bharti - mtn final

TRANSCRIPT

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 1/55

Bharti Airtel ± MTN DealPresented By:

Debajyoti MishraKuldeep Thareja

Pallavi JainSarika Beri

Sonam Khattar

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 2/55

Terming the Bharti Airtel-MTN combine as an ³ emerging market telecom powerhouse´, Sunil Bharti Mittal,Chairman and MD of Bharti Airtel in the media statement (³Media Statement´) issued on May 25, 2009, said,

³Both companies would stand to gain significant benefitsfrom sharing each other¶s best practices in addition tosavings emanating from enhanced scale. We see realpower in the combination and we will work hard tounleash it for all our shareholders. This opportunity also

represents a first of its kind in developing an Indian- African initiative that would serve as a shining example of South-South cooperation.´

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 3/55

Parties InvolvedBharti Airtel Limted

India s first private telecom services provider with a footprint in all the 23telecom circles. Widely regarded as India s largest service provider in termsof annual revenues, Bharti Airtel provides mobile & fixed wireless servicesusing GSM technology across all the telecom circles alongwith broadband &telephone services in 94 cities. All these services are provided under the

Airtel brand. Bharti Airtel, as we understand, also has licenses to operatetelecom operations in Sri Lanka and Seychelles.

MTN

Initially known as M-Tel, MTN was incorporated in the year 1994. It is a leadingservice provider of communication services, offering cellular network accessand business solutions. The MTN Group carries on these services throughits several subsidiaries in most African and Middle East countries with anapproximate market share of 30%-40% in each of the countries.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 4/55

Bharti-MTN DealIndia¶s Bharti Airtel Group was to acquire a 49%

stake in the South Africa¶s largest telephonecompany, MTN.

MTN is the dominant operator in several countriesacross Africa while Bharti is largely an Indianoperator.

The acquisition aimed to create an entity stretchingfrom Cape of Good Hope across the Africancontinent, West Asia and the Indian subcontinentreaching out to over 200 million subscribers.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 5/55

Date Events

May 5, 2008 Bharti Airtel announces that it has entered into exploratory discussionswith the MTN Group.

May 6, 2008 Bharti Airtel denies media reports that it has put an offer on the table for acquiring MTN.

May 16, 2008 Both Parties reach an in-principle agreement and a term sheet wasinitiated between the two Parties.

May 21, 2008 The agreed term sheet is presented to the MTN Board of directors.

May 24, 2008 Bharti Airtel withdraws from the talks, following the MTN boardpresenting a completely different structure to Bharti Airtel. Bharti Airtelsees this new proposal as a convoluted way of getting indirect control of the proposed combined entity, which would have made Bharti Airtel asubsidiary of MTN.

May 26, 2008 Reliance Communications (³ RCom ´) enters into exclusive merger discussions with MTN.

July 19, 2008 RCom and MTN formally end talks.

Chronology of Key Events

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 6/55

May 25, 2009 Bharti Airtel makes a media statement announcing that it has entered into talks withMTN for a strategic merger with exclusivity period till July 31, 2009.

June 22, 2009 Securities and Exchange Board of India (³ SEBI ´), through its informal guidance(³Inf ormal Guida nce ´), exempted MTN and its shareholders from making an openoffer for acquiring 36% economic interest in Bharti Airtel through Global DepositoryReceipts (³ GDRs ´).

July 30, 2009 Companies mutually agree to extend the exclusivity period to August 31, 2009.

Mid August 2009 South African Government¶s Treasury proposes dual listing (³ Dual Listi ng ´) of theCompanies in India and South Africa, respectively.

August 30, 2009 Companies mutually agree to extend the exclusivity period to September 30, 2009.September 15, 2009 The Finance Ministry of India rejected the proposal by the South African

Government to allow the immediate Dual Listing; however, there was no formalclarification sought from the concerned authorities in India for the Dual Listing.

September 22, 2009 SEBI decided in its board meeting to amend the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 1997 (³ Tak e ov e r Cod e ´) to include provision

on trigger of open offer obligations on acquisition of ADRs and GDRs with votingrights.

September 24, 2009 Delegation of the South African Government met the Indian regulators to seekclarity on the Proposed Transaction and possibility of Dual Listing.

September 30, 2009 The Proposed Transaction called off for the second time in two years on the expiryof the exclusivity period.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 7/55

The First Call� In May 2008, Bharti Airtel had proposed to acquire

a majority share in MTN of approximately 40%.

� For the same, an in-principle agreement wasreached on May 16, 2008 between the twocompanies and a term sheet was executed.

� It was reported that on May 21, 2009, MTN, in itsboard meeting, considered the term sheet andinstead proposed an alternate structure whereMTN was to acquire majority of shares held byBharti family and SingTel in Bharti Airtel.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 8/55

� The above structure was not acceptable to Bharti Airtel.

