blades cases.docx

TRANSCRIPT

Blades, Inc. Case

Chapter Two

1. A higher level of inflation in Thailand would most likely affect Blades in a positive

manner. Generally, if a country’s inflation increases it drives the consumers and

corporations of that country to buy more goods overseas, thus Blades’ sales should

2. Anticipated inflation favors Blades. If the inflation in Thailand increases both, the U.S.

and Thailand firms would be forced to raise their prices in order to maintain the profit

margin. Since Blades’ cost of goods sold in Thailand is relatively small, it should not be

affected as much by the inflation. This means that Blades should not have to raise prices

as much as the competitors, putting Blades in a favorable position.

3. Decreasing level of national income in Thailand would negatively impact Blades. Local

consumers will have less money to spend. In addition, because Blades’ product is not

a necessity but a leisure-product, the demand for it will drastically decrease. There is

also a chance that the importer may terminate the future arrangements due to the poor

4. Continued depreciation in baht would negatively impact Blades because Blades invoices

its product in this currency. Baht denominated revenue will consequently be converted

in fewer U.S. dollars. However, the demand for Blades products might be positive in

comparison to the U.S. competitors in Thailand. The U.S. competitors that export their

roller-blades to Thailand invoice their products in the U.S. dollars. In order to pay for the

dollar denominated products the importers will have to convert more baht to dollars, thus

making demand for Blades’ products increase in comparison to the U.S. competitors.

Blades, Inc.

Case 5

1. The possible options are: 1) Option 1 with the exercise price of $0.00756; the exercise

price is 5% above the spot rate; pay the premium that has increased to 2% of the exercise

price (the option premium is higher than what the company desires to pay). 2) Option 2

with the exercise price of $0.00792; exercise price is 10% above the spot rate; pay the

premium of 1.5%. From the given choices one can see that the tradeoff exists between

paying a higher premium or a higher exercise price. In my opinion, Blades should choose

option 1. Paying a higher exercise price limits the cause of a hedge. In addition, it would

benefit Blades more to pay a premium of $1,890 in order to limit the payables to $94,500.

2. In my opinion it should not. Given the historical data that suggests that there will most

likely be a decrease in a current spot rate, the volatile movements, and the recent event

that caused uncertainty about the yen’s future value, it would be vise to hedge. Another

alternative would be to consider future contracts. This is viable because the spot rate or

the futures rate of the yen did not change after the event. Blades can lock in its future

payment at the price same as before the event.

3. $0.006912. The futures rate is equal to the expected spot rate at the delivery date.

4. The best choice would be to buy a futures contract. The cost on the delivery date is the

same as remaining unhedged and it equals $86,400, however, not hedging in this case, is

not as logical option because of the possible yen fluctuation between the order date and

the delivery date. Given the other things remain constant this is the most cost efficient

solution (see spreadsheet).

Question 4

Remain unhedgedamount in yen 12,500,000expected spot rate 0.006912cost after 2 months 86,400

Buy one futures contractamount in yen 12,500,000futures price per yen 0.006912cost after 2 months 86,400

Buy two options Option 1 Option 2amount in yen 6,250,000 6,250,000exercise price 0.00756 0.00792premium per yen 0.0001512 0.0001134

2 x Option 1 2 x Option 2Options 1 & 2

Total premium in yen 1,890 1,417.50 1653.75exercise price 86,400 86,400 86,400cost after 2 months 88,290 87,817.50 88,053.75

Question 6Expected spot rate 0.006912

Remain unhedged Standard deviation 0.0005

amount in yen 12,500,000Spot rate 2 S.D. increase

0.007912

expected spot rate 0.007912cost after 2 months 98,900

Buy one futures contractamount in yen 12,500,000futures price per yen 0.006912cost after 2 months 86,400

Buy two options Option 1 Option 2amount in yen 6,250,000 6,250,000exercise price 0.00756 0.00792premium per yen 0.0001512 0.0001134

2 x Option 1 2 x Option 2Options 1 & 2

Total premium in yen 1,890 1,417.50 1653.75exercise price 94,500 98,900 96,700cost after 2 months 96,390 100,317.50 98,353.75

Blades, Inc.

Case 8

1. The inflation-exchange relationship can be found in the PPP theory. The theory

suggests that the currency of the country with the higher inflation rate should

depreciate to compensate the inflation differential. High levels of inflation in

Thailand should cause baht to depreciate since it is a freely floating currency.

