brettenwood system with refrance to imf & world bank

DESCRIPTION

Brettenwood System With Refrance to IMF & World BankTRANSCRIPT

The System of Bretton woods 1.

Introduction

In times of globalisation the economic environment changes rapidly. Capital movements become larger and at the same time less controllable. Therefore, the need for a stabilising system becomes more and more apparent. In the past such a system has been established at the conference of Bretton Woods. Already in 1944 the British economist John Maynard Keynes emphasised “the importance of rule-based regimes to stabilise business expectationssomething he accepted in the Bretton Woods system of fixed exchanged rates.”1 Recently leading industrial nations have been calling for a renewal of the purpose and the spirit of this system in order to cope with the growing size of international trade and capital flows. This essay gives a short overview of the system’s development from 1944 until today and stresses especially problems and obstacles. It identifies mistakes that have been made and points out aspects that have to be taken into account when implementing a “new system of Bretton Woods”.

2. Development of the system

2.1. The international economic situation After World War I most countries wanted to return to the old financial security and stable situation of pre-war times as soon as possible. Discussions about a return to the gold standard began and by 1926 all leading economies had re-established the system, according to which every nation’s circulating money had to be backed by reserves of gold and foreign currencies to a certain extent. But several mistakes in implementing the gold standard (mainly that a weakened Great Britain had to take the leading part and that a number of main currencies where over- or undervalued) led to a collapse of the economic and financial relations, peaking in the Great Depression in 1929. Every single country tried to increase the competitiveness of its export products in order to reduce its payment balance deficit by deflating its currency. This strategy only led to success as long as a country was deflating faster and more strongly than all other nations. This fact resulted in an international deflation competition that caused mass unemployment, bankruptcy of enterprises, the failing of credit institutions, as well as hyper inflations in the countries concerned. In the 1930s several conferences dealing with the world monetary problems caused by the Great Depression had ended in failure. But after World War II the need for a stabilizing system that avoided the mistakes, which had been made earlier, became evident. Plans were made for an innovative monetary system and a supervising institution to monitor all actions. First negotiations took place under wartime conditions.

2.2. The conference of Bretton Woods

In 1944 an international conference took place in Bretton Woods, New Hampshire (USA). 44 countries attended this conference in order to restructure international finance and currency relationships. The participants of this conference created the International Monetary Fund (IMF) and the International Bank for Reconstruction and Development (IBRD/World Bank).

Additionally, they agreed on implementing a system of fixed exchange rates with the U.S. dollar as the key currency.

The plans for the system of Bretton Woods were developed by two important economists of these days, the American minister of state in the U.S. treasury, Harry Dexter White, and the British economist John Maynard Keynes who stated: “ We, the delegates of this Conference, Mr President, have been trying to accomplish something very difficult to accomplish.[...] It has been our task to find a common measure, a common standard, a common rule acceptable to each and not irksome to any.” 2 This statement outlines the difficulty of creating a system that every nation could accept. The ideas of John Maynard Keynes and Harry Dexter White have been described as very different from each other on several occasions but in fact there are extraordinary similarities. According to the White plan, a Bank for Reconstruction (today the World Bank) and an International Stabilisation Fund should be established. The Keynes plan called for the same. The only difference was that Keynes wanted to vest the IMF with possibilities to create money (a fact that can easily be understood in the background of Great Britain’s suffering from the deflation policies in the Inter-War period) and with the authority to take actions on a much larger scale. In case of balance of payments imbalances John Maynard Keynes recommended that both sides, debtors and creditors, should change their policies. Countries with payment surpluses should increase their imports from the deficit countries and thereby create a foreign trade equilibrium. Harry Dexter White, on the other hand, saw an imbalance as a problem only of the deficit country. Economists today agree that White was mistaken and Keynes was more farsighted.3 However, Keynes’ plan was never discussed seriously at Bretton Woods and the participants agreed on the White plan. The United States defined the value of its dollar in terms of gold, so that one ounce of gold was equal to $ 35. All other members had to define the value of their money according to what was called the “par value system” in terms of U.S. dollars or gold.

2.3. The dominant role of the USA

The USA has been and still is the dominating power of the Bretton Woods system. After World War II the United States was the country with the biggest economic potential. The U.S. dollar was the currency with the most purchasing power and it was the only currency that was backed by gold. Additionally, all European nations that had been involved in World War II were highly in debt and transferred large amounts of gold into the United States, a fact that contributed to the supremacy of the USA. Thus, the U.S. dollar was strongly appreciated in the rest of the world and therefore became the key currency of the Bretton Woods system. The headquarters of the two main institutions (the IMF and the World Bank) are situated in Washington D.C. The dominant role of the USA already became apparent when the American ideas of the Bretton Woods system gained more acceptance than those of Great Britain. The plans of the British economist John Maynard Keynes were rejected and the model of the American economist White was favoured. Despite “Keynes’s part in constructing the Bretton Woods system, [...] his vain

struggle, over five wartime missions to Washington, to preserve Britain’s financial independence from the United States” 4 the Bretton Woods system is dominated by the USA.

3. The International Monetary Fund

3.1. Purpose The IMF was officially established on December 27, 1945, when the 29 participating countries at the conference of Bretton Woods signed its Articles of Agreement. It commenced its financial operations on March 1, 1947. The IMF is an international organisation, which today consists of 183 member countries. The purposes of the IMF are to promote international monetary cooperation by establishing a global monitoring agency that supervises, consults, and collaborates on monetary problems. It facilitates world trade expansion and thereby contributes to the promotion and maintenance of high levels of employment and real income. Furthermore, the IMF ensures exchange rate stability to avoid competitive exchange depreciation. It eliminates foreign exchange restrictions and assists in creating systems of payment for multilateral trade. Moreover, member countries with disequilibrium’s in their balance of payments are provided with the opportunity to correct their problems by making the financial resources of the IMF available for them.

3.2. Operations

When joining the IMF, each country must contribute a certain sum of money, which is called a quota subscription and is a sort of credit deposit. These quotas form the largest source of money at the IMF’s disposal and the IMF uses this money to grant loans to member countries with financial difficulties. Each nation that has joined the system can immediately withdraw 25 per cent of its quota in case of payment problems and it may request more if this sum is insufficient. The debts have to be paid back as soon as possible. Additionally, the country must demonstrate how the payment difficulties will be solved. The higher a country’s contribution is, the higher is the sum of money it can borrow from the IMF. Furthermore, the quotas determine the voting power of each member.

The money, which the IMF lends, should not be compared to a loan of a conventional credit institution. For the country that files an application it is rather an opportunity to buy a foreign currency and paying with gold or the national currency. Within three to five years the country has to pay back its debts. According to the IMF in the course of a typical year circa 20 currencies are borrowed and “most potential borrowers want only the major convertible currencies: the U.S. dollar, the Japanese yen, the deutsche mark, the pound sterling, and the French Franc.”5 Therefore, although quotas are worth about $193 billion in theory, the sum at the IMF’s disposal is deceptively large.

3.3. Organization

The IMF has no control over national economic policies of its members. On the contrary, the chain of command runs from the governments of the member countries to the IMF. The highest authority is the Board of Governors, which consists of one Governor (usually the minister of finance or the head of the central bank) of each member country. Additionally, there is an equal number of Alternates (representative Governors). The Board of Governors gathers only on the occasion of annual meetings.

The IMF’s day-to-day work is managed by the Executive Board, which is formed of 24 Executive Directors who meet at least three times a week to supervise the implementation of the IMF’s policies. The member countries with the highest quotas send one Executive Director to the Board, who has as many votes as the quota regulation assigns to his country. The remaining Directors are elected by the rest of the countries and they only have as many votes as they had in the election. This point illustrates the dominance of the USA in the System of Bretton Woods as the “United States, with the world’s largest economy, contributes most to the IMF, providing about 18 percent of total quotas (about $35 billion)”.6 Thus the USA have most votes, by now more than 265.000.

