bofaml banking & insurance conference rsa insurance …€¦ · bofaml banking & insurance...

TRANSCRIPT

BofAML BANKING & INSURANCE CONFERENCE

30 September 2014

Stephen Hester

Group Chief Executive

RSA Insurance Group: Path to Performance

This presentation may contain ‘forward-looking statements’ with respect to certain of the Group’s plans and its current

goals and expectations relating to its future financial condition, performance, results, strategic initiatives and objectives.

Generally, words such as “may”, “could”, “will”, “expect”, “intend”, “estimate”, “anticipate”, “aim”, “outlook”, “believe”,

“plan”, “seek”, “continue” or similar expressions identify forward-looking statements. These forward-looking statements

are not guarantees of future performance. By their nature, all forward-looking statements involve risk and uncertainty

because they relate to future events and circumstances which are beyond the Group’s control, including amongst other

things, UK domestic and global economic business conditions, market-related risks such as fluctuations in interest rates

and exchange rates, the policies and actions of regulatory authorities (including changes related to capital and solvency

requirements), the impact of competition, inflation, deflation, the timing impact and other uncertainties of future

acquisitions or combinations within relevant industries, as well as the impact of tax and other legislation or regulations in

the jurisdictions in which the Group and its affiliates operate. As a result, the Group’s actual future financial condition,

performance and results may differ materially from the plans, goals and expectations set forth in the Group’s forward-

looking statements. Forward-looking statements in this presentation are current only as of the date on which such

statements are made. The Group undertakes no obligation to update any forward-looking statements, save in respect of

any requirement under applicable law or regulation. Nothing in this presentation should be construed as a profit forecast.

TODAY’S PRESENTATION UPDATES ON…

3

Design slide

s s 0

What RSA will

look like as we

complete the

‘turnaround’

plan

How we have

thought through

what needs to

be done

What we are

doing and

planning to do

to drive

performance

1 2 3

FOCUSED; STRONGER; BETTER

4

A leading international general insurer focused on Northern developed

markets, plus a growth business in Latin America

Aiming to compete only where we can win. And to win where we compete

Well capitalised, targeting sustainable attractive returns

Strong operational delivery; transparent and easy to understand

Enduring customer appeal

1

2

3

4

5

Our ambition for RSA:

WHAT WILL MAKE RSA ATTRACTIVE

5

Leading market positions

in stable markets

Well balanced business

by geography, customer,

channel and product

Capital efficiency from

diversification

Cash generative

business model

Group synergies of

expertise, cost and

revenues

Disciplined and

focused execution

Strong brands and market

reputation

RSA’S CORE MARKETS – BUILT AROUND LEADERSHIP POSITIONS

6

Canada

Market size2: £27bn

Top 3 market position

overall

67% Personal,

33% Commercial lines

Broker and affinity

distribution

Latin America

Market size2: £62bn

No.1 Chile, No.2 Uruguay,

No. 6 Argentina, Leading

niche position in Brazil.

Operations in Mexico and

Colombia

UK

Market size2: £42bn

Top 4 market position

overall

45% Personal,

55% Commercial lines

Direct, broker and affinity

distribution

Scandinavia

Market size2: £21bn

Top 4 market position

overall

Only multi-national insurer in

the region

51% Personal,

49% Commercial lines

Principally direct distribution

Scandinavia30%

Canada20%

Latin America

10%

UK1

35%

Ireland5%

Indicative

future shape

of the core

Group (share

of NWP)

