bloomberg exercises for investments and … · bloomberg exercises for investments and financial...

TRANSCRIPT

BLOOMBERG EXERCISES FOR INVESTMENTS AND

FINANCIAL MARKET CLASSES

R. Stafford Johnson

Department of Finance

Xavier University

William College of Business

3800 Victory Parkway

Cincinnati, Ohio 45207

513-745-3108

Submitted for possible presentation at the 2014 Financial Management Association Annual Meeting

1

BLOOMBERG EXERCISES FOR INVESTMENTS AND

FINANCIAL MARKET CLASSES

INTRODUCTION

Today, Bloomberg terminals are becoming more common in universities where they are used for

research, teaching, and managing student investment funds. Given the breadth and depth of

information and analytics provided by Bloomberg, finance professors are faced with the

challenge of how best to incorporate Bloomberg into their classes. For professors whose students

have accessed to Bloomberg terminals, one way to include Bloomberg as part of the pedagogy is

with exercises related to the subject matter that can also explain how to use the Bloomberg slide.

The purpose of this paper is to share a sample of Bloomberg exercises that have been

developed and used by the author in his investment, fixed-income, financial markets, and

derivative classes. Part 1 of the paper shows a sample of take-home questions used in an

investment and portfolio management class in which the students were asked to write essays and

also conduct Bloomberg projects associated with each essay question. The essay/Bloomberg

projects covered subjects related to portfolio ranking, Markowitz portfolio analysis, APT, equity

style investment, portfolio insurance, market timing, and ETF constructions. Part 2 of the paper

shows a sample of essay/Bloomberg project questions used in the investment and portfolio class

and also a fixed-income and debt markets class. The questions covered subjects related to

estimating bonds spreads, total return analysis, the relationship between CDS spreads, default

probabilities, and credit spreads, equilibrium bonds prices and strip securities, yield curve shifts

and strategies, horizon analysis, bond duration, and managing a bond portfolio’s duration using

interest rate swaps. The paper presents samples of Bloomberg slides that students are expected to

turn in and also place on their Bloomberg Launchpad. In addition to the Essay/Bloomberg

2

projects, an extensive number of Bloomberg exercises used in the investment and portfolio

management, fixed-income, and derivative classes are also included in the appendix.

I. PORTFOLIO ANALYSIS:

1. Essay: Explain how the following parameters are used for analyzing a stock or portfolio:

Coefficient of determination

Beta

Convexity: Beta+ and Beta−

Alpha

Bloomberg Part: Use Bloomberg’s Beta and PC screens to evaluate a stock in terms of

these parameters.

Sample:

Linear regressions for the Disney Corporation and General Electric are shown in Exhibit 1. Both

regressions were done on Bloomberg’s “Beta” screen. In each regression, the stock’s daily

percentage returns are regressed against the percentage changes in the S&P 500 (SPX) for the

period from 5/1/06 to 4/28/11. The Beta screen shows the scatter diagram, regression estimates,

and qualifiers. From this regression, Disney has a beta 1.067, alpha of .040, σ(ε) of 1.193 (V(ε) =

1.42325), t-statistic = β/ σ(β) = 50.04, and R2 of .6667:

GE has a beta 1.158, alpha of –.029, σ(ε) of 1.663 (V(ε) = 2.7656), t-statistic = β/ σ(β) =

38.941, and R2 of .547:

42325.1)R(V)067.1()r(V

)(V̂)R(Vˆ)r(V

)R(E067.1040.)r(E

)R(Eˆˆ)r(E

M2

M2

M

M

3

Given the betas of GE and Disney, the covariance formula for these stocks based on the

estimated regression equation is

)R(V)158.1)(067.1()rr(Cov

)R(V)rr(Cov

M21

M2121

From the regression, alpha can be used as a measure of the stock’s return above or below its

market risk-adjusted return—abnormal return. That is, if the intercept is positive it suggests the

stock is generating a return in excess of the market risk premium. For example, a stock with a beta

of one and an alpha of zero, would increase by 10% when the market is up by 10% and decrease by

10% when the market is down by 10%. Its return, matches the return in the market. If the stock had

a beta of one and an alpha of .02 (or 2%), then it would increase by 12% when the market increases

by 10% and decrease by only 8% when the market decreases by 10%. Its return is always 2%

better than the market return. The alpha for the Disney stock shown in Exhibit 2 is a positive 0.04,

whereas the alpha for GE is –0.029. It should be noted that with a portfolio it is possible to

diversify away firm and industry risk. If this is the case, then a portfolio with a positive alpha would

be providing its investors with an excess or abnormal return.

The security’s adjusted beta shown is derived using a Bayesian approach in which the

historical beta is modified by moving the regression beta (raw beta) toward the market average.

The adjusted beta for Disney is 1.045 compared to its historical or raw beta of 1.067 and the

adjusted for GE is 1.105 while its raw beta is 1.158.

The Beta+, Beta

+ and convexity for Disney and GE calculated from the previous

regression period are shown in Exhibit 2. As shown, Disney has a Beta+ of 1.161 and Beta

+ of

.98 and convexity of .090. The stock is more responsive when the market increases than when it

decreases—increasing 1.161% for a 1% increase in the market, while decreasing by 0.98% for a

1% decrease in the market. Thus, it has greater gain to loss relation or a positive convexity. In

contrast, GE has a Beta+ of 1.089 and Beta

+ of 1.222 and a convexity of –.067. The stock is more

responsive when the market decreases than when it increases—decreasing 1.222% for a 1%

decrease in the market, while increasing by 1.089% for a 1% increase in the market. It has

greater loss to gain relation or a negative convexity.

7656.2)R(V)158.1()r(V

)(V̂)R(Vˆ)r(V

)R(E158.1029.)r(E

)R(Eˆˆ)r(E

M2

M2

M

M

4

Exhibit 3 shows a comparison of the R2’s or systematic risk measures, Betas, and alphas for

GE and related companies in its industry taken from Bloomberg’s PC screen. Based on its R2,

approximately 50% of GE’s variability is explained by market factors. This is similar to the R2’s of

its peers. GE’s beta of 1.254 exceeds the beta of most of its peers, with the exception being

Caterpillar and Abbot Labs. Finally, GE is only one of two in the peer group with a negative alpha

for the regression period analyzed.

Exhibit 1: Disney and GE Regressions from Bloomberg’s Beta Screen

Exhibit 2: Disney and GE Beta+ and Beta

– and Convexity

from Bloomberg’s Beta Screen

BETA Screen, Beta+ and Beta

– and Convexity

5

Exhibit 3: Comparison of Systematic Risk (R2), Betas, and Alphas

for GE and its Peers: Bloomberg’s PC Screen

6

2. Essay: Explain intuitively and with an example the borrowing and lending line. Explain how

the borrowing and lending line is a good objective measure for ranking portfolios. Explain

the other measures for ranking portfolios.

Bloomberg Part 1

Use the FMA screen to identify several equity funds

Select one of the funds and study it using the PORT screen

Using your selected fund’s RV screen, compare the fund with other similar funds

in terms of Sharpe, Treynor, and Jensen ranking indexes (on the yellow RV

screen, type in Sharpe, Treynor, and Jensen to create a column for each.

Alternatively, you can use the performance measures found on PORT.

Bloomberg Part 2: Select a portfolio you have constructed from one of the class

exercises or one of your group’s portfolios and compare its performance. Use PORT,

HRA (put portfolio in CIXB basket), and COMP. Explain the features of your portfolio

(sector allocation, dividend yield, debt/equity, etc.) relative to the S&P 500.

Sample Screens for XSIF Fund:

Exhibit 4: PORT Screens for a Xavier Student Equity Investment Fund (XSIF Equity)

7

8

3. Essay: Explain the Elton, Gruber, Padberg, and Manfred technique for determining the best

efficient portfolio.

Bloomberg Part: Explain the Markowitz/Bloomberg Excel. Use the Markowitz Excel

portfolio to determine the best efficient portfolio for a portfolio you have constructed.

Sample

The Markowitz Excel Program determines the portfolio allocations using the Elton, Gruber,

Padberg, and Manfred technique for a portfolio imported from the Bloomberg PRTU screen. Using

the “Markowitz” Excel program, one can import the names of the stocks in a portfolio created in

PRTU into the program. The user can then select a risk-free rate from a dropdown, an index (S&P

500 or Dow Jones), a regression time period, and a length of period (daily or weekly). The program

then calculates i, i, and V(i), and then each stock’s E(ri) and V(ri), and j based on the average

market return and variability or the user’s inputted values for E(RM

) and V(RM

). The user can also

elect to used Bloomberg’s adjusted beta or the regression beta (raw beta). Calculation Sheet 2 of the

Excel program shows each stocks parameter values in the order of their j’s and the Elton,

Gruber, Padberg, and Manfred parameter calculations of Ci, C*, and optimum weights. Exhibit 5

shows a Bloomberg PRTU slide of a 10-stock portfolio, the input page of the Excel program where

the S&P 500, 5-year Treasury, and a weekly time period from 3/24/2008 to 5/16/2011 were selected

for the regressions, and (3) the Calculation Sheet 2 where the allocations for the portfolio are shown.