Because of the export deal Blades has struck, it is unable to alter its prices so they

go in line with the level of inflation. Therefore Blades’ revenue would be negatively

affected. Blades’ costs will increase as Thai exporters adjust their prices to inflation.

Blades exports are baht-denominated thus baht depreciation will lead to a conversion

of baht into fewer dollars. However, according to the PPP the baht depreciation

should counter high levels of inflation therefore creating an impact on the high prices.

The net effect of this relationship on Blades is negative.

2. Factors that prevent PPP from occurring in the short run are: relative interest rates,

government regulations, national income, lack of proper substitute products, etc.

The reason being is that the exchange rates are impacted by factors other than the

inflation. PPP will not hold if countries negotiate trade arrangements under which

they commit themselves to the purchase or sale of a fixed number of goods over a

specified period of time. At lest it will not hold in the short run. The logic behind

this statement is that there will be a setback on the impact of inflation, and thus

the exchange rates because of the committed trade arrangements that are not easily

terminated due to the legal power of a contract.

Blades, Inc.

Case 9

1. There are several ways Blades can benefit. Blades generates baht-denominated cash

inflows and then converts them to U.S. dollars. Forecasting the exchange rate may allow

Blades to make hedging decisions. Furthermore, it is mentioned that Blades may establish

a subsidiary in Thailand. If this was to happen, profits earned by this subsidiary will be

in baht. These earnings will then be sent back to the parent or reinvested in Thailand. In

both scenarios forecasting exchange rate is vital for company’s future.

2. A market-based forecast is the easiest to use because it is based on either spot rate or the

forward rate. In this case it would be better to use forward rates.

3. The forward rates would yield a better market-based forecast. It is said that the available

forward rates currently exhibit a large discount, which implies higher interest rate, which

then implies higher inflation. Higher inflation is associated with a downward pressure on

the baht, which is a valid forecast. Using the present spot rate to forecast future spot rate

would mean that the value of the baht would not fluctuate, which is not likely to happen.

4.

market-based forecast -

By using the forward rate market-based forecast it is shown that baht is expected to

change by -8.70 percent. The value of the baht in 90 days according to this forecast will

-0.08696

be $0.021.

5. Weekly accuracy of technical forecast indicates market inefficiency for the baht-dollar

exchange rates. Technical forecasting involves the use of historical exchange rate data to

predict future rates and mostly apply to very shot-term periods such as one day. Given

the conditions Thailand is in, examination of past movements will not be useful for

indicating future rates.

6.

fundamental forecast -

The expected change using the fundamental forecast is -6.85 percent.

-0.0685

forecasted value of the baht -

The forecasted value of the baht using the expected value as the forecast is $.0214.

absolute error- technical forecasting -absolute error- fundamental forecasting -absolute error- market-based forecasting -

0.021425

-0.01727-0.02614-0.04545

The absolute forecast errors are as follows: technical forecasting – 1.73%; fundamental

forecasting – 2.61%; and the market-based forecast – 4.54%. Observing given forecasting

techniques and their absolute errors the conclusion arises that the most accurate technique

is the technical forecasting.

7. It will not. As mentioned earlier, technical forecasting involves the use of historical

exchange rate data to predict future rates. Examination of past movements will

most likely not be as useful for indicating future rates in Thailand. There are a lot of

uncertainties when it comes to exchange rates in this country. There is a high volatility

of the baht-dollar exchange rate. In addition, Thai economy is experiencing unfavorable

conditions that will have an affect on exchange rates.

Blades, Inc.

Case 10

1. Blades is subject to transaction and economic exposure. Transaction exposure is the

exposure of an organization’s contractual transactions to exchange rate movements.

Economic exposure is any exposure of a company’s cash flows to exchange rate

movements.

2. See attached spreadsheet.

3. It will reduce Blades’ transaction exposure. The reason being is that if the dollar revenue

is decreased due to baht depreciation, the dollar cost will also decrease due to the

depreciation of yen (Blades generates baht-denominated net inflows, but its outflows are

yen-denominated).

4. I don’t think it should. Blades’ only way of reducing its net transaction exposure lies in

importing from Japan due to the high correlation level between baht and yen. It is less

likely that the correlation between these two currencies will last for the extended period

of time. The correlation has been low in the past and will most likely return to its normal

state in the future.

5. The transaction exposure will have a slight increase. In this scenario two factors impact

transaction exposure. Firstly, Blades’ net cash inflows would be denominated in foreign

currencies driving the transaction exposure upwards. Secondly, the correlation between

baht and yen on one side, and British pound on the other, is not significantly high. This

means that changes in one currency (BP) may not drastically affect the other (baht).

