bpi-philam · bpi-philam life assurance corporations is a strategic alliance between two leading...

TRANSCRIPT

4

3

BPI-PHILAMAT A GLANCE

BPI AT A GLANCE

PHILAM LIFEAT A GLANCE

AIA AT A GLANCE

MESSAGE FROMTHE CEO

FINANCIALHIGHLIGHTS

pages 1 - 2

page 4

pages 4

pages 4

pages 5 - 6

pages 7 - 8

4CONTENTS

BUSINESSHIGHLIGHTS

CAPITAL STRUCTURE

LIST OFSTOCKHOLDERS

BOARD OF DIRECTORS

CORPORATEGOVERNANCE

FINANCIALSTATEMENTS

pages 9 - 81

pages 32

pages 33 -34

pages 34 - 46

pages 48 - 72

pages 73 - 81

3

AT A GLANCEBPI-Philam Life Assurance Corporations is a strategic alliance between two leading financial companies in the Philippines - The Philippine American Life and General Insurance Company (Philam Life) and Bank of the Philippine Islands (BPI).

As a combined brand, Filipinos can trust BPI-Philam to help achieve their dreams through solutions that are accessible, affordable and personalized.

We at BPI-Philam understand that the Filipinos’ needs continue to evolve as they go through the different life stages and they want to be able to easily access solutions that help them live healthier, longer and better lives.

The Philippine American Life and General Insurance Company (Philam Life) is the country’s premier and most trusted life insurer for over seven decades now. We focus our knowledge and experience on the Philippines and, as part of the AIA Group, are strengthened by their presence in the Asia-Pacific region.

Bank of the Philippine Islands is a leading commercial bank in the country with over 160 years of experience in the local banking industry and an extensive branch network of more than 1,000 branches and 3,000 ATMs.

BPI-Philam is the bancassurance arm of AIA in the Philippines. AIA is the second largest life insurance company in the world that operates in 18 markets in Asia Pacific.

70 YEARSMARKET LEADER

160 YEARSEXPERIENCE

18 MARKETSIN ASIA PACIFIC

A member of the AIA Group

3

AT A GLANCEBPI-Philam Life Assurance Corporations is a strategic alliance between two leading financial companies in the Philippines - The Philippine American Life and General Insurance Company (Philam Life) and Bank of the Philippine Islands (BPI).

As a combined brand, Filipinos can trust BPI-Philam to help achieve their dreams through solutions that are accessible, affordable and personalized.

We at BPI-Philam understand that the Filipinos’ needs continue to evolve as they go through the different life stages and they want to be able to easily access solutions that help them live healthier, longer and better lives.

The Philippine American Life and General Insurance Company (Philam Life) is the country’s premier and most trusted life insurer for over seven decades now. We focus our knowledge and experience on the Philippines and, as part of the AIA Group, are strengthened by their presence in the Asia-Pacific region.

Bank of the Philippine Islands is a leading commercial bank in the country with over 160 years of experience in the local banking industry and an extensive branch network of more than 1,000 branches and 3,000 ATMs.

BPI-Philam is the bancassurance arm of AIA in the Philippines. AIA is the second largest life insurance company in the world that operates in 18 markets in Asia Pacific.

70 YEARSMARKET LEADER

160 YEARSEXPERIENCE

18 MARKETSIN ASIA PACIFIC

A member of the AIA Group

1

4

#1in

Bancassurance

1,306Bancassurance

Sales Executives

1,098,180lives insured

#3 in Life Insurancebased on Insurance

Commission Statistical Report 2017

102,164New Policies Sold

(from January-December 2018)

4

#1in

Bancassurance

1,306Bancassurance

Sales Executives

1,098,180lives insured

#3 in Life Insurancebased on Insurance

Commission Statistical Report 2017

102,164New Policies Sold

(from January-December 2018)

2

3

VISIONTo be the leading life insurance company in the country by making insurance accessible, affordable and personalized

for every Filipino

MISSIONWe make sure that insurance is easy to get and easy to have for every Filipino, no

matter what class they belong to

3

4

GLANCE

7.9 MILLIONCLIENTS 1,056

(including BanKo branch and BanKo branch lite-units)

Branches3,034ATMs & CAMs

3 FOREIGNOFFICES

AT A GLANCEAlmost

8000 agents nationwide

Over

2,200,000 insured group members

Over

500,000 individual policies

Over

4,000 group policies issued

Excess capital 6x the amount set by the Insurance Commission

Php 1.39 billion in capital for its life insurance license

Php 500 million in capital for its

non-life insurance license

GLANCEThe Largest Listed Company on the Hong Kong Stock Exchange

2nd Largest Life Insurer in the world

#1 Worldwide for MDRT Members

Serving over 30 million individual policyholders

Over 16 million participating members of group insurance schemes

Provides protection to people across the region with total sum of over USD 1T

4

3

FROM THE CEO

5

4

To our valued stakeholders,

In 2018, we continued with our pursuit of providing accessible and affordable insurance for the Filipino. Business continues to grow, closing the year with 1,098,180 in-force policies.

With the support of our partners – BPI, Citibank, our Institutional Distribution partners, and the Philam Group; our sales force and staff, and most importantly, our policyholders.

2018 was a fruitful year for BPI-Philam, we kicked off our Project Dominate (PD) Propel 5-year strategy focusing on customer centricity. There are five (5) Pillars to PD Propel, namely (1) Expand/Strengthen Distribution Channels, (2) Accelerate Productivity, (3) Strengthen Customer Retention, (4) Optimize Omni-Channel Approach, and (5) Complete Integration of Systems.

The first year of the PD Propel strategy anchored on making life insurance a core product of the bank, expanding the distribution channels, increasing productivity, and focusing on Protection and Wellness through Vitality as customer proposition.

A few notable achievements for the year include the record-breaking months of May and October in which over half a billion in annualized new premium (ANP) was generated and over 10,000 case submissions for each month. This was bolstered by the Euro Mastercard Visa (EMV) cards distribution activities of the bank wherein our salesforce participated.

Our sales and engagement for Philam Vitality are also higher than ever, 82% of our salesforce actively sell these Vitality-Integrated Products which makes up 39% of our total production today.

Our salesforce also grew by 25% in 2018, closing the year with a 1,306 headcount. This growth went hand in hand with the continuous expansion of the bank’s branch network. We now have at least one Bancassurance Sales Executive in every BPI branch, ready to serve our numerous customers.

We also continue to improve our operations, by further strengthening our efforts behind our ePlan Customer Portal, eADA auto-pay facility and our various digital efforts. Of course, we do not forget to give back. We donated P4,180,754.00 to our Philam Foundation in 2018. We continue to support their Philam Paaralan, Philam SAVES and Alpha Initiative programs.

We are also very proud to once again be recognized by the World Finance Magazine as the “Best Life Insurance Company of 2018”. This now makes it 2 years in a row that BPI-Philam has been recognized for its efforts in providing affordable and accessible life insurance for every Filipino.

Again, we thank our policyholders; our partners in BPI, Citibank, Philam Life, the AIA Group; our employees, board of directors, shareholders, our host of resource and supply partners; and our friends from the media.

Together, we continue to empower every Filipino in leading healthier, longer, better lives.

Thank you!

