bill gloyn - the chartered insurance institute limited is authorised and regulated by the financial...

TRANSCRIPT

Aon Limited is authorised and regulated by the Financial Services Authority in respect of insurance mediation activities only.

Apres moi the deluge A reflection on 45 years in commercial property insurance

Bill GloynChairman, Real Estate Europe

Aon Mergers & Acquisitions Group

Slide 2©2009

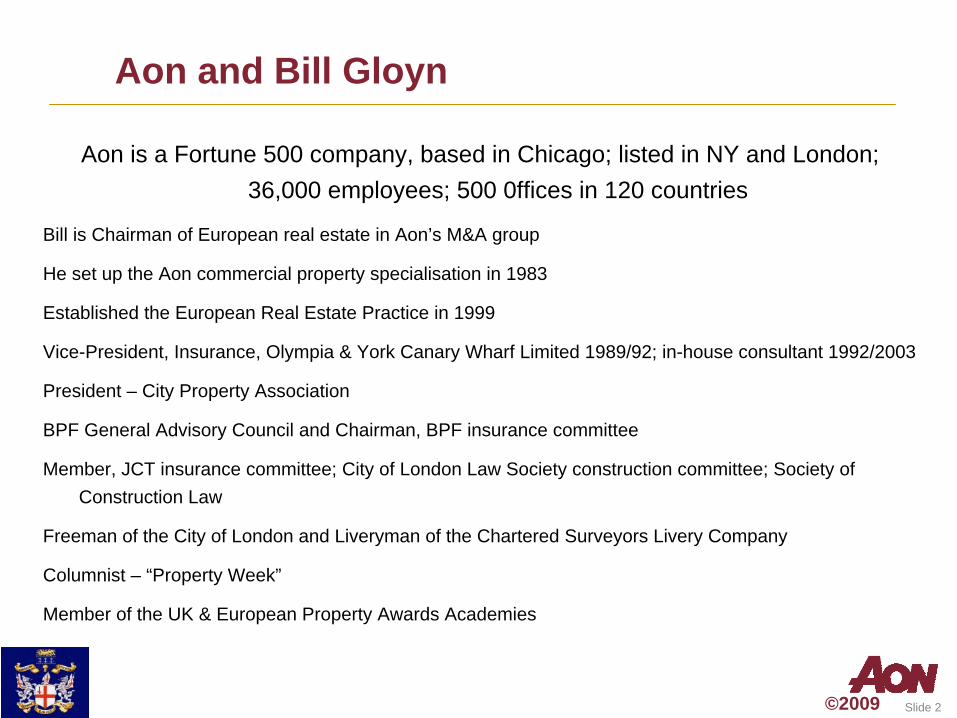

Aon and Bill Gloyn

Aon is a Fortune 500 company, based in Chicago; listed in NY and London; 36,000 employees; 500 0ffices in 120 countries

Bill is Chairman of European real estate in Aon’s M&A group

He set up the Aon commercial property specialisation in 1983

Established the European Real Estate Practice in 1999

Vice-President, Insurance, Olympia & York Canary Wharf Limited 1989/92; in-house consultant 1992/2003

President – City Property Association

BPF General Advisory Council and Chairman, BPF insurance committee

Member, JCT insurance committee; City of London Law Society construction committee; Society of Construction Law

Freeman of the City of London and Liveryman of the Chartered Surveyors Livery Company

Columnist – “Property Week”

