bpva presentation at 11th forum solarpraxis

DESCRIPTION

BPVA Presentation at 11th Forum SolarpraxisTRANSCRIPT

Abu Dhabi

The British Photovoltaic Association

Your Gateway to the UK PV market James Steynor

Chief Executive Officer

Friday, 12th November

What’s to follow

The emergence of the BPVA The BPVA – a solid foundation The BPVA mission – to focus on PV Partnerships and alliances UK market overview Installed capacity development The FIT – an overview The UK FIT v others Insolation/ irradiance UK Estimated regional development The BPVA short-term objectives BPVA at Ecobuild Closing remarks

The emergence of the BPVA

Backdrop: – Major drive by UK government (DECC) towards reducing UK carbon emissions –

photovoltaic a significant component – The feed-in tariff (FIT) April 1st sends clear message to users and investors alike (as

confirmed following spending review yesterday) – Widespread adoption of PV key to meeting target of 80% reduction in carbon emissions

by 2050 Focus:

– PV has a unique profile v other alternative sources of renewable energy (wind/tide etc) – PV offers scalable projects from existing homes through to large commercial installations – Unlike other renewable energy sources, PV is on a local scale and can contribute directly

to local energy requirements – PV is regarded as so key it is a standalone initiative in most countries

Support: – The BPVA is filling a need identified by a key group of companies – Other PV associations outside the UK want to see a focus in the UK market – A fully independent initiative is needed with no distractions (or conflicts) from alternative

renewable energy technologies

The BPVA – a solid foundation

A fully independent non profit making association 100% dedicated to photovoltaic in the UK – Focusing on the technology and application of PV – An ambassador for PV both in the UK and representing home interests internationally – No favour: all members treated equally

Dedicated to make the most of the UK market for PV – Educate and inform the consumer and other user groups – Stimulate interest in PV in a broad range of applications – A catalyst to investment – both indigenous and from abroad – Stimulate growth in the UK PV sector – job creation both in innovation and application

Dynamic management – Streamlined structure to react fast to market demands – Close contact to members through Board level representation – Proactive; driving force behind PV in the UK

The BPVA mission – to focus on PV

To educate and inform – Awareness of technology and benefits to consumer – Promotion at grassroots level – eg schools – Demystifying and encouraging widespread adoption

To stimulate growth in the UK photovoltaic industry – Facilitating PV roll-out – planning assistance, gateway to technology support etc. – Both working with and lobbying government (local and national) – Advising key decision-makers on policies to develop a sustainable PV market

Establish photovoltaic power as a leading energy source in the UK – Selling and promoting the vision – Stimulating growth in infrastructure and technologies behind PV – The catalyst to providing significant environmental and monetary benefits

Assist members in their business development – In the UK, the European Union and beyond – Networking opportunities through BPVA events – Building a foundation for growth

Government & Media Department of Energy & Climate Change, Carbon Trust, Solar Installer, Photon, Solar in Building Design & Construction, Sun & Wind Energy

Associations & Academia

EPIA, SER, ASIF, GIFI , SEIA, SEPA, PV Group,

IPVEA , ISES, JPEA, BSW, CSIA

Fraunhofer Institute, Royal Institute of British

Architect (RIBA) NRF

Partnerships & Alliances

UK market overview (1)

Drivers for renewables: – UK is primarily very dependent on fossil fuels. – Since 2004 rapid price increase in electricity stimulates interest in alternative energy

solutions – UK government mission: to make renewable energy account for 15% of its total energy

mix by 2020 with an 80% reduction in carbon emissions by 2050 Potential

– Population more than 61 million represents one of the largest PV markets in Europe – Drivers include Political, Economical, Social, Technical and Environmental factors – Great public support for renewable energy – Large number of houses (>22M) and flats owner occupied (>65% of all houses) allowing

easier adoption of PV – Estimated potential for PV 60TWh per year - over one-third (>20TWh per year) in

domestic retro fit; commercial sector: 5.5 TWh per year in small 4-10 kW systems.