SURENDRA MENONChief Executive Officer

6

3

HIGHLIGHTSREVENUEAll amounts in Philippine Peso

PHP 3,399,548

PHP 3,044,975

FIR

ST

YE

AR

PR

EM

IUM

S 2018

2017

12% increase

PHP 8,802,790

PHP 6,553,560

RE

NE

WA

L P

RE

MIU

MS

2018

2017

34% increase

7

4

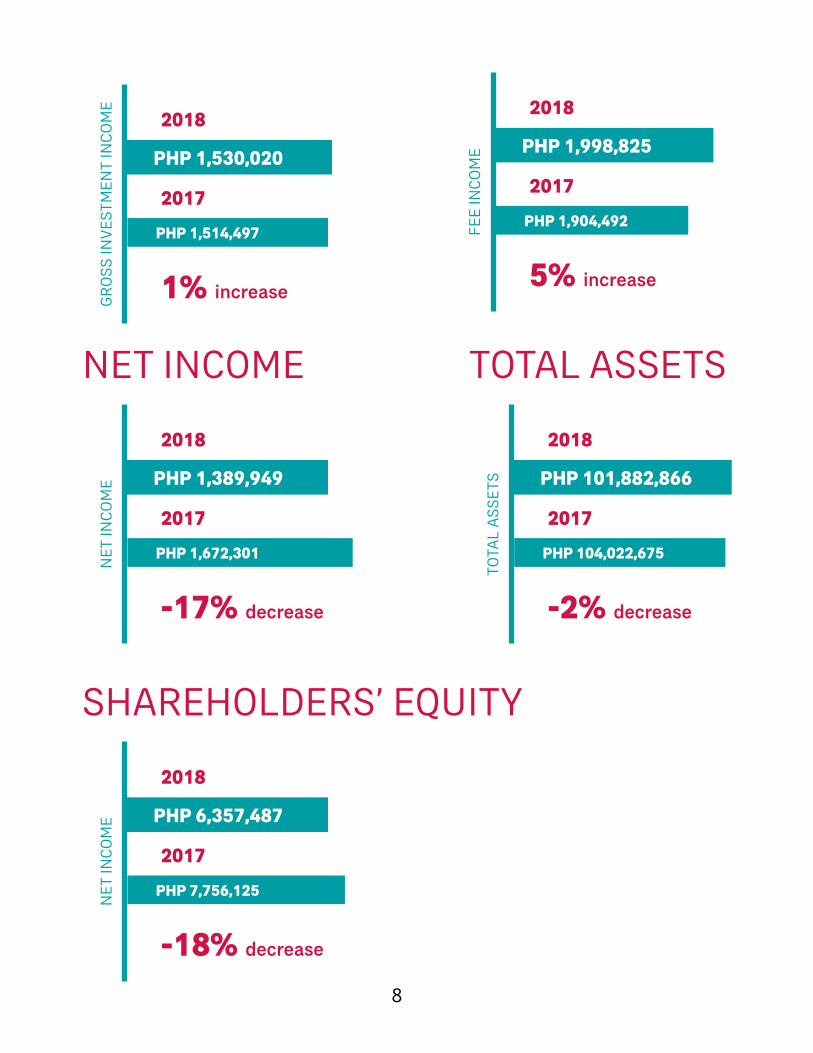

PHP 1,530,020

PHP 1,514,497

GR

OS

S IN

VE

STM

EN

T IN

CO

ME

2018

2017

1% increase

PHP 1,998,825

PHP 1,904,492

FE

E IN

CO

ME

2018

2017

5% increase

NET INCOME

PHP 1,389,949

PHP 1,672,301

NE

T IN

CO

ME

2018

2017

-17% decrease

TOTAL ASSETS

PHP 101,882,866

PHP 104,022,675

TOTA

L A

SS

ETS

2018

2017

-2% decrease

SHAREHOLDERS’ EQUITY

PHP 6,357,487

PHP 7,756,125

NE

T IN

CO

ME

2018

2017

-18% decrease

8

3HIGHLIGHTS

9

4

PRODUCTSWe launched our Smart Health Shield, the very first in BPI-Philam’s product line to provide protection for the whole family specifically against mosquito-borne and other minor illnesses prevalent in the Philippines. Smart Health Shield is a yearly renewable health and accident insurance product that provides fixed coverage upon diagnosis of five (5) mosquito-borne illnesses (Dengue, Zika, Chikungunya, Japanese Encephalitis and Malaria) and three (3) other minor illnesses (Cholera, Typhoid Fever and Leptospirosis). It was launched on August 28 and is available through Telemarketing.

10

3

/PHILAM VITALITYPartnership Distribution realized the proposition strength of Vitality, and fully committed to push for Vitality Integrated Products sales, evident in seller penetration and annual net premium (ANP) growth to 82% and 64%. With this growth came heightened program engagement, led by Distribution’s primary ambassadors – its employees, who closed the year at a launch high 65%. This enthusiasm haloed to BPI, primarily the bank partners, whose Vitality referrer ratio soared to 68% while slowly increasing momentum in their personal Vitality journey at 34%.

MONTHAs with previous years, we continued with our annual celebration of October as Bancassurance month. We celebrated this year by focusing our efforts on educating the general public on the concept of bancassurance and why getting their insurance through the bank is their best option. We also focused on BPI-Philam being the affordable and accessible insurance that best suits their financial planning and protection needs.

We refocused our activities to be held in-branch and spearheaded by the BSEs. This allowed us to bring in over 35,000 additional leads for Bancassurance Month alone.

11

4

MARKETINGIn 2018, we were successful in shifting our product mix from a savings-heavy product suite to become a more protection and health-focused portfolio. This shift went hand in hand with our continuous push for Philam Vitality.

The science-backed wellness program empowers our customers to live healthier, longer, better lives, while it allows us to be part of their daily lives.

MARKETINGWe further strengthened our digital marketing efforts throughout 2018, adapting industry best practices to better reach out to our existing customers and the untapped market.

Content marketing, social media marketing and email marketing have proven to be successful strategies for us in pushing our thought leadership, health and wellness, and financial tips content to our audience.

12

3

BANKINGBPI’s EMV card distribution gave BPI-Philam’s Personal Banking Segment the opportunity to extend protection coverage to more lives. A new customer engagement module about relevant health trends was introduced as part of EMV’s sustaining initiatives, which further strengthened the company’s value proposition as the customers’ partner in living healthier, better, and longer lives. Health and Wellness forums empowered the sales team to converse about proactive measures centered on improving customers’ lifestyle instead of negative uncertainties; making face-to-face appointments more relatable, positive, and vibrant. Lastly, a new sales channel called “Field BSE Sales” was developed. This channel catered to customer retail needs outside the branch, including EMV cards distribution to BPI payroll accounts.

BANKINGThe Preferred Banking Segment took advantage on BPI’s EMV card distribution opportunity to touch base and increase engagement with its banking clients leading to discussions of their financial needs. It also resulted to significant increase in referred leads versus the previous year’s actual experience. Estate Planning pocket forums were organized where clients are invited to a timely, practical talk on Estate Planning. In response to the introduction of the TRAIN law last January 2018, the value proposition has been expanded from simple estate tax planning to a more encompassing solution to wealth creation, conservation and distribution. Coffee Talks were institutionalized for the BPI Relationship Managers and BPI-Philam Sales to have a more meaningful and personal needs-based conversation with their clients outside the branch. This was supported by the Free P1M Personal Accident coverage which was offered to the clients during the coffee conversations. Lastly, BPI, in cooperation with BPI-Philam, launched Welcome to a Life Preferred Event, the very first forum for Preferred clients where insurance was the main offering.

BANKING2018 is the year when Private Segment’s efforts to reach out to its customer were in full swing. Estate Planning runs continued on as the need for legacy planning evolved with the developments in taxations brought by TRAIN law. These were reinforced by clan/family presentations, smaller-scale estate planning talks, to deliberately tackle Private Clients’ legacy planning needs unique to their family and situation. These engagement activities were the engines that brought new business for the segment. A seamless and pleasant customer experience was also priority for the year. Customer Journey specific to Private was crafted; it now defines the ideal customer experience which would also be guiding the strategies and initiatives for the segment in the long-run. Aligned with this, groundwork has been laid before the year ended to improve application/new business experience and after-sales servicing through initiatives undertaken to reorganize New Business processes and enhance SLAs with medical exam partners.

13

4

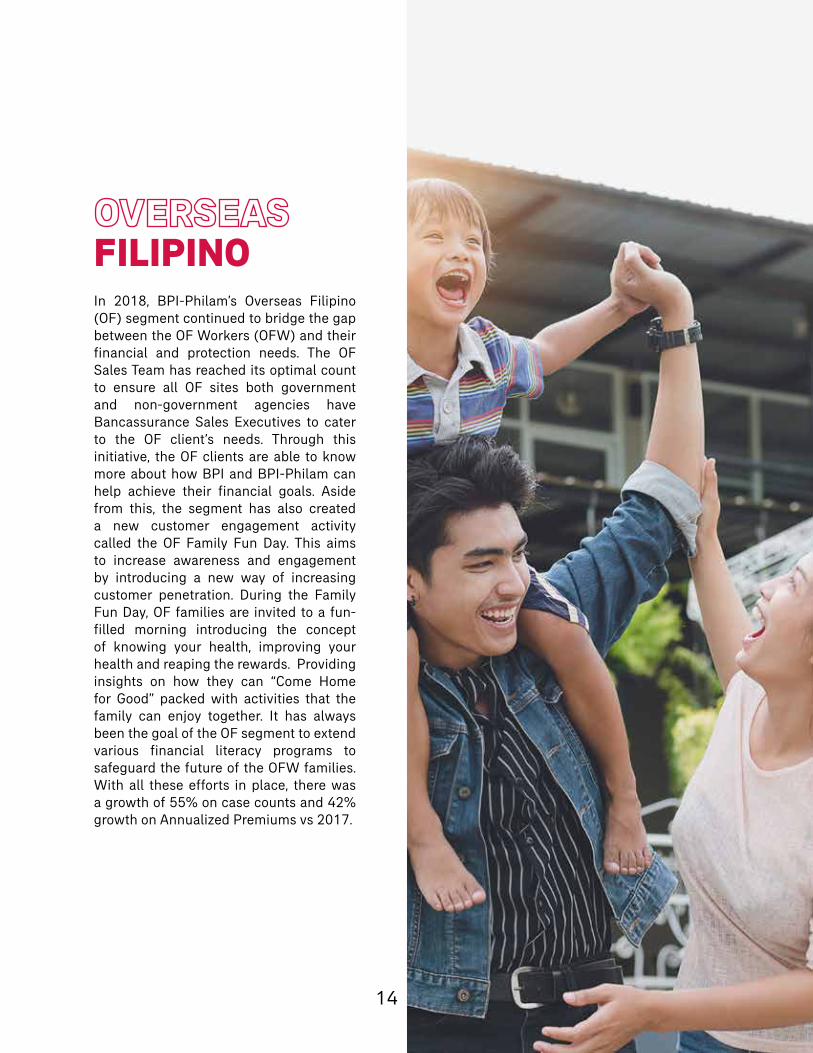

FILIPINOIn 2018, BPI-Philam’s Overseas Filipino (OF) segment continued to bridge the gap between the OF Workers (OFW) and their financial and protection needs. The OF Sales Team has reached its optimal count to ensure all OF sites both government and non-government agencies have Bancassurance Sales Executives to cater to the OF client’s needs. Through this initiative, the OF clients are able to know more about how BPI and BPI-Philam can help achieve their financial goals. Aside from this, the segment has also created a new customer engagement activity called the OF Family Fun Day. This aims to increase awareness and engagement by introducing a new way of increasing customer penetration. During the Family Fun Day, OF families are invited to a fun-filled morning introducing the concept of knowing your health, improving your health and reaping the rewards. Providing insights on how they can “Come Home for Good” packed with activities that the family can enjoy together. It has always been the goal of the OF segment to extend various financial literacy programs to safeguard the future of the OFW families. With all these efforts in place, there was a growth of 55% on case counts and 42% growth on Annualized Premiums vs 2017.

