bluescope asia day india business - amazon s3...page 4 india – steel industry in review fy06 (e)...

TRANSCRIPT

BlueScope Asia DayIndia Business

29 June 2006

Page 2

India – Our business in context

50 : 50 Joint Venture with Tata Steel Tata BlueScope SteelAll agreements finalised 29th May 2006

Will cover all facilities, including:Bhiwadi – LYSAGHT™ rollforming facilityJamshedpur - Metal coating and paint linePune – LYSAGHT™ rollforming facilities

– BUTLER™ PEB and design centreChennai – LYSAGHT™ rollforming facilityColumbo – LYSAGHT™ rollforming facilities

Why JV and not 100%?Great brand recognition of TataBlueScope Steel has trading but limited operating experience in IndiaTata Steel have strong growth ambitions, and a marketing/branding ethos like BlueScope.

Page 3

• Joint Venture Board

• Joint Venture Company Management

Pune

Bhiwadi

Chennai

Jason Ellis (BSL)President Building Solutions

Shantanu Pal (Tata)Chief, Coated Steel

Shyam Sunder (BSL)CFO

Chetan Tolia (Tata)

CEO

India – Joint venture company structure

Chetan Tolia (Tata)CEO

BSLX3 Directors

Kathryn Fagg (BSL)Chairperson

TataX3 Directors

• Head office located in Pune

Page 4

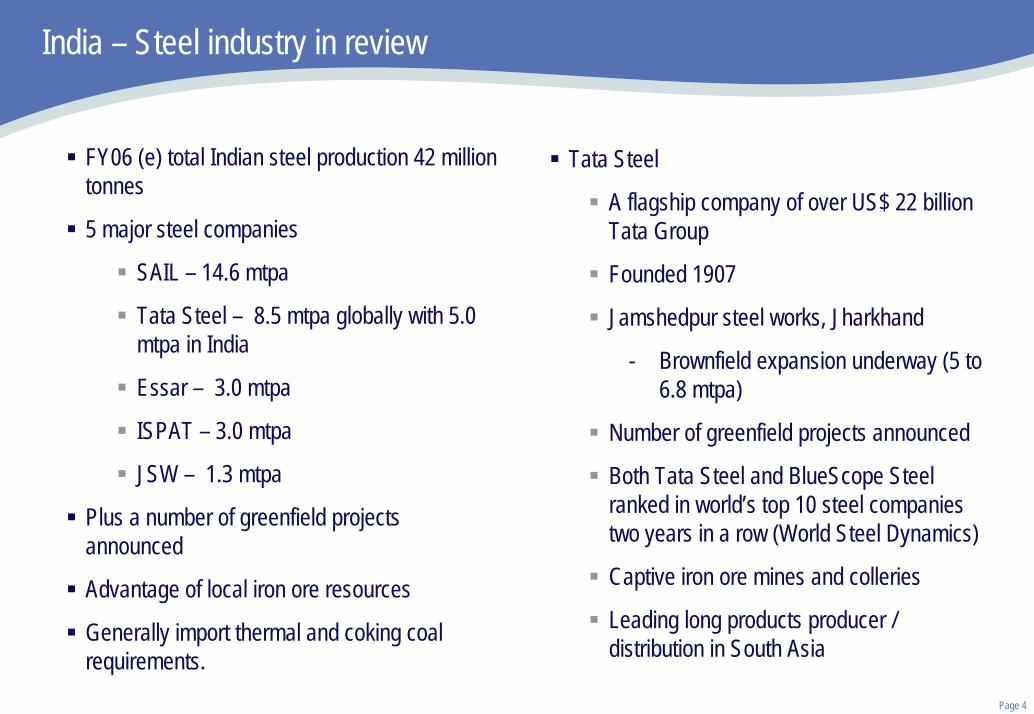

India – Steel industry in review

FY06 (e) total Indian steel production 42 million tonnes

5 major steel companies

SAIL – 14.6 mtpa

Tata Steel – 8.5 mtpa globally with 5.0 mtpa in India

Essar – 3.0 mtpa

ISPAT – 3.0 mtpa

JSW – 1.3 mtpa

Plus a number of greenfield projects announced

Advantage of local iron ore resources

Generally import thermal and coking coal requirements.

