu and Song model online P2P Lending as a process, noting interesting dis-

tinctions between the process in P2P lending versus traditional lending [47]. They conclude

that ”P2P lending provides users more privilege in choosing the lending manner and lending

objects...so the information flow...is more frequent and transparent”, but also find that loan

management is subpar in online P2P lending as compared to a traditional bank, mostly due to

its inability to track post-loan information as well [47]. Zeng and Brill both look at the legal

framework for P2P lending with different perspectives. While Zeng takes a global approach, Brill

specifically looks at how the Dodd-Frank act effects the online lending environment [50, 25].

2.2.1 On Borrowers and Default Risk

The most expansive academic literature about peer-to-peer lending focuses on the borrowers, de-

termining different qualities that effect their ability to receive credit. We have already mentioned

how Berger and Glesiner find that group leaders serve as financial intermediaries, improving

credit conditions. Ghasemkhani and Tan look at how reputations affect borrowing ability, using

an unnamed online marketplace that provides borrowers history of loans on the marketplace [31].

Gonzalez and McAleer show that higher amounts and certain purposes slow funding in Prosper

and Zopa and that the number of lenders increases with higher credit ratings and loan sizes,

indicating ”lenders set limits as per rule of thumb in terms of diversification [32]”. Pope and

Sydnor, in an appalling study, find that racial disparities between profile pictures on Prosper

affect interest rates and ability to obtain credit, finding that those with darker skin tend have

higher interest rates and default rates than those with whiter skin, on average [42].

LendingClub, in its current form, is a much simpler platform than many of those studied in

previously mentioned articles. Its data consists of a number of numeric features, excluding most

identifying information of a member. As such, our default prediction methodology focused on

these numeric features, detailed in Chapter 3. However, a few studies have emerged focusing on

13

this very problem, though many are still quite distinct from the default prediction analysis we

conduct in Chapter 4.

A study from the University of Zaragoza analyzes the various features on the data available

publicly on LendingClub using a logistic regression to predict default. The study finds that

the grade assigned by LendingClub is the most predictive, but other factors are also predictive,

especially the debt-to-income ratio [44]. Machine learning blog yhat studies the same dataset

and uses a random forest to predict loan defaults, creating an analysis tool that allows one to

input various parameters to return a probability of default [49]. Cunningham also provides an

interesting history of defaults on Lending Club, showing how the company’s move upward to a

borrower’s average FICO Score of 700 decreased the default rate overall of borrowers [29]. In

determining default, we also want to consider the effects of the LendingClub assigned grade and

the FICO Score on default and thus investment strategy analysis. While the Zaragoza study and

the yhat application provide some insights into these effects, our isolation of the FICO Score

was primarily due to recent research that suggests that the FICO Score as a measure of credit

risk may need to be rethought. In particular, a joint study by Istanbul Sehir University and

Johns Hopkins uses LendingClub data to find that ”the traditional credit scoring methods fall

short in identifying risky borrowers and that social lending has different dynamics compared to

traditional lending [26]”. Additionally, they note that so-called ”social data” is important to

consider.

These studies, for the most part, differ from ours primarily in that they lack an analysis of the

marginal value add in predictive accuracy by various features. As we will discuss in Chapter 4,

our formulation allows us to generally understand the effect of these features on default in a more

nuanced way than the previous analyses, though the models constructed in previous studies are

sometimes more involved than the ones used in our analysis.

2.2.2 On Online P2P Investing

In terms of previous research on investment strategies in LendingClub, specifically analysis of

grade allocations and filters, the academic publications are few and far between. Ethan Namvar

writes an article outlining Online P2P loans as an investment strategy, detailing several online

14

marketplaces, diversification strategies among P2P loans and between P2P loans and asset classes

[40]. He further lists several risks inherent with investing in online loans: regulatory, default,

prepayment and liquidity [40]. However, the article does not supplement its analysis with any

details on investment strategy, rather simply indicates that the investment opportunities are

possible [40]. A working paper from the National Bureau of Economic Research in 2010 outlined

the use of LendingClub loans to determine risk aversion by determining the effects of housing

market declines on portfolio allocation strategies [41]. Other than these selected examples,

we found it difficult to find articles or studies published in reputable academic journals that

dealt with online P2P loans as investment assets. As such, the majority of literature published

on the subject comes from blogs, such as the aforementioned LendingMemo or LendAcademy,

and forums dedicated to the subject. This reality poses several difficulties, but also has some

advantages. To start off, there is an expansive community of thousands of investors who share

ideas on the subject. However, they share these ideas solely for the purpose of personal gain

and thus very rarely engage in an academic discussion of the subject matter. As a result, as

mentioned in the introduction, there is an incredible diversity of opinions on investment strategies

in LendingClub, as a quick Google seach of just that will quickly inform you.

A report on US News entitled ”4 Tips for Investing with P2P Loans” notes the following

about investment strategies:

”I have been taking my expansion beyond A-rated credit slowly. I have invested in

notes from those with B and C credit, and once I invested in a note from someone

with E credit (there was a compelling story in the profile). However, I know those

who balance their P2P lending portfolios by investing half in those with A-rated

credit, and the other half with those with D, E, and F ratings [37].”

This strategy meets its counterpart in LendAcademy’s Peter Renton’s article ”Why I Avoid

A-Grade Loans on Lending Club and Prosper [43]”. His view is that

”It all comes down to your goals for your investment. For me I want double-digit

investment returns from peer to peer lending. With that in mind all A-grade invest-

ments on Lending Club and AA-grade investments on Prosper pay less than this. So

15

if I invest in these loans then I am hurting my chances of hitting my goal of 10% or

more [43].”

These views are inherently disparate and such controversy is commonplace in the Online P2P

Lending library, where there are hundreds of discussions on the best filters and allocations to

use. We have provided a sampling of these discussions here. LendAcademy’s Ryan Lichtenwald

writes that his main strategy for LendingClub is to use D and E rated loans, while filtering

only on the purpose of the loan [36]. Cunningham decides to invest in E,F,G notes, filtering

on home ownership, inquiries, income and geography [30]. A blog entitled ”Write your own

reality” advises a grade allocation across C,D,E,F and G, and filters on the inquiries in the last

six months, purpose, income and employment length [21]. Nick Clements, of Magnify Money,

notes that ”all types of diversification are important” and thus would probably disagree with

Lichtenwald’s grouping among only 2 grades [27].

These differences can perhaps best be described by this response to a question on LendA-

cademy’s anonymous forums.

”Fred, I am talking to the original poster Rob. He is the one asking other people

who have D and E investments about their portfolio’s performance. Since you do not

invest in these kind of notes there is no need for you to offer your opinions. Please

let us D and E investors commiserate and discuss with each other [5].”