Member of the UK & European Property Awards Academies

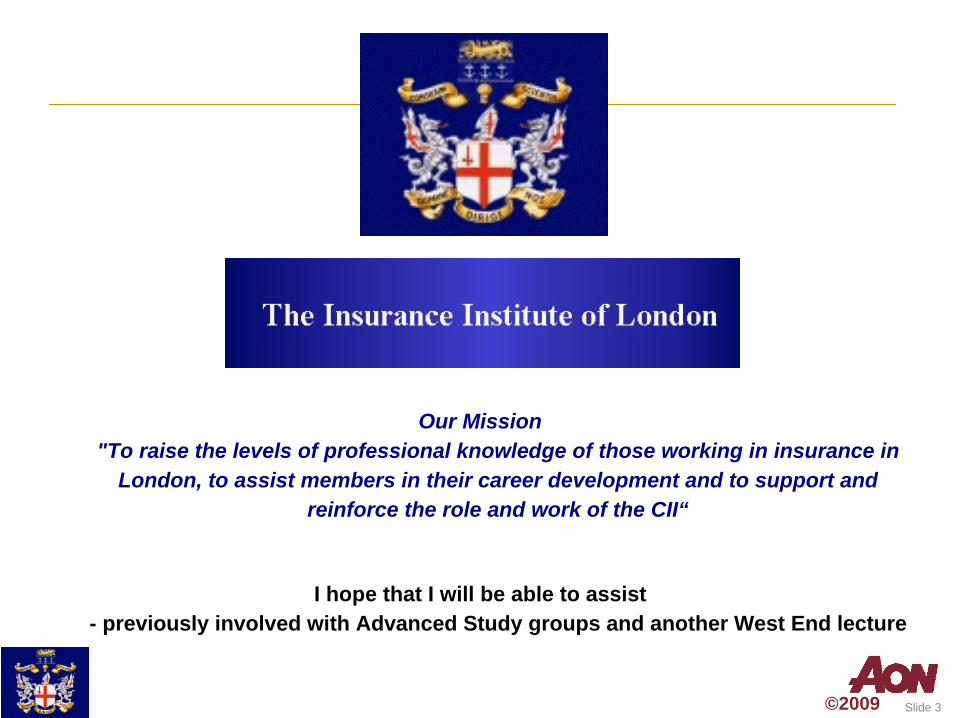

Slide 3©2009

Our Mission "To raise the levels of professional knowledge of those working in insurance in

London, to assist members in their career development and to support and reinforce the role and work of the CII“

I hope that I will be able to assist - previously involved with Advanced Study groups and another West End lecture

Slide 4©2009

Life at the Commercial Union in the early 1960sThey were different days

- Alternate Saturday morning working

- smoking at the desk before 10.00 and after 4.15

- Clerks had a separate lavatory to Principals

- all letters and memos countersigned by at least one superior

- records kept by hand

- policy facsimile books in Kalamazoo binders

- wet photo-copies – I was an early Xerox user (“another string to your bow”)

- standard policy and endorsement wordings

- marking up the Goad maps that recorded where insured risks were located

- running to the R/I dept if capacity exceeded - otherwise a disciplinary offence

Slide 5©2009

Life in the CU- Fire Offices Committee - keeping the tariff rate books up-to-date

- Standard, clearly transparent, rates of commission –– 15 or 17½% plus postages

- Clerks didn’t type!

- No electric typewriters

- Mistakes meant a complete re-type

- No computers or even pocket calculators

Slide 6©2009

And the resultant amounts?

All written by hand on a page of accounting paper!

They never tallied up across and down

Rates were split into fire and separate perils – each with separate loadings

Cons Loss rates were different

We worked in £.s.d – needed decimal conversion tables

Pro-rata calculations required Odd Time Tables

No wonder that insurance was a major employer

Slide 7©2009

My first experience as a broker

Recruited by Rose Thomson Young after 11 months

Working for two MP directors – also involved with property companies

Scratch-boy at Lloyds

Learnt the tricks of the trade – queuing all day for the Head Broker

Went up the tree – got my own ticket

Ended up as an Account Executive – without the title!

Slide 8©2009

Life as an Insurance Manager – first time round

Offered role as Insurance Manager for a client in 1969

English Property Corporation – major listed company – became 28% owned by Eagle Star after the early 1970’s property crash

De-listed following acquisition by Olympia & York

Established Albany Insurance Management – 3rd party business

Became Registered Insurance Broker following new legislation in 1977

First involvement with British Property Federation – an outsider!