� In its statement to media, Bharti Airtel stated that the structureproposed by MTN would have compromised the interest of minority shareholders of Bharti Airtel and

� also would not capture the synergies of a combined entity ascontemplated by Bharti Airtel.

� Bharti Airtel also mentioned that Bharti s vision of transforming itself from a home-grown Indian company to atrue Indian multinational telecom giant, symbolising the prideof India, would have been severely compromised and this wascompletely unacceptable to Bharti Airtel.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 9/55

� Independent directors of MTN were concerned with the IndianForeign Direct Investment (³ F DI´) r e stri c tio n s, wh ich ma n dat ep rior a pp roval f rom the Gov e r n m en t o f In dia.

� They also expressed their displeasure on the amount of debt thatproposed combined entity would be burdened with.

� Mr. Cyril Ramaphosa, Chairman of MTN, did not give his approval tothe merger which resulted in the board rejecting the proposal.

� As there was a speculation that Mr. Ramaphosa might succeedPresident Thabo Mbeki whose tenure ended in September 2008, hewas agreeable to the change in ownership of MTN, but for politicalreasons wanted the company to exist.

� MTN¶s financial advisors approached another Indian telecomcompany, RCom, which had also expressed its interest in havingdiscussions for possible synergies with MTN.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 10/55

Why was the second call made?� After the talks between MTN and Bharti Airtel had fallen through,

there have been few significant changes which tilted the balance infavour of Bharti Airtel.

� In 2008, the talks were not viewed as being on an even plane for MTN had more subscribers as compared to Bharti Airtel.

� However now with both companies having a 100 million strongsubscriber base each, the negotiations switched to other considerations like ± per-subscriber cost of acquisition,

± tilting the scales in favour of Bharti Airtel.

� The financial impact of the global financial tsunami has probablybeen instrumental for MTN and Bharti Airtel to reconsider the idea of merger on mutually acceptable terms.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 11/55

Rationale for resuming talks� For Bharti :� It will get a strategic access to emerging South African market with

higher ARPU.� For MTN :� The proposed Transaction would give access to MTN into hitherto

untapped Asian sub-continental markets without having the need tocreate any ancillary infrastructure. The fact that the combine wouldbe one of the largest telecom service providers in the world would,we believe help MTN to leverage its position in the global market

giving it more commercial visibility.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 12/55