4. The World Bank

4.1. Goals The World Bank is the world’s most important source of financial aid for developing nations. It provides “nearly $16 billion in loans annually to its client countries. It uses its financial resources, highly trained staff, and extensive knowledge base to help each developing country onto a path of stable, sustainable, and equitable growth in the fight against poverty.”7 Its goals are to improve living standards and to eliminate the worst forms of poverty. It supports the restructuring process of economies and provides capital for productive investments. Furthermore, it encourages foreign direct investment by making guarantees or accepting partnerships with investors. The World Bank aims to keep payments in developing countries balanced and fosters international trade. It is active in more than 100 developing economies. It forms assistance strategies by cooperating with government agencies, nongovernmental institutions and private enterprises. It offers financial services, analytical, advisory, and capacity building.

4.3. Organisation

The World Bank is an independent organisation of the United Nations. Each country that wants to join it, has to be a member of the IMF. The highest authority of the World Bank is the Council of Governors, which consists of one representative of each country. The Executive Board consists of five Directors to whom the Council of Governors transfers responsibility for nearly all issues. The President of the World Bank is de facto elected by the U.S. government and then confirmed by the Executive Board. He is involved in the current activities

5. Adjustments and reactions to the changing environment

5.1. Integration of developing countries

Only a few years after the establishment of the Bretton Woods System an economic restructuring throughout the world necessitated a new orientation of the organizations. In the 1950s the decolonialization of many developing countries took place. In order to meet the challenge of integrating those countries into the Western world and solving their social and economic problems the IMF and the World Bank changed their plans and founded new organizations. However, in this phase the developing countries were seen only as suppliers of important resources, a fact that led to vehement protests of the developing nations and the Eastern-Block states, since they did not perceive this role as promoting. For this reason two affiliated organizations of the World Bank were created. In 1956 the International Finance Cooperation (IFC) was established. Its purpose is to grant credits to private organizations that lack capital for projects in the developing world. In 1961 the International Development Association (IDA) was founded and its main function is to grant credits to especially poor countries at very favorable conditions. For example the period of repayment can be up to 50 years and the interest rates are far below market standard. The establishment of both mentioned organizations made the World Bank the centre of foreign aid of the United Nations today.

5.2. Special Drawing Rights

In the 1960s the world experienced a substantial economic expansion, especially the warring nations of World War II grew unexpectedly fast. This led to a weakening of the position of the USA and a devaluation of the U.S. dollar. It appeared that the reserves were inadequate to back the trade expansion and slowed down economic development. The IMF reacted by issuing Special Drawing Rights (SDRs), which member countries could add to their holdings of foreign currencies and gold. SDRs were assigned with a value based on the average worth of the world’s major currencies. These were the U.S. dollar, the French franc, the pound sterling, the Japanese yen, and the German mark.

5.3. Crisis of the system

In the 1960s and 1970s enduring imbalances of payments between the Western industrialized countries weakened the system of Bretton Woods. One substantial problem was that one national currency (the U.S. dollar) had to be an international reserve currency at the same time. This made the national monetary and fiscal policy of the United States free from external economic pressures, while heavily influencing those external economies. To ensure international liquidity the USA was forced to run deficits in their balance of payments, otherwise a world inflation

would have been caused. However, in the 1960s they ran a very inflationary policy and limited the convertibility of the U.S. dollar because the reserves were insufficient to meet the demand for their currency. The other member countries were not willing to accept the high inflation rates that the par value system would have caused and “the dollar ended up being weak and unwanted, just as predicted by Gresham’s law: Bad money drives out good money.”8 The system of Bretton Woods collapsed.

Another fundamental problem was the delayed adjustment of the parities to changes in the economic environment of the countries. It was always a great political risk for a government to adjust the parity and “each change in the par value of a major currency tended to become a crisis for the whole system.”9 This led to a lack of trust and destabilizing speculations.

In March 1973 the par value system was abandoned and the member countries agreed on permitting different kinds of ways for determining the exchange value of a nation’s money. The IMF required that the countries no longer based this value on gold and that it was common knowledge how each nation determined its currency’s value. Today many large developed countries allow their currencies to float freely, which means that only supply and demand at the market determine what it is worth. Some nations try to influence this process by buying and selling their own currency. Another method is to peg the value of the money to one of the main currencies. After this reform the system of Bretton Woods was more about “information exchange and consultation, conditional policy understandings, than about rule based guarantees.”10 In the years of floating exchange rates the level of cooperation varied with the economic and political developments.

5.4. Recent activities

The field of activities of the Bretton Woods institutions was broadened by the deep-rooted changes in the East-bloc economies and the collapse of the Soviet Union. In the past the communist states had feared entrance into the IMF and the World Bank because of the economic superiority of the United States but after the changes in their own economies they saw the chance of solving their problems by joining those organizations. Thus, supporting the process of economic restructuring is one of the main activities of the Bretton Woods institutions nowadays. A massive campaign was started to establish free-enterprise systems and to shift from centrally planned to market economies.

Furthermore, the IMF and the World Bank want to ensure that their mechanisms and operations meet the requirements of the new world of integrated global markets. Especially the heavy financial crises in Mexico and Asia during the 1990s exposed weaknesses in the international financial system. The increasing size and importance of cross-border capital flows necessitated a better surveillance of the member countries. In particular the assessment of potential risks in member countries has been improved by collecting more timely and accurate data to ensure transparency. A second major field is the development and assessment of internationally

accepted standards of good practices. To prevent future crises the IMF created the Contingent Credit Lines in 1999, which motivate countries to “adopt strong policies, be transparent, adhere to internationally accepted standards, and have a sound financial system.”

6. The future of the system of Bretton Woods

During the last five to ten years especially the system of Bretton Woods has been topic of many public discussions with controversial opinions. Human rights activists argue that the programmers for the structural adjustment of the developing countries initiated by the World Bank and the IMF led to a “third worldisation” of the East-bloc states, which means that they dramatically increased poverty in those countries. Large-scale agrarian and industrial projects destabilized national economies, destroyed the environment and social patterns. It is pointed out that the inner structure of the Bretton Woods institutions, where the right to say is proportional to the amount of money that each country contributes, is symbolic of the capitalistic ideology, which completely ignores the interests of the people living in developing countries. Thus, human rights activists demand that the IMF and the World Bank stop interfering in national policies of sovereign countries. The World Bank is well aware of the problems that can be caused by projects in less developed areas. It reacted by providing the possibility to file requests to an Inspection Panel. A person that files a request to the World Bank has to show that he/she lives in the project area and will most likely be affected negatively by activities related to the project. These negative effects must be caused by a failure from the World Bank to follow its policies and procedures. Additionally, the request must have been discussed with the Bank management with an unsatisfactory outcome contrast to these discussions the major industrialized nations have begun to worry about the implications of the growing size and the speculative nature of financial movements in times of globalization. Calls for a “new system of Bretton Woods” could be heard in almost every industrialized country. In 1996, Michel Camdessus, the Managing Director of the IMF, stated that even though the monetary system had changed since 1944 the goals of Bretton Woods were as valid today as they had been in the past. He underlined that international cooperation would be required to create a new Bretton Woods system, which in his point of view means that “ countries must make a greater effort to understand the economic policies of other countries and that they must listen to the judgment of others about their own national policies. It also means that they must take a more enlightened view of their own national interests, recognizing that it is in their own self-interest to take the interests of other countries into account.”

Chapter 2 WORLD BANK

IntroductionIn 1944, as the 2nd World War neared its end, a conference was convened by the victorious countries in Bretton Wood, in the United States. It was here that the World Bank and the International Monetary fund were born- in the hope that they would provide the foundation of a peaceful and prosperous future for the world.

69years later, these two multi-lateral institutions also known as Bretton Woods Institutions (BWIs) occupy a dominant position in the global political economy, but they are the target of powerful attack- both in the streets and in media. And in the course of these 69years, they have been joined by a whole range of other multilateral institutions. These institutions also play an important role in elimination of world poverty.

World Bank:

Formation : - 27 December, 1945.

Headquarter :-Washington D.C, United States.

