billing in the common nordic end - user market · billing in the common nordic end-user market ......

TRANSCRIPT

1

Billing in the common Nordic end - user market

Evaluation of responses from the public consultation

Report 6/2011

2

BILLING IN THE COMMON NORDIC END-USER MARKET

Evaluation of responses from the public consultation

Nordic Energy Regulators 2011

3

Report 6/2011

NordREG c/o Danish Energy Regulatory Authority Nyropsgade 30 DK-1780 Copenhagen V Denmark Telephone: (+45) 72 26 80 70 Telefax: (+45) 33 18 14 27 E-mail: [email protected] Internet: www.nordicenergyregulators.org

September 2011

4

Table of contents 1 Public consultation ....................................................................... 5

2 Introduction ................................................................................... 7

2.1 General findings from stakeholders’ responses to the draft report .. 7

3 Summary of the responses .......................................................... 9

4 Summary of general comments ................................................. 23

5 Annex ........................................................................................... 29

5.1 Questionnaire: ............................................................................... 29

5

1 Public consultation

During May and June 2011 NordREG arranged a public consultation on the preliminary consultant report Consideration of alternative billing regimes for the Common Nordic End-User Market. Below is a list of the respondents to this consultation.

Altogether 119 responses were received:

Organisation Name

AB Piteenergi

Agder Energi

Ale El Elhandel AB

Ale Elförening

Ale Elförening Ek förening

Andrs Hjalmarsson

Arvika Teknik AB

Bengtsfors Energi Nät AB

BestEl

BestKraft

Bjärke Energi ek för

Boo Energi ekonomisk förening

Boo Energi Försäljnings AB

Borås Elnät AB

C4 Elnät AB

CodeMint

Dala Kraft AB

Danish Energy Association

Degerfors Energi AB

Dong Energy

E.ON Elnät Sverige AB

E.ON Försäljning Sverige AB

E.ON Suomi Oy

E.ON Sverige

Elitkraft Sverige AB

Elverket Vallentuna El AB

EMIX

Empower Oy

Energinet.dk

Energy Norway

Enkla Elbolaget i Sverige AB

Etelä-Savon Energia Oy

Falkopings Municipality

Falu Elnät AB

Filipstad Energinät AB

Finnish Consumer Agency

Finnish Energy Industries (ET)

Fortum Distribution (Fin/Swe/No)

Fortum Markets (Fin/Swe/Nor)

FSE The Association of Danish

End Users of Energy

GodEl

GodEl i Sverige AB

Grästorp Energi AB

Grästorp Energi ek för

GS1 Sweden

Göteborg Energi DinEl AB

GÖTEBORG ENERGI NÄT AB

Götene Elförening

Herrljunga Elektriska AB

Hjo Energi AB

Hjo Energi Elhandel AB

Härryda Energi AB

Joint position of 30 local energy companies in Finland:Etelä-Savon Energia Oy, Haminan Energia Oy, Keravan Energia Oy, Kokemäen Sähkö Oy, KSS Energia Oy, Köyliön-Säkylän Sähkö Oy, Lammaisten Energia Oy, Lankosken Sähkö Oy, Leppäkosken Sähkö Oy, Mäntsälän Sähkö Oy, Nurmijärven Sähkö Oy, Paneliankosken Voima Oy, Porvoon Energia Oy, Vatajankosken Sähkö Oy, Sata-Pirkan Sähkö Oy, Imatran Seudun Sähkö Oy, Parikkalan Valo Oy, Esse Elektro-Kraft Ab, Oy Herrfors Ab, Herrfors Nät-Verkko Oy Ab, Jakobstads Energi, Korpelan Voima kuntayhtymä, Verkko Korpela Oy, Kronoby Elverk, Nykarleby Kraftverk, Vetelin Sähkölaitos Oy, Kuoreveden Sähkö Oy, Ålands Elandelslag, Valkeakosken Energia Oy and Rovakaira Oy

Karlsborgs Energi AB

Karlsborgs Energi Försäljning AB

Karlshamn Energi Elförsäljning AB

Karlskoga Elnät AB

Karlstads Elnät AB

Karlstads Energi AB

Koillis-Satakunnan Sähkö Oy

Kristinehamns Elnät AB

KS Bedrift Energi og Defo

6

Kvänum energi AB

Kvänumbygdens Energi ek. för

Landskrona Energi AB

Lerum Energi AB

LEVA i Lysekil AB

Lier Everk AS

Logica AS

Mälarenergi AB

Mälarenergi Elnät AB

Mölndal Energi AB

Nurmijärven Sähkö Oy (DSO)

Nurmijärven Sähkö Oy (supplier)

Näckåns Elnät AB

Näckåns Energi AB

Oberoende Elhandlare

Olofströms Kraft Nät AB

Oulun Sähkönmyynti Oy

Rovakaira Oy

Sandhult-sandareds El ek för

Savon Voima Oyj

SFE Kraft AS

SFE Nett AS

Sjogerstads EDF

Sjogerstasds Energi AB

Sjöbo Elnät AB

Sjöbo Energi AB

Skara Energi AB

Skellefteå Kraft AB (DSO)

Skellefteå Kraft AB (supplier)

Skövde Elnät

Sollentuna Energi Elhandel AB

Solletnuna Energi AB

Svensk Energi - Swedenergy - AB

Tibro Energi AB

Tibro Energi Försäljning AB

Tidaholms Elnät AB

Tidaholms Energi AB

Tieto

Utsikt Katrineholm Elnät AB

Utsikt Nät AB

Vara Energi

Vara Värme

Varberg Energi AB

Varberg Energimarknad AB

Vattenfall AB

Vattenfall Eldistribution AB

& Vattenfall Verkko Oy

Vinninga Elektriska FöreningEk För

VOKKS Nett

Västra Orusts Energitjänst

Ystad Energi AB

Ålands Elandelslag

Öresundskraft AB

Österfärnebo El ek.för

Österfärnebo Krefta AB

Österlens Kraft AB

Österlesn Kraft Försäljning AB

Øvre Eiker Nett AS

7

2 Introduction During the winter and spring of 2011 NordREG hired the consultant Dr. Philip Lewis from Vaasa ETT to look into the main different billing models that could be used for the future common Nordic end user market. The intention of the report is to provide a basis for a decision concerning the choice of billing regime within the common Nordic retail market. The report considers four different alternative billing regimes and it predicts also an impact assessment of these alternatives within the context of the future Nordic retail market.

