brazilian rates’ bull market is not over - banco itaú · demographic scenario. ... •...

TRANSCRIPT

Brazilian rates’ bull market is not over

LatAm Fixed Income Strategy Monthly March 17, 2017

Please refer to page 22 of this report for important disclosures, analyst certifications and additional information. Itaú BBA does and seeks to do business with Companies covered in this research report. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the sole factor in making their investment decision.

Itaú Corretora de Valores S.A. is the securities arm of Itaú Unibanco Group. Itaú BBA is a registered mark used by Itaú Corretora de Valores S.A.

Highlights

The noisy domestic news flow prompted some players to take profits

in Brazilian rates.

Despite this short-term volatility, we retain a constructive view on

Brazilian fundamentals and see potential for further compression in

nominal rates.

We have been emphasizing that BCB was open to the idea of

accelerating the easing pace…

…and the February IPCA reinforced the sharply-falling trend in

inflation.

Likewise, the latest Focus survey showed a hefty downward revision

in the consensual expectation for inflation this year, which is now

closer to our forecast.

Given the Central Bank’s signaling of possible intensification in

frontloading the easing cycle, the disinflationary scenario and the

decline in expectations, we changed our Selic call on March 14.

We now expect two cuts of 100bps (in April and May), two cuts of

75bps (in July and September), and one cut of 50bps (in October).

In the Box, we show that interest rate derivatives price in an

acceleration of BCB’s rate cut cycle. The probability attributed to our

baseline rose after the Fed’s dovish hike and Moody’s outlook

upgrade.

STRATEGY TEAM Ciro Matuo, CNPI [email protected]

Eduardo Marza [email protected]

Contents

1) Currencies p.

- Brazilian Real 3

- Mexican Peso 4

- Chilean Peso 5

- Colombian Peso 6

Box: Disinflation and the Fed give

BCB the leeway to accelerate 6

2) Rates

- Brazil Rates 9

- Non Brazil Rates 12

3) Appendix 16

Page 2

Latam Fixed Income Strategy Monthly – March 17, 2017

1) Currencies For a thorough macroeconomic discussion, see LatAm Macro Monthly – Positive global environment, but for how long?, March 10.

Overview

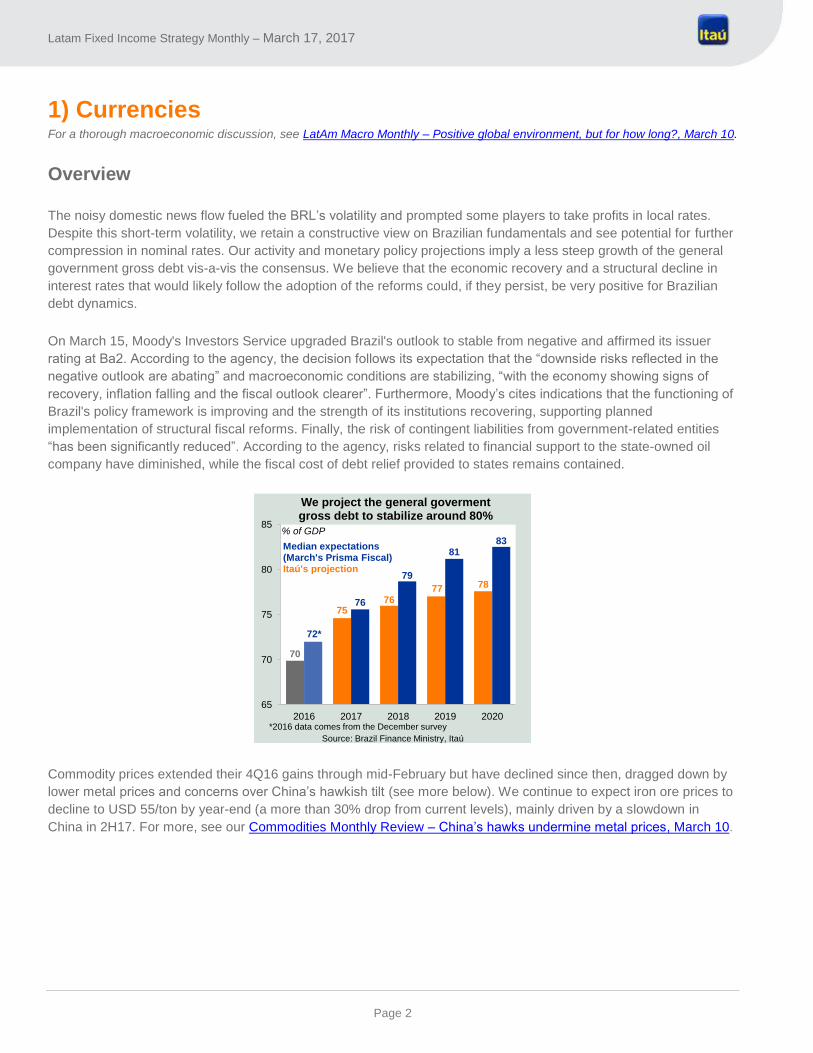

The noisy domestic news flow fueled the BRL’s volatility and prompted some players to take profits in local rates.

Despite this short-term volatility, we retain a constructive view on Brazilian fundamentals and see potential for further

compression in nominal rates. Our activity and monetary policy projections imply a less steep growth of the general

government gross debt vis-a-vis the consensus. We believe that the economic recovery and a structural decline in

interest rates that would likely follow the adoption of the reforms could, if they persist, be very positive for Brazilian

debt dynamics.

On March 15, Moody's Investors Service upgraded Brazil's outlook to stable from negative and affirmed its issuer

rating at Ba2. According to the agency, the decision follows its expectation that the “downside risks reflected in the

negative outlook are abating” and macroeconomic conditions are stabilizing, “with the economy showing signs of

recovery, inflation falling and the fiscal outlook clearer”. Furthermore, Moody’s cites indications that the functioning of

Brazil's policy framework is improving and the strength of its institutions recovering, supporting planned

implementation of structural fiscal reforms. Finally, the risk of contingent liabilities from government-related entities

“has been significantly reduced”. According to the agency, risks related to financial support to the state-owned oil

company have diminished, while the fiscal cost of debt relief provided to states remains contained.

Commodity prices extended their 4Q16 gains through mid-February but have declined since then, dragged down by

lower metal prices and concerns over China’s hawkish tilt (see more below). We continue to expect iron ore prices to

decline to USD 55/ton by year-end (a more than 30% drop from current levels), mainly driven by a slowdown in

China in 2H17. For more, see our Commodities Monthly Review – China’s hawks undermine metal prices, March 10.

70

7576

77 78

72*

76

79

8183

65

70

75

80

85

2016 2017 2018 2019 2020

We project the general goverment gross debt to stabilize around 80%

Source: Brazil Finance Ministry, Itaú

Median expectations (March's Prisma Fiscal)Itaú's projection

% of GDP

*2016 data comes from the December survey

Page 3

Latam Fixed Income Strategy Monthly – March 17, 2017

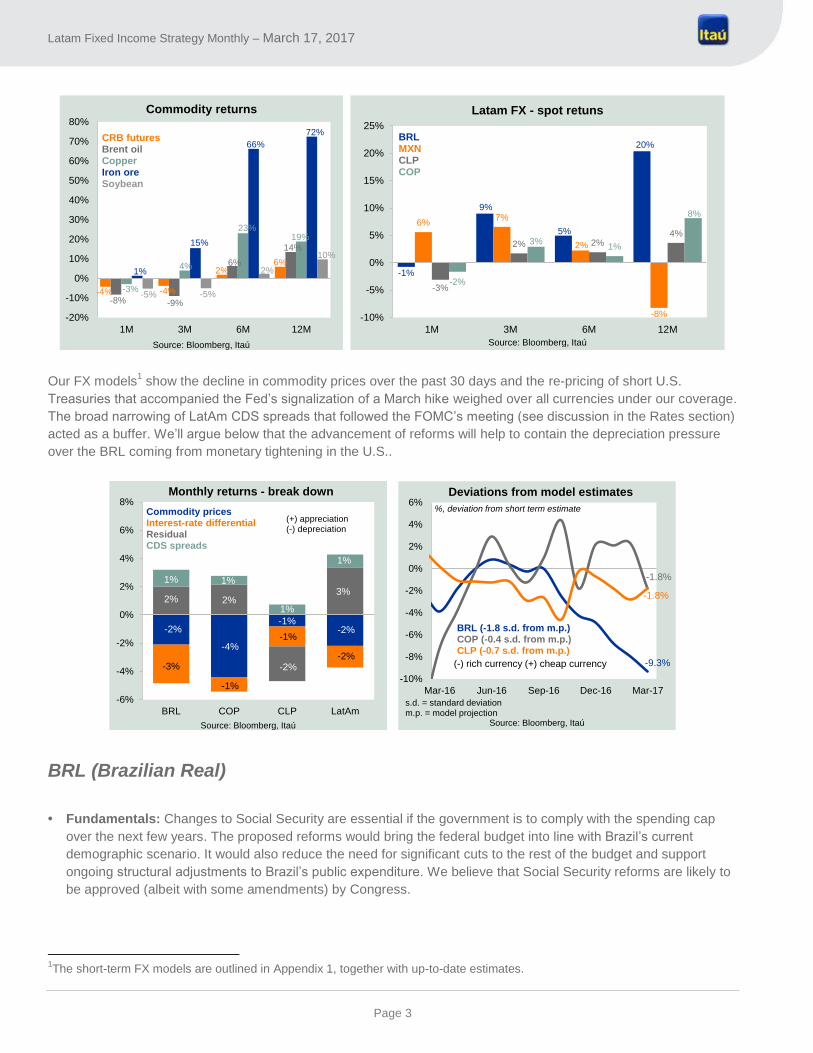

Our FX models1 show the decline in commodity prices over the past 30 days and the re-pricing of short U.S.

Treasuries that accompanied the Fed’s signalization of a March hike weighed over all currencies under our coverage.

The broad narrowing of LatAm CDS spreads that followed the FOMC’s meeting (see discussion in the Rates section)

acted as a buffer. We’ll argue below that the advancement of reforms will help to contain the depreciation pressure

over the BRL coming from monetary tightening in the U.S..

BRL (Brazilian Real)

• Fundamentals: Changes to Social Security are essential if the government is to comply with the spending cap

over the next few years. The proposed reforms would bring the federal budget into line with Brazil’s current

demographic scenario. It would also reduce the need for significant cuts to the rest of the budget and support

ongoing structural adjustments to Brazil’s public expenditure. We believe that Social Security reforms are likely to

be approved (albeit with some amendments) by Congress.

1The short-term FX models are outlined in Appendix 1, together with up-to-date estimates.

-4% -4%

2%6%

-8% -9%

6%

14%

-3%

4%

23%19%

1%

15%

66%

72%

-5% -5%

2%

10%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

1M 3M 6M 12M

Commodity returns

Source: Bloomberg, Itaú

CRB futuresBrent oilCopperIron oreSoybean

-1%

9%

5%

20%

6%7%

2%

-8%

-3%

2% 2%4%

-2%

3%1%

8%

-10%

-5%

0%

5%

10%

15%

20%

25%

1M 3M 6M 12M

Latam FX - spot retuns

Source: Bloomberg, Itaú

BRLMXNCLPCOP

-2%

-4%

-1%-2%

-3%

-1%

-1%

-2%

2% 2%

-2%

3%

1% 1%

1%

1%

-6%

-4%

-2%

0%

2%

4%

6%

8%

BRL COP CLP LatAm

Monthly returns - break down

Source: Bloomberg, Itaú

(+) appreciation(-) depreciation

Commodity pricesInterest-rate differentialResidualCDS spreads

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

Deviations from model estimates

Source: Bloomberg, Itaú

%, deviation from short term estimate

(+) cheap currency (-) rich currency

BRL (-1.8 s.d. from m.p.)COP (-0.4 s.d. from m.p.)CLP (-0.7 s.d. from m.p.)

s.d. = standard deviationm.p. = model projection

-9.3%

-1.8%

-1.8%

Page 4

Latam Fixed Income Strategy Monthly – March 17, 2017

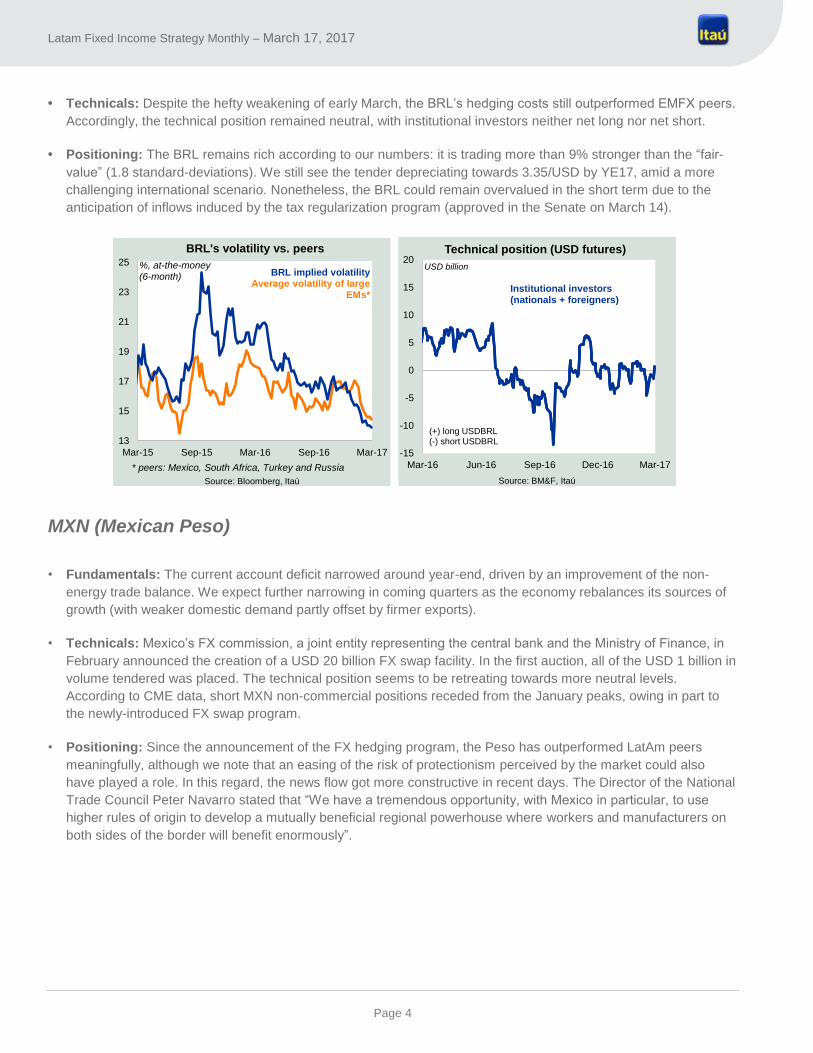

• Technicals: Despite the hefty weakening of early March, the BRL’s hedging costs still outperformed EMFX peers.