UK market overview (2)

The UK FIT – April 2010: UK implemented generous feed-in tariff (FIT) - the “Clean Energy Cashback”

scheme (unlike other European countries where these are being cut back) – Many European countries only benefit from energy sold back to the grid - UK scheme

provides payment for energy generated – Uncapped: should make this one of the most successful European PV markets – Set for 25 years giving great stability to adopters

Installed capacity approx 30 MW end 2009: Forecast – 60 MWp by the end of 2010 – 1 GWp as early as 2013 – >5 GWp as early as 2016

Factors effecting potential: – Consumer awareness – Number of MCS accredited installers and infrastructure in general – Money supply (green loans through the Green Investment Bank – GIB) – System costs – components and critically installation (30% higher in UK than Germany as

of today)

Assumptions of baseline scenario: Lack of MCS certified installers leads to bottleneck No “green loans” available System installation costs remain high

Assumptions of progressive scenario: MCS accreditation without problems Green loan introduced in 2011 Considerable reductions in system installation costs

MCS, green loans and system installation costs are key factors in market development

Installed capacity development

Background to capacity development

Growth of domestic sector fuels Progressive scenario – key factors: – Availability of MCS accredited suppliers/installers – Green loans – Public awareness

Open space/commercial installations growth observations: – FIT and cost of installation key factors in ROI – Financing is more readily available for large contracts – Not dependant on MCS accreditation – larger contracts are more self regulated (ROO-FIT)

Baseline scenario Progressive scenario [MWp] [MWp]

Enhanced financing, certification and system cost levels favor the residential segment above average