9

Exhibit 5: Bloomberg and Markowitz Excel Program Using

Elton, Gruber, Padberg, and Manfred Technique for Determining Allocation

Rf 5 Y Treas

Rm Index SPX

Start date 3/24/2008

Ending date 5/16/2011

Daily or weekly w

Beta Type raw beta

Relativev Index SPX

Start date 3/24/2008

Ending date 5/16/2011

Daily or weekly w

Import Data Type Portfolio portfolio_members

ID or Name u5945505-40 u5945505-40 client

Error Check

Stock j No. Ticker Ticker Name

Included in

Portfolio? Weight

1 APC UN Equity APC UN Equity ANADARKO PETROLEUM CORP Yes 1.7%

2 CAT UN Equity CAT UN Equity CATERPILLAR INC Yes 6.5%

3 CBG UN Equity CBG UN Equity CB RICHARD ELLIS GROUP INC-A Yes 5.4%

4 COF UN Equity COF UN Equity CAPITAL ONE FINANCIAL CORP Yes 2.7%

5 DHR UN Equity DHR UN Equity DANAHER CORP Yes 22.4%

6 DIS UN Equity DIS UN Equity WALT DISNEY CO/THE Yes 7.5%

7 IBM UN Equity IBM UN Equity INTL BUSINESS MACHINES CORP Yes 33.9%

8 SO UN Equity SO UN Equity SOUTHERN CO Yes 7.8%

9 UTX UN Equity UTX UN Equity UNITED TECHNOLOGIES CORP Yes 5.5%

10 V UN Equity V UN Equity VISA INC-CLASS A SHARES Yes 6.6% Stock j No. Ticker Name E(Rj) Bj V(ej) Rf V(Rm) Lambda B Wi

1 CBG UN Equity CB RICHARD ELLIS GROUP INC-A 76.05 2.31 96.21 1.72 2.47 32.20 5.4%

2 IBM UN Equity INTL BUSINESS MACHINES CORP 27.03 0.83 4.96 1.72 2.47 30.67 33.9%

3 DHR UN Equity DANAHER CORP 25.80 0.82 6.80 1.72 2.47 29.48 22.4%

4 V UN Equity VISA INC-CLASS A SHARES 23.32 0.86 15.98 1.72 2.47 25.19 6.6%

5 SO UN Equity SOUTHERN CO 10.42 0.36 5.14 1.72 2.47 24.41 7.8%

6 COF UN Equity CAPITAL ONE FINANCIAL CORP 52.08 2.15 78.82 1.72 2.47 23.45 2.7%

7 CAT UN Equity CATERPILLAR INC 32.29 1.46 13.79 1.72 2.47 20.93 6.5%

8 DIS UN Equity WALT DISNEY CO/THE 23.62 1.09 7.24 1.72 2.47 20.15 7.5%

9 APC UN Equity ANADARKO PETROLEUM CORP 31.19 1.59 25.12 1.72 2.47 18.56 1.7%

10 UTX UN Equity UNITED TECHNOLOGIES CORP 19.27 0.95 4.57 1.72 2.47 18.53 5.5%

Beta Start Date 20080324

Beta End Date 20110516

Beta Relativev Index SPX

Beta Periodcity w

Name Adjusted Beta Raw Beta

Standard

Deviation of Error ALPHA (Intercept)

R^2

(Correlation^2)

ANADARKO PETROLEUM CORP 1.392147062 1.588241476 0.111023721 0.272643652 0.559682416

CATERPILLAR INC 1.307338932 1.461028008 0.082263808 0.290596305 0.662068159

CB RICHARD ELLIS GROUP INC-A 1.8724587 2.308716137 0.217300921 0.714148496 0.412151833

CAPITAL ONE FINANCIAL CORP 1.764712009 2.147094484 0.196682042 0.477093648 0.425352247

DANAHER CORP 0.877905602 0.816871572 0.057750788 0.236247798 0.554108637

WALT DISNEY CO/THE 1.058153863 1.087246667 0.059599815 0.210065613 0.673948481

INTL BUSINESS MACHINES CORP 0.883583667 0.825388754 0.049325242 0.248463499 0.634931637

SOUTHERN CO 0.571130539 0.356704375 0.050201951 0.090110608 0.238722267

UNITED TECHNOLOGIES CORP 0.964823612 0.94724989 0.04734542 0.168871566 0.713160019

VISA INC-CLASS A SHARES 0.905104768 0.857670728 0.088551684 0.210793692 0.368155804

10

4. Essay: Explain the APT by comparing it to the CAPM. Describe how factor models like the

RAM model are used for constructing portfolios

Bloomberg Part: Use the MRA screen to run a multiple regression of the returns of a

portfolio you have formed. For your dependent variable, use the portfolio index created

in CIXB. For your explanatory variables consider economic and financial data found in

ECOF or ECO (e.g. productivity, GDP, economic indicators, interest rates, and the like):

MRA <Enter>; select a set for inputting information; on the set screen select dependent

variable (use index ticker of your portfolio created in CIXB: .Ticker <Index>) and select

independent variables (for economic information use their tickers, which can be found in

ECOF or ECO); save the set by typing 1 and hitting <Enter> and select the time period

and frequency (daily, weekly, etc.) by hitting 2 <Enter>.

MRA: Bloomberg’s Multiple Regression Screen

Example: Multiple Regression of XSIF portfolio returns against U.S. industrial production (IP),

U.S. government 10-year rates 1116623), and inflation index (CPIROC01)

11

5. Essay: Explain the Efficient Market Theory in terms of its propositions and implications,

hypotheses, and some of the empirical studies. Explain how some investment funds (or

styles) could be constructed based on the efficient market theory (e.g., size, earnings

announcements, P/e, etc.).

Bloomberg Part: Use Bloomberg to construct a portfolio based on efficient markets (you

may use the style exercise as a guide or a style portfolio that you set up). Analyze your

portfolio using the PMEN functions (include: PORT, etc.) and make a basket out of the

portfolio (CIXB) to analyze your portfolio on the index menu (COMP and HRA). Include

screens in your answer and bullet points on key observations of your portfolio relative to

the index.

Sample:

Stocks with the potential for consistent earnings and dividend growth without high volatility:

Market Cap.: Greater than or Equal to $2.0B

P/E (TTM Intraday): Less than or Equal to 20

Book Value Growth (5-Yr Avg.): Greater than or Equal to 5%

EPS Growth: 5-Yr Hist.: Greater than or Equal to 10%

Ret. on Equity (TTM): Greater than or Equal to 20%

Beta: Less than or Equal to 1.25

Divd. Growth Rate (5-Yr Avg.): Greater than or Equal to 5%

12

6. Essay: The economic climate is quite uncertain. Explain how portfolio insurance and range

forward strategies can be used to manage a stock portfolio.

Bloomberg Part: Construct a portfolio insurance position for one of your portfolios

using S&P 500 options. Use the Bloomberg OSA screen to import your portfolio and

SPX options. Determine the index put positions you would need to create a portfolio

insurance strategy (consider the horizon period when you select the maturity of the

13

option). Use OSA to generate a profit graph and/or market value graph of your hedged

portfolio. Import a call (with higher X) and set up a range forward position for your

portfolio. Include screens in you answer and bullet points on key observations.

Sample:

The value of the XSIF portfolio on August 31, 2012 was $1,221,287, the S&P 500 closed at

1400, and December 1400 S&P 500 put option was trading at 59.70 ($100 multiplier) and

December 1475 S&P 500 call was trading at 21.60.

Portfolio Insurance: np = $1,221,287/(1,400 x $100) = 8.72

Long Nine S&P 500 put contracts; Cost = (9)(100)(59.70) = $53,730

Range Forward:

14

7. Essay: Suppose you’re a market timer who is very bullish. Explain how you could use options

(calls and puts to form a synthetic long position) or index futures to increase the beta of your

portfolio.

Bloomberg Part: Select a portfolio you have created and add S&P 500 spot or futures

options and S&P 500 futures to the portfolio using Bloomberg’s OSA screen. Determine

the number of options or futures needed to change your portfolio’s beta. Using OSA,

compare your profit, profit percentage, or market value graphs with and without the

options or futures.

Sample:

The value of the XSIF portfolio on August 31, 2012 was $1,221,287, the S&P 500 closed at

1,400, a December 1,400 S&P 500 put option was trading at 59.70 ($100 multiplier) and

December 1,400 S&P 500 call was trading at 57.05.

Synthetic Long Position:

np = $1,221,287/(1,400 x $100) = 8.72

nc = $1,221,287/(1,400 x $100) = 8.72

Long Nine S&P 500 1,400 call contracts and short nine short nine S&P 500 1,400 put

contracts

Cost = Cost = [(9)(100)(59.70)] − [(9)(100)(57.05) = $34,290 = $2,385

Profit percentage graph without options:

For 20% plus and minus range in value, the portfolio’s profit and loss percentage ranges

between −11.57% and +32.64%

15

Profit percentage graph with options:

For 20% plus and minus range in value, the option-enhanced portfolio’s profit and loss

percentage ranges between −31.38% and +54.36%

8. Essay: Explain how ETFs are constructed.

Bloomberg Part 1: Use the Bloomberg fund search screen (FSRC) or the ETF Screen to

search for different ETFs. Select several ETFs and examine their features using the ETF’s

Des screen.

Sample

Examples of ETFs—Bloomberg Description Files

16

Bloomberg Part 2: Construct a simple market index or sector ETF. Test the correlation

of your ETF with the appropriate index by putting the portfolio in a CIXB basket and

then examining its correlation. Use HRA screen to see R2 and Beta. Comment on your

correlation.