President: - Mr. Jim Yong Kim

No. Of. Member Countries :- 188 member countries

Currencies mainly used :- $, Pound, Yen, Euro.

Languages used :- English, French, Spanish.

The World Bank group is a partner in opening markets and strengthening economies. Its goal is to improve the quality of life and expand prosperity for people everywhere, especially the world’s poorest.

The World Bank group of institutions is:-

1) The International Bank For Reconstruction and Development (IBRD) founded in 1944 in the single developing countries and a major catalyst of similar financing from other sources.

2) The International Development Association (IDA) founded in 1960, assists the poorest countries by providing interest free credits with 35 to 40 years maturities.

3) The International Finance Corporation supports private enterprise in the developing countries by providing interest free credits with 35 to 45 years maturities.

4) The Multilateral Investment Guarantee Agency (MIGA) offers investors insurance against non-commercial risk and helps developing country governments to attract foreign investment.

5) The International Centre for the Settlement of International Disputes (ICSID) encourages the flow of foreign investment to developing countries through arbitration and conciliation facilities.

Over the years, the World Bank has made two significant departures in its policy of lending; it changes its policy of lending to government and public sector and concentrated on private sector, and it changed its approach from a project based lending to sector-based lending.

Functions and Objectives:

World Bank performs the following functions:

(i) Granting reconstruction loans to war devastated countries.

(ii) Granting developmental loans to underdeveloped countries.

(iii) Providing loans to governments for agriculture, irrigation, power, transport, water supply, educations, health, etc.

(iv) Providing loans to private concerns for specified projects.

(v) Promoting foreign investment by guaranteeing loans provided by other organizations.

(vi)Providing technical, economic and monetary advice to member countries for specific projects

(vii) Encouraging industrial development of underdeveloped countries by promoting economic reforms.

Resources:

The World Bank had initially authorized capital of $10 billion subscribed by the member countries in accordance with their economic strength. The United States of America is the largest subscriber. The Bank collects funds from members as well as by issue of international bonds

Conceived in 1944 to reconstruct war-torn Europe, the World Bank Group has evolved into one of the world’s largest sources of development assistance, with a mission of fighting poverty with passion by helping people help themselves.

New World, New World Bank GroupMuch of the news from the developing world is good: During the past 40 years, life expectancy has risen by 20 years—about as much as was

achieved in all of human history before the mid-20th century. During the past 30 years, adult illiteracy has been nearly halved to 25 percent. During the past 20 years, the absolute number of people living on less than $1.25 a day has

begun to fall for the first time, even as the world’s population has grown by 1.6 billion people.

During the past decade, growth in the developing world has outpaced that in developed countries, helping to provide the jobs and boost revenues that poor countries’ governments need to provide essential services.

Moreover, in our fast-evolving, multipolar world economy, some developing countries have become economic powers, and others are rapidly becoming additional poles of growth. These countries have increasingly provided the demand that is driving the global economy. As important importers of capital goods and services, developing countries have accounted for more than half the increase in world import demand since 2000. Millions of people in transition and developing countries are joining the world economy as their incomes and living standards rise.The developing world, however, confronts new and difficult challenges.A devastating global economic crisis has interrupted growth and slowed the rate of poverty reduction, and recovery remains uncertain and uneven; pandemics have threatened the lives of millions; food insecurity has undermined the well-being of many; armed struggle has destroyed lives and dimmed the future in conflict-affected regions; and the need to mitigate the effects of climate change—particularly in developing countries—is more urgent than ever before.

Role of the World Bank GroupThe World Bank Group, also referred to as the Bank Group, is one of the world’s largest sources of funding and knowledge for developing countries. Its main focus is on working with the poorest people and the poorest countries. Through its five institutions the Bank Group uses financial resources and its extensive experience to partner with developing countries to reduce poverty, increase economic growth, and improve the quality of life.The Bank Group is managed by its member countries, whose representatives maintain offices at the Bank Group’s headquarters in Washington, D.C. Many developing countries use BankGroup assistance ranging from loans and grants to technical assistance and policy advice. The Bank Group works in partnership with a wide range of actors, including government agencies, civil society organizations, other aid agencies, and the private sector.

The Millennium Development GoalsAlong with other development institutions, in 2000 the Bank endorsed the Millennium Development Goals (MDGs), which commit the international community to promoting human

development as the key to sustaining social and economic progress in all countries. These goals, which call for eliminating poverty and achieving sustained development (box 2), are used to set the Bank Group’s priorities and provide targets and yardsticks for measuring results. They are the Bank Group’s road map for development. With the deadline for the MDGs fast approaching, a new cloud of uncertainty shadows developing countries’ efforts. The world experienced a historic financial and economic crisis, which began in the richest economies of the world and threatened to slow progress in the poorest. Lessons from past crises show that the harm to human development during bad times cuts far deeper than the gains during upswings. Under these conditions, protecting the gains to date and pressing ahead with actions for further progress to achieve the MDGs are especially important.The World Bank Group has stepped up to the challenge posed by the crisis. It has taken numerous initiatives to limit the slide in global economic growth and avert the collapse of the banking and private sectors in many countries. The Bank Group has also provided financing to governments and to the private sector, thereby softening the impact of the crisis on the poor.Efforts to strengthen social safety nets have also been scaled up.

World Bank ReformsAlthough its fundamental mission of reducing poverty and improving lives has not changed, the Bank is adjusting its approaches and policies in response to the needs of developing countries in the new economic context. Rising to the challenges of development now requires institutions that are not only close to the people in developing countries but also able to mobilize key actors—whether governments, the private sector, or civil society—to address global threats together. It requires institutions that are innovative, adaptable, and able to seize new opportunities. To step up to the challenge, the Bank Group is sharpening its focus on strategic priorities, reforming its business model, and improving its governance. These reforms, which promote inclusiveness, innovation, efficiency, effectiveness, and accountability, fall into five areas: Reforming the lending model. Increasing voice and participation. Promoting accountability and good governance. Increasing transparency, accountability, and access to information Modernizing the organization

Governance of the World Bank GroupEach of the five institutions of the World Bank Group has its own Articles of Agreement or an equivalent founding document. These documents legally define the institution’s purpose, organization, and operations, including the mechanisms by which it is owned and governed. By

signing these documents and meeting the requirements set forth in them, a country can become a member of the Bank Group institutions.

Ownership by Member CountriesEach Bank Group institution is owned by its member countries which are its shareholders. The number of member countries varies by institution, from 187 in the International Bank for Reconstruction and Development (IBRD) to 146 in the International Centre for Settlement of Investment Disputes (ICSID), as of April 2011. In practice, member countries govern the Bank Group through its institutions’ Boards of Governors and the Boards of Directors. These bodies make all major policy decisions for the organization.

Boards of GovernorsThe World Bank Group operates under the authority of its Boards of Governors. Each of the member countries of the Bank Group institutions appoints a governor and an alternate governor, who are usually government officials at the ministerial level or the head of the country’s central bank. If a member of IBRD is also a member of the International Development Association (IDA) or International Finance Corporation (IFC), the appointed governor and alternate governor serve ex officio on the IDA and IFC Boards of Governors. Their term of office is five years, and it may be renewed. Multilateral Investment Guarantee Agency (MIGA) governors are appointed separately to its Council of Governors. ICSID has an Administrative Council rather than a Board of Governors. Unless a government makes a contrary designation, its appointed governor for IBRD sits ex officio on ICSID’s Administrative Council.The governors admit or suspend members, review financial statements and budgets, make formal arrangements to cooperate with other international organizations, and exercise other powers that they have not delegated. Once a year, the Boards of Governors of the Bank Group the International Monetary Fund (IMF) meet in a joint session known as the Annual Meetings. Because the governors meet only annually, they delegate many specific duties to the executive directors.