Dr. Lewis findings were presented in the draft report Consideration of alternative billing regimes for the Common Nordic End-User Market. The stakeholders of the Market Rules Task Force within the retail market project contributed to the content of the consultancy report through discussions and written input during three meetings with VaasaETT during the winter and spring of 2011, but since the billing regime constitutes a very significant part of the market design, which will have great influence on the daily lives of all stakeholders in the electricity market, it was very important for NordREG to provide all stakeholders with an opportunity to comment on the consultancy report before finalising NordREGs recommendations. Therefore the draft consultancy report was published for consultation from the 24th of May until the 21st of June 2011. The consultation was open for anyone to answer. In total NordREG received 119 responses from different stakeholders.

The final conclusions of the draft report as well as the suggestions indicated in the report are not to be considered as NordREGs own suggestions, but will be used by NordREG as a basis for deciding on further recommendations.

This evaluation report includes a summary of the stakeholders’ responses and in addition some NordREG comments on the views presented by the stakeholders.

The evaluation of the responses will be taken into account during the finalization of the billing report and before NordREG issues recommendations on the future billing model.

2.1 General findings from stakeholders’ responses to the draft report

NordREG received altogether 119 answers to the public consultation from different stakeholders. From these answers 61 was from DSOs, 39 from suppliers, 1 from a consumer organisation (for large customers/industry), 5 from industry organisations, 2 from public authorities, 1 from a TSO and 11 from others stakeholders (mainly IT-providers and integrated energy companies).

8

Graph 1. Distribution of respondents

A vast majority of the comments were sent by Swedish stakeholders – altogether 92 responses. However, 45 of the Swedish comments – 31 of these from local DSOs and 14 from suppliers - were identical including also the exact same comments.

Sixteen responses were received from Finland. However, concerning the Finnish comments it should be noted that one the comment from Finland included joint views from 30 local electricity companies.

There were nine responses from Norway and four responses from Denmark.

It should also be noted that all of the four industry organisations responded to the consultation as well as a few it-companies but unfortunately only two respondents that could be viewed as representing consumers (the Finnish Consumer Agency and the Association of Danish End Users of Energy). The lack of consumer interest reflected in the respondents is also the main cause for concern regarding this public consultation.

It could be argued that the identical responses and comments from the group of Swedish companies should be statistically treated the same way as the single joint answer from the 30 Finnish companies. Another reason for discussion could be the fact that some companies operating in more than one country, or companies with both DSO and supply businesses have sometimes provided joint answers and sometimes separate but identical answers. NordREG has however analysed the stakeholder answers solely from a qualitative perspective, not from a quantitative perspective.

9

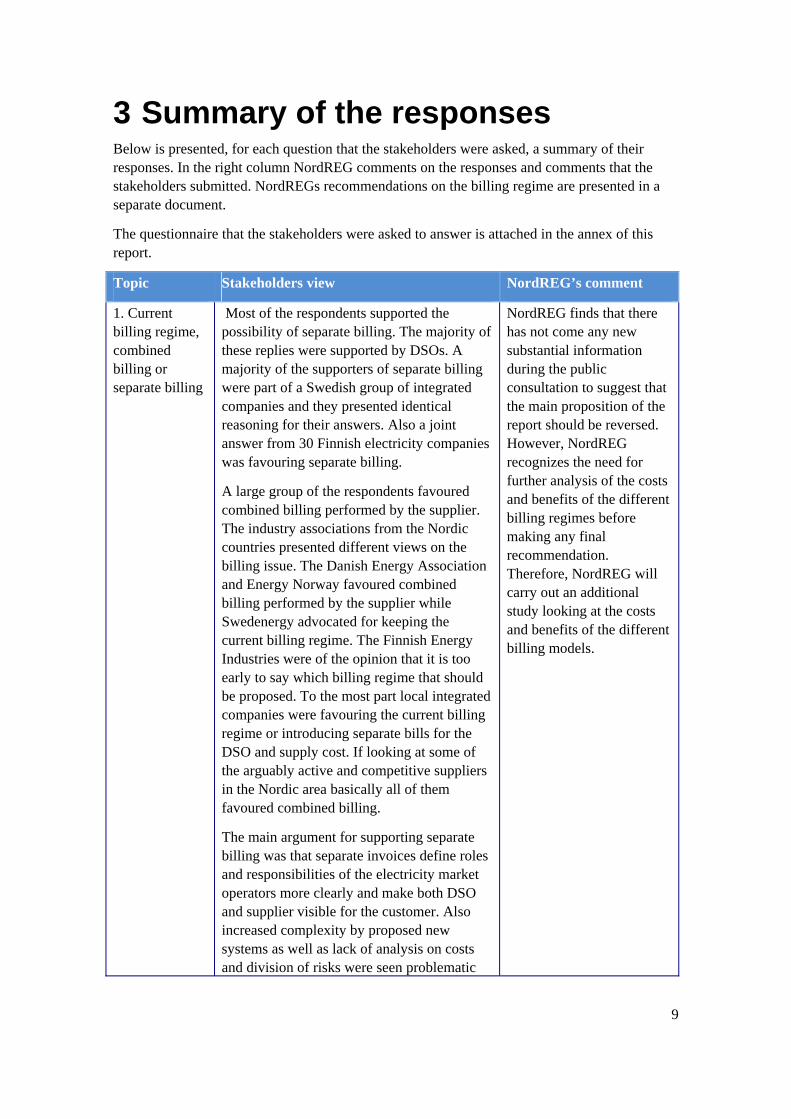

3 Summary of the responses Below is presented, for each question that the stakeholders were asked, a summary of their responses. In the right column NordREG comments on the responses and comments that the stakeholders submitted. NordREGs recommendations on the billing regime are presented in a separate document.