1 Includes European commercial lines2 Approximate size of non-life market premiums. Source: Swiss Re Sigma 3/2014

Household22%

Personal Motor20%

Personal Other10%

Commercial Property

20%

Liability10%

Commercial Motor

9%

Marine & other9%

RSA’S BUSINESS MIX - WELL BALANCED

7

By customer and product…

Commercial48%

Personal

52%

Pro-forma

for core

business

based on H1

2014 NWP

Pro-forma

for core

business

based on H1

2014 NWP0% 25% 50% 75% 100%

UK Personal

UK Commercial

ScandinaviaPersonal

ScandinaviaCommercial

Canada Personal

Canada Commercial

Direct Broker Agent/affinity

… and by distribution channel

P&C MARKET CHARACTERISTICS INFORMING RSA’S STRATEGY

8

Large, enduring

and stable markets

Proactive mainstream

players holding their

own vs specialists /

disruptors

Business models

need to cope with

market cycles and

underwriting volatility

Important evolutions in

customer expectations,

regulation and technology,

as in other industries

Scale important, but

principally at a market

level, not globally

Competitive and

challenging markets,

consolidated structure, no

patents, so most players

doing similar things

Few existential

threats or

transformative

opportunities

General

insurance

markets

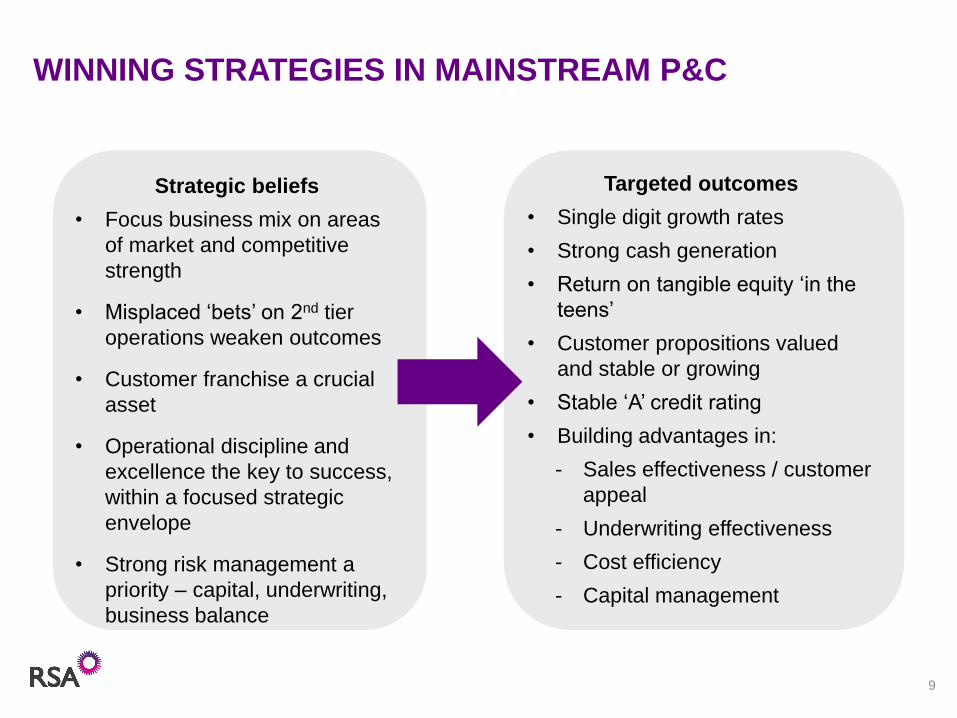

WINNING STRATEGIES IN MAINSTREAM P&C

9

Strategic beliefs

• Focus business mix on areas

of market and competitive

strength

• Misplaced ‘bets’ on 2nd tier

operations weaken outcomes

• Customer franchise a crucial

asset

• Operational discipline and

excellence the key to success,

within a focused strategic

envelope

• Strong risk management a

priority – capital, underwriting,

business balance

Targeted outcomes

• Single digit growth rates

• Strong cash generation

• Return on tangible equity ‘in the

teens’

• Customer propositions valued

and stable or growing

• Stable ‘A’ credit rating

• Building advantages in:

- Sales effectiveness / customer

appeal

- Underwriting effectiveness

- Cost efficiency

- Capital management

CHALLENGES FOR RSA AT THE START OF 2014

10

Capital Erosion Reliance on Prior Year

Expenses Industry issues

• Weather trends

• Technology spend and effectiveness

• Underwriting discipline and competition

• Low yield environment

0

20

40

60

80

100

120

2008 2009 2010 2011 2012 2013

Key capital metrics 2008 – 2013(2008 = 100)

TNAV: Premiums IGD Surplus ECA Surplus

6.46.0

5.24.7 4.8 5.0

0

2

4

6

8

-100

0

100

200

300

400

2008 2009 2010 2011 2012 2013Normalised

Group Underwriting Profits and Reserve Margin2008 - 2012

PYD CY Margin as % reserves

£m %

1 2

43

30

20

25

35

28.6

G

27.5

FED

28.2

CPeer

average

29.0

B

31.1

RSA

31.2

29.6

1.6

A

33.8

28.1 28.0

RSA headline ratioAdjustment due to central costs not included

in RSA’s headline expense ratio that are

generally included in peers’ expense ratios

Total expense ratio1 vs. peer group2, 2012, %

1 Includes commissions2 Peer group includes: Ace, Allianz, Aviva, AXA, Generali, QBE, Zurich

BENCHMARKING PERFORMANCE –THOUGH BUSINESS MIX ALSO A DRIVER

11

UK

Scandinavia

Canada

Source: As reported in published financial statements.