Accordingly, the technical position remained neutral, with institutional investors neither net long nor net short.

• Positioning: The BRL remains rich according to our numbers: it is trading more than 9% stronger than the “fair-

value” (1.8 standard-deviations). We still see the tender depreciating towards 3.35/USD by YE17, amid a more

challenging international scenario. Nonetheless, the BRL could remain overvalued in the short term due to the

anticipation of inflows induced by the tax regularization program (approved in the Senate on March 14).

MXN (Mexican Peso)

• Fundamentals: The current account deficit narrowed around year-end, driven by an improvement of the non-

energy trade balance. We expect further narrowing in coming quarters as the economy rebalances its sources of

growth (with weaker domestic demand partly offset by firmer exports).

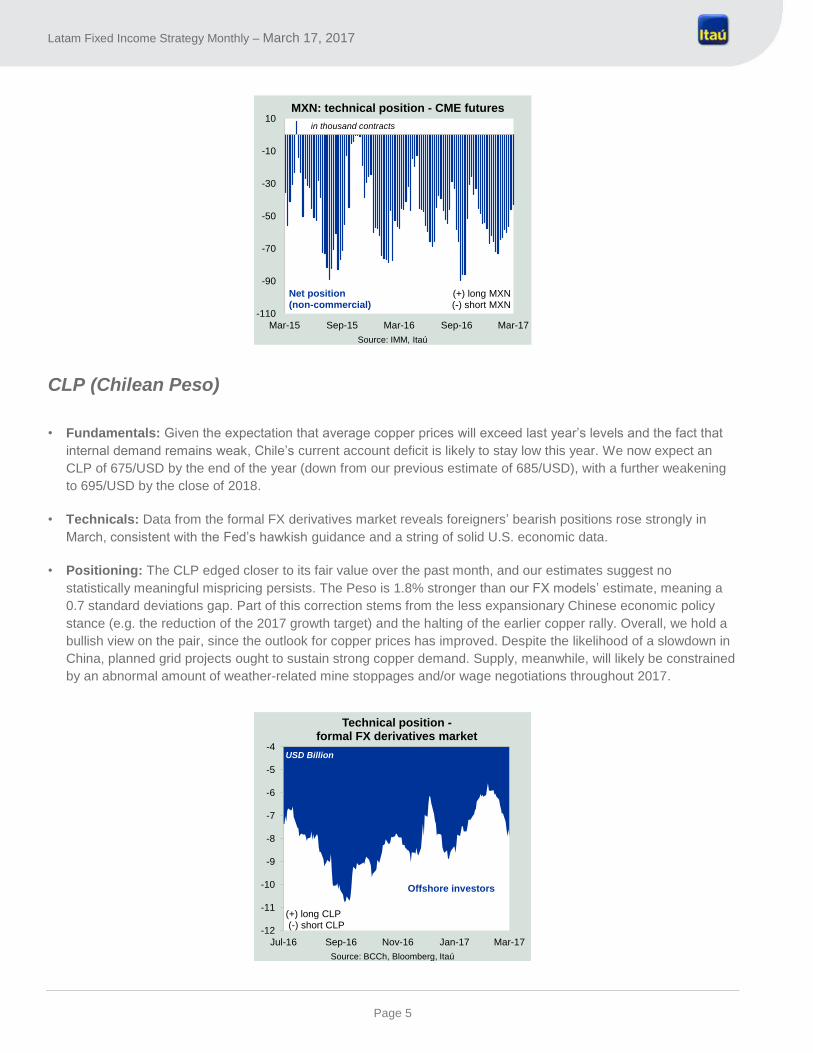

• Technicals: Mexico’s FX commission, a joint entity representing the central bank and the Ministry of Finance, in

February announced the creation of a USD 20 billion FX swap facility. In the first auction, all of the USD 1 billion in

volume tendered was placed. The technical position seems to be retreating towards more neutral levels.

According to CME data, short MXN non-commercial positions receded from the January peaks, owing in part to

the newly-introduced FX swap program.

• Positioning: Since the announcement of the FX hedging program, the Peso has outperformed LatAm peers

meaningfully, although we note that an easing of the risk of protectionism perceived by the market could also

have played a role. In this regard, the news flow got more constructive in recent days. The Director of the National

Trade Council Peter Navarro stated that “We have a tremendous opportunity, with Mexico in particular, to use

higher rules of origin to develop a mutually beneficial regional powerhouse where workers and manufacturers on

both sides of the border will benefit enormously”.

13

15

17

19

21

23

25

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

BRL's volatility vs. peers

Source: Bloomberg, Itaú

BRL implied volatility Average volatility of large

EMs*

%, at-the-money(6-month)

* peers: Mexico, South Africa, Turkey and Russia

-15

-10

-5

0

5

10

15

20

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

Technical position (USD futures)

Institutional investors (nationals + foreigners)

USD billion

(+) long USDBRL(-) short USDBRL

Source: BM&F, Itaú

Page 5

Latam Fixed Income Strategy Monthly – March 17, 2017

CLP (Chilean Peso)

• Fundamentals: Given the expectation that average copper prices will exceed last year’s levels and the fact that

internal demand remains weak, Chile’s current account deficit is likely to stay low this year. We now expect an

CLP of 675/USD by the end of the year (down from our previous estimate of 685/USD), with a further weakening

to 695/USD by the close of 2018.

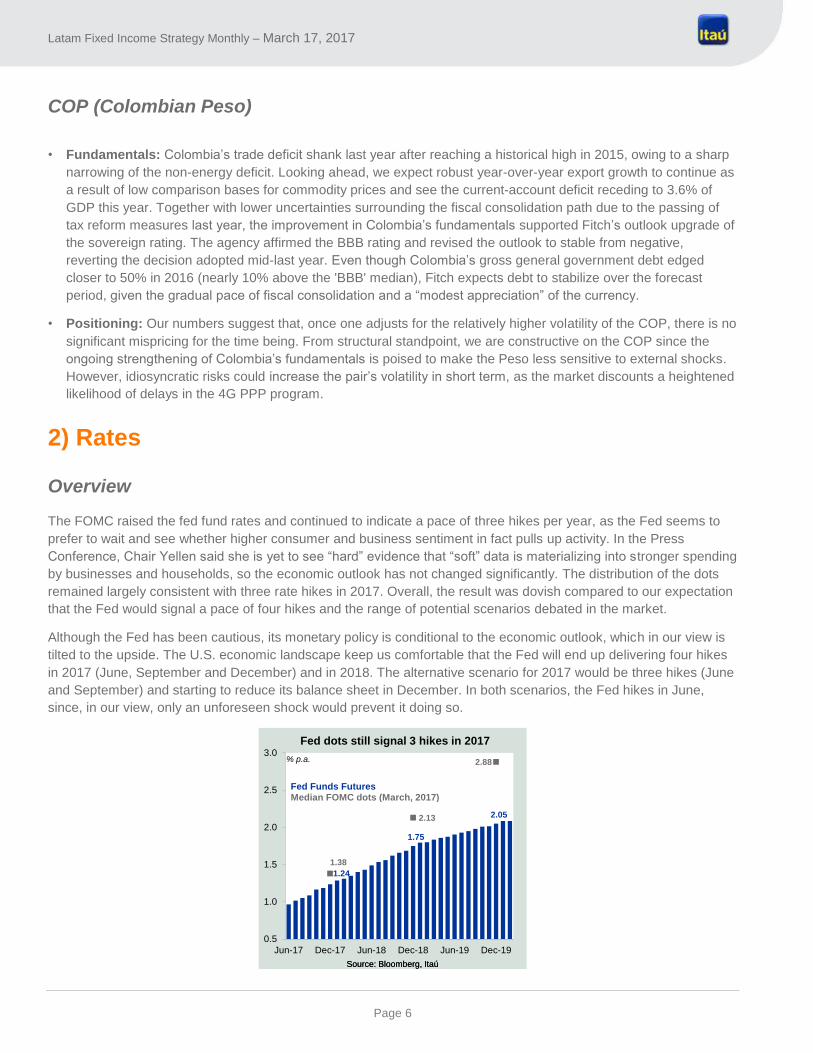

• Technicals: Data from the formal FX derivatives market reveals foreigners’ bearish positions rose strongly in

March, consistent with the Fed’s hawkish guidance and a string of solid U.S. economic data.

• Positioning: The CLP edged closer to its fair value over the past month, and our estimates suggest no

statistically meaningful mispricing persists. The Peso is 1.8% stronger than our FX models’ estimate, meaning a

0.7 standard deviations gap. Part of this correction stems from the less expansionary Chinese economic policy

stance (e.g. the reduction of the 2017 growth target) and the halting of the earlier copper rally. Overall, we hold a

bullish view on the pair, since the outlook for copper prices has improved. Despite the likelihood of a slowdown in

China, planned grid projects ought to sustain strong copper demand. Supply, meanwhile, will likely be constrained

by an abnormal amount of weather-related mine stoppages and/or wage negotiations throughout 2017.

-110

-90

-70

-50

-30

-10

10

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

MXN: technical position - CME futures

Source: IMM, Itaú

Net position (non-commercial)

in thousand contracts

(+) long MXN (-) short MXN

-12

-11

-10

-9

-8

-7

-6

-5

-4

Jul-16 Sep-16 Nov-16 Jan-17 Mar-17

Technical position -formal FX derivatives market

Source: BCCh, Bloomberg, Itaú

Offshore investors

USD Billion

(+) long CLP (-) short CLP

Page 6

Latam Fixed Income Strategy Monthly – March 17, 2017

COP (Colombian Peso)

• Fundamentals: Colombia’s trade deficit shank last year after reaching a historical high in 2015, owing to a sharp

narrowing of the non-energy deficit. Looking ahead, we expect robust year-over-year export growth to continue as

a result of low comparison bases for commodity prices and see the current-account deficit receding to 3.6% of

GDP this year. Together with lower uncertainties surrounding the fiscal consolidation path due to the passing of

tax reform measures last year, the improvement in Colombia’s fundamentals supported Fitch’s outlook upgrade of

the sovereign rating. The agency affirmed the BBB rating and revised the outlook to stable from negative,

reverting the decision adopted mid-last year. Even though Colombia’s gross general government debt edged

closer to 50% in 2016 (nearly 10% above the 'BBB' median), Fitch expects debt to stabilize over the forecast

period, given the gradual pace of fiscal consolidation and a “modest appreciation” of the currency.

• Positioning: Our numbers suggest that, once one adjusts for the relatively higher volatility of the COP, there is no

significant mispricing for the time being. From structural standpoint, we are constructive on the COP since the

ongoing strengthening of Colombia’s fundamentals is poised to make the Peso less sensitive to external shocks.

However, idiosyncratic risks could increase the pair’s volatility in short term, as the market discounts a heightened

likelihood of delays in the 4G PPP program.