The questionnaire that the stakeholders were asked to answer is attached in the annex of this report.

Topic Stakeholders view NordREG’s comment

1. Current billing regime, combined billing or separate billing

Most of the respondents supported the possibility of separate billing. The majority of these replies were supported by DSOs. A majority of the supporters of separate billing were part of a Swedish group of integrated companies and they presented identical reasoning for their answers. Also a joint answer from 30 Finnish electricity companies was favouring separate billing.

A large group of the respondents favoured combined billing performed by the supplier. The industry associations from the Nordic countries presented different views on the billing issue. The Danish Energy Association and Energy Norway favoured combined billing performed by the supplier while Swedenergy advocated for keeping the current billing regime. The Finnish Energy Industries were of the opinion that it is too early to say which billing regime that should be proposed. To the most part local integrated companies were favouring the current billing regime or introducing separate bills for the DSO and supply cost. If looking at some of the arguably active and competitive suppliers in the Nordic area basically all of them favoured combined billing.

The main argument for supporting separate billing was that separate invoices define roles and responsibilities of the electricity market operators more clearly and make both DSO and supplier visible for the customer. Also increased complexity by proposed new systems as well as lack of analysis on costs and division of risks were seen problematic

NordREG finds that there has not come any new substantial information during the public consultation to suggest that the main proposition of the report should be reversed. However, NordREG recognizes the need for further analysis of the costs and benefits of the different billing regimes before making any final recommendation. Therefore, NordREG will carry out an additional study looking at the costs and benefits of the different billing models.

10

among the respondents. It was also stated that the current unfair system where in practice only incumbent suppliers have a real opportunity to offer combined billing should be removed.

The group of Swedish companies that presented identical answers highlighted their proximity to the customers and that customers want to keep the close communication that they have today with the local integrated companies. There was also a view among these companies that the billing regime could be kept unchanged.

The main support for combined billing is to be found among suppliers. However, there are also a number of DSOs and other stakeholders that support such a billing regime. Among these respondents combined billing performed by the supplier was seen the best option since it will increase customer friendliness as well as improve the efficiency in many processes. It was also seen to be potentially a cost efficient solution in the long term and the logical option in case of a supplier centric model at the same time as combined billing would mean that the electricity market would be more perceived as any other market by customers. This group of respondents also highlighted the possibility to increase the relationship between the supplier and the customer as a positive effect. Fears were also raised for the option of separate billing since many stakeholders said that such a billing regime would increase costs due to double systems etc.

The comments from the fourteen respondents that favoured the current billing regime were that current national regimes works just fine today and there are no need for changes.

Current billing regime 14, Separate billing 64, Combined billing performed by supplier 35, No answer 5

2. In case of combined

When comparing the views on whether the combined billing should be mandatory or

NordREG finds that there has not come any new

11

billing, should it be mandatory or voluntary

voluntary, the voluntary approach was far less popular among the respondents that mandatory approach. Mandatory combined billing was also said to put more focus on good customer service and also increase the possibility to introduce innovative products. Another argument presented was that mandatory combined billing would ensure that the DSOs could focus more on their core business and the important task of facilitating an efficient market. It was stated in many responses that voluntary billing regime would be less efficient and leads to dual processes, which means higher costs and increased complexity in the interaction between the players. On the other side, the voluntary approach was supported with the argument that with mandatory combined billing the smaller suppliers might risk termination if they are unable to manage to handle process.

However, the majority of respondents were not supporting either mandatory or voluntary approach. This is a logical consequence of the answers given to the previous question concerning the billing regime as many of these respondents were favouring separate billing regime. These respondents stated that there is overconfidence in the importance of a combined invoice and that the implementation of a Nordic end-user market could be accomplished in the easiest and least expensive manner with basic harmonization.

Mandatory combined billing 38, Voluntary combined billing 6, Indifferent 57, No answer 17

substantial information during the public consultation to suggest that the main proposition of the report should be reversed. However, NordREG recognizes the need for further analysis of the costs and benefits of the different billing regimes before making any final recommendation. Therefore, NordREG will carry out an additional study looking at the costs and benefits of the different billing models.

3. Integrated or simple integrated billing

‘Integrated Combined’ refers to billing that primarily, in a single format, shows only what the customer owes to the supplier. DSO elements of the bill (distribution fees owed by the customer) may or may not be visibly separated, but even if they are, the bill looks clearly like one bill rather than two bills in one. Typically, such bills will only show one set of taxes as opposed to taxes separated according to whether they relate to

NordREG takes note of the stakeholders’ comments and will consider whether to make any recommendations on this issue at a later stage.

12

distribution or supply.

Approximately half of the respondents were in favour of integrated combined billing. In many of these responces combined integrated regime was seen to be the most efficient and also the most customer friendly solution. According to the responses integrated billing also conforms to other industries. However, some respondents remarked that it should be investigated further prior decision-making whether the DSO price and tariff structure should be presented on the invoice or not, to identify best practices from a competition and customer satisfaction perspective.

