bpo sector overview

TRANSCRIPT

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 1/22

BPO SECTOR OVERVIEW

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 2/22

Globalization

�The most important f orce shaping global economics and politics in the early twenty-f irst century is a triple convergence - of new players, on a new playing f ield, developing new

processes and habits f or horizontal collaboration."

�"The 'hot line,' which used to connect the

Kremlin with the White House has been replaced by the 'help line,' which connects everyone in America to call centers in Bangalore."

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 3/22

ITES-BPO Industry

BPO predicted to overtake ITO in next 5 years

� The term captures: customer f acing, voice activities

non-customer f acing, back off ice activities

� end-to-end integrated services

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 4/22

Why India?

Still seen as paving the way among developing

countries

Most of the export of IT and ITES go to the UKand US

Off -shoring largely f ollows the contours of

linguistic and cultural compatibility, arising

f rom the legacy of empire and colonialism

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 5/22

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 6/22

Activities

Horizontals

± Processes that are seen as being similar across industries

(Customer interaction and support, f inance and

accounting, HRM, procurement services, and knowledgeservices)

Verticals

± Processes which require vertical-specif ic knowledge and

are not easily replicable across industries, such as claims processing f or the insurance industry or credit card

collections f or the credit services industry

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 7/22

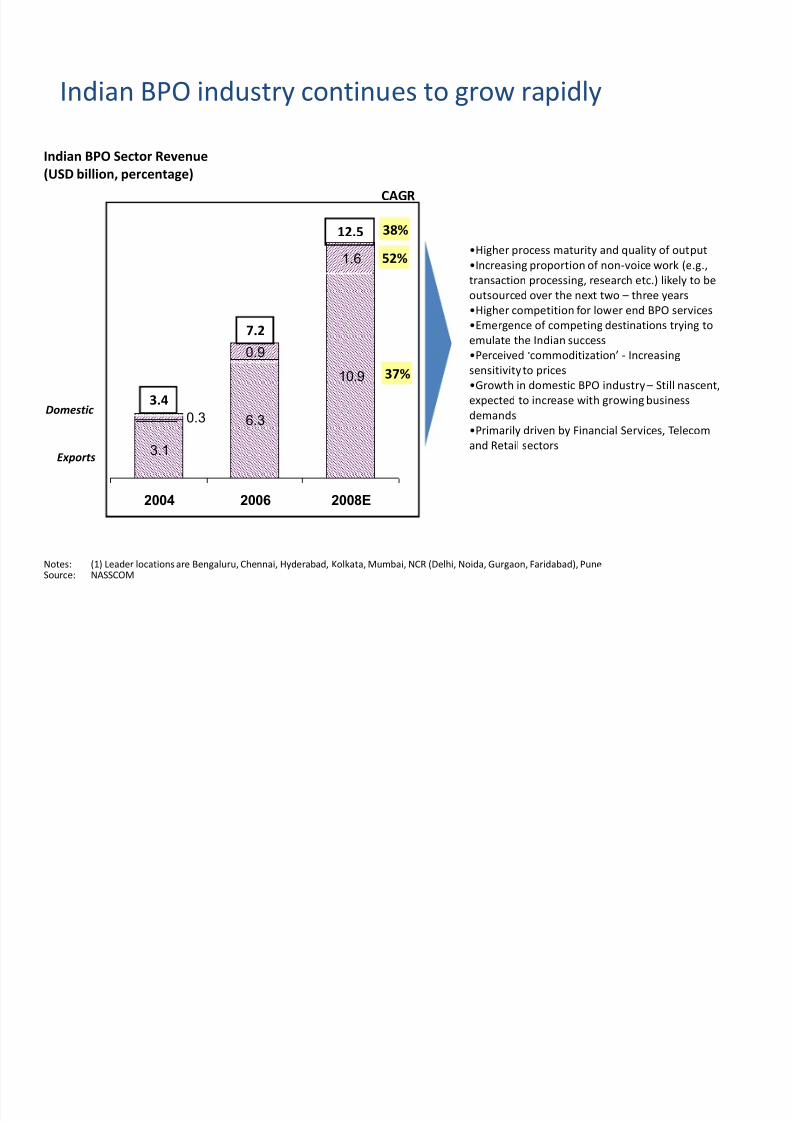

Indian BPO industry continues to grow rapidly

Notes: (1) Leader locations are Bengaluru, Chennai, Hyderabad, Kolkata, Mumbai, NCR (Delhi, Noida, Gurgaon, Faridabad), PuneSource: NASSCOM

Exports

Domestic

Indian BPO Sector Revenue

(USD billion, percentage)

3.1

6.3

10.9

0.9

1.6

0.3

2004 2006 2008E

3.4

7.2

12.5

CAGR

38%

37%

52%Higher process maturity and quality of output

Increasing proportion of non-voice work (e.g.,

transaction processing, research etc.) likely to be

outsourced over the next two three years

Higher competition f or lower end BPO services

Emergence of competing destinations trying to

emulate the Indian success

Perceived commoditization - Increasing

sensitivity to prices

Growth in domestic BPO industry Still nascent,

expected to increase with growing business

demandsPrimarily driven by Financial Services, Telecom

and Retail sectors

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 8/22

Underlying dynamics

ICTs, which have enabled market expansion, removed geographical constrictions and reduced the need f or inf rastructure (Miozzo and Ramirez, 2003)

Time is compressed while space and distance are expanded (Massey 2007)

Distance shrinking ICTs enabled remote delivery and generated

economies of scale through the centralisation of previously-dispersed f acilities ± Work can take place anywhere there is a phone line thus making it easy to

establish operations nearly anywhere on the globe (Ritzer and Lair 2008: 40).