Tata Steel

A flagship company of over US$ 22 billion Tata Group

Founded 1907

Jamshedpur steel works, Jharkhand

- Brownfield expansion underway (5 to 6.8 mtpa)

Number of greenfield projects announced

Both Tata Steel and BlueScope Steel ranked in world’s top 10 steel companies two years in a row (World Steel Dynamics)

Captive iron ore mines and colleries

Leading long products producer / distribution in South Asia

Page 5

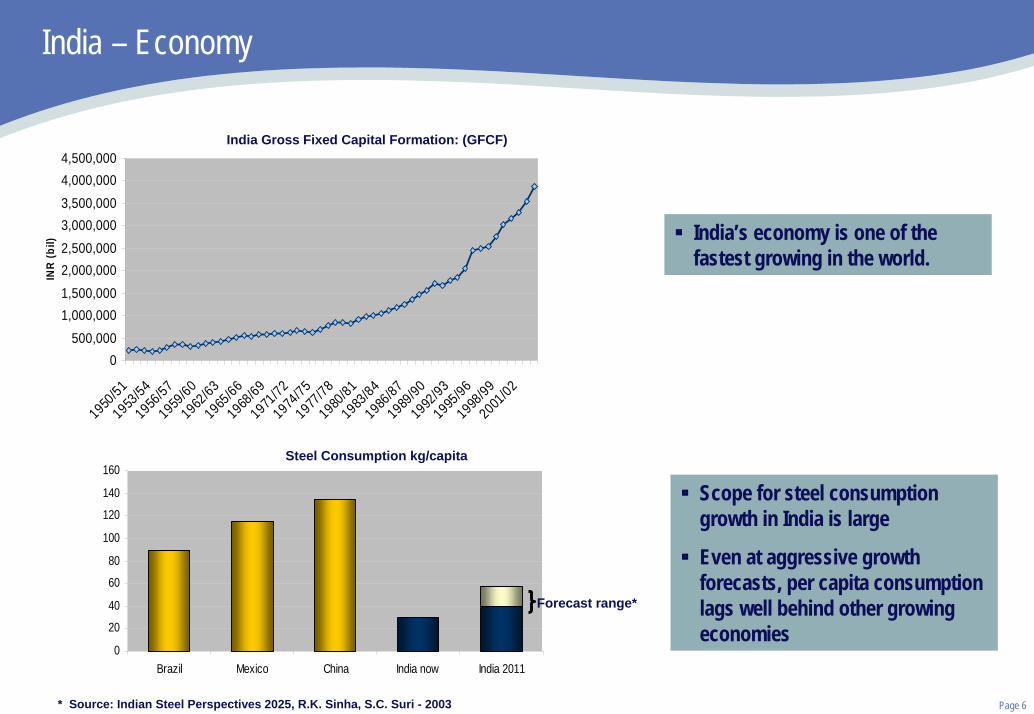

India – Economy

EconomyStrong growth continuesMonsoon has arrived early promising a good year.Continued momentum in reform and privatisation progress is key

Population1.095 billion (June 2006 estimate)

PoliticalEconomic reform underway, but slowContinued changing landscape does not help

Foreign Direct Investment, India

02000400060008000

100001200014000

FY2002 FY2003 FY2004 FY2005 FY2006 FY2007

US$m

illio

n

TargetEstimatedActual

Source: Reserve Bank of India, Press reports

GDP growth (real) - India

0

2

4

6

8

10

FY2002 FY2003 FY2004 FY2005 FY2006 FY2007

%EstimatedActual

Source: IMA Asia

Page 6

India – Economy

0

20

40

60

80

100

120

140

160

Brazil Mexico China India now India 2011

0500,000

1,000,0001,500,0002,000,0002,500,0003,000,0003,500,0004,000,0004,500,000

1950/51

1953/54

1956/57

1959/60

1962/63

1965/66

1968/69

1971/72

1974/75

1977/78

1980/81

1983/84

1986/87

1989/90

1992/93

1995/96

1998/99

2001/02

INR

(bil)

Scope for steel consumption growth in India is large

Even at aggressive growth forecasts, per capita consumption lags well behind other growing economies

Forecast range*

India Gross Fixed Capital Formation: (GFCF)

* Source: Indian Steel Perspectives 2025, R.K. Sinha, S.C. Suri - 2003

Steel Consumption kg/capita

India’s economy is one of the fastest growing in the world.

Page 7

India – New project developments

Approvals

December 2004 (total cost A$100m (BSL’s share A$50m))

− Pune - BUTLER™ PEB facility and design centre

- LYSAGHT™ rollforming facility

− Chennai - LYSAGHT™ rollforming facility

− Bhiwadi (New Delhi) – LYSAGHT™ rollforming facility

November 2005

− JV agreement signed

− Investment approved for Jamshedpur metal coating and paint line (total cost A$265m (BSL’s share

A$132.5m)

All facilities will be owned by the Joint Venture (BlueScope’s share 50%)

