biia october 2006 - all rights reserved 2006 - business information industry association asia...

TRANSCRIPT

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

1

BIIA

Credit Reporting Systems in Africa

Role of Public Sector Information in Risk

Assessment

6 October 2006

Cape Town, South Africa

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

2

BIIA

Public Sector Information and Risk Assessment

Joachim C. Bartels Managing Director

Business Information Industry Asia Pacific – Middle East

Limited

Hong Kong

Stefano Stoppani Credit Bureau and Risk Management Advisor

Global Financial Markets Development – International

Finance Corporation

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

3

BIIA

Agenda

• Value of Information and Economic Development

• The State of Information – Global Overview

• The Digital Divide in Lending

• How to Bridge the Digital Divide?

• General Discussion

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

4

BIIA

Economic Benefits

Information

Economy• More Stable Financial Sector• Economic Growth with Lesser

Need for a ‘Bail-out’ of Banks• Stabilizes Allocation of Capital

• Accurate Risk Prediction• Can Lend to Broader Risk Segments• Pricing Reflecting Individual Risk

Financial Sector

Businesses

• Objective Assessment• Better Access to Credit• Quicker Reward for

Responsible Credit Behavior

Consumers• More Accurate

Information on Health of Financial Sector

Bank Supervision

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

5

BIIA

Credit and Information

• Strong Positive Linkages between Financial Sector and Economic Growth*

• Strong Linkage between Greater Access to Credit / Higher Bank Borrowings and Existence of Credit Information Companies or Credit Bureaus* * Source: World Bank

** Small and Medium Size Enterprises

• A Well-functioning Financial Sector Provides Individuals, SMEs** and Corporations with Access to Credit*

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

6

BIIA

SMEs and the Problem of Obtaining Credit

• “The Difficulty of Obtaining

Credit is Consistently Rated

by SMEs as one of the

Greatest Barriers to

Operation and Growth”

World Bank 2003 Study on Credit ReportingWorld Bank 2003 Study on Credit ReportingEstimates Based on Data on 5000 Firms in 51 CountriesEstimates Based on Data on 5000 Firms in 51 Countries

49%49%

28%28%

High Financing High Financing ConstraintsConstraints

Probability of Probability of Obtaining a Obtaining a LoanLoan

Source: World BankSource: World Bank

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

7

BIIA

Relevance of Credit Bureaus

49%49%

27%27%

% of Firms Reporting % of Firms Reporting High Financing High Financing ConstraintsConstraints

Without Without With With Credit BureauCredit Bureau

Probability of Obtaining Probability of Obtaining a Bank Loana Bank Loan

28%28%

40%40%

Without Without With With Credit BureauCredit Bureau

Source: World BankSource: World Bank

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

8

BIIA

Impact on Availability of CreditA

vail

abil

ity

of I

nfo

rmat

ion

Penetration of Credit

< 33%< 33% 35 - 66%35 - 66% > 66%> 66%

Subjective Credit Granting – High Risk - No Transparency

Subjective Credit Granting – High Risk - No Transparency

High Credit Losses - Little Transparency

High Credit Losses - Little Transparency

Moderate Credit Losses – Accurate Risk Prediction

USAUSA

UKUK

NoneNone

HighHigh

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

9

BIIA

Impact on Availability of CreditA

vail

abil

ity

of I

nfor

mat

ion

Penetration of Personal Credit

< 33%< 33% 35 - 66%35 - 66% > 66%> 66%

No Information No Information Sharing Sharing No Credit BureauNo Credit Bureau

No Information No Information Sharing Sharing No Credit BureauNo Credit Bureau

Negative Negative Information Information onlyonly

Positive and Positive and Negative Negative Information Information Sharing with Sharing with Credit BureauCredit Bureau

Source: McKinsey & Company 2002Source: McKinsey & Company 2002

Subjective Credit Granting – High Risk - No Transparency

Subjective Credit Granting – High Risk - No Transparency

High Credit Losses - Lack of Transparency

High Credit Losses - Lack of Transparency

Moderate Credit Losses – Accurate Risk Prediction

•Overall China Credit Penetration app.. 5%Overall China Credit Penetration app.. 5%** Under Development** Under Development

