breakingedge; a capco thought leadreship quarterly

DESCRIPTION

Articles and content developed by Capco thought leaders on banking, finance, and fintech.TRANSCRIPT

B R E A K I N G E D G E

Contents

01

02

03

A Future Unfolds: Welcome to Magic Banking

Heed ‘Em or Weep

Will Blockchain Kill Clearing?

Could your Bank Become your New BFF? 6

New Rules for Payments Innovation 12

Part I: Talkin’ ‘Bout a Revolution - The Promise of Blockchain

18

04 1007 13

05 1108 14

06 12 1509

Will Blockchain Kill Clearing? Machines vs HackersBiometrics. The Good, the Bad and the Ugly

Fedcoin

Trading Around Volcker If Bitcoin Behaves… History in the Making

Biometrics. The Good, the Bad and the Ugly

Devils in the Details Pruning Bank BranchesThe Reality of Virtual Reality

Part II: Fad or Financial Revolution? What’s Really Happening on the Street?

Has Cyber-security Exceeded the Limitations of Human Intellect?Part II: Considering the Cons -

Biometrics and Financial Services

A Better Bit?

A Trader’s Attempt at Gaming the System The Burgeoning of Blockchain Technology Payments March On

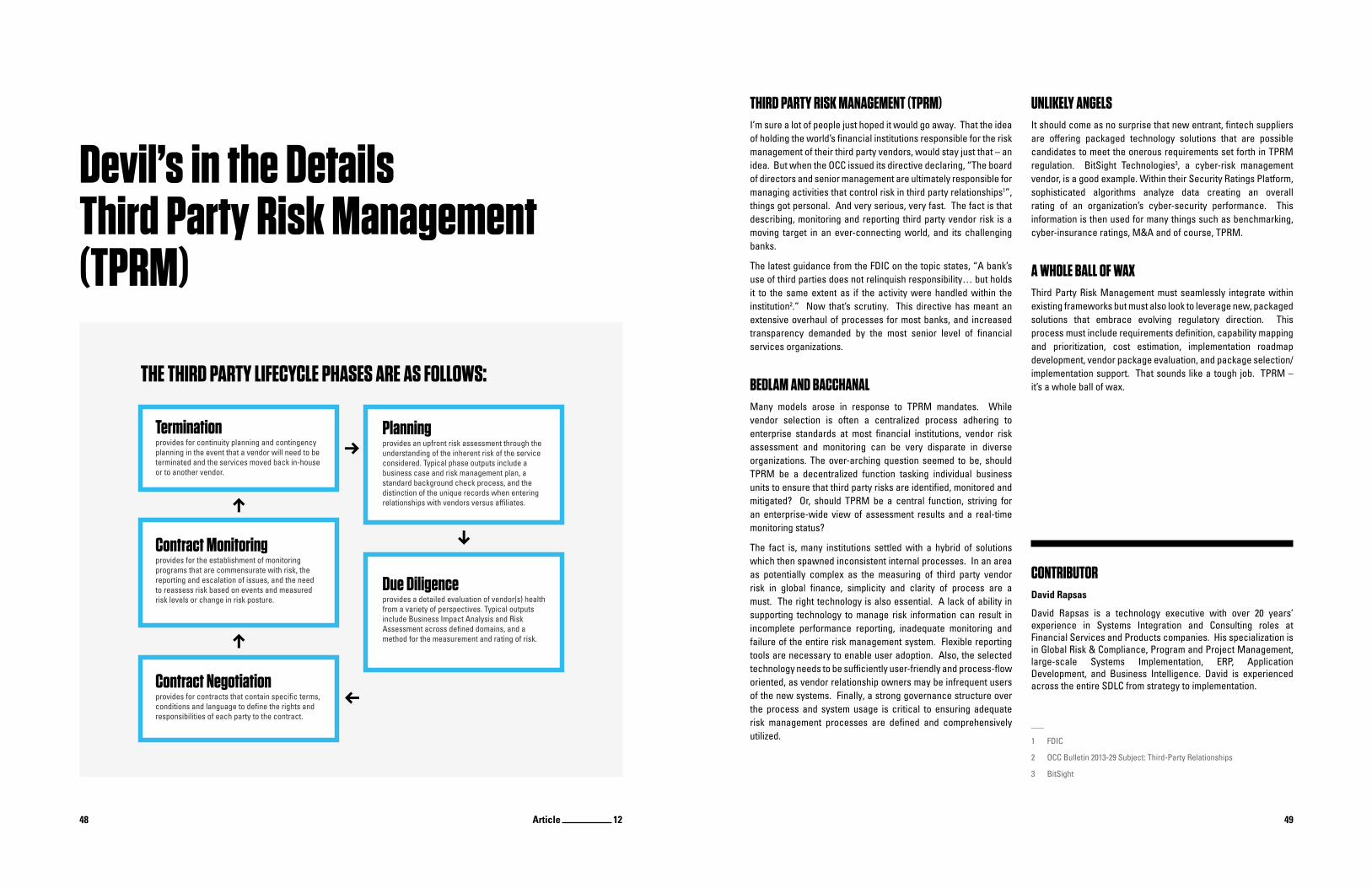

Part I: The Bounty of BiometricsThird Party Risk Management (TPRM) Good Business or Bad?

A Mindtrip for Banks

19 4234

52

24 44 56

3048 62

38

Biometrics. The Good, the Bad and the UglyPart III: The Ugly. Flies in the Ointment. What Determines the Success or Failure of Biometric Rollouts?

36

7 6

Experts predict that the home of the future will be so convenient, so connected, it will actually anticipate your desired environment, and deliver it. As you walk from room to room, everything about the space begins to change to please you, anticipating your wants and needs. Temperatures and lighting alter according to historic preferences, overlaid with information regarding present mood, determined biometrically. Even the artwork, they say, will change as you enter, based perhaps on your Pinterest1 account? Recent Google2 searches? Your heart rate?

It may sound like sci-fi at first, but if you think about the power of using data - and digital delivery - to tailor customer experience on a profoundly personal basis, you really start to think. What if

banks could give their customers so customized an experience,

so artfully presented, that they actually helped those customers

live better, and more simply? This, they say, is the future of

banking.

CLOSING THE GAPIn a recent consumer banking survey conducted by fintech giant FIS3, which spanned nine countries and 9000 subjects, consumers were impressed with their banks. They rated their banks above average in providing convenience and connectivity, seamlessly and uniquely. Not bad. Where customers needed more from banks, was in understanding their options dynamically, in a way that was easily digestible, to help them make the best decisions for their financial future, in real-time. If banks could continue on their, so far, successful digital journey, while at the same time rising to the occasion and providing pertinent, meaningful information to help people think, and plan - the future of financial services could get very interesting.

REAL LIFE BANKINGTake two simple, futuristic examples. In one, a typical New Yorker consistently promises to take the subway, but due to unforeseen drizzle, and a case of laziness, he usually hails a cab. When he pays with his watch, his bank realizes that this is his third 8 am cab ride in three days, and assists him in analyzing his present behaviors and future goals. If he chose to grab a cab each morning and evening for the remainder of his career, the long-term estimated cost, presented by his bank, would be almost $250,000. This, in turn, would push back the age at which he could retire by 18 months! Conveniently, his bank also informs him of a ride-share arrangement around the corner, at a fraction of the price of a cab.

Or let’s say you’re away for the weekend with your partner, and can’t help but peruse real estate in the bucolic setting. At dinner you ask your bank, “Could I ever afford a house in the country?” Based on your GPS, recent Zillow searches4, and applying a conservative percentage of disposal income to the options, your

A Future Unfolds: Welcome to Magic Banking. Could your Bank Become your New BFF?

bank delivers you property ideas in the area, within your means, reflecting your likes and interests. And since your bank helps you to save money, and realize your long-term financial aspirations, you are probably going to give them the wealth management, or mortgage business you’re considering. And so it goes. You do more business with your bank, they get more information, products get more customized, you do more business with your bank - and so on, and so forth.

Let’s face it. For banks to compete and succeed in finance’s future, long-term, trusted-advisor relationships are a must-have. If banks can continue to deliver on digital, and use those channels to forge closer personal relationships, it’s a win-win. Financial services are about to move, from banking to living.

Article 1

9 8

“ What if banks could give their customers so customized an experience, so artfully presented, that they actually helped those customers live better, and more simply? Financial services are about to move, from banking, to living.”

Article 1

11 10

CONTRIBUTORBethel M. Desmond

Bethel M. Desmond is a veteran Wall Street executive, presently responsible for driving the thought leadership function at Capco, a leading financial services consultancy. Beth’s career began on the front lines as a commodity derivatives trader at leading banks and trading houses throughout the industry. Drawn into advisory roles due to changing industry regulations, Ms. Desmond moved into strategic consulting and has worked in senior positions for the Big Four firms internationally. A finance writer at heart and by training, Beth wrote for The Economist before her current role and has been published in the Wall Street Journal. Beth is an accomplished business writer, a talented facilitator and a strong public speaker with deep experience in the creation, production and marketing of thought leadership work and finance reporting.