‘Simple Combined’ refers to billing that effectively contains two sub bills. In its most simple form the supplier does not make any alterations to the DSO bill but simply adds it to the same invoice and presents one total sum for the customer to pay. Approximately half of the respondents supported simple combined billing. It was stated that combined integrated billing is too complex and will possible lead to very high operational costs. Simple combined billing also keeps customers aware of the DSO costs.

A majority of the respondents didn’t provide an answer as they don’t support combined billing regime at all.

Integrated 27, Simple combined 25, Indifferent 11, No answer 55

4. Billing monthly backwards (towards the customers)

A majority of respondents supported the solution that billing should be conducted monthly backwards towards the customer. Some respondents justified their answer by saying that the situation is like this today. Some saw that monthly backwards billing would reduce the credit risk. However, some of the respondents who were favouring monthly backwards billing stated in their comments that it should also be possible for customers to negotiate or be given other alternatives. There were also comments that

NordREG takes note of the great support there is among stakeholders for having monthly backwards billing. The main question is if it should be regulated or not. There are both pros and cons with the different solutions, with decreased risk as a positive effect if regulated at the same time as it would reduce customer

13

advocated that monthly backwards billing should be considered as industry standard and that there is no need to regulate this issue.

Those respondents who didn’t support this regime were generally in the opinion that it should be possible for the customer together with the supplier to decide the billing interval because billing frequency was seen to be a competitive issue.

Yes 89, No 17, Indifferent 7, No answer 6

choice. Since this issue is connected to risk management it will be studied further in an upcoming NordREG study.

5. DSOs need to keep possibility to invoice customers directly if billing is mandatory combined

Most of those respondents who provided an answer to this question agreed that DSO in some special cases needs to keep the possibility to invoice customers even if the billing regime is mandatory combined billing performed by suppliers. It was stated that DSOs will need to invoice for example for new connections and similar services which are not handled by the supplier in the normal invoices.

Thirteen respondents didn’t see a need for DSO to keep possibility to invoice customers but it should be noted that some of them also said that the DSOs need to invoice new connections. So in practice only very few respondents stated that DSOs should not invoice customers in any cases. In those answers it was argued that the retention of billing facilities at DSO will be costly. Therefore some of the respondents view was that it may be more optimal for society to make the combined billing at suppliers mandatory in all cases.

A majority of the respondents didn’t provide an answer to this question at all as their standpoint is that the DSO should invoice all of its charges to end-users.

Agree 45, Disagree 13, Indifferent 2, No answer 60

NordREG takes note of the stakeholder’s assessment that DSOs will need to keep billing capabilities even though there is mandatory combined billing to the end customer. NordREG also takes note of the fear for the costs that such a solution could bring.

6. Data hub needed if there is combined billing

A majority of the respondents did not provide any feedback on the question whether a data hub is necessary to be able to get an efficient (mandatory or voluntary) combined billing.

NordREG takes note of the stakeholder comments. The issue of information exchange and the possible

14

A clear majority of those respondents who did provide an opinion on this matter were in favour of a data hub as a solution to provide combined billing. Among these stakeholders there were comments stating that a data hub should be the actual billing engine, a data hub helps to facilitate neutrality among the stakeholders and many consider a data hub as the easiest way to handle the increased information exchange needs that comes with a Nordic market.

A minority of the respondents disagreed to the need for a data hub. Among these stakeholders there were comments supporting more decentralized solutions than one hub per country.

Agree 40, Disagree 7, Indifferent 0, No answer 74

future for data hubs is currently looked at thoroughly in the Business Process Task Force and any NordREG recommendations on this topic will be published once that TF has finalised its work.

7. Single contract in case of combined billing

A clear majority of the respondents stated that it is possible to use a single contract in case of combined billing while a minority of the respondents did not agree to this. Some respondents highlighted the need for certain types of, mainly larger, customers to have separate contracts even though the mass market could use single or combined contracts.

Yes 98, No 15, Indifferent 3, No answer 4

NordREG takes note of the responses and comments to the issue of single or dual contracts. There is currently an on-going study within the Customer Empowerment Task Force looking at this issue. NordREG will not issue any recommendations regarding one or two contracts prior to the completion of this study.

8. Two contracts in case of combined billing

A significant group of the respondents agreed that it is possible to have two contracts (one contract with the supplier and one with the DSO) in case of combined billing.

A majority of the respondents chose to not respond to this question.

Yes 49, No 6, Indifferent 2, No answer 63

NordREG takes note of the responses and comments to the issue of single or dual contracts. There is currently an on-going study within the Customer Empowerment Task Force looking at this issue. NordREG will not issue any recommendations regarding one or two contracts prior to the completion of this study.

15

9. All billing related customer service provided by supplier in case of combined billing

The next question in the questionnaire was related to the whether all billing related customer service should be provided by the supplier.

On one hand some of the respondents supported the proposal and were of the opinion that the company which sends out the bill should provide a customer service on all possible questions. It is natural to have a single point of contact for billing related queries and services as in the telecom sector and in deregulated markets it should obviously be the suppliers role also to take care of the customer contact which includes billing. The suppliers have also larger incitements to generate efficient processes on customer service and billing compared with the DSO’s.

Other respondents supported that even with a simple customer interface the supplier should also be able to forward questions regarding network specific questions. As many DSO’s already today have customer functions they in principle should be "moved" to the suppliers instead. Required network expertise is necessary somewhere. Therefore not all billing related customer service, but maybe some of it could be moved to the supplier.

On the other hand many answers pointed out that local customer services, social responsibility and proximity to customers are very important features for customers and should not be taken away from the DSO. This means that a billing service is necessary at the DSO.