USAUSA

UKUK

ShanghaiShanghai**

JapanJapan TaiwanTaiwan

Singap.*Singap.***

India**India**

KoreaKorea HKHK

China**China**

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

10

BIIA

0

1,000

2,000

3,000

4,000

5,000

6,000

UK Example – Non-Performing Loan Provisions

Pounds Sterling [000]McKinsey Report on State of UK McKinsey Report on State of UK BankingBanking

• Recommending Greater Reliance Recommending Greater Reliance on External Information and on External Information and Credit ScoresCredit Scores

McKinsey Report on State of UK McKinsey Report on State of UK BankingBanking

• Recommending Greater Reliance Recommending Greater Reliance on External Information and on External Information and Credit ScoresCredit Scores

• UK Banks Revamped Credit Systems

• UK Banks Revamped Credit Systems

NPL ProvisionsNPL ProvisionsNPL ProvisionsNPL Provisions

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

11

BIIA

AGENDA

• Linkages: Value of Information and Economic Development

• Overview: State of Information

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

12

BIIA

• The Imperfect World of The Imperfect World of InformationInformation

• Attitudes and Infrastructure Attitudes and Infrastructure Impact Availability & Impact Availability & ReliabilityReliability

State of Information

• Complexity of Risk is Complexity of Risk is Growing Growing

• New Demands on Information New Demands on Information

• Overcoming the Overcoming the Information DeficitInformation Deficit

• Investment in Public / Private Investment in Public / Private Sector InformationSector Information

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

13

BIIA

THE STATE OF INFORMATION

0

10

0 10

Effectiveness of Information in Credit Risk Assessment

Co

un

try

Infr

astr

uct

ure

Co

un

try

Infr

astr

uct

ure

Co

un

try

Infr

astr

uct

ure

Co

un

try

Infr

astr

uct

ure

GovernmentLegalITCreditBusinessHR

State of Registers, Information Exchange Mandated & Voluntary Disclosure

Information AvailabilityInformation Availability

Thailand Pre 1990’s

Finland

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

14

BIIA

Government

LegalInfrastructure

COUNTRY INFRASTRUCTURE CRITERIA

• Communication Quality & Availability

• New IT Meeting Business Needs

• Data Security Enforced

• Communication Quality & Availability

• New IT Meeting Business Needs

• Data Security Enforced

Information

Infrastructure

• TransparencyTransparency• Bribery and Bribery and

CorruptionCorruption• Parallel EconomyParallel Economy

• TransparencyTransparency• Bribery and Bribery and

CorruptionCorruption• Parallel EconomyParallel Economy

• Legal Framework Legal Framework for Commercefor Commerce

• Justice – Dispensed Justice – Dispensed FairlyFairly

• Rights & Rights & Responsibilities of Responsibilities of ShareholdersShareholders

• Legal Framework Legal Framework for Commercefor Commerce

• Justice – Dispensed Justice – Dispensed FairlyFairly

• Rights & Rights & Responsibilities of Responsibilities of ShareholdersShareholders