These heated discussions, though a bit comedic, highlight the intense difference of opinions

that categorize the LendingClub investor community. As mentioned in the introduction, it is in

this discussion that our thesis finds its place. While a number of applications provide analytics

on LendingClub filter strategies (NickleSteamroller, PeerCube, LendingRobot), none provide

ways to simultaneously test grade allocations and filters and thus do not provide an accurate

representation of the investment decisions made on LendingClub. Further, on an investment

analysis basis, few provide a way to assess the risk-reward value of a strategy concurrently,

instead focusing on metrics such as the return-on-invesment, annual-percentage-rate and Loss

ratio.

Our framework diverges from these methods, introducing simple method for analyzing the

investment value of an investment strategy. Borrowing from the tools of portfolio analysis, we

16

use the Sharpe ratio, a measure of the mean-variance efficiency of a portfolio, to ascertain the

quality of an investment strategy, using a method we will fully describe in Chapter 5.

17

Chapter 3

Dataset

In this chapter, we discuss the LendingClub dataset and specifically focus on the features used in

the analyses of default and investment strategies. The LendingClub data contains statistics on

over 640,000 loans funded over the course of 8 years from June 2007 to July 2015 [6]. Additionally,

the dataset contains limited information on loans that were rejected by the site from the years

2007 to 2011. Since these loans were never funded, we exclude them from the analysis. Without

these loans, we can sort the data into 6 categories based on their current status. These statuses

can be found in Table 2.1.

As the table suggests, the majority of loans are current. This is largely due to the fact that

many of the loans have term lengths of 3 or 5 years, so many loans in recent years have yet to

be fully paid off or charged off. We assigned current, late and defaulted loans a ultimate status

based on a method consistent with LendingClub’s own approximations which we will outline

more completely in Section 4.5. This process yields an adjusted dataset with a total default

rate of 11%, in line with what many consider LendingClub’s base rate [29]. With that in mind,

we provide some exploratory analysis on this adjusted dataset in its entirety. Importantly, this

dataset is distinct from the one used in default prediction. We describe the reasons and methods

for the change in dataset in Chapter 4.

18

3.1 Features

After cleaning the data, we were left with over 50 features for each loan, many of which were

relevant for our default prediction models. Out of these features, we will now provide some detail

and exploratory analysis on the ones that were used in the models. We limited our predictive

features to non-performance related variables. In other words, the behavior of the borrower after

he or she receives the loan (their payment rates, how often they are late, etc.) is excluded from

the analysis as we wish to formulate a prediction methodology based on inherent characteristics

of the borrower and his or her credit to attempt to better understand how to navigate the peer

to peer lending marketplace. We also excluded several text based variables that could not be

suitably rendered into numbers that conveyed any valuable information to the classifiers. Finally,

we excluded time-based variables (except for those that are relative, such as how many months

since the borrower’s last delinquency) because our analysis is time-independent. Though there

might be a relationship between time and defaults (i.e. a recession), we assume that we purchase

our portfolio of loans at some arbitrary time and thus cannot use any variables outside of the

characteristics of the borrower known at application.1

We provide information about what each variable means in Table 3.1. These descriptions

are taken from the supplementary information to the Lending Club data. We made a few minor

modifications to the data for our analysis. For Grade, we mapped the letter-number combinations

given by Lending Club (A1-G5) to the numbers 1-35. For more information see Appendix A.3.

For employment length, employment length beyond 10 years was characterized as 10+ in the

data. We mapped values of 10+ to 11. For the variables that are mths_since_x, a value of

0 indicates that the borrower in question had no derogatory actions on file. For the variables

entitled home_ownership and purpose, we transformed them into multiple binary variables,

each of which corresponding to a possible value of these variables. See Table 3.3 for possible

values and further information.

Our default prediction analysis fundamentally attempts to use combinations of features to

predict the Loan Status (a binary variable that indicates whether a loan is charged off). The rest

of the features nicely separate into five categories. Since one of our objectives is to isolate the

1Notably, we use the issue date and last payment date variables for our investment strategy analysis, but thesearen’t features of the dataset used for classification (see Section 5.1 for more information).

19

Variable Description

loan_status Current status of the loanfico_range_high The upper boundary of range the borrower’s FICO belongs to.fico_range_low The lower boundary of range the borrower’s FICO belongs to.fico_median Median of range of borrower’s FICO Score at application.last_fico_range_high The last upper boundary of range the borrower’s FICO belongs

to pulled.last_fico_range_low The last lower boundary of range the borrower’s FICO belongs

to pulled.loan_amnt The listed amount of the loan applied for by the borrower. If

at some point in time, the credit department reduces the loanamount, then it will be reflected in this value.

term The number of payments on the loan. Values are in months andcan be either 36 or 60.

int_rate Interest Rate on the loangrade LC assigned loan gradeaddr_state The state provided by the borrower in the loan applicationemp_length Employment length in years. Possible values are between 0 and

10 where 0 means less than one year and 10 means ten or moreyears.

annual_inc The annual income provided by the borrower during registration.dti A ratio calculated using the borrower’s total monthly debt pay-

ments on the total debt obligations, excluding mortgage andthe requested LC loan, divided by the borrower’s self-reportedmonthly income.

delinq_2yrs The number of 30+ days past-due incidences of delinquency inthe borrower’s credit file for the past 2 years

collections_12_mths_ex_med Number of collections in 12 months excluding medical collectionsinq_last_6mths The number of inquiries by creditors during the past 6 months.mths_since_last_delinq The number of months since the borrower’s last delinquency.mths_since_last_record The number of months since the last public record.mths_since_last_major_derog Months since most recent 90-day or worse ratingpub_rec Number of derogatory public recordstotal_acc The total number of credit lines currently in the borrower’s credit

fileopen_acc The number of open credit lines in the borrower’s credit file.revol_util Revolving line utilization rate, or the amount of credit the bor-

rower is using relative to all available revolving credit.revol_bal Total credit revolving balancepurpose A category provided by the borrower for the loan request.home_ownership The home ownership status provided by the borrower during reg-

istration. Our values are: RENT, OWN, MORTGAGE, OTHER.

Table 3.1: Descriptions of variables [6].

20

effects of the FICO Scores and the LendingClub assigned grades, these two are each have their

own category. The Basic Loan Information category consists of several variables that describe

the loan including its purpose, amount and term. These are asked for or specially assigned by

Lending Club. The Member Information category consists of information about the borrower

that is not on his or her Credit Report and again specifically asked for or calculated by Lending

Club. The Member Credit Information, on the other hand, consists of variables that are included

in a standard credit report and combine to create the FICO Score. In Table 3.2, we summarize

the variables in each category along with their correlations with default status.