It would be difficult for the suppliers to respond to grid related questions and therefore it is better with two separate invoices. One bill could also give a lot of complications regarding tariffs, taxation and collateral. The smaller suppliers have normally not the recourses also to handle the DSO related billing questions.

Finally, it were also suggested the DSO should instead be the invoicing party when

It is natural that the customers first contact point for complaints or inquiries related to the bill is also directed at the sender of the bill. However, NordREG recognises the customers need to in some cases be in direct contact with the DSO. A supplier also has limited possibilities to provide information on details of network tariffs or respond to complaints regarding network tariffs etc. Therefore it is important that the supplier has the possibility to forward such questions to the relevant DSO.

This issue is also closely linked to the issue of what information should be displayed to the customer in the bill. NordREG will address the information in the bill at a later stage.

16

having combined billing – if a clean two invoice model could not be preserved.

Agree 50, Disagree 67, Indifferent 0, No answer 4.

10. Suppliers responsible for debt collection, (supplier obliged to pay the DSO independent of the customer's payment)

According to the majority of the answers it is the supplier who monitors the behaviour of the customer payments and also naturally carries the risk. The normal way in other markets is that the billing party also is responsible for debt collection. Other alternatives would be too complicated and costly to handle. The billing responsible should handle payments and related questions in order to get an efficient process.

But it was also stated that this solution could increase the entrance barrier for suppliers.

The risk increases for the suppliers when they are responsible for debt collection. If, however, the suppliers should take the risk, there could be an agreement between DSO and supplier where the DSO pays the supplier to take the risk on his behalf. It should be voluntary business deals and not regulated.

Another argument was that the DSO should not get all the risk if some suppliers have a doubtful ethical standard. Other respondents have asked for separate invoices to solve the risk management problem.

Some respondents do not see a need for a third party solution, as the non-paying customers are very few. A solution could instead a transparent payment solution, performed by the supplier, and with each parties claim on the amount paid by the customer.

The need to look on the issue in greater detail was also emphasized, as a supplier can't take all the risk and a DSO can't have a risk-free situation. The supplier must have instruments to limit their risk concerning insolvent customers. A solution could be a client account, where the supplier and DSO share the risk for bad payers.

NordREG takes note of the majority of the stakeholder’s assessment that the suppliers should be responsible for the debt collection (and are obliged to pay the DSO’s independent of the customer's payment).

There are both pros and cons with the different solutions to decrease risks. The prerequisites for the billing between DSO‘s, suppliers and energy service companies need to be further investigated.

Since this issue is connected to risk management it will be studied further in an upcoming NordREG study.

NordREG will, during the autumn of 2011, launch a study which should look into what appropriate measures that could be taken to ensure that credit risk is allocated appropriately between suppliers and DSOs. The goal of the study should be to find a way to introduce combined billing without increasing entry barriers for suppliers.

17

Agree 85, Disagree 21, Indifferent 2, No answer 12

11. Monthly billing between stakeholders (DSOs, suppliers and energy service companies)

The majority of the respondents agreed on a standardized invoicing interval if combined billing is introduced. A standard agreement for all market actors should be developed including billing, payments and debt collection. Billing between stakeholders should, as a general rule, be based on actual measured consumption. A rather short billing period is preferred since it simplifies eventual complaint handling processes.

Some answers also stressed that the basic rule should be for revenue and expenses to correlate time-wise regardless of the billing model. The important point is that the cash flow between DSOs, suppliers and energy service companies mirrors the cash flow from the end users to the suppliers. Otherwise, the suppliers could be left with a liquidity problem, which would increase the entrance barrier into the retail market (or, alternatively, would increase the DSOs’ risk unduly, if the terms are very favourable for the suppliers).

Other answers pointed to the legal aspects would be easier, although some national laws have to be changed to give the supplier the opportunity to demand a disconnection of a customer due to non-payment or non-compliance.

Some respondents understand the suggestion on monthly billing as a more theoretical solution and they prefer separate invoices. The main argument is it will grant more freedom of choice for the companies. The monthly, bimonthly and quarterly invoices of today should also be possible in the new market.

Finally, some of the answers have pointed to that the prerequisites for the invoicing between DSO and retailer need to be further investigated.

Agree 102, Disagree 4, Indifferent 3, No

NordREG takes note that a very large proportion of the stakeholders would agree on the suggestion of having monthly billing between the stakeholders.

There are both pros and cons with the different solutions to decrease risks. The prerequisites for the billing between DSO‘s, suppliers and energy service companies need to be further investigated.

Since this issue is connected to risk management it will be studied further in an upcoming NordREG study.

NordREG will, during the autumn of 2011, launch a study which should look into what appropriate measures that could be taken to ensure that credit risk is allocated appropriately between suppliers and DSOs. The goal of the study should be to find a way to introduce combined billing without increasing entry barriers for suppliers. The study should also consider the pros and cons of introducing mandatory monthly backwards billing between all stakeholders (including customers).

18

answer 11

12. Suppliers should be given extra days (month plus 10-15 days) of credit concerning payments to DSO

The proposal is an advantage for suppliers but could create liquidity problems for DSOs, which would then be forced to cover the substantial outstanding amounts.

Many respondents find therefore the suggestion as financially unacceptable. If implemented they believe a DSO shall also extend its payment period by the corresponding time for TSO. The problem is avoided with separate invoices. Increased credit costs will lead to increased costs for the customer (”cost driving”).

If the payments are done to a client account it is not necessary to have the extra days.

Some respondents wrote that it depends on how the risk issue is resolved and what happens if an invoice is not paid. 10-15 days is generous if the bill is paid on time but not generous if the bill is not paid. Other suggested only 5-10 extra days, and a few even supposed it should be possible with only 5 extra days or 2-3 bank days of credit, as also the DSO’s faces a hard time schedule when they should supporting meter reading.