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

15

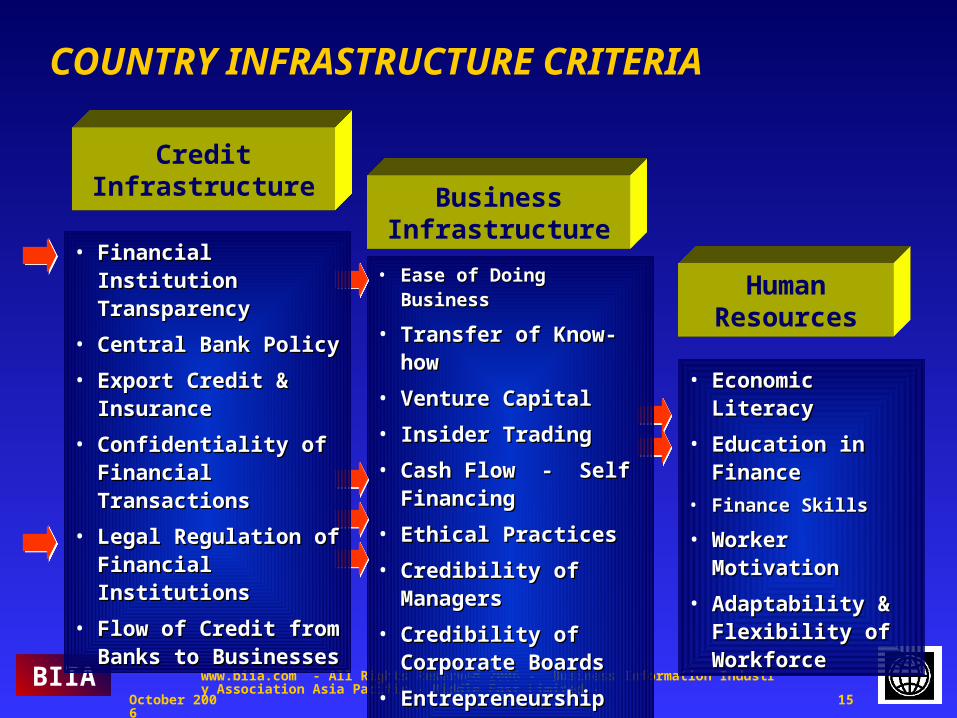

BIIA

CreditInfrastructure

Human Resources

BusinessInfrastructure

COUNTRY INFRASTRUCTURE CRITERIA

• Economic LiteracyEconomic Literacy

• Education in FinanceEducation in Finance

• Finance SkillsFinance Skills

• Worker MotivationWorker Motivation

• Adaptability & Adaptability & Flexibility of Flexibility of WorkforceWorkforce

• Ease of Doing BusinessEase of Doing Business

• Transfer of Know-howTransfer of Know-how

• Venture CapitalVenture Capital

• Insider TradingInsider Trading

• Cash Flow - Self Cash Flow - Self FinancingFinancing

• Ethical PracticesEthical Practices

• Credibility of ManagersCredibility of Managers

• Credibility of Corporate Credibility of Corporate BoardsBoards

• EntrepreneurshipEntrepreneurship

• Adaptability of CompaniesAdaptability of Companies

• Financial Institution Financial Institution TransparencyTransparency

• Central Bank PolicyCentral Bank Policy

• Export Credit & Export Credit & InsuranceInsurance

• Confidentiality of Confidentiality of Financial TransactionsFinancial Transactions

• Legal Regulation of Legal Regulation of Financial InstitutionsFinancial Institutions

• Flow of Credit from Banks Flow of Credit from Banks to Businessesto Businesses

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

16

BIIA

CreditAcceptance of the Concept of Information Pooling

BusinessAttitudes and Compliance

GovernmentAvailability of Information

LegalRequirement to Disclose

INFORMATION AVAILABILITY

• Efficient Credit BureausEfficient Credit Bureaus

• Voluntary DisclosureVoluntary Disclosure

• Attitudes Towards Disclosure Attitudes Towards Disclosure and Transparencyand Transparency

• Reliability / Reliability / Accuracy of Accuracy of DataData

• Disclosure - SECDisclosure - SEC• Disclosure - Filing of FinancialsDisclosure - Filing of Financials

• Availability of Court RecordsAvailability of Court Records• Access to Court RecordsAccess to Court Records

• UCC Filings or EquivalentUCC Filings or Equivalent• State of Public RegistersState of Public Registers• Access to Public RegistersAccess to Public Registers• ComplianceCompliance