14

315

4

EXPERIENCEIn Q1 2018, we strengthened customer loyalty through 5 major programs, namely: (1) Premium Collection Campaign which encouraged timely payment of premiums for continued insurance protection; (2) Reinstatement Campaign which provided a hassle-free opportunity for customers to reactivate their lapse or discontinued policies; (3) Anniversary Program for Preferred Segment or managed accounts; (4) Welcome and Anniversary Survey for customers who are on-the-go and prefer the digital channel; and (5) ePlan Activation Campaign to ensure utilization of the Customer Portal for policy inquiry and simple transactions.

In the same year, we also reached a premium collection rate of 90% which is 10 basis points higher than industry standard. This result was brought by retention campaigns which influenced regular and on-time payment of premiums, as well as driving payment reminders for identified months with lowest collection activities. During these slow months, special programs were conducted to entice clients in paying premiums on time, while branch salesforce supported in re-engaging with clients for premium renewals and reinstatements.

We also formulated a Total Weighted Premium Income (TWPI) taskforce to review premium collection systems and processes especially the electronic Auto-Debit Arrangement (eADA) facility. The taskforce reviewed the customer journey, business gaps, and address process and platform-related matters to control adverse effects of non-collection and attrition.

We also expanded the nurturing programs to the managed accounts of BPI-Philam via the Anniversary Program. Aside from revisiting the client to review his BPI-Philam policy, the program encouraged Preferred clients to share improvement areas in service handling and review current financial state through a financial and wellness needs analysis meeting. Clients who completed the Anniversary Program were entitled to a raffle entry for surprise tokens.

Last year, we also rolled out the Customer Journey Mapping programs together with our BPI partners and Philam Life Stakeholders through the guidance of our AIA Group Customer Experience representatives. During this 2-day event, the participants were guided to an introduction of Design Thinking or Human-Centered Design and the AIA prescribed mapping of a customer’s journey from brand discovery to onboarding and claims. As a result, the teams completed three (3) customer journey maps for defined segments of BPI-Philam: (a) Sea-based Overseas Filipino Workers; (b) Millennial and employees working in BPOs; and (c) Entrepreneurs.

16

3

OPERATIONSOn our mission to provide Filipinos with easily accessible and affordable insurance, we focused on strengthening the capability of our digital platforms to ensure that we are are able to manage our growing customer base.

We optimized our enrolment process for Auto Debit Arrangement (eADA) payment facility for renewal premiums. To further increase the enrolment rate of the digital platform, we launched a campaign to the Bancassurance Sales Executives (BSEs) in-branch which aimed to make the Customer Portal a part of their selling proposition to their customers. Towards the end of 2018, the enrolment rate increased to 56% (of which has an activation rate of 54%).

We also spearheaded the deployment of Mobile Customer Service Associates to selected branches, targeting areas with high volume of aftersales transactions. Their working relationship with their partner BSEs improved the management of aftersales transactions and enabled our sales executives to focus on new business acquisition.

To make sure that everyone is well informed of the different customer touchpoints, we conducted an aftersales training for the BSEs. This served as an avenue for us to tackle the various touchpoints and digital tools such as the Customer Portal, Call Center, iCARE, and the Bancassurance Portal – all focusing on promoting customer centricity and improving aftersales servicing to clients.

17

418

3

SALESFORCEBPI-Philam values its people as our success is a result of their determination to serve the Filipino people. Our growing salesforce is consistently contributing to our wins, and we continue to empower and recognize them with valuable learning experiences in and out of the country.

To usher in the new fiscal year, we held our 2018 Sales Kick Off at the Philippine International Convention Center (PICC). Our chosen theme, Rise of the Champions, called upon our salesforce to overcome the challenges in their way, proving to the world that they are indeed champions of bancassurance.

Soon after, we celebrated our 2017 Annual Awards in Manila Marriott Hotel with the theme “Symphony of Success: Propel to Greatness”. Our in-branch sales team and our bank partners whose endless pursuit of excellence were recognized with an evening of sumptuous food and dazzling entertainment.

For the annual Sales Learning Convention, qualifiers from both BPI and BPI-Philam travelled to Greece, China, and Australia; 30 qualifiers flew to Santorini, 56 qualifiers for Shanghai, and 68 qualifiers for Sydney. While learning is the primary goal of each trip, our qualifiers were also treated to the best local delicacies and restaurants, cultural and heritage tours, and were billeted in premium housing for the duration of the trip.

By the end of 2018, our salesforce grew to 1,306 people, coming from 991 in 2017, all of whom are trained and equipped to be the best-in-class in bancassurance.

We endeavor to train and mold our team into the professional and genuine salesforce that we need in order to serve every Filipino. We believe that through the hard work and determination of our salesforce, we continue to serve the Filipino people and their need for protection.

19

420

321

4

SOLUTIONSThis 2018, BPI-Philam Corporate Solutions focused on growing its business. Towards the end of the year, we were able to achieve a 24% growth on the overall portfolio compared to the previous year. Another achievement of the team is the 114% attainment of the 2018 target for Credit Life product.

The team was also able to close 249 Employee Benefit case counts. This growth resulted to an increase in our customer base, now reaching a total of 373,262 lives covered since inception. This milestone is a testament to the fruitful and effective strategy of Corporate Solutions by working closely with the Relationship Managers and counterparts from BPI Corporate Solutions.

22

3

PEOPLE

At the heart of BPI-Philam’s strategic priorities lies customer-centricity. In our organization, it is our duty to foster a collaborative environment so that innovation can flourish and employees are able to create a delightful and seamless experience to the people they work with. In 2018, we enabled our employees to “Make It Possible” by providing them the necessary trainings, programs and exposure.

In this same year, we enabled our employees to live life to the fullest and enjoy more quality time with their loved ones by helping them improve their health holistically through Philam Vitality. We have implemented initiatives that inspired employees to be productive in a youthful, dynamic, and active environment.

23

4

ENGAGEMENTIn 2018, initiatives to drive effective leadership were implemented nationwide to guide managers to explore, enhance and refine understanding of their people’s workplace need and use available resources to address them. All people managers were invited to undergo a workshop designed to help them understand, measure and create engagement. As a way to empower our leaders to take charge of their team’s engagement, toolkits were provided to remind managers of the things vital to employee engagement and help them celebrate important occasions and milestones within the team.

We also launched I Make It Possible, a leader-led workshop that introduced the 4 steps to make any circumstance possible as we want to instil the culture of creative thinking, innovation and collaboration within the organization. This initiative took us a step closer to achieving our goals.

Apart from the regular developmental courses, the Leadership Accelerator Program (LEAP) was launched to pave the way and accelerate development of future leaders. The LEAP program enabled and prepared 29 individual contributors to transition to their managerial roles by undergoing several learning programs and revalida.

Our employees are at the cornerstone of our business. It is our responsibility to ensure that our employees are engaged, motivated and committed so that the organization can achieve its goals. We have launched a program called Stellar Awards to recognize team members for their outstanding leadership, for providing service that is above and beyond what is expected and for demonstrating exemplary behaviour that contributed to achieving our strategic priorities. Moreover, we also opened the retirement plan voluntary contribution for employees last March 2018 as we fully support financial preparedness most especially for our employees.

24

325

4

ANDWELL-BEINGAs the only organization in the Philippines who offers total wellness to clients we understand that for people to get more out of life, their health must be optimized. Similarly, we use the same philosophy with our employees. We encourage our employees to live healthier, longer and better so that they can spend more quality time with their loved ones.

Aside from the annual wellness day where employees were required to complete their physical examination, given the option to avail of Flu Vaccine in a discounted price, consult and eye doctor and/or a nutritionist, we launched a campaign to enable employees to live healthier, longer and better in a fun and collaborative way.

The Race to Gold program is designed to guide employees in their journey to total wellness and become true ambassadors of healthier, longer and better lives to their loved ones by achieving Gold Philam vitality status.

Using the Philam Vitality program, we grouped our employees into teams, identified team captains and vitality ambassadors to guide each team, identified and cascaded vitality goals a monthly basis which teams were required to accomplish and in return will earn points and be rewarded.

26

3

SOCIAL RESPONSIBILITY

27

4

BPI-Philam continues its commitment of giving back to the community by supporting the various initiatives of Philam Foundation by allocating a portion of its income annually for CSR. The annual donation to Philam Foundation by allocating a portion of its income annually for CSR. The annual donation to Philam Foundation helps fund programs that focus on education, health and financial well-being – Philam Paaralan, Philam Savings Awareness and Values Education Sessions (SAVES), and Alliance for the Philippines’ Health and Advocacy (ALPHA Initiative).