A comparative Analysis

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 13/55

Bh arti Airt e l-M TN c ombi ne as c om p ar e d to ot he r te lc os

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 14/55

Deal Sweetener

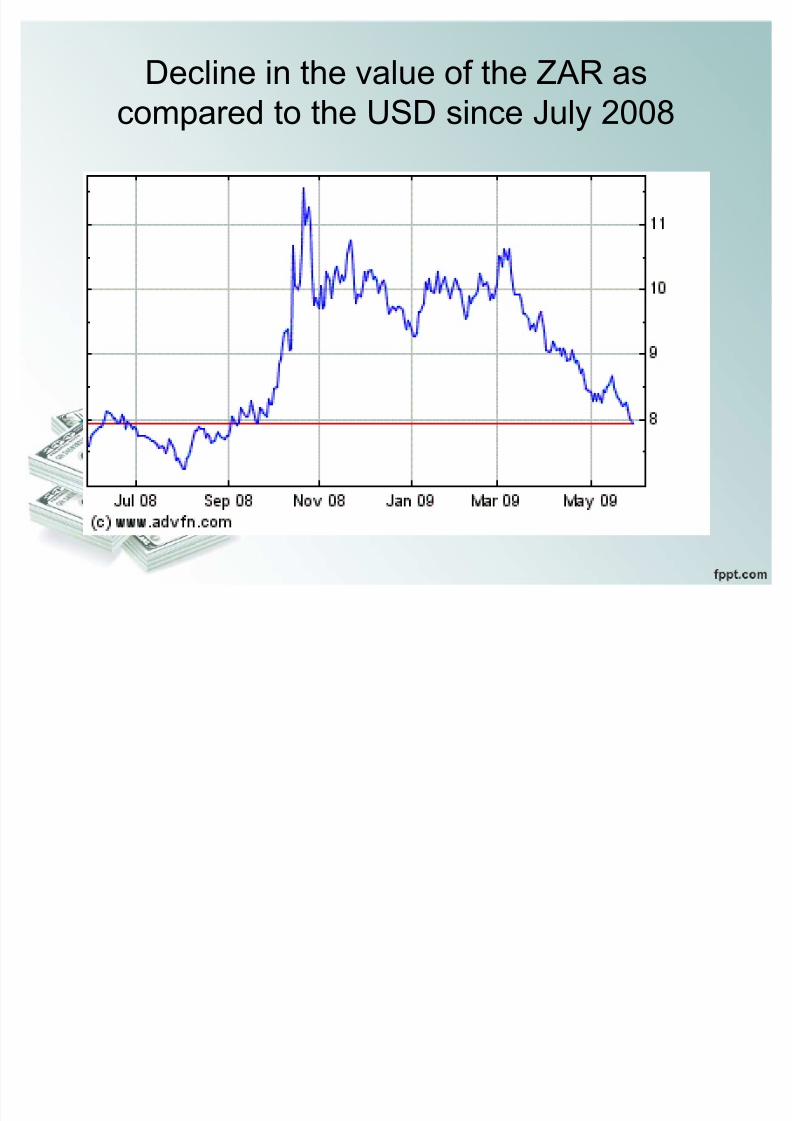

� What sweetens the deal in favour of Bharti Airtel is thefact that the South African ZAR fell far more against thedollar last year than the Indian rupee.

� Rupee fell by 22% where as ZAR fell by 80%.� lower value of the ZAR would have a reducing effect onthe valuation of the deal.

� Point of concern for Bharti Airtel is the fact that the ZARhas rallied more than 2 percent, touching an 8-monthhigh of 8.066 to the USD, partly on optimism over theproposed deal, which in the future may lead to arenegotiation of the existing valuation.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 15/55

Decline in the value of the ZAR ascompared to the USD since July 2008

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 16/55

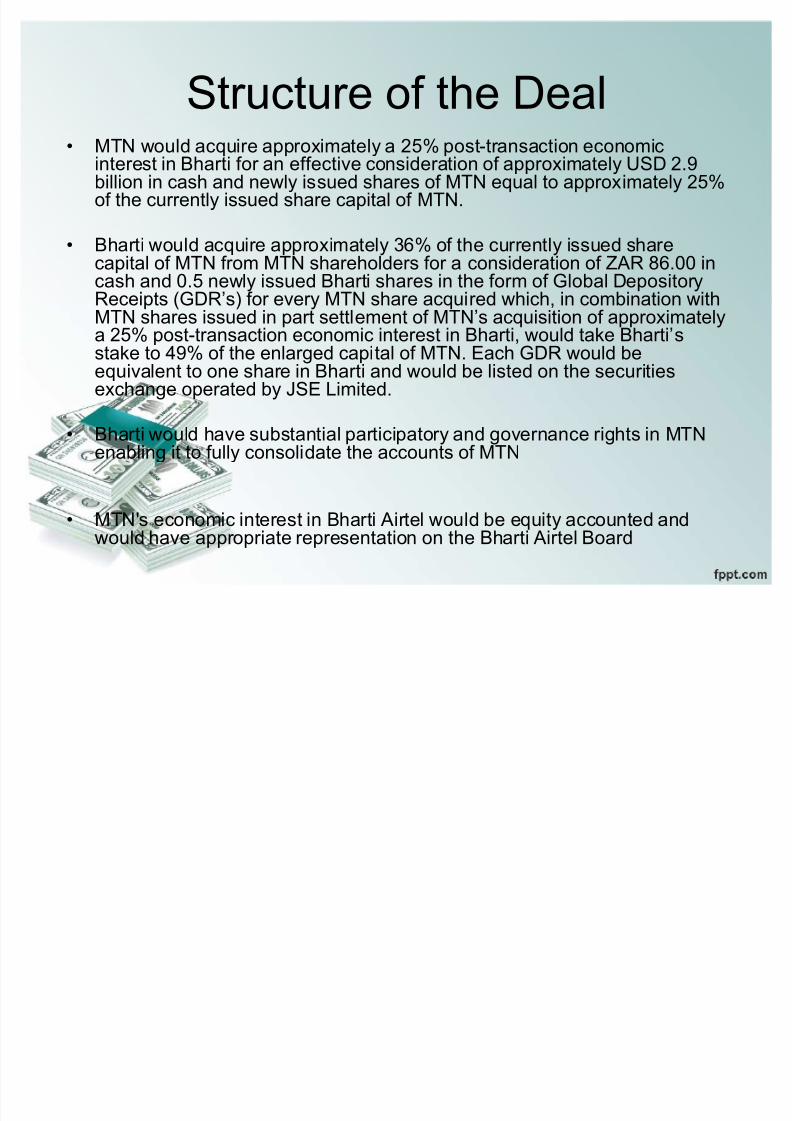

Structure of the Deal� MTN would acquire approximately a 25% post-transaction economic

interest in Bharti for an effective consideration of approximately USD 2.9billion in cash and newly issued shares of MTN equal to approximately 25%of the currently issued share capital of MTN.