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

17

BIIA

0

1

2

3

4

5

6

7

8

9

10

Information Availability

High

High

Low

Low High0 1 2 3 4 5 6 7 8 9 10 0 1 2 3 4 5 6 7 8 9 10

Cou

ntr

y In

fras

tru

ctu

re

Low

High

China

Hong Kong

Indonesia

India

Singapore

Japan

ASIA / PACIFICASIA / PACIFIC

Finland

Australia

Korea

Philippines

Malaysia

New Zealand

Taiwan

Thailand

Low

Trend UpTrend Up

Trend DownTrend Down

No ChangeNo Change

Source: IMD 2003 Source: IMD 2003 & IEI 2003 Surveys& IEI 2003 Surveys

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

18

BIIA

0

1

2

3

4

5

6

7

8

9

10

Information Availability

High

High

Low

Low High

0 1 2 3 4 5 6 7 8 9 10 0 1 2 3 4 5 6 7 8 9 10

Low

Source: IMD 2003 & Source: IMD 2003 & IEI 2003 SurveysIEI 2003 Surveys

Cou

ntr

y In

fras

tru

ctu

re

Low

High

S. AfricaS. Africa

Slovak RSlovak R

PolandPoland

Finland

Czech RCzech R

RomaniaRomania

RussiaRussia

HungaryHungary

TurkeyTurkey

SloveniaSlovenia

Trend UpTrend Up

Trend DownTrend Down

No ChangeNo Change

GermanyGermany

FranceFrance

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

19

BIIA

1

2

3

4

5

6

7

D&

B C

oun

try

Ris

k R

atin

g

Information Availability

Low

Low Risk

High

High Risk

High Risk

Low Risk

Finland

0 1 2 3 4 5 6 7 8 9 10 0 1 2 3 4 5 6 7 8 9 10

High Risk

Pakistan

Azerb

Nepal

Sri Lanka

Bangladesh

Georgia

Kazakhstan

Myanmar

Vietnam

Congo DR

Tanzania

Nigeria

Zimbabwe

Kenya

Angola

Algeria

Peru

Cuba

Paraguay

Source: D&B IRPRSource: D&B IRPR& IEI 2003 Surveys& IEI 2003 Surveys

Bulgaria

Ukraine

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

20

BIIA

5

6

7

8

9

10C

oun

try

Infr

astr

uct

ure

Information Availability

High

High

Low

Low High

Low

High

6 7 8 9 10 6 7 8 9 10

Source: IMD 2004 & IEI 2003 SurveysSource: IMD 2004 & IEI 2003 Surveys

France

Austria

Italy

Finland

Denmark

IrelandNetherlands

Sweden

Belgium

Spain

Portugal

Germany

POTENTIAL ROLE MODELS

Trend UpTrend Up

Trend DownTrend Down

UK

Switzerland

September 2006

FEBIS ANNUAL CONFERENCE 2006 - WWW.BIIA.COM - All Rights Reserved -

21

BIIA

• Market Characteristics

• Introduction to BIIA

• Content Information Market

• World Bank Survey

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

22

BIIA

Agenda

• Value of Information and Economic Development

• The State of Information – Global Overview

• The Digital Divide in Lending

• World Bank Survey on Public Sector / Private Sector Information Relationship

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

23

BIIA

The Digital Divide

• Short term bank and trade credit are the largest sources for short term capital

• The existence of bank & trade credit depends on accurate, reliable and timely information and credit management skills

• In many countries trade credit has not reached its full potential because of the lack of accurate, reliable and timely information caused by underdeveloped and dysfunctional public records infrastructures

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

24

BIIA

The Imperfect World of The Imperfect World of InformationInformation

• Difficult to Access Difficult to Access

• Paper BasedPaper Based

• Poor Quality – Out of DatePoor Quality – Out of Date

• Lax ComplianceLax Compliance

• Underdeveloped Underdeveloped InfrastructuresInfrastructures

• Underdeveloped Underdeveloped InfrastructuresInfrastructures

• Information is Secret!Information is Secret!

• Lack of Voluntary and Legal Lack of Voluntary and Legal DisclosureDisclosure

• No Enforced ComplianceNo Enforced Compliance

• Lack of TransparencyLack of Transparency

• Attitudes of Attitudes of Businesses Businesses

• Attitudes of Attitudes of Businesses Businesses

How to Create Value ?How to Create Value ?

?