Boards of DirectorsGeneral operations of IBRD are delegated to a smaller group of representatives, the Board of Executive Directors. These same individuals serve ex officio on IDA’s Board of Executive Directors and on IFC’s Board of Directors under the Articles of Agreement for those two institutions. Members of MIGA’s Board of Directors are elected separately, but it is customary for the directors of MIGA to be the same individuals as the executive directors of IBRD.The president of the Bank Group serves as the chair of all four boards, but he or she has no voting power. IBRD has 25 executive directors. The five largest shareholders—the

United States, Japan, Germany, France, and the United Kingdom—each appoint one executive director. The other countries are grouped into constituencies, each of which elects an executive director as its representative.The members themselves decide how they will be grouped. Some countries—China, the Russian Federation, and Saudi Arabia—form single country constituencies. The executive directors are based at Bank Group headquarters in Washington, D.C. They are responsible for making policy decisions affecting the Bank Group’s operations and for approving all lending proposals made by the president. The executive directors function in continuous session and meet as often as Bank Group business requires, although their regular meetings occur twice a week. Each executive director also serves on one or more standing committees: the Audit Committee, the Budget Committee, the Committee on Development Effectiveness, Human Resources, and the Committee on Governance and Executive Directors’ Administrative Matters.

World Bank Group President and Managing DirectorsThe World Bank Group president is selected by the executive directors. The president serves a term of five years, which may be renewed. There is no mandatory retirement age. In addition to chairing the meetings of the Boards of Directors, the president is responsible for the overall management of the Bank.The executive vice presidents of IFC and MIGA report directly to the World Bank Group president, and as mentioned previously, the president serves as chair of ICSID’s Administrative Council. Within IBRD and IDA, most organizational units report to the president and, through the president, to the executive directors. The two exceptions are the Independent Evaluation Group and the Inspection Panel, which report directly to the executive directors. In addition, the president delegates some of his or her oversight responsibility to three managing directors, each of whom oversees several organizational units.

The Five World Bank Group InstitutionsAlthough the institutions that make up the World Bank Group specialize in different aspects of development, they work collaboratively toward the overarching goal of poverty reduction. The terms World Bank and Bank refer only to IBRD and IDA, whereas the terms World Bank Group and Bank Group include all five institutions.

The World Bank: IBRD and IDAThrough its loans, risk management, and other financial services; policy advice; and technical assistance, the World Bank supports a broad range of programs aimed at reducing poverty and improving living standards in the developing world. It divides its work between IBRD, which works with middle-income and creditworthy poorer countries, and IDA, which focuses exclusively on the world’s poorest countries. Developing countries use IBRD’s and IDA’s financial resources, skilled staff members, and extensive knowledge base to achieve stable, sustainable, and equitable growth. IBRD and IDA share staff and headquarters, report to the

same senior management, and use the same standards when evaluating projects. Some countries borrow from both institutions. For all its clients, the Bank emphasizes Investing in people, particularly through basic health and education Focusing on social development, inclusion, governance, and institution building as key

elements of poverty reduction Strengthening governments’ ability to deliver quality services efficiently and transparently Protecting the environment Supporting and encouraging private business development; and Promoting reforms to create a stable macroeconomic environment conducive to investment

and long-term planning.

Bank programs—which give high priority to sustainable social and human development and to strengthened economic management—place an emphasis on inclusion, governance, and institution building. In addition, within the international community, the Bank has helped build consensus around the idea that developing countries must take the lead in creating their own strategies for poverty reduction. It also plays a key role in collaborating with countries to implement the Millennium Development Goals (MDGs), which the United Nations (UN) and the broader international community seek to achieve by 2015. In conjunction with the International Finance Corporation, the Bank is also working with its member countries to strengthen and sustain the fundamental conditions for attracting and retaining private investment. With Bank support, both lending and advice, governments are reforming their overall economies and strengthening their financial systems. Investments in human resources, infrastructure, and environmental protection also help enhance the attractiveness and productivity of private investment.

The International Bank for Reconstruction and DevelopmentIBRD is the original institution of the World Bank Group. When it was established in 1944, its first task was to help Europe recover from World War II. Today, IBRD plays an important role in improving living standards by providing its borrowing member countries—middle-income and creditworthy poorer countries—with loans, guarantees, risk management, and other financial services, as well as analytical and advisory services. It provides these client countries with risk management tools and access to capital on favorable terms in larger volumes, with longer maturities, and in a more sustainable manner than the market in several important ways: By supporting long-term human and social development needs that private creditors do not

finance By preserving borrowers’ financial strength through support during crisis periods, which is

when poor people are most adversely affected By using the leverage of financing to promote key policy and institutional reforms (such as

safety net or anticorruption reforms) By creating a favorable investment climate to catalyze the provision of private capital

By providing financial support (in the form of grants made available from IBRD’s net income) in areas critical to the well-being of poor people in all countries.

IBRD is structured like a cooperative that is owned and operated for the benefit of its 187 member countries. Shareholders of IBRD are sovereign governments, and its borrowing members, through their representatives on the Board of Executive Directors, have a voice in setting its policies and approving each project and loan. IBRD finances its activities primarily by issuing AAA-rated bonds to institutional and retail investors in global capital markets. IBRD’s financial objective is not to maximize profit, but to earn adequate income to ensure its financial strength and to sustain its development activities. Although IBRD earns a small margin on this lending, the greater proportion of its income comes from investing its own capital. This capital consists of reserves built up over the years and money paid in from the Bank’s 187 member country shareholders. IBRD’s income also pays for World Bank operating expenses and has contributed to IDA, debt relief, and other development causes.

The International Development AssociationAfter the rebuilding of Europe following World War II, the Bank turned its attention to the newly independent developing countries. It became clear that the poorest developing countries could not afford to borrow capital for development on the terms offered by the Bank; hence, a group of Bank member countries decided to found IDA as an institution that could lend to very poor developing nations on easier terms. To imbue IDA with the discipline of a bank, these countries agreed that IDA should be part of the World Bank. IDA began operating in 1960.

IDA partners with the world’s poorest countries to reduce poverty by providing credits and grants. Credits are loans at zero or low interest with a 10-year grace period before repayment of principal begins and with maturities of 20 to 40 years. These credits are often referred to as concessional lending. IDA credits help build the human capital, policies, institutions, and physical infrastructure that these countries urgently need to achieve faster, environmentally sustainable growth. IDA-financed operations address primary education, basic health services, clean water and sanitation, environmental safeguards, business climate improvements, infrastructure, and institutional reforms. These projects pave the way toward economic growth, job creation, higher incomes, and better living conditions.IDA is funded largely by contributions from the governments of its high-income member countries. Representatives of donor countries meet every three years to replenish IDA funds. Since 1960, IDA has lent $222 billion. Annual lending figures have increased steadily and have averaged about $14 billion over the past two years. Additional funds come from World Bank Group transfers and from borrowers’ repayments of earlier IDA credits, including voluntary and contractual acceleration of credit repayments from eligible IDA graduates.Donor contributions to the 16th replenishment of IDA, known as IDA16, amounted to $49.3 billion, an 18 percent increase over the previous replenishment.

These resources will finance IDA’s commitments over the three year period ending June 30, 2014. This strong outcome was the result of a global coalition of traditional and new donors, borrowing countries, and the World Bank Group, involving the continuing support of traditional donors, IDA graduates agreeing to accelerate their credit repayments to IDA, economically more advanced. IDA countries contributing through differentiated borrowing terms, a number of new donors joining, and several existing donors increasing their contributions.Fifty-two donor countries pledged to contribute to IDA16, including traditional donors and emerging donors. IDA’s largest direct contributions continue to come from the Group of Seven and other Organization for Economic Co-operation and Development (OECD) countries. However, emerging donors play an increasingly important role, with IDA graduates such as China, the Arab Republic of Egypt, the Republic of Korea, the Philippines, and Turkey now joining as donors.IDA lends to countries that lack the financial ability to borrow from IBRD and that in fiscal year 2011 had an annual per capita income of less than $1,165. Together these countries are home to around 2.5 billion people, half the total population of the developing world. An estimated 1.5 billion people there survive on incomes of $2 or less a day. Blend borrower countries, such as India, Uzbekistan, and Vietnam, are eligible for IDA loans because of their low per capita incomes while also being eligible for IBRD loans because they are financially creditworthy. Seventy-nine countries are currently eligible to borrow from IDA.IDA eligibility is a transitional arrangement that gives the poorest countries access to substantial resources before they are capable of obtaining the financing they need from commercial markets. As their economies grow, countries graduate from IDA eligibility. The repayments, or reflows, that they make on IDA loans are used to help finance new IDA loans to the remaining poor countries. Some 35 countries have graduated from IDA since its founding. Examples include, in addition to the countries listed previously, Albania, Botswana, Chile, Costa Rica, Morocco, and Thailand. Eight countries subsequently “reverse graduated,” however, and once again became IDA eligible.