Several of the variables in Table 3.2 are boolean variables. We provide additional informa-

tion on these variables in Table 3.3. To better understand the non-boolean variables, we also

provide histograms for these variables in Figures 3.1 through 3.16. For three of the variables,

collections_12_mths_ex_med , mths_since_last_major_derog and mths_since_

last_record, over 95% of the data was 0, so the histogram did not provide much informa-

tional value. As such, we did not include those histograms here. In addition, addr_state,

the numerical encoding of the state of the loan, would not have any informational value in a

histogram, so we did not include a histogram for that variable. To see a geographic visualization

of the LendingClub data, see Appendix A.4.

21

Variable Correlation with Loan Status

Lending Club Information

grade -0.137int_rate -0.156

FICO Scores

fico_range_low 0.054fico_range_high 0.054

Basic Loan Information

purpose_credit_card 0.037purpose_home_improvement 0.008purpose_car 0.002purpose_major_purchase 0.0loan_amnt -0.002purpose_vacation -0.002purpose_renewable_energy -0.005purpose_house -0.008purpose_medical -0.009purpose_educational -0.009purpose_debt_consolidation -0.01purpose_moving -0.01purpose_wedding -0.011purpose_other -0.021term -0.04purpose_small_business -0.043

Member Information

annual_inc 0.04home_ownership_mortgage 0.033emp_length 0.016addr_state 0.01home_ownership_own 0.005home_ownership_none -0.002home_ownership_other -0.007dti -0.02home_ownership_rent -0.036

Member Credit Information

mths_since_last_major_derog 0.024total_acc 0.024revol_bal 0.02pub_rec 0.019open_acc 0.018mths_since_last_delinq 0.011collections_12_mths_ex_med 0.009mths_since_last_record 0.009delinq_2yrs 0.006revol_util -0.045inq_last_6mths -0.069

Table 3.2: Correlation Table: Loan Status of 1 is Fully Paid, Loan Status of 0 is Charged Off(Default). Negative correlation indicates increase in variable increases likelihood of default.

22

Variable Number Percentage Default Rate

Purpose

purpose_credit_card 137,746 0.22 0.05purpose_car 6,438 0.01 0.07purpose_small_business 8,072 0.01 0.17purpose_wedding 2,255 0.0 0.11purpose_debt_consolidation 367,107 0.6 0.07purpose_major_purchase 12,001 0.02 0.07purpose_medical 5,609 0.01 0.09purpose_home_improvement 34,223 0.06 0.06purpose_moving 3,739 0.01 0.1purpose_vacation 3,159 0.01 0.08purpose_house 2,739 0.0 0.1purpose_renewable_energy 418 0.0 0.11purpose_educational 312 0.0 0.17purpose_other 29,032 0.05 0.09

Home Ownership

home_ownership_rent 249,740 0.41 0.08home_ownership_own 54,895 0.09 0.07home_ownership_mortgage 308,033 0.5 0.06home_ownership_none 42 0.0 0.14home_ownership_other 139 0.0 0.19

Table 3.3: Analysis of Boolean Variables.

23

Figure 3.1: Annual Income Figure 3.2: Delinquencies Figure 3.3: DTI

Figure 3.4: EmploymentLength

Figure 3.5: FICO Range(High)

Figure 3.6: FICO Range(Low)

Figure 3.7: Grade Figure 3.8: Credit Inquiries Figure 3.9: Interest Rate

24

Figure 3.10: Revolver Bal-ance

Figure 3.11: Revolver Uti-lization Figure 3.12: Loan Amount

Figure 3.13: Months SinceDelinquency Figure 3.14: Total Account Figure 3.15: Open Account

Figure 3.16: PublicRecords

25

This exploratory analysis provides a number of interesting insights into the dataset. First,

looking at the correlation table, we find that the FICO Scores and the Lending Club assigned

data are correlated the highest with default rate, suggesting that these variables predict default

quite well. Additionally, loans with the 60 month term have higher default rates than those of the

36 month limit (8% versus 6%), and higher loan amounts seem to increase likelihood of default

as well. The FICO Mean is approximately 697, further evidence of the move to a 700 average, as

described by Cunningham [29]. Looking at the boolean variables, very few are highly correlated

with loan default, although we do see that those who take loans for credit cards typically are

more likely to pay off their loan whereas those who take loans for small businesses are less likely

to pay off their loan. With the exception of revol_util and inq_last_6mths, very few

member credit information features have a strong relationship with the default rate.

Interestingly, variables typically thought to be correlated with loan defaults in the broader

consumer market, such as employment length, home ownership and annual income, have weaker

relationships than one might expect. While they are still among the highest correlated variables,

their correlation is not as high as several credit related metrics, such as revol_util and

inq_las_6mths. We will extensively discuss these relationships and many more in Chapter 4.

26

3.2 Variable Sets

As discussed in the introduction, we found in exploratory analysis that many of these variables

have nuanced effects on one another when they are used to classify loans. For this reason,

we separated our loans into sensible categories, since a exhaustive combinatoric formulation is

computationally infeasible. To provide an even more nuanced view of the effects of the features

on default, we combine these categories into ten variable sets, each of which provides a different

combination of variable categories that are then used in a classifier to predict default. With these

variable sets, along with the analysis found in Chapter 4, we are able to answer the questions

we initially posed regarding the predictive value of each feature and even isolate the effects of

the FICO Score and LendingClub assigned grade to some degree. Additionally, we are able to

determine the optimal subset for prediction of default and use that subset in the lending strategy

analysis. The variable sets are detailed below.

• SFICO: Includes only the FICO Scores of the borrower.

• SLC : Includes only Lending Club Information

• S1: Includes only Basic Loan Information

• S2: Includes only Basic Member Information

• S3: Includes only Member Credit Information

• S4: Includes Basic Loan Information and Basic Member Information

• S5: Includes Basic Loan Information and Member Credit Information

• S6: Includes Member Credit Information and Basic Member Information

• S7: Includes Basic Loan, Basic Member and Member Credit Information

• S8: Includes Basic Loan, Basic Member and Member Credit Information as well as Lending

Club Information. Corresponds to all variables known at time of investment except for the

FICO Score.

27

Chapter 4

Default Prediction

In this chapter we extensively discuss the default prediction problem. The ultimate goal of this

analysis is twofold: (1) to ascertain the value of each feature, specifically focusing on attempting

to determine the predictive value of the (2) FICO Score and the LendingClub assigned subgrade.

In doing so, we will have determined the optimal subset for prediction of default, which we can

then use to determine default probability, a measure essential to our analysis of lending strategies

in Chapter 5.