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

25

BIIA

Digital Information and Credit Risk Assessment

Public

Sector

Data Sources

PrivateSector CreditInformation

Private

Sector

Credit

Grantors

Private

Sector

Borrowers

Value Creation and Impact on Economic

Development

Value Creation and Impact on Economic

Development

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

26

BIIA

Digital Information and Credit Risk Assessment

Private

Sector

Borrowers

PrivateSector CreditInformation

Private

Sector

Credit

Grantors

Public

Sector Data

Sources

Low Value Creation Impaired Economic

Development

Low Value Creation Impaired Economic

Development

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

27

BIIA

From Data to Knowledge

Public

Sector

Data Sources

PrivateSector CreditInformation

Private

Sector

Credit

Grantors

Private

Sector

Borrowers

RawData

Data Collection

Data Validation

Modeling External Internal

Data Decision

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

28

BIIA

CREDIT INFORMATION CYCLE

Public Sector Information

Public Sector Information

Register & Court DataRegister & Court Data

Private SectorCreditors

Private SectorCreditors

Credit BehaviorCredit

Behavior

Credit Grantors

Credit Grantors

Risk Assessment

Risk Assessment

Credit Information

Credit Information

Private Sector Value AddedInformation

Private Sector Value AddedInformation

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

29

BIIA

PRIMARY USERS

0

25

50

75

100

Banks

Cred

it I n

sure

rs

Trad

e Cr

edit

Retai

l

Cred

it Ca

rd I

Regul

ator

s

Source: World Bank Survey 2006

% o

f R

espo

nden

ts

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

30

BIIA

Public Sector – Private Sector Information Sources

Public Sector Private SectorPrivate SectorBusiness Registers

Court System

News Media

Company News & Information

Trade Directories

Compulsory VoluntaryPrivate Sector Publications

Trade InformationTrade Information

Financial StatementsFinancial Statements

InvestigationInvestigation

Press Clippings

Product Information

RegisterDataRegisterData

Suits, Liens JudgmentsSuits, Liens Judgments

FinancialStatementsFinancialStatements

Database

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

31

BIIA

MOST FREQUENTLY USED DATA SOURCES

0

25

50

75

100

Source: World Bank Survey 2006

% o

f R

espo

nden

ts

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

32

BIIA

DEFICIENCIES IN PUBLIC SECTOR INFORMATION (PSI)

0

25

50

75

100

CorporateRegisters

Court Collateral

Paper Format Electronic Format

Source: World Bank Survey on Business Credit Information and PSI

% o

f R

espo

nden

ts

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

33

BIIA

PSI – QUALITY AND RELATIONSHIP

123456789

10

CorporateRegisters

Court Records CollateralRegisters

Data Quality Relationship

Source: World Bank Survey on Business Credit Information and PSI

1 –

10 R

anki

ng

September 2006

FEBIS ANNUAL CONFERENCE 2006 - WWW.BIIA.COM - All Rights Reserved -

34

BIIA

SUCCESS FACTORS

0%

5%

10%

15%

20%

25%

30%P

ublic

Secto

r

Mandato

ry

Dis

clo

sure

/

Regula

tory

Bank

Secre

cy

Tra

de

Info

rmatio

n

Data

Qualit

y

Attitu

des

tow

ard

s

Custo

mer

Educatio

n

Speed o

f

Serv

ice

Fre

shness

of data

Technolo

gy

Sta

ndard

s

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

35

BIIA

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

36

BIIA

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

37

BIIA

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

38

BIIA

AGENDA

• Linkages: Value of Information and Economic Development

• Overview: State of Information

•How to Bridge the Digital Divide?

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

39

BIIA• Data-Pooling (A) Data-Pooling (A)

- Credit Bureaus -- Credit Bureaus -

Bridging the Digital Divide

• Investments in Modern Investments in Modern Information SystemsInformation Systems

• Electronic Access to Electronic Access to RegistersRegisters

• PartneringPartnering

• Value AddedValue Added

• Change ‘Mind Set’Change ‘Mind Set’ • Broadening DisclosureBroadening Disclosure

• Encourage Voluntary DisclosureEncourage Voluntary Disclosure

• Improvement in Corporate Improvement in Corporate GovernanceGovernance

• Value of TransparencyValue of Transparency

• Value of Information in Credit Value of Information in Credit TransactionsTransactions

• Value of Information PoolingValue of Information Pooling

RegistersRegistersRegistersRegisters CourtsCourtsCourtsCourts

Public SectorPublic SectorPublic SectorPublic Sector Central BanksCentral BanksInternational / NationalInternational / NationalCentral BanksCentral BanksInternational / NationalInternational / National

Credit Credit Grantors Grantors (A)(A)

Credit Credit Grantors Grantors (A)(A)

InformationInformationSuppliers Suppliers (A)(A)

InformationInformationSuppliers Suppliers (A)(A)

Private SectorPrivate SectorPrivate SectorPrivate Sector

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

40

BIIA

The Thai Example

0

10

0 10

FinlandC

ou

ntr

y In

fras

tru

ctu

reC

ou

ntr

y In

fras

tru

ctu

reC

ou

ntr

y In

fras

tru

ctu

reC

ou

ntr

y In

fras

tru

ctu

re

Information AvailabilityInformation Availability

Thailand

Success Factors ?