The International Finance CorporationIFC’s three businesses—investment services, advisory services, and asset management—foster sustainable economic growth in developing countries by financing private sector investment, mobilizing capital in the international financial markets, providing advisory services to businesses and governments, and channeling finance to the poor. IFC helps companies and financial institutions in emerging markets create jobs, generate tax revenues, improve corporate governance and environmental performance, and contribute to their local communities. The goal is to improve lives, especially for the people who most need the benefits of growth.Since its founding in 1956, IFC has committed more than $100 billion of its own funds for private sector investment in the developing world, and it has mobilized additional billions from

others. With funding support from donors, it has provided more than $1.7 billion in advisory services since 2001.Direct lending to businesses is the fundamental contrast between IFC and the World Bank: under their Articles of Agreement, IBRD and IDA can lend only to the governments of member countries. IFC was founded specifically to address this limitation of World Bank lending. IFC provides equity finance, long-term loans, syndicated loans, loan guarantees, structured finance and risk management products, and advisory services to its clients. It seeks to reach businesses in regions and countries that otherwise would have limited access to capital. It provides financing in markets deemed too risky by commercial investors in the absence of IFC participation.IFC also supports the projects it finances by providing advice to businesses and governments on access to finance, corporate governance, environmental and social sustainability, the investment climate, and infrastructure. Much of the advisory work is funded by IFC’s donor partners, through trust funds, or through facilities with a regional or thematic focus.To maximize its effect on development, IFC emphasizes five strategic priorities: strengthening the focus on frontier markets; building long-term client relationships in emerging markets; addressing climate change and ensuring environmental and social sustainability; addressing constraints to private sector growth in infrastructure, health, education, and the food supply chain; and developing domestic financial markets.

Project financingIFC offers an array of financial products and services to companies in its developing member countries: Loans for IFC’s account Equity investments Syndications Structured and securitized finance Trade finance Quasi-equity finance Equity and debt funds Intermediary services Risk management products Local currency finance Subnational financeIt can also combine its financial products and services with advice tailored to the needs of each client. The bulk of the funding, as well as leadership and management responsibility, however, lies with the private sector owners. IFC charges market rates for its products and does not accept government guarantees. Therefore, it carefully reviews the likelihood of success for each enterprise. To be eligible for IFC financing, projects must be profitable for investors, must benefit the economy of the host country, and must comply with IFC’s environmental and social standards.

IFC finances projects in all types of industries and sectors, including manufacturing, infrastructure, tourism, health, education, and financial services. Financial services projects are the largest component of IFC’s portfolio, and they cover the full range of financial institutions, including banks, leasing companies, stock markets, credit-rating agencies, and venture capital funds. IFC does not lend directly to microenterprises, to small and medium size enterprises, or to individual entrepreneurs; however, many of its investment clients are financial intermediaries that on-lend to smaller businesses.Even though IFC is primarily a financier of private sector projects, it may provide financing for a company with some government ownership, provided there is private sector participation and the venture is run on a commercial basis.To ensure participation by investors and lenders from the private sector,IFC limits the total amount of own-account debt and equity financing it will provide for any single project. For new projects, the maximum amount is 25 percent of the total estimated project costs or, on an exceptional basis, up to 35 percent for small projects. For expansion projects, IFC may provide up to 50 percent of the total project costs, provided that its investments do not exceed 25 percent of the total capitalization of the project company. IFC investments typically range from $1 million to $100 million.

Resource mobilizationThrough its syndicated loan (or B-loan) program, IFC offers commercial banks and other financial institutions the chance to lend to IFC-financed projects that they might not otherwise consider. These loans are a key part of IFC’s efforts to mobilize additional private sector financing in developing countries and to broaden its development effects. Through this mechanism, financial institutions share fully in the commercial credit risk of projects, whereas IFC remains the lender of record. Participants in IFC’s B-loans share the advantages that IFC derives as a multilateral development institution, including preferred creditor access to foreign exchange in the event of a foreign currency crisis in a particular country. Where applicable, these participant banks are also exempted from the mandatory country-risk provisioning requirements that regulatory authorities may impose if these banks lend directly to projects in developing countries.

Advisory servicesIFC supports private sector development both by investing and by providing advisory services that build businesses. Its advisory services are organized into five business lines: access to finance, corporate advice, environmental and social sustainability, investment climate, and infrastructure. Much of IFC’s advisory services work is conducted through facilities managed by IFC but funded through partnerships with donor governments and other multilateral institutions. Some facilities operate within specific regions, and others are concerned with such cross-cutting themes as carbon finance, cleaner technologies, social responsibility, sustainable investing, investment climate, and gender.

Asset managementA new line of business for IFC is asset management, part of a financial intermediation model in development that allows long-term investors to take advantage of growth opportunities in Africa and other less developed regions. The objective is to increase the supply of long-term equity capital to developing and frontier markets in a way that enhances IFC’s development goals and generates profits for investors.

The Multilateral Investment Guarantee AgencyBy providing political risk insurance (PRI), or guarantees, to investors and lenders against losses caused by noncommercial risks, MIGA promotes foreign direct investment (FDI) in emerging economies and thereby contributes to economic growth, poverty reduction, and the improvement of living standards.Projects financed by MIGA create jobs; provide water, electricity, and other basic infrastructure; strengthen financial systems; generate tax revenues; transfer skills and technological know-how; and allow countries to tap natural resources in an environmentally sustainable way. MIGA helps investors and lenders by insuring projects against losses related to currency inconvertibility and transfer restriction, expropriation, war and civil disturbance, breach of contract, and failure to honor sovereign financial obligations.MIGA insures cross-border investments made by investors from a MIGA member country into a developing country that is also a member of MIGA. Its operational strategy, which is designed to attract investors and private insurers into difficult operating environments, focuses on four priorities where it can make the greatest difference: Investments in IDA-eligible countries. These markets typically have the most need and stand

to benefit the most from foreign investment, but they are not well served by the private insurance market.

Investments in conflict-affected countries. Although these countries tend to attract considerable donor goodwill once conflict ends, aid flows eventually decline. With many investors wary of potential risks, PRI is essential to bring in investment.

Investments in complex projects, mostly in infrastructure and the extractive industries. Given that 1.6 billion people still do not have electricity and 2.3 billion depend on traditional biomass fuels, investments in these sectors are critical for the world’s poorest nations.

Support for South-South investments. Investments between developing countries are contributing an ever-increasing proportion of FDI flows. But private insurers or national export credit agencies in these countries, if they exist at all, are often not sufficiently developed and lack the ability and capacity to provide PRI.

Development effects and prioritiesSince its creation in 1988, MIGA has provided more than $22 billion in guarantees (PRI) for more than 600 projects in more than 100 developing countries. MIGA is committed to promoting

socially, economically, and environmentally sustainable projects that are, above all, developmentally responsible. Projects that MIGA supports have widespread benefits, such as generating jobs and taxes and transferring skills and know-how. In addition, local communities often receive significant secondary benefits through improved infrastructure. Projects encourage similar local investments and spur the growth of local businesses. MIGA ensures that projects are aligned with World Bank Group Country Assistance Strategies and integrate the best environmental, social, and governance practices.MIGA helps countries define and implement strategies to promote investment through technical assistance services managed by the Foreign Investment Advisory Services of the World Bank Group. Through this vehicle, MIGA’s technical assistance is facilitating new investments in some of the most challenging business environments in the world. As part of its mandate to support FDI in emerging markets, MIGA also shares knowledge on political risk and FDI through its website and through the Political Risk Insurance Center, which is a free service providing in-depth analysis on political risk environments and management issues affecting 160 countries.The agency uses its legal services to protect the investments it supports and to remove possible obstacles to future investment by working with governments and investors to resolve any differences.