� Bharti would acquire approximately 36% of the currently issued sharecapital of MTN from MTN shareholders for a consideration of ZAR 86.00 incash and 0.5 newly issued Bharti shares in the form of Global DepositoryReceipts (GDR¶s) for every MTN share acquired which, in combination withMTN shares issued in part settlement of MTN¶s acquisition of approximatelya 25% post-transaction economic interest in Bharti, would take Bharti¶sstake to 49% of the enlarged capital of MTN. Each GDR would beequivalent to one share in Bharti and would be listed on the securitiesexchange operated by JSE Limited.

� Bharti would have substantial participatory and governance rights in MTNenabling it to fully consolidate the accounts of MTN

� MTN's economic interest in Bharti Airtel would be equity accounted andwould have appropriate representation on the Bharti Airtel Board

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 17/55

T ransaction Leg 1:� MTN gets 25% economic interest in Bharti Airtel� Bharti Airtel gets USD 2.9 billion + acquires 25% stake in MTN

(effectively around 20% on enlarged capital base post issuance of shares to Bharti Airtel)

T ransaction Leg II:� Bharti Airtel acquires 36% of the existing shares from the MTN

shareholders (effectively around 29% on enlarged capital base post

issuance of shares to Bharti Airtel)� MTN shareholders get ZAR 86 + 0.5 GDR per MTN share

Summarily, Bharti Airtel will effectively acquire 49% interest in MTN for USD 24.1 billion, of which USD 20 billion will be offset by

share/GDR swap resulting in a net cash outflow of USD 4.1 billionfrom Bharti Airtel to MTN.

Since Bharti Airtel will have substantial participatory and governancerights in MTN enabling it to fully consolidate the accounts of MTN,MTN is likely to become a subsidiary of Bharti Airtel.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 18/55

Tricks and Traps of Strategic

Merger � Merger of Bharti MTN is likely to walk the tight rope of foreign direct investment (³FDI´) regulations, which,though eased by the introduction of Press Note 2 of 2009, still requires foreign shareholding in Bharti Airtel tobe below 74%

� Foreign investment in Bharti Airtel, is likely to be craftedin a manner that also leaves enough headroom for further foreign investment in Bharti Airtel

� If the Transaction goes through, Bharti Airtel will acquire49% shareholding in MTN (through a combination of share transfer and fresh issuance), MTN shareholderswill acquire 11% GDRs with Bharti Airtel s underlyingshares and 25% ³economic interest´ in Bharti Airtel .

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 19/55

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 20/55

Major Cause of Failure of the

DealThe treasury of South Africa insisted that for thedeal to go through, the potential merged companyshould remain domiciled in South Africa andshould be listed in both countries, something thatwas not a possibility under existing Indian laws.

The motive behind the demand seems to be thatthe South African Government wanted to ensureliquidity and market for MTN and its shareholders.The structure as demanded would have enabledMTN shareholders to transact on both the Indianand the South African bourses.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 21/55

E conomic Nationalism:� The Government of South Africa gave precedence to economic

nationalism over the corporate benefits of the multibillion dollar

Proposed Transaction.

� It was of utmost importance for the Government of South Africa toensure that MTN maintained its identity as the leading South Africantelecom company

� MTN is viewed locally as a national champion, having launched in1994 as South Africa emerged from apartheid with the election of Nelson Mandela.

� It also is the last South African-owned telecom company after theU.K.'s Vodafone Group PLC bought control of Vodacom Group

Limited, the second largest mobile company in South Africa.� The South African Government handled the deal with abundant

caution and objected to losing the leading mobile company in thecountry after losing the second largest company already.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 22/55

Discontent amongst the Shareholders of MTN:

� The shareholders of MTN objected to the valuation by Bharti, initiallyamounting to USD 13 billion, broken down into USD 7 billion in cashand USD 6 billion in stocks.

� The shareholders were very vocal in their demand for enhancing thecash component of the deal and expressed their discontent in beingdumped with the GDRs of Bharti Airtel.

� Bharti Airtel proposed a last minute µsweetenerµ to appease theshareholders on MTN. Bharti increased the cash component of itsoffer for a 49% stake in MTN to USD 10 billion from a proposedUSD 7 billion with USD 4 billion in stock for a total increasedpackage of USD 14 billion

� When the shareholders themselves were not too happy with thedeal, the South African Government had no reason to approve theTransaction and witness the country losing its leading telecomcompany to a foreign owner

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 23/55

F luctuation in South African Rand:

� Appreciation of µrand¶ against dollar by around 6% during thependency of the Proposed Transaction had increased thecash component that Bharti Airtel had to pay to MTNshareholders.

� Bharti Airtel had decided to make cash payment of 86 ZAR for every MTN share. The total dollar outgo at that time came toaround USD 6.94 billion. With the ZAR appreciating againstthe dollar, this total amount shot by around USD 413 million toaround USD 7.38 billion

� Bharti Airtel was supposed to get USD 2.9 billion in cash from

MTN but due to the rupee depreciation against the dollar theamount went up by USD 72 million.