It was also mentioned that an extended credit time can be viewed as a solution to counterbalance the transfer of credit risk from the DSO to the supplier. However, the economic consequences for the DSOs should be reviewed and compensated in the event financial revenues are reduced and credit risk is increased.

For the supplier it is important to have the customer pay before he has to pay the DSO. However, the supplier usually has to pay for the electricity before the customer has paid his bill and that is handled today. If the DSO wants its money before the customer this can be handled in a business agreement.

Finally, some recommend the issue to be analyzed further before making any final decisions.

NordREG takes note that a very large proportion of the stakeholders cannot agree on the suggestion of extra credit related to payments by the suppliers.

There are different solutions regarding this liquidity issue. The prerequisites need to be further investigated. Since this issue to some extent is connected to risk management it will be studied further in an upcoming NordREG study focused on risk management.

19

Agree 32, Disagree 79, Indifferent 3, No answer 7

13. Handling of increased risks for suppliers and DSOs

In general some respondents did find that claims are transferred and there must be some form of guarantee like a bank guarantee, security deposit or insurance. Irrespective of the solution it will lead to increased costs for the customer. DSOs can’t choose their counterparties. Another answer pointed out that it will be a cost, but it must be seen as a necessary one. Reduced risk (by e.g. customer accounts) might lead to lower overall costs for the customers.

Another comment was that as in any other business credit losses may occur and they can be handled as in any other business.

Financially strong actors have to some extent a natural advantage of their capital strength.

And again some respondents suggested two invoices to avoid the guarantee problem.

One argument in favour of mandatory payment guarantee is the doubtful ethical behaviour of certain suppliers which request some type of security. A fee to an insurance scheme (per country) could be a way out. Or there could be a mandatory payment guarantee between the DSO and the supplier, and between the customer and the supplier (it could be up to the contract). On the other hand can mandatory payment guarantees also lead to some type of barriers for new entrants on the market.

It has also been suggested that by required guarantees, supplier’s risks will expand, increasing the required return and price margin. This would mean that only big partners can asset guarantees to sell Nordic wide.

To protect the customer in case of a supplier losing any license to act on the market, mandatory processes and rules for supplier of last resort must somehow be in place.

Some answers prefer a solution similar to a

NordREG takes note of the stakeholder’s assessment that mandatory payment guarantees could be one of many tools to manage risks for suppliers and DSO’s if combined billing is introduced.

To gather more information NordREG will, during the autumn of 2011, launch a study which should look into what appropriate measures that could be taken to ensure that credit risk is allocated appropriately between suppliers and DSOs. The goal of the study should be to find a way to introduce combined billing without increasing entry barriers for suppliers.

20

client account, that is a type of transparent payment solution with each parties claim on the amount paid by the customer. Others doubt whether it is necessary to have a third party solution as the non-paying customers are very few.

Other answers have argued that all stakeholders should be responsible for their own. E.g. a joint insurance scheme can be arranged as a voluntary option for the players.

Finally, could an alternative be to minimize increased risk e.g. be regulatory requirements regarding financial liability and credit assessment of market players.

Mandatory payment guarantees 85, Voluntary private industry schemes 6, Indifferent 9, Other 9, No answer 9

14.Competition will improve with mandatory combined billing

Some respondents suggest the competition will increase but when looking at the end price of a customer it could be difficult to motivate to diminish this margin with the inefficiencies and system cost that will take place. In short, the margins in the Nordic are too low to increase the number of new suppliers.

One view is that mandatory combined billing regime, as opposed to the voluntary, will improve competition and efficiency, and in the end benefit the customers. There is a great opportunity for competition to improve but the risk issue needs to be solved and payment conditions carefully planned. Small companies might suffer cash flow issues that may be enhanced by combined billing.

Many of the respondents suggest there will be less competition by the proposal. The smaller DSOs and suppliers will disappear and there will be fewer but larger companies within the business, thereby less competition and greater distance to the customer. As the model favours larger suppliers this will potentially lead to less competition in the end-user market as the Nordic market becomes dominated by a handful of oligopolistic

NordREG takes note of the stakeholder comments. The majority of respondents disagree that competition will improve by introduction of mandatory combined billing.

It is difficult if not impossible today to estimate the final effect by establishing mandatory combined billing as many other parameters have to be taken into consideration. However, NordREG does however not share the view of the respondents that believe that combined billing will reduce competition. However, two important factors that are brought up are implementation and cost. It is important that any implementation of a new billing regime is carried out in a way that reduces any

21

companies. Some find that duplicate customer service systems will raise costs, and smaller supplier can't invest in Nordic wide systems. It will favour the already large Nordic companies.

Some respondent’s states that today there are already more suppliers on the electricity market than for instance when looking at the number of suppliers of broadband, mobile phone etc.

A few respondents believe there should be separate trademarks and company names for all DSO and suppliers acting on the market. The costs for grid and supply bundled together on an invoice would mean the customer cannot see which part of the invoice to influence by changing supplier.

One respondent fears new administrative burdens. Combined billing is ok but it should be handled simple and not as a hybrid with new burdens. Active cooperation with consumer authorities would help given that communication, transport and rail have managed to do it in a deregulated environment. Consumers have for instance never paid for the milk delivery to the stores at a separate cash register.

Finally, some of the answers can see both pros and cons. There can be reasons for the customer preferring the supplier only to bill the energy without DSO tariffs. On the other hand a mandatory combined billing solution is simpler to understand. But it is unclear whether the benefits by mandatory combined billing are in any proportion to the cost. Or to put in another way it is not possible to say anything about the competition as the effects of combined billing have not been analysed sufficiently enough. The proposed retail market model most probably will increase the complexity of the market structure. Whether competition improves depends on far more factors than the billing model alone.