Under Philam Paaralan, 34 new fully-furbished classrooms were built throughout the country, bringing the Foundation’s total number of classrooms built since 2011 to 171. By end of 2018, Philam Paaralan is present in 40 out of 81 provinces in the Philippines, with a target to build classrooms in each province.

Philam SAVES provides financial literacy sessions to Grade 4 to Grade 5 students, community, teachers and parents. It ended the year with 13,454 Grades 4

and 5 students, parents and teachers educated on the importance of saving. Over 600 volunteers participated throughout 2018, committing 1,801 hours for the program.

The Alliance for the Philippines’ Health and Advocacy (ALPHA Initiative) continues its partnership with the Cancer CARE Registry Foundation. In 2018, the initiative partnered with 20 hospitals nationwide for the installation of the cancer registry through CARE Philippines, Inc., a web-based cancer registry program launched to collect and analyze data from Filipinos diagnosed with cancer from various public and private hospitals nationwide.

BPI-Philam through Philam Foundation will continue to work towards making better lives possible among our countrymen through its programs that make each Filipino “Healthy, Wealthy, and Wise”.

28

329

4

STRUCTURE

AUTHORIZE CAPITAL STOCK

PHP 1 Billion

SUBSCRIBE & PAID-UP CAPITAL STOCK

PHP 749,993,979.00

PAR VALUE

PHP 1.00 per share

TREASURY SHARE

PHP 6,000.00

30

331

4

STOCKHOLDERSSHARES HELD CLASS AMOUNT PAID

(PHP)% OF

OWNERSHIPNATIONALITY BENEFICIARY

OWNERSHIPDATE OF FIRST APPOINTMENT

THE PHILIPPINE AMERICAN LIFE AND GENERAL INSURANCE (Philam Life) COMPANY

JACKY CHANNon-Executive DirectorChairman

KELVIN ANGNon-Executive Director

SURENDRA MENON Executive DirectorChief Executive Officer

JESUS P. TAMBUNTING Independent Director

BANK OF THE PHILIPPINE ISLANDS (BPI)

CEZAR P. CONSINGNon-Executive Director

MARIA CONSUELO A. LUKBANNon-Executive Director

ROMEO L. BERNARDOIndependent Director

OTHERS(Minority Stockholders)

TOTAL

382,496,926 Common 382,496,926.00 51% Hong Kong SAR

1 Common 1.00 Chinese Philam Life 15 June 2018

1 Common 1.00 Malaysian Philam Life21 January

2019

1 Common 1.00 Singaporean Philam Life 22 January 2016

1 Common 1.00 Filipino Philam Life 27 November 2009

357,554,432 Common 357,554,432.00 47.67% Filipino

100 Common 100.00 Filipino BPI 03 April 2014

100 Common 100.00 Filipino BPI09 November

2018

100 Common 100.00 Filipino BPI 24 April 2006

9,942,317 Common 9,942,317.00 1.33% Filipino

749,993,979 749,993,979.00

32

333

4

DIRECTORS

34

3

JACKY CHAN (55)

Mr. Jacky Chan, is the Regional Chief Executive responsible for the Group’s businesses operating in Hong Kong and Macau, Singapore and Brunei, Indonesia, Philippines and Cambodia as well as the Group Agency Distribution. He is a director of various companies within the Group, including AIA Co. and AIA International. Mr. Chan has extensive life insurance industry experience having worked at AIA for the past 31 years. Prior to becoming a Regional Chief Executive, Mr. Chan was Chief Executive Officer of AIA Hong Kong and Macau since 2009. Previously, he held several senior positions including the Country Head of AIA China, responsible for overall business performance and results in China; Executive Vice President - Distribution & Marketing of Nan Shan Life Insurance - Taiwan; Senior Vice President & Head of Life Profit Centre of AIA - Asia (ex-Japan & Korea).

Mr. Chan holds a Bachelor of Science Degree from the University of Hong Kong. He is a Fellow of Society of Actuaries (FSA), a member of American Academy of Actuaries (MAAA) and a Fellow of Canadian Institute of Actuaries (CIA).

AIA Regional Chief Executive Non-Executive DirectorChairman of the Board

BO

AR

D O

F D

IREC

TOR

S

35

4

SURENDRA MENON (60)

Surendra Menon is the Chief Executive Officer of BPI-Philam Life Assurance Corporation. Prior to his appointment, Mr. Menon held the role of Regional Director for Bancassurance of the AIA Group. As a catalyst in the Bancassurance industry, he has built and developed various profitable businesses in Asia including Indonesia, Singapore, and the Philippines. He joined AIA in 2003 and was responsible for acquisition of 10 partnerships in Indonesia including BCA, CIMB, ANZ and was the Deputy CEO and CDO. He then became the subject matter expert for the AIA Group in Bancassurance for 2013 to 2015. Helping many countries in Asia with 2014 & 2015 focused on BPI-Philam in Philippines. As the current CEO, he has steered BPI-Philam to transform the business into one of the leading life insurance companies in Philippines. Mr. Menon has actuarial, financial planning and investment management qualifications from UK, Singapore and Indonesia, respectively. Prior to joining AIA, he worked in DBS Bank in Singapore, BDNI Life in Indonesia, and the Insurance Corporation of Singapore (now known as Aviva in Singapore). He was also a director of GT Asset Management in forming the first mutual fund in Indonesia and, was a police inspector in the Singapore Police Force and Captain in the Singapore Civil Defense as part of his national service duty.

Executive DirectorChief Executive Officer

BO

AR

D O

F D

IREC

TOR

S

36

3

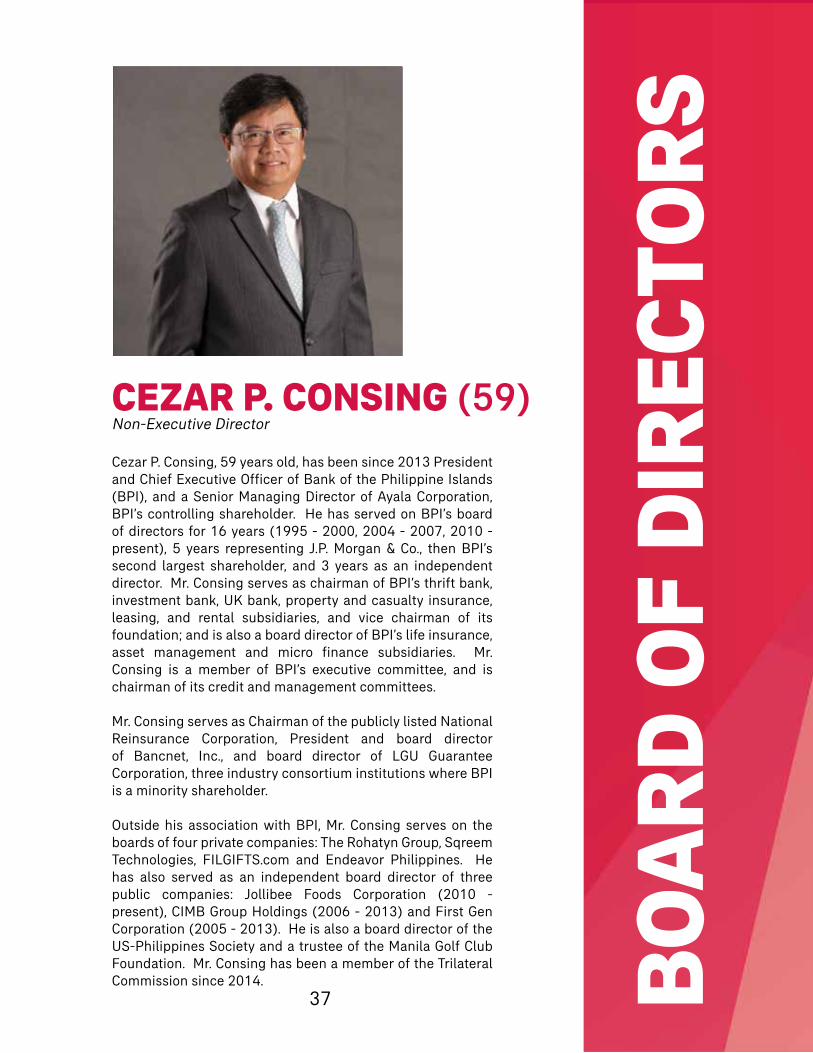

CEZAR P. CONSING (59)

Cezar P. Consing, 59 years old, has been since 2013 President and Chief Executive Officer of Bank of the Philippine Islands (BPI), and a Senior Managing Director of Ayala Corporation, BPI’s controlling shareholder. He has served on BPI’s board of directors for 16 years (1995 - 2000, 2004 - 2007, 2010 - present), 5 years representing J.P. Morgan & Co., then BPI’s second largest shareholder, and 3 years as an independent director. Mr. Consing serves as chairman of BPI’s thrift bank, investment bank, UK bank, property and casualty insurance, leasing, and rental subsidiaries, and vice chairman of its foundation; and is also a board director of BPI’s life insurance, asset management and micro finance subsidiaries. Mr. Consing is a member of BPI’s executive committee, and is chairman of its credit and management committees.

