blch41 financial markets financial markets refer to the market and to the market. new variable...

Post on 20-Dec-2015

221 views

TRANSCRIPT

BlCh4 1

Financial Markets

• Financial markets refer to the market and to the market.

• New variable considered:• Goals of the chapter:

– To find how in these markets.

– To find how to influence the interest rate.

– To introduce the link between the financial and the goods markets.

BlCh4 2

Money versus bondsThere are many forms of financial assets,

from cash to shares.In this chapter we only consider 2 forms•

– the liquid form– which does not earn – which is used for – and is defined as

• – a liquid form– which earn– which are not used for– and bonds somehow stand for all the other less liquid forms.

BlCh4 3

• Question:

wealth can be held

either in bonds

or in money

in what proportion will it be?

BlCh4 4

Main variables affecting the decision

1. – The higher ,– the the need for money,

but there is a cost in holding money instead of bonds as money does not earn interest

2. – the higher ,– the more it is to hold wealth in the form

of bonds rather than money.

BlCh4 5

The demand for money Md

• The amount of money needed for transaction depends on (i.e. on income).

• The opportunity cost of holding money instead of interest bearing bonds depends

• so

€

Md =

BlCh4 6

The demand for money - graphEffect of an increase in Y or in P

i

M

Inversely related to the rate of interest.

An increase in Y or in P results in a rightward shift of the curve.

BlCh4 7

The demand for bonds Bd

• It is related to the demand for money through

W (note that all these variables are nominal)

So Bd =

• It follows that (ceteris paribus):– If W increases, Bd by the amount– If PY increases, Md and Bd – If i increases, Bd and Md

BlCh4 8

Determination of the interest rate• Since the interest rate can be considered

it can be determined like any other price on the money market.• However as money is defined as 1.

2. there are 2 suppliers: 1.

2.

BlCh4 9

Problem 2: wealth W = $50,000 - income Y = $60,000

Money demand is Md = PY(.35 - i) with P = 1

a. When i = 5%

Md = = and Bd = W - Md =

When i = 10% Md = and Bd =

b. Md when i and Bd when i

c. i = 10% and Y2 = .5Y1 = $30,000

Since Md is proportional to Y we have Md2 = .5Md

1 =

d. i = 5% same story

e. Independent of i (at every level of i, the money demand will be halved)

BlCh4 10

• To simplify, we assume at first that currency is the only form of money and the Fed, the only supplier.

• In the second part of the chapter, the role of the commercial banks in creating money in the form of deposits will be explained.

BlCh4 11

Supply of money Ms

The Fed determines the amount of money Ms

(central bank currency in this section) it supplies to the economy.