Agree 27, Disagree 72, Indifferent 6, No

problems, especially for those market actors that have less resource. An efficient implementation would most likely also reduce costs.

However, NordREG recognizes the need for further analysis of the costs and benefits of the different billing regimes before making any final recommendation. Therefore, NordREG will carry out an additional study looking at the costs and benefits of the different billing models.

22

answer 15

23

4 Summary of general comments Quotes1 from the respondents general comments to the billing report:

Falu Elnät

Let the supplier offer products to the market that can be dynamic. That is not for the DSO to handle, bigger customers excluded where the DSO can have economic or dimensional benefits.

DSO will still have contact with the customers when needed and also possibility to inform about work in specific areas, meter change, new connections.

Information on the bill however about the DSO (name, home page, phone number) should be obligated for the supplier to provide.

FSE The Association of Danish End Users of Energy

A Nordic harmonisation is not an end in itself. In general, a harmonisation encompassing The Single European Electricity Market must be the end goal. Therefore, the Nordic harmonisation must not in any way delay or potentially impede an EU harmonisation.

Ale Elförening Ek förening

This proposal will not develop the nodic electricity market to a more competitiv market, only drive costs. Our proposal is to focus more on new electricity production instead.

Elitkraft Sverige AB

It is of great importance to get ride of the "anvisningsleverantör". Today it helps integrated companies to get huges amount of customer without any competition. For the customer it means a very high price an a bad product (Tillsvidarepris). By introducing one contract this problem will be solved and the competition for customers moving in would be fair!

Today integrated suppliers can use the extra money earned on these customers to compete for the active customers which is unfair competition.

2015 is a good year for implementing the new market model!

EMIX

Implementation of the proposal requires an active, sustained and strong regulator.

Energy Norway

Energy Norway fully agrees with the objectives of the common Nordic end-user market. We believe that the proposals in the report support these objectives. The proposed billing regime is not a replica of any existing model. On the contrary, the proposal seems to represent a mix of characteristics and best-practice solutions from different markets.

Ålands Elandelslag

1This is not a comprehensive list of all the stakeholders comments, but is meant to be seen as examples of

some of the stakeholders general comments.

24

- We feel that the project is a political project instead of being started by the end-users of electricity. The customers have not called for this project but they have called for a stable, transparent and functional whole sale market.

- There is no cornerstone to build a common end-user market on before we have a common whole sale market without price areas, harmonized legislation, currency and taxation. There will also be problems with languages.

Vattenfall AB

...before deciding upon costly changes, the benefits of the suggested market model must be analyzed in more detail.

The implementation of the new market model should be carried out in a planned and structured way to minimize any negative impact on market actors as well as customers.

In a combined billing regime, it is important to protect the customer’s rights in a case of reclamation for either the network service, supply or both of them. The customer should always have the possibility to withhold from paying the reclaimed part of the invoice until the reclamation is handled correctly without the Supplier initiating disconnection of power.

Mälarenergi AB

Its extremely important that a contract/agreement exists between DSO and Supplier that handles rights and obligations that’s places the ground for economical issues.

Empower Oy

Supply profit margins are very small and clear industry processes would allow for centralized services and systems that would cut costs for all market actors. Having to interpret and develop company or region specific de facto ways of implementation as is now prevalent is not sustainable.

Agder Energi

The DSO`s are worried about their possibility to give the costumers price signals/incentives through contracts and/or invoicing when/if there is only one contractual ralationship and the grid tariffs is hided inside the combined bill. This will be a challenge in a future scenario where the costumer not only takes energy out from the grid but also put energi in to the grid. With dynamic grid tarifs varying from area to area depending on local grid capasity the suggested model will be challenging both for the suppliers and the DSO`s.

Finnish Energy Industries

The report argues combined billing assuming customers’ feelings. There are different views of what customers want or how significant the issue of one or two bills is. Analyzing the results of customer surveys is always a question of interpretation. There are also other important issues to be taken account of.

The whole system has to be designed to be cost-effective. The costs for customers must not increase unjustly.

The implementation of the chosen model will greatly impact the overall result. The project must find knowledge and know-how to achieve this.

25

The companies are concerned of building a common end-user market when at the same time there are problems in the wholesale market (too small price areas). A functional and competitive wholesale market is a pre-requisite for a functional end-user market.

At least the combined billing regime must not be implemented so that DSOs disappear completely into the background.

It is important to design the market model carefully and to make sure that customers know who they should contact in different issues. Otherwise customers may be confused and unsatisfied.

Olofströms Kraft Nät AB

The customer wants a local contact, thats is very important, they want to visit us on our local office!

E.ON Sverige

...the report as such covers a much larger area than just billing. While we appreciate the complex nature, and interdependency between billing and the other areas, e.g. data hubs and contracts, we feel the author has a too big role in making recommendations in these areas. Hence, we feel it is important to treat the report, especially in these areas, as a guiding way forward, rather than as recommendations as such. It is up to the designated task forces in these areas to investigate the best solutions regarding data hubs and processes in general, contracts and tariff harmonization.

Further, we feel that the area of a voluntary billing regime undermines the entire report. Not only are the reasons for a voluntary combined billing (for multi-utilities) based on arguments which, arguably weaken competition, the suggested “exception” would also be given to a large part of the market. We would also like to highlight the customer survey performed by Synovate in June 2010 which showed that only 9 percent of the customers would prefer two invoices. That figure could not motivate a voluntary regime which would erode all efficiency potential.

Identical comment from 45 Swedish companies

We see that we have an important role in society primarily with respect to conversion to environmental oriented energy systems. This work is taking place primarily at a local level e.g. energy efficiency, local electricity production, conversion from electric and oil based heating to renewable sources of energy.