Yet paradoxically, place and space takes on increasing importance

New regulatory f rameworks, competitive sectoral markets, and broader

changes associated with liberalisation, privatisation and de-regulation ± GATS

± Deregulation of Indian telecoms industry

± Pressure f rom NASSCOM f or benef its to ITES-BPO sector

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 9/22

Tiered cities

No. of providers

per city

Average centre

Size (employees)

Tier 1

Delhi-NCR,Mumbai, Bangalore

120-150 350-45

Tier 1.5

Chennai,

Hyderabad, Pune,Kolkata

75-100 250-300

Tier 2/3 10-15 180-220

Tier 3/4 ?? ??

(Nasscom-Everest 2008)

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 10/22

However, most of this growth is currently concentrated in

~7 leading locations

Success and economic growth of these locations has led to significant interest from

other states / locations to leverage this sector as a growth driver for their economies

The top 7 locations account for around 90% of the

industry¶s employment today

These locations have helped in transforming their

states into a knowledge driven economy with high

per capita income

However, the hyper and concentrated growth acrossmost of these leading locations have resulted in:

± Saturation and deteriorating infrastructure

± Presence of large number of IT-BPO players

resulting in high attrition and increased

wages

± Rapid growth of other sectors, resulting in

greater competition for talent

± Rising real estate costs

± Deteriorating social and living environment

Hyderabad

Delhi

Faridabad

Bangalore

Mumbai

Pune

Chennai

Noida

Kolkata

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 11/22

Choice of an

off shoring

destination

country

Accelerator SteeringSmooth

Brake

Brake

Primary

motivating

f actors

Inhibiting

f actors

Facilitating

f actors

A f ramework f or evaluating the attractiveness of a

country f or off shoring

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 12/22

Bangalore

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 13/22

Hyderabad

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 14/22

� Cities are at breaking point, and f urther

growth will have to come f rom entirely new

business districts outside of T1 and T2 cities

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 15/22

Electronic City Bangalore

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 16/22

� The processes of social reproduction then crystallize into a relatively permanent patchwork quilt of local, interregional and

even international specialisation. This patchwork quilt may then also be associated with marked differentials in the value and value-productivity of labour power

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 17/22

Population of urban agglomerations with 10m+ inhabitants

1975

1 Tokyo 26.6m

2 New York-Newark 15.9m

3 Mexico City 10.7m

1950

1 New York-Newark 12.3m

2 Tokyo 11.3m

2007

1 Tokyo, Japan 35.7m

2 New York-Newark 19m

3 Mexico City, Mexico 19m

4 Mumbai, India 19m

5 Sao Paulo, Brazil 18.8m6 Delhi, India 15.9m

7 Shanghai, China 15m

8 Kolkata, India 14.8m

8 Dhaka, Bangladesh 13.5m

10 Buenos Aires, Argentina 12.8m

(United Nations 2007)

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 18/22

Leaders Challengers Followers Aspirants

� Ahmedabad(2)

� Bhubaneshwar � Chandigarh(

)

� Coimbatore

� Indore

� Jaipur

� Kochi

� Lucknow

� Madurai� Mangalore

� Nagpur

� Thiruvananthapuram

� Tiruchirappalli

� Vadodara

� Visakhapatnam

� Aurangabad

� Bhopal� Goa

� Gwalior

� Hubli-Dharwad

� Kanpur

� Mysore

� Nashik

� Pondicherry� Salem

� Surat

� Vijayawada

� Allahabad

� Dehradun� Durgapur

� Gangtok

� Guwahati

� Ludhiana

� Patna

� Raipur

� Ranchi� Shimla

� Siliguri

� Srinagar

� Varanasi

Findings indicate that the 50 locations in India are categorized along a typical f our stage

development path

Location Classification

Increasing Location Attractiveness

Bangalore

Chennai

Hyderabad

Kolkata

Mumbai

NCR

Pune

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 19/22

TRAINING & DEVELOPMENT

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 20/22

NEED FOR T&D

� Productivity

� Team

� Organization Culture� Organization Climate

� Quality

� Healthy work environment� Health and Safety

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 21/22

BENEFITS

� Increased job satisf action and morale among employees.

� Better inter personal relationship and

customer satisf action.

� Increased employee motivation.

� Increased eff iciencies in processes, resulting in

improved f inancial gain.� Increased capacity to adopt new technologies

and methods.

8/4/2019 BPO Sector Overview

http://slidepdf.com/reader/full/bpo-sector-overview 22/22

THANKYOU