*Peer group consist of:

1) UK: Aviva, DLG, AXA (UK&I), Allianz and Zurich

2) Scandinavia: Top, Tryg, Gjensidige and If. Expense ratio for Top and Tryg reported on a GEP basis and has been recalculated to be on a NWP basis.

3) Canada: Intact, Aviva, Cooperators and Economical.

Note that there may be slight differences in accounting treatment for COR and ER between local peers and RSA.

Peer* Combined Ratio 2013 Peer* Expense Ratio 2013

99.2%95.2% 96.9% 35.1%29.0% 32.4% 34.1%

91.5%87.7% 88.9% 19.1%15.3% 16.9%

104.1%94.6% 100.6%99.5% 32.9%28.9% 31.4%

HighestLowest

RSA

HighestLowest

RSA

RSA RSA

RSA

(ex. Noraxis)RSA

(ex. Noraxis)

Mean Mean

Mean Mean

Mean Mean

88.1%

STRATEGY AND ACTION PLAN FOR RSA

12

1. Tighten strategic focus of the Group

• Disposals and portfolio action

• Concentrate resources and management effort on a coherent core

2. Reset the quality and quantity of capital strength

• The bar is higher for financial institutions than before

• Trust in risk profile and quality of financial statements a must

• RSA was undercapitalised at the end of 2013

3. Improve business performance and capability to sustain it

• Actions, where needed, on underwriting, portfolios, expense and distribution

• Invest in technology to drive competitive advantage

• High performance, disciplined culture. Build track record of delivery

Serve customers well. Operate with capital strength.

Focus on driving shareholder value

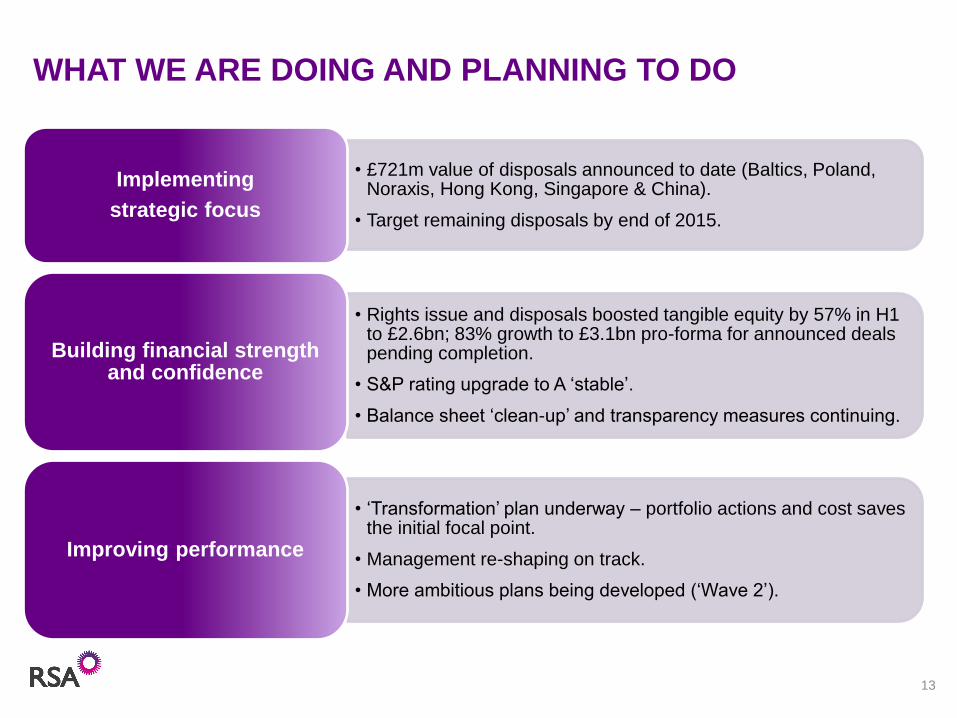

WHAT WE ARE DOING AND PLANNING TO DO

13

• £721m value of disposals announced to date (Baltics, Poland, Noraxis, Hong Kong, Singapore & China).