Page 8

India – Pune Project Update

BUTLER™ PEB facility and Design Centre

LYSAGHT™ rollforming facility

Original scheduled completion second half CY2006

Commissioning commenced April 2006

First order despatched May 2006

Page 9

India – Chennai project update

LYSAGHT™ sales & rollforming facility

Original scheduled completion - mid CY2007

Likely completion - fourth quarter CY2006

Construction status (using Butler PEB)Earthworks completePrimary framing completeSecondary framing completeRoof & wall under way

Page 10

India – Bhiwadi (New Delhi) project update

LYSAGHT™ sales & rollforming facility

Original scheduled completion – mid CY2007

Likely completion – last quarter CY2006

Construction status (using Butler PEB)Civil, electrical, mechanical, structural now complete10% of equipment is now installed & commissionedOperating licenses under way

Page 11

India – Jamshedpur metal coating and paint line facilities

Coated manufacturing facilities (100%)250ktpa metal coating line150ktpa paint lineSlit / recoil linePackaging line

Original scheduled completion – mid CY2008

Likely completion – fourth quarter CY2008

Delay due to additional engineering and local approvals

Construction statusSite secured and site office establishedSite leveling >30% completeBoundary wall construction commencedEnvironmental License Public Hearing complete

Page 12

India – Feedstock sources

Sources1. Cold rolled coil for the coating line:

Primary source will be from the neighbouring Tata Steel facilityBackup supply is available from other Indian steel manufacturers

2. Rollforming facilities:Currently sourcing metallic coated and pre-painted steel from BlueScope Steel’s Asian and Australasian networkThe JV coating facility at Jamshedpur will be the primary source of metallic coated and pre-painted steel from 2009Other steel inputs are sourced locally or from Australia

Other influencesTariff regime

Indian steel import tariffs are low, at or near WTO levels.no import restrictions for coated steel

Page 13

India – Metal coating line production current expected ramp up profile

Full capacity achieved by 2012

0

50

100

150

200

250

300

FY2007 FY2008 FY2009 FY2010 FY2011

Imports Prime Product Non-PrimeNAMEPLATE CAPACITY 250,000 tpa

000’s tonnes

Page 14

India – Paint line production current expected ramp up profile

NAMEPLATE CAPACITY 150,000 tpa

000’s tonnes

020406080

100120140160

FY2007 FY2008 FY2009 FY2010 FY2011

Imports Prime Product Non-Prime

Full capacity achieved by 2012

Page 15

India – Our markets

0

5

10

15

20

25

JuneQ'04

SepQ'04

DecQ'04

MarQ'04

JuneQ'05

SepQ'05

DecQ'05

% G

DP R

eal

Source: Reserve Bank of India

Construction Sector Growth - India

Reinforced Concrete45%

Steel29%

Others5%

Asbestos Sheet21%

* Industrial Building, Roofing and Walling (Source: Tata BlueScope Steel analysis)

Intermaterial Share*2003/4

Industrial / commercial construction segment is the fastest growing but residential remains the biggestIndustrial construction while only 10% of total construction investment, is expected to grow at CAGR of 33% over the next 5 years (source: CRIS Infac)