Currency inflow outflow net inflow-outfllw expected exchange rateBritish pound 16,000,000 16,000,000 1.5Japanese yen 12,648,000 12,648,000 0.0083Thai baht 826,920,000 206,712,000 620,208,000 0.024

Currency net inflow-outflowpossible e.r. range from

possible e.r. range to range in U.S. $ from

British pound 16,000,000 1.47 1.53 23,520,000.00Japanese yen 12,648,000 0.0079 0.0087 99,919.20Thai baht 620,208,000 0.020 0.028 12,404,160.00

Blades, Inc.

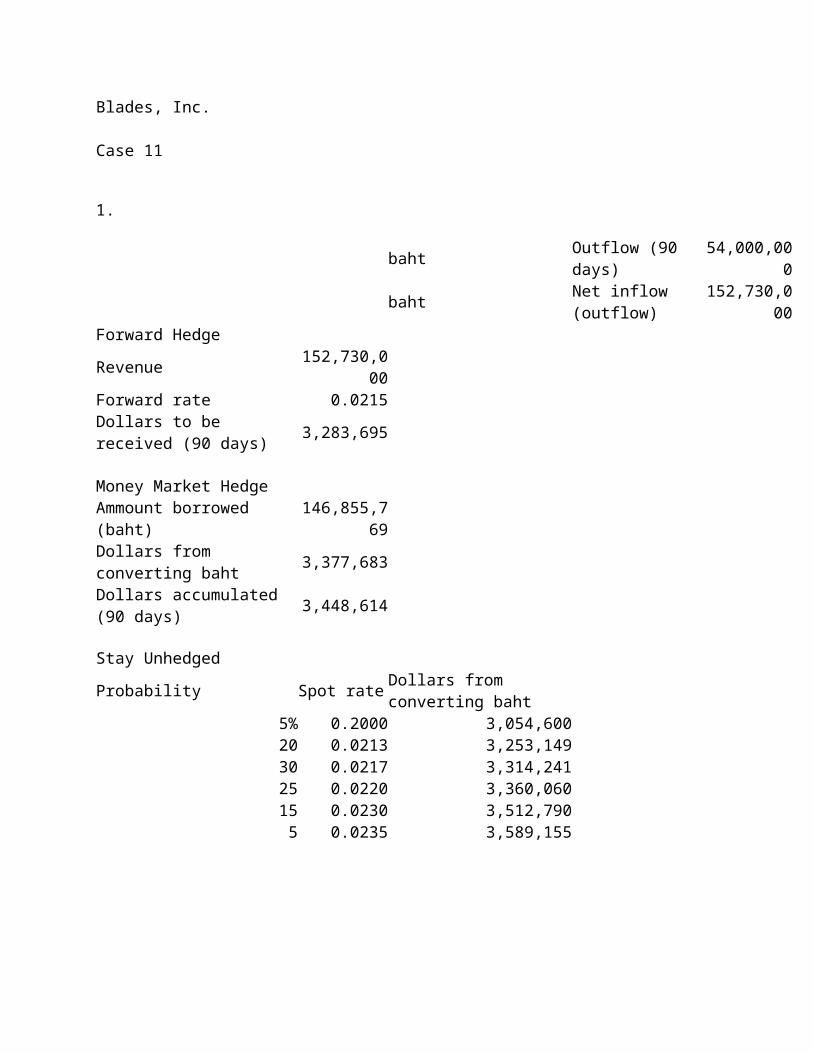

Case 11

1.

baht Outflow (90 days) 54,000,000

bahtNet inflow (outflow)

152,730,000

Forward HedgeRevenue 152,730,000Forward rate 0.0215Dollars to be received (90 days)

3,283,695

Money Market HedgeAmmount borrowed (baht) 146,855,769Dollars from converting baht 3,377,683Dollars accumulated (90 days) 3,448,614

Stay Unhedged

Probability Spot rateDollars from converting baht

5% 0.2000 3,054,60020 0.0213 3,253,14930 0.0217 3,314,24125 0.0220 3,360,06015 0.0230 3,512,7905 0.0235 3,589,155

The best option would be to use the money market hedge.

2.

BP Inflow (90 days) 4,000,000BP Outflow (90 days)

BPNet inflow (outflow)

4,000,000

Forward HedgeRevenue 4,000,000Forward rate 1.49Dollars to be received (90 days)

5,960,000

Money Market HedgeAmmount borrowed (BP) 3,921,569Dollars from converting BP 5,882,353Dollars accumulated (90 days) 6,005,882

Stay UnhedgedProbability Spot rate Dollars from converting baht

5% 1.4500 5,800,00020 1.4700 5,880,00030 1.4800 5,920,00025 1.4900 5,960,00015 1.5000 6,000,0005 1.5200 6,080,000

The best option would be to use the market hedge.

