bonds issued by authorities under the city revitalization and improvement zone law

TRANSCRIPT

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Beyond the Plain Vanilla Bond Issue:

Bonds Issued by Authorities Under the City Revitalization and Improvement Zone

(CRIZ) Law

Timothy J. Horstmann

717.237.5462

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Origins

Originally created by Act 52 of 2013; substantially amended by passage of Act 84 of 2016.

Program is administered jointly by the Department of Community and Economic Development (DCED), Department of Revenue, and the Governor’s Office of the Budget.

72 P.S. § 8801-C

2

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Origins

Program Focus – “provide opportunity to spur new growth in cities that have struggled to attract development, helping to revive downtowns and create jobs for the residents in the regions....”

DCED Program Guidelines, November 2014 (DCED has not yet revised its Guidelines to reflect the substantial changes made by 2016 Amendment).

3

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Origins

Program is similar in purpose to other Commonwealth-run economic development programs – but is meant to be an alternative

CRIZ zone cannot overlap with numerous state-administered “keystone zone” and similar programs (e.g., KOZ’s, KOEZ’s, KOIZ’s, KIZ’s)

But – no mention in statute of Local Economic Revitalization Tax Assistance Act (LERTA)

4

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Forming a CRIZ Authority

CRIZ Authority may be formed by a city, municipality or home rule county.

Certain entities are excluded

E.g. - A city that is enrolled in Act 47 and located in a home rule county may not form a CRIZ Authority. The home rule county may instead form a CRIZ Authority on the distressed city’s behalf.

5

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Forming a CRIZ Authority

CRIZ Authority may be a new entity, or municipality may designate an existing entity as the CRIZ Authority

Must be formed under Municipality Authorities Act, Third Class County Convention Center Authority Act or the County Code.

CRIZ Authority effectively has a life of thirty years, measured from the creation of the CRIZ Zone.

6

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Power and Projects of a CRIZ Authority

CRIZ Authority may:

o Designate the CRIZ zone

o Engage in acquisition, development, construction, including “infrastructure” and site preparation, reconstruction or renovation of “facilities”

o Engage in public or private financing

o Utilize tax revenues for purposes permitted by CRIZ Law

7

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Power and Projects of a CRIZ Authority

Facility – “a structure ... in a zone to be used for commercial, industrial, sports, exhibition, hospitality, conference, retail, community, office, recreational or mixed-use purposes”

Infrastructure – “any improvements in or out of the zone primarily related to the development of and required by a facility in the zone”

o Specifically includes: utilities, water, sewer, storm water, parking, road improvements or telecommunications

8

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Power and Projects of a CRIZ Authority

Permitted uses of tax revenues:

o Acquisition, development, construction, including related infrastructure and site preparation, reconstruction, renovation or refinancing of all or a part of a facility

o Improvement or development of all or part of a zone

o Payment of debt service on bonds issued to finance or refinance above

o Replenishment of amounts in debt service reserve funds established to pay debt service on bonds

9

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Power and Projects of a CRIZ Authority

Permitted uses of tax revenues:

o Employment of an independent auditing firm to audit the CRIZ Authority’s list of businesses in the zone

o Improvement projects, including fixtures and equipment for a facility owned, in whole or in part, by a public authority

o Payment or reimbursement of reasonable administrative, auditing and compliance services (but not professional services); costs may not exceed 5% of tax revenues

10

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Power and Projects of a CRIZ Authority

CRIZ Authority also possesses powers granted to it by the law under which it was incorporated.

Similarly, its exercise of those powers – and the powers granted by the CRIZ Act – are limited by that law.

Consult incorporating statute before proceeding

11

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Establishment and Approval of the CRIZ Zone

CRIZ Zone may not exceed 130 acres, and may include an area in one or more contiguous municipalities.

CRIZ Authority must hold at least one public hearing on the plan for designation of the zone, and post name and address of business and property owners in the zone

12

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Establishment and Approval of the CRIZ Zone

CRIZ Authority must submit an application to DCED for plan approval, which must include the following:

o Map of the proposed zone – including parcel numbers

o Economic development plan – identify facilities, bonds to be issued, etc.

o Be specific – include infrastructure and site preparation, reconstruction/renovation

o DCED may request additional information or outline other requirements

13

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Establishment and Approval of the CRIZ Zone

Application must be approved by DCED, Revenue, and Budget

While CRIZ Law outlines factors to consider in approving a plan, agencies have discretion in choosing whether to approve.