Page 16

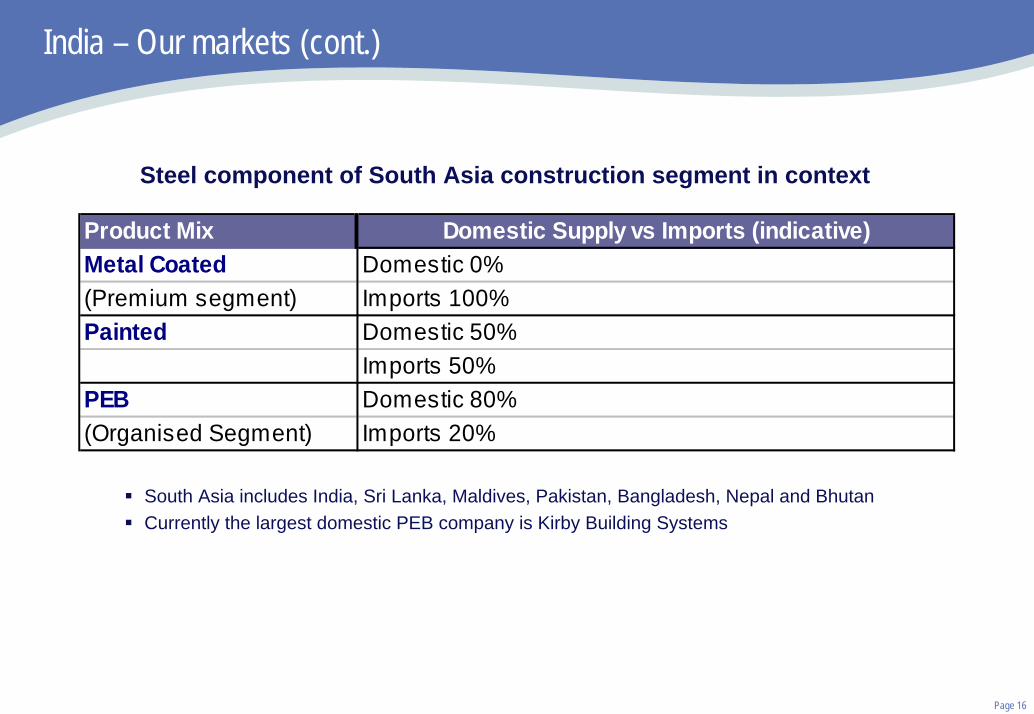

India – Our markets (cont.)

Steel component of South Asia construction segment in context

Product Mix Domestic Supply vs Imports (indicative)Metal Coated Domestic 0%(Premium segment) Imports 100%Painted Domestic 50%

Imports 50%PEB Domestic 80%(Organised Segment) Imports 20%

South Asia includes India, Sri Lanka, Maldives, Pakistan, Bangladesh, Nepal and BhutanCurrently the largest domestic PEB company is Kirby Building Systems

Page 17

India – Our markets (cont.)

Current principal markets are located in:South and west, however strong demand is now being seen in the east as further natural resources are developed

Other regional opportunitiesBangladesh and Pakistan are strong and growing construction marketsBlueScope Steel products are well established in Sri Lanka and Maldives

Channels to marketDirect to building ownersConstruction contractorsRetail / distribution opportunities

Page 18

India – Brand recognition

Coated steel: 4 of the 8 most recognised brands are associated with Tata BlueScope Steel:

46% Tata BlueScope Steel41% BlueScope Steel20% COLORBOND® coated steel19% ZINCALUME® coated steel

Building solutions: 4 of the 8 most recognised brands are associated with TataBlueScope Steel:

42% Tata BlueScope Steel38% BlueScope Steel Building Solutions17% BUTLER™ buildings13% LYSAGHT™ building products

“Tata Steel” is the most widely recognised brand across ALL categories

Source: AC Neilson Brand Awareness Survey, May 2006

Page 19

India – Product flow

Metal Coating Line

Colour Coating Line

Roll Forming Lines

Beam Fabricaton Line

Cold Rolled Coilfrom

Tata Steel

Zinc/Aluminiumcoated steel

Colour coatedsteel

Roll-formed roofingand walling solutions

Pre-EngineeredMetal Buildings

Page 20

India – Our coated steel products

POWER BRANDS - accounting for the majority of mix Alternate products, for specific applications

Bare

AZ70 Zinc / Aluminiumcoated steel

(Truss, GI substitute)

AZ150 Zinc / Aluminiumcoated steel

(Economical colour coated steel)

TEXTURA™(woodgrain finish coated steel)

INTERBOND™(for interior, false ceiling applications)

Pain

ted COLORBOND® range of coated

steel products:COLORBOND® Ultra

COLORBOND® XRWCOLORBOND® XPD

COLORBOND® Metallic

Page 21

India – Our building solutions products

Pre-Engineered Buildings

Best in class, premium quality metal buildings for industrial and commercial segments

Lower priced metal buildings for industrial and commercial segments

Range of buildings from cold formed steel structural elements – light buildingsSMARTBUILDTM

Roofing & Walling

Range of top quality roofing and walling solutions

Page 22

India – Opportunities / challenges

Opportunities

Rapid growth in industrial and commercial buildings – the primary target for both the coated steel and building solutions businesses

Eastern India is growing rapidly (from a buildings perspective)

Development of South Asian Association for Regional Cooperation (SAARC) countries (in particular Bangladesh and Pakistan) will offer many opportunities to Tata BlueScope Steel

Challenges

Skilled employee retention is challenging

Tax : sound indirect tax management is more of a competitive advantage in India as opposed to a compliance issue

Rapid growth but poor infrastructure makes a difficult business environment for start ups such as Tata BlueScope Steel for basic goods and services

Page 23

India – Summary

Tata BlueScope Steel 50/50 Joint Venture is establishing a good base for growth in SAARC countries

Downstream business (Buildings Solutions Division)

Facilities coming on stream now

Market reaction to commencement of operations has exceeded our expectations

Midstream business (Coated Steel Division)

Demand for flat steel in construction is growing at a high rate, off a low base

Market seeding program (importing) is accelerating to keep up with domestic demand growth

Construction activity has commenced for the domestic coating line facility

Tata BlueScope Steel challenge is to meet the high expectations of the market, not only in India but also in the other SAARC countries.

BlueScope Asia DayIndia Business

29 June 2006