• Target remaining disposals by end of 2015.

Implementing

strategic focus

• Rights issue and disposals boosted tangible equity by 57% in H1 to £2.6bn; 83% growth to £3.1bn pro-forma for announced deals pending completion.

• S&P rating upgrade to A ‘stable’.

• Balance sheet ‘clean-up’ and transparency measures continuing.

Building financial strength and confidence

• ‘Transformation’ plan underway – portfolio actions and cost saves the initial focal point.

• Management re-shaping on track.

• More ambitious plans being developed (‘Wave 2’).

Improving performance

ACTION PLAN – TARGET TIMELINE

14

2014 2015 2016

Strategic focus

Capital & balance sheet strengthening

Operational improvement

2017

• Core / review portfolio

• First wave of

disposals

• Complete disposal

programme

• Proceeds from rights

issue, disposals & earnings

• Balance sheet ‘clean up’

• Sub-debt opportunity

• Further disposals &

earnings

• Target restart of

dividends

• Preparation for

Solvency II

• Transformation plan

• Management team

• Implementation starts:

- Cost base

- Portfolio actions

• Assess scope to go

Further (‘Wave 2’)

• Implementation:

- Cost base

- Underwriting / sales

effectiveness

- Systems investment

• ‘Wave 2’ initiatives

commencing

• Benefits building

• Implementation:

- Cost base

- Underwriting / sales

effectiveness

• Benefits building

• ‘Wave 2’ initiatives

continue

• Systems Investment

Cleaner

benefits

‘run rate’

‘Wave 2’

initiatives

continue

P&C peer group growth H1

2014

-1%

2%

-2%

-4% -2% 0% 2% 4%

MARKET DYNAMICS FORCING EVEN MORE EMPHASIS ON OPERATIONAL IMPROVEMENT

15

Market conditions:

• Most markets highly competitive

• Softening wholesale insurance rates putting pressure down the value chain

• Low interest rates pressuring investment income

High volume/price

sensitivity

RSA H1 2014 underlying trend:

% change in

NWPRate Volume

Scandinavia 3% (1)%

Canada 2% (4)%

UK 2% (10)%

Ireland 5% (21)%

Emerging

Markets2% 5%

Total Group 2% (5)%

Source: Company results

Note: UK peer group includes Aviva, AXA, Zurich, Allianz, DLG; Scandinavia peer group includes If, Tryg, Gjensidige, Lansforsakringar, Topdanmark;