With respect to customer mobility, it is the customers’ choice. The customer wants a local contact. What is wrong with that? One can ask whether the number of supplier changes is a measure of a successful market. Many times the change of supplier is a measure of dissatisfaction with a supplier either with respect to price, service etc.

We also believe that the proposal will lead to increased costs, both with respect to data information and invoicing. Small electricity suppliers will probably not sell outside of their home markets since it can be difficult to invoice many different network charges.

Fortum Markets (Fin/Swe/Nor)

26

Implementation cost and risks are not well enough described and many details are still open. Testing against the key requirements needs to be continued in the detailing processes. There should be a true opportunity to re-evaluate the solution if further analyses show that the implementation is not feasible.

Dual processes (e.g. caused by voluntary combined billing) should not be accepted!

o In our experience, one FTE in billing drives approximately 6 FTEs in accounts receivable, credit control, debt collection and related call center services. A supplier's decision to start or terminate combined billing thus gives substantial effects on the DSO's FTE need, which will vary substantially over time -> not effective since it introduces redundancy and dual processes.

o With voluntary combined billing the DSO has to have a billing system that can send bills to all customers and a process to distinguish between which customers to send bills to.

o Efficient/standardized processes and interfaces are prerequisites for combined billing - the reasoning in the report for a voluntary solution (invoicing also DSO charges would create a too big threshold) is thereby not relevant.

Varberg Energi AB

If there is any form of payment guarantees between supplier and DSO:s, we see an increased financial risk for the DSO:s. For example, if a supplier charge their customers network charges, and then go bankrupt and not pay the network charges to DSO:s.

If the suppliers are to charge their customers network charges the financial risk increases for the suppliers. There is an increased amount of money the suppliers must charge, and risk not getting paid for by the customers. They must in turn pay to the DSO, although they have not been paid by the customer.

Swedenergy

SWEDENERGY welcomes the ambition to create a common Nordic retail market. We believe however that the basic market model used in the Nordic countries should in principle be maintained when entering into a common market and harmonization should be focused solely on core processes.

The most decisive success factor in striving for a common Nordic end-user market is that the same system can be used regardless of the geographical location of the customer and supplier, which means that the business processes must be harmonized. Uniform structural data, standardized message formats and development of common timeframes are required as well. With regard to the business processes, however, SWEDENERGY believes that the billing process is an exception from that which can be considered critical to harmonize since, in addition to national legislations, similar regulations are being drafted in every individual country as a consequence of the Third Electricity Market Directive. SWEDENERGY thereby supports the “no harmonization” alternative and believes that this should be the platform on which to build further. And although the customers’ need for a combined bill should be satisfied even in a model of this type, it should be based on voluntary implementation and industry consensus rather than mandatory rules.

27

After all, if the final policy decision would mean harmonization of the billing process in accordance with the proposal for a combined billing, several very important and complicated issues have to be resolved. In such a situation, we hope that the conditions will create room for effective competition, well-functioning cross-border routines and a high degree of customer satisfaction.

Etelä-Savon Energia Oy

This is a waste of time.

There are many much bigger issues to improve in the electricity market than combined billing. The order of planning the common Nordig retail market is totally wrong. NordREG have to listen the electricity industry: fix the big things first.

But nowadays NordREG doesn't listen at all !!

Joint position of 30 local Finnish energy companies

The basis for harmonizing and integrating Nordic end-user markets hinges on the assumption that currently markets are uncompetitive and customers lack choice. This is categorically untrue. In Finland there are over 40 suppliers of electricity and end-user electricity prices are amongst the lowest in Europe. Moreover, markets in other sectors, such as telecommunications and insurance, exhibit far less competition with a higher degree of market concentration. What is required is an apolitical re-assessment of the present market situation that puts the end-user electricity market into a broader perspective. Narrowly focusing on marginal issues, such as billing regimes, will not help remove the larger obstacles – namely, a common wholesale market without price areas along with variations in legislation, currency and taxation - impeding the creation of an integrated Nordic retail market for electricity.

The proposed retail market model with mandatory combined billing is likely to increase the complexity of operating in the market. Furthermore, the lack of a common Nordic currency as well as language requirements will create new barriers to entry.

Göteborg Energi DinEl AB

DinEl is very positive to the market developing in this direction as it would be healthy for the Nordic electricity market to consolidate, and get the same set of business and operating rules cross boarders. A common Nordic retail market will strengthen our position in the European market, attract new entrants and investments and make it possible for the Nordic region to take the lead in market and service development in the energy sector.

GS1 Sweden

For consumer companies it must be possible to have the choice not to receive combined invoices.

Energinet.dk

...the challenges of multi-utility bills are described. For Energinet.dk it is still more attractive for customers to receive a combination of electricity tariffs and electricity consumption rather than electricity tariffs and district heating/water etc tariffs on one bill and electricity consumption on another.

28

Tieto

Separate billing builds OPEX into the utility market through development and maintenance of regulatory compliance for dual systems both in the DSO and suppliers’ business organisations.

We strongly believe that combined billing will increase customers understanding of our industry and lower the total cost of operations and IT systems.

Based on our experience from other industries, we recommend that also the utility market embrace an open competitive HUB model. The regulator should define a set of rules for the market to comply, but let the competitive market forces drive innovation and implementation for efficient HUB operations.

KS Bedrift Energi og Defo

When the electronic billing gets more common, there will not be the same need for simplicity

29

5 Annex

5.1 Questionnaire:

30

31

NordREG c/o Danish Energy Regulatory Authority Nyropsgade 30 DK-1780 Copenhagen V Denmark Telephone: (+45) 72 26 80 70 Telefax: (+45) 33 18 14 27 E-mail: [email protected] Internet: www.nordicenergyregulators.org