Our default prediction methodology is largely based on the classification problem, prevalent

in machine learning. The problem fundamentally reduces to the following: given a datapoint

with several features, how can we best classify this datapoint into one of several possible groups

of datapoints which have the same features? Using existing machine learning techniques, we

investigate the effect of varying the feature subset on the accuracy of loan classification, thereby

providing a relative measure of the predictive value of each feature. As we will show in Section 4.5,

in many cases, these classification methods inherently provide methods to determine the default

probability of a loan, which is fundamentally the probability that the loan is classified in the

”defaulted” group.

In Section 4.1, we discuss the methodology used to determine the predictive value of each

feature as well as the optimal combination of variables for default prediction. Specifically, we

discuss the implementation of a greedy algorithm discussed in Friedman et. al. to assess the

28

predictive value of specific features within specific subsets [34]. The result of this algorithm is

the ranked optimal subset of the best features for predicting defaults within a given variable

set. By applying this algorithm over a variety of variable sets, we can see which variables are

included in the optimal subset (and, as importantly, which variables are excluded), providing an

understanding of the relative predictive values of features in the dataset. While not necessarily

as quantitative as the correlations and model parameters used in previous analyses (see Zaragoza

[44]), the use of variable sets and optimal subsets nuances our understanding of the interplay

between the features, allowing us to note, for example, that in the presence of a certain feature,

other features previously included in an optimal subset are now excluded. The separation into

variable sets additionally allows us to compare the accuracies of various features, noting how

allowing a classifier to access other features in the dataset provides (or fails to provide) additional

predictive value.

In Section 4.2, we provide the theoretical foundation for many of the existing classification

methods used in our analysis. In Section 4.3, we discuss the results of separating the features into

variable sets and using various classification methods to derive predictive value. In Section 4.4,

we focus on the problem of determining the value of the FICO Score as a predictor of credit risk,

essentially attempting to assess the marginal value of the FICO values when added to each of

the variable sets defined in the last chapter. Finally, we conclude the default prediction analysis

by showing how to adjust our prediction to determine a default probability for each loan.

4.1 Methods

In classification, our goal is to find a function f such that

f(X) = Y , (4.1)

whereX is a loan with the features described in Table 3.2 and Y ∈ {Charged Off,Fully Paid} =

{0, 1}. In supervised learning, which we will exclusively use in this analysis, we feed a classifier

a set of training data, which allows optimization of a function f . We then use the optimized

function f to attempt to predict test data, which the classifier has never seen before. The funda-

29

mental idea is that if the classifier has seen a large enough training set, it will be able to correctly

classify items, even if it has never before seen an item with specific features before. Adhering

to standard classification notation, we term X as a loan when referring to it’s features and xi

when referring to an observed value [34]. Y similarly is a loan status and yi is an observed loan

status. Xi refers to feature i in X. Y is a prediction for the status of the loan whereas yi is an

observed prediction. Additionally, we call X the N × f matrix such that N is the number of

loans and f is the number of features. Similarly, y is the N × 1 matrix of loan statuses. Since

we are specifically interested in the predictive value of specific subsets and features, we nuance

our function f such that

f ji (X) = Y , (4.2)

where i is refers to a subset Si (i.e. SLC , SFICO, S1, S2, ..S8) and 1 ≤ j ≤ l(Si) refers to the

best j features in terms of prediction where l(Si) is the number of features in a given subset.

In other words, S1LC refers to the best feature in SLC . We will use a number of classification

techniques outlined in Section 4.2 as well as the greedy algorithm defined in this section to find

the function f ji that maximizes the accuracy a(f ji ) which is essentially the percentage of correct

predictions yi = yi.

4.1.1 Balancing the Dataset

The robust dataset overall provided an excellent base with which to run the tests outlined above.

However, an important feature of the dataset is it’s skewed nature. As shown in Table A.3, 89%

of the loans are fully paid whereas only 11% are charged off using the full dataset as described

in Section 4.5. If we remove all loans except for those that are fully paid or charged off, we only

improve to 82% fully paid and 18% charged off. Thus, if we run the classifiers on this skewed

dataset, our classifiers simply always classify loans as fully paid because it maximizes accuracy,

thereby nullifying any valuable information about feature importance. Maria Carolina Monard

explains this problem in ”Learning with Skewed Class Distributions”. She notes that a skewed

dataset of this nature may result in ”the learning system [having] difficultires to learn the concept

related to the minority class [39]”.

30

She notes three major ways to solve this issue: assigning misclassification costs, under-

sampling and over-sampling [39]. Of these, under-sampling makes the most sense for our dataset.

Monard describes under-sampling as ”articially balancing the class distributions by eliminating

examples of the majority class [39]”. For our dataset, this translates to limiting the number of

Fully Paid loans to be equal to the number of Charged Off Loans so the dataset used for classi-

fication consists of 50% Fully Paid Loans and 50% Charged Off Loans (we remove all Current,

Late, and Defaulted Loans from the dataset). A classifier that always classified the loans as fully

paid would thus only be 50% accurate instead of 82% accurate.