� This increase would have been over and above thesweeteners which Bharti Airtel had to offer to MTNshareholders for the deal to go through.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 24/55

Political ConsiderationsSouth African Perspective:

� South African government was adamant about keeping theidentity of MTN, while just a year ago it allowed the VodacomGroup Limited, a mobile venture that had been owned equallyby South Africa¶s Telkom SA Ltd. and Vodafone Group PLC tobe fully acquired by the UK company

� Congress of South African Trade Unions (COSATU) hadprotested against the deal between MTN and Bharti throughSouth African communication regulator, IndependentCommunications Authority of South Africa (ICASA)

� South African government justified this move by saying thatthey have become all the more watchful after the Vodacomdeal and since they have already lost one of their major players they do not want more companies to lose their Africanidentity

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 25/55

The F acts:

Unlike Vodacom, MTN is closer to the Governmentbecause the largest shareholder of MTN is the PublicInvestment Corporation (³PIC´) which is South AfricanGovernment¶s pension fund manager.

PIC has around 21% stake in MTN and has to be a keyreason for the protectionist attitude of the South AfricanGovernment towards Bharti Airtel ± MTN deal unlike theVodafone Vodacom deal.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 26/55

What South African Authorities Suggested

To get the deal through, the South Africanauthorities suggest proposed Bharti ±MTN should go for Dual listing in both thecountries as South Africa already has duallisting business structure in their country.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 27/55

Dual Listing Company A dual-list e d c om p a ny or DLC is a corporate structure in which

� two corporations function as a single operating business through a legaleq ualizatio n a g r ee m en t ,� but retain separate legal identities and stock exchange listings.

In a conventional merger or acquisition, the merging companies become a single legalentity, with one business buying (for cash or stock) the outstanding shares of theother.

However, when a DLC is created, the two companies continue to exist, and to haveseparate bodies of shareholders, but they agree to share all the risks and rewards of the ownership of all their operating businesses in a fixed proportion, laid out in acontract called an "equalization agreement.³

The equalization agreements are set up to ensure equal treatment of both companies¶shareholders in voting and cash flow rights. The contracts cover issues thatdetermine the distribution of these legal and economic rights between the twinparents, including issues related to dividends, liquidation, and corporate governance.

Usually the two companies will share a single board of directors and have an integrated

management structure. A DLC is somewhat like a joint venture, but the two partiesshare everything they own, not just a single project

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 28/55

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 29/55

Merits and Demerits of DLCMe rits

� First step to merger

� Tax Benefits

� Retaining Identities of Companies

� Operational Issues

� Perception of Better Access toCapital Markets

� Concerns over Flow Back

De m e rits

� Complexity of Operations

� Regulatory Issues

� Liquidity, Transparency andShareholder Value Issues

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 30/55

LEG AL AND R EGUL ATO RY

C ONSI DER ATIONS

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 31/55

SOUTH AFRICAN LAW IMPLICATIONS

South African Securities Regulation Code onTakeovers and Mergers (³Code´)Under the provisions of the South African Securities

Regulation Code on Takeovers and Mergers (³ SA T ak e ov e r Cod e´) , a ny a cq uir e r (³Acq uir e r ́ ) a cq uiri ng mor e th a n35% o f s ec uriti e s o f a S out h Af ri c a n Com p a ny (³T ar ge t´)is f urt he r obli g at e d to mak e a n o pen o ffe r to a cq uir e all the r e mai n ing s ec uriti e s o f the T ar ge t f rom the ex isti ngs h ar eh old e rs o f the T ar ge t

Since Bharti Airtel will be acquiring 49% stake in MTN, Bharti Airtel may be obligated to make an open offer for acquisitionof all the remaining shares of MTN

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 32/55

� Under the provisions of the SA Companies Act ³Scheme´drawn between the Target and its shareholders, is required to

be approved by a majority of three-fourths of its shareholdersin value

� Once the Scheme has been approved by the Court, itbecomes unconditional and will be applicable to thedissenting minority shareholders too

� Making an offer to public may be mandatory under the SATakeover Code unless:Bharti Airtel procures a dispensation from Securities RegulationPanel

Enters into an agreement with existing shareholders agreeing towaive the requirement to make mandatory open offer The Scheme is sanctioned by 75% shareholders. Since theacquisition is proposed to be by way of court approved scheme, therole play of minority shareholders will be fairly limited

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 33/55

I ndependent Communications Authority of South Africa Apart from the need to make a mandatory open offer asdiscussed above, approval of the IndependentCommunications Authority of South Africa (³ IC ASA´)was be required

O ther I ssuesOther Laws applicable to Bharti Airtel and MTN :The Securities Services Act, 2004 entailing provisions pertaining toinsider trading and market manipulation

The Competition Act, 1998, regulating mergers and combination of entities As securities of MTN are listed on JSE, the companies would berequired to meet with the Listing Requirements of the JohannesburgStock Exchange Limited