Sample

Energy ETF (Energy) constructed to replicate S&P 500 Energy Index (S5ENRS):

ETF Features and correlation with index: Regression of Energy ETF against S&P Energy index

(9/11/06/9/7/12): R2 = .969, Beta = 1.079; Alpha = .015

17

II. BOND AND BOND PORTFOLIO QUESTIONS

1. Essay: Explain the methodology for estimating a bond’s option adjusted spread.

Bloomberg Part: Select a bond with embedded options and use Bloomberg’s YA and

OAS1 screens to estimate the bond’s spreads.

Sample:

The YA screen (below) for the 7.5% callable Ford bond with a maturity of 8/20/2032 shows that

on 4/13/2012 the bond was priced at 98.758 per $100 face value to yield 7.692811%. The YA

screen also shows a comparable Treasury that pays a 3 ⅛% coupon, matures on 11/15/32, and is

priced to yield 3.123289%. Using this Treasury as the benchmark, the spread on the Ford bond

over the Treasury is 456.95 basis points.

The Bloomberg OAS1 screen shows the calculated OAS and also the spread of the bond

if there were no embedded options—the option-free spread. The spread due to the embedded

option can be estimated by subtracting the option-free spread from the total spread. The OAS1

screen for the Ford bond on 4/13/2012 shows an option-free spread of 406.3 basis points using

the Black-Derman-Toy model. Given the total spread of 456.95 bp, Ford’s estimated call spread

is therefore 50.65 bp. Thus, the total spread of 456.95 consists of a call risk spread of 50.65 bp

and a credit and liquidity risk spread of 406.30 bp.

18

2. Essay: Explain the following concepts and their relation: interest rate risk, horizon analysis,

and bond immunization.

Bloomberg Part: Select a bond and conduct horizon analysis using either the Bloomberg

FIZH screen or the TRA screen. Explain how the screens work.

Sample:

The Bloomberg TRA screen calculates the total return on a selected bond for a selected horizon

period, discount yield at the HD, and reinvestment rate. Exhibit 6 shows the total return calculations

for a Kraft bond with a 5.375% coupon and a maturity date = 2/10/2020. On 4/13/2012, the bond

was trading at 116.961 to yield 2.929268% and had a duration of 6.63 (duration can be found on

the Bloomberg YA screen). The exhibit shows Bloomberg Total Return Analysis screens for the

Kraft bond for the horizon scenarios of six years and one year. The scenarios vary from three

parallel yield curve shifts from –300 bp to +300 bp for both discount rate and reinvestment rates.

For the six-year horizon the total returns for all the scenarios are approximately 3% (range

between 2.94% and 2.98%), whereas for the one-year scenario the total returns vary from a –

6.70% to 13.51%.

Note: With the duration of the Kraft bond of approximately 6 years, an investor with horizon

of six years would find this Kraft bond would minimize her interest rate risk. In contrast, an

investor with a one-year horizon would find this Kraft bond subjecting her to interest rate risk.

Exhibit 6: Total Return/Horizon Analysis—Bloomberg TRA Screens

Kraft Bond: 5 3/8 Coupon Maturity, Date = 2/10/2020, Duration = 7.086

Horizon = 6 years and 1 year

Bloomberg Total Return Screen: TRA

19

3. Essay: Explain the theory of why the spread payment on a CDS should be equal to the credit

spread on a bond and the probability of default.

Bloomberg Part: Select at least two corporate bonds and use Bloomberg’s DRSK and

CDSW screens to compare the bonds’ five-year CDS’s and implied probabilities with other

comparable bonds. Explain how the screens function.

Sample:

The exhibit shows the Bloomberg DRSK and CDSW screens for Ford and Kraft showing their five-

year CDS and implied probabilities.

DRSK: The DRSK screen provides estimates for the default probability, credit rating, and the

five-year CDS spread for a selected company and its peers (click grey Industry Comparison).

Kraft

Ford

20

Credit Default Swap Screen, CDSW: The Bloomberg CDSW screen shows the terms of the

selected bond’s issuer’s CDS and the implied probability of default.

Kraft and Ford

4. Essay: Define the different types of yield curve shifts and explain yield curve strategies that

you would used to profit from the shifts. Explain what is meant by trading-down the yield

curve.

Bloomberg Part 1: Use Bloomberg’s IYC9 total return/yield curve screens, examine the

total return for different yield curve shift scenarios. Explain how the IYC9 screens work.

Sample

Exhibit 7 shows a number of Bloomberg IYC9 (total return/yield curve screens). The IYC9 screen

shows the total returns for different horizons and yield curve shift scenarios based on the U.S. on/off

the run sovereign yield curve. The screens can be used to identifying strategies for trading down the

yield curves given different interest rate forecasts. The top screen in the exhibit shows the total

returns for each maturity from buying a Treasury and selling it one year later given no change in

rates. As the total return graph shows, the largest returns occur from the intermediate-term and long-

term maturities. The middle screen shows returns for a one year horizon given a 100 bp upward

shift in the yield curve and a 50 bp decrease in the yield curves. For the upward shift, the total

returns are negative with the losses increasing with maturity. For the downward shift, total returns

are positive and increasing with maturity. Finally, the lower screen shows scenarios for increasing

and decreasing yield curve shifts for a three-year horizon period.

21

Exhibit 7: Total Returns Given Different Horizons and

Yield Curve Shifts, Bloomberg IYC9 Screens, 4/9/2012

22

Bloomberg Part 2: Suppose you are a bond portfolio manager who over the past year

has focused your Treasury investments in intermediate bonds (8-10 year maturities).

Further suppose you are preparing your annual report on your fund’s performance and

would like to explain how the changes in the yield curve over the past year affected the

rates on your Treasury holdings.

Use the CRVF screen to shown the shift in the Treasury yield curve over the past

year.

Use the IYC8 screen to do your historical analysis of the total returns from your

bond given the changes in yield curve.

CRVF screen shows yield curves for different countries, sectors, and regions for selected

periods

IYC8 shows yield curves for different periods and the total returns for that period that would be

realized by buying bonds with different maturities.

23

5. Essay: Define the equilibrium bond price and explain the equilibrium using an arbitrage

argument of buying bonds and stripping them or buying strips and bundling

Bloomberg Part 1: Using the Bloomberg FIT screen to identify a Treasury strip and

describe its features using DES, YA, and ALLQ screens.

Sample:

Exhibit 8 shows the Bloomberg FIT screen for strips and the description and price quotes of one

strip. The strip shown was issued on 2/15/2001, pays a zero coupon, and a principal on

2/15/2030. The information on the YA screen, shows the strip yields a return of 3.041014%

based on the price of 58-14⅜.

Exhibit 8: Treasury Strips

24

Bloomberg Part 2: Select a bond (corporate or Treasury) and use Bloomberg’s strip

analysis screen to analyze the profit from buying and stripping the bond. Explain how the

SP screen functions.

Sample:

On the SP screen, the rates shown on the spot curve (X) are spot rates generated from the

international yield curve; the curve reflects the yields of different maturities that a dealer stripping

the securities might use to set the selling price. The screen allows the user to change the yield

(shifts) by adding or subtracting basis points from the selected maturities on the curve. The screen

shows the value (V) of each stripped security and the profit from the strips (value of strips minus the

cost of the bond).

Selected Security: Kraft Bond and U.S. Treasury, 4/8/12:

6. Essay: Explain the important characteristics of one of the bond portfolios you or your group

constructed: Market value, duration, convexity, quality distribution, duration distribution, etc.

Use PORT and PREP.

Bloomberg Part: Conduct a two-year horizon analysis using PORT. In you horizon

analysis, include both parallel shifts and twist in yield curves. Comments on the relation

you observe between total return, yield changes, and the duration of your portfolio.

Sample

Horizon Analysis:

Exhibit 9 shows the horizon analysis conducted on the Xavier Student Investment Bond Fund using

the Bloomberg BSA screen for parallel and non-parallel shifts. For parallel shifts from +300 bp to

−300 bp, the total returns for a two-year horizon range from 10.12% to −3.39%. The non-parallel

25

shifts include a yield curve flattening, with long-term yields decreasing 100 bp and 50 bp, yield

curve not changing, and yield curve steepening, with long-term rates increasing 50 bp and 100 bp.

As shown, the total returns for a two-year horizon range from 5.55% to 1.24%. The relatively small

range in total returns for the non-parallel shift scenarios compared to the parallel shift scenarios

shown in the exhibit is explained by the portfolio having a relatively small proportion of bonds with

durations exceeding 10. This can be seen by examining the Bloomberg PREP screen that shows the

portfolio’s duration distribution. The portfolio has approximately 58% of its holding concentrated in

bonds with durations between two and six years and only 15% in durations exceeding 10. The

portfolio can, in turn, be described as being closer to a bullet portfolio with a duration distribution

focused more on intermediate bonds than long-term one. As a result, the fund is less sensitive to

yield curve shifts that affect the long-end of the curve.

