brazil: the heartbeat of the south … - sao paulo technology center antonio bardella avenue, 322...

TRANSCRIPT

AMT - Sao Paulo Technology Center

Antonio Bardella Avenue, 322

Sorocaba - SP

01427-002

Brazil

Telephone: +55 (15) 9806-7981

E-mail: [email protected]

www.AMTonline.org

BRAZIL: THE HEARTBEAT OF THE SOUTH AMERICAN MARKET

Achilles Arbex, General Manager, AMT Sao Paulo Technology Center

It is true that the BRICS have slowed down their growth in 2013. Nevertheless, among them, Brazil has been surprisingly resilient and offers a strong opportunity for manufacturing technology suppliers. The presentation will provide a status report about the Brazilian market while discussing the outlook for its industrial growth. Brazil seen from the inside, presents many more opportunities then when looked upon from the outside. This presentation is one that comes from within and will also cover the challenges that still exist, but at the same time, indicating the roadmap to overcome the barriers and for participating in the many business opportunities that are only accessible by the companies that have a direct and significant presence in the country. This presentation will also discuss the newly established "AMT Sao Paulo Technology Center" in Sorocaba, SP, and the many resources that the Center offers to AMT members.

Achilles P. Arbex joined AMT as General Manager of the AMT Sao Paulo Technology Center in Sorocaba, Brazil, in May 2013. Achilles graduated as an Automation and Control Engineer and has a post-graduate degree in Strategic Project Management from ITA – The Aeronautics Technology Institute in Sao Jose dos Campos, SP, Brazil. Prior to the current position at AMT, Achilles held positions at ZF Brazil, ZF Germany and Dana Industries. Achilles’ experience involves business development and industrial investment in Brazil at international and domestic manufacturing companies and at various industrial segments, including automotive, aerospace, electric and electronic, oil and gas, alternative energy, and others.

AMT – The Association For Manufacturing Technology

7901 Westpark Drive

McLean, VA 22102-4206

Telephone: 703-827-5228

Fax: 703-749-2753

E-mail: [email protected]

www.AMTonline.org

BRAZIL: THE HEARTBEAT OF THE SOUTH AMERICAN MARKET

Mario Winterstein, Business Development Director, AMT – The Association For Manufacturing Technology

It is true that the BRICS have slowed down their growth in 2013. Nevertheless, among them, Brazil has been surprisingly resilient and offers a strong opportunity for manufacturing technology suppliers. The presentation will provide a status report about the Brazilian market while discussing the outlook for its industrial growth. Brazil seen from the inside, presents many more opportunities then when looked upon from the outside. This presentation is one that comes from within and will also cover the challenges that still exist, but at the same time, indicating the roadmap to overcome the barriers and for participating in the many business opportunities that are only accessible by the companies that have a direct and significant presence in the country. This presentation will also discuss the newly established "AMT Sao Paulo Technology Center" in Sorocaba, SP, and the many resources that the Center offers to AMT members.

Mr. Winterstein’s experience involves industrial engineering, production and manufacturing processes in the metalworking industry, combined with 25 years in sales engineering, sales management and international marketing. Mr. Winterstein received his degree in São Paulo, Brazil, as an Industrial Engineer; he communicates fluently in six languages. He lived and worked in Brazil, Mexico and Europe prior to residing in the USA. Prior to joining AMT in January 1998, he held various positions in metal cutting and metal forming machine tool builders in the United States. Mr. Winterstein’s responsibility at AMT is to provide international business support to AMT members in the Americas and Japan.

10/14/2013

1

Brazil: The Heartbeat of the South American MarketAchilles Arbex

Mario Winterstein

Introduction

Mario C. Winterstein

Business Development Director

AMT – The Association For Manufacturing Technology

McLean, VA – USA

Achilles P. Arbex

General Manager

AMT Brazil Sao Paulo Technology Center

Sorocaba, SP – Brazil

10/14/2013

2

Agenda

Introduction

Why Brazil?

Outlook, Opportunities and Threats

Myths vs. Reality

AMT Sao Paulo Technology Center

Q&A

Why Brazil?

Brazilian trade is expected to rise by 50% to 100% or

more over the next ten years, depending on the

market. (Oxford Economics)

Brazil’s auto market is the biggest in Latin America

and the fourth biggest in the world. (Ernst & Young)

Brazil’s domestic market is bigger than that of Mexico,

Argentina, Colombia, Chile, and Peru combined.

(Oxford Economics)

10/14/2013

3

Why Brazil?

Brazil GDP growth was 0.9% in 2012, and is trending to

2.4% in 2013. Estimated growth is at 2.2% for 2014

(Reuters).