__

1 pinterest.com2 google.com3 closethegaps.fisglobal.com4 zillow.com

GLOBAL PERFORMANCE GAPS BY ATTRIBUTE IMPORTANCE

LOWER IMPORTANCE AND OUTPERFORMING EXPECTATIONS

HIGHER IMPORTANCEAND UNDERPERFORMING

EXPECTATIONS

MOST IMPORTANT

IMPORTANCE

Anticipates

Leading-edgeproducts

Immediate

In-personservice

Digital payments

LEAST IMPORTANT

OUTPERFORMING EXPECTATIONS

Omnichannel

Connected

Simplicity

Recognition

Customized

AspirationsAdvice

Fairness

Safety

Security

Reliable

Transparent

Control

PERF

ORMA

NCE

UNDERPERFORMING EXPECTATIONS

“ If banks can continue to deliver on digital, and use those channels to forge closer personal relationships, it’s a win-win. ”

Article 1

13 12

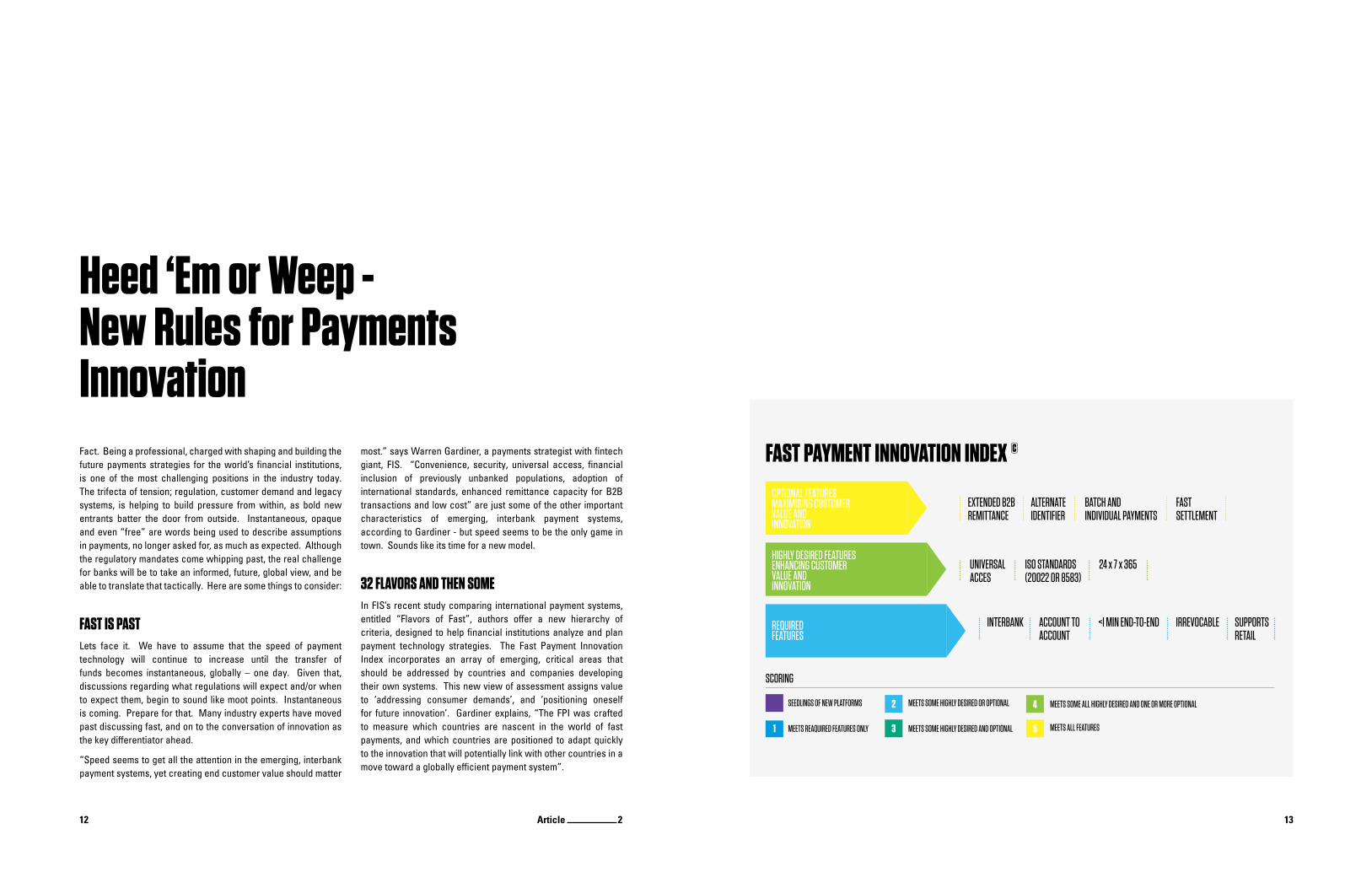

Fact. Being a professional, charged with shaping and building the future payments strategies for the world’s financial institutions, is one of the most challenging positions in the industry today. The trifecta of tension; regulation, customer demand and legacy systems, is helping to build pressure from within, as bold new entrants batter the door from outside. Instantaneous, opaque and even “free” are words being used to describe assumptions in payments, no longer asked for, as much as expected. Although the regulatory mandates come whipping past, the real challenge for banks will be to take an informed, future, global view, and be able to translate that tactically. Here are some things to consider:

FAST IS PASTLets face it. We have to assume that the speed of payment technology will continue to increase until the transfer of funds becomes instantaneous, globally – one day. Given that, discussions regarding what regulations will expect and/or when to expect them, begin to sound like moot points. Instantaneous is coming. Prepare for that. Many industry experts have moved past discussing fast, and on to the conversation of innovation as the key differentiator ahead.

“Speed seems to get all the attention in the emerging, interbank payment systems, yet creating end customer value should matter

most.” says Warren Gardiner, a payments strategist with fintech giant, FIS. “Convenience, security, universal access, financial inclusion of previously unbanked populations, adoption of international standards, enhanced remittance capacity for B2B transactions and low cost” are just some of the other important characteristics of emerging, interbank payment systems, according to Gardiner - but speed seems to be the only game in town. Sounds like its time for a new model.

32 FLAVORS AND THEN SOMEIn FIS’s recent study comparing international payment systems, entitled “Flavors of Fast”, authors offer a new hierarchy of criteria, designed to help financial institutions analyze and plan payment technology strategies. The Fast Payment Innovation Index incorporates an array of emerging, critical areas that should be addressed by countries and companies developing their own systems. This new view of assessment assigns value to ‘addressing consumer demands’, and ‘positioning oneself for future innovation’. Gardiner explains, “The FPI was crafted to measure which countries are nascent in the world of fast payments, and which countries are positioned to adapt quickly to the innovation that will potentially link with other countries in a move toward a globally efficient payment system”.

FAST PAYMENT INNOVATION INDEX ©

EXTENDED B2B REMITTANCE

ALTERNATE IDENTIFIER

BATCH AND INDIVIDUAL PAYMENTS

FASTSETTLEMENT

INTERBANK

SEEDLINGS OF NEW PLATFORMS

SCORING

MEETS REAQUIRED FEATURES ONLY

MEETS SOME HIGHLY DESIRED OR OPTIONAL

MEETS SOME HIGHLY DESIRED AND OPTIONAL MEETS ALL FEATURES

MEETS SOME ALL HIGHLY DESIRED AND ONE OR MORE OPTIONAL

ACCOUNT TO ACCOUNT

<I MIN END-TO-END IRREVOCABLE SUPPORTSRETAIL

UNIVERSAL ACCES

ISO STANDARDS (20022 OR 8583)

24 x 7 x 365

OPTIONAL FEATURESMAXIMISING CUSTOMERVALUE AND INNOVATION

HIGHLY DESIRED FEATURESENHANCING CUSTOMERVALUE AND INNOVATION

REQUIREDFEATURES

1

2

3

4

5

Heed ‘Em or Weep - New Rules for Payments Innovation

Article 2

15 14

“ Fact. Being a professional, charged with shaping and building the future payments strategies for the world’s financial institutions, is one of the most challenging positions in the industry today. ”

Article 2

17 16

CONTRIBUTORSTommy Marshall, Partner

Tommy is a partner in the Banking and Wealth Management practice at Capco. His passion for consumer finance, payments, and wealth management has been fulfilled through over 15 years of successful management consulting engagements. Tommy seeks out and thrives in the midst of transformation initiatives. He is currently playing a role in the evolution of digital financial services across the enterprise and the reengineering of the payments capability at some of the world’s largest financial institutions.

Tim White, Managing Principal

Tim White has over 25 years experience as a manager and consultant to the financial services industry. He has worked extensively with some of the largest retail banks in North America with engagements ranging from strategy-related initiatives to transformational programs that involve either outsourcing or insourcing functions that extend the clients capabilities. Tim holds an MBA from Northwestern University Kellogg School of Management and a Bachelors degree from the University of Texas at Austin.