3. It is easier for Blades to hedge its inflows denominated in foreign currencies. The reason

being that Blades outflows are impacted by payables denominated in foreign currencies

and the future exchange rate, while the dollar inflows are impacted only by the exchange

rates.

4. None of the hedges would require Blades to over-hedge. In addition, Blades is not subject

to over-hedge with a money market hedge. The arrangements with Thai and British

companies are using fixed prices.

5. Blades could modify the timing in order to reduce its transaction exposure. The way

Blades can do this is by importing materials in order to manufacture 68,910 pairs of

Speedos (quarterly revenue / cost per pair of Speedos). The Thai customer can then make

a direct payment to the Thai supplier. The tradeoff of this modification is that in order to

reduce transaction exposure for this quarter, Blades sacrifices transaction exposure for the

future, making it higher. In addition, Blades will have to deal with excess inventory.

6. Blades could modify the payment practices to reduce its transaction exposure. Blades

has a policy of paying Thai imports upon a day of delivery in order to maintain a good

trade relationship. This means that Blades pays the suppliers 60 days ahead of the

allowed period. Any currency changes in this period could affect Blades. The tradeoff

would be that Blades will not be able to use baht-denominated costs to balance its baht-

denominated revenues.

7. Given all the conditions, Blades could benefit from long-term forward contracts for

both baht and BP, agree to a parallel loan, or swap currencies. The reason being is that

long-term hedging is possible for companies that can estimate their foreign currency

receivables and payables.

Blades, Inc.

Case 12

1. Blades would be negatively affected in several ways. Firstly, if the commitment is

renewed the agreed prices would be fixed. In addition, high level of inflation would

cause baht to depreciate, thus decreasing the dollars gained from baht-denominated

sales. Finally, the costs of goods sold in Thailand would be negatively impacted by the

2. With the current conditions it is less likely that Thai importer will renew its commitment.

The reason being - negative economical effects. With the high inflation and possibility

of baht depreciating, Thai customers will be less willing to spend money on leisure

products. However, if the economy returns to the high growth level, Thai importer will

more likely want to renew the deal. The importer will be confident in the future sales.

3.

0.022 0.0209 0.0198bahtSales 1.53 1.485 1.5BPU.S. 62,400,000 62,400,000 62,400,000Thai 18,192,240 17,282,628 16,373,016British 24,480,000 23,760,000 24,000,000Total 105,072,240 103,442,628 102,773,016

Cost U.S. 57,400,000 57,400,000 57,400,000Thai 5,280,000 5,016,000 4,752,000Total 62,680,000 62,416,000 62,152,000

ExpensesU.S. Fixed 2,000,000 2,000,001 2,000,002U.S. Variable 6,864,000 6,864,000 6,864,000Total 8,864,000 8,864,001 8,864,002CF before taxes 33,528,240 32,162,627 31,757,014

Blades doesn’t seam to be impacted much by the high level of economic exposure.

4.