Inflation to drop from 5.8% in 2013 to 5.7% for the

coming year (Banco Central).

The BRL is expected to remain around BRL 2.2 per USD

until the end of 2014 (Reuters).

Industrial output recorded 2.1% in 2013, while the

forecast is 2.65% for 2014 (Reuters).

Why Brazil?

200 million consumers with increased purchasing

power

Half of the economy of Latin America.

Per capita income 30% higher than China, and a

growing consumer class (World Bank)

Weathered the financial crisis better than most

markets

Agricultural superpower

10/14/2013

4

Brazil and the World

Source: CNN Money

U.S.A.$16.2

Japan$5.1

China$9.0

Germany$3.6

France$2.7 Brazil

$2.5 England$2.4

Russia$2.2

Italy$2.1

India$2.0

View by Size | Growth

2013

GDP in Trillions of U.S. DollarsWorld’s sixth‐largest economy

Major Industrial Clusters

South Precision Components (Eaton,

MWM, Bosch) Die & Mold (Suspensys,

Hassmann, Voelstapine) Machine Tools (Gühring,

Welle Laser, Haas) Auto (GM, BMW, VW,

Renault, Master, Suspensys) Trucks & Buses (NC², Agrale,

Volvo, DAF/Paccar) Agricultural Equipment

(AGCO, CNH, Jacto, Agrale)

Southeast Precision Components

(Grauna Aerospace, ThyssenKrupp, Cummins)

Die & Mold (Motopeças, Cinpal, Engrecom)

Machine Tools (Trumpf, Romi, Makino, Mazak)

Auto (GM, Fiat, Iveco, MAN LA, Peugeot‐Citroen, Chery, Hyundai, Sany)

Trucks & Buses (MAN, MBB, Iveco, Ford)

Agricultural Equipment (CNH, JCB, Deere)

Aerospace (Helibrás, Embraer)

Oil & Gas (Petrobrás, Emerson, Vanasa)

Electronics (Samsung, Foxcom, Flextronics, ABB)

Central‐East Agricultural Equipment

(Deere, MTZ) Auto (Hyundai, Mitsubishi)

North (Manaus Area) Motorcycles (Honda,

Kasinski, Yamaha, Suzuki) Bicycles (Dorel /Caloi,

Monark, Prince) Home Appliances (Brastemp,

Electrolux, Elgin) Electronics (CCE, Flextronics,

Evadin)

Northeast Auto (Ford, Fiat, Baterias

Moura) Oil & Gas (Emerson, Tyco,

Pentair, Dresser/GE) Energy (Feralcom, WMF,

Voith)

10/14/2013

5

Industrial Production

Source: IBGE.

Recovering from a decline period in 2011 –

2012

Increase in capital goods’ production since

the beginning of 2013

Intermediary and consumer goods’ industry

experienced a small but healthy change in the

last two years

Manufacturing output growth rates are way

ahead of the GDP growth

Industrial Productivity

Source: IBGE.

Industrial productivity in the processing

industry has been increasing since 2003

Productivity growth of 30% over last two

quarters

Brazil historically showed better resilience

to financial crisis when compared with

other markets

Government offers incentives to boost

industrial productivity to encourage

investment

10/14/2013

6

Installed Capacity Utilization

Source: FGV/BCB.

2013 Utilization Processing Industry Average by Month: 83.7%

Brazil: Installed Capacity Average Utilization in Processing Industry (%)

Description Average 2012

Average 2013

2012 2013

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Processing Industry 83.9 83.7 83.6 84.4 84.9 85.4 85.2 84.8 83 83.3 83 84 84 84 84

Selected SectorsConsumer Goods 84.4 83.1 84.1 86.1 86.7 86.9 86.8 87.0 83.3 82.9 83.0 83.1 84.0 83.0 82.6Capital Goods 82.2 82.7 81.0 82.6 82.0 82.1 80.9 82.0 81.0 82.8 84.3 83.7 82.2 82.9 82.2Building Material 87.5 89.1 86.4 87.0 88.0 87.4 90.3 88.4 89.2 89.5 88.6 90.0 88.9 88.8 89.0Intemediary Goods 84.9 85.4 85.1 85.5 85.1 85.5 85.3 84.9 84.1 84.9 84.6 85.3 86.3 86.2 86.5