IMPLEMENTING INFINITYRolling-out new payment systems is not a minor task, and yet the obstacle does not offer an easy way around. The electronic payment systems that were designed for the world’s banks in previous decades, can no longer serve a society where devices with enormous computing power are literally in the hands of most individuals. That is for certain. And yet a program to deliver the depth of change necessary would have implications for every aspect of payment system design, development, implementation, maintenance and customer service. The checklist of activities that must continue consistently, and yet advance seamlessly include, but are not limited to: detection of real-time fraud and money-laundering, sophisticated routing decisioning, automation of exception management processes, flexibility to meet changing regulatory requirements, and the reliability and scalability to ensure 24x7x365 service. This type of transformation is not for the faint of heart.

“...WITH A LITTLE HELP FROM MY FRIENDS”The development of a domestic payment system that is worthy of an FPII rating of 5 is a multi-stage process, best achieved by partnering with experienced, payment subject matter experts. Management must be very clear that it will be necessary to adopt a multi-year plan that involves a current state assessment, target operating model, roadmap defining stages and deliverables of program. Capco Payments Partner, Tommy Marshall shares, “The partnership is key here. Programs of this complexity, involving competing stakeholders with differing priorities, makes the implementation of an optimal, viable solution all the more difficult.” Marshall reports “My clients tell me that an experienced partner is valuable in steering conversations and work efforts around previous lessons learned, and providing credibility and objectivity outside of organizational silos.” The industry is proving that when all stakeholders co-operate in true partnership, much can be achieved. The future of fast payments systems will take a village.

THE QUESTIONS 1. What are the challenges that our existing customers have in making

and receiving payments and in managing payments information?

2. How can we leverage our fast payment system in order to solve those problems?

3. How will fraudsters attempt to take advantage of the specific characteristics of the fast payment system?

4. What kind of dispute management capabilities do we need in order to handle transactions that are either erroneous or fraudulent, in spite of the irrevocable nature of fast payments?

THE CHALLENGES1. The challenge of internal integration with legacy systems that tend

to be batch oriented and not designed to handle a continuous flow of messages and responses, 24x7x365.

2. The needs for changes to the bank’s infrastructure to support payment processing within seconds on a reliable basis, including staffing, hardware and services designed to ensure high availability.

3. An entirely new paradigm of multi-channel customer experience that is required to manage the end-to-end initiation and confirmation of payments within seconds, including the potential for payment rejection when the bank on the receiving end is unable to validate and confirm.

4. What kind of dispute management capabilities do we need in order to handle transactions that are either erroneous or fraudulent, in spite of the irrevocable nature of fast payments?

THE GOALS1. Make the initiation and receipt of non-automated payments easier and

less expensive.

2. Facilitate the entire transaction value chain – helping the end customer to make purchasing, delivery and financing decisions.

3. Enhance payment information flows to make it easier for customers to efficiently reconcile their financial accounts, easily retrieve historical activity and conduct trend analysis to better inform budgeting and forecasting.

“ Speed seems to get all the attention in the emerging interbank payment systems, yet creating end customer value should matter most.” says Warren Gardiner.

Article 2

19 18

PART 1: “TALKIN’ ‘BOUT A REVOLUTION – THE PROMISE OF BLOCKCHAIN”Think about this. When I started commodity derivatives trading in the 80’s on Wall Street, I booked trades by writing up tickets. Archaic I know, but it’s the honest truth. Each commodity had a code (AU for Gold), and each futures contract had a symbol for the month (Q for August). When I wanted to sell August Gold, I would take out a ticket, circle ‘S’ for sell, write AUQ and the volume, and then, get this, time stamp it, and throw it in a basket. At the end of the day I would go through the trades, rip off the top copy for my records, and take the carbon copies left to the ‘back of the office’ where hopefully they would be processed into the bank’s central system. Seems absolutely antiquated I know, but yet, what if blockchain technology is about to make us feel that

way about how we process trades today? Could blockchain be about to change the way we trade?

PASSED PAYMENTSWhere Bitcoin and other digital currencies have captivated the imagination of audiences initially, we are now seeing a compelling shift of focus to Bitcoin’s more promising attribute – its underlying blockchain technology. We first started to hear the buzz in the payments space. Current payment systems used in the majority of the world are based on technology that is over 40 years old, called Automated Clearing House or ACH. ACH technology batches transactions together and sends them out to be cleared in set intervals of time, which is why most bank transactions historically took 2- 4 days to go through.

But times are changing, customers want more and regulators are demanding transparency and speed. By integrating blockchain technology in modern day banking, transactions are now being cleared instantly, cheaply, and more securely. When industry hitters like CIO of Swiss Bank, Oliver Bussmann, say, - “It is my personal prediction that blockchain technology will not only change the way we do payments, but it will change the whole trading and settlement topic*.” - people start to listen.

TRANSFORMING TRADING?In theory, the decentralized system of blockchain for verifying information means transactions need no longer be channeled through banks, clearing houses or other third parties. This “trustless” structure means that direct transfers of ownership can occur, over the blockchain, almost instantaneously without the risk of default or manipulation by an intermediating third party. Imagine what this reduction in friction could mean for cost savings, improved processing and elimination of counter-party exposures.

This new approach to the old concept of keeping ledgers presents exciting potential in its ability to massively reduce the cost and time to clear and settle the exchange of financial assets. However, how will incumbent banks, exchanges and clearing houses respond to this transformational technology? One thing’s for sure, the game just got more interesting. It remains to be seen, if and how, traditional market facilitators will react. Will present industry players be able to make blockchain their new BFF, or will they risk being shook up by new entry startups?

Will Blockchain Kill Clearing?CONTRIBUTORSGeraldine Balaj

Geraldine Balaj is a Principal Consultant in Technology at Capco with a long career serving the Financial Services industry specializing in designing enterprise level solutions for highly complex business issues. Possessing both technology expertise and keen Capital Markets knowledge, Geraldine specializes in large-scale platform redesigns from a top-to-bottom perspective. Her most recent projects include a complex national transformation of Wealth Management entity to a correspondent clearing model and front to back design of a complex cross product portfolio margin solution for a top tier bank. She has also served as the primary solution owner for several platform redesigns for numerous national stock exchanges.

Tim Jennings

Tim has spent over 20 years in the Capital Markets arena working mainly with the primary market makers for FX, Equity, Precious Metals and Interest Rate Derivatives. He has worked as a partner with Front Office Trading personnel for all that time. His experience has also covered Middle Office functions, working on initiatives from opening new branches for a global FX options trading division and consolidating regional FX trading centers around the world onto a single, global, trading platform for a major bank. He worked as a senior business analyst for Murex integration and implementation initiatives at various financial institutions. In addition, Tim has extensive testing experience from Unit Testing, SIT, UAT through to Regression Testing. Consultancy has given him the opportunity to use his knowledge and experience in divergent business environments.

Mei Ling Liew

Mei Ling is a Managing Principal at Capco, specializing in derivative products. She has achieved considerable success in trading systems implementation, derivative pricing and risk analysis. She has worked within the Front/Middle Office functions of the Investment banking industry for several years where she has gained over 15 years’ experience. Her experiences include Capital Markets, Interest Rate Derivatives, Credit Derivatives, Equity Derivatives and FX Derivatives.

“ Where Bitcoin and other digital currencies have captivated the imaginations of audiences initially, we are now seeing a compelling shift of focus to Bitcoin’s more promising attribute – its underlying blockchain technology.”

___

* Blockchain Project Aims to Bring Speed, Transparency to Wall Street Trading

www.coindesk.com/blockchain-technology-to-improve-outdated-wall-street-trading/

Blockchain Technology Can Significantly Simplfy Modern Banking

www.cryptocoinsnews.com/blockchain-technology-can-significantly-simplify-modern-banking/

Coinsetter Unveils Project High Line: On-Blockchain Trade Settlement

www.coinsetter.com/blog/2015/02/25/coinsetter-unveils-project-high-line/

Article 3

21 20

PART II: “FAD OR FINANCIAL REVOLUTION? WHAT’S REALLY HAPPENING ON THE STREET”Adapting blockchain technology to enhance legacy post trade processing and asset servicing is quickly becoming a reality on Wall Street. Banks and other financial services firms are investing time and money to determine the best adaptation of blockchain technology into their enterprise strategies. One example is what’s going-on over at Coinsetter. Coinsetter, a global Bitcoin exchange based in New York City, recently announced a new venture called “High Line” that aims to improve how trades across Wall Street are cleared and settled through the application of Bitcoin’s blockchain technology1. Their new “On-Blockchain Settlement” system attains a never before seen level of stark transparency.::

A ‘TRUSTLESS’ SYSTEMCurrently, most trades in the industry involve numerous intermediaries who reassign ownership of assets utilizing slow, opaque and outdated technology. They also rely on bank transfer systems to settle payments for trades, which are limited at best. By introducing blockchain’s transparent, decentralized, public ledger into the trade settlement process, Project High Line can provide line-of-sight view of funds for users, after trades are executed. No middleman, or account balance on a website, will be necessary to verify location or ownership of funds.