2) Rates

Overview

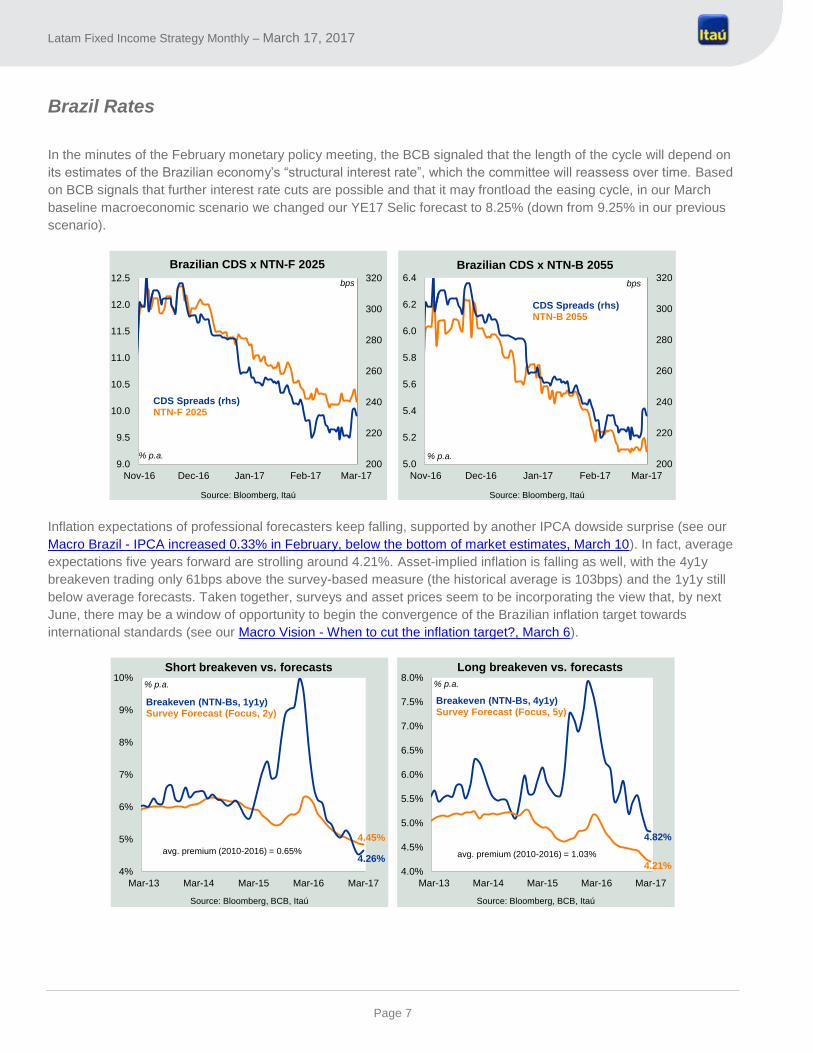

The FOMC raised the fed fund rates and continued to indicate a pace of three hikes per year, as the Fed seems to

prefer to wait and see whether higher consumer and business sentiment in fact pulls up activity. In the Press

Conference, Chair Yellen said she is yet to see “hard” evidence that “soft” data is materializing into stronger spending

by businesses and households, so the economic outlook has not changed significantly. The distribution of the dots

remained largely consistent with three rate hikes in 2017. Overall, the result was dovish compared to our expectation

that the Fed would signal a pace of four hikes and the range of potential scenarios debated in the market.

Although the Fed has been cautious, its monetary policy is conditional to the economic outlook, which in our view is

tilted to the upside. The U.S. economic landscape keep us comfortable that the Fed will end up delivering four hikes

in 2017 (June, September and December) and in 2018. The alternative scenario for 2017 would be three hikes (June

and September) and starting to reduce its balance sheet in December. In both scenarios, the Fed hikes in June,

since, in our view, only an unforeseen shock would prevent it doing so.

1.24

1.75

2.05

1.38

2.13

2.88

0.5

1.0

1.5

2.0

2.5

3.0

Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19

Fed dots still signal 3 hikes in 2017

Source: Bloomberg, Itaú

Fed Funds FuturesMedian FOMC dots (March, 2017)

% p.a.

Source: Bloomberg, Itaú

Page 7

Latam Fixed Income Strategy Monthly – March 17, 2017

Brazil Rates

In the minutes of the February monetary policy meeting, the BCB signaled that the length of the cycle will depend on

its estimates of the Brazilian economy’s “structural interest rate”, which the committee will reassess over time. Based

on BCB signals that further interest rate cuts are possible and that it may frontload the easing cycle, in our March

baseline macroeconomic scenario we changed our YE17 Selic forecast to 8.25% (down from 9.25% in our previous

scenario).

Inflation expectations of professional forecasters keep falling, supported by another IPCA dowside surprise (see our

Macro Brazil - IPCA increased 0.33% in February, below the bottom of market estimates, March 10). In fact, average

expectations five years forward are strolling around 4.21%. Asset-implied inflation is falling as well, with the 4y1y

breakeven trading only 61bps above the survey-based measure (the historical average is 103bps) and the 1y1y still

below average forecasts. Taken together, surveys and asset prices seem to be incorporating the view that, by next

June, there may be a window of opportunity to begin the convergence of the Brazilian inflation target towards

international standards (see our Macro Vision - When to cut the inflation target?, March 6).

200

220

240

260

280

300

320

9.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

Brazilian CDS x NTN-F 2025

% p.a.

bps

CDS Spreads (rhs)NTN-F 2025

Source: Bloomberg, Itaú

200

220

240

260

280

300

320

5.0

5.2

5.4

5.6

5.8

6.0

6.2

6.4

Nov-16 Dec-16 Jan-17 Feb-17 Mar-17

Brazilian CDS x NTN-B 2055

% p.a.

bps

CDS Spreads (rhs)NTN-B 2055

Source: Bloomberg, Itaú

4.45%

4.26%

4%

5%

6%

7%

8%

9%

10%

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

Short breakeven vs. forecasts

Source: Bloomberg, BCB, Itaú

Breakeven (NTN-Bs, 1y1y)Survey Forecast (Focus, 2y)

% p.a.

avg. premium (2010-2016) = 0.65%

4.82%

4.21%4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

Long breakeven vs. forecasts

Source: Bloomberg, BCB, Itaú

Breakeven (NTN-Bs, 4y1y)Survey Forecast (Focus, 5y)

% p.a.

avg. premium (2010-2016) = 1.03%

Page 8

Latam Fixed Income Strategy Monthly – March 17, 2017

The front end pricing is no longer consistent with our macroeconomic baseline. In fact, even after removing our

historical term premium estimate, the curve implies only 330bps of cuts for 2017, whereas we see the BCB reducing

the Selic rate by 400bps this year. Given the Central Bank’s signaling of possible intensification in frontloading the

easing cycle, the disinflationary scenario and the decline in expectations, we now expect two cuts of 100 bps (in April

and May), two cuts of 75 bps (in July and September), and one cut of 50 bps (in October). The risks to this forecast

are the same that we envisage for the inflation path and seem symmetric2. In contrast to the front end, the back end

valuation changed little over the past month. The 5y5y forwards are trading around 10.7% - fairly close to our “fair

value” estimate3, which is currently around 10.2%.

2 For a thorough discussion, we refer to our Macro Brazil - Lower expectations, faster pace - March 14.

3 This estimate assumes the real U.S. terminal rate is 1.0%, the steady-state inflation is 4.5% and uses 10-year CDS spreads

(310bps) as the country risk proxy. Together with our term premium estimate, we arrive at an upper bound of 10.4%.

-290

-332

-18

-305

-29

-350

-300

-250

-200

-150

-100

-50

0

2017YE 2018YE

DI Futures: implicit rate hikes by...

Source: Bloomberg, BCB, Itaú

Unadjusted for TP*Adjusted for TP*

Analysts' consensusbps

* TP = Term-premium

1.0%

3.1%

4.5%

1.6%

10.7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Brazil

Fair value for long term rates - Brazil

Source: Bloomberg, Itaú

Total:10.2%

p.a. U.S. real terminal rateCDS spread (10-year)

Domestic inflation targetTerm premium

Forward rate (5y5y)

Page 9

Latam Fixed Income Strategy Monthly – March 17, 2017

Box: Disinflation and the Fed give BCB the leeway to accelerate

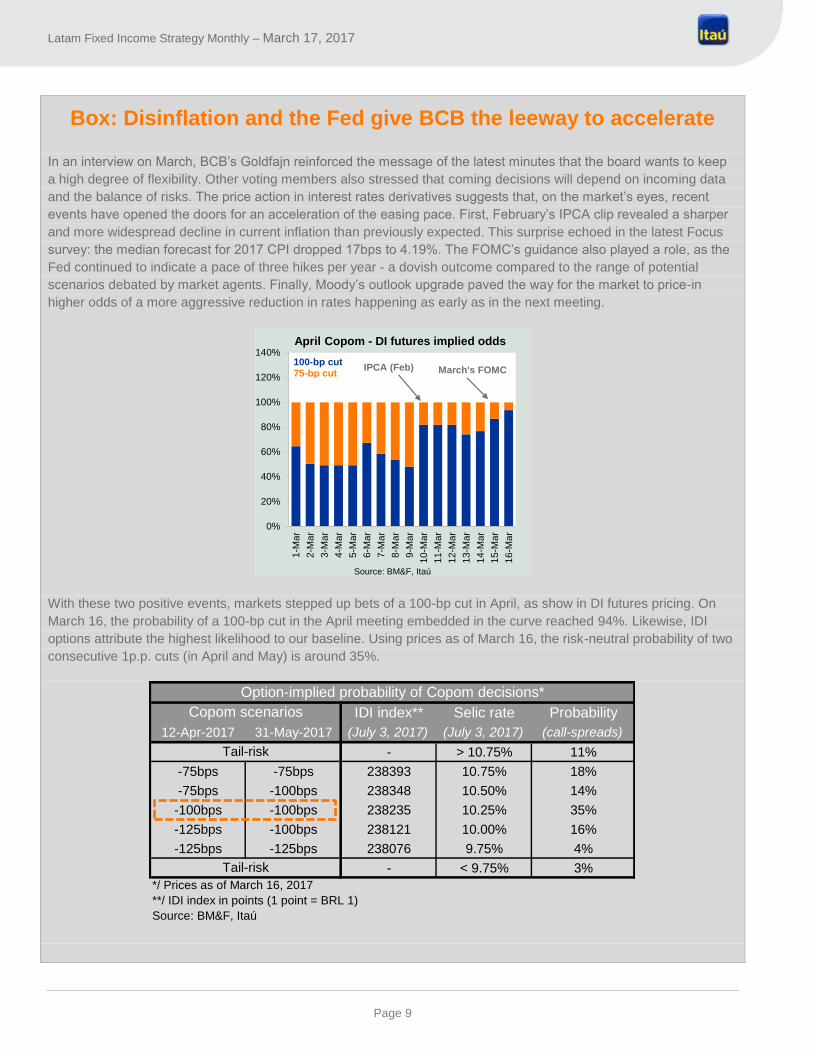

In an interview on March, BCB’s Goldfajn reinforced the message of the latest minutes that the board wants to keep

a high degree of flexibility. Other voting members also stressed that coming decisions will depend on incoming data

and the balance of risks. The price action in interest rates derivatives suggests that, on the market’s eyes, recent

events have opened the doors for an acceleration of the easing pace. First, February’s IPCA clip revealed a sharper

and more widespread decline in current inflation than previously expected. This surprise echoed in the latest Focus

survey: the median forecast for 2017 CPI dropped 17bps to 4.19%. The FOMC’s guidance also played a role, as the

Fed continued to indicate a pace of three hikes per year - a dovish outcome compared to the range of potential

scenarios debated by market agents. Finally, Moody’s outlook upgrade paved the way for the market to price-in

higher odds of a more aggressive reduction in rates happening as early as in the next meeting.

With these two positive events, markets stepped up bets of a 100-bp cut in April, as show in DI futures pricing. On

March 16, the probability of a 100-bp cut in the April meeting embedded in the curve reached 94%. Likewise, IDI

options attribute the highest likelihood to our baseline. Using prices as of March 16, the risk-neutral probability of two

consecutive 1p.p. cuts (in April and May) is around 35%.

0%

20%

40%

60%

80%

100%

120%

140%

1-M

ar

2-M

ar

3-M

ar

4-M

ar

5-M

ar

6-M

ar

7-M

ar

8-M

ar

9-M

ar

10

-Mar

11

-Mar

12

-Mar

13

-Mar

14

-Mar

15

-Mar

16

-Mar

April Copom - DI futures implied odds

Source: BM&F, Itaú

100-bp cut75-bp cut

IPCA (Feb) March's FOMC

IDI index** Selic rate Probability

12-Apr-2017 31-May-2017 (July 3, 2017) (July 3, 2017) (call-spreads)

- > 10.75% 11%

-75bps -75bps 238393 10.75% 18%

-75bps -100bps 238348 10.50% 14%

-100bps -100bps 238235 10.25% 35%

-125bps -100bps 238121 10.00% 16%

-125bps -125bps 238076 9.75% 4%

- < 9.75% 3%

*/ Prices as of March 16, 2017

**/ IDI index in points (1 point = BRL 1)

Source: BM&F, Itaú

Copom scenarios

Tail-risk

Tail-risk

Option-implied probability of Copom decisions*

Page 10

Latam Fixed Income Strategy Monthly – March 17, 2017

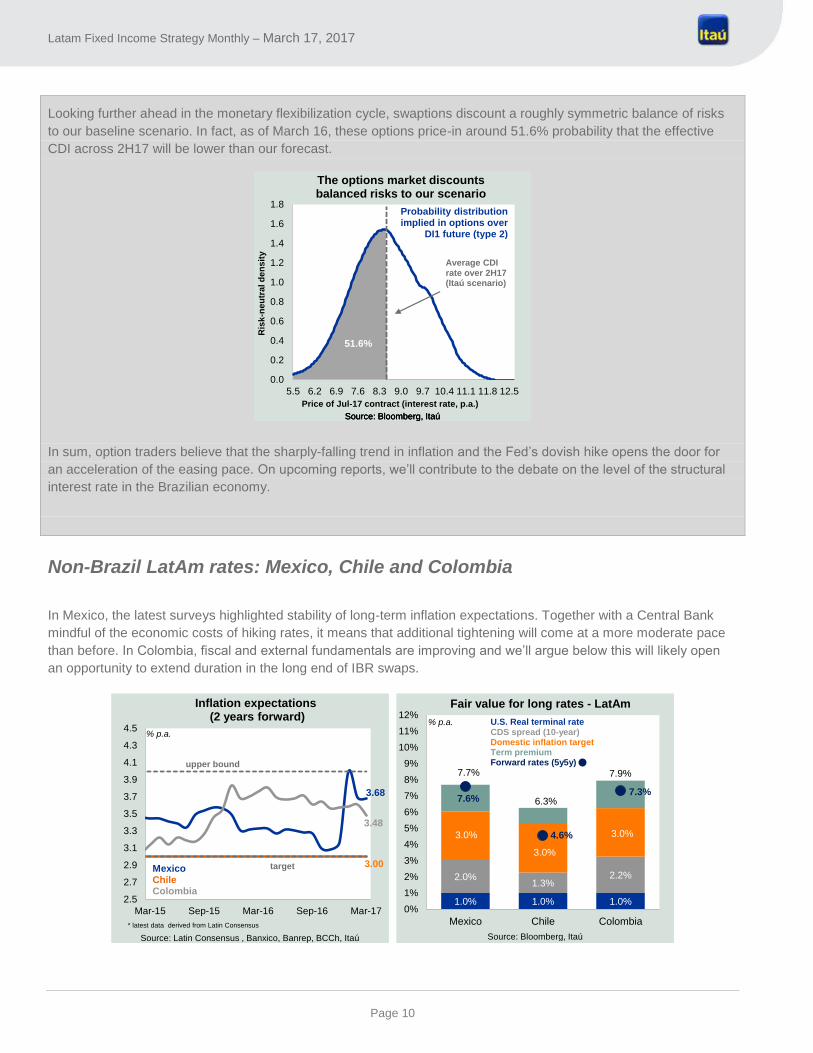

Looking further ahead in the monetary flexibilization cycle, swaptions discount a roughly symmetric balance of risks

to our baseline scenario. In fact, as of March 16, these options price-in around 51.6% probability that the effective

CDI across 2H17 will be lower than our forecast.