IndustriesMetallurgy 85.1 85.7 84.3 86.7 86.5 87.1 86.0 85.9 84.5 86.5 84.9 85.5 86.7 85.9 85.9Mechanics 82.8 83.6 83.1 81.6 81.4 82.7 82.1 81.0 81.5 82.7 85.0 83.9 83.9 83.8 84.5Electrical and Telecom 83.9 84.4 83.9 85.7 84.9 84.9 83.5 83.4 82.7 84.2 84.7 85.7 85.8 84.6 83.3Plastics 84.7 83.5 82.0 84.7 85.8 85.7 88.0 87.2 84.5 82.0 83.1 84.7 84.3 82.8 83.0Miscellaneous 80.3 80.7 78.5 77.8 80.6 82.1 81.9 83.7 81.4 79.5 80.0 80.9 80.3 81.7 81.1

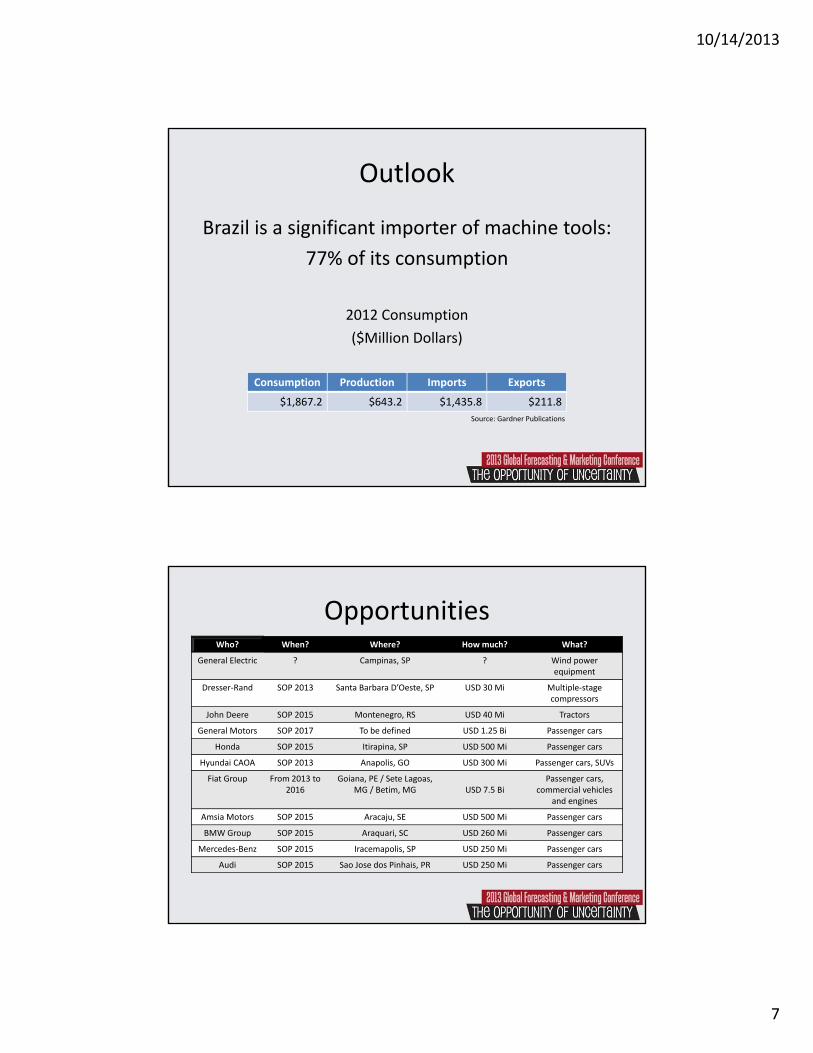

Imports by Country and Product 2012 Total Machine Tools Imports: USD 1.43 Bi

Imports over the last four quarters: USD 1.13 Bi

World’s 17th large producer of machine tools in

2012, with USD 643 Mi revenue

Machine tool production decreased 28% in

comparison to 2011

Forging, bending and stamping machines lead

machine tool imports with USD 446 Mi over the last

four quarters, followed by machining centers and

lathes that total USD 142 Mi and USD 140 Mi,

respectively.

10/14/2013

7

Outlook

Brazil is a significant importer of machine tools:

77% of its consumption

2012 Consumption

($Million Dollars)

Consumption Production Imports Exports

$1,867.2 $643.2 $1,435.8 $211.8

Source: Gardner Publications

OpportunitiesWho? When? Where? How much? What?