Project High Line supplants old transaction rails, allowing users to opt-in to a system that ensures their funds are exactly where promised. Coinsetter CEO, Jaron Lukasiewicz, says that the project is a “shift from the status quo on Wall Street”. It aims, says Lukasiewicz, “to solve the problem of having to place trust in an exchange or intermediary, while also allowing market participants to have full visibility into trade settlement, as well as tangible access to moving their assets 24/7”. ‘On-Blockchain Settlement’ is currently in the process of also binding trade execution directly to transactions on the Bitcoin blockchain. These are important advancements in an evolving industry.

NEXT UP - NASDAQ Nasdaq OMX Group Inc. is also launching an official pilot program, and appointed a ‘Blockchain Technology Evangelist’, VP Fredrik Voss, to lead ‘proof of concept’ strategic development for several applications of “blockchain-esque” technology to trading platforms. If the effort is deemed successful, Nasdaq plans to use ‘customized blockchain technology in its stock market, one of the world’s largest, which would galvanize other market participants and vendor systems to shake up systems that have facilitated the trading of financial assets for decades’2. According to Robert Greifeld, Nasdaq CEO, “Utilizing the blockchain is a natural digital evolution for managing physical securities.” The technology, he says, “holds the potential to benefit the broader global capital markets community.”

Nasdaq’s foray is significant because it marks one of the first times a large, multinational financial services company is leveraging blockchain technology in a non-currency manner. The company’s first application will provide a fully electronic, distributed, ledger-style solution for accurate record keeping, which will ‘modernize, streamline and secure typically cumbersome administrative functions’ . The pro for its customers, according to the exchange, is that it will simplify the overwhelming challenges private companies face with manual ledger record keeping.

AND THE LIST KEEPS GROWING…Every week we are hearing about more financial institutions arriving to the blockchain, block party. The New York Stock Exchange and Goldman Sachs Group Inc. are investing in blockchain oriented service systems. New startup, Digital Asset Holdings, led by former J.P. Morgan Chase & Co. executive Blythe Masters, like Nasdaq, is also developing a blockchain-based system for settling transfers of securities and funds. According to Mei Ling Liew, a Managing Principal at leading financial services consultancy Capco, new requests from clients to help tailor blockchain solutions to meet their needs and give them a competitive advantage, are steadily on the rise.

“We are working with clients on long-term, strategic road mapping for design, implementation and cost measurement of blockchain initiatives.” says Liew. “At Capco, we saw this revolution coming

___

1 www.coinsetter.com/blog/2015/02/25/coinsetter-unveils-project-high-line/

2 Nasdaq Launches Enterprise-Wide Blockchain Technology Initiative

3 Blockchain Technology - A Threat to, or an Opportunity for, Legacy Banking, Clearing & other Financial Services?

4 www.nasdaq.com/press-release/nasdaq-launches-enterprisewide-blockchain-technology-initiative-20150511-00485

bitcoinbytes.blogspot.com/p/blog-page_1.html

Nasdaq’s blockchain pilot spells the beginning of the end for lawyers

www.ibtimes.co.uk/nasdaqs-blockchain-pilot-spells-beginning-end-lawyers-1500656

Will Blockchain Kill Clearing?down the pike for our clients across the financial services value chain. We purposely got involved early on in helping launch one of the first, and only, U.S. Regulated Bitcoin Exchanges, just to build our knowledge and contacts in the blockchain marketplace. That investment is really paying off. It feels great working with clients to help them transform their offerings with the application of this inspiring, emerging technology.”

instantaneous confirmation & settlement simplified dodd frank reporting via real time auditing transactions posted to the blockchain

lack of need to warehouse ‘physical’ assets but rather record securely using blockchain technology

reduced counterparty and delivery risk

immediate pricing transparency from point of execution

reduced indirect transaction costs

enhanced settlement security reduced in back office operations overhead

increased market liquidity with immediate settlement

OTHER MAJOR AREAS OF ENHANCEMENT INCLUDE BUT ARE NOT LIMITED TO

Article 4

23 22

“ Where Bitcoin and other digital currencies have captivated the imaginations of audiences initially, we are now seeing a compelling shift of focus to Bitcoin’s more promising attribute – its underlying blockchain technology.”

Article 4

25 24

The looming Volcker Rule is poised to be the key piece of financial regulation to decisively end Wall Street trading as we know it. With banks expected to comply, beginning for some by July 2015, the industry is getting dead serious about understanding exactly what compliance will look like. Virtually all trading desks across business lines will be impacted, and right now banks on Wall Street are facing the risk of wide gaps between comprehensive compliance programs, and everyday business implementation realities.

SOUNDS LIKE…VULTUREFrom the trader’s point of view, Volcker sounds more like “vulture” every day, as it picks the bones of proprietary trading clean. This 300-page document should send shivers down the spine of any trader, who actually had the time or appetite to read it. In short, the Volcker Rule slaps a saddle on the back, and a bit in the mouth, of the trader and leads him, tethered and silenced, away from any inkling of proprietary trading or position taking toward a pure, customer-only driven, agency trading model. Can modern trading desks survive this type of leashing in a market where regulation will slash margins and substantially increase trading costs, or are we witnessing the last breath of Wall Street Swagger?

Trading Around Volcker; A Trader’s Attempt at Gaming the System

HERE’S HOW VOLCKER CATCHES ‘PROP TRADING’Regulators have gone to great lengths to attempt to assure through Volcker, that no profits are made across the nation’s FDIC insured bank trading desks, from a trader’s “view of the market”. That, in their opinion, is what got us into trouble in the first place. Washington has spent quite a bit of time deciding on the metrics to determine when proprietary (prop) trading is evidenced, and plan on actively enforcing limits on such activity. Not only does the Volcker rule not want you to lose money “betting” on market trends, it doesn’t want you to make any money either. And here’s how they plan to catch you.

The Volcker Rule requires that all market participants falling under its jurisdiction report trading activity using 17 different indicators, that loosely fall into 4 categories, covering revenue-based metrics, revenue to risk metrics, inventory metrics and customer flow metrics. By looking at such things as Daily Profit and Loss Volatility, Daily VaR Volatility, Open Inventory and Customer Flow Trade numbers, the folks at various federal agencies (including the Fed, FDIC, OCC and SEC) are out to see who’s been naughty or nice, and they intend to look quite closely.

Volcker Rule - Proprietary Trading

NO

NO

YES

YES

NO

Is a banking entity engaged in proprietary trading under the volcker rule?• Is the principal position a “covered financial position”?• Is the account a “trading account”?

• Market Making-Related Activities

• Underwriting Activities• Risk-Mitigating Hedging

Activities

Is the activity precluded by a backstop prohibition? Material conflict of interest between the banking entity and its

clients, customers or couterparties?• Material exporsure of the banking entity to high-risk assets or

trading strategies?• Threat to the safety and soundness of the banking entity or U.S.

financial stability?

• Trading in Government Obligations• Trading on Behalf of Customers• Trading by a Regulated Insurance

Company• Trading Activities of Foreign Banking

Entities Outside the United States

ACTIVITY IS NOT PROPRIETARY TRADING, AND NOT WHITHIN THE

SCOPE OF THE VOLCKER RULE

ACTIVITY IS PROHIBITEDPROPRIETARY TRADING

ACTIVITY IS PERMITTEDPROPRIETARY TRADING

TIERED COMPLIANCE PROGRAM AND REPORTING REQUIREMENTS APPLY

Is proprietary trading explicitly permitted under the volcker rule?

YES

Step

3

Step

2

Step

1

Article 5

27 26

CONTRIBUTORJennifer Liu

Jennifer Liu is a Principal Consultant in Capco Capital Markets practice. She has over 11 years of business strategy and initiative implementation experience within the financial services industry, including Capital Markets, Corporate and Investment Banking, and Retail Banking. Her current focus is on market infrastructure development in the new era, post-financial crisis.

__

1 Federal Register / Vol. 79, No. 21 / Friday, January 31, 2014 / Rules and Regulations

http://www.occ.gov/news-issuances/federal -register/79fr5536.pdf

2 Study & recommendations on prohibitions on proprietary trading & certain relationships with hedge funds & private equity funds

http://www.volckerrule.com/docs/Tab.14.FSOC%20Study.PDF http://www.volckerrule.com/proprietary/prop_files/gif_2.gif

LOOKING FOR LOOPHOLESAt first read, through the eyes of a trader, one might be encouraged, as the rule seems to give a tad of flexibility in its interpretation. Those in the trenches might be a bit buoyed in believing that perhaps there may be a way around this troll at the bridge. The remaining optimists would be smart to look again, however. Volcker knows your game and is talking severe punishments for violators that dare to push the boundaries of this prop-trading killer.