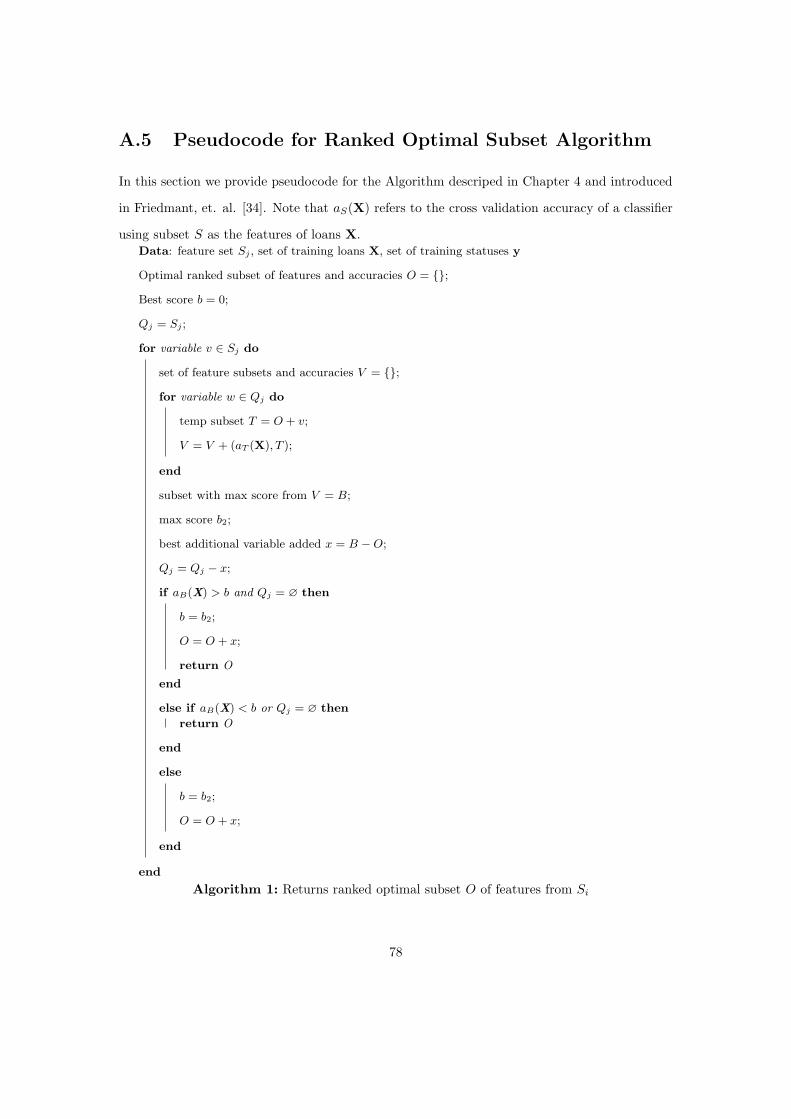

4.1.2 Ranked Optimal Subset Algorithm

We initially split this new balanced dataset into a training set and a test set, with the training

set consisting of 75% of the loans and the test set consisting of the remaining 25%, ensuring

that both the training and the test sets also were balanced in terms of charged off and fully paid

loans. We then proceeded to the most important part of our methods for default prediction, an

algorithm that determines the ranked optimal variables within a set Sj . The algorithm proceeds

as follows: for a given variable set Sj , we calculate the accuracy of a prediction using each vari-

able. We select the best performing variable and store it. We then iterate through the variables

again and select the variable that provides the highest marginal addition to the accuracy of the

learning technique and add that variable to our optimal subset. We continue this until we cannot

improve the accuracy of the classifier or until all variables are exhausted. We then have our opti-

mal subset which we use to predict the test values, leading to a test accuracy which we compare

with the other classifiers. The variables in this optimal subset provide predictive value in deter-

mining default status, with variables ranked higher providing more marginal value (the variable

ranked first is necessarily the most predictive variable in the subset). Variables not included in

this optimal subset were deemed to provide insufficient predictive value to substantially effect

accuracy. We show the pseudocode for this in Appendix A.5.

The accuracy is calculated as the percentage of correct predictions in the test set. Addition-

ally, to determine the optimal subset we use 5-fold cross validation on the training set. Five-fold

cross validation essentially splits the training set into 5 sections. For each of the sections (”folds”),

31

cross validation ”pretends” that the selected fold is the test set and uses the remaining four folds

as the training set. It tests the classifier created by the training set on the test set to return an

accuracy. In the case of the loan status predictions, we use stratified cross validation to ensure

than the percentage of defaulted loans in each fold is similar to that of the full training set. Since

this cross validation strategy also provides the standard deviation of the accuracy, we only select

variables in the algorithm if their marginal contribution to the accuracy exceeds the standard

deviation of cross validation. We run this algorithm for each of the seven different statistical

learning techniques for each of the ten different variable sets, also calculating coefficients of the

model when appropriate. With the variation in feature subset, we can determine the effects of

each feature and additionally show how the presence of some features affects the inclusion or

exclusion of other features from the optimal subset.

We will discuss the runtime of each classifier in Section 4.2. For now, let’s call O(c) the runtime

of a given classifier. Since we iterate through all f variables potentially f times throughout the

algorithm, we have to run the classifier a potential f2 times. Additionally, for each time, we

also run cross validation with d folds (in our case 5), making the total time complexity of our

algorithm O(f2dc).

4.2 Overview of Classification Methods

In this section, we provide the theoretical foundations for the classifiers used. All of the clas-

sifiers are quite standard and have been thoroughly researched in a number of settings, so we

simply provide basic information about these models. In Section 4.3, we only show results for

four of the classifiers, the K-Nearest Neighbors, Decision Tree, Linear Regression and Logistic

Regression classifiers. We do so because we found those to be the most accurate and intuitive.

The description and results for the remaining three classifiers, the Perceptron Algorithm, the

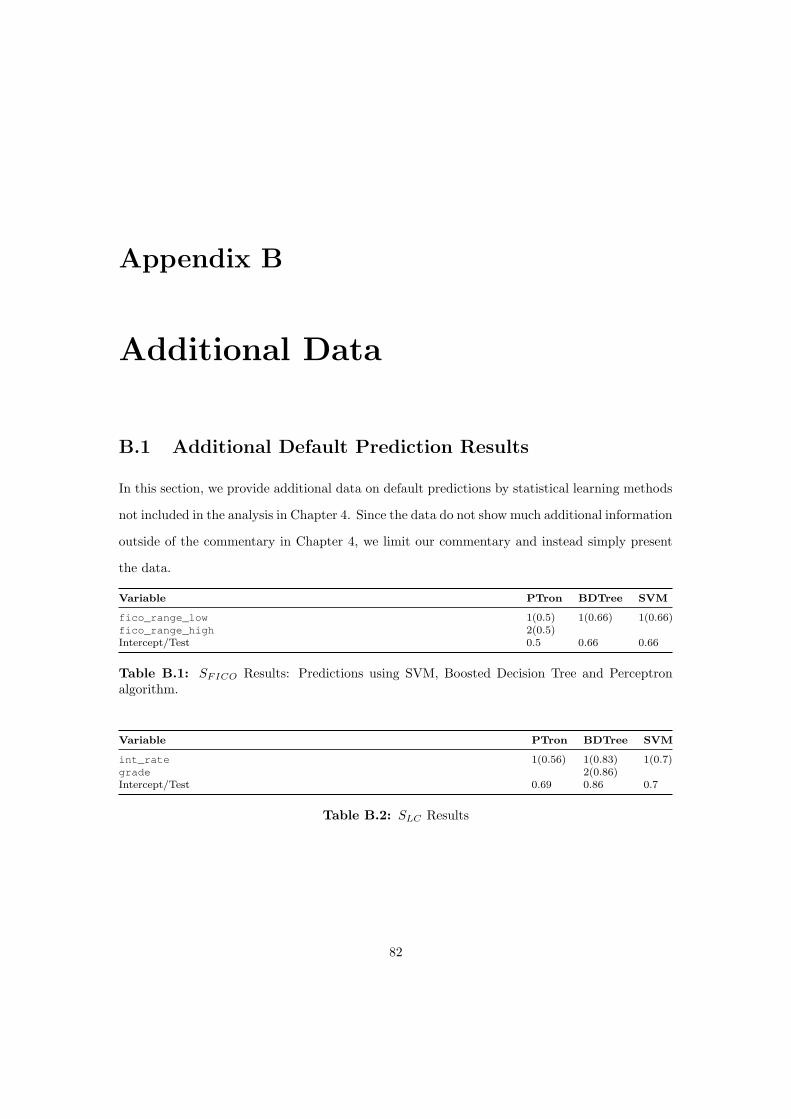

Support Vector Machine and the Boosted Decision Tree can be found in Appendix A.6 and B.1.