Exhibit 9: The Xavier Student Investment Bond Portfolio Fund as of April 13, 2012:

Parallel Shifts

26

Issuer Coupon Rate Duration Convexi ty BPV -300bp -200bp -100bp No Change +100bp +200bp +300bp

Portfolio 5.3 4.43 0.42 440.7 10.12 8.47 6.03 3.29 0.82 -1.4 -3.39

FEDERAL HOME LOAN BANK 4 1.36 0.03 2.86 0.38 0.38 0.38 0.91 1.55 2.2 2.84

E.I. DU PONT DE NEMOURS 5 1.21 0.02 3.19 0.81 0.81 0.81 1.52 2.33 3.13 3.93

SOUTHERN POWER CO 4.88 3 0.11 13.21 4.07 4.07 4.07 3.29 2.25 1.23 0.22

WAL-MART STORES INC 7.55 11.19 1.68 66.16 39.3 30.64 18.28 7.59 -1.72 -9.84 -16.94

VERIZON COMMUNICATIONS 4.9 3.17 0.12 7.13 3.34 3.34 3.34 2.4 1.2 0.02 -1.13

KRAFT FOODS INC 6.13 4.94 0.29 17.89 8.86 8.86 7.73 4.53 1.49 -1.42 -4.22

CVS CAREMARK CORP 5.75 4.45 0.24 15.79 7 7 6.52 3.88 1.36 -1.07 -3.42

FANNIE MAE 5 2.83 0.1 4.8 1.7 1.7 1.7 1.13 0.29 -0.53 -1.34

CITIGROUP INC 5.5 2.34 0.07 6.27 5.35 5.35 5.36 5.13 4.74 4.36 3.98

GOLDMAN SACHS GROUP INC 7.5 5.38 0.36 18.49 16.09 16.09 13.71 9.8 6.11 2.6 -0.74

CONOCOPHILLIPS 5.9 12.87 2.21 56.92 48.21 35.95 20.83 8.02 -2.9 -12.23 -20.23

INTL PAPER CO 7.4 1.98 0.05 4.39 4.52 4.52 4.52 4.54 4.53 4.52 4.52

US TREASURY N/B 4.75 4.78 0.27 14.32 5.46 5.46 4.78 1.87 -0.92 -3.61 -6.19

US TREASURY N/B 9.13 4.9 0.3 21.72 6.44 6.44 5.11 2.04 -0.87 -3.65 -6.31

US TREASURY N/B 4.25 4.98 0.29 23.42 6.07 6.07 5.13 2 -0.99 -3.86 -6.61

US TREASURY N/B 4.63 4.13 0.2 16.98 3.87 3.87 3.79 1.55 -0.59 -2.66 -4.68

US TREASURY N/B 4.5 3.55 0.15 14.27 2.61 2.61 2.61 1.24 -0.32 -1.85 -3.34

DUKE ENERGY CAROLINAS 5.63 0.61 0.01 1.25 0.54 0.54 0.54 1.76 3.17 4.58 5.99

FREDDIE MAC 3 2.21 0.06 11.71 0.98 0.98 0.98 0.86 0.64 0.43 0.21

US TREASURY N/B 4.5 3.3 0.13 3.77 2.21 2.21 2.21 1.12 -0.18 -1.46 -2.72

BANK OF AMERICA CORP 4.75 3.01 0.11 6.28 7.59 7.59 7.59 6.75 5.64 4.54 3.47

FREDDIE MAC 6.25 12.82 2.19 27.25 46.13 34.17 19.31 6.71 -4.02 -13.21 -21.09

NEW YORK LIFE GLOBAL FDG 5.38 1.37 0.03 5.12 0.99 0.99 1 1.5 2.13 2.77 3.4

FANNIE MAE 5.25 0.29 0 0.6 0.06 0.06 0.06 1.29 3.02 4.74 6.47

GENERAL ELECTRIC CO 5 0.78 0.01 1.21 0.47 0.47 0.47 1.64 2.87 4.11 5.34

FREDDIE MAC 3.75 6.18 0.44 14.06 10.56 10.56 7.76 3.29 -0.93 -4.93 -8.73

US TREASURY N/B 2.63 2.14 0.06 15.77 0.71 0.71 0.71 0.63 0.48 0.34 0.19

US BANK NA 6.3 1.71 0.04 7.43 2.24 2.24 2.24 2.39 2.68 2.96 3.25

DOMINION RESOURCES INC 5.95 13.14 2.45 30.88 53.08 38.92 22.76 9.31 -1.96 -11.45 -19.47

US TREASURY N/B 4.75 1.97 0.05 7.54 0.63 0.63 0.63 0.66 0.68 0.71 0.73

Horizon Analysis for Non-Parallel Yield Curve Shifts—Bloomberg BSA Screen

27

7. Essay: Suppose you are a bond manager for an insurance company and have to invest an

amount equal to the market value of the portfolio you analyzed in Question 6 (in the bonds

comprising your portfolio) to meet a liability that is equal to the duration of your portfolio.

Explain the concept of bond immunization and how you would immunize your investment

against interest rate risk.

Bloomberg Part: Using Bloomberg’s BSA screen do a horizon analysis with your

portfolio with the time horizon set equal to your duration. Comment on the total returns

you get for different scenarios and the effectiveness of your bond immunization strategy.

Sample:

Exhibit 10 displays a Bloomberg BSA screen showing a total return analysis for the bond portfolio

given a six-year horizon. The total returns for the six-year period range from 16.78% (annual rate =

(1.1678)1/6

– 1 = 2.62%) for a –300 bp shift to 11.67% annual rate = (1.1167)1/6

– 1 = 1.86%) for a

+300 bp shift. The relatively small variability is explained by the portfolio’s duration of 5.5 being

close to the six-year horizon. Thus, a pension or insurance company who wanted to minimize

market risk in meeting a liability with duration of six years might consider investing in this portfolio

with its 5.5 duration.

28

Exhibit 10: Total Returns for Portfolio with Duration of 5.5 and Horizon of 6

Bloomberg PRTU, PSD, BSA, and PREP Screens

The bond portfolio consists of five investment-grade option-free bonds. The portfolio consists of

1,000 issues of each bond and was constructed using the Bloomberg PRTU screen. On 4/13/2012

the portfolio was worth $5,681,848, and it had of 5.5.

29

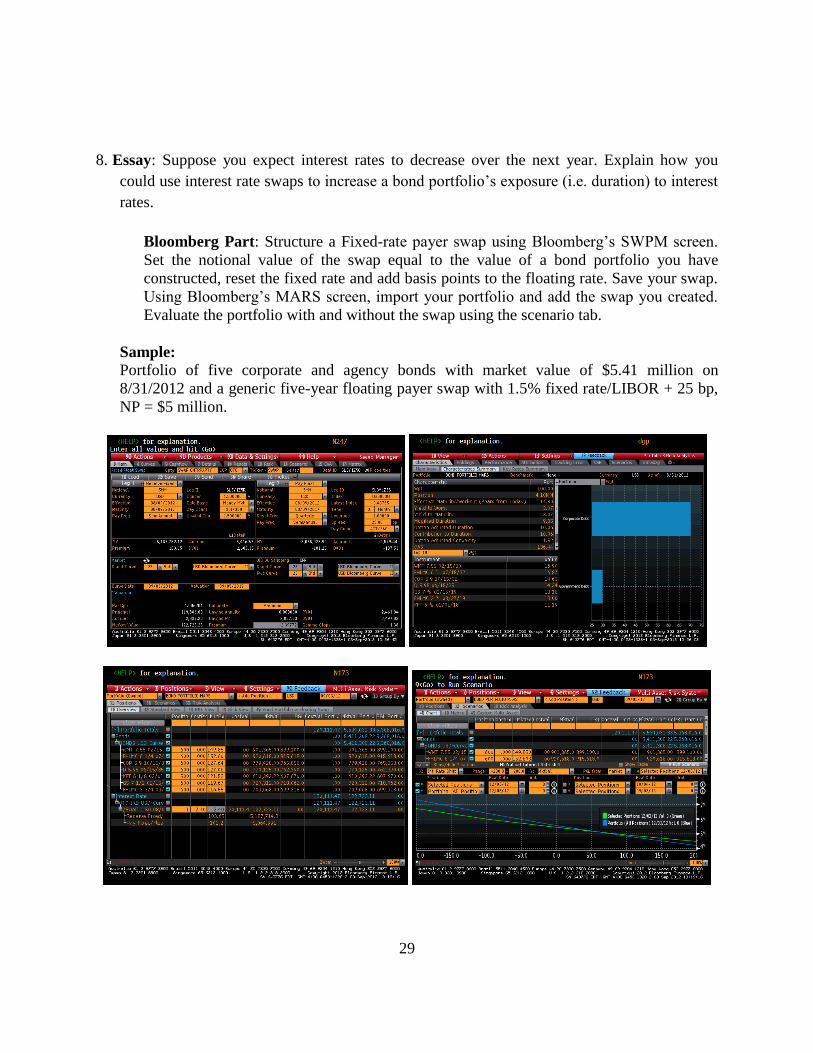

8. Essay: Suppose you expect interest rates to decrease over the next year. Explain how you

could use interest rate swaps to increase a bond portfolio’s exposure (i.e. duration) to interest

rates.

Bloomberg Part: Structure a Fixed-rate payer swap using Bloomberg’s SWPM screen.

Set the notional value of the swap equal to the value of a bond portfolio you have

constructed, reset the fixed rate and add basis points to the floating rate. Save your swap.

Using Bloomberg’s MARS screen, import your portfolio and add the swap you created.

Evaluate the portfolio with and without the swap using the scenario tab.

Sample:

Portfolio of five corporate and agency bonds with market value of $5.41 million on

8/31/2012 and a generic five-year floating payer swap with 1.5% fixed rate/LIBOR + 25 bp,

NP = $5 million.