O&Y decided that there was no future in UK/European development

Planned to wind down the company and sell the rump

Offered opportunity to stay, go to a managing agent or seek my fortune

Slide 9©2009

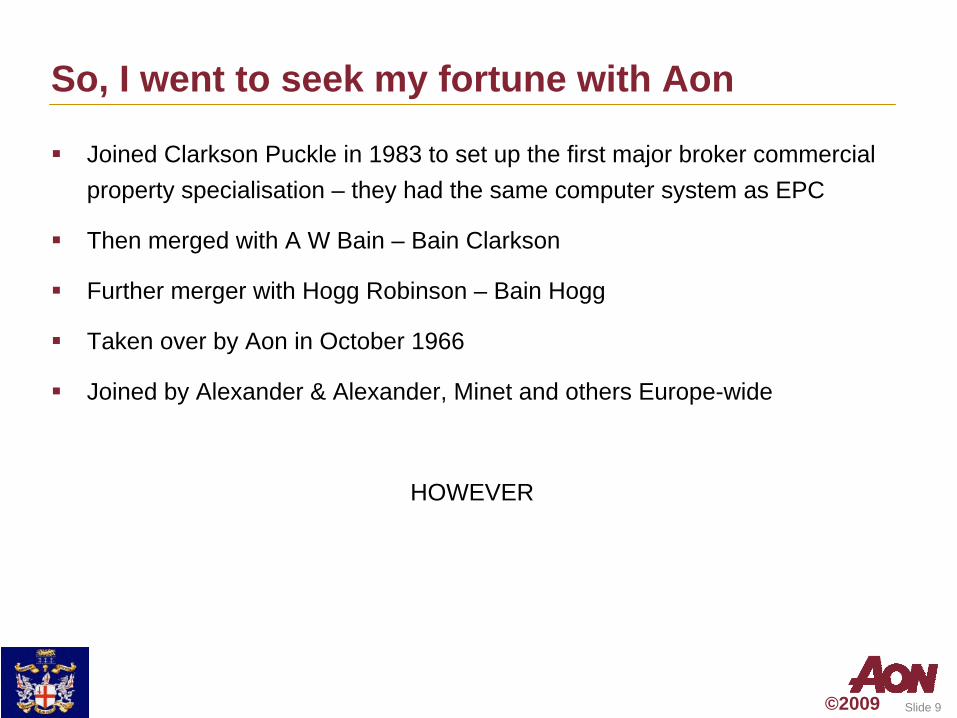

So, I went to seek my fortune with Aon

Joined Clarkson Puckle in 1983 to set up the first major broker commercial property specialisation – they had the same computer system as EPC

Then merged with A W Bain – Bain Clarkson

Further merger with Hogg Robinson – Bain Hogg

Taken over by Aon in October 1966

Joined by Alexander & Alexander, Minet and others Europe-wide

HOWEVER

Slide 10©2009

Canary Wharf

Olympia & York were seduced back to the UK by Margaret Thatcher - to rescue the Docklands regeneration dream

The Canary Wharf development agreement was signed in 1987

Started some consultancy work in 1988

Joined O&Y Canary Wharf as Vice-President Insurance in 1989

First desk top computer and Excel spreadsheets – mind-blowing!

Focus on construction insurance until first phases complete in 1991

Appointed to represent the BPF on JCT insurance committee – first client- up to then it was controlled by the contractors

Slide 11©2009

The property crash of the 1990’s

O&Y in Administration in 1992

Rejoined Aon (Bain Hogg) to take up from where I left off

Retained by Canary Wharf Limited, then a listed company, as Insurance Consultant for another 10 years – saw the vision realised

Slide 12©2009

Slide 13©2009

The rest of the Aon story – to date

Aon encouraged the expansion into a European operation with close US links

Set up the European Real Estate Practice in 1999

Decided to move into the M&A consultancy team from 2007

A change in direction to mark an age milestone

Still working closely with the commercial property team

Two major industry recognitions

Invitation to join the Chartered Surveyors Livery Company – only the 3rd non-qualified member after the CE of the RICS and the CE of the BPF

Election as President of the City Property Association- the first insurance person to hold high office in any property organisation?

Slide 14©2009

With the Lord Mayor at last year’s annual CPA luncheon

Slide 15©2009

The City Property Association

Founded in 1904

Originally for property owners

Now represents all those with an interest in City property – owners, developers, tenants, residents and consultants

150+ members – not enough from the insurance world; although they are major occupiers and owners – as well as consultants

Recent Past Presidents – Roger Reeves, PWC - Peter Cole, Hammerson - Mike Hussey, Land Securities

Our vision is to foster the right environment – where business can thrive;

to promote the City as a place where people should want to work, reside and visit, and be best placed to compete fully with business rivals in Europe and throughout the world

Slide 16©2009

CPA activities

Lobbying – EDF, Empty rates, Post Office closure and Planning

Seminars - Transport, Mapping and Sustainability

- Security, Flooding and The Future

Annual Luncheon – Lord Mayor

Annual Reception - Stuart Fraser, City Chairman of Policy & Resources

Much of this activity is undertaken in close liaison with the City. A supportive and mutually beneficial relationship

Aon Limited is authorised and regulated by the Financial Services Authority in respect of insurance mediation activities only.