14

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Establishment and Approval of the CRIZ Zone

How Many CRIZ Zones will be approved?

o CRIZ Law originally provided only for approval of three CRIZ Zones, which were awarded to Cities of Lancaster and Bethlehem, and Borough of Tamaqua.

o 2016 Amendment – permits the creation of up to two additional CRIZ Zones in each calendar year, beginning in 2016.

15

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Establishment and Approval of the CRIZ Zone

To date, no new zones have been approved

May not see new zones until next administrationo Wolf Administration recently rejected all applications received under

KOZ program on basis of unaffordability and lack of “equity” in state’s tax system generally, and similarly announced no new CRIZ Zones as well.

o Can Administration refuse to implement new

provisions of CRIZ Law using this justification?

16

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Funding a CRIZ Authority

CRIZ Law sends tax revenues generated within the zone above “baseline” to the CRIZ Authority, instead of Harrisburg.

Each business within zone must file reports with Department of Revenue and local taxing authority to assist in identifying the amount of revenue to be transferred to CRIZ Authority

17

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Funding a CRIZ Authority

What taxes are included?o Corporate net income tax, capital stock and franchise tax, bank

shares tax, business privilege tax and personal income tax attributable from pass-through business ownership

o Amusement tax

o Sales and use tax

o Hotel occupancy tax

o Personal income tax

o Local services tax

o Earned income tax

o Liquor, wine or malt or brewed beverage taxes

18

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

The CRIZ Law

Funding a CRIZ Authority

Calculation and Transfer of Revenues

o June 15 – deadline for businesses to file reports

o Department of Revenue and taxing authority calculate the amount of eligible taxes generated by each business within the zone

o Calculation is done business-to-business, with no

netting

19

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Why Issue Bonds? Three Possible Scenarios

Fund Grants for Economic Development in CRIZZone

CRIZ Authority borrows money and uses proceeds to fund grants for economic development within the CRIZ Zone.

May be paired with a plan to directly return a portion of the zone business’ share of eligible tax revenues that were received by the CRIZ Authority.

20

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Why Issue Bonds? Three Possible Scenarios

Fund Infrastructure Improvements in CRIZ Zone

CRIZ Authority borrows money and uses proceeds to fund needed infrastructure improvements in or out of the zone that are related to zone facilities

CRIZ Authority works with local businesses and developers to identify the needed improvements and ensure that improvements complement plans for economic development

21

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Why Issue Bonds? Three Possible Scenarios

Acquire Derelict Properties for Rehab and Reuse

CRIZ Authority borrows money and uses proceeds for site acquisition, cleanup, etc. to remove blight and enhance property values

CRIZ Authority partners with developers and local businesses to identify problem properties and assist in redevelopment

22

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

How Does This Work?Structuring a CRIZ Financing

Key Considerations in Structuring Transaction

Indenture Framework – Flow of Funds

o Close attention should be paid to flow of funds under the Indenture, to ensure that it matches up with the flow of funds outlined in the CRIZ Law

o Debt service payments on Bonds should be timed to receipt of funds from State Treasury

23

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

How Does This Work?Structuring a CRIZ Financing

Key Considerations in Structuring Transaction

Other Critical Transaction Documents may vary depending on nature of project financed by the Bonds

o E.g., if proceeds will be used to fund grants –consider establishing a standard form of grant agreement that addresses the use of funds, tax compliance, etc.

24

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

How Does This Work?Structuring a CRIZ Financing

Key Considerations in Structuring Transaction

Security for Obligations

o Obligations principally secured by tax revenues received by CRIZ Authority under CRIZ Law

o Debt Service Reserve Fund may be necessary to offer additional security in the event of delays in receipt of funds

o Is that sufficient security? Consider provisions of the CRIZ Law.