BIG BROTHER IS WATCHING - YOUR BID/OFFERSFor instance, under the rule there exists an exemption for “market making” which is described as a bank being “willing to buy and sell and quote markets on a continuous basis”1. This is essential for liquidity, and a must to ensure a well-oiled, trading machine and marketplace. But, any trader worth their salt knows that there are quotes and then there are quotes. If I were a trader, wanting to look like I was complying with Volcker but in actuality wanting to take on a long position, my “bid” quote might just so happen to be a lot better than my “offer” quote. As such, my buy quotes might get hit with much more frequency than my sell quotes and before you know it - I am long - even though I have kept “continuous quotes” in the market as per Volcker. Voila! A legitimate way around the regulations!

But not so fast. The federal agencies did not invest in hiring would be and ex-post traders for nothing. Let’s see what the Financial Oversight Committee (FOSC), in charge of birthing Volcker, has to say about such practices - “where a market maker posts continually at or near the best bid, but does not also post at or near the best offer, the market maker‘s activities would not generally qualify as bona fide market making for purposes of the market making exception”2. Gotcha - Big Brother is watching.

THINK AGAIN Let’s take another loophole and see if we can hang ourselves. Under Volcker, amassing a position, or “acquiring inventory and maintaining risk exposures to satisfy current or expected customer demand” is permissible. It is seen as a necessary evil of market making, or responding to customer needs to run your agency flow business. If I were trading and wanted to get long based on my view of the market however, I might “acquire my

inventory to satisfy expected customer demand and then - “oops - excuse me, Commissioner - my customer didn’t come in with the demand I thought he would or with the volume expected so looks like I was off on my idea of “expected customer demand” - but I was definitely NOT proprietarily trading - no sir - and I wasn’t doing it last week either!” Think again. On this subject the FSOC recognizes and documents, “proprietary traders that build inventory, but do so with the expectation that inventory will appreciate in the near term, rather than using the inventory to facilitate customer transactions as would a market maker” are using “practices that are clearly prohibited”. Bam!

CLARITY ON CHANGEBut the directives around Volcker are not always crystal clear, making it difficult to set policy and guide employee protocols. The FSOC itself admits, “The ability to hold inventory in this context is a principal complexity: the same inventory built with the intention of facilitating liquidity for clients could also be built with the intention of engaging in impermissible proprietary trading and discerning between the two is a key challenge in implementing the Volcker Rule.” So the problem for the financial industry is two-fold; first, gaining a clear understanding of exactly what is being demanded from Washington and second, actually changing behaviors.

Changing behaviors to this degree involves attempting to change the risk culture of an organization, which is extremely different than merely changing a risk limit or risk reporting. Let’s face it, most people are on a trading desk because it is in their nature to take risk and that’s why they choose their jobs. The fact that Volcker now is changing the game will leave institutions clamoring to explain the new roles to their trading staff. The fact

“ From the trader’s point of view, Volcker sounds more like “vulture” every day, as it picks the bones of proprietary trading clean. ”

that Volcker restricts “incentive-based compensation based on risk-taking” does not help matters. From a trader’s point of view, first they take the fun, and then they take the money.

VAST AND INTRICATEAt Capco, a leading financial services consulting firm, client needs regarding complying with Volcker have become so vast and intricate, the consultancy has created a Global Volcker Center of Excellence. “Our clients rely on us to bring a deep knowledge of bank operations to bridge the gap between high level interpretation and individual desk implementation.”, says Capco’s Jennifer Liu. “We work very closely with them to drive a target operating model that will optimize desk structures, operational processes and infrastructural alignment, in addition to refining reporting practices. There is nothing simple about Volcker.” Complying with Volcker will be a difficult path for most banks. Clarifying the change necessary to comply will be the first step in a long journey.

Article 5

29 28

“ In short, the Volcker Rule slaps a saddle on the back, and a bit in the mouth, of the trader and leads him, tethered and silenced, away from any inkling of proprietary trading or position taking toward a pure, customer-only driven, agency trading model. ”

Article 5

31 30

PART I: THE BOUNTY OF BIOMETRICSAccording to the Association of Certified Fraud Examiners (ACFE), U.S. organizations lose an estimated 5% revenue to fraud every year. Five cents on every dollar has a way of really adding up. Based on projected U.S. Gross World Product, fraud costs will enter the trillions1 for US businesses, with no signs of stopping. As millions of customers migrate onto digital infrastructures for their shopping and banking needs, fraud and cyber-crime have officially become a major concern for financial services institutions.

In a recent global study by the industry’s largest financial technology provider FIS2, findings show that safety and security are the top priority for bank customers, including protecting their personal identities. Currently, the survey results indicate, that financial services consumers feel banks are failing slightly in this area. If cyber-security slips, it could become a key differentiator in deciding customer loyalty and continued business. When The Wall Street Journal reports a 10% annual increase in cyber-security by “critical infrastructure industries”3, people sit up and listen. This folks, is big business. Can biometrics save the day?

WILL BIOMETRICS RETURN BANKS BILLIONS?Biometrics is the science and technology of measuring and analyzing biological data. Data encompasses things such as DNA, fingerprints, eye retinas and irises, voice patterns, facial patterns, hand measurements and more. The data, or combinations of the data, uniquely identify an individual for authentication purposes. Automatic recognition of an individual through their behavioral or physical characteristics is not new technology. Facial

Biometrics; The Good, the Bad and the Ugly

recognition technology has been used for over 20 years. Yet, with the screaming pace of technological advancement, biometric uses and systems have been improving - at lightening speeds. Fraudulent access, and the unauthorized usage of bank accounts by international crime syndicates, is robbing unprecedented amounts from banks. Unique authentication methods through the use of biometrics have therefore become a prominent agenda item for institutions looking to take an innovative and defensive strategy against white-collar, financial criminals.

GOVERNMENT LEADING BANKS IN BIOMETRICS?Banks, however, are lagging behind other industries in developing biometric solutions, while governments are already adopting biometric technology on a large scale. The US, UK and Canadian governments presently use biometrics at their border entry and exit points. The Unique Identification Authority of India is in the process of issuing everyone in that country (1.3bn people) biometric registered ID cards, and exposing APIs to this data. Not only will this help the government identify people, but it will also help provide banking services to the unbanked, by enabling verification for each and every individual user on the system.

FROM CONCEPT TO CUSTOMERThe widespread use of biometrics by governments will accelerate the use of this technology by other industries, including financial services. Banks are already rolling out fingerprint, voice and facial recognition methods for authenticating users. As the technology improves and adoption increases, we expect to see biometric authentication become the industry norm for the

CONTRIBUTORSJibran Ahmed

Jibran Ahmed is a Principal Consultant in Capco’s London office. He has over 6 years’ experience in program management, defining target operating models and stakeholder management in the investment banking industry.

Owen Priestley

Owen Priestley operates as Capco’s Chief Connecter and is a member of the North American Digital leadership team working in new product development and as a Consultant for Capco for over 6 years.

___

1 Report to the Nations on Occupational Fraud and Abuse http://www.acfe.com/rttn/docs/2014-report-to-nations.pdf Customer Loyalty Does Not Translate to Cross-sales for Community Banks

2 ttp fisglo al co custo erlo alt inde t Unique Identification Authority of India https://uidai.gov.in

3 Companies Wrestle With the Cost of Cybersecurity http://www.wsj.com/articles/SB100014240527023048347045794034215397

34550

4 No Password, No Problem: FIS Adds Biometric Access to Mobile Solutions ttp fisglo al co

5 US Navy sees 110,000 cyber attacks every hour, or more than 30 every single second

http://thenextweb.com/us/2012/12/05/us-navy-sees-110000-cyber-attacks-every-hour-or-more-than-30-every-single-second/

authorization of banking services. FIS announced that it would be providing biometric access to its more than 30 million mobile banking users, via Apple’s touch ID. With this innovation, FIS was the first provider to offer fingerprint access and “Cardless Cash” to banks and their customers when the ATM authentication went live in April of this year4. The use of this two-factor authentication – your mobile device and your fingerprint – combines to confirm identities with far superior results than historically possible. And from there, the possibilities seem endless.

FACING THE RISING THREATUnauthorized access to online information has become increasingly common over the past decade, and is a major concern for both banks and their customers. The US Navy alone maintains a network of over 800,000 men and women at 2,000 locations around the world to protect against of 110,000 cyber-attacks every hour. That’s 30 every second!5 Experts are hoping that the introduction of biometric technology will become a major help in ensuring security.

HOW DOES IT WORK?While it’s been proven that fingerprints can be spoofed, it’s not easy – certainly not as easy as peeping over someone’s shoulder to get their PIN or password. Voice, facial and iris recognition are even more difficult to fake and would require significant skill and determination to fraudulently overcome. Future biometric technologies – such as electrocardiogram (ECG) recognition, which measures and records your heart beat pattern – will be nearly impossible to fool. Combining more than one of these methods together will lead to an almost foolproof approach to correctly identifying and authenticating individual users. Biometric technology will drastically decrease the chances of someone fraudulently accessing a customer’s bank account, and could eliminate identity theft altogether.