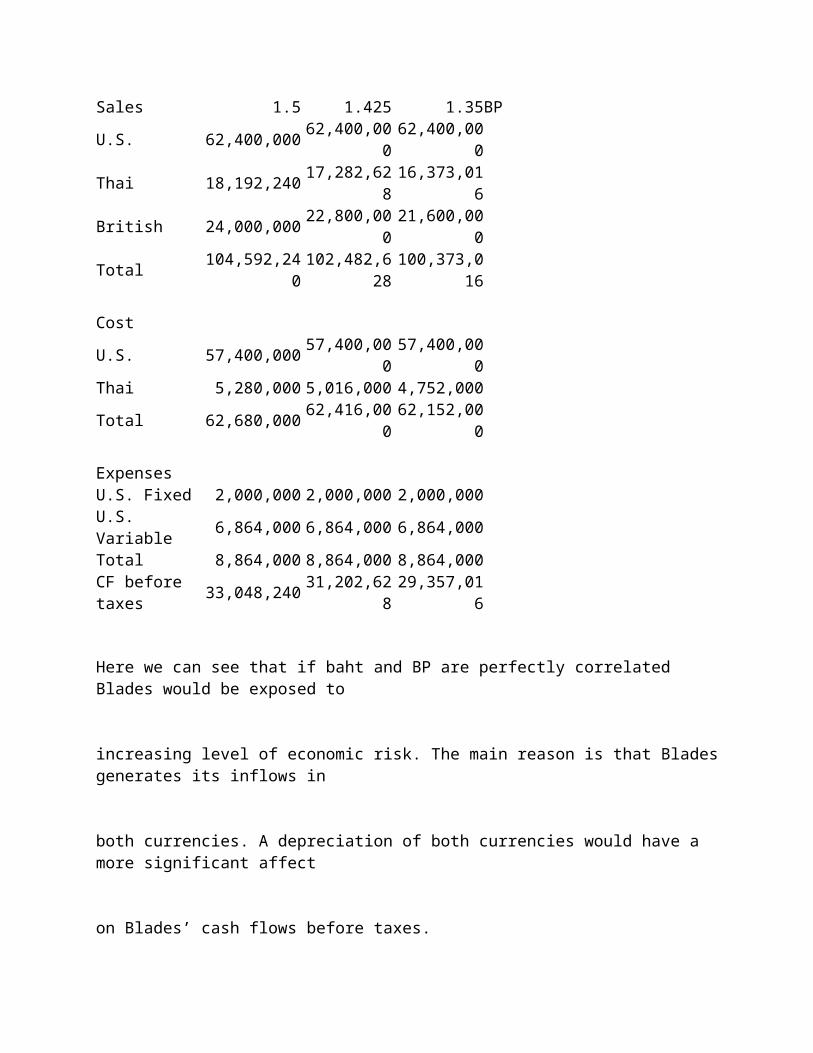

0.022 0.0209 0.0198bahtSales 1.5 1.425 1.35BPU.S. 62,400,000 62,400,000 62,400,000Thai 18,192,240 17,282,628 16,373,016British 24,000,000 22,800,000 21,600,000Total 104,592,240 102,482,628 100,373,016

Cost U.S. 57,400,000 57,400,000 57,400,000Thai 5,280,000 5,016,000 4,752,000Total 62,680,000 62,416,000 62,152,000

Expenses

U.S. Fixed 2,000,000 2,000,000 2,000,000U.S. Variable 6,864,000 6,864,000 6,864,000Total 8,864,000 8,864,000 8,864,000CF before taxes 33,048,240 31,202,628 29,357,016

Here we can see that if baht and BP are perfectly correlated Blades would be exposed to

increasing level of economic risk. The main reason is that Blades generates its inflows in

both currencies. A depreciation of both currencies would have a more significant affect

on Blades’ cash flows before taxes.

5. Blades can choose to do several things to reduce its level of economic exposure to

Thailand. One option would be to diversify the selection of countries to do business

with. By incorporating countries that have insignificant correlation to each other, Blades

reduces its economic exposure. Furthermore, Blades can engage in buying supplies in

Thailand, thus creating more cash outflows in baht. Blades could borrow in baht, pay off

baht-denominated loans, and convert baht to dollars to pay U.S. supplies. Finally, Blades

could borrow in baht, pay off baht-denominated loans, and convert baht to dollars to pay

U.S. supplies.

Blades, Inc.

Case 13

1. Given the current situation, there are several things that would factor in a positive

DFI. Firstly, Blades generates higher profit margin in Thailand. In addition, the cost of

materials is significantly cheaper in Thailand. DFI in Thailand would diversify the risk.

In other words, Blades would not be solely reliant on the U.S. economic conditions.

Finally, Blades would increase its overall market share.

2. The main tradeoff is between the initial outlay required to invest and operating under

uncertain economic conditions. If Blades was to engage in DFI now, the initial outlay

will be low. However, the primary concern is that Thai consumers have not been affected

yet by the unfavorable economic conditions, and the possibility that the economic

conditions will not improve in the future. If this was to happen, Blades would pay a price.

Nevertheless, If Blades waits one year and economy improves, the initial outlay required

would be high, and there is a change there might be heavier competition. As a financial

consultant for Blades, I would advise a scenario analysis, as well as the series of other

financial analysis (applying various ratios, etc.) prior to making this decision. Scenario

analysis would be useful because we can see the possible outcomes and the changes

for worst, best, and average situation. We could go from there. Based on the current

situation, however, I would advise Ben Holt to wait with the DFI.