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 34/55

THE INDIAN LAW IMPLICATIONS

F DI RegimePress Note 5 of 2005 (³Press Note 5´), Press Note 3 of

2007 (³Press Note 3´) and Press Note 2 of 2009 (³PressNote 2 of 2009´) provide for the regulatory framework for FDI in telecom sector and are instrumental to ascertainthe trend and degree of regulation that the Governmentof India intended and intends to administer on FDIattendant downstream investments in the telecom sector

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 35/55

P ress N ote 5 � Initially FDI in telecom sector was capped at 49%. Government of

India, with a commitment to liberalize the FDI regime, decided toenhance the FDI ceiling from 49% to 74% in certain telecomservices which included such as Basic, Cellular, Unified AccessServices, National/ International Long Distance, V-Sat, PublicMobile Radio Trunked Services (PMRTS), Global Mobile PersonalCommunications Services (GMPCS) and other value addedservices subject to certain conditions, which amongst other included,prior approval of FIPB for enhancing FDI from 49% up to 74%

� As regards computation of FDI, Press Note 5 provided that 74% FDIlimit shall apply to FDI infused into the telecom services companyboth µdirectly¶ or µindirectly¶

� Press Note 5 clarified that in the instances of indirect holding in theoperating company, the extent of FDI would be calculated on a

proportionate basis

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 36/55

P ress N ote 3

� The Press Note 3 was an extension of the earlier PressNote 5, and clarified that the extant Indian shareholdingin telecom companies cannot be less than 26%

� Both Press Note 5 and Press Note 3 provide for certainsecurity conditions that have to be considered whileapproving FDI proposals in the Telecom sector

� The Bharti-MTN proposed deal subject to a morestringent scrutiny by FIPB

� Calculation of indirect foreign investment was stillsupposed to be on proportionate basis

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 37/55

D ecoding P ress N ote 2 Press Note 2 of 2009 clarifies the manner and mechanism

for calculating indirect foreign investments in Indiancompanies

� If an Indian investing company, which is ³ owned´ or ³controlled´ by ³non-resident entities´, then the entireinvestment by the investing company into the subject

downstream Indian investee company would be consideredas indirect foreign investment� In the case of ³indirect foreign holding´ of an Indian company

in a restricted sector (³Target´) which is held through another Indian company (³Investing Company´), the indirect foreignholding will counted as foreign holding in the Target only if:the foreign ownership in the Investing Company is more than 50%

of the equity capital of the Investing Company, or the right to appoint the majority of directors to the board of the