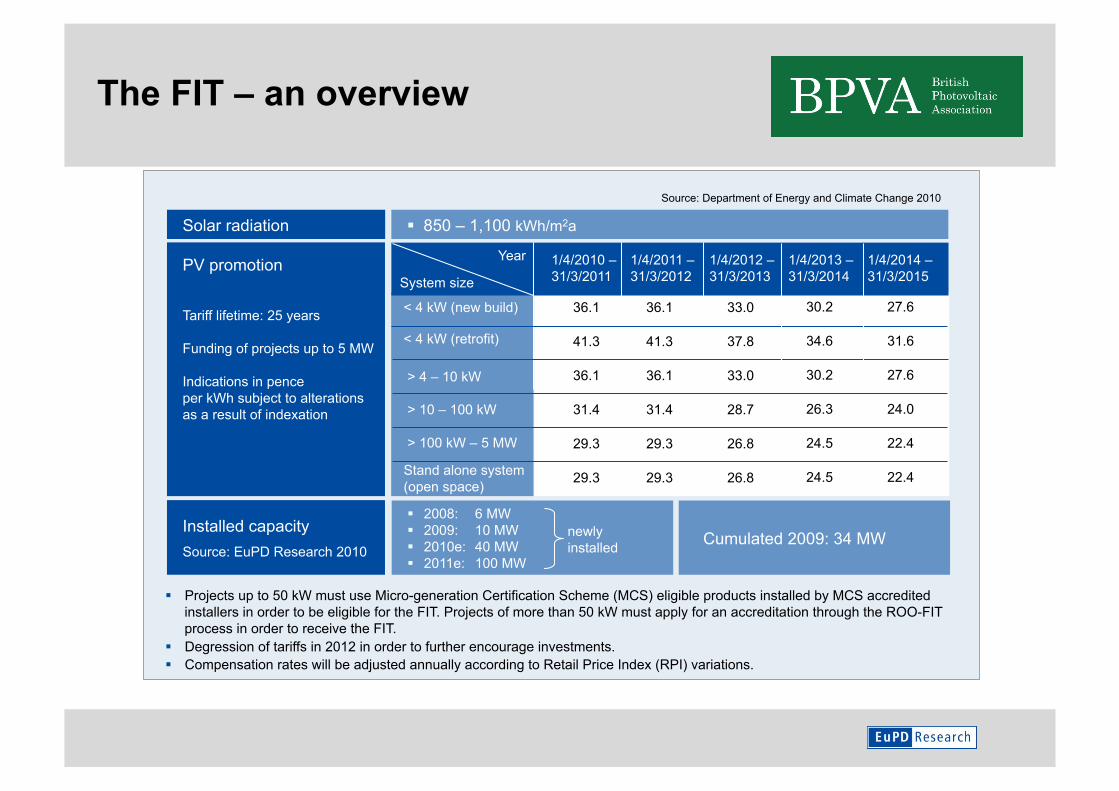

The FIT – an overview

850 – 1,100 kWh/m2a Solar radiation

2008: 6 MW 2009: 10 MW 2010e: 40 MW 2011e: 100 MW

Installed capacity Source: EuPD Research 2010

Cumulated 2009: 34 MW newly installed

PV promotion

Tariff lifetime: 25 years

Funding of projects up to 5 MW

Indications in pence per kWh subject to alterations as a result of indexation

System size

> 4 – 10 kW

< 4 kW (retrofit)

1/4/2010 – 31/3/2011

36.1

41.3

36.1

36.1

41.3

36.1

33.0

37.8

33.0

< 4 kW (new build)

Year

> 10 – 100 kW

> 100 kW – 5 MW

Stand alone system (open space)

31.4 31.4 28.7

29.3 29.3 26.8

29.3 29.3 26.8

Projects up to 50 kW must use Micro-generation Certification Scheme (MCS) eligible products installed by MCS accredited installers in order to be eligible for the FIT. Projects of more than 50 kW must apply for an accreditation through the ROO-FIT process in order to receive the FIT.

Degression of tariffs in 2012 in order to further encourage investments. Compensation rates will be adjusted annually according to Retail Price Index (RPI) variations.