3. Again the main tradeoff is profits versus the risk of poor economic conditions. If Blades

renews the agreement with the retailer for another 3 years, it will tie itself to relatively

low prices it charges the Thai retailer. If economic conditions improve, there would be

an expected increase in the demand for Blades’ products. Blades would generate higher

profit margins if decided to enter the market through the subsidiary, or construct a more

favorable deal with another retailer. On the other hand, if economic conditions continue

to worsen, the agreement would be profitable for Blades. Again I believe that a set of

financial analysis are needed prior to making this decision.

4. Given all the conditions mentioned, Thai government would have to consider the impact

of Blades subsidiary on the employment, as well as the impact of Blades subsidiary

to local businesses. Generally, Blades (and companies likes Blades) could reduce

the unemployment rate if they were to commit to employ local workers. However,

Thai government should be concerned about the local businesses. In the long run,

companies like Blades could run Thai competitors out of business, thus increasing the

unemployment even more. In reality, it all depends on the government policy to allow

foreign investments. I believe that Thai government would most likely welcome MNC’s

subsidiaries in order to deal with the unemployment in a short run. Another promising

solution would be possible mergers and acquisitions.

Blades, Inc.

Case 14

1. In the given scenario, sales from the existing agreement should not be included in the

capital budgeting analysis. The reason being is that Blades would have these sales with

or without the subsidiary in Thailand. The cost savings for the pairs not sourced from

Thailand should be included because these sales would not happen if Blades continued

to import from Thailand. Finally, the sales resulting from a renewed agreement should be

included in the capital budgeting analysis because this revenue is incremental to creating

2. See spreadsheet. Blades should establish the subsidiary in Thailand under the given

conditions. The capital budgeting analysis shows a positive NPV if Blades renews the

agreement with Entertainment Products and establishes the subsidiary

3. See spreadsheet. The capital budgeting analysis indicates that Blades should establish a

subsidiary and not renew its agreement. The NPV was $8,746,688

4. See spreadsheet. The salvage value is not that critical. The capital budgeting analysis in

question 2 is the most feasible alternative. As spreadsheet suggests (comparing question

3 and question 4), even if Blades’ salvage value is reduced to 0 (Blades does not sell the

subsidiary), the NPV remains positive.

5. See spreadsheet. The capital budgeting analysis shows a positive NPV of $5,620,315 for

the worst case scenario. Therefore, Blades should establish the subsidiary even if baht

depreciates by 5 percent annually.

Capital Budgeting Analysis PROBLEM # 2 Year 0 Year 1 Year 2 Year 3 Year 4Demand - Entertainment Products 180,000 180,000 180,000Price per unit - baht 4,594 4,594 4,594Revenue from agreement 0 826,920,000 826,920,000 826,920,000Other retailers 120,000 120,000 220,000 220,000Price per unit - baht 5,000 5,600 6,272 7,025Revenue from other retailers 600,000,000 672,000,000 1,379,840,000 1,545,420,800Total revenue 600,000,000 1,498,920,000 2,206,760,000 2,372,340,800Variable cost per unit 3,500 3,920 4,390 4,917Total variable cost 420,000,000 1,176,000,000 1,756,160,000 1,966,899,200Less: cost savings 32,400,000

Other fixed expenses 25,000,000 28,000,000 31,360,000 35,123,200Depreciation 30,000,000 30,000,000 30,000,000 30,000,000Total expenses 442,600,000 1,234,000,000 1,817,520,000 2,032,022,400EBT of susidiary 157,400,000 264,920,000 389,240,000 340,318,400Host government tax (25%) 39,350,000 66,230,000 97,310,000 85,079,600After tax earnings of subsidiary 118,050,000 198,690,000 291,930,000 255,238,800NCF to subsidiary 148,050,000 228,690,000 321,930,000 285,238,800Baht remitted by susidiary 148,050,000 228,690,000 321,930,000 285,238,800Witholding tax on remitted funds (10%)

14,805,000 22,869,000 32,193,000 28,523,880

Baht remitted after witholding taxes 133,245,000 205,821,000 289,737,000 256,714,920Salvage valueExchange rate - baht 0.02300 0.02254 0.02209 0.02165 0.02121CF to parent 3,003,342 4,546,421 6,272,057 5,446,070PV of parent CF (25% discount rate) 2,402,674 2,909,710 3,211,293 2,230,710Initial investment by parent 12,650,000Cumulative PV -10,247,326 -7,337,617 -4,126,323 -1,895,613