Investing Company rests with foreign parties

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 38/55

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 39/55

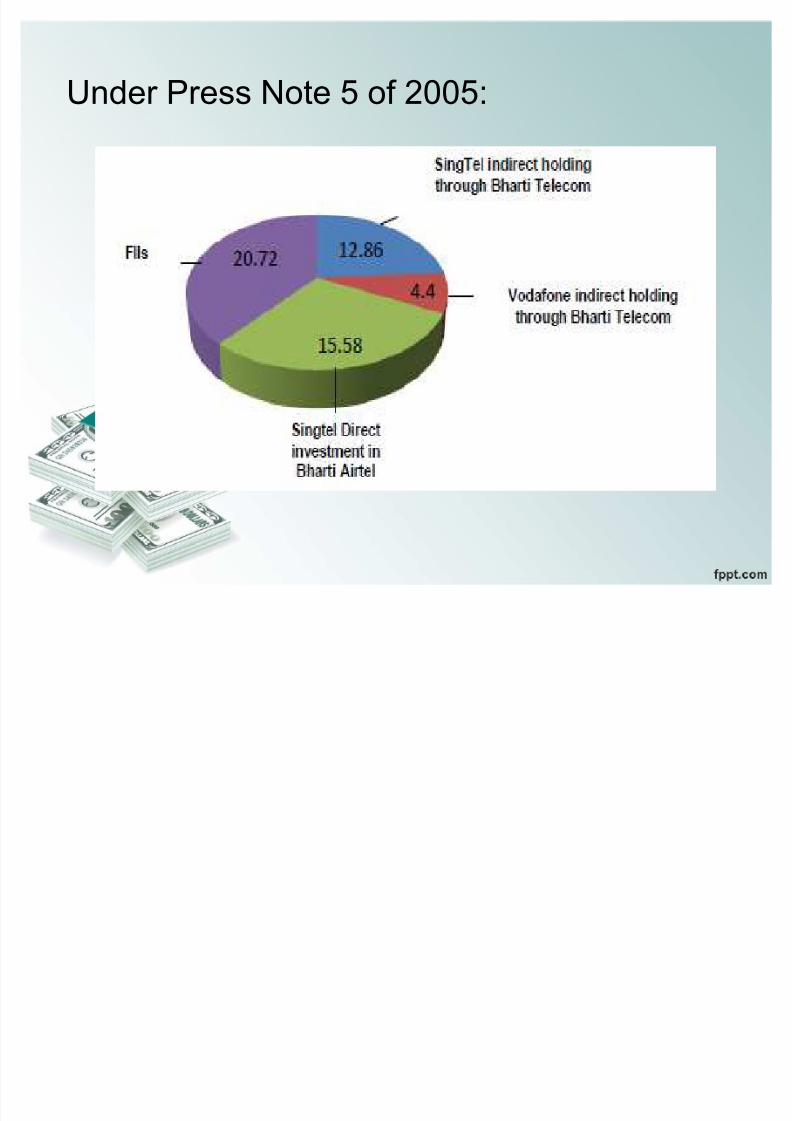

Under Press Note 5 of 2005:

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 40/55

� Until the issue of Press Note 2 of 2009, foreign investment in Bharti Airtel was calculated to include Singtel and Vodafone¶s shareholding

in Bharti Telecom translating to 12.86% and 4.4% effective interestin Bharti Airtel, respectively

� However, in line with the manner of calculation of foreign investmentin downstream companies as stipulated in Press Note 2 of 2009

total foreign investment in Bharti Airtel shall not take intoconsideration any foreign investments at the holding company level,unless the holding company is owned or controlled by non residents

� So, in the above instance, if Press Note 2 of 2009 is followed

thereby excluding indirect foreign shareholding of foreign investorsin Bharti Telecom including SingTel and Vodafone, there should beenough headroom to accommodate further foreign investment inBharti Airtel

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 41/55

Shareholding patterns of both Bharti Airtel and its parent,Bharti Telecom in 2009

Sh ar eh oldi ng in Bh arti Airt e l: Sh ar eh oldi ng in Bh arti Te lec om

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 42/55

Role of Different Indian

Regulator � SEBI� Cabinet Committee on Economic Affairs

(³CC EA¶)� Foreign Investment Promotion Board (³ F IP B´) /

Department of Telecom (³ DOT´)� RBI

� Ministry of Corporate affairs

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 43/55

Role of SEBI

� Applicability of takeover code

� One of the most important questions being debated over

is whether or not will MTN have to make the mandatoryopen offer for acquisition of 25% economic interest inBharti Airtel. Under regulation 10 of the SEBI(Substantial Acquisition and Takeovers) Regulations,1997 (³ Tak e ov e r Cod e´) , a ny pe rso n a cq uiri ng 15%s h ar e s or voti ng ri gh ts in a list e d c om p a ny is obli g at e d to mak e a n o pen o ffe r f or the a cq uisitio n o f 20% additio n al s h ar e s.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 44/55

Role of Sebi (Contt..)� The role of SEBI in the entire scheme of events is of great interest

and has left many wondering about its stand on the deal. On June18, 2009, Bharti Airtel sought clarification from SEBI under the SEBI(Informal Guidance) Scheme, 2003 on whether the acquisition of 36% economic interest in Bharti Airtel by MTN through GDRs wouldtrigger the open offer requirement under Regulation 10 of theTakeover Code.

� SEBI delivered Informal guidance on June 22, 2009 and clarifiedthat such acquisition would only trigger the disclosure requirementsunder Chapter II of the Takeover Code and not the open offer obligation.

� It was also clarified by SEBI that the open offer obligation under Regulation 10 of the Takeover Code would be triggered onconversion of the GDRs into underlying equity.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 45/55

Role of Sebi (Contt..)� Mr. Deepak Mehra, a shareholder of Bharti Airtel appealed to Securities

Appellate Tribunal (³SAT´) against the Informal Guidance of SEBI onwhy open offer should not get triggered upon issuance of GDRs butSAT dismissed the same on August 28, 2009 and upheld the decisionof SEBI.

� On September 22, 2009, SEBI decided in its board meeting to amendthe provisions of the Takeover Code in relation to the exemptiongranted to ADRs and GDRs.

� Prior to the amendment under regulation 3(2) of the Takeover Code,acquisition of ADRs / GDRs were exempted from open offer requirement under Chapter III of the Takeover Code till the time of its

conversion into underlying equity shares.� Under the proposed new provision, such exemption from open offer would be available only till the time the ADR / GDR holders remain aspassive investors without any kind of voting arrangement with theoverseas depository on the underlying equity shares.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 46/55

Role of Sebi (Contt..)� The amendment ignited a twofold issue for the deal which had the

potential to derail the Proposed Transaction.� The amendment obligated MTN and / or its shareholders to make an

open offer for acquisition of additional 20% shares from the public

shareholders of Bharti Airtel under Regulation 10 of the Takeover Code on acquisition of Bharti Airtel GDRs if such GDRs entitled itsholders to exercise voting rights on underlying shares.