25

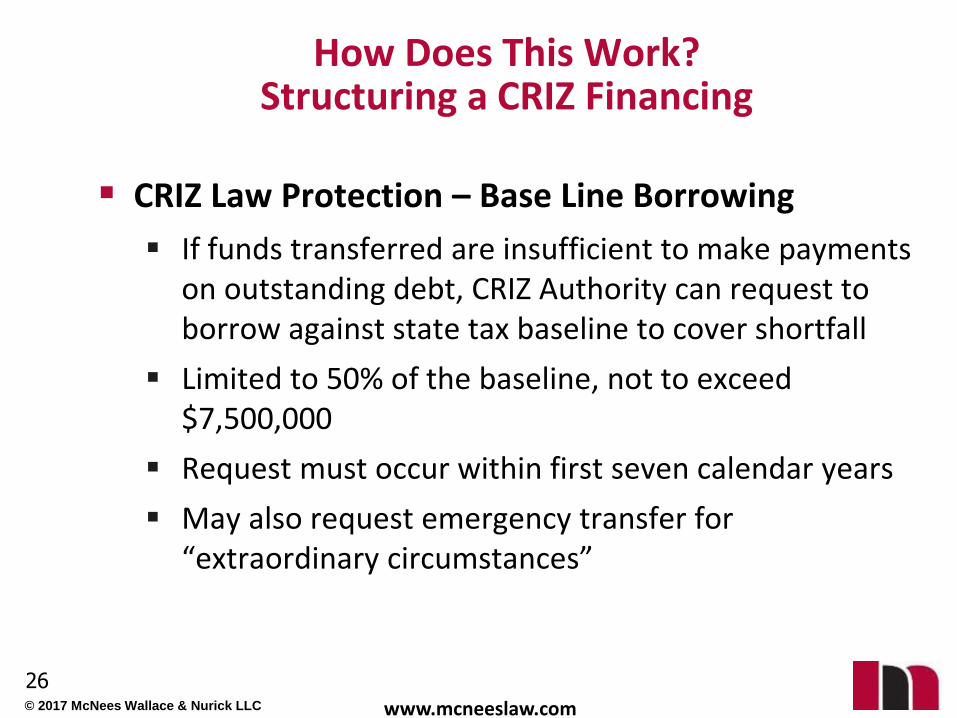

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

How Does This Work?Structuring a CRIZ Financing

CRIZ Law Protection – Base Line Borrowing

If funds transferred are insufficient to make payments on outstanding debt, CRIZ Authority can request to borrow against state tax baseline to cover shortfall

Limited to 50% of the baseline, not to exceed $7,500,000

Request must occur within first seven calendar years

May also request emergency transfer for “extraordinary circumstances”

26

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

How Does This Work?Structuring a CRIZ Financing

CRIZ Law Protection – Base Line Borrowing

Amounts transferred are loans – and must be paid back within twelve years

Failure to repay results in the liability shifting from the Authority to the municipality which created it – with a 10% penalty

Could municipality be forced to raise taxes to repay the loan?

27

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

How Does This Work?Structuring a CRIZ Financing

Other CRIZ Law Protections

State Pledges not to:

o Abolish or reduce the size of the zone, or transfer zone designation from a parcel contrary to CRIZ Law

o Amend or repeal certain provisions of CRIZ Law that are to the detriment of the issuer of any bonds

o Limit or alter the rights vested in CRIZ Authority in a manner inconsistent with the obligations of CRIZ Authority

o Impair revenue to be paid to CRIZ Authority necessary to pay debt service

28

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

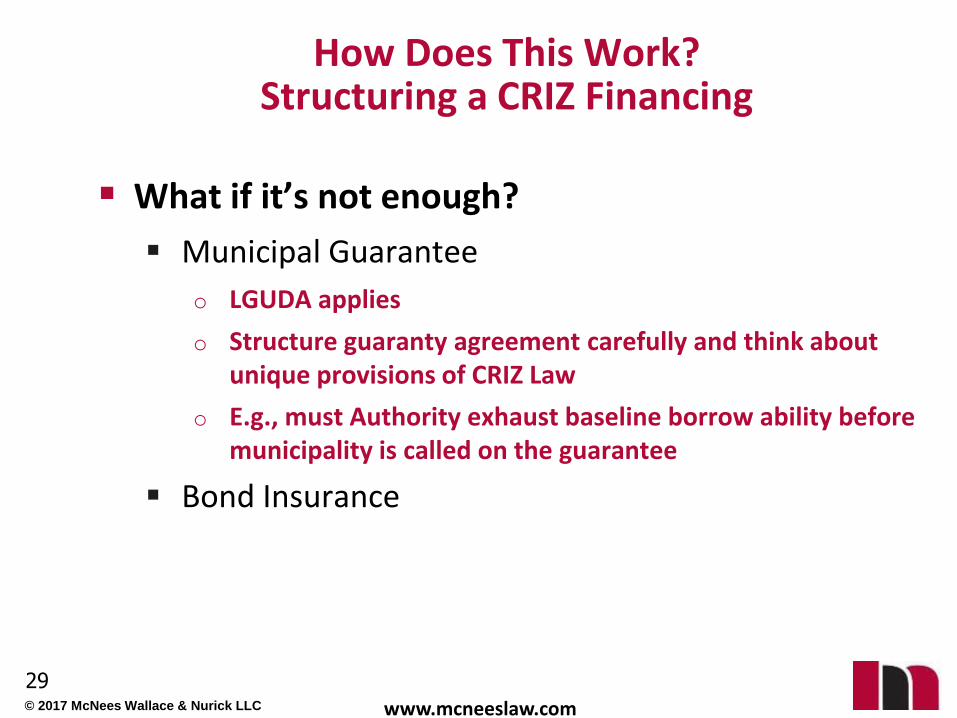

How Does This Work?Structuring a CRIZ Financing

What if it’s not enough?

