brexit report, what does this "calamity" mean to your portfolio?

TRANSCRIPT

22016 Midyear Outlook Eyes on the Horizon

A Letter to Investors from Darrell CronkWe’ve been through a lot in the first half of 2016. We began January with the worst start to a calendar year in history for domestic equities. Concerns about China’s growth rate, slowing U.S. growth, and a new downturn in oil prices had many questioning the viability of the recovery and an aging bull market.

A climax of negative sentiment finally arrived in February only to see markets fully recover in April and May to levels approaching 2015 highs. We also celebrated the seven-year anniversary of the current U.S. equity bull market in March, and by the end of April, we found ourselves in the second longest bull market in history, surpassed only by the bull market from 1987 to 2000.

Let’s reflect on the five major changes we anticipated in our 2016 Outlook with an eye toward what we expect between now and year-end. We believe the five changes we discussed in our December report are as relevant today as they were then.

The first two changes, Changing Consumer Behavior and Change in the Political Landscape, are exactly where we expected them to be at midyear. Consumer spending remains the bulwark of U.S. and global economic growth. Despite a tepid start, spending is now accelerating at midyear as consumers benefit from lower energy prices and improved labor markets. We believe that the consumer is poised to increase spending even more in the second half of this year.

Separately, this election year is shaping up to be one of the more important in recent memory as all three branches of government (executive, legislative, and judicial) remain in flux. Divergent views, Washington gridlock, and important progress needed on key policy issues mean that investors will need to remain vigilant in understanding evolving political agendas and their implications for financial markets. Later in this report, we outline key factors about this election for investors to watch.

Last December, we also highlighted a continuing Shift in Monetary Policy. We had expected the Federal Reserve (Fed) to moderate its guidance for interest-rate hikes, and we forecast that other major central banks’ easing policy initiatives would widen the global interest-rate differentials. That is exactly what has transpired during the first half of this year as tepid growth and global instability led the Fed and the markets to downshift their interest-rate expectations closer to our outlook during the first quarter of 2016. Simultaneously, the Bank of Japan and European Central Bank continued down their paths of easing monetary policy.

Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value

52016 Midyear Outlook Eyes on the Horizon

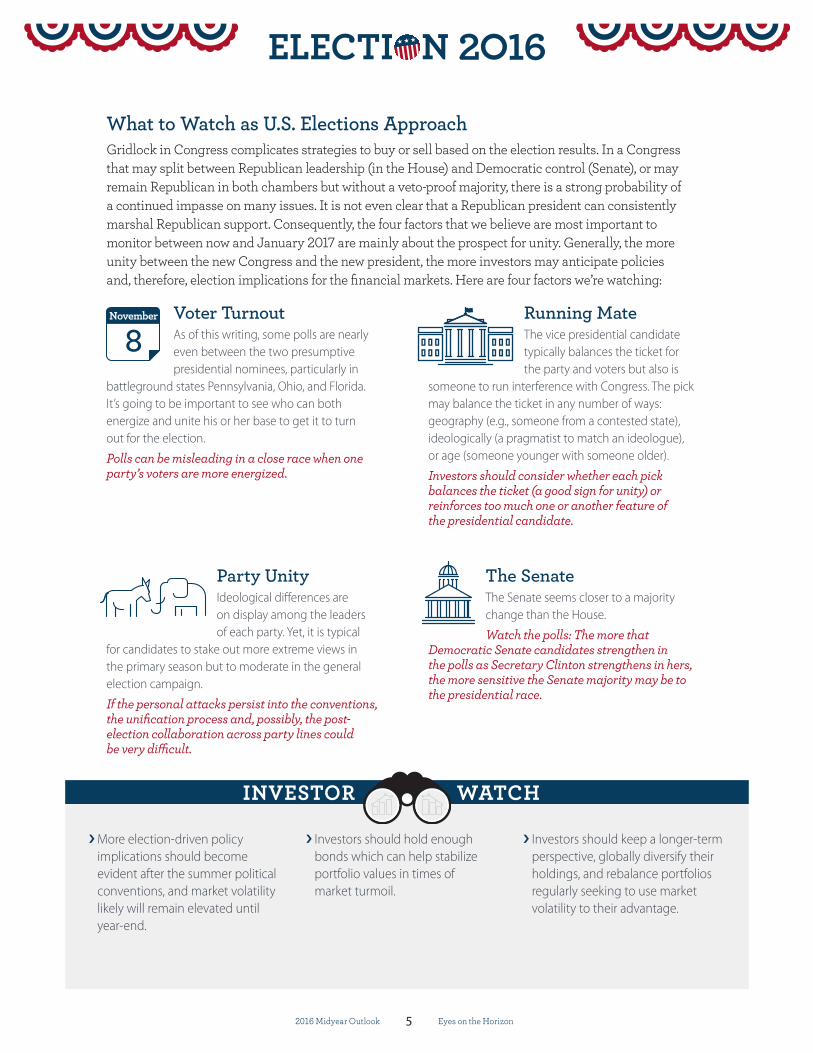

What to Watch as U.S. Elections ApproachGridlock in Congress complicates strategies to buy or sell based on the election results. In a Congress that may split between Republican leadership (in the House) and Democratic control (Senate), or may remain Republican in both chambers but without a veto-proof majority, there is a strong probability of a continued impasse on many issues. It is not even clear that a Republican president can consistently marshal Republican support. Consequently, the four factors that we believe are most important to monitor between now and January 2017 are mainly about the prospect for unity. Generally, the more unity between the new Congress and the new president, the more investors may anticipate policies and, therefore, election implications for the financial markets. Here are four factors we’re watching:

Voter TurnoutAs of this writing, some polls are nearly even between the two presumptive presidential nominees, particularly in

battleground states Pennsylvania, Ohio, and Florida. It’s going to be important to see who can both energize and unite his or her base to get it to turn out for the election.

Polls can be misleading in a close race when one party’s voters are more energized.

Running MateThe vice presidential candidate typically balances the ticket for the party and voters but also is

someone to run interference with Congress. The pick may balance the ticket in any number of ways: geography (e.g., someone from a contested state), ideologically (a pragmatist to match an ideologue), or age (someone younger with someone older).

Investors should consider whether each pick balances the ticket (a good sign for unity) or reinforces too much one or another feature of the presidential candidate.

Party UnityIdeological differences are on display among the leaders of each party. Yet, it is typical

for candidates to stake out more extreme views in the primary season but to moderate in the general election campaign.

If the personal attacks persist into the conventions, the unification process and, possibly, the post-election collaboration across party lines could be very difficult.

The SenateThe Senate seems closer to a majority change than the House.

Watch the polls: The more that Democratic Senate candidates strengthen in the polls as Secretary Clinton strengthens in hers, the more sensitive the Senate majority may be to the presidential race.

INVESTOR WATCH

More election-driven policy implications should become evident after the summer political conventions, and market volatility likely will remain elevated until year-end.

Investors should hold enough bonds which can help stabilize portfolio values in times of market turmoil.

Investors should keep a longer-term perspective, globally diversify their holdings, and rebalance portfolios regularly seeking to use market volatility to their advantage.

8November

72016 Midyear Outlook Eyes on the Horizon

Global inflation pressures remain subdued along with global growth and commodity prices. Inflation trends are rising from a near-zero pace to more historically typical levels in some developed economies, including the U.S., but the normalization is slow, especially in Europe and Japan. Inflation risks in emerging economies have been more balanced—lower commodity prices and weak trade have offset higher pricing pressures via accumulated currency depreciation since 2014.