So what lessons to be

learned from 45 years?

Slide 18©2009

The IIL Mission

“To raise the levels of professional knowledge of those working in insurance in London”

Not enough to be technically proficient in insurance

Need to understand the client’s business - backwards

Insurance needs to enhance its profile in the wider commercial world

Participation in trade bodies

We want to be regarded as fellow professionals but don’t behave like them

It’s tough and needs commitment – outside the comfort zone

Nobody wants to talk about insurance!

Slide 19©2009

Understanding the client’s risk – and responding

The market has failed to deliver an acceptable solution to Latent Defects

It needs an amalgam of property damage, business interruption and PI

Too many vested interests and artificial internal barriers

Now is the time to develop Residual Value Insurance

It would bring a different dimension to the investment market

Who has the vision for that? – Cuthbert Heath would have done it!

At this time, Credit Risk is paramount – to owner and bank. Where is the market?

There must be a price and a profit – it needs innovation and courage

There used to be people like that around – killed by the corporate environment

Slide 20©2009

Working with international clients – real estate is now a global business

Don’t expect things to be the same as they are here – they are not!

The cover, culture and customs are different

Language is a barrier

Nobody – certainly not you – wants to admit that they don’t understand

Challenge the answer if you have any doubts

Levels of integrity and professionalism sometimes fall short of UK ones- even in the most “civilised” countries

Don’t expect it to be done – check that it has been

Make sure that you completely understand the coverage and conditions

Slide 21©2009

Commission and disclosure

Generally, clients still don’t trust their broker regarding income

Understandable while clients themselves are often suspect

The lawyers are at fault – poor lease drafting

The situation got out of control

FSA regulation went some way but there are always clever ways around

2007 Lease Code has brought it closer to attention

Tenant enquiries and problems will do more

The FSA transparency investigation is not over

There are likely to be serious problems ahead – for some

Slide 22©2009

Terrorism

The market responded in 1992 – just

It was much slower to respond in 2002 – still not completely sorted out- extent of cover, especially for BI and clean-up

The ABI has lost its teeth – now anti-competitive to have a unified response

The IRA, and its clones, had kept us on our toes – never far away

Since then, we have become complacent – about defence, protections and the actual cover

Mumbai was a salutary warning of what is still possible

The UK has the best cover in the world

It may be seriously tested in the lead-up to the Olympics

Slide 23©2009

Climate Change

On the top of insurers and reinsurers agenda

An international problem – not just the UK

Not just flood –

Storms and rainfall

Wind and typhoons

Earthquakes

Temperature increases

Post 9/11 improvements in data analysis should have made underwriters more aware of their exposures – no more Goad maps

No guarantee that cover for some risks will continue – despite leases

Insurers are not charities – they only have shareholders to satisfy

Don’t confuse morals with insurance – as if you would!

Aon Limited is authorised and regulated by the Financial Services Authority in respect of insurance mediation activities only.

Flood – today’s big one!

Slide 25©2009

Flood insurance – some background

Defra report in 2002 - £220bn at risk - 1 in 13 homes plus business & farmland

Insurers objected - it is a political problem

Historic poor funding for infrastructure

Government promised increased investment

Planning regime needed serious overhaul

Improved drainage network during 2005 - 2010

ABI and HMG finally agreed a protocol in 2003

ABI announced a new Statement of Principles from 1st January 2006

Dependant on HMG meeting its promises – it didn’t!