Canada peer group includes Intact, Aviva, Co-operators, Desjardins, Economica

UK

Scandinavia

Canada

5 year government bond

yields 2014 YTD

0

0.5

1

1.5

2

2.5

%

UK

Canada

Sweden

Euro

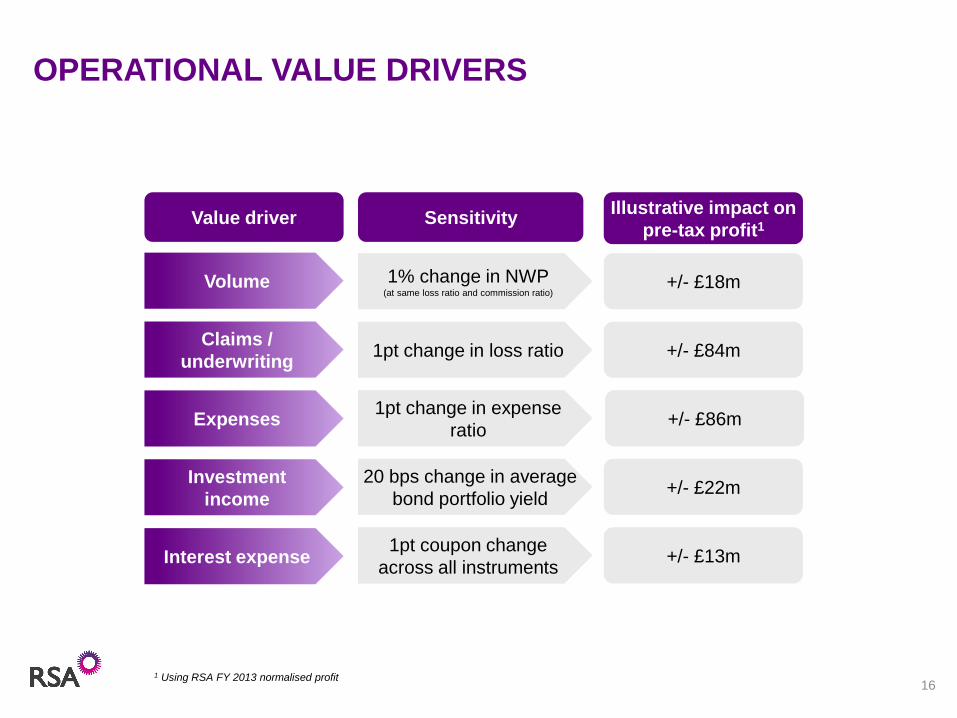

OPERATIONAL VALUE DRIVERS

16

Volume

Claims /

underwriting

Expenses

Investment

income

Interest expense

1% change in NWP(at same loss ratio and commission ratio)

1pt change in loss ratio

1pt change in expense

ratio

20 bps change in average

bond portfolio yield

1pt coupon change

across all instruments

+/- £18m

+/- £84m

+/- £86m

+/- £22m

+/- £13m

Value driver SensitivityIllustrative impact on

pre-tax profit1

1 Using RSA FY 2013 normalised profit

17

1

OPERATIONAL ACTIONS – SALES EFFECTIVENESS / CUSTOMER APPEAL

Customer Actions

• Distribution Retain direct/ broker/ affinity choice for clients. Affinity growth

in focus particularly

• Speed, convenience

and flexibility

Digital trends at the forefront of customer evolution

• Proposition Drive to sharpen targeted customer propositions

• Service Differentiate on service standards and delivery

• Satisfaction Target strong positive NPS and effective brand promise

Sales Actions

• Salesforce effectiveness Multiple disciplines to improve delivery to customers

• Trading capabilities Greater market responsiveness in pricing and policy make up

• Pricing expertise Richer risk segmentation

• E-trading / SME

competencies

Drive “industrialisation” of SME delivery for price

competitiveness and growth

1

2

UK Personal Household

UK Personal Motor

UK Pet

UK Commercial Motor

UK Commercial Property

UK Commercial Liability

UK Marine

Scandi Household

Scandi Motor

Scandi Personal Other

Scandi Commercial Motor

Scandi Commercial Property

Scandi Commercial Liability

Scandi Marine

Canada Household

Canada Personal Motor

Canada Commercial Property

Canada Liability Canada Marine

50

60

70

80

90

100

110

120

130

-15-10-50510

Th

ree y

ear

Ave

rag

e C

OR

% (

201

1-1

3)

Change in current year underlying loss ratio - H1 2014 vs H1 2013

OPERATIONAL ACTIONS – UNDERWRITING EFFECTIVENESS

18

Lower loss ratioHigher loss ratio

Enhancing RSA’s

underwriting effectiveness

• Improve sophistication,

agility and flexibility of rating

platforms

• Reduce the number of

products and simplify

processes that support them

• Improve robustness and

consistency of process to

move from technical rates to

‘trading’ price

• Improve frequency of

updating claims cost models

• Improve MI / data

warehousing

Driving pricing discipline / portfolio action

OPERATIONAL ACTIONS – COSTS; WITH MORE TO DO….

19

2013 ownexpense base

Foreignexchange

Inflation Disposals Costreductions

2016 indicativecost base

£2.2bn

In excess of

£180m gross cost

reductions by end

of 2016

1 Cost reduction range as a percentage of each region’s 2013 controllable expense base less foreign exchange and disposals impact.2 Includes Emerging Markets head office costs.

RegionUnderlying cost

reduction range1

UK 18% - 19%

Ireland 11% - 13%

Scandinavia 2% - 3%

Canada 2% - 3%

Emerging Markets (ex

review businesses) 2 12% - 14%

Head office 13% - 15%

Cost Initiatives

- Simplification of end-to-end processes through redesign and automation of processes, e.g.

avoiding waste in re-keying of data via simpler, fewer systems

- Transformation of our information systems through rationalisation of complex architecture,

decommissioning of obsolete systems and renegotiation of unfavourable contract conditions

- Optimisation of procurement, renegotiating main contracts to bring them in line with market

best practice and improving adherence to quality standards

- Streamlining of spans, layers and support functions, reducing the number of managers

and the number of management layers

- Simplification of our product offering

- Optimisation of footprint, consolidating offices and branches where beneficial

Indicative movement in cost base 2013-16

‘BELOW THE LINE LEAKAGE’ ALSO IN FOCUS

20

£m

FY 2013

normalised

results

Underwriting profit 309

Investment result 365

Insurance result 674

Central expenses (73)