30

APPENDIX

Bloomberg Exercises used in Investment, Financial

Markets, Fixed-Income, and Derivative Classes

Bond Valuation and Return

1. Select an option-free (bullet) corporate bond of interest. You may want to use the Bloomberg search/screen

function, SRCH, to find your bonds. Evaluate the bond in terms of its price, yield, yield spread, and price-yield

curve. In your evaluations, you may want to consider the following screens on the bond’s menu screen:

a. CSHF screen to find the bond’s cash flow

b. YA screen to determine price and yield

c. PT screen to view price-yield curve (enter percent steps in increments box)

d. TDH and ALLQ to determine the liquidity on the bond based on it trading activity and bid-ask

spreads.

2. Select a callable corporate bond of interest. You may want to use the Bloomberg search/screen function, SRCH,

to find your bonds. Using the YA screen (click grey “Call” tab) or the YTC screen, examine the call structure

of the bond and determine its yield to next call, yield to maturity, and yield to worst.

3. Select a U.S. Treasury bond with a long-term maturity (15 to 20 years). You may want to use the FIT screen to

find your bond.

a. Conduct a total return analysis of the bond using the FIHZ screen for an instantaneous change in

rates (set the horizon to the current settlement date) given different discount rates and reinvestment

rates.

b. Conduct a total return analysis of the bond using the FIHZ screen for a given horizon period (e.g.,

one year) given different discount rates and reinvestment rates.

c. Conduct a total return analysis of the bond using the TRA screen. Select different horizon periods

(current date, one-year horizon, etc.), yield shifts, and reinvestment rates.

Comment on the bond’s sensitivity to interest rate changes.

4. Select an intermediate-term to long-term speculative-grade corporate bond. Using the bond’s GY or GP screen,

examine its price, yield to maturity, yield to next call (if applicable) and spread over its benchmark over the past

year. Click the “Event” checkbox and set the event settings to see if the spikes in spreads can be explained by

certain events.

5. Select a U.S. Treasury bond or note with an intermediate-term or long-term maturity (10 to 20 years). You may

want to use the FIT screen to find your bond. Use the SP screen on the selected bond’s menu screen (CUSIP

<Govt> <Enter>) to evaluate the profitability of stripping the bond. What is the profit from buying the bond at

its current price, stripping it, and selling the strips at the spot rate yields given on the screen? On the SP screen

look for the profit for no shift scenario. What is the profit from buying the bond at a lower price, stripping it,

and selling the strips at the spot rate yields given on the screen? What is the profit from buying the bond at a

higher price, stripping it, and selling the strips at the spot rate yields given on the screen?

6. Select an option-free (bullet) corporate bond of interest. Evaluate the bond in terms of its yield spread, credit

risk, liquidity, and interest rate risk. In your evaluations, you may want to consider the following screens on the

bond’s YA screen: Yield & Spread Tab to determine the bond’s spread and Graphs Tab to evaluate the bond’s

spread history. Do a comparative spread and credit risk analysis of the bond using the bond’s COMB screen.

31

Level and Structure of Interest Rates

1. Using the Bloomberg YCRV screen, explore the yield curves on U.S. Treasuries (U.S. on/off- the-run

sovereign, I111) over the last 10 years. Provide some economic and policy arguments that might explain the

differences in yield curves you observe in different periods. Use information from the Federal Reserve sites

(FED <Enter>; FOMC <Enter>) and some of the economic indicators from ECOF to find information to

support your arguments. Possible indicators:

U.S. Nominal GDP: GDP CUR$ <Index>

U.S. Real GDP: GDP CHWG <Index>

U.S. Inflation: CPY YOY <Index>

S&P/Case-Schiller: SPCS20 <Index>

U.S. Unemployment Rate: USURTOT <Index>

U.S. Deficit: FDEBTY <Index>

Government Debt: PUBLDEBT <Index>

Money Supply (M2): M1NS <Index>

Balance of Payments: USCABAL <Ticker>

Energy Prices: CPUPENER <Ticker>

2. Using the YCRV screen, compare current yield curves on Treasuries (I111) with different quality bonds, such

as those for industrials (e.g., F884 for composites). Provide some economic and policy arguments that might

explain the differences in yields.

3. Use the IYC9 screen to develop strategies for trading down the Treasury yield curve given the following

scenarios and horizons:

a. An upward yield curve shift of 100 bps and an horizon of one year

b. A downward yield curve shift of 100 bps and an horizon of one year

c. A flattening of the yield curve where short-term rates increase (e.g. 100 bps), intermediate-term

and long-term rates remain the same and a one year horizon.

d. An upward yield curve shift of 100 bps and an horizon of three years

e. A downward yield curve shift of 100 bps and an horizon of three years

f. No change in the yield curve and an horizon of three years.

4. Suppose you are a bond portfolio manager who over the past year has focused your Treasury investments in

intermediate bonds (8-10 year maturities). Further suppose you are preparing your annual report on your fund’s

performance and would like to explain how the changes in the yield curve over the past year affected the rates

on your Treasury holdings.

a. Use the IYC6 screen to shown the shift in the Treasury yield curve over the past year.

b. Use the IYC8 screen to do your historical analysis of the total returns from your bond given the

changes in yield curve.

5. Use the FWCV screen to determine forward rates one, two, and three years forward. Given your projected one-

year forward rates determine your one-year expected total return for different maturity investments using the

IYC9 screens and inputting your forward rates.

6. Using the YCRV screen, compare municipal yield curves for different states: YCRV <Enter>; look for curves

by “Curves Types,” “Municipal Curves,” and “State Specifics.” Provide some economic arguments that might

explain the differences in yields.

32

Bond Risk and Duration

1. Use the Bloomberg RATC screen to identify bonds that have had recent ratings changes. On the RATC screen,

you may want to limit your search to bonds in a particular industry (select industry from the red “Search”

dropdown). Examine one of the bonds with ratings changes using the RSKC, CRPR, and DRSK screens.

Comment on the ratings changes and information you find from the screens, such as Altman Z-score,

probability of default, changes in financials, CDS spreads, and litigation.

2. Select a callable investment-grade corporate bond of interest. You may want to use the Bloomberg

search/screen function, SRCH, to find your bonds. Evaluate the bond in terms of its YTM, yield to first call, and

yield to worst. Use the OAS1 screen to determine the option-free spread on the bond, and the YAS screen to

determine its total spread. What is the bond’s credit and liquidity spread? What is its callable spread?

3. Select a U.S. Treasury bond or note with an intermediate-term or long-term maturity (10 to 20 years). You may

want to use the FIT screen to find your bond.

a. Using the YA screen on the selected bond’s menu screen (CUSIP <Govt> <Enter>), determine the

bond’s Macaulay and modified duration.

b. Conduct a total return analysis of the bond using the TRA screen. Select different horizon periods,

yield curve shifts, and reinvestment rates.

c. Conduct a total return analysis of the bond using the FIHZ screen using different horizon periods,

discount rates, and reinvestment rates.

4. Suppose you have a horizon that matches the duration of the bond you selected in Exercise 4. Evaluate the

interest rate risk on the bond using the FIHZ and TRA screens:

a. Using the FIHZ screen for the selected bond, evaluate its interest rate risk by setting the screen to

the horizon matching the bond’s duration and then selecting a discount rate and reinvestment rate

showing a low interest rate scenario and then rates reflecting a high interest rate scenario.

b. Using the TRA screen for the selected bond, evaluate interest rate risk by setting the screen to the

horizon matching the bond’s duration and then selecting a reinvestment rate.

5. Select five investment-grade option-free bonds with different maturities (e.g., 3, 7, 10, 15, and 20 years). Using

the YA and DES screens find each one’s maturity, coupon rate, quality rating, YTM, spread, modified duration,

Macaulay duration, and convexity. Summarize your information in a table. Comment on the properties of

duration and convexity in terms of the bonds you selected. If your horizon were three years, which bond would

you select if you expected interest rates to decreases? Which bond would you select if you expected rates to

increase?

Bond Strategies

1. Conduct a horizon/total return analysis on five Treasury notes and bonds with different maturities (e.g., 3, 7, 10,

15, and 20). Use FIT to help you select the bonds. To conduct the analysis, construct a portfolio of the bonds

using PRTU (enter the bond’s CUSIP on the PRTU screen). Once you have constructed the portfolio, use the

BSA screen to conduct the scenario analysis. To evaluate each bond in terms of its sensitivity, download the

BSA scenario to Excel report (click Excel from “Reports” tab). This report shows total returns for each shift for

the portfolio and the individual bonds.

2. Construct a portfolio of investment-grade corporate bonds and U.S. Treasuries using the PRTU screen. You

may want to use the Bloomberg search/screen function, SRCH, to identify the bonds for your portfolio. After

constructing the bond fund, evaluate the portfolio. Possible evaluations you may want to consider:

a. Evaluate the portfolio’s features using the PREP, PSD, PCF, and KRD screens.

b. Using the BSA and/or PSA screens, evaluate the portfolio’s duration and it sensitivity to different interest

rate changes for different horizon periods.

33

c. Using the BSA and/or PSA screens, evaluate the portfolio’s total return for rate changes in which the yield

curve steepens and for changes in which it flattens.

d. Using the KDR screen, evaluate the duration distribution of your portfolio.

e. Using the PREP screen, evaluate the bonds in your portfolio in terms of their “ratings and spreads” and

“ratings and duration.” For spread analysis, select on the PREP screen “Spread Distribution” from the “1st

Distr” dropdown and select “Spread Measure” from the “Column” dropdown; for duration, select on the

PREP screen “Effective Duration” from the “1st Distr” dropdown and “Duration Measure,” “Spread

Measure” or “Analysis” from the “Column” dropdown.

f. Using the corporate actions calendar, CACT, and events calendar, EVTS, identify past and future events

that merit consideration. You may want to consider setting up alerts from the “Actions” tab).