U.S. Dollar Appreciation on Hold for a While LongerThe U.S. dollar weakened in the first quarter, reflecting a changing global monetary policy environment. Despite negative interest rates across Japan and parts of Europe, the dollar’s recent reversal lower seems to acknowledge the sentiment that extraordinary monetary stimulus now faces much stronger headwinds than it did previously from low oil prices, contracting global trade, and weak China growth. As the dollar turned lower, many emerging-market currencies reversed higher from deeply pessimistic valuations, but these same factors may limit their further gains. Considering the muted influence of monetary policy, we think the dollar could finish the year close to current values but may swing significantly higher and lower in the meantime.

Furthermore, some major risk events—new and closely watched elections in Europe and the U.S. and potentially another summer cash crisis in Greece—could cause sharp dollar moves higher or lower. Recent short-term monetary policy impotence and upcoming event risks do not suggest a quick resumption of dollar strength but also may fail to sustain a dollar downtrend.

Main Risks to Our OutlookOne principal risk to our economic and dollar outlook is that a new swoon in oil prices or trade, or new Chinese economic stress, may undermine the faster second-half economic pace we expect in the U.S., Europe, and developed Asia. For perspective, we see ongoing economic growth and put the probability of a U.S. recession at no more than 25 percent this year.

What is our forecast for the U.S. dollar?

We believe the U.S. dollar’s key exchange values will

finish the year close to their mid-May levels, between

$1.10-$1.14 per euro and ¥107–¥113 yen per dollar.

What impact can a rising or falling dollar

have on investors?Strong gains in the dollar tend to come when the

U.S. economy is stronger than those abroad. This favors U.S. markets and allocations. Conversely,

falling dollar values against key currencies suggest

international economies are improving and tend to benefit international

allocations.

INVESTOR WATCH

Even if oil prices, China, and trade do not relapse, pessimism and sentiment swings may accompany market-unfriendly political news. While the global economy is gradually gaining pace, growth is still in low gear and sentiment remains potentially vulnerable.

A neutral view on currencies and ultra-low yields does not justify adding international developed-market sovereign debt exposure at this time, and we reiterate our advice to hold less than target allocations.

The outlook is for global improvement with volatility. To reduce the potential impact, stay well-diversified.

92016 Midyear Outlook Eyes on the Horizon

economic growth likely will leave investors skeptical about earnings growth this year. By year-end, advancing structural reforms may improve the earnings outlook and could move us to get more constructive on international markets. Until then, we remain neutral on international developed and underweight emerging-market equities.

Seven Reasons U.S. Earnings Should ImproveYear-to-year earnings declines in recent quarters have been particularly negatively impacted by decreases of between 50 percent and 90 percent in Energy-sector earnings. We believe earnings comparisons will slowly improve as:1. Year-to-year crude oil price comparisons and energy earnings comparisons

become easier during the last half of the year and into 2017.2. The combination of low energy prices and low interest rates favorably

impacts both consumers and most nonenergy corporations.3. The Fed continues on a “lower for longer” course for interest rates as

inflation remains modest. Low inflation, low interest rates, and lifting consumer and investor confidence should bolster price-to-earnings (P/E) valuations in coming quarters (see chart on page 8).

4. Global monetary policy remains dovish and supportive over the next 12 months.

5. Modest domestic job growth, increasing consumer confidence, and real consumer income growth bolster consumer spending and the housing market this year and into 2017.

6. Late-cycle industrial demand slowly lifts as capacity utilization tightens.7. The dollar offers less of a headwind this year than during most of 2015.

We forecast roughly flat S&P 500 Index operating earnings this year ($119) and expect Energy-sector earnings to pare roughly 4 percentage points of annual earnings growth. We also believe investors are looking past the negative energy earnings drag and forward to better overall economic growth. We are carrying a 2190-2290 year-end target range for the S&P 500 Index.