In sum, option traders believe that the sharply-falling trend in inflation and the Fed’s dovish hike opens the door for

an acceleration of the easing pace. On upcoming reports, we’ll contribute to the debate on the level of the structural

interest rate in the Brazilian economy.

Non-Brazil LatAm rates: Mexico, Chile and Colombia

In Mexico, the latest surveys highlighted stability of long-term inflation expectations. Together with a Central Bank

mindful of the economic costs of hiking rates, it means that additional tightening will come at a more moderate pace

than before. In Colombia, fiscal and external fundamentals are improving and we’ll argue below this will likely open

an opportunity to extend duration in the long end of IBR swaps.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

5.5 6.2 6.9 7.6 8.3 9.0 9.7 10.4 11.1 11.8 12.5

Ris

k-n

eu

tra

l d

en

sit

y

Price of Jul-17 contract (interest rate, p.a.)

The options market discounts balanced risks to our scenario

Source: Bloomberg, Itaú

Probability distributionimplied in options over

DI1 future (type 2)

Source: Bloomberg, Itaú

Average CDI rate over 2H17 (Itaú scenario)

Source: Bloomberg, Itaú

51.6%

3.68

3.00

3.48

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

4.1

4.3

4.5

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

Inflation expectations(2 years forward)

Source: Latin Consensus , Banxico, Banrep, BCCh, Itaú

% p.a.

MexicoChile Colombia

upper bound

target

* latest data derived from Latin Consensus

1.0% 1.0% 1.0%

2.0%1.3%

2.2%

3.0%

3.0%

3.0%

1.7%

1.0%

7.6%

4.6%

7.3%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

Mexico Chile Colombia

Fair value for long rates - LatAm

Source: Bloomberg, Itaú

U.S. Real terminal rateCDS spread (10-year)Domestic inflation targetTerm premiumForward rates (5y5y)

% p.a.

7.7%

6.3%

7.9%

Page 11

Latam Fixed Income Strategy Monthly – March 17, 2017

MEXICO

Banxico continues to focus on potential second-round effects of higher gasoline prices and the MXN depreciation -

namely a “further increase of inflation expectations”, as stated in the latest inflation report. However, the central bank

now highlights its view that hiking rates to fight short-term inflation shocks can be “inefficient and costly in terms of

economic activity”. We see the next Banxico hike coming by the end of March and expect it to take the reference rate

to 7.0% by YE17, through three 25-bp rate hikes that follow respective moves of the same magnitude by the Fed in

the near-term. The curve implies 50bps in hikes this year, after controlling for the term premium.

The near-perfect correlation of Mexican yields with the MXN observed in the beginning of the year has subsided after

the implementation of the FX hedging program. For the 1-year tenor, the correlation dropped to roughly 0.3, whereas

for longer-dated rates it is still high. Likewise, breakevens receded from the historical high reached after the early-

January inflationary shocks. Given our view that the government will deliver its fiscal targets for 2017 – thus

potentially averting a sovereign downgrade – and the ongoing adjustment in Mexico’s external fundamentals, we

believe the case for extending duration in Mexican yields have strengthened. Notwithstanding the recent correction,

implied inflation is still too-high relative to our baseline scenario. Moreover, the measures announced by the

exchange rate commission will likely lead to less-aggressive monetary tightening.

5.25%

5.75%

6.25%

6.75%

7.25%

7.75%

Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Sep-19 Mar-20

Forward curve pricing (TIIE swaps) vs. analysts' projections

Source: Bloomberg, Latin Consensus, Itaú

% p.a.

* TP = Term-premium (historical)

Market pricingMarket pricing (ex-TP*)Itaú forecastConsensus forecast

70

5

54

-16

95

85

-30

-10

10

30

50

70

90

110

2017YE 2018YE

TIIE swaps: implicit rate hikes by...

bps

* TP = Term-premium

Unadjusted for TP*Adjusted for TP*Analysts' consensus

Source: Bloomberg, Latin Consensus, Itaú

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Mar-16 May-16 Jul-16 Sep-16 Nov-16 Jan-17 Mar-17

Rates-FX correlation in Mexico

Source: Bloomberg, Itaú

Correlation coefficient (100 days)

1Y TIIE Swap2Y TIIE Swap5Y TIIE Swap

10Y TIIE Swap

critical level

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Mar-14 Sep-14 Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

Mexican breakeven inflation

Source: Bloomberg, Itaú

2-year5-year

% p.a., 30-day moving average

lower bound

upper bound

target

Page 12

Latam Fixed Income Strategy Monthly – March 17, 2017

CHILE

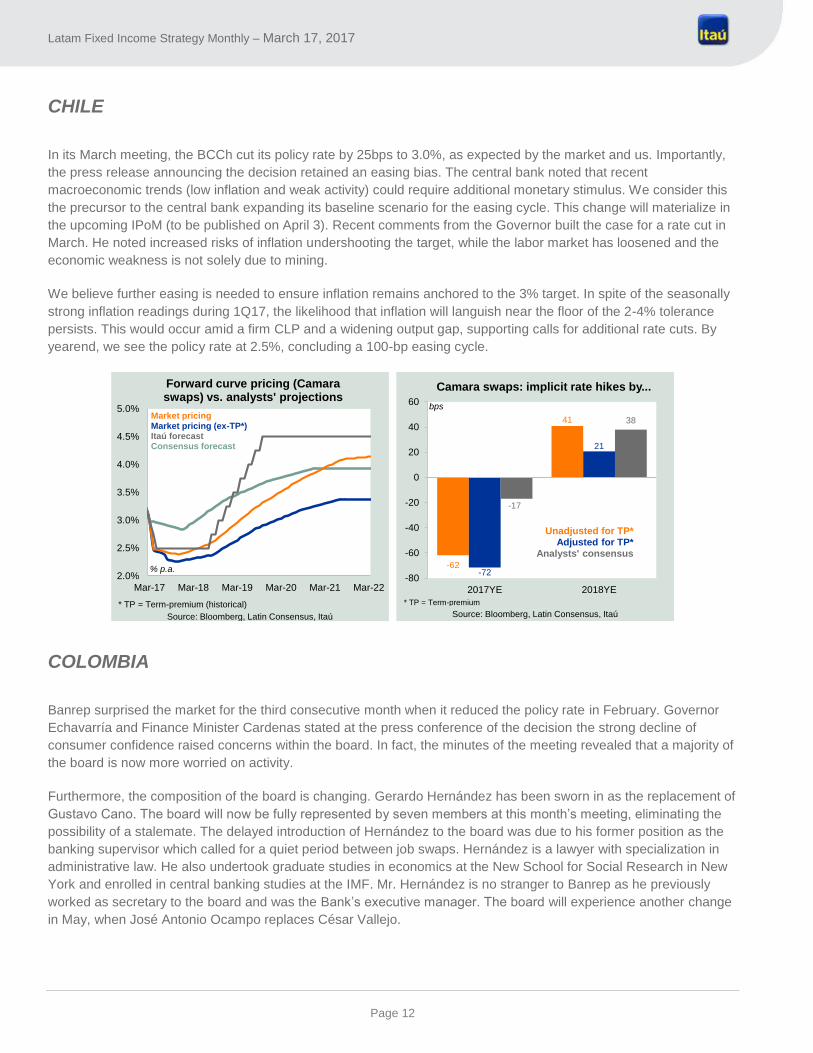

In its March meeting, the BCCh cut its policy rate by 25bps to 3.0%, as expected by the market and us. Importantly,

the press release announcing the decision retained an easing bias. The central bank noted that recent

macroeconomic trends (low inflation and weak activity) could require additional monetary stimulus. We consider this

the precursor to the central bank expanding its baseline scenario for the easing cycle. This change will materialize in

the upcoming IPoM (to be published on April 3). Recent comments from the Governor built the case for a rate cut in

March. He noted increased risks of inflation undershooting the target, while the labor market has loosened and the

economic weakness is not solely due to mining.

We believe further easing is needed to ensure inflation remains anchored to the 3% target. In spite of the seasonally

strong inflation readings during 1Q17, the likelihood that inflation will languish near the floor of the 2-4% tolerance

persists. This would occur amid a firm CLP and a widening output gap, supporting calls for additional rate cuts. By

yearend, we see the policy rate at 2.5%, concluding a 100-bp easing cycle.

COLOMBIA

Banrep surprised the market for the third consecutive month when it reduced the policy rate in February. Governor

Echavarría and Finance Minister Cardenas stated at the press conference of the decision the strong decline of

consumer confidence raised concerns within the board. In fact, the minutes of the meeting revealed that a majority of

the board is now more worried on activity.

Furthermore, the composition of the board is changing. Gerardo Hernández has been sworn in as the replacement of

Gustavo Cano. The board will now be fully represented by seven members at this month’s meeting, eliminating the

possibility of a stalemate. The delayed introduction of Hernández to the board was due to his former position as the

banking supervisor which called for a quiet period between job swaps. Hernández is a lawyer with specialization in

administrative law. He also undertook graduate studies in economics at the New School for Social Research in New

York and enrolled in central banking studies at the IMF. Mr. Hernández is no stranger to Banrep as he previously

worked as secretary to the board and was the Bank’s executive manager. The board will experience another change

in May, when José Antonio Ocampo replaces César Vallejo.

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 Mar-22

Forward curve pricing (Camara swaps) vs. analysts' projections

Source: Bloomberg, Latin Consensus, Itaú

% p.a.

* TP = Term-premium (historical)

Market pricingMarket pricing (ex-TP*)Itaú forecastConsensus forecast

-62

41

-72

21

-17

38

-80

-60

-40

-20

0

20

40

60

2017YE 2018YE

Camara swaps: implicit rate hikes by...

Source: Bloomberg, Latin Consensus, Itaú

bps

* TP = Term-premium

Unadjusted for TP*Adjusted for TP*

Analysts' consensus

Page 13

Latam Fixed Income Strategy Monthly – March 17, 2017

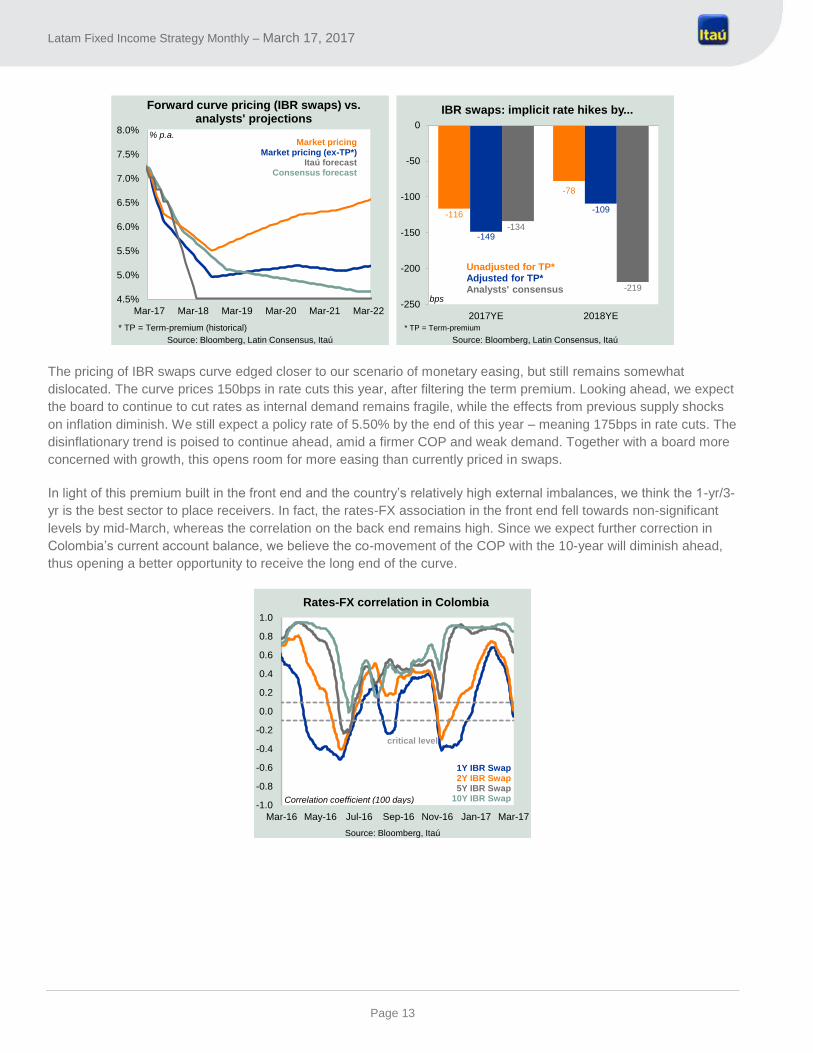

The pricing of IBR swaps curve edged closer to our scenario of monetary easing, but still remains somewhat

dislocated. The curve prices 150bps in rate cuts this year, after filtering the term premium. Looking ahead, we expect

the board to continue to cut rates as internal demand remains fragile, while the effects from previous supply shocks

on inflation diminish. We still expect a policy rate of 5.50% by the end of this year – meaning 175bps in rate cuts. The

disinflationary trend is poised to continue ahead, amid a firmer COP and weak demand. Together with a board more

concerned with growth, this opens room for more easing than currently priced in swaps.