These methods are more or less derivates of the aforementioned classifiers and ended up provided

essentially no additional value or information.

As shown in Equation 4.1, a classifier attempts to solve the problem

32

f(X) = Y

.

Assuming square error loss, this function can be rewritten for a particular input x as

f(xi) = E(Y |X = xi). (4.3)

In other words, the best prediction of Y at any point X = xi is the conditional mean [34].

The various standard classification techniques described in this section attempt to implement

this idea in very different ways1.

4.2.1 K-Nearest Neighbors

k-Nearest neighbors, the first type of learning technique we discuss often is one of the best

performing prediction techniques in real-world datasets [34]. However, the drawback of using

this technique is that the use of this model provides very little structural information about

the dataset. This illustrates one of the tradeoffs present in learning techniques, that between

structure and accuracy. In techniques such as linear regression, we assign a very strict set of

constraints on the form the model can take to understand more about the roles the features play

in classification or regression. Though this provides much insight into the datasets structure, the

accuracy of these learning techniques may suffer as a result. A k-Nearest-Neighbor classifier is

the opposite. It is memory based and requires no model to be fit. For this reason, many term

techniques of this sort ”black-box” techniques [34].

The nearest neighbors technique takes the form [34]

f(xi) =1

k

∑xj∈Ck(xi)

yj . (4.4)

In other words, we find the k closest values to xi in the input space and average their values.

Ck(xi) is the set of the k closest loans to xi. In the case of classification we simply use majority

vote to determine y. The ”closeness” is determined by Euclidean distance. Thus, the nearest-

1The information in the next sections largely comes from Friedman, et. al. We have cited whenever appropriate.

33

neighbors methods directly implement Equation 4.2. We are conditioning on a region nearby

the point whose y-value we are attempting to predict and averaging over the y-values of these

nearby points [34]. We used a nearest neighbors with k = 70 after running some optimization

on this value.

While a number of simplifications exist such as the KD-Tree and Ball Tree, the runtime

complexity of the original and brute force algorithm is O(fn2), where f is the number of features

and n is the number of points in the dataset [19]. The implementation used in our analysis

has improvements over this runtime, but for our purposes this suffices. Despite these runtime

improvements, we found that in practice, the KNN algorithm was prohibitively time complex.

To rectify this, we used a technique known as bagging. Bagging takes i random subsets of the

training data and trains a different classifier on each one, and then aggregates the individuals

predictions by averaging to output a final prediction [34]. The effect of this is a reduction in

variance (sensitivity) at the expense of bias (training dataset error), but based on initial results,

we found that using the the bagging classifier provides essentially no change in the accuracy of

the classifiers. In fact, using a larger training set provides hardly any marginal accuracy after

n ≈ 10, 000. Bagging improves the actual, but not asymptotic, runtime of the classifier.

4.2.2 Decision Tree

The binary decision tree is, in many ways, an extension of the nearest neighbors classifier. In

essence, a binary tree works by recursively splitting the feature space into regions based on a

value of a given feature f . Analyzing every possible region split is computationally infeasible, so

a decision tree classifier uses a greedy algorithm that optimizes these splits in the decision tree.

The algorithm, especially when restricted to binary splits, as is typically done, is quite elegant.

Essentially, the algorithm works to find a variable j and a value s that collectively define a

split of the feature space into two sections, R1 and R2 such that [34]

R1(j, s) = {X|Xj ≤ s} and R2(j, s) = {X|Xj > s} (4.5)

The goal of the decision tree, then, is to minimize the squared error loss in both regions. In

other words, [34]

34

minj,s

[minc2

∑xi∈R1(j,s)

(yi − c1)2 + minc2

∑xi∈R2(j,s)

(yi − c2)2], (4.6)

where the minimization on c1 and c2 can be solved by [34]

ci = ave(yi|xi ∈ Ri(j, s)). (4.7)

We continue to grow the tree by repeatedly solving this optimization problem recursively on

all splits. We can see how the average over a specified region resembles the intuition behind

the KNN classifier quite closely. The optimization problem solved, however, often improves the

accuracy of the decision tree beyond that of the KNN classifer. The runtime of a decision tree

classifier is O(fn log n) [16].

4.2.3 Linear Regression

Linear models are probably the most famously and commonly used statistical techniques. Linear

models attempt to assign a structure to the function f(X), [34]

f(X) = Y = β0 +

f∑j=1

Xj βj , (4.8)

where β0 is the intercept (also known as the bias) and f is the number of features of X.

In matrix form, we can augment X with a constant term to account for β0 to simplify the

equation to [34]

y = XT β, (4.9)

where β = (β0, β1, ...βf ) We need to pick β to optimize the accuracy of the regressor. As we

did with the k-Nearest Neighbors classifier, we assign the regressor a loss function and then seek

to minimize that loss. In the case of linear regression, the most common method, and the one

we will use, is least squares in which we pick β to minimize the residual sum of squares, [34]

RSS(β) =

N∑i=1

(yi − f(xi))2 = (y −Xβ)T (y−Xβ), (4.10)

35

where y is the matrix of outputs in the training set and X is the matrix of inputs. Taking a

derivative and solving for the minimum, we find that [34]

β = (XTX)−1XTy. (4.11)

Thus, [34]

f(X) = y = XT β. (4.12)

In using linear regression for classification (as we do in predicting loan defaults), another step

must be taken, because while the classes have value yi ∈ {0, 1}, the linear regression has no such

bound, f(xi) ∈ R. To account for this, we create a function that maps the outputs of the linear

regression to our classes.

To do so, we define a boundary 0 ≤ b ≤ 1 and a classification function

f(y, b)

1, if y ≥ b

0, if y < b

(4.13)

In our case, b = 0.5, the midpoint of the range of classes {0, 1}.

The runtime of linear regression is O(f2n) when n > f [18].

4.2.4 Logistic Regression

Logistic regression is a relative of the linear model used for modeling the probabilities that a given

X is in each class Y ∈ {0, 1}. The logistic regression model ensures that these probabilities sum

to one and are ∈ [0, 1] [34]. These probabilities are modeled by linear functions of the inputs, X.

The coefficients of the logistic regression model can be usefully interpreted as log-odds, meaning

that ei − 1, where i is a coefficient, represents the percent change in the probability for a unit

change in the variable [34].

While the logistic model can be quite complex, in the case of a binary outcome, the model

simplifies significantly. This variant of the model is the most relevant to our problem and is also

used quite frequently in a variety of applications.