Mr. Consing serves as Chairman of the publicly listed National Reinsurance Corporation, President and board director of Bancnet, Inc., and board director of LGU Guarantee Corporation, three industry consortium institutions where BPI is a minority shareholder.

Outside his association with BPI, Mr. Consing serves on the boards of four private companies: The Rohatyn Group, Sqreem Technologies, FILGIFTS.com and Endeavor Philippines. He has also served as an independent board director of three public companies: Jollibee Foods Corporation (2010 - present), CIMB Group Holdings (2006 - 2013) and First Gen Corporation (2005 - 2013). He is also a board director of the US-Philippines Society and a trustee of the Manila Golf Club Foundation. Mr. Consing has been a member of the Trilateral Commission since 2014.

Non-Executive Director

BO

AR

D O

F D

IREC

TOR

S

37

4

Mr. Consing first worked for BPI, in corporate planning and corporate banking, from 1980 - 1985. He worked for J.P. Morgan & Co., based in Hong Kong and Singapore, from 1985 - 2004, rising to co-head or head the firm’s investment banking business in Asia Pacific from 1997 - 2004, the last five years as President of J.P. Morgan Securities (Asia Pacific) Ltd. As a senior Managing Director of J.P. Morgan, Mr. Consing was a member of the firm’s global investment banking management committee and its Asia Pacific management committee.

Mr. Consing was a partner at The Rohatyn Group from 2004 - 2013, headed its Hong Kong office and its private investing business in Asia, and was a board director of its real estate, and energy and infrastructure private equity investing subsidiaries.

Mr. Consing received an A.B. Economics degree (Accelerated Program), magna cum laude, from De La Salle University, Manila, in 1979. At university, he was a member of the student council, the student newspaper and the varsity track and field team. In recent years, he has served on the advisory committees of the university and its school of economics. Mr. Consing obtained an M.A. in Applied Economics from the University of Michigan, Ann Arbor, in 1980.

BO

AR

D O

F D

IREC

TOR

S

38

3

KELVIN ANG (54)

Mr. Kelvin Ang, Philam Life’s Chief Executive Officer is a home-grown talent with over 20 years of service in AIA. He has served in various Leadership and Agency Distribution roles across the AIA Group Office and the local Business Units – including Hong Kong, Malaysia, Indonesia, Vietnam and China. In his role as Chief Agency Officer of China and General Manager of Shanghai, he played a key role in the success of AIA China’s agency transformation. Mr. Ang also led the successful AIA-ING agency integration in Malaysia in 2015-2018. After his successful stint in AIA Malaysia, he was appointed as Regional Chief Agency Officer, with AIA Hong Kong, China and Vietnam in his portfolio, with the mission to future proof the business through digitalization and new market expansion.

Mr. Ang earned his Bachelor’s degree at the Royal Melbourne Institute of Technology in Australia and his Master’s degree in Business Administration from Bath University in United Kingdom. He is also currently a corporate member of the Philippine Life Insurance Association Inc. (PLIA).

Non-Executive Director

BO

AR

D O

F D

IREC

TOR

S

39

4

ROMEO L. BERNARDO (54)

Romeo L. Bernardo, 64, Filipino, is Managing Director of Lazaro Bernardo Tiu and Associates (LBT), a financial advisory firm based in Manila. He is also a GlobalSource economist in the Philippines. He is Chairman of ALFM Family of Funds and Philippine Stock Index Fund. He is likewise a director of several companies and organizations including Aboitiz Power, BPI, Globe Telecom Inc., RFM Corporation, Philippine Investment Management (PHINMA), Inc., National Reinsurance Corporation of the Philippines (NRCP). He is a member of the Philippine World Bank Advisory Group and a member of the Panel of Conciliators of the International Centre for Settlement of Investment Disputes. He previously served as Undersecretary of Finance and as Alternate Executive Director of the Asian Development Bank. He was an Advisor of the World Bank and the IMF (Washington D.C.). Mr. Bernardo holds a degree in Bachelor of Science in Business Economics from the University of the Philippines (magna cum laude) and a Masters Degree in Development Economics at Williams College from Williams College in Williamstown, Massachusetts.

Independent Director(until April 10, 2019)

BO

AR

D O

F D

IREC

TOR

S

40

3

JESUS P. TAMBUNTING, OBE (81)Ambassador Tambunting is Chairman of Capital Shares Investment Corporation, an investment and management company. He was Chairman of Planters Development Bank, the Philippines’s leading bank for promoting and growing SMEs, which he founded in 1971. From 1993 to1998, he served as the Philippines’ Ambassador to the United Kingdom of Great Britain and Northern Ireland and concurrently, to the Republic of Ireland. In 2016, he was appointed by President Benigno Aquino III as Chairman of the Small Business Corporation.

In 2017, Her Majesty Queen Elizabeth II awarded Ambassador Jesus P. Tambunting the recognition as an Officer of the Order of the British Empire.

He was conferred Master Entrepreneur and Entrepreneur of the Year 2009 by the British firm Ernst & Young and the SGV Foundation, and inducted into the World Entrepreneur Academy in Monaco in June 2010. He also received the International Alumnus Award from the University of Maryland in April 2011, the first Ramon V. del Rosario Sr. Award in Nation Building in 2010, the Distinguished Person of the Year 2009 from the Association of Development Financing Institutions in Asia and the Pacific, the Management Man of the Year 2003 from the Management Association of the Philippines, the Lifetime Achievement Award for 2005 from the Asian Bankers Association, the Distinguished Service Award from the Department of Foreign Affairs and “Knight Commander with Star” in 2008 and “Knight Grand Cross” in 2016 from the Equestrian Order of the Holy Sepulchre of Jerusalem.

Independent Director

BO

AR

D O

F D

IREC

TOR

S

41

4

Other roles include being Co-chairman of the Philippine-British Business Council, member of the Board of Trustees of the Carlos P. Romulo Foundation, Philippine Business for Education, PinoyMe Foundation, and Caritas Manila. He is a member of the Makati Business Club National Issues Committee. From 2004 until May 2008, he served as Chairman of the Association of Development Financing Institutions in Asia and the Pacific, a regional organization of 127 development banks and institutions in 44 countries. He was elected to the Board of Directors of BPI-Philam Life Assurance Inc. in 2009.

The Ambassador earned his Bachelor of Science degree in Economics from the University of Maryland. Prior to that, he had obtained his secondary education from the Culver Military Academy in Indiana and his elementary education from the Ateneo de Manila University.

BO

AR

D O

F D

IREC

TOR

S

42

3

MARIA CONSUELO A. LUKBAN (54)

Ms. Lukban is the Senior Vice President and Head of the Strategic and Corporate Planning Department of Bank of the Philippine Islands (BPI). She is primarily responsible for financial planning and capital management, investor relations. She is also a member of the Board of Directors for BPI-Philam Life Assurance Inc. and National Reinsurance.

She has over 30 years of banking experience, taking on various senior roles within BPI as Head of Risk and Systems Management in its asset management and trust business (2000-2004), as Head of Product Development and Corporate Sales in its life insurance business (2004-2009), Head of Corporate Banking Marketing (2010-2011) and Deposit Products (2012-2017).

Ms. Lukban completed her MBA at the University of Chicago in 1992 and BS Management Engineering in 1986 at the Ateneo de Manila University.

Non-Executive Director

BO

AR

D O

F D

IREC

TOR

S

43

4

JESSE ANG (54)

Mr. Jesse Ang is an Independent Director of Bank of the Philippine Islands (BPI) Capital Corporation and BPI Asset Management and Trust Corporation.

After more than 18 years, Mr. Jesse Ang retired from the International Finance Corporation (IFC) in June 2018. Previously, he was the Resident Representative for the Philippines office of the International Finance Corporation. He has extensive financial sector expertise and a solid track record in putting together investment deals in infrastructure, including power, mining, water and telecommunications. He was the first Filipino to become the head of the IFC Philippine office. Since retirement, Jesse has joined BPI Capital and BPI AMTC as independent director.

He joined IFC Philippines in February 2000 as a Senior Investment Officer primarily responsible for business development. Prior to joining IFC, he was the Chief Financial Officer and Treasurer of the Philippine International Air Terminals Company based in Manila. He worked in New York City for several years in various capacities, such as Director of the Global Structured Finance department in ANZ Investment Bank, Vice President of the Trade and Commodity Finance department in Generale Bank and Assistant Vice President in Irving Trust Company. His work experience involved significant travel to Latin American countries such as Mexico, Chile, Colombia, Venezuela, Brazil and Argentina and East Asian countries including Korea, Taiwan, Hong Kong and the Philippines.

He earned his Master’s degree in Business Administration from the Wharton Graduate School of Business and a BS Industrial Engineering degree from the University of the Philippines.

Independent Director(Effective April 10, 2019)

BO

AR

D O

F D

IREC

TOR

S

44

3

SUPPORT

45

4

CARLA J. DOMINGO (54)

Atty. Domingo is currently the Chief Legal Officer & Corporate Secretary of The Philippine American Life and General Insurance (Philam Life) Company. She also serves as the Corporate Secretary of BPI-Philam Life Assurance (BPLAC) Corporation (formerly Ayala Life).