In light of this premium built in the front end and the country’s relatively high external imbalances, we think the 1-yr/3-

yr is the best sector to place receivers. In fact, the rates-FX association in the front end fell towards non-significant

levels by mid-March, whereas the correlation on the back end remains high. Since we expect further correction in

Colombia’s current account balance, we believe the co-movement of the COP with the 10-year will diminish ahead,

thus opening a better opportunity to receive the long end of the curve.

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 Mar-22

Forward curve pricing (IBR swaps) vs. analysts' projections

Source: Bloomberg, Latin Consensus, Itaú

% p.a.

* TP = Term-premium (historical)

Market pricingMarket pricing (ex-TP*)

Itaú forecastConsensus forecast

-116

-78

-149

-109

-134

-219

-250

-200

-150

-100

-50

0

2017YE 2018YE

IBR swaps: implicit rate hikes by...

bps

* TP = Term-premium

Unadjusted for TP*Adjusted for TP*Analysts' consensus

Source: Bloomberg, Latin Consensus, Itaú

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Mar-16 May-16 Jul-16 Sep-16 Nov-16 Jan-17 Mar-17

Rates-FX correlation in Colombia

Source: Bloomberg, Itaú

Correlation coefficient (100 days)

1Y IBR Swap2Y IBR Swap5Y IBR Swap

10Y IBR Swap

critical level

Page 14

Latam Fixed Income Strategy Monthly – March 17, 2017

Appendix 1: FX models

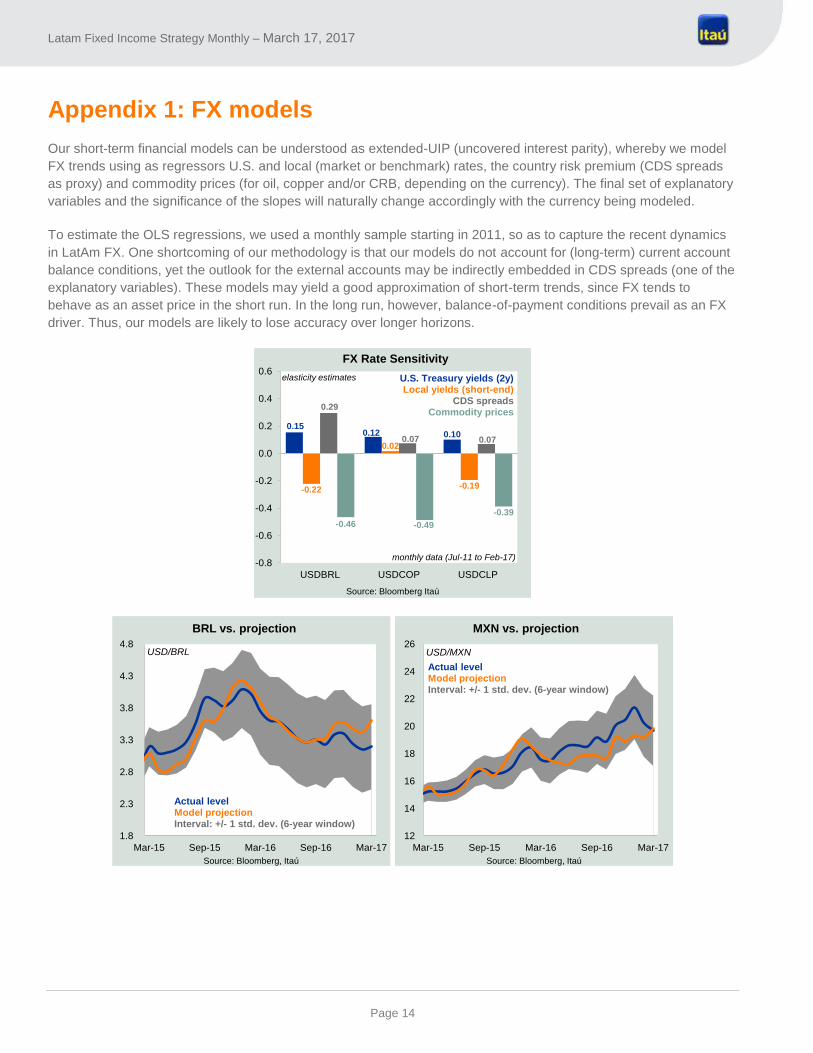

Our short-term financial models can be understood as extended-UIP (uncovered interest parity), whereby we model

FX trends using as regressors U.S. and local (market or benchmark) rates, the country risk premium (CDS spreads

as proxy) and commodity prices (for oil, copper and/or CRB, depending on the currency). The final set of explanatory

variables and the significance of the slopes will naturally change accordingly with the currency being modeled.

To estimate the OLS regressions, we used a monthly sample starting in 2011, so as to capture the recent dynamics

in LatAm FX. One shortcoming of our methodology is that our models do not account for (long-term) current account

balance conditions, yet the outlook for the external accounts may be indirectly embedded in CDS spreads (one of the

explanatory variables). These models may yield a good approximation of short-term trends, since FX tends to

behave as an asset price in the short run. In the long run, however, balance-of-payment conditions prevail as an FX

driver. Thus, our models are likely to lose accuracy over longer horizons.

0.150.12 0.10

-0.22

0.02

-0.19

0.29

0.07 0.07

-0.46 -0.49

-0.39

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

USDBRL USDCOP USDCLP

FX Rate Sensitivity

Source: Bloomberg Itaú

elasticity estimates

monthly data (Jul-11 to Feb-17)

U.S. Treasury yields (2y)Local yields (short-end)

CDS spreadsCommodity prices

1.8

2.3

2.8

3.3

3.8

4.3

4.8

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

BRL vs. projection

Source: Bloomberg, Itaú

Actual levelModel projectionInterval: +/- 1 std. dev. (6-year window)

USD/BRL

12

14

16

18

20

22

24

26

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

MXN vs. projection

Source: Bloomberg, Itaú

USD/MXN

Actual levelModel projectionInterval: +/- 1 std. dev. (6-year window)

Page 15

Latam Fixed Income Strategy Monthly – March 17, 2017

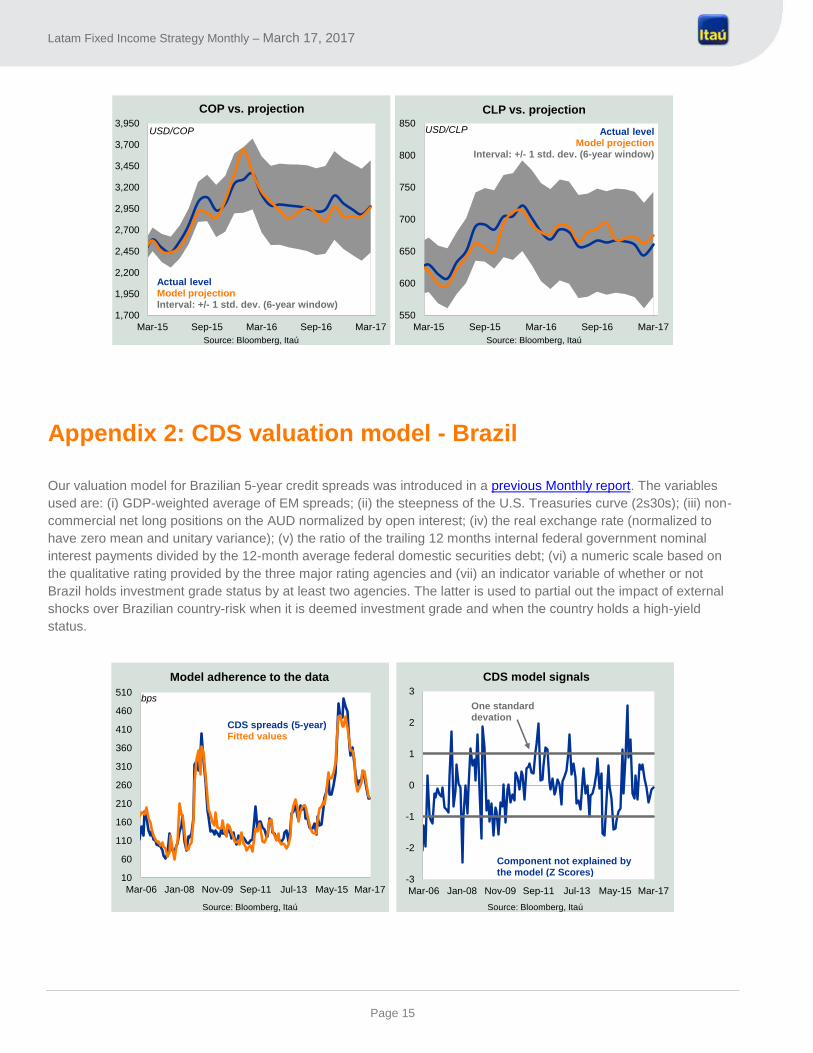

Appendix 2: CDS valuation model - Brazil

Our valuation model for Brazilian 5-year credit spreads was introduced in a previous Monthly report. The variables

used are: (i) GDP-weighted average of EM spreads; (ii) the steepness of the U.S. Treasuries curve (2s30s); (iii) non-

commercial net long positions on the AUD normalized by open interest; (iv) the real exchange rate (normalized to

have zero mean and unitary variance); (v) the ratio of the trailing 12 months internal federal government nominal

interest payments divided by the 12-month average federal domestic securities debt; (vi) a numeric scale based on

the qualitative rating provided by the three major rating agencies and (vii) an indicator variable of whether or not

Brazil holds investment grade status by at least two agencies. The latter is used to partial out the impact of external

shocks over Brazilian country-risk when it is deemed investment grade and when the country holds a high-yield

status.

550

600

650

700

750

800

850

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

CLP vs. projection

Source: Bloomberg, Itaú

USD/CLP Actual levelModel projection

Interval: +/- 1 std. dev. (6-year window)

1,700

1,950

2,200

2,450

2,700

2,950

3,200

3,450

3,700

3,950

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17

COP vs. projection

Source: Bloomberg, Itaú

USD/COP

Actual levelModel projectionInterval: +/- 1 std. dev. (6-year window)

10

60

110

160

210

260

310

360

410

460

510

Mar-06 Jan-08 Nov-09 Sep-11 Jul-13 May-15 Mar-17

Model adherence to the data

Source: Bloomberg, Itaú

CDS spreads (5-year)Fitted values

bps

-3

-2

-1

0

1

2

3

Mar-06 Jan-08 Nov-09 Sep-11 Jul-13 May-15 Mar-17

CDS model signals

Source: Bloomberg, Itaú

Component not explained by the model (Z Scores)

One standard devation

Page 16

Latam Fixed Income Strategy Monthly – March 17, 2017

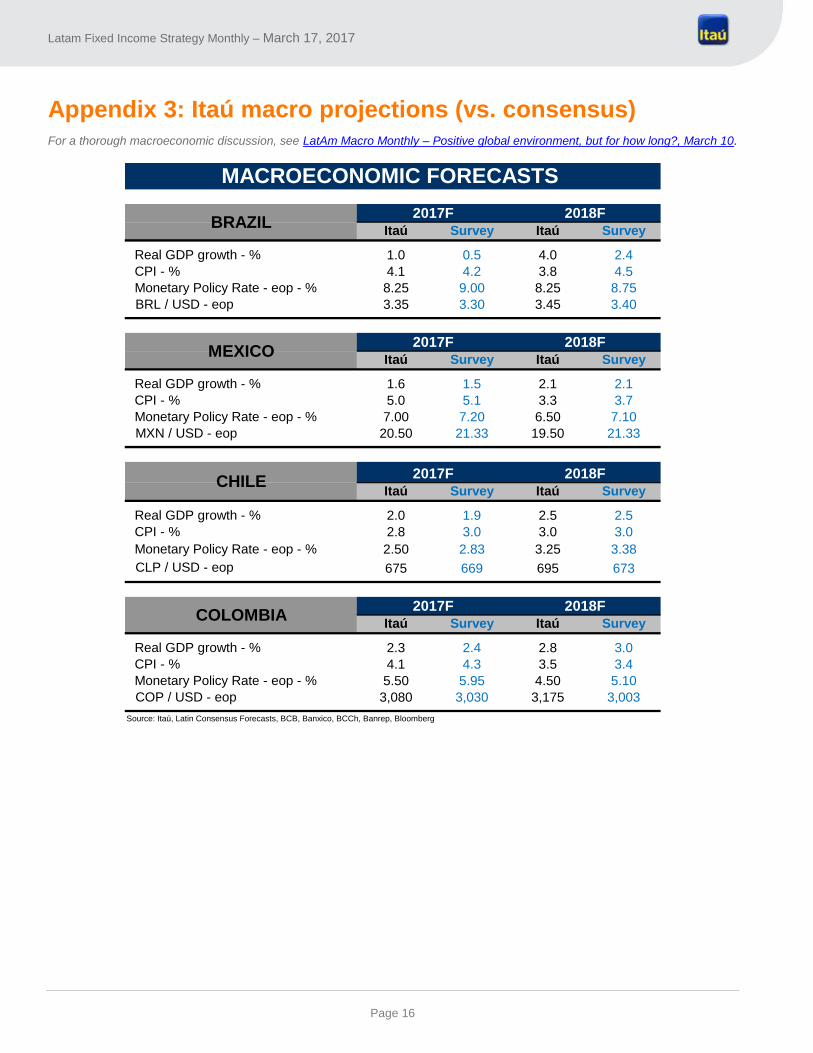

Appendix 3: Itaú macro projections (vs. consensus) For a thorough macroeconomic discussion, see LatAm Macro Monthly – Positive global environment, but for how long?, March 10.