So the level of the money supply does not depend

M

i

BlCh4 12

Equilibrium in the financial markets

• If the money market is in equilibrium, the bonds market

• Proof: W So W = When the money market is in equilibrium,

so in this case • As a result we need only focus on one

market equilibrium, the money market,

BlCh4 13

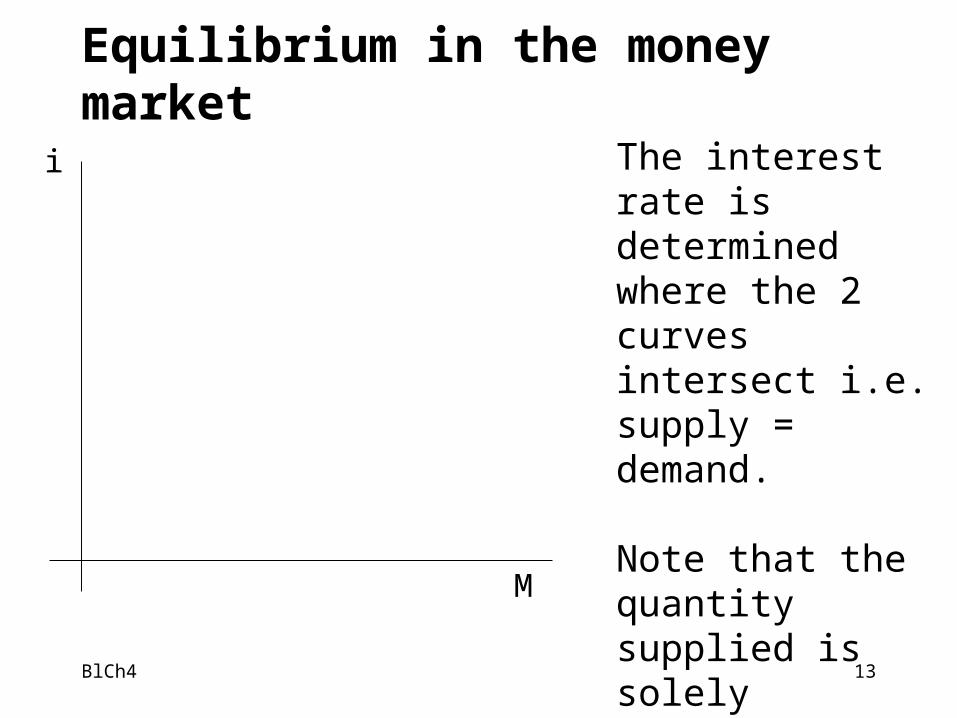

Equilibrium in the money market

i

M

The interest rate is determined where the 2 curves intersect i.e. supply = demand.

Note that the quantity supplied is solely determined by the Fed and not by the equilibrium supply/demand.

BlCh4 14

Shifts in the demand for money

i

M

An increase in P or in Y, results in a shift of the demand curve to the right and an increase in the equilibrium interest rate. There is no change in supply, but the public needs more money for transaction and bid up the price of money i.

BlCh4 15

Shifts in the supply of money

i

M

An increase in the money supply - due to expansionary monetary policy - results in a rightward shift of the Ms curve and a drop in the equilibrium interest rate i

BlCh4 16

Problem #4 Md = PY(.25 - i) with P = 1 and Y = $100

and Ms = $20

a. In equilibrium Md = Ms i.e.

or 25 - 20 = 100i i = 5/100 =

b. If the Fed wants to increase i by 10 percentage points to 15%, it must the money supply to:

Md = (or by 20 - 10 = 10)

BlCh4 17

Velocity of money

• Definition: V =

• PY is output - it is a

• M is the money supply - a

• If PY = and M = i.e. we only have one bill, we will have to use the same bill times to buy all the goods corresponding to PY during the year, so the velocity of money is .

BlCh4 18

Velocity cont.

• It seems that the velocity of money has increased historically: i.e. we need less cash in hand to buy the same amount of goods.

• This is due to innovations in the financial markets (ATM, credit cards etc.)

• Empirical studies also show a positive relation between velocity and interest rates.

BlCh4 19

Open market operations

• The Fed can affect the quantity of money in the economy

• When the Fed wants to increase Ms,

• When the Fed wants to cut Ms, it (old) bonds from its bonds holdings to the public and money from the public: (i.e. money is taken out of circulation).

BlCh4 20

The Fed’s balance sheet

Assets Liabilities

BlCh4 21

The Fed’s balance sheetOpen market purchase

Assets Liabilities

BlCh4 22

Relation between the price of bonds and the interest rate

• Let’s consider a 1 year Treasury Bill that promises a $100 payment (its face value) at maturity.

• PB is the price paid for the bond now.

• The rate of return on the bond, i.e. the

interest rate is

• This is indeed an relation between the price of the bond and the interest rate.€

i =

BlCh4 23

Illustration

PB i

$90 %

$80 %

$70 %€

i =$100 − PB

PB

or

€

PB =$100

1+ i

BlCh4 24

Rational

• If the interest rate on newer bonds is higher, people will sell their old bonds to take advantage of the better returns and by doing so they will depress the prices overall on the bond market.

BlCh4 25

Monetary policy

• Expansionary: Open market (MS )

The Fed bonds:

PB as the demand for bonds Bd

so i

• Contractionary: Open market (MS ) The Fed bonds:

PB as the supply of bonds Bd

so i

BlCh4 26

Interest Rate determination w/ Ms = CU + D• Let’s now assume that

Money = currency + deposit

• Role of commercial banks: financial intermediaries

– Banks receive funds from the public that they use to make loans or to buy government bonds

– Public depositing own funds at banks can use these bank balances to write checks used to make payments