Added valueMIGA gives private investors the confidence they need to make sustainable investments in developing countries. As part of the World Bank Group,MIGA brings security and credibility to an investment, acting as a potent deterrent against government actions that may adversely affect investments.If disputes do arise, the agency’s leverage with host governments frequently enables it to resolve differences to the mutual satisfaction of all parties.MIGA is a leader in assessing and managing political risks, developing new products and services, and finding innovative ways to meet clients’ needs.The agency can also enable complex transactions to go ahead by offering innovative coverage of the nontraditional sub sovereign risks. MIGA complements the activities of other investment insurers and works with partners through its coinsurance and reinsurance programs. By doing so, it expands the capacity of the PRI industry and encourages private sector insurers to enter into transactions they would not otherwise have undertaken. MIGA’s guarantees can be used on a stand-alone basis or in conjunction with other World Bank instruments, which offer an additional set of benefits.

CHAPTER 3: IMF

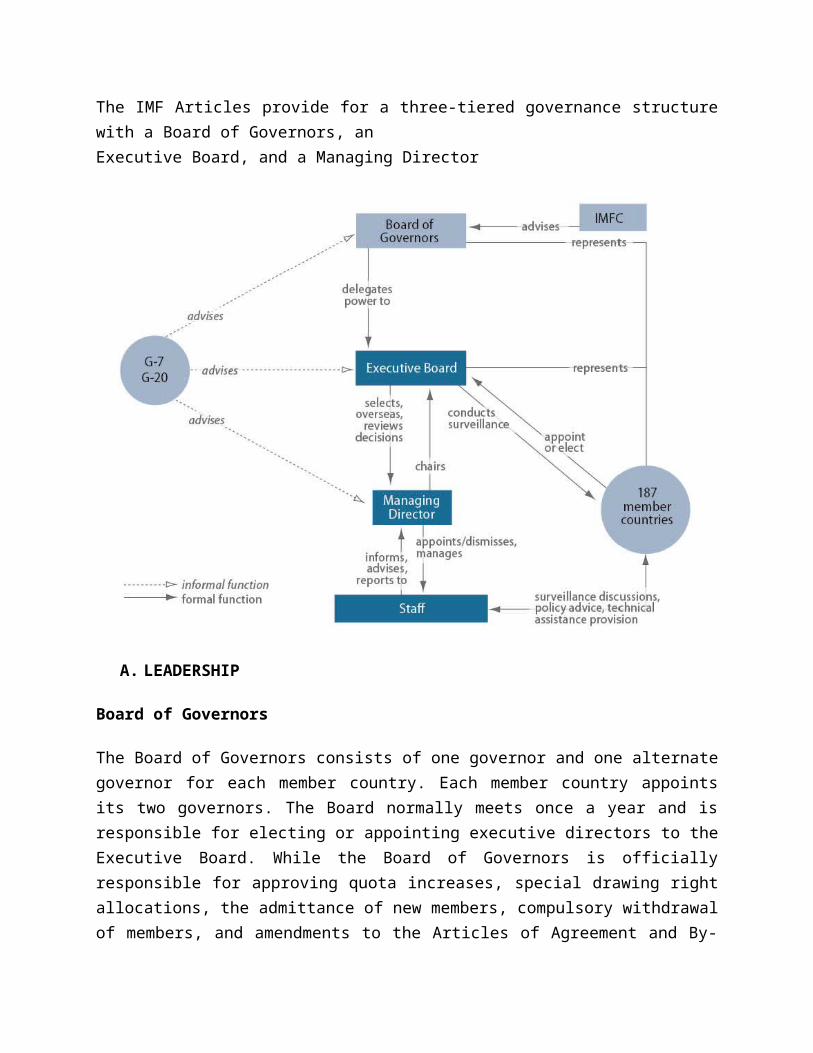

2.1 ORGANIZATIONAL STRUCTUREThe IMF Articles provide for a three-tiered governance structure with a Board of Governors, anExecutive Board, and a Managing Director

A. LEADERSHIP

Board of Governors

The Board of Governors consists of one governor and one alternate governor for each member country. Each member country appoints its two governors. The Board normally meets once a year and is responsible for electing or appointing executive directors to the Executive Board. While the Board of Governors is officially responsible for approving quota increases, special drawing right allocations, the admittance of new members, compulsory withdrawal of members, and amendments to the Articles of Agreement and By-Laws, in practice it has delegated most of its powers to the IMF's Executive Board.

The Board of Governors is advised by the International Monetary and Financial Committee and the Development Committee. The International Monetary and Financial Committee has 24

members and monitors developments in global liquidity and the transfer of resources to developing countries. The Development Committee has 25 members and advises on critical development issues and on financial resources required to promote economic development in developing countries. They also advise on trade and global environmental issues.

Executive Board

24 Executive Directors make up Executive Board. The Executive Directors represent all 188 member-countries. Countries with large economies have their own Executive Director, but most countries are grouped in constituencies representing four or more countries.

Following the 2008 Amendment on Voice and Participation, eight countries each appoint an Executive Director: the United States, Japan, Germany, France, the United Kingdom, China, the Russian Federation, and Saudi Arabia. The remaining 16 Directors represent constituencies consisting of 4 to 22 countries. The Executive Director representing the largest constituency of 22 countries accounts for 1.55% of the vote.

Managing Director

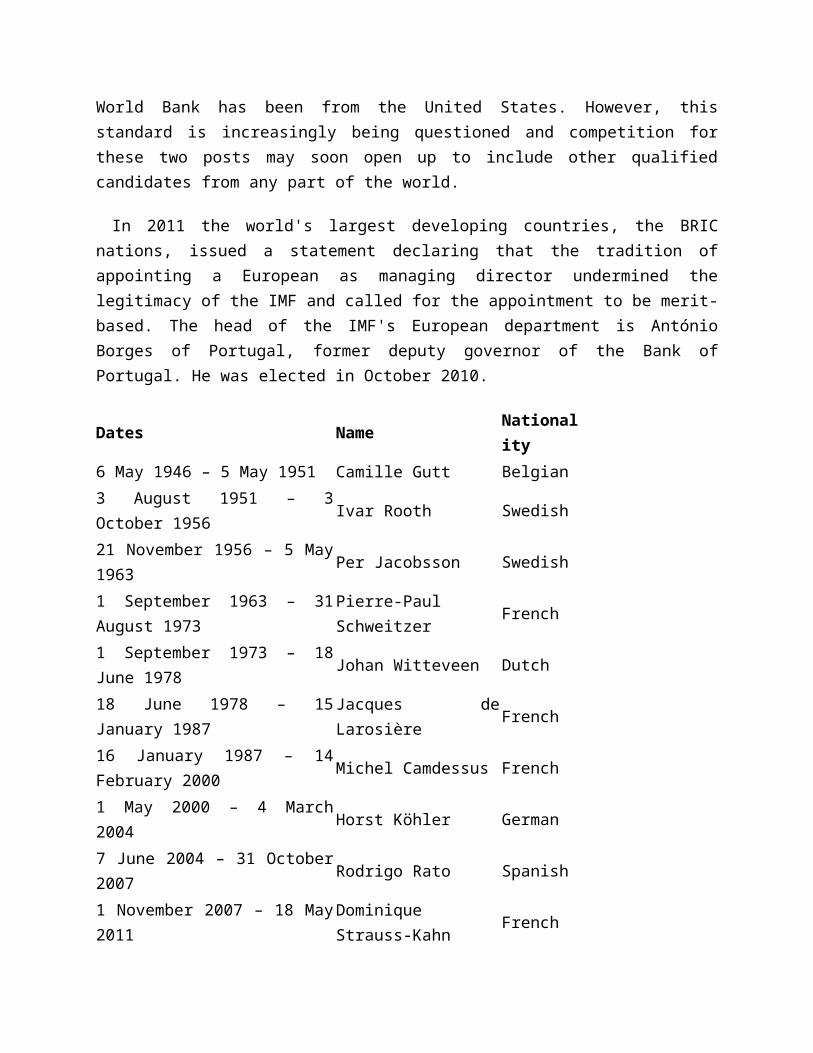

The IMF is led by a managing director, who is head of the staff and serves as Chairman of the Executive Board. The managing director is assisted by a First Deputy managing director and three other Deputy Managing Directors. Historically the IMF's managing director has been European and the president of the World Bank has been from the United States. However, this standard is increasingly being questioned and competition for these two posts may soon open up to include other qualified candidates from any part of the world.