Itaú Survey Itaú Survey

Real GDP growth - % 1.0 0.5 4.0 2.4

CPI - % 4.1 4.2 3.8 4.5

Monetary Policy Rate - eop - % 8.25 9.00 8.25 8.75

BRL / USD - eop 3.35 3.30 3.45 3.40

Itaú Survey Itaú Survey

Real GDP growth - % 1.6 1.5 2.1 2.1

CPI - % 5.0 5.1 3.3 3.7

Monetary Policy Rate - eop - % 7.00 7.20 6.50 7.10

MXN / USD - eop 20.50 21.33 19.50 21.33

Itaú Survey Itaú Survey

Real GDP growth - % 2.0 1.9 2.5 2.5

CPI - % 2.8 3.0 3.0 3.0

Monetary Policy Rate - eop - % 2.50 2.83 3.25 3.38

CLP / USD - eop 675 669 695 673

Itaú Survey Itaú Survey

Real GDP growth - % 2.3 2.4 2.8 3.0

CPI - % 4.1 4.3 3.5 3.4

Monetary Policy Rate - eop - % 5.50 5.95 4.50 5.10

COP / USD - eop 3,080 3,030 3,175 3,003

Source: Itaú, Latin Consensus Forecasts, BCB, Banxico, BCCh, Banrep, Bloomberg

BRAZIL2018F

2018F

2018F

2018F

MACROECONOMIC FORECASTS

2017F

2017F

MEXICO

COLOMBIA

CHILE

2017F

2017F

Page 17

Latam Fixed Income Strategy Monthly – March 17, 2017

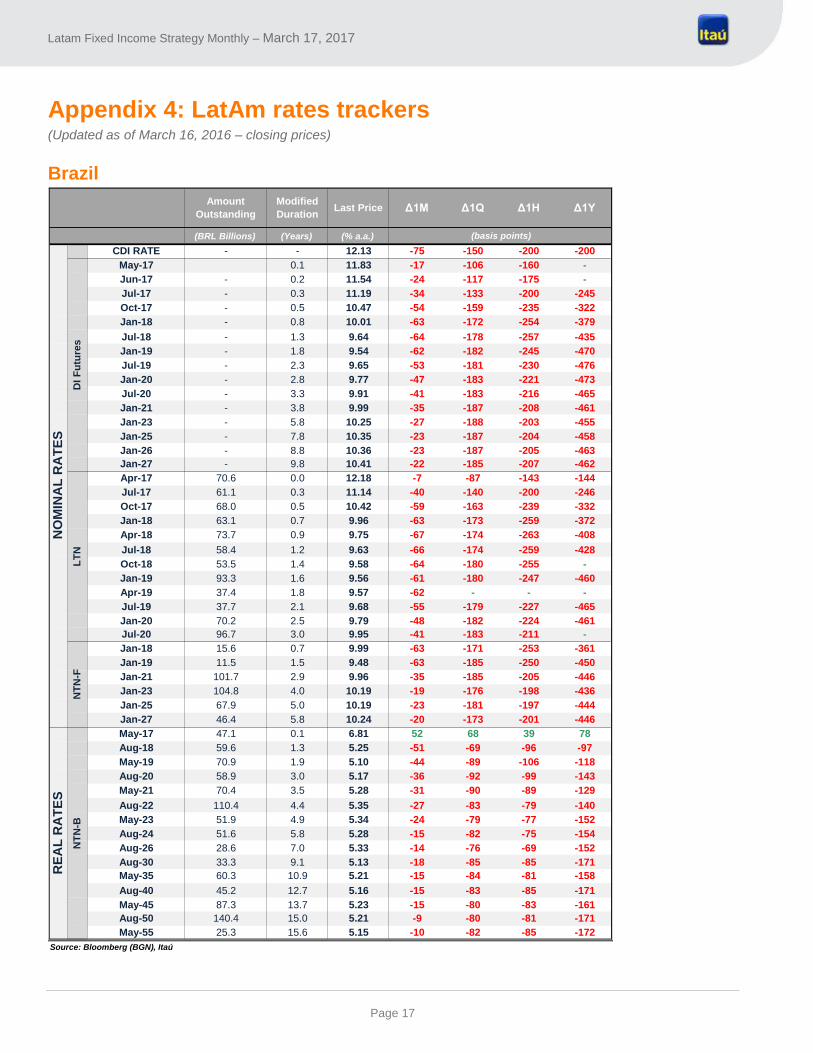

Appendix 4: LatAm rates trackers (Updated as of March 16, 2016 – closing prices)

Brazil

Amount

Outstanding

Modified

DurationLast Price Δ1M Δ1Q Δ1H Δ1Y

(BRL Billions) (Years) (% a.a.)

CDI RATE - - 12.13 -75 -150 -200 -200

May-17 0.1 11.83 -17 -106 -160 -

Jun-17 - 0.2 11.54 -24 -117 -175 -

Jul-17 - 0.3 11.19 -34 -133 -200 -245

Oct-17 - 0.5 10.47 -54 -159 -235 -322

Jan-18 - 0.8 10.01 -63 -172 -254 -379

Jul-18 - 1.3 9.64 -64 -178 -257 -435

Jan-19 - 1.8 9.54 -62 -182 -245 -470

Jul-19 - 2.3 9.65 -53 -181 -230 -476

Jan-20 - 2.8 9.77 -47 -183 -221 -473

Jul-20 - 3.3 9.91 -41 -183 -216 -465

Jan-21 - 3.8 9.99 -35 -187 -208 -461

Jan-23 - 5.8 10.25 -27 -188 -203 -455

Jan-25 - 7.8 10.35 -23 -187 -204 -458

Jan-26 - 8.8 10.36 -23 -187 -205 -463

Jan-27 - 9.8 10.41 -22 -185 -207 -462

Apr-17 70.6 0.0 12.18 -7 -87 -143 -144

Jul-17 61.1 0.3 11.14 -40 -140 -200 -246

Oct-17 68.0 0.5 10.42 -59 -163 -239 -332

Jan-18 63.1 0.7 9.96 -63 -173 -259 -372

Apr-18 73.7 0.9 9.75 -67 -174 -263 -408

Jul-18 58.4 1.2 9.63 -66 -174 -259 -428

Oct-18 53.5 1.4 9.58 -64 -180 -255 -

Jan-19 93.3 1.6 9.56 -61 -180 -247 -460

Apr-19 37.4 1.8 9.57 -62 - - -

Jul-19 37.7 2.1 9.68 -55 -179 -227 -465

Jan-20 70.2 2.5 9.79 -48 -182 -224 -461

Jul-20 96.7 3.0 9.95 -41 -183 -211 -

Jan-18 15.6 0.7 9.99 -63 -171 -253 -361

Jan-19 11.5 1.5 9.48 -63 -185 -250 -450

Jan-21 101.7 2.9 9.96 -35 -185 -205 -446

Jan-23 104.8 4.0 10.19 -19 -176 -198 -436

Jan-25 67.9 5.0 10.19 -23 -181 -197 -444

Jan-27 46.4 5.8 10.24 -20 -173 -201 -446

May-17 47.1 0.1 6.81 52 68 39 78

Aug-18 59.6 1.3 5.25 -51 -69 -96 -97

May-19 70.9 1.9 5.10 -44 -89 -106 -118

Aug-20 58.9 3.0 5.17 -36 -92 -99 -143

May-21 70.4 3.5 5.28 -31 -90 -89 -129

Aug-22 110.4 4.4 5.35 -27 -83 -79 -140

May-23 51.9 4.9 5.34 -24 -79 -77 -152

Aug-24 51.6 5.8 5.28 -15 -82 -75 -154

Aug-26 28.6 7.0 5.33 -14 -76 -69 -152

Aug-30 33.3 9.1 5.13 -18 -85 -85 -171

May-35 60.3 10.9 5.21 -15 -84 -81 -158

Aug-40 45.2 12.7 5.16 -15 -83 -85 -171

May-45 87.3 13.7 5.23 -15 -80 -83 -161

Aug-50 140.4 15.0 5.21 -9 -80 -81 -171

May-55 25.3 15.6 5.15 -10 -82 -85 -172

Source: Bloomberg (BGN), Itaú

(basis points)

DI

Fu

ture

sL

TN

RE

AL

RA

TE

S

NT

N-B

NT

N-F

NO

MIN

AL

RA

TE

S

Page 18

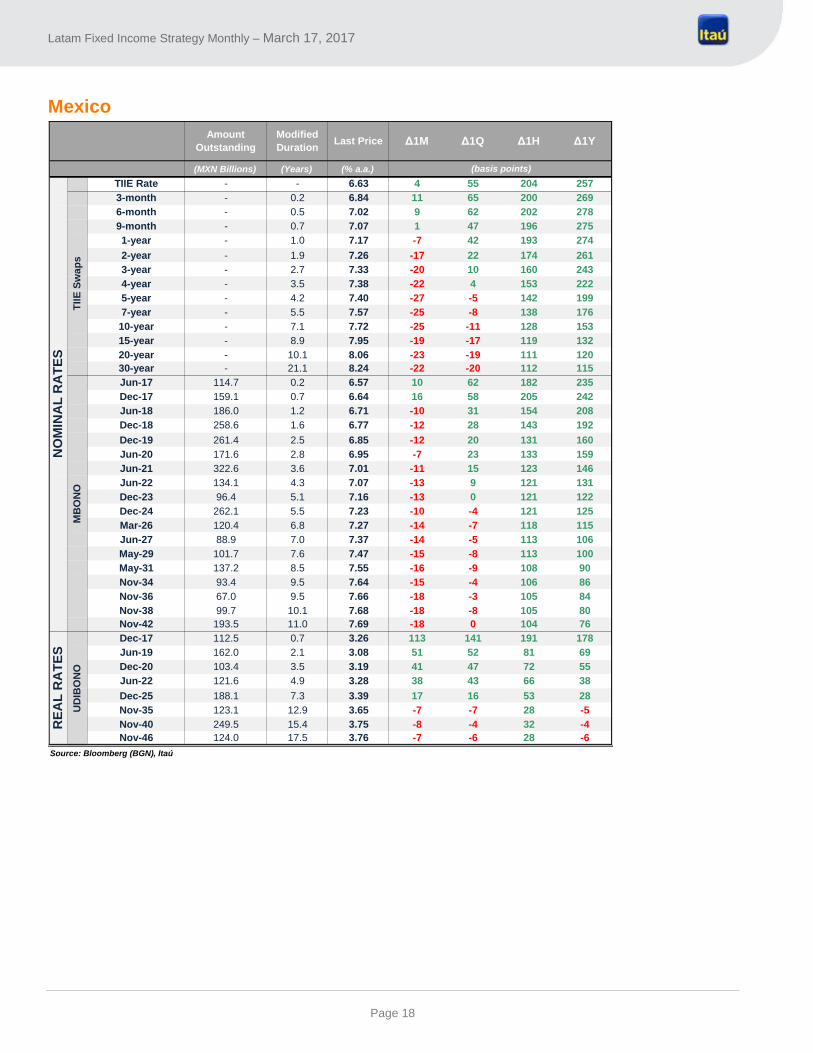

Latam Fixed Income Strategy Monthly – March 17, 2017

Mexico

Amount

Outstanding

Modified

DurationLast Price Δ1M Δ1Q Δ1H Δ1Y

(MXN Billions) (Years) (% a.a.)