30.2

34.6

30.2

26.3

24.5

24.5

27.6

31.6

27.6

24.0

22.4

22.4

1/4/2011 – 31/3/2012

1/4/2012 – 31/3/2013

1/4/2013 – 31/3/2014

1/4/2014 – 31/3/2015

Source: Department of Energy and Climate Change 2010

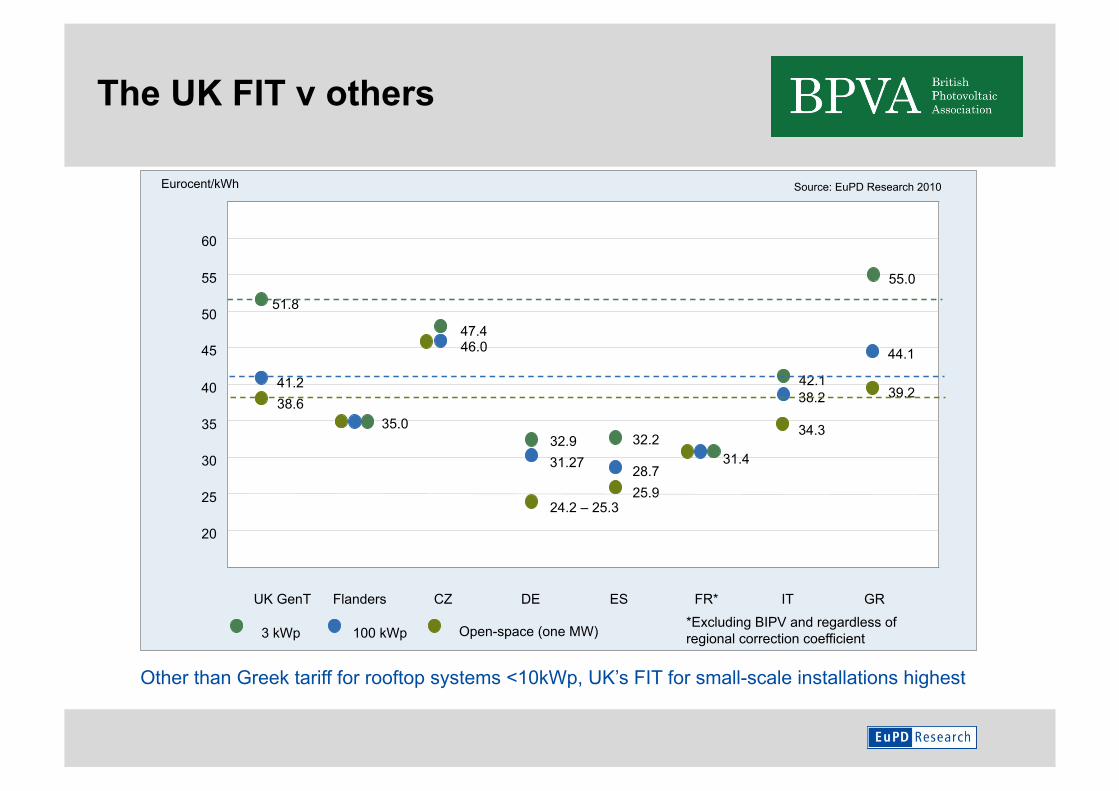

The UK FIT v others

Other than Greek tariff for rooftop systems <10kWp, UK’s FIT for small-scale installations highest

UK GenT Flanders CZ DE ES FR* IT GR

Eurocent/kWh

60

50

40

30

20

25

35

45

55

3 kWp 100 kWp Open-space (one MW)

32.2

25.9

31.4

39.2

55.0

34.3

38.2

47.4 46.0

35.0

51.8

41.2 38.6

28.7

32.9

24.2 – 25.3

Source: EuPD Research 2010

31.27

*Excluding BIPV and regardless of regional correction coefficient

44.1

42.1

Insolation/irradiance UK

Stated irradiation level (average) for UK 850 kWh/m2 per year

Cornwall 1,100 kWh/m2 per year

Education for the UK consumer: PV does not need direct sunlight

Data courtesy of NASA

Estimated regional development

Scotland

Northern Ireland

North East

North West

Yorkshire& Humberside

East Midlands

Eastern

London

South East South West

West Midlands

Wales

0-6% 7-10% 11-15% 16-25% 26-35%

Activity seen by installers /distributers

25.6 % active across the UK and not just specific regions.

Highest levels of activity found in London and the South East at levels between 26-35%.

PV-activity in Wales, Eastern and Yorkshire & Humberside is lowest(7%).

South West, East and West Midlands and North West 11% to 15%

Scotland and the North East region 7% to 10%

Despite low levels of irradiation even Northern rural regions still have moderate potential in open-space developments

London and South East have highest levels of activity.

BPVA short-term objectives

To educate – Rollout of educational leaflets to go to schools/households – General awareness of opportunities in the UK

To inform – Represent the facts about PV – Permanent showcase in the BPVA HQ at The Building Centre (London)

To facilitate – Organise regular events with a clear sector focus

• Solar in Building Design and Construction • Solar in Farming and Agriculture • Solar Bankability and Finance • Solar in Commercial and Industrial applications • Solar in Sport and Leisure • Solar in Education

And overall to support our members

BPVA at Ecobuild – March 2011

“The future of design, construction and the build environment” Largest event of its kind in the UK

– Over 1,000 exhibitors and 41,000 visitors in 2010 – even larger in 2011 – Mix of trade, industry, consumer – both UK and from abroad – High profile political attendance

The BPVA stand – Large member area (145 m2) with showcase table top stands (limited – first come first

serve) – Dedicated on-stand theatre with presentations running 10 am to 4pm all 3 days – Participating showcase BPVA members listed in promotional material and on-stand

branding including presentation opportunities Join us and be part of this exciting event!

Closing remarks

The UK - a tremendous opportunity

To realise this will demand a great focus - from education through to infrastructure

The BPVA: A driver and catalyst to maximise the potential of PV in the UK

Thank you for your time With particular thanks to

James Steynor, CEO BPVA [email protected]

www.bpva.org.uk