General Electric ? Campinas, SP ? Wind power equipment

Dresser‐Rand SOP 2013 Santa Barbara D’Oeste, SP USD 30 Mi Multiple‐stage compressors

John Deere SOP 2015 Montenegro, RS USD 40 Mi Tractors

General Motors SOP 2017 To be defined USD 1.25 Bi Passenger cars

Honda SOP 2015 Itirapina, SP USD 500 Mi Passenger cars

Hyundai CAOA SOP 2013 Anapolis, GO USD 300 Mi Passenger cars, SUVs

Fiat Group From 2013 to 2016

Goiana, PE / Sete Lagoas, MG / Betim, MG USD 7.5 Bi

Passenger cars, commercial vehicles

and engines

Amsia Motors SOP 2015 Aracaju, SE USD 500 Mi Passenger cars

BMW Group SOP 2015 Araquari, SC USD 260 Mi Passenger cars

Mercedes‐Benz SOP 2015 Iracemapolis, SP USD 250 Mi Passenger cars

Audi SOP 2015 Sao Jose dos Pinhais, PR USD 250 Mi Passenger cars

10/14/2013

8

Opportunities

Threats Closed Economy: Trade represents less than

20% of GDP, compared with 62% of Chile and

Mexico and 48% for Peru (World Bank, World

Development Indicators).

The BRL is expected to remain around BRL 2.2

per USD for the rest of 2013.

Obscure tax structure

Inflexible labor market

High tariffs (20%) & complicated

taxes (Up to 60% FOB)

Enforcement of Intellectual

Property Rights

Onerous licensing & regulatory

requirements

Lack of transparency &

bureaucracy

10/14/2013

9

Myths vs. Reality

• 5 injured in shooting at celebration

• Grocery workers days away from strike

• City leads nation in violent crime

• Workers allege nepotism at embattled state public assistance agency

• Drug raid yields man wanted in murder

• Shooting Death Prompts Looting, Rioting

• 5 injured in shooting at (Hmong) celebration (in Tulsa, OK), October 13, 2013, CNN

• Grocery workers (could be) days away from strike, October 10, 2013, King 5 TV (Seattle)

• (Tennessee) leads nation in violent crime, October 8, 2013, The Tennessean

• Workers allege nepotism at embattled state public assistance agency, October 12, 2013, Milwaukee Journal Sentinel

• Drug raid yields man wanted in (Georgia) murder, October 14, 2013, KRQE News 13 (New Mexico)

• (Kimani Gray) Shooting Death Prompts Looting, Rioting (in Brooklyn), March 14, 2013, U.S. News & World Report

Myths and Reality

“Having a direct presence in Brazil is cost prohibitive”

“Brazilian builders influence the government to

limit importation”

“Brazilians prefer European or Asian made machines”

“I can handle my sales and service for Brazil

from the United States”

“I cannot compete in the market because the costs of importation makes my prices become too high”

10/14/2013

10

Myths and Reality

With proper local support, any company can be competitive

True! But Brazilian builders are

unable to satisfy the market needs

Only if they have better after‐sales and support services.

You must be present to compete and win

Local manufacturers pay high taxes to build their

products in Brazil.

REALITY

10/14/2013

11

AMT Sao Paulo Technology Center

Located in Sorocaba, SP

Industrial city that includes various business areas of

national and multinational companies

Full access to airports and most important highways

Close to many industrial clusters (Campinas, Sao

Bernardo do Campo, Sao José dos Campos, Indaiatuba)

Close to Santos Sea Port

Diverse range of educational institutions – more than

15 universities

AMT Sao Paulo Technology Center 3 private offices;

4 high‐level, ample, and permanent

workstations;

6 additional ad‐hoc workstations;

Conference room with space for 6 people, and

another with capacity of 12 people;

75‐person conference area at the Federation of

Industry Building next door to the Centre;

The partnership with an engineering school

ensured a room to promote conferences for

more than 120 people.

10/14/2013

12

Manufacturing Technology Room 872 ft² available for active members at AMT

Brazil

Display room for tools, small equipment and

products promoting technologies provided by

members;

Space for impromptu meetings;

Target audience: industry, students, professors,

investors and other organizations interested in

advanced manufacturing technologies;

Location for focused events featuring a different

technology each month.

10/14/2013

13

Custom Brokerage / Temporary

Import Program Management

Customized Marketing and Sales Planning

HR Selection and Recruitment / Proxy‐Hiring Program

Import‐Export & Logistics

Start‐up and Operation Guidance

Market Intelligence and Competitor Analysis

Installation, Setup,

Troubleshooting and After Sales

Support

Market Penetration / Distribution Channel

Streamlining

Distributors Search

Office and Exhibit Space

Customer Lists and Contacts

Networking

AMT Sao Paulo Technology Center

AMT Sao Paulo Technology Center Enables you to get to the market fast, while we

provide you with the ideal environment for you to be

successful in the Brazilian market

Allows you to establish instant relationships and

networking opportunitieswhile we take care of the

details from behind the scenes

Guides you in dealingwith a complex, bureaucratic

system

Mitigates the risks due to unfamiliarity with local

business practices

Grants you resources and capabilities developed with

you and your customers’ particular needs in mind

10/14/2013

14