IMPROVING ODDS OVERALLBiometrics can’t stop the proverbial, ‘holding a gun to someone’s head and forcing them to log onto an account’ scenario, but what it can do is prevent fraud caused by millions of criminals stealing credit cards, PIN numbers and passwords. That alone will dramatically reduce cases of online fraud. To really prevent identity fraud however, biometrics need to be integrated into all aspects of banking – not just access to online and mobile

accounts. That means biometric authentication should also be used when a customer walks into a branch, when they use their credit cards in a store and even when they make payments on retail websites. That way, a fraudster can never pretend to be you or spend your money in any instance without a detailed, biometric signature. The sooner banks sign on, the better. Providing security in an ever expanding cyber world will not be a small responsibilityStay tuned for Part II of “Biometrics: The Good, The Bad and the Ugly”. Next we will assess the possible dangers of a biometric world in Considering the Cons - Biometrics in Financial Services.

Article 6

33 32

“ Unique authentication methods through the use of biometrics have therefore become a prominent agenda item for institutions looking to take an innovative, and defensive, strategy against white-collar, financial criminals.”

Article 6

35 34

PART II: CONSIDERING THE CONS - BIOMETRICS AND FINANCIAL SERVICESIn Part I of our series “Biometrics; The Good, The Bad and the Ugly” – “The Bounty of Biometrics”, we explored the many plusses of biometrics for the financial services industry – improved security, lower identity theft, vast cost re-capture. But do biometrics also carry potential negatives for big banks and their customers? One con to consider is this: where will all the criminals go? As biometrics make it more difficult for criminals to pretend to be someone they’re not, and steal from private citizens, it could force sophisticated crime syndicates to target bank systems directly instead. A rise in hacking and cyber-attacks on financial institutions has already begun. Cyber crime is more organized than ever before and more than 50% of attacks now focus exclusively on financial and e-commerce services1.

TARGETING BANKS WITH POISON ARROWSThere are a number of different ways that criminals are trying to target financial institutions. One is through social engineering exploits, which include when an end-user receives e-mail, supposedly from their bank, asking them to confirm their account information. Cyber criminals then use the information to gain

access to the user’s financial records and banking accounts. Malware is another weapon. In these instances, criminals distribute malicious software to trick users into installing programs on their device. When an end-user then enters their credentials, the program can capture all of the information, allowing criminals to gain access to the account. Industry cyber security experts claim that they see about 120 million new types of malware every month1! And that’s not all. Phishing attacks are also on the rise. These tactics target the

bank employees, tricking them to download malware that lies dormant in the bank’s internal systems. When the criminal wants to capture the desired information, he activates the malware and then easily transfers data to thirsty third parties. It’s enough to keep you up at night!

COULD BIOMETRICS BACKFIRE?Another possible problem arising from increased biometric use by banks is the way in which data is captured and transmitted. Ultimately, biometric systems still need to communicate data back to a system, which is authenticating the user - it’s only that the data is different. Just as with traditional usernames and passwords, biometrics can be susceptible to, “man in the browser” or, “man

Biometrics. The Good, the Bad and the Ugly

in the middle” attacks. Today there are some tactical methods to prevent biometrics from such attacks. Apple, the US Government and India’s UIDAI program for instance, all use cryptography together with other techniques to ensure only partial, encrypted or unique tokenized data, rather than the biometric data itself, is shared. As the use of biometrics increases however, so too will the need to consider standards around the proliferation of biometric data. In order to accept biometric data, participating systems should be forced to abide by a structured storage and transmission framework and protocol.

TIME MARCHES ON – ONE FINGERPRINT AT A TIMEBiometric Innovation will wait for no man and despite the risks, stories regarding financial institutions moving ahead with biometric services abound. Fingerprint authentication for access to mobile banking applications, for instance, works fairly well. Users already have the necessary hardware built into their iPhones, making the authentication process quick and seamless. Also, users don’t need to go through a separate biometric registration process specific to different mobile apps.

Think of the iPhone fingerprint recognition system. You only have to provide your fingerprint details to the iPhone once. After that, any app, which has the ability to use fingerprint authentication, can make use of the iPhone’s authentication. The customer only has to register once, and then their other service providers can authenticate data against the biometric profile created when they first registered on the iPhone. It doesn’t mean that anyone can access accounts if the phone is lost because a would be criminal would still need to unlock the phone with the right PIN or fingerprint, and then provide the correct fingerprint each time they want to use the user’s banking apps.

Facial and voice recognition aren’t as elegant. While the users have the hardware needed in their phones, they need to go through a separate registration process for these more complicated authentications. Many would-be users are frustrated and report that the effectiveness of the authentication can be impacted by background noise, lighting and even sore throats or colds. They’re also not as quick or seamless to use. Customers complain that facial registration can be awkward and difficult because the user must hold one’s phone at arms-length, while trying to find the best lighting, and attempting to keep one’s face inside the authentication circle. Having said that, once facial recognition is authenticated it is incredibly secure due to “liveness detection” (can’t be fooled by holding up a picture) through “expression detection” (e.g. raise your eyebrows, smile etc.). Some say the current inconveniences may be a reasonable cost to pay for the advanced security until the usability kinks are ironed out.

ROUND AND ROUND SHE GOES…The industry has seen a number of big names in financial services take serious steps towards implementing biometrics security over the past year. The Royal Bank of Scotland (RBS) and NatWest, now enable fingerprint recognition to access their banking apps using Apple’s Touch ID on iPhones2. Other banks in the US, like Barclays and U.S. Bank3, are already using voice recognition to authenticate customers when they call into call centers, use telephone banking services or access their mobile banking app. MasterCard has also recently announced voice and facial recognition for mobile payments. Where she stops, nobody knows, but one thing is for certain – the use of biometrics in fighting mounting security issues must be explored. It is imperative that pioneers in the field of biometrics think carefully about the potential ramifications for this new technology. Careful regulation, process and procedure will be key to keeping biometrics in the voices, the eyes, the faces… and the hands, of the good guys.

CONTRIBUTORSJibran Ahmed

Jibran Ahmed is a Principal Consultant in Capco’s London office. He has over 6 years’ experience in program management, defining target operating models and stakeholder management in the investment banking industry.

Owen Priestley

Owen Priestley operates as Capco’s Chief Connecter and is a member of the North American Digital leadership team working in new product development and as a Consultant for Capco for over 6 years.

___

1 er cri e in financial institutions

http://www.cso.com.au/article/556587/cyber-crime-financial-institutions/

2 and at est custo ers get o ile an ing at t eir fingerprints

http://www.rbs.com/news/2015/february/rbs-and-natwest-customers-get-mobile-banking-at-their-fingertips.html

3 Banking on the power of speech

https://wealth.barclays.com/en_gb/home/international-banking/insight-research/manage-your-money/banking-on-the-power-of-speech.html

Article 7

37 36

PART III: THE UGLY - FLIES IN THE OINTMENT - WHAT DETERMINES THE SUCCESS OR FAILURE OF BIOMETRIC ROLLOUTSIn parts I and II of our series, “Biometrics: The Good, The Bad and The Ugly”, we investigated the pros and cons of biometrics’ use in financial services. Now its time to turn our attention to the realities of using biometrics, and the attention to detail that will make this approach work, or not, in global banking. Trust is a critical factor that often doesn’t get the attention it deserves. In a recent global survey by leading fintech provider FIS1, security and the protection of one’s identity ranked highest in customer concerns and demands. With the spate of recent hackings, data losses and intelligence agency scandals, the general public has good reason to be cautious about giving up their biometric data. Organizations collecting this data need to be transparent about how the data will be used, and provide adequate assurances that user data will be held securely and not made available to third parties without their permission. They also need to make registration as easy as possible, and highlight the security advantages of the new technology in order to encourage people to register.

Biometrics. The Good, the Bad and the Ugly

IN BANKS WE TRUST? Unfortunately due to comfort levels around providing biometrics to a third party, multi-factor authentication will be the intermediary step that banks may need to go through to make customers comfortable. Hopefully the extensive use of biometrics by governments should increase the general public’s comfort with using biometrics and sharing their data with large corporations. For the time being however, PINs and passwords, as well as our biometric identification, will probably have to run in parallel. The quicker financial institutions get to an authentication that is strong, reliable and individual – such as biometrics – the quicker they can marry increased security with a better customer experience, something the banking industry has struggled with traditionally.

THE NEED FOR SPEEDFor a biometric authentication system to have any hope of mass adoption, it has to be as easy – if not easier – than typing in a username and password. Fingerprint recognition by phone is a great example of quick and easy authentication, but not all biometric methods compare. Current facial recognition methods can take up to 10 seconds to scan facial features and decide if authentication is permissible. Although that seems like a

reasonable amount of time, it’s just too slow. In that time, the customers could have typed in a username and password. And they will.