36

The model has the following structure: [34]

logPr(Y = 0|X = xi)

Pr(Y = 1|X = xi)= βTxi, (4.14)

where β includes an intercept term β0 and xi includes a constant to account for this intercept.

It can be shown, furhermore, that [34]

Pr(Y = 0|X = xi) =eβ

T xi

1 + eβT xi, (4.15)

and that [34]

Pr(Y = 1|X = xi) =1

1 + eβT xi, (4.16)

satisfying our constraint that the conditional probabilities sum to 1.

We estimate β with the maximum likelihood estimation using a Newton-Raphson procedure.

Explaining this procedure in depth is unnecessary, for more information please see Friedman et.

al. [34]. The logistic regression, similar to linear regression, has runtime O(nf2) [38].

4.3 Results

In this section we discuss the results of our default prediction analysis, starting with some overall

results and then diving into the outputs of the greedy algorithm for each variable set with each

classifier.

4.3.1 Overall Results

We first show an overview of the results of our analyses. Table 4.1 shows the accuracies of the 5

different statistical learning techniques using the 10 different variable sets. Again, accuracies in

each case refer to the percentage of test loans in the balanced dataset that the classifier correctly

assigned a default status.

Though this table does not detail the variables used, it nonetheless provides a wealth of

information by which to understand the data and we can answer many of our initial questions

37

Variable KNN LR Logit DTree PTron BDTree SVM Mean

SFICO 0.66 0.66 0.66 0.66 0.5 0.66 0.66 0.64SLC 0.76 0.76 0.77 0.86 0.69 0.86 0.7 0.77S1 0.61 0.6 0.59 0.64 0.5 0.64 0.64 0.6S2 0.62 0.61 0.61 0.58 0.5 0.58 0.61 0.59S3 0.64 0.64 0.65 0.6 0.5 0.61 0.64 0.61S4 0.63 0.64 0.64 0.64 0.59 0.64 0.64 0.63S5 0.63 0.67 0.67 0.67 0.5 0.67 0.67 0.64S6 0.66 0.66 0.66 0.6 0.5 0.6 0.66 0.62S7 0.63 0.68 0.67 0.67 0.5 0.67 0.67 0.64S8 0.78 0.79 0.77 0.86 0.65 0.86 0.71 0.77Mean 0.66 0.67 0.67 0.68 0.54 0.68 0.66

Table 4.1: Overview of Default Prediction Analysis: Scores refer to test accuracy of best subsetof each prediction method.

through this table alone. First, we find that the accuracy of SFICO is at best 0.66, regardless

of prediction method, which is not remarkable. This accuracy lends credence to the idea that

perhaps the value of the FICO Score in determining loan defaults is overstated.

One of our initial goals was to determine the value of SFICO and in this aim we have succeeded.

S1 and S2, which refer to Basic Loan Information and Basic Member Information, respectively,

have a mean accuracy of 0.61 across the classifiers. In effect, this shows that knowing a borrower’s

FICO Score only provides an 5% advantage over only knowing the purpose, loan amount and

term for a loan, again providing evidence that the value of the FICO Score might be limited.

When we combine two or more of the Baisc Loan, Member and Member Credit Information

categories, such as in S5, S6 and S7, we essentially create a classifier with the same predictive

ability as SFICO. This supports the conclusion that by using relatively naive classification

methods, we can recreate the informational value of the FICO Score using its various parts.

This idea will be further developed in Section 4.4.

The data also provides information as to the value of LendingClub’s propietary algorithm.

We can see that using only the Lending Club data, SLC , we reach an accuracy of 0.86. When

all the other variables are added to SLC (variable set S8), we still do not surpass this 0.86

benchmark, an idea we will touch upon shortly. With the entire unbalanced dataset as described

in Section 4.5, we find a default rate of 11%, indicating that the accuracy of their algorithm is

probably somewhere around the 90% range. An 86% accuracy using relatively naive classifiers

on a balanced dataset seems reasonable, given this information.

38

Finally, we see that all the prediction methods seem to approximately have the same accu-

racies across the variable sets, with the decision tree classifier being slightly more accurate than

the other methods and the Perceptron algorithm much less accurate than the others, probably

because our dataset overlaps considerably between the two classes. Boosting the decision tree

does not seem to increase accuracy either.

In the next section, we dive into the differences between the variable sets and the classification

techniques, focusing the analysis on k-Nearest Neighbors, Linear Regression, Logistic Regression

and Decision Tree for the reasons mentioned above.

4.3.2 Variable Set Results

In this section we discuss the results of the algorithm on the various subsets with each classifiers.

Please note that the caption to Table 4.2 contains information that is constant through the rest

of the tables in the section. In other words, each table has an identical format. For the results

for the other machine learning methods, please see Appendix B.1.

SLC and SFICO Results

We first discuss the variables with which we compare the rest of our variable sets, the Lending

Club assigned subgrade and corresponding interest rate (SLC), and the FICO Scores of the

borrower (SFICO). Table 4.2 and Table 4.3 show the results of the algorithm when run upon

these two variable sets.

Variable KNN LR Logit DTree Coef Odds

fico_range_low 1(0.66) 1(0.65) 1(0.65) 1(0.66) 0.01 0.02Intercept/Test 0.66 0.66 0.66 0.66 -3.22 -1.0

Table 4.2: SFICO Results: Predictions using nearest neighbors, linear and logistic regressionand decision tree classifiers. Coef refers to coefficients of Linear Regression. Odds refer toexponential of Logistic regression coefficients.

We see that the other variable in the FICO Scores (fico_range_high) did not provide

additional predictive value over 0.66. The odds of the FICO Score logistic regression implied

that an increase by a single point of fico_range_low decreases the likelihood of default by 2%.

For SLC we see that both int_rate and grade were used by the algorithm in the optimal subset

39

Variable KNN LR Logit DTree Coef Odds

int_rate 1(0.76) 1(0.71) 1(0.7) 1(0.83) -17.64 -1.0grade 2(0.78) 2(0.76) 2(0.78) 2(0.86) 0.08 0.24Intercept/Test 0.76 0.76 0.77 0.86 1.88 128.36

Table 4.3: SLC Results

and that the decision tree, with its ability to recursively split into regions, was significantly more

accurate than the other methods. Using LendingClub assigned subgrades provided significantly

more accurate predictions of default status than using the borrower’s FICO Score, indicating that

LendingClub’s methods and use of additional social data provide significant predictive value, in

an initial confirmation of the perceived flaws in the FICO methodology.

S1 Results

We then discuss variable set S1, which contains Basic Loan Information, or information about

the loan’s amount, term and purpose.