3. Examine the performance of the portfolio you constructed in Exercise 9 over the past year relative to one or

both of the following bond indexes:

a. J.P. Morgan Global Aggregate Bond Index: JGAGUSUS <Index> <Enter>

b. One of the Bloomberg Bond Government Indices, such as All Bond Government Index: USGATR

<Index> <Enter>

In examining the past performance, create a basket of historical returns of the bonds from the portfolio you

formed in Exercise 2 using the CIXB screen. See CIXB Box for steps to import a search or portfolio in order to

create a CIXB basket. After creating the basket, evaluate your portfolio of bonds relative to the indexes using

the total return screen, COMP, on the index menu (Basket ticker name (e.g., .BOND <Index> <Enter>).

4. Suppose you are a bond portfolio manager for an insurance company and you are looking at investing premiums

to meet expected liabilities in seven years. Construct a portfolio of investment grade corporate bonds and U.S.

Treasuries with a portfolio duration of approximately seven years using the PRTU screen. You may want to

limit you search to bonds with maturities between 10 and 15 years. After constructing the bond fund, evaluate

the portfolio’s duration features using the PORT, PSD, PREP and KRD screens. Using the BSA screen,

evaluate the portfolio’s interest rate risk given different interest rate changes for a horizon of seven years.

5. Suppose you are a bond portfolio manager constructing a high yield fund. Use the Bloomberg search/screen

function, SRCH, to help you identify possible bonds to include in your portfolio. After identifying your bonds,

construct a portfolio using the PRTU screen and evaluate the portfolio. Possible evaluations:

a. Evaluate the portfolio’s features using the PORT, PSD, PREP, DRAM, and PCF.

b. Using the PREP screen, evaluate the bonds in your portfolio in terms of their ratings and spreads. For

spread analysis, select on the PREP screen “Spread Distribution” from the “1st Distr” dropdown and select

“Spread Measure” from the “Column” dropdown; for ratings, select on the PREP screen “Ratings” from the

“1st Distr” dropdown and select “Spread Measure” or “Analysis” from the “Column” dropdown.

c. Evaluate the ratings histories of the bonds in your portfolio using the CRAT screen.

d. Evaluate the default risk of each of the bonds in the portfolio using the DRAM screen.

e. Use the corporate actions calendar, CACT, and events calendar, EVTS, to identify past and future events

that merit consideration. You may want to consider setting up alerts from the “Actions” tab).

6. Examine the performance of the high yield portfolio you constructed in the previous exercise over the past year

relative to the J.P. Morgan Global Aggregate Bond Index (Ticker: JGAGUSUS; JGAGUSUS <Index>

<Enter>). In examining the past performance, create a basket consisting of the bonds from the portfolio you

formed in Exercise 5 using the CIXB screen. See the CIXB Box for steps to import a search or a portfolio in

order to create a CIXB basket. After creating the basket, evaluate your portfolio of bonds relative to the indexes

using the total return screen, COMP, on the index menu (Basket ticker name (e.g., .HYBOND <Index>

<Enter>).

7. Set up an RV screen for evaluating and monitoring the companies comprising the high-yield portfolio you

constructed in Exercise 5. To set up the screen, you may want to use PRTU to form an equity portfolio of the

companies whose credits you hold in your high yield bond portfolio. Once you have constructed the portfolio,

34

bring up the RV screen. Use the equity screen for one on the companies in your portfolio and then import your

equity portfolio (select “Portfolio” from the “Comp source” tab and select your equity portfolio from “Name”

tab). Customize your columns by selecting financial parameters that will help you evaluate credit risk.

Parameters to consider: Debt/EBDIT, EBIT/Interest Expenses, Debt/Equity, liquidity ratios, operating

performance measures, Altman Z-Score, and 5-year CDS (items can be inserted by typing in the name in the

yellow box on the RV screen). Be sure to save your screen.

Financial Securities and Markets

Government

1. Find the features on T-bills, T-notes, and T-bonds recently issued at a Treasury auctions by going to the

Bloomberg FIT/BBT screen; BBT <Enter>, click T/ACT. To access the menu screen enter CUSIP (or coupon

rate and maturity) <Govt>. Screens on the menu you may want to consider include description (DES), dealer

bid-ask quotes (ALLQ), and calculation of the yield on the bill (YA).

2. Treasury-Inflation Protection Securities, TIPSs, are popular Treasuries. Select a TIP from the BBT screen and

study its features: BBT <Enter>, click TIPs. To access the menu screen enter CUSIP (or coupon rate and

maturity) <Govt>. Screens on the menu you may want to consider include description (DES), dealer bid-ask

quotes (ALLQ), and calculation of the yield on the bill (YA). On the YA screen, change the inflation

assumption and determine the yield based on the assumed inflation rate.

3. STRIPS are popular Treasuries. Select a STRIP from the BBT screen and study its features: BBT <Enter>, click

strip. To access the menu screen enter CUSIP (or coupon rate and maturity) <Govt>. Screens on the menu you

may want to consider include description (DES), dealer bid-ask quotes (ALLQ), and calculation of the yield on

the bill (YA).

4. Using the PX screen, select and evaluate several types of Treasury and agency securities using the functions on

the security’s menu screen (Des, ALLQ, YA, HDS, and CSHF (payment schedule). Types of securities to possibly

select: US Currents, US Strips, US Bonds, Active Agencies, Active Brady, and Foreign government bonds (e.g.,

Greece – Government Bonds).

5. Select a recently issued T-note (e.g. 5-years to 10-years) from the PX screen. On the menu screen for the

selected note use the SP function (Strip Analysis) to see how the bond could be stripped into interest-only and

principal-only strips.

6. Study the features from the description screens (Des) of some of the following GSEs:

Federal Home Loan Mortgage Corporation: FHLMC <Corp> <Enter>

Federal National Mortgage Association: FNMA <Corp> <Enter>

Federal Home Loan Bank System: FHLB <Corp> <Enter>

Federal Agriculture Mortgage Association: FAMCA <Corp> <Enter>

Federal Farm Credit Bank: FFCB <Corp> <Enter>

Tennessee Valley Authority: TVA <Corp> <Enter>

World Bank (International Bank for Reconstruction and Development): IBRD <Corp> <Enter>

Student Loan Marketing Association: SLMA <Corp> <Enter>

7. The 2008 financial crisis led to the American Recovery and Reinvestment Act and the Emergency Economic

Stabilization Act, Troubled Relief Program (TARP), and Total Asset-Backed Security Asset Loan Facility

(TALF). Review these and other programs by going to the following Bloomberg screens:

a. TARP <Enter>: TARP Program

b. TALF <Enter>: TALF Program

c. STRS <Enter>: Stress Test Overviews

35

d. GGRP <Enter> Government Relief Programs

e. NI TARP <Enter>: TARP News

f. RESQ <Enter>: Bailout and Rescue Menu

g. WWCC <Enter>: Worldwide Credit Crunch

8. Changes in U.S. government debt depend on the federal government expenditures and revenues. Information on

U.S. government’s expenditures, revenues, and deficits can be found on the ECOF screen (budget tab). Examine

and comment on the number of budget deficits that have occurred over the last 20 years. Comment on the deficit

increases after 2008. Data series to consider: U.S. Treasury federal budget yearly summary deficit or surplus,

net outlays, revenues, types of revenues, types of expenditures, and deficits as a percentage of GDP.

9. Determine the growth in the government’s debt over the last 20 years by going to the ECOF screen (debt tab).

Data series to consider: U.S. total public debt outstanding, U.S. debt as a percentage of GDP, U.S. total public

debt outstanding total non marketable.

10. Information on current and recent Treasury auctions can be found on AUCT, ECO20, and PX: AUCT <Enter>;

ECO20 <Enter>; PX <Enter>.

a. Using AUCT, find information about the size of the auction and the amount of competitive and

noncompetitive on a recent or pending Treasury auction (e.g. 10-year note).

b. Use ECO 20 to find details about purchases and sales of recent or proposed issues.

c. Use PX to find a recently issued Treasury or agency and then evaluate the security by using the

functions on its menu screen.

11. Find municipals for a particular state by going to MUN2 (or by going to SMUN, clicking state of interest, and

clicking Muni Bond Browser (MUN2)). Using the tabs, select municipals with certain features (coupon,

maturity, structure, and issued). Study several of the bonds using the functions on the bond’s menus screen.

12. Use MSRC to search for bonds for the following types of bonds:

a. Insured general obligations (select from “Industry” tab) in a state or particular region (e.g.,

Northeast). You may want to narrow the search by limiting the search by maturity and coupon

type.

b. Specific revenue bond (select from “Industry” tab: Airport, assisted living, Community

Development, etc. or select from “Sources & Uses” tab) in a particular region (e.g., Northeast).

You may want to narrow the search by limiting the search by maturity and coupon type.

Study several of the bonds from each search using the functions on the bond’s menus screen

CUSIP <MUNI>. Functions to include: DES, CF (Official Statement or Annual Report), QR,

And CN (news).