TIIE Rate - - 6.63 4 55 204 257

3-month - 0.2 6.84 11 65 200 269

6-month - 0.5 7.02 9 62 202 278

9-month - 0.7 7.07 1 47 196 275

1-year - 1.0 7.17 -7 42 193 274

2-year - 1.9 7.26 -17 22 174 261

3-year - 2.7 7.33 -20 10 160 243

4-year - 3.5 7.38 -22 4 153 222

5-year - 4.2 7.40 -27 -5 142 199

7-year - 5.5 7.57 -25 -8 138 176

10-year - 7.1 7.72 -25 -11 128 153

15-year - 8.9 7.95 -19 -17 119 132

20-year - 10.1 8.06 -23 -19 111 120

30-year - 21.1 8.24 -22 -20 112 115

Jun-17 114.7 0.2 6.57 10 62 182 235

Dec-17 159.1 0.7 6.64 16 58 205 242

Jun-18 186.0 1.2 6.71 -10 31 154 208

Dec-18 258.6 1.6 6.77 -12 28 143 192

Dec-19 261.4 2.5 6.85 -12 20 131 160

Jun-20 171.6 2.8 6.95 -7 23 133 159

Jun-21 322.6 3.6 7.01 -11 15 123 146

Jun-22 134.1 4.3 7.07 -13 9 121 131

Dec-23 96.4 5.1 7.16 -13 0 121 122

Dec-24 262.1 5.5 7.23 -10 -4 121 125

Mar-26 120.4 6.8 7.27 -14 -7 118 115

Jun-27 88.9 7.0 7.37 -14 -5 113 106

May-29 101.7 7.6 7.47 -15 -8 113 100

May-31 137.2 8.5 7.55 -16 -9 108 90

Nov-34 93.4 9.5 7.64 -15 -4 106 86

Nov-36 67.0 9.5 7.66 -18 -3 105 84

Nov-38 99.7 10.1 7.68 -18 -8 105 80

Nov-42 193.5 11.0 7.69 -18 0 104 76

Dec-17 112.5 0.7 3.26 113 141 191 178

Jun-19 162.0 2.1 3.08 51 52 81 69

Dec-20 103.4 3.5 3.19 41 47 72 55

Jun-22 121.6 4.9 3.28 38 43 66 38

Dec-25 188.1 7.3 3.39 17 16 53 28

Nov-35 123.1 12.9 3.65 -7 -7 28 -5

Nov-40 249.5 15.4 3.75 -8 -4 32 -4

Nov-46 124.0 17.5 3.76 -7 -6 28 -6

Source: Bloomberg (BGN), Itaú

UD

IBO

NO

RE

AL

RA

TE

S

(basis points)

TII

E S

wap

sM

BO

NO

NO

MIN

AL

RA

TE

S

Page 19

Latam Fixed Income Strategy Monthly – March 17, 2017

Chile

Amount

Outstanding

Modified

DurationLast Price Δ1M Δ1Q Δ1H Δ1Y

(CLP Billions) (Years) (% a.a.)

Interbank Rate - - 3.50 - - - 0

3-month - 0.3 2.98 -11 -34 -54 -69

6-month - 0.5 2.96 -10 -25 -52 -80

9-month - 0.7 2.94 -9 -23 -50 -87

1-year - 1.0 2.92 -9 -23 -53 -94

18-month - 1.5 2.95 -10 -20 -49 -100

2-year - 2.0 3.01 -7 -16 -38 -94

3-year - 2.9 3.25 -2 -10 -21 -80

4-year - 3.8 3.49 2 -7 -7 -69

5-year - 4.6 3.71 6 -5 2 -57

6-year - 5.4 3.88 8 -6 8 -49

7-year - 6.2 4.01 6 -9 10 -44

8-year - 6.9 4.09 6 -13 8 -41

9-year - 7.6 4.20 8 -11 9 -36

10-year - 8.3 4.26 7 -11 10 -34

15-year - 11.2 4.39 5 -16 10 -31

20-year - 13.5 4.49 7 -13 12 -33

Jan-18 450.0 1.0 3.20 -8 -26 -45 -83

Mar-18 344.1 1.0 3.17 -9 -25 -53 -83

Jan-19 290.0 1.9 3.23 -12 -26 -47 -90

Jan-20 762.5 2.8 3.53 0 -12 -28 -69

Feb-21 1,000.0 3.9 3.73 0 - - -

Mar-21 700.0 3.9 3.83 10 - - -

Jan-22 475.4 3.7 3.88 14 2 -10 -39

Jan-24 530.0 5.4 4.00 -1 -21 -10 -41

Mar-26 1,348.0 6.9 4.36 18 0 - -8

Jan-32 464.7 9.4 4.50 16 -5 1 -9

Jan-34 415.0 10.3 - - - - -

Mar-35 547.0 11.4 - - - - -

Jan-43 1,176.3 13.6 4.81 - - - -2

Mar-18 246.8 1.0 3.18 -3 -20 -47 -78

May-18 83.6 1.0 3.18 -11 -25 -42 -78

Jun-18 243.2 1.0 3.20 -8 -25 -41 -74

Jan-19 400.0 2.0 3.32 -3 -16 -34 -

Apr-20 450.0 2.9 3.59 -3 -8 - -63

Jun-20 900.0 2.9 3.66 5 -2 - -57

Jul-20 450.0 2.9 3.43 -6 -19 -39 -75

Feb-21 470.0 3.7 3.75 -1 -10 -22 -51

Mar-22 350.0 4.6 3.82 6 -4 -16 -46

Mar-23 245.0 4.5 - - - - -

May-17 204.0 0.1 -0.64 -89 -254 -164 -134

Jul-17 328.4 0.3 0.48 51 -83 - -42

Jan-18 348.8 0.8 0.55 28 -50 -22 -29

Mar-18 606.6 0.9 0.56 13 -54 -22 -27

Jul-18 440.5 1.3 0.58 21 -53 -25 -29

Aug-18 214.5 1.3 0.58 20 -52 -21 -30

Oct-18 147.5 1.5 0.58 - -51 -21 -30

May-19 25.4 2.0 0.64 19 -48 -20 -36

Feb-21 1,165.4 3.7 0.91 11 -23 -12 -23

Mar-22 609.2 4.6 0.96 15 -20 -8 -18

Sep-22 221.2 4.9 1.01 18 -15 -4 -17

Mar-23 291.4 5.5 - - - - -

May-28 304.1 9.5 1.42 8 -11 4 -5

Feb-31 741.6 11.5 1.49 6 -15 2 -8

Feb-41 741.6 17.6 1.80 6 -11 18 13

Source: Bloomberg (BGN), Itaú

BC

P

NO

MIN

AL

RA

TE

S

(basis points)

CA

MA

RA

Sw

ap

sB

TP

BC

U

Page 20

Latam Fixed Income Strategy Monthly – March 17, 2017

Colombia

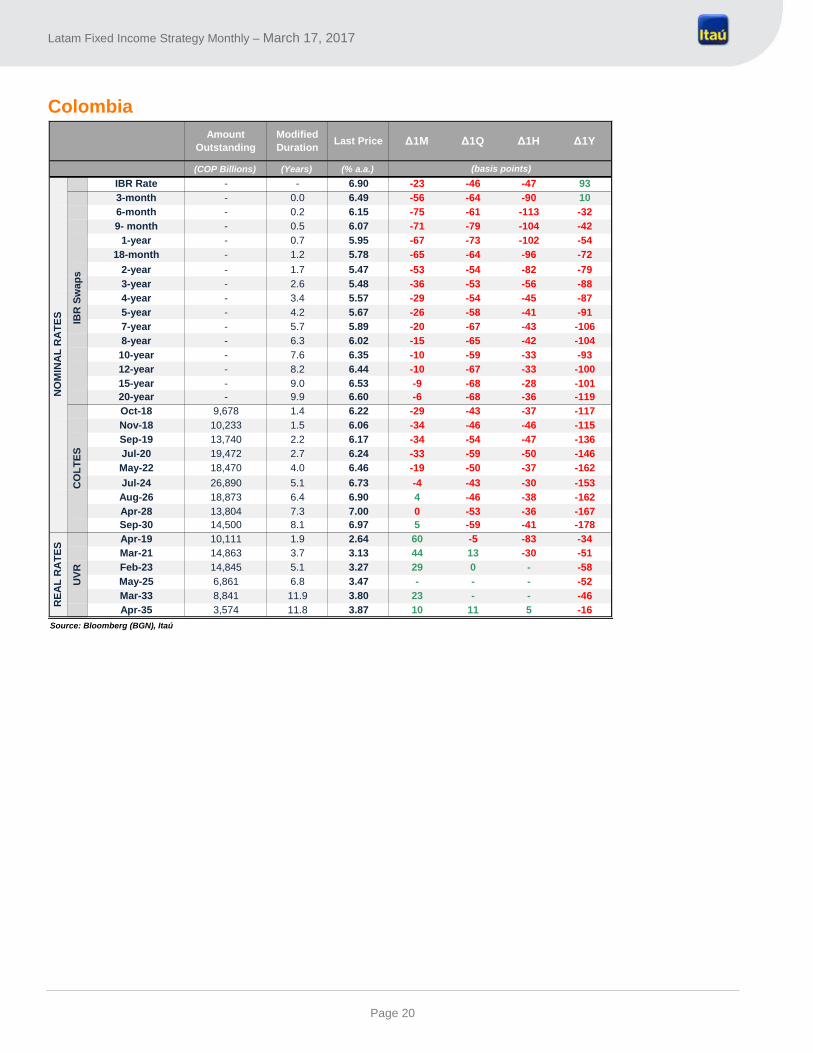

Amount

Outstanding

Modified

DurationLast Price Δ1M Δ1Q Δ1H Δ1Y

(COP Billions) (Years) (% a.a.)

IBR Rate - - 6.90 -23 -46 -47 93

3-month - 0.0 6.49 -56 -64 -90 10

6-month - 0.2 6.15 -75 -61 -113 -32

9- month - 0.5 6.07 -71 -79 -104 -42

1-year - 0.7 5.95 -67 -73 -102 -54

18-month - 1.2 5.78 -65 -64 -96 -72

2-year - 1.7 5.47 -53 -54 -82 -79

3-year - 2.6 5.48 -36 -53 -56 -88

4-year - 3.4 5.57 -29 -54 -45 -87

5-year - 4.2 5.67 -26 -58 -41 -91

7-year - 5.7 5.89 -20 -67 -43 -106

8-year - 6.3 6.02 -15 -65 -42 -104

10-year - 7.6 6.35 -10 -59 -33 -93

12-year - 8.2 6.44 -10 -67 -33 -100

15-year - 9.0 6.53 -9 -68 -28 -101

20-year - 9.9 6.60 -6 -68 -36 -119

Oct-18 9,678 1.4 6.22 -29 -43 -37 -117

Nov-18 10,233 1.5 6.06 -34 -46 -46 -115

Sep-19 13,740 2.2 6.17 -34 -54 -47 -136

Jul-20 19,472 2.7 6.24 -33 -59 -50 -146

May-22 18,470 4.0 6.46 -19 -50 -37 -162

Jul-24 26,890 5.1 6.73 -4 -43 -30 -153

Aug-26 18,873 6.4 6.90 4 -46 -38 -162

Apr-28 13,804 7.3 7.00 0 -53 -36 -167

Sep-30 14,500 8.1 6.97 5 -59 -41 -178

Apr-19 10,111 1.9 2.64 60 -5 -83 -34

Mar-21 14,863 3.7 3.13 44 13 -30 -51

Feb-23 14,845 5.1 3.27 29 0 - -58

May-25 6,861 6.8 3.47 - - - -52

Mar-33 8,841 11.9 3.80 23 - - -46

Apr-35 3,574 11.8 3.87 10 11 5 -16

Source: Bloomberg (BGN), Itaú

(basis points)

IBR

Sw

ap

sC

OL

TE

S

NO

MIN

AL

RA

TE

SR

EA

L R

AT

ES

UV

R

Page 21

Latam Fixed Income Strategy Monthly – March 17, 2017

Appendix 5: Closed recommendations

Price Date Price Date

Mexico TIIE Swaps: receive 1-year, pay 10-year (DV01-neutral) 252 bps 16-Nov-15 210 bps 10-Feb-16 -45 bps

Chile Camara Swaps: pay the 7-year 4.37% 9-Oct-15 4.37% 2-Feb-16 0 bps

Mexico TIIE Swaps: pay the 7-year 5.80% 2-Dec-15 5.60% 29-Jan-16 -120 bps

FX Buy MXN; Sell COP 174.49 8-Oct-15 173.68 03-Nov-15 -57 bps

Brazil DI Futures: receive Jul16, pay Jan21 (DV01-neutral) 22 bps 8-Oct-15 100 bps 23-Oct-15 78 bps

Mexico TIIE Swaps: Pay the 5-year 5.53% 14-Aug-15 5.20% 15-Aug-15 -151 bps

Chile Camara Swaps: Pay the 10-year 4.58% 14-Aug-15 4.75% 17-set-15 +142 bps

Colombia IBR Swaps: Receive 1-year, Pay 10-year (DV01-neutral) 165 bps 14-Aug-15 185 bps 6-Aug-15 +20 bps

FX Long MXN, Short COP 4.709 10-Aug-15 4.790 20-Aug-15 -194 bps

Colombia IBR Swaps: pay the 5-year 5.36% 16-Mar-15 5.75% 6-Aug-15 +162 p.b.