In 2011 the world's largest developing countries, the BRIC nations, issued a statement declaring that the tradition of appointing a European as managing director undermined the legitimacy of the IMF and called for the appointment to be merit-based. The head of the IMF's European department is António Borges of Portugal, former deputy governor of the Bank of Portugal. He was elected in October 2010.

Dates Name Nationality

6 May 1946 – 5 May 1951 Camille Gutt Belgian

3 August 1951 – 3 October 1956 Ivar Rooth Swedish

21 November 1956 – 5 May 1963 Per Jacobsson Swedish

1 September 1963 – 31 August 1973 Pierre-Paul Schweitzer French

1 September 1973 – 18 June 1978 Johan Witteveen Dutch

18 June 1978 – 15 January 1987 Jacques de Larosière French

16 January 1987 – 14 February 2000 Michel Camdessus French

1 May 2000 – 4 March 2004 Horst Köhler German

7 June 2004 – 31 October 2007 Rodrigo Rato Spanish

1 November 2007 – 18 May 2011 Dominique Strauss-Kahn French

5 July 2011 – Christine Lagarde French

On 28 June 2011, Christine Lagarde was named managing director of the IMF, replacing Dominique Strauss-Kahn. Previous managing director Dominique Strauss-Kahn was arrested in connection with charges of sexually assaulting a New York room attendant. Strauss-Kahn subsequently resigned his position on 18 May. On 28 June 2011 Christine Lagarde was confirmed as managing director of the IMF for a five-year term starting on 5 July 2011.

Ministerial Committees

The IMF Board of Governors is advised by two ministerial committees, the International Monetary and Financial Committee (IMFC) and the Development Committee.

The IMFC has 24 members, drawn from the pool of 187 governors. Its structure mirrors that of the Executive Board and its 24 constituencies. As such, the IMFC represents all the member countries of the Fund.

The IMFC meets twice a year, during the Spring and Annual Meetings. The Committee discusses matters of common concern affecting the global economy and also advises the IMF on the direction its work. At the end of the Meetings, the Committee issues a joint communiqué summarizing its views. These communiqués provide guidance for the IMF's work program during the six months leading up to the next Spring or Annual Meetings. There is no formal voting at the IMFC, which operates by consensus.

The Development Committee is a joint committee, tasked with advising the Boards of Governors of the IMF and the World Bank on issues related to economic development in emerging and developing countries. The committee has 24 members (usually ministers of finance or development). It represents the full membership of the IMF and the World Bank and mainly serves as a forum for building intergovernmental consensus on critical development issues.

Governance Reform

To be effective, the IMF must be seen as representing the interests of all its 188 member countries. For this reason, it is crucial that its governance structure reflect today’s world economy. In 2010, the IMF agreed wide-ranging governance reforms to reflect the increasing

importance of emerging market countries. The reforms also ensure that smaller developing countries will retain their influence in the IMF.

B. MEMBER COUNTRIES

The 188 members of the IMF include 187 members of the UN and the Republic of Kosovo. All members of the IMF are also International Bank for Reconstruction and Development (IBRD) members and vice versa.

Former members are Cuba (which left in 1964) and the Republic of China, which was ejected from the UN in 1980 after losing the support of then US President Jimmy Carter and was replaced by the People's Republic of China. However, "Taiwan Province of China" is still listed in the official IMF indices. Apart from Cuba, the other UN states that do not belong to the IMF are Andorra, Liechtenstein, Monaco, Nauru and North Korea.

The former Czechoslovakia was expelled in 1954 for "failing to provide required data" and was readmitted in 1990, after the Velvet Revolution. Poland withdrew in 1950—allegedly pressured by the Soviet Union—but returned in 1986.

Qualifications

Any country may apply to be a part of the IMF. Post-IMF formation, in the early postwar period, rules for IMF membership were left relatively loose. Members needed to make periodic membership payments towards their quota, to refrain from currency restrictions unless granted IMF permission, to abide by the Code of Conduct in the IMF Articles of Agreement, and to provide national economic information. However, stricter rules were imposed on governments that applied to the IMF for funding.

The countries that joined the IMF between 1945 and 1971 agreed to keep their exchange rates secured at rates that could be adjusted only to correct a "fundamental disequilibrium" in the balance of payments, and only with the IMF's agreement. Some members have a very difficult relationship with the IMF and even when they are still members they do not allow themselves to be monitored. Argentina for example refuses to participate in an Article IV Consultation with the IMF.

Benefits

Member countries of the IMF have access to information on the economic policies of all member countries, the opportunity to influence other members’ economic policies, technical assistance in

banking, fiscal affairs, and exchange matters, financial support in times of payment difficulties, and increased opportunities for trade and investment.

2.2 FUNCTIONS OF THE IMF In practice, the IMF’s mandate of promoting international monetary stability translates into threemain functions: (1) surveillance of financial and monetary conditions in its member countries andin the world economy; (2) financial assistance to help countries overcome major balance-ofpaymentsproblems; and (3) technical assistance and advisory services to member countries.

A. SURVEILLANCEWhen a country joins the IMF, it agrees to subject its economic and financial policies to the scrutiny of the international community. It also makes a commitment to pursue policies that are conducive to orderly economic growth and reasonable price stability, to avoid manipulating exchange rates for unfair competitive advantage, and to provide the IMF with data about its economy. The IMF's regular monitoring of economies and associated provision of policy advice is intended to identify weaknesses that are causing or could lead to financial or economic instability. This process is known as surveillance.

Country surveillance

Country surveillance is an ongoing process that culminates in regular (usually annual) comprehensive consultations with individual member countries, with discussions in between as needed. The consultations are known as "Article IV consultations" because they are required by Article IV of the IMF's Articles of Agreement. During an Article IV consultation, an IMF team of economists visits a country to assess economic and financial developments and discuss the country's economic and financial policies with government and central bank officials. IMF staff missions also often meet with parliamentarians and representatives of business, labor unions, and civil society.

The team reports its findings to IMF management and then presents them for discussion to the Executive Board, which represents all of the IMF's member countries. A summary of the Board's views is subsequently transmitted to the country's government. In this way, the views of the global community and the lessons of international experience are brought to bear on national policies. Summaries of most discussions are released in Press Releases and are posted on the IMF's web site, as are most of the country reports prepared by the staff.

Regional surveillance

Regional surveillance involves examination by the IMF of policies pursued under currency unions—including the euro area, the West African Economic and Monetary Union, the Central African Economic and Monetary Community, and the Eastern Caribbean Currency Union. Regional economic outlook reports are also prepared to discuss economic developments and key policy issues in Asia Pacific, Europe, Middle East and Central Asia, Sub-Saharan Africa, and the Western Hemisphere.

Global surveillance

Global surveillance entails reviews by the IMF's Executive Board of global economic trends and developments. The main reviews are based on the World Economic Outlook reports, the Global Financial Stability Report, which covers developments, prospects, and policy issues in international financial markets, and the Fiscal Monitor, which analyzes the latest developments in public finance. All three reports are published twice a year, with updates being provided on a quarterly basis. In addition, the Executive Board holds more frequent informal discussions on world economic and market developments.