She was the Deputy Company Secretary of AIA Group Limited from February 9, 2014 to February 6, 2015. She was also Corporate Secretary of various Philam companies from 2008 to January 2014, to wit: Philam Equitable Life Assurance Company; Philam Properties Group of Companies; Philam Asset Management Inc.; Philam Call Center Services, Inc.; the Tower Club, Inc. and Philam Foundation, Inc.

Atty. Domingo is a member of the Integrated Bar of the Philippines, and a Fellow of the Institute of Corporate Directors. Atty. Domingo is a graduate of the University of the East, with a Bachelor of Arts degree major in Political Science, where she graduated Magna Cum Laude. She took her Bachelor of Laws degree in San Beda, College of Law.

Corporate Secretary

46

347

4

WITH CORPORATEGOVERNANCEBPI-Philam confirms its full compliance with the Code of Corporate Governance. Its commitment to the highest standards of corporate governance is rooted in the belief that culture of integrity and transparency is essential to the consistent achievement of its common goals. Creating a sustainable culture, where trust and accountability are vital as skill and wisdom, steers us towards achieving long-term value for shareholders and clients, and strengthens our confidence in the institution.

48

3

AND

OF THE BOARDThe Board of Directors exercises all the powers of the corporation; all business conducted and all properties of the corporation are controlled and held by them. The Board is completely independent from management and major stockholders.

The Board is accountable to the shareholders and as such it shall ensure the highest standard of governance in running the Company’s business and setting the strategic directions. The detailed role and responsibilities are set forth in the By Laws and the Manual of Corporate Governance.

For 2018, The Board of Directors, through its Board Risk and Audit & RPT Committees, has conducted a regular review of the Company’s material controls (including operational, financial and compliance controls) and risk management systems. The Board Risk Committee, the Audit & RPT Committee and the Board of Directors have declared their satisfaction and confidence on the Company’s internal controls and risk management systems.

AND DIVERSITYEach of the independent directors meets the guidelines set in the Manual of Corporate Governance. None of the independent directors has any business or significant financial interest in the Company or any of its subsidiaries. They, therefore, continue to be considered independent.

BPLAC adopts AIA Policy on Diversity, and believes in the power of diverse, talented people to create value and deliver on their customer and shareholder expectations. Fundamental to all the Company’s inclusion efforts is zero-tolerance for discrimination or harassment in any form, across all aspects of diversity, including gender, race, nationality and sexual orientation.

PROCESSThe Board meetings are held on a quarterly basis unless a special meeting is necessary to consider urgent matters. Minutes of meetings of the Board and all Committees are kept by the Corporate Secretary, and are open for inspection by the Board and Stockholders upon request. Board materials are sent to the members at least five (5) business days in advance of the scheduled board meetings.

49

4

In addition to the regular meetings, the directors also engage in informal meetings on a quarterly basis to further discuss issues and strategies. Non-executive directors also find time to meet separately to discuss the business affairs of the Corporation. Independent Directors likewise, regularly meet with management, the internal auditors and the external auditors, separately, to ensure proper check and balance is achieved by the Corporation.

SUCCESSION ANDSELECTION PROCESS

REMUNERATION OFDIRECTORS

The Board ensures that plans are in place for orderly succession to the Board and senior management to maintain a balance of appropriate skills and experiences within the Company. The Company’s Corporate Governance Manual prescribes a formal, rigorous and transparent procedures for the selection and appointment of directors of the Board and senior management. Appointments to BPLAC Board of Directors or Senior Management are made on merits and subject to objective criteria as set forth in the Manual. Careful deliberation and consideration is done to ensure that nominees are qualified to sit in the Board or in Senior Management. The Company, through its major shareholder, considers the knowledge, competencies, skills, and experience that the nominee-director or executives, seriously taking into account the Company’s business objectives and strategies. The Company ensures that its Board membership and Senior Management consist of persons with sufficiently diverse and independent backgrounds and possesses a record of integrity and good repute. Part of the selection process of the Company is the use of independent/third party professional search firms to identify and source qualified directors and senior executives.

The Independent Directors definitely play very significant roles in order to achieve the Company’s business objectives today and in the future. As independent directors, they effectively participate and provide objective, independent judgment in the business affairs of the Company, and at the same time ensure that proper checks and balances are in place.

50

3

Considering the above, and in view of the stricter corporate and regulatory environment in the country, the Company believes that the independent directors should be adequately compensated for the knowledge, skills, and expertise they share and impart to the Board; for the time and efforts they provide to the Company; and for potential risks and liability they may be exposed of as its members. The fee structure of the independent directors are based on various factors, such as but not limited to director’s qualification and experience, skills, and expertise; financial services sector benchmark; market condition; and regulatory environment.

As reviewed and approved by the shareholders of the Company on an annual basis, the independent directors receive fixed directors’ fees per Board and Committee meeting attended, and annual bonus. For 2018, the total annual gross directors’ fees of the Company’s independent directors Mr. Romeo Bernardo and Amb. Jesus P. Tambunting amounted to Philippine Pesos Three million Four Hundred Eighteen Thousand (PhP3,418,000.00). The executive and non-executive directors do not receive any remuneration for their directorship in BPLAC.

AND CHIEF EXECUTIVEOFFICERBPLAC provides total rewards package to the Executive Director and Chief Executive Officer that consist of guaranteed and variable components that rewards performance and value created for the Company. Our CEO’s reward components support our rewards framework: 1) Guaranteed compensation which includes base salary, allowances and contractual bonus that is reviewed annually to reflect market, individual performance and value created for the company; 2) Short Term Incentive to reward achievement of business and individual performance metrics enabling the individual to share in the immediate success of the company; 3) Discretionary Long Term Incentive to motivate and reward the individual for individual who have contributed significantly to AIA’s success and is likely to continue to do so; and 4) Benefits that are carefully structured supplementing our cash compensation.

51

4

OF DIRECTORS

The Company uses a transparent procedure for the election of directors. The Governance, Nomination and Remuneration Committee looks into the qualifications of directors and thereafter the Board deliberates on the recommendation of the Committee. At the stockholders’ meeting, the shareholders are duly informed by the Corporate Secretary of the qualified nominees and of the voting method and vote counting system. Each stockholder with voting privilege shall be entitled to cumulate his/her vote in the manner provided by law. After the election process, the Corporate Secretary shall count the votes and thereafter declare the duly elected members of the Board.

AND TRAINING OF

DIRECTORSFor newly elected directors, the Corporate Secretary schedules and provides comprehensive orientation to explain the organizational profile, charters, by laws, policies and procedures of the Company. In compliance with the Circular issued by the Insurance Commission, BPI-Philam ensures that all its directors have attended a training and orientation course on Corporate Governance conducted by duly accredited training providers of the Commissions.

The Board members are also encouraged to attend further training and inform the Corporation on such trainings attended. BPI-Philam provides necessary resources in developing and updating its director’s knowledge and capabilities. The Company encourages the directors to attend continuous professional education programs such as Professional Directors’ Program of the Institute of Corporate Directors.

EVALUATIONThe Company has established its own performance evaluation, the criteria of which are based on the Insurance Commission’s Circular on Corporate Governance. Every April of each year, the Board, as well as the Committees, conducts annual self-assessment of its performance, the results of which are submitted to the Governance, Nomination and Compensation Committee and to the Board of Directors.

52

3

In the Annual Board Performance Evaluation Survey, the Board members are required to rate the performance of the Chairman, the CEO, the Board, the Board Committees, and independent directors based on the standards and criteria provided therein. Among the criteria set include but not limited to the following: the appropriateness of the Board’s composition; the director’s skills, expertise, and their participation and contribution in the Board and Committee discussions; the working relationship among the Board, the Chairman, and the senior management; the overall performance of the Chairman, the CEO, the independent directors, the Board and the various Board Committees. In the Survey, the Board members are required to give the subject either an ‘excellent’; consistently good’; ‘adequate’; or ‘needs major improvement’ rating. The directors are also required to provide other ideas and suggestions on how they could further improve the performance of the Board. After accomplishing the survey, the directors will submit the same to the Corporate Secretary, who will then consolidate and evaluate the answers and submit the results to the Governance, Nomination and Remuneration Committee for its approval. The results will then be reported to the Board for its notation.

For 2018, the Annual Board Performance Evaluation Survey was participated by the members of the Board, where the Board registered an overall rating of “excellent”. The result clearly exemplifies the effectiveness and competence of the Company’s Board of Directors. It also shows that it clearly understands the Company’s objectives, as well as the major roles it plays to the Company, its shareholders and stakeholders.

BENEFITBPI-Philam sought the services of Mercer to provide a formal retirement plan for the employees. We adapted the Defined Contribution (DC) Retirement Plan wherein the employer, employee or both make contributions on a regular basis. Monthly contributions are pooled and invested by an assigned fund manager which means that future benefits fluctuate on the basis of investment earnings. During the launch in 2014, employees were given an option to elect the new DC Retirement Plan or remain under statutory minimum normal retirement benefits. The board of directors elected BPI Asset Management and Trust Corporation (BPI AMTC) as fund manager while Zalamea administrates the individual ledgers of each employee. All employees are provided an online account which allows them to view their monthly statements and keep track of contributions and investment earnings.