Municipal Guarantee

o LGUDA applies

o Structure guaranty agreement carefully and think about unique provisions of CRIZ Law

o E.g., must Authority exhaust baseline borrow ability before municipality is called on the guarantee

Bond Insurance

29

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Private Activity Bond Concerns

A Bond is a Private Activity Bond (and therefore taxable) if it meets:

o (1) the Private Business Use Test and the Private Security or Payment Test; or

o (2) the Private Loan Financing Test

30

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Private Business Use Test

Test is met if more than 10% of the proceeds of the issue are to be used in the trade or business of any person other than a governmental unit

Reduced to 5% where the private business use is unrelated to the governmental use or exceeds the governmental use

31

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

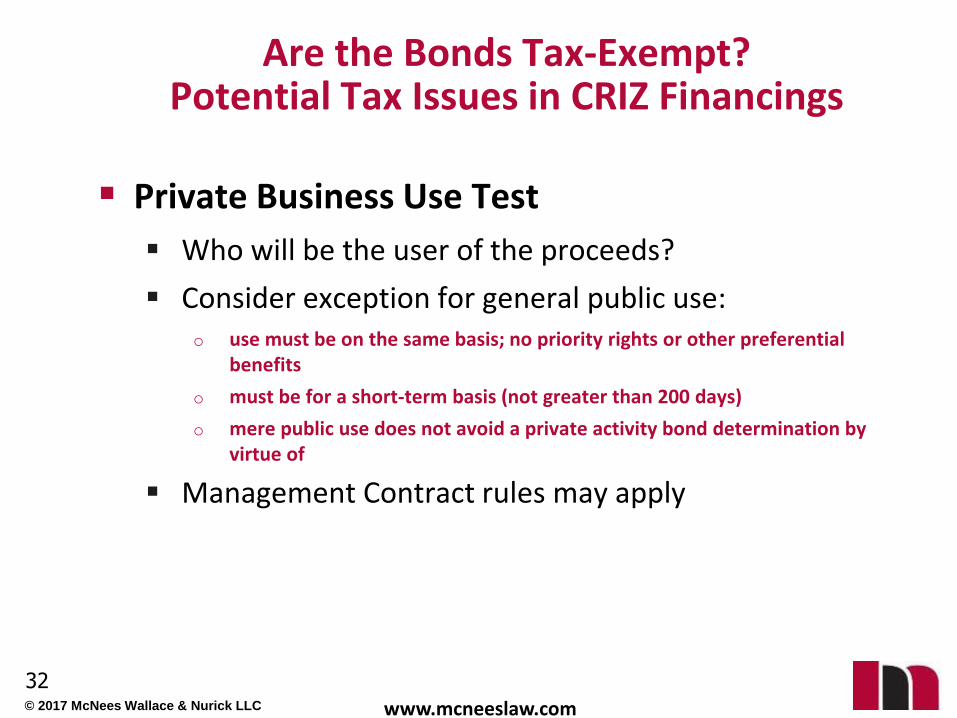

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Private Business Use Test

Who will be the user of the proceeds?

Consider exception for general public use:o use must be on the same basis; no priority rights or other preferential

benefits

o must be for a short-term basis (not greater than 200 days)

o mere public use does not avoid a private activity bond determination by virtue of

Management Contract rules may apply

32

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Private Security or Payment Test

Test is met if more than 10% of the payment of principal of or interest on the issue is, directly or indirectly, secured by property used in a trade or business, or derived from payments related to property used in a trade or business

Reduced to 5% where the private business use is unrelated to the governmental use or exceeds the governmental use)

Remember – must meet both tests for bonds to be private activity bonds

33

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Private Security or Payment Test

Exception for “Generally Applicable Taxes”o Are the taxes paid by zone businesses “generally applicable”?

o Treasury Regulation §1.141-4(e) - a tax is “generally applicable” if it is an “enforced contribution exacted pursuant to legislative authority in the exercise of the taxing power that is imposed and collected for the purpose of raising revenue to be used for governmental or public purposes.”

o “A generally applicable tax must have a uniform tax rate that is applied to all persons of the same classification in the appropriate jurisdiction and a generally applicable manner of determination and collection.”

o Does it matter that the zone taxes are remitted to the Authority?