B. FINANCIAL ASSISTANCE

Notwithstanding its macroeconomic surveillance, the IMF is perceived as an institution thatprimarily provides temporary financing to troubled economies. The IMF’s financial structure canbest be characterized as that of a credit union (see box). IMF member countries deposit hardcurrency and some of their own currency, from which they can draw the currencies of othercountries if they face significant problems in managing their balance of payments. As notedabove, supplemental resources are available from the NAB or GAB if quota resources are insufficient.

In the past, there have been debates about whether the austerity conditions that are often the coreof IMF conditionality are productive in increasing economic growth. In 2000, one heavily citedpaper found that participating in IMF programs lowers growth rates during the program, as wouldbe expected. In addition, however, the study found that once countries leave the program, theygrow faster than if they had remained, but not faster than they would have without participating inthe IMF program in the first place.20After heavy criticism of the conditions attached to IMF loans to East Asia in the late 1990s, theIMF revamped its conditionality guidelines in 2002. Additional reforms, including new IMFlending instruments based on economic prequalification (ex-ante conditionality) rather thantraditional structural adjustment (ex-post conditionality) also address these concerns.21

C. IMF LOAN PROGRAMS

The changing nature of lending Lending to preserve financial stability Conditions for lending Main lending facilities Helping low-income countries Debt relief

A country in severe financial trouble, unable to pay its international bills, poses potential problems for the stability of the international financial system, which the IMF was created to protect. Any member country, whether rich, middle-income, or poor, can turn to the IMF for financing if it has a balance of payments need—that is, if it cannot find sufficient financing on affordable terms in the capital markets to make its international payments and maintain a safe level of reserves.

IMF loans are meant to help member countries tackle balance of payments problems, stabilize their economies, and restore sustainable economic growth. This crisis resolution role is at the core of IMF lending. At the same time, the global financial crisis has highlighted the need for effective global financial safety nets to help countries cope with adverse shocks. A key objective of recent lending reforms has therefore been to complement the traditional crisis resolution role of the IMF with more effective tools for crisis prevention.

The IMF is not a development bank and, unlike the World Bank and other development agencies, it does not finance projects.

The changing nature of lending

About four out of five member countries have used IMF credit at least once. But the amount of loans outstanding and the number of borrowers have fluctuated significantly over time.

In the first two decades of the IMF's existence, more than half of its lending went to industrial countries. But since the late 1970s, these countries have been able to meet their financing needs in the capital markets.

The oil shock of the 1970s and the debt crisis of the 1980s led many lower- and lower-middle-income countries to borrow from the IMF.

In the 1990s, the transition process in central and eastern Europe and the crises in emerging market economies led to a further increase in the demand for IMF resources.

In 2004, benign economic conditions worldwide meant that many countries began to repay their loans to the IMF. As a consequence, the demand for the Fund’s resources dropped off sharply .

But in 2008, the IMF began making loans to countries hit by the global financial crisis The IMF currently has programs with more than 50 countries around the world and has committed more than $325 billion in resources to its member countries since the start of the global financial crisis.

While the financial crisis has sparked renewed demand for IMF financing, the decline in lending that preceded the financial crisis also reflected a need to adapt the IMF's lending instruments to the changing needs of member countries. In response, the IMF conducted a wide-ranging review of its lending facilities and terms on which it provides loans.

In March 2009, the Fund announced a major overhaul of its lending framework, including modernizing conditionality, introducing a new flexible credit line, enhancing the flexibility of the Fund’s regular stand-by lending arrangement, doubling access limits on loans, adapting its cost structures for high-access and precautionary lending, and streamlining instruments that were seldom used. It has also speeded up lending procedures and redesigned its Exogenous Shocks Facility to make it easier to access for low-income countries. More reforms have since been undertaken, most recently in November 2011.

Lending to preserve financial stability

Article I of the IMF's Articles of Agreement states that the purpose of lending by the IMF is "...to give confidence to members by making the general resources of the Fund temporarily available to them under adequate safeguards, thus providing them with opportunity to correct maladjustments in their balance of payments without resorting to measures destructive of national or international prosperity."

In practice, the purpose of the IMF's lending has changed dramatically since the organization was created. Over time, the IMF's financial assistance has evolved from helping countries deal with short-term trade fluctuations to supporting adjustment and addressing a wide range of balance of payments problems resulting from terms of trade shocks, natural disasters, post-conflict situations, broad economic transition, poverty reduction and economic development, sovereign debt restructuring, and confidence-driven banking and currency crises.

Today, IMF lending serves three main purposes.

First, it can smooth adjustment to various shocks, helping a member country avoid disruptive economic adjustment or sovereign default, something that would be extremely costly, both for the country itself and possibly for other countries through economic and financial ripple effects (known as contagion).

Second, IMF programs can help unlock other financing, acting as a catalyst for other lenders. This is because the program can serve as a signal that the country has adopted sound policies, reinforcing policy credibility and increasing investors' confidence.

Third, IMF lending can help prevent crisis. The experience is clear: capital account crises typically inflict substantial costs on countries themselves and on other countries through contagion. The best way to deal with capital account problems is to nip them in the bud before they develop into a full-blown crisis.

Conditions for lending

When a member country approaches the IMF for financing, it may be in or near a state of economic crisis, with its currency under attack in foreign exchange markets and its international reserves depleted, economic activity stagnant or falling, and a large number of firms and households going bankrupt. In difficult economic times, the IMF helps countries to protect the most vulnerable in a crisis.

The IMF aims to ensure that conditions linked to IMF loan disbursements are focused and adequately tailored to the varying strengths of members' policies and fundamentals. To this end, the IMF discusses with the country the economic policies that may be expected to address the problems most effectively. The IMF and the government agree on a program of policies aimed at achieving specific, quantified goals in support of the overall objectives of the authorities' economic program. For example, the country may commit to fiscal or foreign exchange reserve targets.

The IMF discusses with the country the economic policies that may be expected to address the problems most effectively. The IMF and the government agree on a program of policies aimed at achieving specific, quantified goals in support of the overall objectives of the authorities' economic program. For example, the country may commit to fiscal or foreign exchange reserve targets.

Loans are typically disbursed in a number of installments over the life of the program, with each installment conditional on targets being met. Programs typically last up to 3 years, depending on the nature of the country's problems, but can be followed by another program if needed. The government outlines the details of its economic program in a "letter of intent" to the Managing Director of the IMF. Such letters may be revised if circumstances change.

For countries in crisis, IMF loans usually provide only a small portion of the resources needed to finance their balance of payments. But IMF loans also signal that a country's economic policies are on the right track, which reassures investors and the official community, helping countries find additional financing from other sources.

Main lending facilities

In an economic crisis, countries often need financing to help them overcome their balance of payments problems. Since its creation in June 1952, the IMF’s Stand-By Arrangement (SBA) has been used time and again by member countries, it is the IMF’s workhorse lending instrument for emerging market countries. Rates are non-concessional, although they are almost always lower than what countries would pay to raise financing from private markets. The SBA was upgraded in 2009 to be more flexible and responsive to member countries’ needs. Borrowing limits were doubled with more funds available up front, and conditions were streamlined and simplified. The new framework also enables broader high-access borrowing on a precautionary basis.

The Flexible Credit Line (FCL) is for countries with very strong fundamentals, policies, and track records of policy implementation. It represents a significant shift in how the IMF delivers Fund financial assistance, particularly with recent enhancements, as it has no ongoing (ex post) conditions and no caps on the size of the credit line. The FCL is a renewable credit line, which at the country’s discretion could be for either 1-2 years, with a review of eligibility after the first year. There is the flexibility to either treat the credit line as precautionary or draw on it at any time after the FCL is approved. Once a country qualifies (according to pre-set criteria), it can tap all resources available under the credit line at any time, as disbursements would not be phased and conditioned on particular policies as with traditional IMF-supported programs. This is justified by the very strong track records of countries that qualify to the FCL, which give confidence that their economic policies will remain strong or that corrective measures will be taken in the face of shocks.