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

41

BIIA

The Thai Example

Pre 1994Pre 1994

• Paper Based

• No Online Distribution

• Paper Based

• No Online Distribution

Registration DataBalance Sheets

Ministry of Ministry of CommerceCommerceBusiness Business RegistrationRegistration

Public SectorPublic Sector

BankruptciesAuctions

Ministry of Ministry of JusticeJusticeCourt SystemCourt System

• How to Digitize Data?

• How to Provide Online Distribution?

• How to Digitize Data?

• How to Provide Online Distribution?

• Public Sector Initiative?

• Private Sector Involvement?

• Public Sector Initiative?

• Private Sector Involvement?

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

42

BIIA

The Thai Example

Private SectorPrivate Sector

• Information Skills?

• Marketing Skills?

• Add Value?

• IT Skills?

• Proven Track Record?

• Information Skills?

• Marketing Skills?

• Add Value?

• IT Skills?

• Proven Track Record?

Registration DataBalance Sheets

Ministry of Ministry of CommerceCommerceBusiness Business RegistrationRegistration

Public SectorPublic Sector

BankruptciesAuctions

Ministry of Ministry of JusticeJusticeCourt SystemCourt System

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

43

BIIA

The Thai Example

‘Business Online’ Database760,000

Companies7 Years of Financial Statements (Basel II)

• Data• Company Register• Bankruptcy

• Data• Company Register• Bankruptcy

• Information• Company Reports• Payment Information• News Briefs from 20 Sources

• Information• Company Reports• Payment Information• News Briefs from 20 Sources

Private Sector (BOL)Private Sector (BOL)Public SectorPublic Sector

From Data to KnowledgeFrom Data to Knowledge

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

44

BIIA

AGENDA

• Linkages: Value of Information and Economic Development

• Overview: State of Information

• How to Bridge the Digital Divide?

• Role Model: Public Sector / Private Sector Partnership Example

• General Discussion

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

45

BIIA

RECOMMENDATION

• Change ‘Mind Set’Change ‘Mind Set’ • Broadening DisclosureBroadening Disclosure

• Encourage Voluntary DisclosureEncourage Voluntary Disclosure

• Improvement in Corporate Improvement in Corporate GovernanceGovernance

• Value of TransparencyValue of Transparency

• Value of Information in Credit Value of Information in Credit TransactionsTransactions

• Value of Information PoolingValue of Information Pooling

RegistersRegistersRegistersRegisters CourtsCourtsCourtsCourts Credit Credit Grantors Grantors

Credit Credit Grantors Grantors

InformationInformationSuppliers Suppliers

InformationInformationSuppliers Suppliers

Public SectorPublic SectorPublic SectorPublic Sector Central BanksCentral BanksInternational / NationalInternational / NationalCentral BanksCentral BanksInternational / NationalInternational / National

Private SectorPrivate SectorPrivate SectorPrivate Sector

• Investments in Modern Investments in Modern Information SystemsInformation Systems

• Investments in Modern Investments in Modern Information SystemsInformation Systems

• Electronic Access to Electronic Access to RegistersRegisters

• Electronic Access to Electronic Access to RegistersRegisters

• PartneringPartnering• PartneringPartnering

• Value AddedValue Added• Value AddedValue Added

• Data-Pooling Data-Pooling - Credit Information Suppliers - - Credit Information Suppliers -

- Credit Bureaus -- Credit Bureaus -

• Data-Pooling Data-Pooling - Credit Information Suppliers - - Credit Information Suppliers -

- Credit Bureaus -- Credit Bureaus -

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

46

BIIA

Disclosure of Loan Information

0

25

50

75

Nam

e of

Ban

k

Loan

A

Loan

Typ

e

On

Tim

e

Past D

ue

Mat

urity

Colla

tera

l

Credit Information User Group

• Closed User Groups vs. Credit Information

% o

f R

espo

nden

ts

Source: World Bank Survey 2006

October 2006

www.biia.com - All Rights Reserved 2006 - Business Information Industry Association Asia Pacific - Middle East Limited -

47

BIIA

Credit Reporting Systems in Africa

Thank You

The presenter and BIIA are not responsible for the use which might be made of the information contained in this presentation or report. Nothing in this presentation implies or expresses a warranty of any kind.

Presented by Joachim C. BartelsPresented by Joachim C. BartelsManaging Director of Business Information Industry Association Asia Pacific – Middle East [email protected]