Slide 26©2009

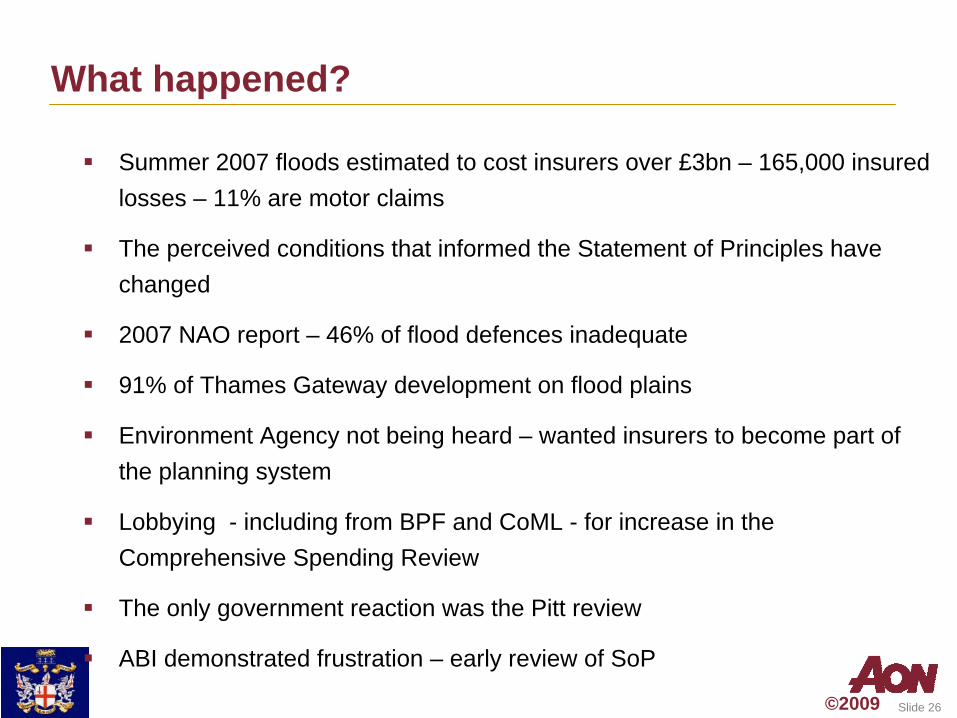

What happened?

Summer 2007 floods estimated to cost insurers over £3bn – 165,000 insured losses – 11% are motor claims

The perceived conditions that informed the Statement of Principles have changed

2007 NAO report – 46% of flood defences inadequate

91% of Thames Gateway development on flood plains

Environment Agency not being heard – wanted insurers to become part of the planning system

Lobbying - including from BPF and CoML - for increase in the Comprehensive Spending Review

The only government reaction was the Pitt review

ABI demonstrated frustration – early review of SoP

Slide 27©2009

2008 Statement of Principles

Now limited to 5 years maximum – with annual review

Subject to no external shocks, such as no reinsurance

Still conditional on Government meeting its obligations – financial, planning and strategic

Doesn’t apply to property built from 2009 – new guidelines for developers still awaited

If flood risk is not significant - less than 1 in 75 years - ABI members will continue to give cover

Cover maintained where risk is more than 1 in 75 years but where improvements are planned within 5 years – can be extended to a satisfactory new owner