Equity Recommendations for the Second Half

Overweight Large-Cap Equities

Evenweight Mid-Cap Equities International Developed-Market Equities

Underweight Small-Cap Equities Emerging-Market Equities

Top Sectors Consumer Discretionary Health Care Industrials Information Technology

INVESTOR WATCH

We prefer U.S. stocks over international developed and emerging-market stocks for the second half of the year.

In terms of market cap size, we prefer large-capitalization over mid-cap and mid-cap over small-cap stocks in the U.S.

We are underweighting the Utility and Telecommunication Services sectors that are likely to be more vulnerable to rate increases. The Consumer Staples sector is also a least-favored sector due to its lower ability to capitalize upon continuing cyclical growth trends.

112016 Midyear Outlook Eyes on the Horizon

Portfolio PositioningCredit: After a difficult start to 2016 for investors in credit, we have seen a pronounced rebound in recent months. The prospects of a prolonged low-interest-rate environment make higher-yielding investments more compelling than in an environment in which the Fed is raising rates on a more frequent and regular basis. After initiating an underweight stance in August 2015, we moved our high-yield recommendation back to evenweight on March 17, 2016, as energy prices rebounded and prospects of a deeper economic slowdown dissipated. It is important to note that illiquidity concerns in the high-yield fixed income class remain a significant consideration. While investors should expect credit-market volatility at times through year-end, we find credit markets currently offer a balanced risk/reward profile.

Municipals: Although municipal securities slightly underperformed their taxable counterparts in the first half of the year, we believe that they offer attractive tax-equivalent return opportunities and are well positioned for growth through the rest of 2016. We recommend focusing on higher-quality issues rated “A” or better in essential service sectors and believe the best opportunity is in the intermediate part of the yield curve with slight premium coupons.1

International: It is difficult to foresee strong returns for international developed-market bonds with yields in the two major index constituents (the Eurozone and Japan) either close to zero or already negative. Taking into account our relatively benign view for interest-rate increases in the U.S. and evidence that any further monetary easing in Europe or Japan will be less effective in weakening currencies, we recommend an underweight stance in developed-market fixed income.

The fundamentals of many emerging-market economies remain challenged. Since we believe that commodity prices will remain in a lower-level trading range, we do not expect the early-2016 rally in emerging-market currencies, which has boosted returns on local-currency debt, to be sustained. We expect more stable returns in dollar-denominated sovereign bonds, which are insulated from currency volatility and for which higher spreads over U.S. Treasury securities attract demand in a low-return environment. We recommend an even weighting in emerging-market debt.

1”A” rated bonds are defined as upper-medium grade quality and subject to low risk.

Fixed-Income Sector Recommendations

Favorable Treasury Inflation-Protected Securities (TIPS)

Corporate Securities Essential Service Revenue

Unfavorable Treasury Securities Municipal High Yield

INVESTOR WATCH

Investors should be prepared for lower returns in high-quality fixed income over the coming years. While we expect returns to remain positive, the low-yield environment will likely pull down total returns relative to historical experience.

For investors looking to maximize income generation, we recommend a well-diversified approach to limit concentration risks.

We favor intermediate maturities. Investors who overweight short-term maturities or cash will likely find little opportunity for yield. Long-maturity instruments can expose portfolios to increased interest-rate volatility.

132016 Midyear Outlook Eyes on the Horizon

year after year. It also means that it is now appropriate to adjust our 2016 year-end targets to reflect the major low of $1,050 per ounce set in December 2015. Thus, we are adjusting our year-end 2016 price range for gold from $950-$1,050 per ounce to $1,150-$1,250 per ounce. To be clear, this is us becoming gold neutral on a strategic basis (10 years or more). We have not become long-term gold bulls—just less bearish.