Operating result 601

Interest expense (117)

Amortisation (42)

Other (incl. Solvency II) (15)

Profit before tax 427

Major improvements targeted:

1. Restructure of Group Head Office

functions

2. Opportunity to refinance sub-debt

at lower coupon

3. Amortisation is non-cash / capital

item

4. Solvency II to be in ‘business as

usual’ in 2016

‘Leakage rate’: 37% of Insurance Result

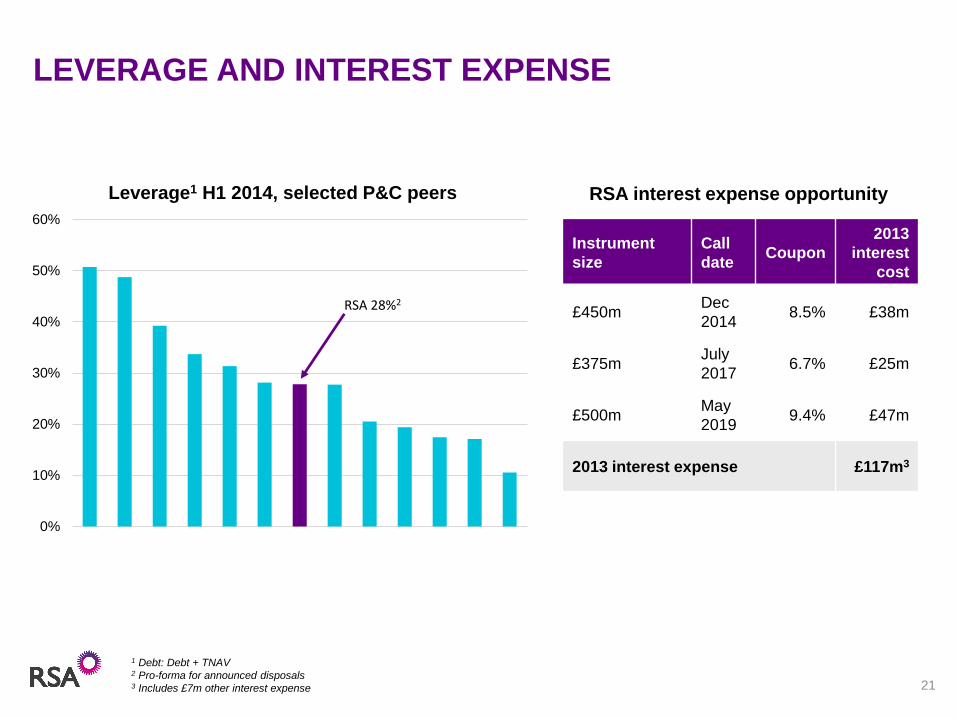

LEVERAGE AND INTEREST EXPENSE

21

Instrument

size

Call

dateCoupon

2013

interest

cost

£450mDec

20148.5% £38m

£375mJuly

20176.7% £25m

£500mMay

20199.4% £47m

2013 interest expense £117m3

RSA interest expense opportunity

0%

10%

20%

30%

40%

50%

60%

Leverage1 H1 2014, selected P&C peers

RSA 28%2

1 Debt: Debt + TNAV2 Pro-forma for announced disposals3 Includes £7m other interest expense

19.2%

33.3%

38.8%2.0%

9.5%

2.6%

5.5%

RSA TNAV:Premium development

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

P&C TNAV:Premium ratios (H1 2014)

RESTORING CAPITAL STRENGTH, RETAINING

BENEFITS OF BUSINESS BREADTH

22

Target range 35-45%Outlook:

Further

disposals

Future

retained

earnings

‘Clean up’ /

restructuring

charges

Note: TNAV:NWP ratios calculated using two times H1 2014 NWP

Generally niche /

specialty or monoline

insurers

Generally

international

multi-line players

Upper end of RSA’s

35-45% target

Source: Company financials

Note: For composite insurers, reported economic capital allocation is used

to determine TNAV allocated to P&C business.

Focused:

• Market leading businesses in Northern developed markets

• Growth business in Latin America

Stronger:

• Well capitalised, targeting sustainable attractive returns

• Business balance; strong risk management

Better:

• Strong customer appeal

• Operational improvements the focus: underwriting and costs especially

• Transparent and easy to understand

SUMMARY

23