BETTER AT BIOMETRICS THAN BANKS? ENTER NEW ENTRANTSAn alternative approach to creating a seamless biometric authentication process is to take the onus away from banks to create the authentication systems altogether. Banks and other organizations can leverage third party applications to quickly create secure, biometric authentication systems. For users, they can be quick to set up (customers only need to enroll once), they’re easy to use, and biometric data is only stored in one place rather than with several different handlers.

There are already many third party products out there, such as 1U by Hoyas Labs2, which can authenticate users for any website using fingerprint and facial recognition. Consumers can already use 1U to access email, Amazon, American Express and other online accounts using a combination of fingerprint and “live” facial recognition. From a security perspective, it’s quite impressive for a third party new entrant. Not only does it register facial recognition, it also allows an additional layer of security by asking the user to perform random facial expressions that haven’t been pre-determined, as well as couple it with a secret facial expression that only that user knows. Cool tricks!

ON THE BIOMETRICS HORIZONAn extremely interesting new solution is the Nymi Band3 which uniquely authenticates an individual based on their electrocardiogram (ECG). This is essentially the user’s heartbeat “signature” which is unique to each individual. The device takes the form of a wristband so authentication is seamless and the same device can authenticate a user for multiple services. Halifax UK and the Royal Bank of Scotland are already piloting this technology. Also on the horizon is finger vein recognition4. This

CONTRIBUTORSJibran Ahmed

Jibran Ahmed is a Principal Consultant in Capco’s London office. He has over 6 years’ experience in program management, defining target operating models and stakeholder management in the investment banking industry.

Owen Priestley

Owen Priestley operates as Capco’s Chief Connecter and is a member of the North American Digital leadership team working in new product development and as a Consultant for Capco for over 6 years.

___

1 nderstand t e onsu er pectations ap http://closethegaps.fisglobal.com/

2 Hoyos Lab 1UTM App http://www.hoyoslabs.com/innovation

3 This wristband works with your heartbeat to pay for things http://mashable.com/2014/11/04/wristband-heartbeat-payments/

4 an custo ers to sign in it finger vein tec nolog http://www.bbc.com/news/business-29062901

technology uses infrared sensors to scan the pattern of the veins beneath the user’s fingertip – again, these are unique to every individual and unlike fingerprints, cannot be easily replicated.

In the future, phone screens will be embedded with fingerprint scanners and devices will authenticate users by using face, voice and ECG recognition together before ever launching a banking app. It’ll be a seamless and foolproof process that’ll make it impossible for fraudsters to impersonate or steal identities. Customers should look forward to this future. The banks, however, have a lot of work to do to keep the bad guys out of their biometrics!

Capture

Verification:Present Biometric

Enrollment:Present Biometric Process Store No Match

Match

Compare

ProcessCapture

Article 8

39 38

Last week a friend told me an interesting story about how she felt going to her local bank. She explained that on a cold March day, she had to walk to the bank and wait in line to speak to a bank representative. Seems the new accounts she wanted to open meant her having to show up in person. She had to explain to a private banker, in a public place, that she needed a joint account with her ex-husband for the kids, a new checking account with her fiancé for the wedding – and a pre-paid credit card so she could reign in her teenager’s emerging expensive tastes. It was like baring her soul to a banker she had never met before. The ‘private’ in private banking was definitely missing. Given the vulnerability she felt – she didn’t even begin to discuss her real financial goals or concerns – like saving with her new spouse, or how to manage established investments individually.

What if she had been able to put on a headset – in the real privacy of her office or home – and through the use of virtual reality, ask all the pertinent questions without fear of being overheard or judged? What if she had been able to leisurely explore product and service options and interact with a quality advisor when and where she wanted? What if, at the same time, she was quite welcome and able to compare products and pricings across financial services companies without feeling embarrassed about doing so? What if she was able to tap and choose various short-term savings or investment options and see how they could affect her finances long-term based on a wealth of data? Welcome to the future world of virtual reality in financial services.

The Reality of Virtual Reality. A Mindtrip for Banks

VIRTUAL REALITY GETS REAL – FROM GAMING TO BANKING?Strong investment in Virtual Reality (VR) from the world’s largest tech groups suggest that VR is at the forefront of becoming the next frontier in immersive technology. Oculus VR, a virtual reality technology company, has only recently released the Oculus Rift Development Kit 2. This ground-breaking VR headset allows users to empathize with the virtual world through an immersive experience. Although, the Development Kit 2 is intended for developers only, there has been massive interest in VR computer-simulated environments across industries.

or financial services irtual ealit could

1. transform the way you learn about new financial products and services

2. get you the best financial advisor at all times

3. let you compare across financial institutions in the blink of an eye

4. enable you to make use of big data for investment decisions

…and this is only scratching the surface of what will be possible.

AN IMMERSIVE EXPERIENCE VR technology enables a fully immersive experience, one in which we can modify the environment by using physical gestures and verbal commands. It will allow us to create structures that suit our needs. It will also be a substitute for discovering and exploring reality that we would not have access to otherwise. Ultimately, it will be able to alter our understanding of the world we live in and challenge the very concept of reality.

While enabling a radically new experience, full immersion into a virtual reality will ultimately depend on the quality of the underlying technology. Imagine walking into your local bank - virtually. What would you expect visually? Would it be good enough to get the same immersive experience that you get from playing a video game on your PlayStation 4? Probably not. In fact, it is highly likely that we will only trust this space with our personal finances if we can fully identify and relate to our virtual selves.

AN INTUITIVE TOUCH AND FEEL FOR DATAMany of us do not know how to interpret financial figures we see in the news or in our banks’ offerings. In fact, human interaction with financial data has been abstract and theoretical. Virtual reality technology will enable an intuitive way to interact with data through multi-dimensional visualization and verbal command.

What is the catch? Immersion alone will not make a computer-simulated experience a real one. If virtual reality wants to have an impact on our lives it must allow users to interact with their environments. Only through a combination of immersion and interaction can we integrate virtual reality into our lives, and let it become part of our real world.

THE MATRIX OF BANKINGBy mirroring reality, virtual reality can explore our most intimate thoughts and those of others. Users will be able to connect with each other and talk about the things that matter most to them. Could VR become a superior way to interact with customers and understand their most personal financial fears and goals, in a completely private and protective setting? For those willing to embrace potential virtual opportunities it may be possible to better connect and engage with customers in a different world. It could allow a better understanding of individual needs, and may even enable them to develop unique and truly intimate relationships with customers they may never have connected with in the past. The reality of virtual reality may just be something that the financial services industry cannot afford to ignore.

* The foregoing blog is the opinion of the writer and does not necessarily reflect the opinion of Capco or FIS.

CONTRIBUTORPhilipp Pohlmann

Philipp Pohlmann is a Consultant with Capco’s Digital practice in Germany. He is passionate about the intersection of new technologies and human-centered design in financial markets. Philipp gained significant knowledge in conceptualizing and developing strategic projects and initiatives in the area of customer experience design and service design thinking.

___

ve al rie e uture ersive irtual ealit a ing perience www.forbes.com/sites/michaelvenables/2013/10/20/eve-valkyrie-the-

future-of-immersive-virtual-reality-gaming-experience/

ersion vs nteractivit irtual ealit and iterar eor www.humanities.uci.edu/mposter/syllabi/readings/ryan.html

ersi elia to unveil i ersive space e perience at s t Anniversary Open House

http://finance.yahoo.com/news/immersion-vrelia-unveil-immersive-space-130000201.html

to launc virtual realit eadset www.ft.com/intl/cms/s/0/601a35e2-bea5-11e4-8d9e-00144feab7de.

html#axzz3UT8KAN7a

irtual realit t s not ust or video ga es http://fortune.com/2014/05/05/virtual-reality-its-not-just-for-video-games/

Virtual reality headset Oculus Rift meets the Bloomberg terminal http://qz.com/218129/virtual-reality-headset-oculus-rift-meets-the-

bloomberg-terminal/

Financial planning gets dose of virtual reality www.usatoday.com/story/money/personalfinance/2014/11/22/financial-

planning-gets-a-dose-of-virtual-reality/19326655/

“ Could VR become a superior way to interact with customers and understand their most personal financial fears and goals, in a completely private and protective setting? The reality of virtual reality may just be something that financial services industry cannot afford to ignore.”

Article 9

41 40

“ Could VR become a superior way to interact with customers and understand their most personal financial fears and goals, in a completely private and protective setting? The reality of virtual reality may just be something that financial services industry cannot afford to ignore.”

Article 9

43 42

Remember back in the day when corporations used to put a handful of guys in a room with a bunch of computers, and hoped they were addressing cyber-security? And then the inevitable outrage – “we’ve got a whole bunch of guys looking at this! How could there have been a breach?” Well, the game has officially changed. Fact is that in 2014, companies reported 42.8 million detected cyber-attacks worldwide, and that’s a 48% Y/Y increase from 20131.