Each employee is credited an employer contribution monthly based on 8% of his/her current monthly basic salary which started in July 2014. Benefits are computed based on the vesting factor and number of years of service. Minimum years of service entitled for Retirement Pay under DC plan is 5 years. The voluntary contribution has just started this April 2018. Employee participation will be incentivized by the company with 50% of voluntary contributions subject to a maximum of 3% of employee’s monthly basic salary.

53

4

POLICYBPLAC shall declare and pay cash dividends, the amount of which shall be determined through consideration of the following factors: a) local statutory requirements relating to solvency and liquidity; b) ongoing sustainability of corresponding insurance fund taking into consideration likely future changes in regulatory requirements; and c) likely future strategic initiatives.

For the year 2018, the Company declared cash dividend of One Peso and Eighty Nine Centavos (P1.89) per share, or a total amount of Philippines Pesos: One Billion Four Hundred Seventeen Million Four Hundred Eighty Eight Thousand Six Hundred Twenty and Thirty One Centavos (P1,417,488,620.31), payable to all shareholders of the Company in proportion to their holdings.

PERFORMANCEBPI-Philam provides a dynamic work environment that encourages employees to bring their best to work each day. In return, the company offers a Total Reward program including growth opportunities and a comprehensive package of pay and benefits which aims to give employees the choice and flexibility to meet their individual needs.

BPI-Philam’s Reward Philosophy is built on the principles of providing an equitable, motivating and market-competitive total remuneration package that fosters a strong performance-oriented culture. Its strong pay-for-performance culture is aligned with the Company’s operating philosophy of doing the right thing, in the right way, with the right people. It aims to ensure that individual rewards and incentives relate directly to the individual’s performance, the function in which they work, and the overall performance of the business.

The Company also has long-term incentive programs that provides executives certain rewards depending on the performance of the company. The Long Term Incentive (LTI) Plan is a discretionary scheme provided by AIA to motivate and reward executives who have not only made a significant contribution to AIA’s and Philam Life’s performance and success, but also have the potential to contribute more in the future. It operates through the grant of Restricted Share Units (RSU). This means that their contributions to AIA’s sustained and profitable performance mean that there is also the potential for the awards to be financially rewarding for them.

54

3

COMMITTEESAUDIT AND PRT COMMITTEE

Romeo L. Bernardo(Independent Director)

Kelvin Ang(Non-Executive Director)

Jesus P. Tambunting(Independent Director)

CHAIRMAN

GOVERNANCE, NOMINATION & COMPENSATION COMMITTEE

Kelvin Ang(Non-Executive Director)

Jesus P. Tambunting(Independent Director)

Cezar P. Consing(Non-Executive Director)

CHAIRMAN

EXECUTIVE COMMITTEE

Kelvin Ang(Non-Executive Director)

Cezar P. Consing(Non-Executive Director)

Surendra Menon(Executive Director)

Maria Consuelo A. Lukban*(Non-Executive Director)

*as alternate of Mr. Consing

CHAIRMAN

VICE CHAIRMAN

INVESTMENT COMMITTEE

Arleen May S. Guevara(Senior Officer)

Surendra Menon(Executive Director)

Maria Consuelo A. Lukban(Non-Executive Director)

Spencer T. Yap(Senior Officer)

Joseph G. De Dios(Senior Officer)

CHAIRPERSON

EXECUTIVE COMMITTEE

Cezar P. Consing(Non-Executive Director)

Jesus P. Tambunting(Independent Director)

Surendra Menon(Executive Director)

CHAIRMAN

55

4

MEETINGSThe Board had a total of eight (8) meetings in 2018. The directors received the meeting pack five days in advance. The meeting pack includes among others, the Board and Committee Meeting Minutes for approval of the Board, the business and financial highlights of the Company and other items that need Board action and approval.

The presence of at least four (4) out of seven (7) directors is necessary to have a quorum and the affirmative votes of the majority of the directors present are required to decide a matter except where the law or the by-laws require a higher number.

The Board exercises discretionary powers and oversees the management of the company.

The number of meetings held in 2018 and the overall attendance rate are as follows:

16 January 2018

16 Apr. 2018

(Outgoing)

16 Apr. 2018

(Organizational)

10 May 2018

29 May 2018

20 July 2018

15 October 2018

09 November 2018

16 January 2018

16 April 2018

20 July 2018

15 October 2018

02 April 2018

01 October 2018

07 November 2018

BOARD AUDIT & RPT COMMITTEE

GOVERNANCE, NOMINATION &

COMPENSATION COMMITTEE

NO. OF MEETINGS HELD & ATTENDED FOR THE YEAR 2018

8 MEETINGS

94.80%

4 MEETINGS

100%

3 MEETINGS

100%

MEMBER

KELVIN ANG*ROMEO L. BERNARDOARIEL G. CANTOS**JACKY CHAN***CEZAR P. CONSINGMARIA CONSUELO A. LUKBAN****AURELIO LUIS R. MONTINOLA III*****SIMON R. PATERNO*****RYANN ROBERT QUINN*****JESUS P. TAMBUNTINGDARREN THOMSON*****JOSEPH GOTUACO******MENON SURENDRA

8 MEETINGS

8 MEETINGS

3 MEETINGS

8 MEETINGS

-

2 MEETINGS

1 MEETING

1 MEETINGS

8 MEETINGS

-

7 MEETINGS

8 MEETINGS

-

4 MEETINGS

4 MEETINGS

N/A

N/A

N/A

N/A

N/A

N/A

4 MEETINGS

N/A

N/A

N/A

-

N/A

3 MEETINGS

N/A

3 MEETINGS

N/A

N/A

N/A

N/A

3 MEETINGS

N/A

N/A

N/A

*effective 21 January 2019 **until 21 January 2019 ***effective 15 June 2018 ****effective 09 November 2018*****until 16 April 2018 ******until 09 November 2018 56

3

PHILOSOPHY

57

4

OF CONDUCTHonesty and integrity are the cornerstones of the AIA business. AIA serves millions of customers across the most dynamic growth region in the world – and is known and admired for its unwavering commitment to these values.

This reputation and the trust it inspires is critical to the success of the organization. Dedication and commitment to high standards have helped build the organization in the past and continue to do so. It can only maintain such reputation to the future when each employee strives harder to do what is right and by being prepared to take their personal responsibilities in observing the highest standards of integrity and conduct at all times and in every dealing.

This is what the AIA Code of Conduct is about. It sets out AIA’s and its member companies’ commitment to the Operating Philosophy of “Doing the Right Thing, in the Right Way, with the Right people... and the Right results will come.” This establishes the unique culture of AIA across all 18 markets within the Asia Pacific region that includes BPI-Philam.

The AIA Code of Conduct sets out the ethical guidelines for conducting business which is the same code that BPI-Philam observes. This serves as a guide in managing the company’s compliance, ethics, and risk issues.

The standards set forth in the Code also apply to business partners including agents, contractors, subcontractors, suppliers, distribution partners, and those who act on behalf of AIA and BPI-Philam. Thus, the corporation, its directors, senior management and employees are mandated to comply with the policies. The Compliance Department is tasked to implement these policies and monitor compliance therewith.

Like AIA, BPI-Philam has always believed in the power of diverse, talented people to create value and deliver on customer and shareholder expectations. Thus, it competes vigorously to create new opportunities for its customers and for itself. However, competitive advantages are sought only through legal and ethical business practices. With the products, services and responsible business practices, BPI-Philam strives to improve the quality of life of every Filipino. Promoting compliance with local laws and local regulatory requirements that apply to the business is at the foundation of BPI-Philam’s good corporate citizenship.

ANNUAL CERTIFICATE PROGRAMTo ensure that all BPI-Philam employees are aware of the provisions of the Code, an annual certification program is conducted whereby all employees confirm their knowledge and understanding about the rules and guidelines written in the Code.

ORIENTATION PROGRAM

At the same time, it is company policy that all new hires attend the Business Conduct Orientation Program (BCOP) whereby this Code and all other relevant compliance policies are discussed. This program is offered on a monthly basis and is conducted either by Compliance or Training Department.58

3

HEALTHY AND SECUREWORKPLACEBPI-Philam conducts its business in a manner that protects the health, safety and security of its employees and customers.

Situations that may pose health, safety, security and environmental hazards must be reported promptly to management or to the appropriate Corporate Security Personnel.

Avoiding security breaches, threats, losses and theft requires that all employees remain vigilant in the workplace and while carrying out business. Employees are encouraged to notify management or Corporate Security of any issue that may impact the company’s security, fire and life safety or emergency readiness.

Using, selling, possessing or working under the influence of illegal drugs at BPI-Philam is strictly prohibited. At the same time, use of alcohol while conducting business for BPI-Philam is also prohibited.

Physical security systems reduce the risk of exposure.

Entry controls are implemented to ensure company’s safety security and protection. Wearing of IDs and uniforms are strictly observed.

BPI-Philam respects the personal information and property of employees. Employees expect the company to carefully maintain the personal information they provide. Employee trust must not be compromised by disclosing this information other than to those with a legitimate need to know.