PROBLEM # 3 Year 0 Year 1 Year 2 Year 3 Year 4Demand - Entertainment Products 5,000 5,000 5,000Price per unit - baht 5,600 6,272 7,025Revenue from agreement 0 28,000,000 31,360,000 35,123,200Other retailers 120,000 120,000 220,000 220,000Price per unit - baht 5,000 5,600 6,272 7,025Revenue from other retailers 600,000,000 672,000,000 1,379,840,000 1,545,420,800Total revenue 600,000,000 700,000,000 1,411,200,000 1,580,544,000Variable cost per unit 3,500 3,920 4,390 4,917Total variable cost 420,000,000 490,000,000 987,840,000 1,106,380,800Less: cost savings 32,400,000Other fixed expenses 25,000,000 28,000,000 31,360,000 35,123,200Depreciation 30,000,000 30,000,000 30,000,000 30,000,000Total expenses 442,600,000 548,000,000 1,049,200,000 1,171,504,000EBT of susidiary 157,400,000 152,000,000 362,000,000 409,040,000Host government tax (25%) 39,350,000 38,000,000 90,500,000 102,260,000After tax earnings of subsidiary 118,050,000 114,000,000 271,500,000 306,780,000NCF to subsidiary 148,050,000 144,000,000 301,500,000 336,780,000Baht remitted by susidiary 148,050,000 144,000,000 301,500,000 336,780,000Witholding tax on remitted funds (10%)

14,805,000 14,400,000 30,150,000 33,678,000

Baht remitted after witholding taxes 133,245,000 129,600,000 271,350,000 303,102,000Salvage valueExchange rate - baht 0.02300 0.02254 0.02209 0.02165 0.02121

CF to parent 3,003,342 2,862,760 5,874,026 6,430,148PV of parent CF (25% discount rate) 2,402,674 1,832,167 3,007,501 2,633,788Initial investment by parent 12,650,000Cumulative PV -10,247,326 -8,415,160 -5,407,658 -2,773,870

PROBLEM # 4 Year 0 Year 1 Year 2 Year 3 Year 4Demand - Entertainment Products 5,000 5,000 5,000Price per unit - baht 5,600 6,272 7,025Revenue from agreement 0 28,000,000 31,360,000 35,123,200Other retailers 120,000 120,000 220,000 220,000Price per unit - baht 5,000 5,600 6,272 7,025Revenue from other retailers 600,000,000 672,000,000 1,379,840,000 1,545,420,800Total revenue 600,000,000 700,000,000 1,411,200,000 1,580,544,000Variable cost per unit 3,500 3,920 4,390 4,917Total variable cost 420,000,000 490,000,000 987,840,000 1,106,380,800Less: cost savings 32,400,000Other fixed expenses 25,000,000 28,000,000 31,360,000 35,123,200Depreciation 30,000,000 30,000,000 30,000,000 30,000,000Total expenses 442,600,000 548,000,000 1,049,200,000 1,171,504,000EBT of susidiary 157,400,000 152,000,000 362,000,000 409,040,000Host government tax (25%) 39,350,000 38,000,000 90,500,000 102,260,000After tax earnings of subsidiary 118,050,000 114,000,000 271,500,000 306,780,000NCF to subsidiary 148,050,000 144,000,000 301,500,000 336,780,000Baht remitted by susidiary 148,050,000 144,000,000 301,500,000 336,780,000Witholding tax on remitted funds (10%)

14,805,000 14,400,000 30,150,000 33,678,000

Baht remitted after witholding taxes 133,245,000 129,600,000 271,350,000 303,102,000Salvage valueExchange rate - baht 0.02300 0.02254 0.02209 0.02165 0.02121CF to parent 3,003,342 2,862,760 5,874,026 6,430,148PV of parent CF (25% discount rate) 2,402,674 1,832,167 3,007,501 2,633,788Initial investment by parent 12,650,000Cumulative PV -10,247,326 -8,415,160 -5,407,658 -2,773,870

PROBLEM # 5 Year 0 Year 1 Year 2 Year 3 Year 4Demand - Entertainment Products 5,000 5,000 5,000Price per unit - baht 5,600 6,272 7,025Revenue from agreement 0 28,000,000 31,360,000 35,123,200Other retailers 120,000 120,000 220,000 220,000Price per unit - baht 5,000 5,600 6,272 7,025Revenue from other retailers 600,000,000 672,000,000 1,379,840,000 1,545,420,800