34

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

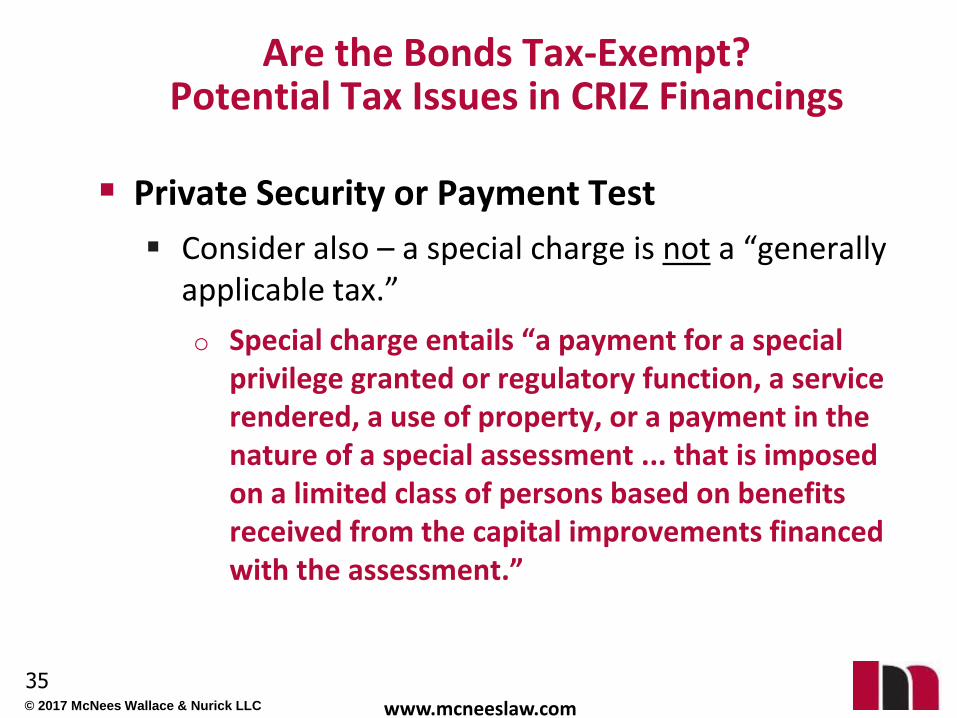

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Private Security or Payment Test

Consider also – a special charge is not a “generally applicable tax.”

o Special charge entails “a payment for a special privilege granted or regulatory function, a service rendered, a use of property, or a payment in the nature of a special assessment ... that is imposed on a limited class of persons based on benefits received from the capital improvements financed with the assessment.”

35

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Private Loan Financing Test

Test is met if proceeds exceeding the lesser of $5M or 5% are used directly or indirectly to finance loans to one or more nongovernmental persons.

o May come into play where the CRIZ Authority intends to make grants of proceeds to businesses in the CRIZ Zone.

o Is it a grant or a loan?

36

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Private Loan Financing Test

Whether a transaction may be treated as a grant or a loan depends on all of the facts and circumstances

“Tax increment financing” exception

o grant using proceeds of an issue secured by generally applicable taxes attributable to the improvements to be made with the grant is not treated as a loan, unless the grantee makes any “impermissible agreements”

37

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Impermissible Agreements:

Imposing personal liability for repayment where none exists in statute

Providing additional credit support such as a third party guarantee, or to pay unanticipated shortfalls

Establishing minimum market value of property subject to property tax

Waiver of right to challenge or seek deferral of the tax

38

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Are the Bonds Tax-Exempt?Potential Tax Issues in CRIZ Financings

Permissible Agreements:

Specifying purposes of grant

Representing expected value of property following the improvement

Insuring the property and, if damaged, restoring

Rescinding grant where taxes not paid

Reducing or limiting the amount of taxes collected to further a bona fide governmental purpose

39

© 2017 McNees Wallace & Nurick LLC www.mcneeslaw.com

Additional Information

DCED: http://dced.pa.gov/programs/city-revitalization-improvement-zone-criz/

Revenue: http://www.revenue.pa.gov/GeneralTaxInformation/IncentivesCreditsPrograms/Pages/City-Revitalization-and-Improvement-Zone-(CRIZ).aspx

City of Lancaster CRIZ: http://www.cityoflancasterpa.com/business/criz

McNees Public Sector Blog: http://www.mcneespublicsector.com/

40