Access to personal information or employee property is only authorized for appropriate personnel with a legitimate reason to access such information or property. From time to time, BPI-Philam may access and monitor employee internet usage and communications to assess compliance with laws and regulations, policies and behavioral standards. Subject to local laws, employees shall have no expectation of privacy with regard to workplace communication or use of AIA and BPI-Philam’s information technology resources.

ETHICAL PRACTICES

The Treating Customers Fairly Policy demands that customers are treated fairly at all times and that products, services, and advice are appropriate to meet customer needs. Marketing, advertising and sales-related materials and services are truthful and accurate, and misrepresenting or attempting to mislead or deceive customers by use of unsupported or fictitious claims about BPI-Philam products or those of its competitors are not acceptable.

BPI-Philam adopts a structured framework in handling complaints related to market misconduct. The Customer Complaints Handling Process ensures that all customer complaints and grievances are immediately addressed. The process defines the step-by-step approach in addressing and handling complaints as a result of any of its sales personnel’s misconduct.

Treating Customers Fairly

59

4

A Regulatory and Compliance Disciplinary Committee evaluates all complaints and determines whether sales personnel have committed any wrongdoing. Any sales personnel found guilty of any market conduct-related offense is subjected to appropriate sanctions.

Misconduct includes but is not limited to misrepresentation of product features, misselling, policy replacement, misappropriation of client monies, and any other infringement of the Market Conduct Guidelines.

BPI-Philam recognizes its responsibilities in protecting personal data and sensitive information of all its stakeholders including employees, customers, intermediaries, business partners and third party service providers. The Board of Directors, Management and staff of BPI-Philam commit themselves to adopt and adhere to the Policy guidelines to ensure protection of personal information and sensitive data collected by and shared with the Company.

The Data Privacy Program of BPI-Philam is aligned with that of AIA’s Data Privacy Policy and with RA 10173, the local Data Privacy Law. Under the program, the BPI-Philam CEO shall be responsible in the implementation of these guidelines across all its business units and in ensuring that all employees, officers and staff are aware of their obligations stated in the guidelines.

Each employee is expected to comply with the standards when managing personal data being collected and handled for processing. Compliance shall be responsible for keeping and maintaining effective guidelines by providing second line oversight and monitoring of implementation.

To strengthen corporate governance, the BPI-Philam Board of Directors appointed a Data Protection Officer for the Company who shall be tasked to oversee the implementation of the law (RA10173) otherwise known as the Data Privacy Act of 2012 based on the issued Implementing Rules and Regulations and ensure that appropriate operational controls are implemented across all units or departments.

BPI-Philam’s Data Privacy Program Manual & Policy Guidelines outlines the company’s policy requirements and provides guidance to all employees, intermediaries & third parties on how personal data should be collected, used, stored, transferred and disposed. It further clarifies the roles and responsibilities of the employees and intermediaries about the relevant standards and procedural controls expected to be observed to secure and protect personal data.

Data Privacy

An employee’s position in BPI-Philam must not be used for inappropriate personal gain or advantage. Any situation that creates, or even appears to create a conflict of interest between personal interests and the interests of the company must be appropriately managed.

Conflicts of interest (whether potential or actual conflicts) must be reported. There is a system being used for the reporting. Managers are expected to take appropriate steps to prevent, identify and appropriately manage conflicts of interests of those they supervise.

All AIA and BPI-Philam employees are prohibited from taking for themselves, or directing to a third party, a business opportunity that is discovered through the use of company’s corporate property information. BPI-Philam employees are prohibited from using corporate property, information or position for personal gain.

Conflict of Interest

60

3

Employees are asked to declare if they have any personal relationships within the group. Immediate family members, members of the household and individuals with whom an employee has a close personal relationship within the group must never improperly influence business decisions. When determining whether a personal relationship might lead to a conflict of interest, the following questions can serve as guide:

• Does one of us have influence over the other at work?• Does one of us supervise or report to the other?• Could an outsider view the situation as a conflict of interest?

BPI-Philam adheres to its Fair Dealing Policy, which ensures that businesses with the customers, service providers, supplier and competitors are conducted in a fair manner. Following AIA’s model, BPI-Philam seeks competitive advantages only through legal and ethical business practices. Every employee must conduct business in a fair manner with customers, service providers, suppliers and competitors.

Disparaging competitors or their products and services are discouraged. Improperly taking advantage of anyone through manipulation, concealment, abuse of privileged information, intentional misrepresentation of facts or any other unfair practice is not and will not be tolerated at BPI-Philam much more in the AIA Group.

It is also the policy of BPI-Philam to uphold creditor’s rights by honouring its contractual obligations with all its creditors and counter parties, in accordance with the provisions of their contracts and the law. In the conduct of its business dealings with third parties, BPI-Philam undertakes to honour all its commitments, stipulations and conditions set forth in their binding agreements.

Fair Dealing and Creditor’s Right

Business partners serve as extensions of BPI-Philam to the extent that they operate within contractual relationships. Business partners are expected to adhere to the spirit of the AIA Code of Conduct and to any applicable contractual provisions.

Business partners must not act in a way that is prohibited or considered improper for a BPI-Philam employee. Employees must ensure that customers, agents, and suppliers do not exploit their relationship with BPI-Philam or use BPI-Philam’s name connection with any fraudulent, unethical or dishonest transaction.

Suppliers and vendors are selected on the basis of performance and merit in accordance with a fair and transparent process. Requirements for suppliers and vendors to follow the standards in the Code must be included in the vendor management programme.

The total expenditure on goods and services from third party suppliers form a significant part of BPI-Philam’s operating cost. Any activity by a line of business to acquire goods/services must be undertaken in a professional manner to ensure BPI-Philam is able to maximize the value and manage risks associated with use of external suppliers.

The local Sourcing Policy, which took effect in November 2013, sets out the framework within which BPI-Philam must engage external suppliers for goods/services and is supplemented by BPI-Philam’s Sourcing Practice Guide. This provides BPI-Philam the standard processes and document templates in engaging suppliers that should be read in conjunction with the policy document.

Sourcing Policy

61

4

The BPI-Philam Sourcing Policy, with the AIA Group Sourcing Policy as a model, was defined with the primary objective to establish standardized sourcing procedures.

As set out in the AIA Group Sourcing Policy, a Local Sourcing Lead (LSL) or a designate is appointed and will be responsible for ensuring implementation, execution, update and compliance of the local policy. This person should closely work with the AIA Group Sourcing (GS) team.

BPI-Philam also complies with the AIA Code of Conduct, which provides that the Company select suppliers and vendors on the basis of performance and merit in accordance with a fair and transparent process. Appropriate due diligence is performed regarding potential agents, consultants and independent contractors prior to engaging their services.

Like AIA, BPI-Philam seeks supplier partnerships with diverse businesses and values suppliers that share the Company’s dedication and commitment to diversity and social responsibility.

Supplier Selection

Inquiries from regulators outside the normal course of BPI-Philam’s regulatory relationships must be reported immediately to the Compliance Officer or a designated Legal Counsel before a response is made.

Financial reporting-related inquiries may be responded to by authorized comptrollers. Responses to regulators must contain complete, factual and accurate information. During a regulatory inspection or examination, documents must never be concealed, destroyed or altered, nor must lies or misleading statements be made to regulators. Requests from auditors are subject to the same standards.

Communicating With Regulators and Other Government Officials

Pursuant to Section 18 of Republic Act (RA) No. 9160, also known as the “Anti-Money Laundering Act of 2001”, as amended by RA No. 9194, RA No. 10167, RA No. 10168 and RA No. 10365, all covered institutions which include insurance companies supervised or regulated by the Insurance Commission are mandated to formulate their respective money laundering prevention program in accordance with the said law.

As a matter of policy, BPI-Philam shall foil any attempt by anyone to use the Company or its affiliates for money laundering purposes. This Anti-Money Laundering Program, together with the Company’s Guidelines, establishes the governing principles and business standards to protect BPI-Philam and its business operations from becoming an unwitting tool of money launderers. The company’s management, officers and staff must remain vigilant in the fight against money laundering and financing of terrorism and shall collectively oppose any effort to violate or flaunt the “Anti- Money Laundering Act of 2001”, as well as its implementing rules and regulations.

In order to promote an effective AML compliance program, the following actions were taken:

Institutionalized the AML Committee to ensure effective implementation of the company’s AML program. The Chairman of the AML Committee is the Chief Legal Officer’s Corporate Secretary with the Head of Operations and Head of Compliance as members.

Anti-Money Laundering and Counter Terrorist Financing

62

3

Adopted a Risk-Based Approach, and strictly implements Enhanced Due Diligence for defined High Risk Customers. Continuous eLearning for employees and face-to-face AML training for its authorized agents.

Adopted the Actimize system with 3 modules – Watch List Filtering or screening against PEPs and sanctioned persons; Customer Due Diligence that provides risk scoring for all clients; and Suspicious Activity Monitoring that provide red flag/ alerts for transactions, particularly, cash transactions.

The Policy is applied alongside the AIA Code of Conduct. It provides guidance on giving and accepting gifts and entertainment. The Anti- Corruption Guidelines specifies the roles, responsibilities and procedural controls for transactions involving government officials. All relevant laws countering bribery and corruption must be upheld. If local laws and regulations require higher compliance standards vis-a-vis the guidelines of the AIA Code of Conduct, then BPI-Philam must meet the higher standards.