13. Use PICK to post and monitor new or secondary municipal bonds. Create a custom bulletin board of

offerings/trades that match your investment strategies (e.g., municipal water authorities in a given state or

region). Select one of the bonds from the PICK search and study it using the functions on the bond’s menus

screen (CUSIP <MUNI>. Functions to include: DES, CF (Official Statement or Annual Report), QR, and CN

(news).

14. Do a relative comparison of states using SMUN and DEMS screen:

SMUN <Enter>: Compare financial conditions by using SMUN. On SMUN select “All States”

from States tab and several templates from the “Types” tab (e.g., General, Pension, Government,

or All). Comment on any state whose financials or changes in financial are significantly different,

indicating a red flag.

DEMS <enter>: Do a relative analysis of state demographics.

36

15. On the SMUN screen, click a state of interest to bring up a menu and state identification number (e.g., STOCA1

for California). Study the economic and financial conditions of the state by going to its menu page (e.g.,

STOCA1 <Equity>). Screens to consider: BLS (Employment), FA SS (financial overview), and FA (on

“Funds” tab you can look at pensions, general, and government financials).

16. Use the BAB screen to search for Taxable Build American Bonds issued in a particular state. Select one of the

bonds from the BAB search and study it using the functions on the bond’s menus screen (CUSIP <MUNI>.

Functions to include: DES, CF (Official Statement or Annual Report), QR, FA, SER (bonds in the series), and

CN (news).

17. Official Statements are important sources of information on a municipal issue. Review the “Official Statement”

on one of the bonds you found in Questions 13 or 14.

18. Taxable municipals are attractive investments for tax-exempt investors. Search for some of these issues by

going to MSRC. On the MSRC search screens, select “Federally Taxable” in the “Tax Provision” tab. You may

want to narrow the search by limiting the search by maturity and coupon type. Use the PICK screen to

customize a search for new and existing taxable municipals to possibly monitor.

19. Bloomberg provides a review of conditions and trends in the municipal bond market in their “Municipal

Market” newsletter. Review recent trends in the municipal market reported in the newsletter. To access: BRIEF

<Enter>.

20. Use the Advanced News Search TNI to customize a news search for the following:

Municipals in a certain area

Sovereign in a distress country

21. Compare the yields on bonds of different maturities (e.g., 5 years and 10 years) for an advanced country using

the DMMV screen. On the screen, click the grey “83) Bonds” tab at the bottom.

22. Click one of the foreign government bonds of interest from the DMMV screen to find its identification number.

Evaluate that bond by using the functions (Des, ALLQ, HDS, and CRVD) on its menu screen: Identification

Number <Govt>. Study the country’s economic and financial conditions using information from the ECOF

menu.

23. Compare the yields on the bonds of different maturities (e.g., 5 years and 10 years) for a developing country

using the EMMV screen. On the screen, click the grey “83) Bonds” tab at the bottom.

24. Click one of the foreign government bonds of interest from the EMMV screen to find its identification number.

Evaluate that bond by using the functions (Des, ALLQ, HDS, and CRVD) on its menu screen: Identification

Number <Govt>. Study the country’s economic and financial conditions using information from the ECOF

menu.

25. Study the credit ratings of different countries using the CSDR screen: CSDR <Enter>.

Corporate Securities and Markets

1. Identify several current or recent investment activities of venture capital and private equity holdings companies by

using the FLNG screen (screen reports 13F filings).

2. Using the FLNG screen, study the past venture capital and private equity activities: FLNG <Enter>; from the

red “Aggregate 13-F filing” tab click “Current Report.” On the uploaded screen, select “Venture Capital” or

37

“Private Equity” from the “Institution” dropdown menu. You can identify activities to view at the bottom of the

screen and you can change the sectors to view activities by sector.

3. Identify several pending corporate deals using EVTS. You can use EVTS for a loaded company: Ticker <Equity>

EVTS. You can also search for events using EVTS and then select an industry or all stocks.

4. Identify and study an IPO using the IPO screen: IPO <Enter>. On the screen, you can access pending IPOs of

private equity firms by clicking “Private Equity” and the deal. To get more information on the company, use its

cursor (found on the deal page) and then go to its equity screen: Cursor <Equity>.

5. Identify and study private equity activities by going to the “Private Equity” menu: PE <Enter>. Bloomberg’s Private

Equity screen displays a menu of links that provide access to specific Bloomberg private equity analysis functions.

6. Given the many types of corporate bonds with their different features (callable, option-free bonds, putable, higher

quality, investment grade, lower quality, non-investment grade, debentures, and secured bonds), use Bloomberg’s

“Advanced Search” to search for bonds with certain features. Possible searches: U.S., dollar-denominated,

investment-grade (BBB and up) corporate bonds for a specific sector; bonds in a certain sector that are callable and

either investment-grade or non investment-grade. To access: SRCH <Enter> and click “Advanced Search.” On

the “Advanced Search” screen customize your search by using the settings: coupon, redemption features, credit

ratings, collateral, and industry sectors.

7. Using Bloomberg’s “Advanced Search” (SRCH <Enter> and click “Advanced Search”), search for callable

bonds that do not have a make-whole premium provision for determining the call. On the screen setting for

redemption features, click callable and “not make whole call.” Take one of the callable bonds from your search and

study its call provisions. Call schedules can be accessed from the bond’s description page.

8. Using Bloomberg’s search function (SRCH <Enter>), search for floating rate notes. To keep the search

manageable, you may want to limit your search to certain sectors. On the screen setting click “Include Only” in

the yellow dropdown “floater” tab. Take one of the floating rate notes from your search and study its features using

the bond’s menu: reference rate, margin, cap, floor, and call features. Most of this information can be found on the

bond’s description page.

9. The protective covenants, collateral, and priority of claims (subordination) for a bond issue can be found in a bond’s

prospectus. Select a bond of interest, identify its covenants and collateral, and determine whether there is any

subordination. The prospectus can be found on the bond’s description page (DES). An alternative and quicker way

to identify the covenants is to access the “Covenant, Default” screen (COV) on the bond’s menu page. Clicking one

of the covenants takes you to the section in the bond’s prospectus describing the covenant.

10. The PGM screen displays MTN program by issuer. Search for a past or current MTN issue of a company using this

screen: PGM <Enter>, click “Medium Term Notes” and then search for issuer and click for series. On the

description page of the issuer, click “Drawdown;” on the drawdown menu, click one of notes.

11. Study the CP market by examining the following screen

PGM: The PGM screen displays CP programs: PGM <Enter>, click Commercial Paper

FDCP: Shows CP outstanding

CPPR: Displays direct CP issuer

12. Select a preferred stock of a company of interest (to find ticker: <Pfd> tk <Enter> or if you know the

company’s ticker: ticker <pfd> to bring up the company’s preferred issues). Study the preferred stock using the

stock’s menu screen. Possible screens to examine from the menus: DES, DVD, and GP

38

13. Bloomberg information on corporate actions such as acquisitions and limited partnership deals can be accessed on

the CACS screen found on the company’s equity menu. Select a company of interest that you know has been active

in acquisitions and divestures and use CACS to search for its previous activities.

14. Identify several past acquisitions, IPOs, or divestures using the CACT screen. Set your search for M&A and IPO, or

use “Custom” tab.

15. The BNKF screen list recent bankruptcy filings (BNKF <Enter>). Use the screen to identify one of more companies

that have filed for bankruptcy and then evaluate the current state of the company by going to its equity menu and

reviewing some of the screens.

16. The DIS screen displays a list of all bonds that have traded at a yield of at least 10% over the Treasury benchmark

rate the last five business days. Use the screen to identify one of more companies with distressed debt and then

evaluate the current state of the company by going to its equity menu and reviewing some of the screens.

17. The LTOP screen displays top underwriters for the major fixed income, equity, equity-linked securities, and

syndicated loan securities markets. Using the screen, identify the top underwriters over the past year for U.S.

equity and fixed-income issues. Using the dropdown menu, study some of the recent deals for several of the top

equity and bond underwriter. To access: LTOP <Enter> On the LTOP screen, right click to access a dropdown

menu showing descriptions and the underwriter’s deals for that period.

18. The Bloomberg NIM and NNIM screens identify new security offerings by security type, period, and region.

The NIM screen can be customized to identify certain types of bonds and securities and news about announced

offerings. Using the NNIM screen, identify some new or expected offerings in the following security categories:

U.S. Bonds

Equity-Linked Securities (Convertibles)

U.S. Corporate/144A

Preferred

Eurobond

19. Identify and study private equity activities by going to the “Private Equity” menu: PE <Enter>. Bloomberg’s Private

Equity screen displays a menu of links that provide access to specific Bloomberg private equity analysis functions.

20. Short Interest is the total amount of shares of stock that are sold short and have not been repurchased to close out the

position. High levels of short interest indicate that numerous sellers have sold the stock short and are expecting a

downturn in the share price. The SI Screen displays monthly short interest information for a selected equity security

that trades on the American Stock Exchange (AMEX), National Association of Securities Dealers Automated

Quotation System (NASDAQ), New York Stock Exchange (NYSE), or Toronto Stock Exchange (TSE). Use the SI

screen for several stocks of interest to determine whether or not there is a bullish or bearish sentiment regarding the

stocks.

Intermediary Securities, Investment Funds, and Markets

1. Learn more about the different types of funds and their classifications by going to the FUND screen and

“Classification” link: FUND <Enter>; click “Fund Classification” and click type; or simply enter MFOD and

click type: Equity, Debt, Money Market, Real Estate, Commodity, and Alternative.