The forceful push of companies, governments and just plain people, onto a digital infrastructure is driving unprecedented cyber security risk. This year, annual federal government spending on cyber security will reach $13.3 billion, earmarked to combat cyber-attacks which have increased a whopping 445% since 2006. Over the last year alone, federal agencies have seen a 78% growth in cyber incidents2. The genie, as they say, is out of the bottle.

THE EVER-MOUNTING THREATCyber security is a major problem. Consider this. It takes 10x as much effort to defend against a cyber-attack as it does to create one. Bad odds for the good guys. Multiply that by the fact that governmental experts are now uncovering 110,000 cyber security breaches every hour and the numbers get scary, fast – that’s 30 breaches every second!

IT spend on security in the US in 2012 was about $60 billion, but in order to counter the surveillance state, that growth rate will need to quadruple to 24%. Over 10 years, this puts security spend

Machines vs Hackers Has Cyber-security Exceeded the Limitations of Human Intellect?

at $639 billion by 2023 – a tenfold increase. But will even that be enough? Global corporations are sucking up cyber security professionals faster than universities can spit them out, but at some point we must ask ourselves - has cyber security exceeded the limitations of human intellect? Are we to the point of needing artificial intelligence (AI) in order to fight cyber crime?

Threats are mounting - spyware, malware, spoofing, phishing, botnets, data leakage, identity theft – it’s almost too much to get the human mind around. This evolutionary leap in threat complexity continues to evolve with malicious software codes and viruses becoming more intelligent every day, and increasingly capable of adapting against legacy defenses. Could introducing the concept of machine learning into the ever-expanding war against cyber crime be our knight in shining amour, come to save the day?

COULD MACHINES LEARN TO FIGHT CYBER CRIME?Machine learning is a branch of AI that focuses on enabling machines with the capability to understand information, both its intent and context. In a world where technology is growing at exponential rates annually, it’s impossible for human intelligence to keep up with the capabilities of technology. In security, hackers are winning the battle being waged in cyber space. For instance, the U.S. Army has 21,000 security analysts tasked with protecting its Cyber Command unit, and yet estimates say they are still outnumbered 100:1 by hackers looking to tamper with the system. Other estimates go as high as 1000:13! All we know for sure is that this problem needs some new thinking quick, and our machines may be best equipped to do just that.

Machine learning could be the answer by allowing machines to learn based on patterns, relationships, and associations between all bytes of data in an entire system. The more data the system is fed, the more connections the machine can make, and begin to learn in the same way humans learn from birth - by associating stimuli with patterns. Computer programming in the cyber security space is behind the times and relies too much on human programmers, who make mistakes and are often limited in the knowledge they can provide to the computer.

A new doctrine of thought suggests that instead of humans teaching machines to think for us, we should be teaching machines to think for themselves. It is impossible for humans to be able to predict every type of attack that could be launched on their systems. Because of this limitation, programmers are facing an uphill battle getting steeper and steeper by the day. Machine learning provides a first-mover advantage for defenders against cyber-attacks because machines can learn patterns humans cannot foresee, and be better prepared for any possible attack.

THE WAKE-UP CALLSeveral cyber security companies have woken up to the vast potential of using AI to fight cyber crime. Two are Rippleshot and Norse. Rippleshot built a machine learning system to fight against credit card account takeovers and swears that it enables them to fight fraud at the speed of data. Their system uses millions of past instances of takeovers as blueprints to defend against future attempts, and can now detect data breaches within hours, or minutes, instead of weeks or months, as was the case for Target. Norse fights attacks from botnets and other compromised hosts. This cyber security firm sends millions of sensors and agents, called honeypots, throughout the internet to detect attacks. The honeypots deliver a risk score on certain websites and blocks those that exceed a score. They also block risky outgoing links to protect against phishing attacks.

In Peter Diamandis’ book, Abundance, he predicts every computer will be as smart as the human brain by the year 2016 and by 2020, every computer will be as smart as all of the human brains in the world combined. Now is the time where we need to use, and trust, technology to do our heavy lifting in the war against cyber crime. Machine learning is the next step in protecting ourselves and our clients against hatching swarms of hackers. Instead of defending against hackers with human intellect, we have no option but to utilize machines that can learn at a much faster pace than humans ever could. Machines are winning at Jeopardy. Machines are driving our cars. Why would we not want machines protecting us from cyber crime? Sorrguys, when it comes to cyber security, my bet’s on Watson*.

CONTRIBUTORSMaxalan Vickers

Maxalan Vickers is a new associate through Capco’s ATP Program. Prior to Capco, Max studied Financial Engineering at New York University and interned at Bank of New York-Mellon in their Broker Dealer Services division.

arles aruguru

Charles Mbaruguru is an Associate within Capco’s Technology Practice in New York. Prior to Capco, Charles gained experiences in the telecommunications and technology industries.

___

1 e n ortunate ro t ector ersecurit www.forbes.com/sites/michaellingenheld/2015/04/27/the-unfortunate-

growth-sector-cybersecurity/

2 eport er ecurit pending portance ill ncrease www.ibtimes.com/report-cyber-security-spending-importance-will-

increase-249428

3 o ul er ri e tatistics and rends n ograp ic www.go-gulf.com/blog/cyber-crime/

ecurit ndustr o pand en old www.forbes.com/sites/richardstiennon/2013/08/14/it-security-industry-

to-expand-tenfold/

lar ing ro t in er ri e rives t e lo al ar et or er ecurit ccording to e eport lo al ndustr nal sts nc

www.virtual-strategy.com/2014/06/24/alarming-growth-cyber-crime-drives-global-market-cyber-security-according-new-report-glob#ixzz3ZqTYWTmP

er attac ers outnu er c er de enders archive.defensenews.com/article/20131028/C4ISRNET18/310280007/Cy-

ber-attackers-outnumber-cyber-defenders

r er o and www.arcyber.army.mil

“ Cyber-security risk - The genie, as they say, is out of the bottle. ”

Article 10

45 44

If Bitcoin Behaves... The Burgeoning of Blockchain TechnologyCRYPTO-CURRENCY AND BLOCKCHAIN: ONE OF THESE THINGS, IS NOT LIKE THE OTHEROk. Let’s just go through this one more time for any recent joiners to the Crypto-discussion. You must separate the concept of virtual currency and blockchain technology. Crypto-currency is virtual currency, a means of transferring value digitally without a physical representation of the value exchanged (like a dollar). The technology that makes this possible is something called “blockchain”, a series of distributed databases that record and verifies transactions between owners of a crypto-currency. The transaction information is masked and made publically available, providing verification of transactions and transfers for future use. Think of Bitcoin and blockchain like e-mail and the Internet. Can you email using the Internet? Yes. Is there a plethora of other things you can achieve using the Internet? Yes, as is the case with blockchain technology.

ENDLESS APPLICATIONS There are endless applications for the proven concept of blockchain technology. Some, if not most, remain undiscovered. The Music1

and Real Estate2 industries are beginning to apply blockchain technologies to potentially solve some of their biggest problem areas, and that’s going pretty well. Imagine if the use of every piece of music was captured, to explain who exactly had enjoyed that product, and who paid for it? Or if while searching for a new home, one could seamlessly peruse the long-term histories of each property without ever approaching a records department at Town Hall! Now do you get it?

Crypto-currency may just be the beginning of a business revolution in which value, assets and information will be transferred securely,

at both high speed and low cost using blockchain technology. A recent study3 conducted on behalf of the insurance industry had this to say about blockchain, “Any financial services professional should be excited by a technology that simultaneously improves integrity and security while also reducing costs.” The study concluded that blockchain technology would shape the future of this 1.1 trillion dollar industry. Blockchain technology could transform how the world executes transactions. Period.

BITCOIN VS CASH – COULD BLOCKCHAIN BE SAFER?And yet with all the other applications of blockchain being heralded across the planet, blockchain did begin with Bitcoin, and for better or worse, it helps to predict the future by looking at the past. Many, from their onset, did associate virtual currencies (like Bitcoin) with illegal transactions or dealings in otherwise illicit goods and services. Media reports have done little to counter the imagery of the ninja-assassin, payment network, or to educate the general population about the true nature and value of crypto-currency and its application to personal finance. The real target for illegal transactions is, and has always been, cash. Cash is anonymous and private. There is no ledger detailing every transaction with cash. Current regulations attempt to stipulate how financial institutions and intermediaries must deal with, and report cash use, but the control mechanism in place currently for currency is a weak one at best. All of a sudden, Bitcoin and blockchains look a lot more mainstream, and manageable.

CRYPTO-CURRENCY AND THE UNDERBANKED For people in places where cash is king, crypto-currencies could usher in a whole new type of loyalty. Existing bricks and mortar

financial institutions underserve many of the world’s citizens when it comes to providing practical economic and commercial transactions. These people will naturally see the inherent value of being able to make good on their promises and debts as easily as they would send a text to a family member. Compound this potential by the fact that the next decades will connect over a billion new consumers to the Internet, and in doing so, potentially to the world of virtual finance. The possibility of bringing other goods and services to billions of underserved individuals is nothing short of mind-blowing.