� The open offer would have cost the South African company another USD 6.78 billion which posed a serious threat to the commercialviability of the deal.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 47/55

Role of Sebi (Contt..)� The second and far more critical issue was the possibility of MTN

crossing the permitted FDI sectoral cap of 74% under the currentFDI policy.

� The FDI policy permits only 49% FDI in an Indian telecom company

under the automatic route which may be further raised up to amaximum of 74% subject to the prior approval of Foreign InvestmentPromotion Board.

� Sing Tel, Singapore already holds a stake (28%) in Bharti Airtel andunder the Proposed Transaction, if MTN acquired 36% economicinterest in Bharti Airtel and on top of it if MTN had to acquire 20%shares in the open offer then it could have breached the FDIsectoral caps.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 48/55

Role of other RegulatorsCabi ne t Committ ee o n Ec o n omi c Aff airs (µCC EA´)

� As per Press Note 7 of 1999 issued by the Department of IndustrialPolicy and Promotion (³DIPP´), any investment proposal in excess of Rs. 6,000 million (approx USD 128 million) requires the prior

approval from the CCEA.� In the proposed transaction, it is estimated that total investment(cash + shares/GDRs) by MTN would be (approx) USD 24.1 billion,thereby necessitating a prior approval from the CCEA.

� The CCEA had provided their approval in principal for the deal.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 49/55

Role of other regulators(Contt«)

F or e ign In ve stm en t P romotio n B oard (³ F IP B´) / Dep artm en t o f Te lec om (³ DOT´)

� In the proposed Transaction, it is likely that there would be anelement of swapping of shares/GDR wherein Bharti Airtel would

issue fresh shares in favour of MTN as consideration for the issue of shares by MTN in favour of Bharti Airtel.� Any FDI in the Telecom sector beyond 49% requires the prior

approval of FIPB and FIPB in turn could refer the matter to DOT.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 50/55

Role of other regulators(Contt«)

� Ministry of Corporate Affairs� The demand for a DLC could have caused amendments to the

corporate law and exchange control regime of the country.� To effectively implement the DLC structure, the Companies Act,

1956 would require significant changes to facilitate accountingdisclosures, prospectus disclosures, financial formats, commonboard and common shareholder meetings as well as defining theimplications of dissolution of one of the DLCs.

� Securities laws would also require changes to the listingrequirements and prospectus disclosures and exchange control

regulations may need to be amended vis-a-vis trading of dual listedstock.� A DLC cannot become a reality in India without incorporating the

above mentioned amendments into our legal system.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 51/55

Role of other regulators(Contt«)

� RBI� The FIPB may refer the matter to RBI since the Transaction will

involve swap of shares which will happen for a consideration other than cash. The RBI approval is likely to come stapled with FIPBapproval.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 52/55

Lack of Capital Account convertibility

� Experts opine that the lack of full CAC in India is the most criticalcause for the failure of the Proposed Transaction.

� The most fundamental amendment for implementing DLC would beto permit full CAC under the Foreign Exchange Management Act,

1999 (³F

EMA´)� CAC refers to the abolition of all limitations and restrictions withrespect to the movement of capital from India to different countriesacross the globe.

� It permits transfer of capital assets from residents to non-residentswithout any obstruction.

� It also allows the people and companies not only to convert rupee tothe other currency, but also free cross-border movement of currencies, without the interventions of the law.

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 53/55

Lack of Capital Account convertibility(Contt..)

� In a bid to attract foreign investment, many developing countrieswent in for CAC in the 1980s not realizing that free mobility of capitalleaves countries open to both sudden and huge inflows as well asoutflows, both of which can be potentially destabilizing.

� Following the East Asian crisis, even the most ardent votaries of CAC in the World Bank and the IMF realized that the dangers of going in for CAC without adequate preparation could becatastrophic.

� Indian regulators including the Reserve Bank of India (³RBI´) do notwant to commit any mistake by rushing into CAC until the Indianeconomy meets the following three conditions:

� Primarily fiscal consolidation� Strengthening of the financial system� Low rate of inflation

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 54/55

Other regulatory concerns� It is assumed that DLC would render the existing Indian FDI policy in

fructuous as Indian authorities would not be able to monitor sectoralcaps on direct and indirect investment that are imposed on 13industry sectors, including telecom sector.

� It is also feared that entities that are ineligible for investing in Indiancompanies could acquire stakes through transactions carried out onthe overseas exchange, in violation of the FEMA.

� DLC has the potential to weaken the SEBI¶s oversight of the stockmarket and it can also lead to trading activity being taken away fromstock exchanges in India resulting in a likely revenue loss for theIndian exchequer

8/7/2019 Bharti - MTN Final

http://slidepdf.com/reader/full/bharti-mtn-final 55/55

Thank you