• Funds in form of checkable deposits are money

BlCh4 27

• Banks must also hold reserves so that they are always able to meet demand (flows in and out not necessarily equal on a daily basis)– By law banks must hold a specific

proportion (10%) of the total deposits in an account at the Fed

BlCh4 28

Balance sheets of Fed and of commercial banks

Assets Liabilities Assets Liabilities

Fed Commercial banks

=

BlCh4 29

Supply and demand for CB money H

• Supply H : determined by • Demand Hd: demand for and for • S=D determine the equilibrium interest rate iDemand for money derived above as Md=

corresponds to We need to know what how much is held as CU and how

much as D or proportion c held as CUIn the US: c =

So demand for currency: CUd = demand for deposits: Dd =

BlCh4 30

Demand for reserves Rd depends on reserve ratio requirement as R =

-Let’s replace D by -

demand for reserves: Rd =

Finally the demand for CB money H is

Hd =

= =

=

BlCh4 31

Interest rate determination

• In equilibrium H = i.e. H = Case 1: people only hold CU so c = 1Equilibrium i determined by H =

-earlier case: no money creation-Case 2: people only hold deposits so c = 0Then H = and H represents of total money supply

BlCh4 32

• In general we have 0 < c < 1 and H represents between 10 % and 100% of the total money in the economy.

•If either P or Y increase, the impact on Hd is the same as the impact on Md

i

H

Hd=Cud+Rd=[c + (1-c)]PYL(i)

BlCh4 33

Money multiplier mm

• We derived H = [c + (1-c)]M

with c = CUd/M and = R/D

so mm = =

If c = 40% and =10%

the money multiplier is ---------------- = 2.17

BlCh4 34

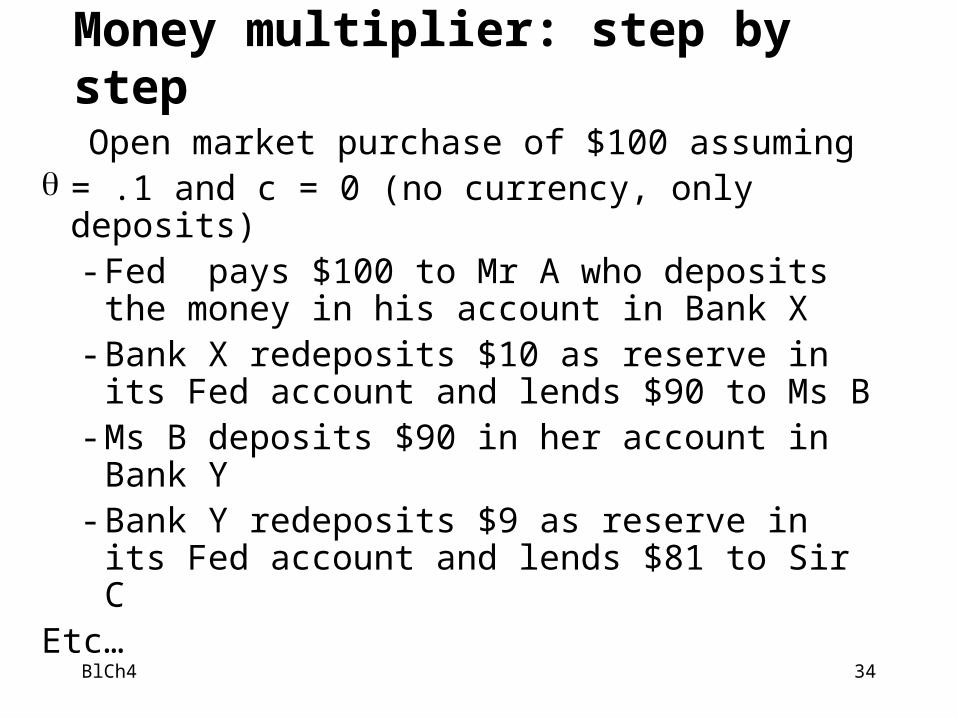

Money multiplier: step by step

Open market purchase of $100 assuming = .1 and c = 0 (no currency, only deposits)

- Fed pays $100 to Mr A who deposits the money in his account in Bank X

- Bank X redeposits $10 as reserve in its Fed account and lends $90 to Ms B

- Ms B deposits $90 in her account in Bank Y- Bank Y redeposits $9 as reserve in its Fed

account and lends $81 to Sir CEtc…

BlCh4 35

How much money has been added in the economy up to now?

$100 +

Total increase in the money supply is:

100 = 100

= 100

Fed Comm. Banks A L A L

BondsReserves

Loans

Reserves

Deposits