Mexico TIIE Swaps: receive 1-year, pay 10-year (DV01-neutral) 266 19-Jun-15 245 30-Jul-15 -22 bps

FX Short BRL/CLP 206.77 17-Jun-15 195.00 28-Jul-15 +484 bps

Brazil DI Futures: receive Jan16, pay Jan25 (DV01-neutral) 173.89 19-Jun-15 156.00 21-Jul-15 +11 bps

FX Buy MXN; Sell COP 155.65 12-May-15 163.50 19-May-15 +502 bps

Mexico TIIE Swaps: Pay the 10-year 6.19% 19-Jul-14 6.30% 13-May-15 +86 bps

Colombia IBR Swaps: pay the 1-year 4.39% 17-Apr-15 4.50% 8-May-15 +11 bps

Chile Camara Swaps: pay the 10-year 4.39% 3-May-15 4.60% 8-May-15 +181 bps

Colombia IBR Swaps: receive the 10-year 5.98% 17-Apr-15 6.10% 5-May-15 -93 bps

Mexico Receive the 1-year and pay the 10-year (DV01-neutral) 213 bps 17-Apr-15 236 bps 30-Apr-15 +17 bps

Brazil Long NTN-B 2018 6.31% 2-Apr-15 6.45% 20-Apr-15 -6 bps

FX Long MXN, Short COP 166.76 15-Apr-15 163.50 17-Apr-15 -196 bps

Brazil Receive DI Jan16 13.68% 19-Mar-15 13.30% 6-Apr-15 +29 bps

Mexico Long Mbono 2021 5.47% 19-Mar-15 5.61% 30-Mar-15 -77 bps

Chile Camara Swaps: receive the 10-year 4.54% 19-Mar-15 4.45% 26-Mar-15 +74 bps

FX Short EURMXN 16.36 16-Mar-15 16.45 26-Mar-15 -67 bps

Chile Camara Swaps: pay the 5-year 4.05% 9-Mar-15 4.10% 18-Mar-15 +23 bps

Mexico TIIE Swaps: pay the 10-year 6.26% 16-Mar-15 6.10% 18-Mar-15 -125 bps

FX Sell COP (Vs. USD) 2,669.98 16-Mar-15 2,630.00 18-Mar-15 -150 bps

FX Buy MXN; Sell COP 168.58 10-Mar-15 169.50 12-Mar-15 +54 bps

FX Sell CLP (Vs. USD) 618.94 27-Feb-15 635.60 12-Mar-15 +258 bps

Mexico TIIE Swaps: pay the 5-year 5.30% 3-Mar-15 5.60% 11-Mar-15 +136 bps

Colombia IBR Swaps: pay the 5-year 5.21% 9-Mar-15 5.30% 11-Mar-15 +40 bps

Mexico TIIE Swaps: pay the 10-year (HEDGE to our long position in MBono 2024) 5.85% 9-Feb-15 6.28% 6-Mar-15 +341 bps

Mexico Long Mbono 2024, Pay 2-year TIIE IRS 140 bps 23-Jan-15 148 bps 6-Mar-15 +318 bps

Chile Camara IRS: pay 5-year, receive 2-year 60 bps 13-Feb-15 65 bps 6-Mar-15 +65 bps

Colombia IBR Swaps: pay the 2-year 4.29% 13-Feb-15 4.47% 6-Mar-15 -35 bps

Brazil Receive April 2015 DI Futures 12.20% 23-Dec-14 12.50% 27-Feb-15 +3 bps

Mexico TIIE Swaps: pay the 5-year 5.17% 9-Oct-14 5.20% 23-Feb-15 +14 bps

Brazil DI Futures: receive Jan17, pay Jan21 56 bps 13-Feb-15 45 bps 23-Feb-15 +32 bps

Brazil Long NTN-B 2018 5.83% 6-Feb-15 6.13% 11-Feb-15 -77 bps

Brazil DI Futures: receive Jan16, pay Jan21 60 bps 6-Feb-15 44 bps 10-Feb-15 +154 bps

Brazil Long NTN-B 2030 5.92% 23-Dec-14 6.05% 5-Feb-15 -97 bps

Colombia Receive COLTES Jun2016 5.03% 23-Dec-14 4.66% 4-Feb-15 +50 bps

FX Buy MXNJPY 8.23 23-Dec-14 7.90 30-Jan-15 -432 bps

Chile Camara Swaps: receive 2-year 3.05% 27-Nov-14 2.80% 23-Jan-15 +50 bps

FX Sell CLP (Vs. USD) 616.16 3-Dec-14 625.00 22-Jan-15 +105 bps

FX Sell EURMXN 18.02 18-Dec-14 16.80 16-Jan-15 +676 bps

Brazil Receive Jan-15 DI (Futures) 11.59% 3-Dec-14 11.59% 2-Jan-15 +5 bps

Mexico TIIE Swaps: pay the 10-year 6.00% 9-Oct-14 6.15% 18-Dec-14 +150 bps

FX Sell COP (Vs. USD) 2,286.28 3-Dec-14 2,365.00 9-Dec-14 +336 bps

Brazil Long NTN-F 2025 12.00% 26-Nov-14 12.15% 7-Dec-14 -94 bps

Brazil Long NTN-B 2050 5.77% 26-Nov-14 5.95% 2-Dec-14 -226 bps

FX Long MXN/COP 158.11 19-Nov-14 162.15 2-Dec-14 +255 bps

Brazil Receive DI Jan-16, Pay DI Jan-21 (no immunization) 11 bps 19-Nov-14 -20 bps 21-Nov-14 -268 bps

Chile Camara Swaps: pay the 5-year 4.13% 9-Oct-14 3.79% 21-Nov-14 -170 bps

FX Sell COP (Vs. USD) 2,026.72 3-Oct-14 2,060.00 17-Oct-14 +164 bps

FX Sell CLP (Vs. USD) 582.30 25-Aug-14 591.00 13-Oct-14 +104 bps

Chile Camara Swaps: receive 1y, pay 5y 52bps 23-Jul-14 103bps 9-Oct-14 +127 bps

Colombia IBR Swaps: pay 5y 5.28% 3-Sep-14 5.35% 9-Oct-14 +35 bps

Mexico Mbono: long Dec15, short Dec18 143 bps 23-Jul-14 157 bps 9-Oct-14 +58 bps

Mexico TIIE Swaps: receive 2y, pay 10y 221 bps 3-Sep-14 219 bps 9-Oct-14 +130 bps

Source: Bloomberg

Trading Idea P&L (bps)Entry Closing

Page 22

Latam Fixed Income Strategy Monthly – March 17, 2017

Relevant Information

1. This report has been produced by Itaú Corretora de Valores S.A (“Itaú BBA”), a subsidiary of Itaú Unibanco S.A., regulated by the Securities and Exchange Commission of Brazil (CVM),

and distributed by Itaú BBA or one of its affiliates (altogether, “Itaú Unibanco Group”). Itaú BBA is the brand name used by Itaú Corretora de Valores S.A., by its affiliates or by other

companies of the Itaú Unibanco Group.

2. This report aims at providing information only and does not constitute, and should not be construed as an offer to buy or sel l, or a solicitation of an offer to buy or sell any financial

instrument, or to participate in any particular trading strategy in any jurisdiction. The information herein is believed to be reliable as of the date on which this report was issued and has

been obtained from public sources believed to be reliable. Itaú Unibanco Group does not make any express or implied representation or warranty as to the completeness, reliability or

accuracy of such information, nor does this report intend to be a complete statement or summary of the investment strategies, markets or developments referred to herein. Opinions,

estimates, and projections expressed herein constitute the current judgment of the analyst responsible for the substance of this report as of the date on which it was issued and are,

therefore, subject to change without notice. Prices and availability of financial instruments are indicative only and subject to change without notice. Itaú Unibanco Group has no obligation

to update, modify or amend this report and inform the reader accordingly, except when terminating coverage of the issuer of the securities discussed in this report.

3. The analyst responsible for the production of this report, whose name is highlighted in bold, hereby certifies that the views expressed herein accurately and exclusively

reflect his or her personal views and opinions about any and all of the subject issuers or securities and were prepared independently and autonomously, including from Itaú

BBA, Banco Itaú BBA S.A and other group companies. Because personal views of analysts may differ from one another, Itaú BBA, its subsidiaries and affiliates may have

issued or may issue other reports that are inconsistent with, and/or reach different conclusions from, the information presented herein. The analyst responsible for the

production of this report is not registered and/or qualified as a research analyst with the NYSE or FINRA and is not associated with Itau BBA USA Securities, Inc. and,

therefore, may not be subject to Rule 2711 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst

account.

4. An analyst’s compensation is determined based upon the total revenues of Itaú BBA, a portion of which is generated through investment banking activities. Like all employees of Itaú

BBA, its subsidiaries and affiliates, analysts receive compensation that is linked to global earnings. Therefore, analyst’s compensation can be considered to be indirectly related to this

report. However, the analyst responsible for the content of this report hereby certifies that no part of his or her compensation was, is, or will be directly or indirectly related to any specific

recommendation or opinion herein or linked to the pricing of any of the securities discussed herein. Itaú Unibanco Group and the funds, portfolios and securities investment clubs

managed by Itaú Unibanco Group may have a direct or indirect stake equal to no more than 1% (one percent) of the capital stock of the companies, and may have been involved in the

acquisition, sale or trading of such shares in the market.

5. The financial instruments discussed in this report may not be suitable for all investors. This report does not take into account the investment objectives, financial situation or particular

needs of any particular investor. Investors wishing to purchase or otherwise deal in the securities covered in this report should obtain relevant documents relating to the financial

instruments and exchanges and confirm their contents. Investors should obtain independent financial advice based on their own particular circumstances before making an investment

decision based on the information herein. Final decision on investments must be made by each investor considering various risks, fees and commissions. If a financial instrument is

denominated in a currency other than an investor’s currency, changes in exchange rates may adversely affect the price or value of, or the income derived from the financial instrument,

and the reader of this report assumes all foreign exchange risks. Income from financial instruments may vary, and therefore their price or value may rise or fall, either directly or indirectly.

Past performance does not necessarily indicate future results, and no representation or warranty, express or implied, is made herein regarding future performance. Itaú Unibanco Group

does not accept any liability whatsoever for any direct or consequential loss arising from the use of this report or its content, and the investor using this report undertakes to irrevocably

exempt the Itaú Unibanco Group from any claims, complaints and/or demands.

6. This report may not be reproduced or redistributed to any other person, in whole or in part, for any purpose, without the prior written consent of Itaú BBA. Additional information on the

financial instruments discussed in this report is available upon request.

7. As required by the Brazilian Securities and Exchange Commission rules, the analysts responsible for this report indicate potential conflict situations in the table below of “Relevant

Information”.

Additional Note to reports distributed in: (i) U.K. and Europe: The sole purpose of this material is to provide information only, and it does not constitute or should be construed as a

proposal or request to enter into any financial instrument or to participate in any specific business strategy. The financial instruments discussed in this material may not be suitable for all

investors, and are directed solely at Eligible Counterparties and Professionals as defined by the Financial Conduct Authority. This material does not take into consideration the objectives,

financial situation or specific needs of any particular client. Clients must obtain financial, tax, legal, accounting, economic, credit and market advice on an individual basis, based on their

personal characteristics and objectives, prior to making any decision based on the information contained herein. By accessing the material, you confirm that you are aware of the laws in your

jurisdiction relating to the provision and sale of financial service products. You acknowledge that this material contains proprietary information and you agree to keep this information

confidential. Itau BBA International plc (IBBAInt) exempts itself from any liability for any losses, whether direct or indirect, which may arise from the use of this material, from its content and is

under no obligation to update the information contained in this document. Additionally, you confirm that you understand the risks related to the financial instruments discussed in this material.

Due to international regulations not all financial instruments/services may be available to all clients. You should be aware of and observe any such restrictions when considering a potential

investment decision. Past performance and forecast are not a reliable indicator of future results. The information contained herein has been obtained from internal and external sources and is

believed to be reliable as of the date in which this material was issued, however IBBAInt does not make any representation or warranty as to the completeness, reliability or accuracy of

information obtained by third parties or public sources. Additional information relative to the financial products discussed in this material is available upon request. Itau BBA International plc

registered office is 20th floor, 20 Primrose Street, London, United Kingdom, EC2A 2EW and is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct

Authority and the Prudential Regulation Authority (FRN 575225) – Itau BBA International plc Lisbon Branch is regulated by Banco de Portugal for the conduct of business. Itau BBA

International plc has representative offices in France, Germany, Spain which are authorised to conduct limited activities and the business activities conducted are regulated by Banque de

France, Bundesanstalt fur Finanzdienstleistungsaufsicht (BaFin), Banco de España respectively. For any queries please contact your relationship manager; (ii) U.S.A: Itau BBA USA

Securities, Inc., a FINRA/SIPC member firm, is distributing this report and accepts responsibility for the content of this report. Any US investor receiving this report and wishing to effect any

transaction in any security discussed herein should do so with Itau BBA USA Securities, Inc. at 767 Fifth Avenue, 50th Floor, New York, NY 10153; (iii) Asia: This report is distributed in Hong

Kong and Japan by Itaú Asia Securities Limited, which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities) regulated activity. Itaú Asia

Securities Limited accepts all regulatory responsibility for the content of this report. In Hong Kong, any investors wishing to purchase or otherwise deal in the securities covered in this report

should contact Itaú Asia Securities Limited at 29th Floor, Two IFC, 8 Finance Street – Central, Hong Kong; (iv) Middle East: This report is distributed by Itau Middle East Limited. Itau Middle

East Limited is regulated by the Dubai Financial Services Authority and is located at Suite 305, Level 3, Al Fattan Currency House, Dubai International Financial Centre, PO Box 482034,

Dubai, United Arab Emirates. This material is intended only for Professional Clients (as defined by the DFSA Conduct of Business module) no other persons should act upon it; (v) Brazil: Itaú

Corretora de Valores S.A., a subsidiary of Itaú Unibanco S.A authorized by the Central Bank of Brazil and approved by the Securities and Exchange Commission of Brazil, is distributing this

report. If necessary, contact the Client Service Center: 4004-3131* (capital and metropolitan areas) or 0800-722-3131 (other locations) during business hours, from 9 a.m. to 8 p.m., Brasilia

time. If you wish to re-evaluate the suggested solution, after utilizing such channels, please call Itaú’s Corporate Complaints Office: 0800-570-0011 (on business days from 9 a.m. to 6 p.m.,

Brasilia time) or write to Caixa Postal 67.600, São Paulo-SP, CEP 03162-971.* Cost of a local call.