No comment about property outside these categories

Only applies to residential and small business

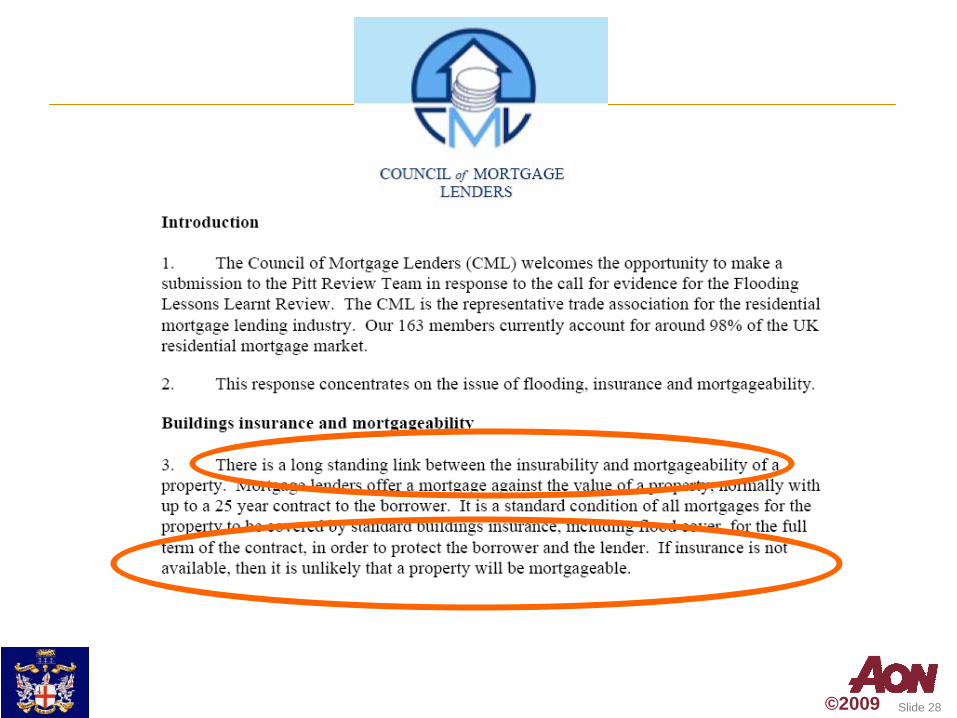

Slide 28©2009

Response to the Pitt Review

Aon Limited is authorised and regulated by the Financial Services Authority in respect of insurance mediation activities only.

What might it mean for our City?

Slide 30©2009

Extracts from the Environment Agency Extracts from the Environment Agency flood risk mapsflood risk maps

Railway Terminus

Hospital

Slide 31©2009

Sea levelsSea levels rising too fast Sea levels rising too fast for Thames Barrierfor Thames BarrierMarch 2008March 2008

Slide 32©2009

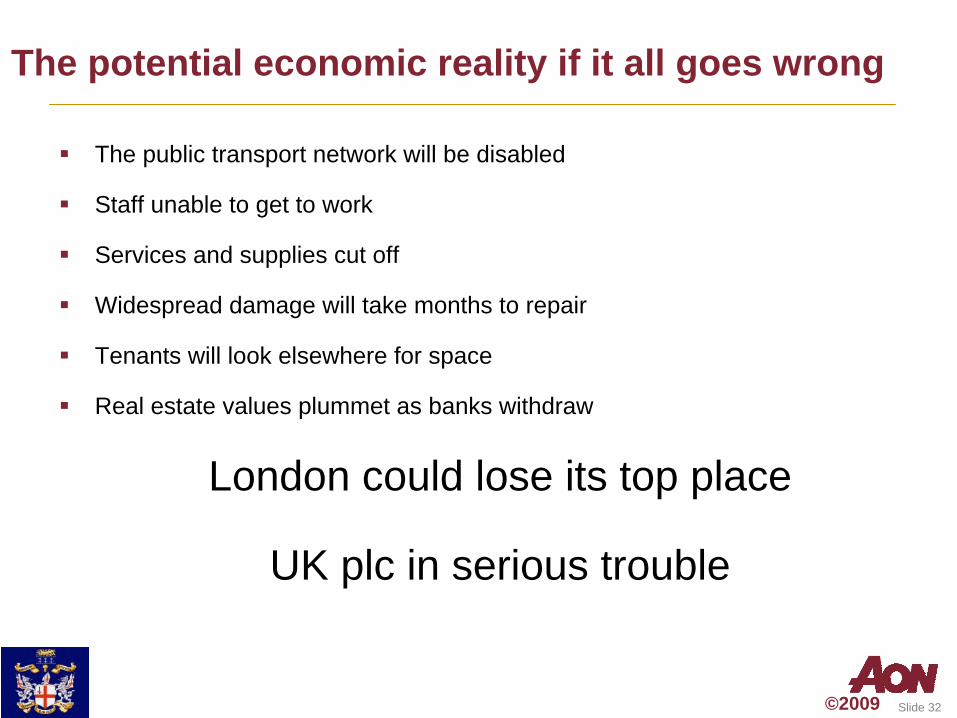

The potential economic reality if it all goes wrong

The public transport network will be disabled

Staff unable to get to work

Services and supplies cut off

Widespread damage will take months to repair

Tenants will look elsewhere for space

Real estate values plummet as banks withdraw

London could lose its top place

UK plc in serious trouble

Slide 33©2009

This has got nothing to do with insurance!

The problem has been caused by the lack of investment – over many years

Insurers will be blamed for restricting cover

An extension to the terrorism Pool Re may be set up

The basic fundamentals of risk management and insurance are being ignored

Ask those affected by the summer 2007 floods –

Would you like insurance or would you prefer not to have been flooded?