2. The performances of funds by type (e.g., mutual, hedge fund, ETFs, and unit investment trust) can be found on

Bloomberg’s Fund Heat Map Screen, FMAP. Use the screen to identify the top performers based on total return

for several types: FMAP <Enter>, Click “Fund Type” in “View By” dropdown.

39

3. The performances of funds by objective (e.g., equity, debt, asset allocation, money market, and alternative) can

be found on Bloomberg’s Fund Heat Map Screen, FMAP. Use the screen to identify the top performers based

on total return for several objectives: FMAP <Enter>, Click “Objective” in “View By” dropdown.

4. Bloomberg’s WMF screen provides snapshots of the best mutual funds by category in terms of their total return.

Using this screen, examine several funds in different categories. Select several of the funds and study them

using the functions on the fund’s menus screen (Fund Ticker <Equity> <Enter>). Functions to include: DES,

historical fund analysis (HFA), fund holdings (MHD), relative valuation (RV), and price graph (GP).

5. Use the Bloomberg fund search screen, FSRC, to search for the following types of equity-type funds and ETFs:

a. Fund Type: Open-End; Classification (Asset Class Focus): Equity; Management Style: Growth or

Growth and Income; Analytic criterion: Input total return for one year of greater than X% (e.g.,

10% or 20%)

b. Fund Type: Open-End; Classification (Asset Class Focus): Equity; Management Style: index fund;

Analytic criterion: input total return for one year of greater than X% (e.g., 10% or 20%)

c. Fund Type: Closed-End; Classification (Asset Class Focus): Equity; Country of Domicile: select

(e.g., U.S.); Analytic criterion: input total return for one year of greater than X% (e.g., 10% or

20%)

d. Fund Type: Unit-investment trust; Analytic criterion: input total return for one year of greater than

X% (e.g., 10% or 20%)

e. Fund Type: Open-end; Classification: Industry Focus: Select industry (e.g., energy); Analytic

criterion: input total return for one year of greater than X% (e.g., 10% or 20%)

f. Fund Type: Open-end; Classification, Geographical Focus: Select Country or Region (e.g.,

Asean)); Analytic criterion: input total return for one year of greater than X% (e.g., 10% or 20%)

g. Fund Type: Exchange-Traded Product; Classification (Asset Class Focus): Equity; Management

Style: Growth or Growth and Income; Analytic criterion: Input total return for one year of greater

than X% (e.g., 10% or 20%)

h. Fund Type: Exchange-Traded Product; Classification (Asset Class Focus): Equity; Management

Style: Value; Analytic criterion: Input total return for one year of greater than X% (e.g., 10% or

20%)

i. Fund Type: Exchange-Traded Product; Classification (Asset Class Focus): Equity; Management

Style: Industry Focus (e.g., Energy).

j. Fund Type: Exchange-Traded Product; Classification (Asset Class Focus): Equity; Management

Style: Classification, Geographical Focus: Select Country or Region (e.g., Eastern European

Region)

k. Fund Type: Fund of Funds; Classification (Asset Class Focus): Equity; Analytic criterion: input

total return for one year of greater than X% (e.g., 10% or 20%)

Select one of the funds from each of your searches and study it using the functions on the fund’s menus screen

(Fund Ticker <Equity> <Enter>. Functions to include: DES, historical fund analysis (HFA), fund holdings

(MHD), relative valuation (RV), and price graph (GP).

6. Use the Bloomberg fund search screen, FSRC, to search for the following types of debt-type funds and ETFs:

a. Fund Type: Open-End; Classification (Asset Class Focus): Debt; Management Style: Total Return;

Analytic criterion: Input total return for one year of greater than X% (e.g., 10% or 20%).

b. Fund Type: Open-End; Classification (Asset Class Focus): Debt; Management Style: Principal

Preservation; Management Style: Maturity band Focus (e.g., Long Term (> 10 years)); Management

Style: Ratings Focus (e.g., Investment Grade); Analytic criterion: Input total return for one year of

greater than X% (e.g., 4% or 10%).

c. Fund Type: Exchange-Traded Product; Classification (Asset Class Focus): Debt; Management Style:

Ratings Focus (e.g., Speculative/High Yield).

40

d. Fund Type: Exchange-Traded Product; Classification (Asset Class Focus): Debt; Management Style:

Ratings Focus (e.g., Investment Grade); Management Style: Maturity band Focus (e.g., Intermediate or

Intermediate/Long).

e. Fund Type: Fund of Funds; Classification (Asset Class Focus): Debt; Analytic criterion: input total

return for one year of greater than X% (e.g., 10%)

Select one of the funds from each of your searches and study it using the functions on the fund’s menus screen

(Fund Ticker <Equity> <Enter>. Functions to include: DES, historical fund analysis (HFA), fund holdings

(MHD), relative valuation (RV), and price graph (GP).

7. Bloomberg’s HFND screen provides a menu for evaluating hedge funds. From the screen, you can access the

WHF screen that ranks hedged funds by category (or you can simply access the screen directly (WHF <enter):

Equity, FI Direct, Event Driven, Emerging Market, Managed Futures, and All Strategies. Using the WHF

screen, examine several hedge funds in different categories. Select several of the funds and study them using

the functions on the fund’s menus screen (Fund Ticker <Equity> <Enter>. Functions to include: DES, historical

fund analysis (HFA), relative valuation (RV), and price graph (GP).

8. Use the Bloomberg fund search screen, FSRC, to search for different types of hedge funds by categories. Hedge

fund categories by style can be screened on the FSRC screen by going to the “Classifications” tab, selecting

“Alternative” style from the “Bloomberg Objective” tab, and then selecting style. That is: Fund Type: Hedge

Fund; Classification (Bloomberg Objective, Alternative): select style. Searches to consider:

Emerging Market Debt

Emerging Market Equity

Event Driven distressed

Event Driven Mergers

Directional Fixed-Income

Global Macro

Multi-Strategy/Multi-Style

Select one of the funds from each of your searches and study it using the functions on the fund’s menus screen

(Fund Ticker <Equity> <Enter>. Functions to include: DES, historical fund analysis (HFA), relative valuation

(RV), and price graph (GP).

9. Use the Bloomberg fund search screen, FSRC, to search for funds of hedge fund: Fund Type: Fund of Hedge

Funds; Analytic criterion: input total return for one year of greater than X% (e.g., 20%). Select one of the funds

from the search and study it using the functions on the fund’s menus screen (Fund Ticker <Equity> <Enter>.

Functions to include: DES, historical fund analysis (HFA), relative valuation (RV), and price graph (GP).

10. Use the Bloomberg fund search screen, FSRC, to search for different types of government,

government/corporate, and global debt funds. That is: Fund Type: Open-end, Exchange-Traded Fund, or

Closed-End Fund; Classification, Bloomberg Objective, Debt: select type; Analytic criterion: input total return

for one year of greater than X% (e.g., 10%). Searches to consider:

Government/Agency—Long Term

Government/Agency—Intermediate Term

Government/Corporate

International Debt

Global Debt

Select one of the funds from your searches and study it using the functions on the fund’s menus screen (Fund

Ticker <Equity> <Enter>. Functions to include: DES, historical fund analysis (HFA), relative valuation (RV),

and price graph (GP).

41

11. Use the Bloomberg fund search screen, FSRC, to search for different types of money market funds. Money

market funds can be screened by going to “Classifications” tab, selecting “Money Market” from “Bloomberg

Objective” tab. That is: Fund Type: Hedge Fund; Classification (Bloomberg Objective, Money Market).

Searches to consider:

Tax-Exempt-State

Taxable Global

Taxable Govt/Agency

Taxable Treasury/Repo

Select some of the funds from your searches and study them using the functions on the fund’s menus screen

(Fund Ticker <Equity> <Enter>. Functions to include: DES, total return (TR), and price graph (GP).

12. Use the Bloomberg fund search screen, FSRC, to search for different types of municipal mutual funds by state.

Funds can be screened by state by going to “Classifications” tab, selecting “Debt” from “Bloomberg Objective”

tab, and then selecting state. That is: Fund Type: Hedge Fund; Classification (Bloomberg Objective, Debt):

select state. Select some of the funds from your searches and study them using the functions on the fund’s

menus screen (Fund Ticker <Equity> <Enter>. Functions to include: DES, historical fund analysis (HFA),

relative valuation (RV), and price graph (GP).

13. Bloomberg’s REIT screen provides a menu for searching for real estate investment trusts by regions: U.S.,

Europe, Asia, Australia, Canada, and other. Using the screens, search and select some REITs from different

regions. Study the REITs using the functions on the REIT’s menus screen (Ticker <Equity> <Enter>).

Functions to include: DES, total return (COMP), relative valuation (RV), holders (HDS), and price graph (GP).

14. Go to the FUND screen to find news and information on mutual funds, hedge funds, and ETFS: FUND <Enter>,

use the “News and Research” links.

15. The hedge fund industry is a leader in creating new investment product. To keep current, go to the BRIEF screen to

access the Bloomberg newsletter: “Hedge Fund.”

16. Many investment funds, ETFs, and hedge funds are constructed to replicate a specific sector or index. Suppose

you were considering constructing a fund or ETF based on an index or style. As a first step, select several

indexes you think would make a good fund\ and study their description and holdings screens. In searching for

indexes, you may want to use the following Bloomberg screens: WEI, <Enter>, SPX <Enter>, RUSS <Enter>,