We are expecting similar range-bound action from most other commodities over the coming years. Oil has seen a healthy bounce and looks to be closing in on the $60 per barrel resistance area. That is the level where we believe extra oil supplies will begin seeping into the marketplace, which could cap the oil-price rally. Our best estimate for an oil range is $30 to $60 over the coming years. Not all commodities should stay range-bound, however, now that Phase 1 looks to be complete. Some have the potential to pull away from the pack. We believe that agricultural commodities, especially, have the potential to outpace the rest. The reason is that China has recently altered its GDP growth strategy. It is now targeting consumer-led GDP growth vs. building more roads, bridges, and the like. The result, we believe, will involve more food consumption, which could pressure many agricultural prices higher.

Potential Opportunties for MLPsWith the major oil low likely in place as of February 2016, we believe select MLPs can now be purchased. As we enter the second half of 2016, the dividend yields on many MLPs remain quite attractive vs. comparable high-yielding investments. We began advising selective buying in March when we released two publications, “MLPs Look Cheap—But for Good Reason” and “MLPs—Quality and Reaching for Yield.” Our advice remains the same today as it was in March—if you are going to buy, buy quality. Don’t reach for yield for yield’s sake only. Reaching for the highest-yielding MLPs is not necessarily the best long-term strategy. We prefer quality, liquid, larger-cap, MLP names.

Fundamentals Attractive for REITsIn the real asset space, we believe that the best fundamentals remain in REITs. This has been the case since 2011. In late 2015, we moved to tactically overweighting REITs, and we are not altering this advice. We have slight valuation concerns as REITs are not overly cheap vs. other comparable high-yielding investments. They are not necessarily expensive either, though, which is why we say our concerns are slight. As we enter the back half of 2016, we continue to recommend a tactical overweight to REITs.

What Is a Super-Cycle?If you look at commodity prices over the very long term (hundreds of years), it becomes evident that

they tend to move in overall bull and bear cycles, some lasting decades. These are super-cycles. If a particular

commodity (gold, for example) is in a bear

super-cycle, you might see short-term bull markets, but over the longer term, lower prices would be expected.

INVESTOR WATCH

Selective MLP buying can be considered now that oil has likely bottomed. We recommend high-quality, large-cap and liquid MLPs.

Gold in the $1,200-$1,300 per ounce area does not appear to be a good entry point to us. Before adding to gold positions, we would wait for prices below $1,150 per ounce, and ideally closer to $1,050 per ounce, the 2015 low.

REITs can continue to be considered as trends are positive and valuations do not appear overly expensive.

152016 Midyear Outlook Eyes on the Horizon

More interesting are the opportunities within Structured Credit. We believe the mark-to-market losses seen in the first quarter were technical in nature and not reflective of weakening fundamentals within commercial and residential real-estate markets. Certain sectors, such as commercial mortgage-backed securities, have not recovered to the extent that high-yield corporate credit has, which we believe creates an attractive opportunity for investors over the next few quarters. Importantly, while Relative Value historically has the lowest volatility measured by standard deviation (a statistical measure of the volatility of returns) among hedge fund strategies, we expect the changing liquidity environment to produce higher volatility for this strategy going forward.

Present Environment Offers OpportunitiesEquity Hedge, especially managers with low-net equity exposure, remains well positioned to benefit from a decline in global, sector, and intra-index correlations as well as a continued increase in dispersion. Despite disappointing performance in the first quarter, we believe this is a stock-picker’s environment with a compelling opportunity to deliver short alpha (performance generated by hedge funds by being short stocks) as the market distinguishes between companies with robust balance sheets and earnings growth and those artificially supported by low interest rates. We need to be mindful, however, of the impact that crowded positions as well as factor (i.e., momentum, growth, value) reversals have on performance.

We anticipate a significant opportunity within both Private Capital and Event Driven–Distressed strategies as the credit cycle peaks. Patience is the better part of valor with this opportunity, however, as we would like to see weakness spread to sectors not tied to commodity weakness, such as Materials, Automotive, and Retail. Ultimately, we think this could be a very robust default cycle with some estimates in excess of $1.5 trillion of defaulted paper that hedge fund managers can parse through and work out to deliver strong returns.