Total revenue 600,000,000 700,000,000 1,411,200,000 1,580,544,000Variable cost per unit 3,500 3,920 4,390 4,917Total variable cost 420,000,000 490,000,000 987,840,000 1,106,380,800Less: cost savings 32,400,000Other fixed expenses 25,000,000 28,000,000 31,360,000 35,123,200Depreciation 30,000,000 30,000,000 30,000,000 30,000,000Total expenses 442,600,000 548,000,000 1,049,200,000 1,171,504,000EBT of susidiary 157,400,000 152,000,000 362,000,000 409,040,000Host government tax (25%) 39,350,000 38,000,000 90,500,000 102,260,000After tax earnings of subsidiary 118,050,000 114,000,000 271,500,000 306,780,000NCF to subsidiary 148,050,000 144,000,000 301,500,000 336,780,000Baht remitted by susidiary 148,050,000 144,000,000 301,500,000 336,780,000Witholding tax on remitted funds (10%)

14,805,000 14,400,000 30,150,000 33,678,000

Baht remitted after witholding taxes 133,245,000 129,600,000 271,350,000 303,102,000Salvage valueExchange rate - baht 0.02300 0.02185 0.02076 0.01972 0.01873CF to parent 2,911,403 2,690,172 5,350,920 5,678,205PV of parent CF (25% discount rate) 2,329,123 1,721,710 2,739,671 2,325,793Initial investment by parent 12,650,000Cumulative PV -10,320,877 -8,599,167 -5,859,496 -3,533,703

Blades, Inc.

Case 15

1. See spreadsheet. Blades should choose to establish a subsidiary in Thailand. The

NPV with acquisition would be $6,641,949. The NVP without the acquisition results

$8,746,668. Therefore, $8,746,668 - $6,641,949 = $2,104,739.

2. See spreadsheet. Blades should reduce the purchase price by $2,104,739 / $0.023 =

$91,510,391. Therefore, the maximum amount Blades should be willing to pay is

$1,000,000,000 - $91,510,391 = $908,489,609 baht.

3. Blades should consider several factors. The price asked for the Skates’n’Stuff is lower

in comparison to the capital budget analysis. Blades should find out why the company is

being sold for that price. In addition, Blades should also look into the acquisition of an

existing business in Thailand. Getting to know the local market is essential. Moreover,

the information I was provided with may be inaccurate. If that is the case the capital

budgeting analysis would be inaccurate. Another important factor is the quality of

roller blades and the production process. The lower quality roller blades produced by

Skaters’n’Stuff may jeopardize Blades’ reputation. Finally, there might be issues with

management if the acquisition happens. Blades would have to make sure that the right

people are “on the bus.” This may lead to a mass layoff.

Capital Budgeting Analysis Year 0 Year 1 Year 2 Year 3 Year 4

Demand - retailers 280,000 280,000 280,000 280,000 280,000Price per unit - baht 4,500 5,040 5,645 6,322

Revenue from retailers 1,260,000,000 1,411,200,000 1,580,544,000 1,770,209,280 1,982,634,394Total revenue 1,260,000,000 1,411,200,000 1,580,544,000 1,770,209,280 1,982,634,394Variable cost per unit 3,500 3,920 4,390 4,917Total variable cost 980,000,000 1,097,600,000 1,229,312,000 1,376,829,440 1,542,048,973Less: cost savings 32,400,000 32,400,000Other fixed expenses 20,000,000 22,400,000 25,088,000 28,098,560 31,470,387Depreciation 60,000,000 60,000,000 60,000,000 60,000,000 60,000,000Total expenses 1,027,600,000 1,147,600,000 1,314,400,000 1,464,928,000 1,633,519,360EBT of susidiary 232,400,000 263,600,000 266,144,000 305,281,280 349,115,034Host government tax (25%) 58,100,000 65,900,000 66,536,000 76,320,320 87,278,758After tax earnings of subsidiary 174,300,000 197,700,000 199,608,000 228,960,960 261,836,275NCF to subsidiary 234,300,000 257,700,000 259,608,000 288,960,960 321,836,275Baht remitted by susidiary 234,300,000 257,700,000 259,608,000 288,960,960 321,836,275Witholding tax on remitted funds (10%) 23,430,000 25,770,000 25,960,800 28,896,096 32,183,628Baht remitted after witholding taxes 210,870,000 231,930,000 233,647,200 260,064,864 289,652,648Salvage valueExchange rate - baht 0.02300 0.02254 0.02209 0.02165 0.02121CF to parent 4,850,010 5,227,702 5,161,080 5,629,732 6,144,827PV of parent CF (25% discount rate) 4,850,010 4,182,162 3,303,091 2,882,423 2,516,921Initial investment by parent 23,000,000Cumulative PV -18,149,990 -13,967,828 -10,664,737 -7,782,314 -5,265,393