Variable KNN LR Logit DTree Coef Odds

loan_amnt 1(0.61) 1(0.59) 1(0.63) -0.0purpose_car 2(0.59) 2.46purpose_debt_consolidation 2(0.6) -0.1term 2(0.62) 1(0.59) 2(0.64) -0.04Intercept/Test 0.61 0.6 0.59 0.64 0.71 3.94

Table 4.4: S1 Results

Analyzing S1 provides some of the first instances of variance among the statistical learning

techniques. Despite this, each classifier trained using feature set S1, resulted in very similar

accuracies, ranging from 0.59 − 0.64. We again find that the decision tree is the most accurate

classifier, while the logistic regression is the least accurate.

Three out of the four classifiers choose to use loan_amnt and term in their optimal subset.

The Logit classifiers additionally uses purpose_car and the coefficient indicates that a loan

being used to pay off a car increases its probability of full repayment by over 240%. Despite

this, the use of purpose_car in the Logit classifier resulted in a increase in accuracy of < 1%,

largely because the incidence of these loans is ≈ 1%.

40

S2 Results

S2, which included home ownership data, income/debt information and the state in which the

borrower resides yielded an accuracy quite similar to that of S1, ≈ 60%. In predicting loan

default, only emp_length and dti were used, with the majority of variables in the dataset

deemed insignificant in terms of default prediction.

Variable KNN LR Logit DTree Coef Odds

emp_length 2(0.62) 2(0.62) 2(0.62) -0.01 -0.05dti 1(0.61) 1(0.61) 1(0.61) 1(0.57) -0.02 -0.08Intercept/Test 0.62 0.61 0.61 0.58 0.86 3.76

Table 4.5: S2 Results

Interestingly, as shown by the Logistic and Linear Regression coefficients in Table 4.5, increas-

ing emp_length seems to increase chances of loan default. However, this perceived relationship

in the balanced dataset must be taken with a grain of salt, as employment length is positively

correlated with likelihood of repayment in the full dataset, as seen in Table 3.2. Interestingly, the

borrower’s absolute income, annual_inc, was noticeably absent from the optimal subsets. In

traditional financial intermediaries, and in many online P2P marketplaces, income is considered

an important feature of determining loan quality. This analysis seems to suggest that the relative

income with respect to debt is more important than the absolute level of income, a hypothesis

that we will fully analyze in Chapter 5.

S3 Results

S3 includes credit features most commonly used in determining the FICO Score. As such,

the accuracy of these features was comparable to that of SFICO,≈ 0.64. We again see some

variabilitly in the features used by the various classifiers. All four classifiers, however, use

revol_util and mths_since_last_major_derog in their optimal subset. Three of the

classifiers additionally used open_acc. In S3, we also see the ability of the logistic regression to

find variables with nonlinear effects on the output, in this case whether or not the loan defaulted.

The logistic regression uses the largest optimal subset in this analysis, consisting of 6 different

variables. From the logistic and linear regression coefficients in Table 4.6, we see that with

41

the exception of total_acc, all of the variables have negative effects on loan status, that is,

increasing the value of these variables increases the likelihood of default.

Variable KNN LR Logit DTree Coef Odds

inq_last_6mths 6(0.65) -0.14mths_since_last_major_derog 2(0.62) 2(0.61) 2(0.62) 2(0.6) -0.01 -0.04pub_rec 4(0.64) 3(0.6) -0.4total_acc 4(0.64) 5(0.65) 0.0 0.02open_acc 3(0.64) 3(0.63) 3(0.64) -0.02 -0.1revol_util 1(0.6) 1(0.59) 1(0.59) 1(0.58) -0.41 -0.85Intercept/Test 0.64 0.64 0.65 0.6 0.89 5.94

Table 4.6: S3 Results

S4 Results

S4 which included the variables in S1 and S2, in other words, basic information about the loan

and the borrower, had an accuracy similar to that of S3, ≈ 0.64. We begin to see that a ceiling

of ≈ 0.65 has developed with the data. So far, regardless of variables used, we cannot predict

with a much higher accuracy than that, unless we additionally know LendingClub’s analysis of

the loan. S4 helps to solidify and expand some of our inferences from S1 and S2: loan_amnt,

dti and term remain significant variables with some classifiers assessing loan_amnt as the

most important and others assessing dti as the most important.

Variable KNN LR Logit DTree Coef Odds

loan_amnt 1(0.61) 2(0.64) 2(0.64) 1(0.63) -0.0 -0.0purpose_debt_consolidation 3(0.64) -0.14term 3(0.65) 2(0.64) -0.01emp_length 4(0.65) -0.03dti 2(0.64) 1(0.61) 1(0.61) -0.02 -0.07Intercept/Test 0.63 0.64 0.64 0.64 1.1 6.18

Table 4.7: S4 Results

S5 and S6 Results

S5 has the largest range of variables used by any variable set, with the four classifiers using

a total of eight variables combined in their results. Again we see that despite the significant

42

variance in optimal subsets, the classifiers do not show much variance in their overall accuracies,

with three of the four predicting 67% of the loan statuses correctly.

Variable KNN LR Logit DTree Coef Odds

loan_amnt 1(0.61) 2(0.61) 1(0.63) -0.0term 4(0.64) 3(0.64) 3(0.67) -0.04mths_since_last_major_derog 3(0.63) 3(0.64) 2(0.62) 2(0.66) -0.01 -0.05pub_rec 6(0.66) -0.41total_acc 5(0.66) 5(0.66) 0.01 0.03open_acc 4(0.65) 4(0.65) -0.02 -0.1revol_util 2(0.62) 1(0.59) 1(0.59) -0.42 -0.83revol_bal 6(0.67) 0.0Intercept/Test 0.63 0.67 0.67 0.67 0.98 24.24

Table 4.8: S5 Results

Much of the information in the previous variable sets is confirmed: revol_util, loan_

amnt, term and mths_since_last_major_derog are considered important by most of the

classifiers.The Logistic Regression, again uses more variables in its analysis, seeming to find

nonlinear relationships with several variables not used by many other classifiers, such as total_

acc and pub_rec. The model coefficients show much of the same information, indicating that

most of the credit variables have negative relationships with loan status.

Variable KNN LR Logit DTree Coef Odds

mths_since_last_record 4(0.66)mths_since_last_major_derog 2(0.64) 2(0.64) 2(0.64) 2(0.6) -0.01 -0.04pub_rec 4(0.66) 4(0.66) 3(0.6) -0.1 -0.41revol_util 3(0.66) 3(0.65) 3(0.66) 1(0.58) -0.28 -0.72dti 1(0.61) 1(0.61) 1(0.61) -0.02 -0.07Intercept/Test 0.66 0.66 0.66 0.6 0.93 6.33

Table 4.9: S6 Results

S6 provides an output which is essentially identical to S5, even though S6 does not contain