Macro strategies are expected to improve diversification and reduce volatility, just as we saw in January and February. Unfortunately, we remain in an environment mired by central-bank intervention, which has a tendency to truncate trends and lead to choppy market conditions. While persistent trends can indeed develop that both discretionary and macro managers can capitalize upon, we believe it is more likely that managers will muddle through the next few quarters until the market has more clarity on the strength of the global economy and the likely direction of asset prices.

Favorable Strategies Relative Value-Asset Backed

Event-Driven-Distressed Equity Hedge & Relative Value

Private Capital

INVESTOR WATCH

Prequalified investors may want to utilize alternative investments to not only reduce beta and provide diversification but also to take advantage of episodic volatility.

We anticipate tactical opportunities within Relative Value-Structured Credit over the medium term.

We remain in a stock-picker’s environment and one in which low-net equity exposure is preferred over more directional equity exposure.

Alternative investments, such as hedge funds and private capital funds are not suitable for all investors and are only available to persons who are “accredited investors” or “qualified purchasers” within the meaning of U.S. securities laws. Any offer to purchase or sell a specific hedge fund or private capital fund will be made by the product’s official offering documents. Investors should carefully review the Confidential Private Placement Memorandum or other offering documents for information regarding terms, including all applicable fees, as well as other factors before investing in these products.

162016 Midyear Outlook Eyes on the Horizon

Economic and Market ForecastGlobal Economy 2016E 2015 2014Domestic U.S. GDP growth 1.9% 2.4% 2.4%

Domestic U.S. inflation 1.4% 0.1% 1.6%

Domestic U.S. unemployment rate 4.8% 5.0% 5.6%

Global GDP growth 3.1% 3.1% 3.4%

Developed-market GDP growth 1.7% 1.9% 1.8%

Developed-market inflation 1.3% 0.4% 0.7%

Emerging-market GDP growth 4.1% 4.0% 4.6%

Emerging-market inflation 5.6% 4.5% 5.3%

Eurozone GDP growth 1.6% 1.5% 0.9%

Eurozone inflation 1.0% 0.0% -0.2%

Dollar/euro exchange rate $1.10-1.14 $1.09 $1.21

Yen/dollar exchange rate ¥107-113 ¥120 ¥119

Global EquitiesS&P 500 Index 2190-2290 2044 2059

S&P 500 operating earnings per share $119 $118 $119

Russell Midcap® Index 1650-1750 1596 1663

Russell Small Cap Index 970-1070 1135 1205

MSCI Europe, Australasia, Far East (EAFE) Index 1590-1690 1716 1775

MSCI Emerging Markets (EM) Index 720-800 794 956

Global Fixed Income10-year U.S. Treasury yield 2.0-2.25% 2.3% 2.17%

30-year U.S. Treasury yield 2.5-2.75% 3.00% 2.75%

Fed funds rate 0.5-0.75% 0.50% 0.25%

Global Real AssetsWest Texas Intermediate Crude price $35-45 $38 $53

Brent Crude price $40-50 $37 $57

Gold price $1150-1250 $1061 $1184

We see modest domestic GDP growth and put the probability of a U.S. recession at no more than 25 percent this year.

We may see sharp dollar moves higher or lower; we take a neutral view on the dollar.

While increased levels of market volatility would not be surprising, we expect stocks in the end will be higher than at midyear.

We expect one rate increase from the Fed, which means a continued low-rate environment.

Oil prices have stabilized, and we believe they will be range-bound for the remainder of the year.

Sources: FactSet, Bloomberg, and Wells Fargo Investment Institute, May 31, 2016GDP = gross domestic productE = estimateWest Texas Intermediate Crude Oil is a light, sweet (i.e., low sulfur) crude oil which is the main type of U.S. crude oil traded in U.S. futures markets. Brent Crude Oil is a light, sweet crude oil extracted from the North Sea. It serves as a major benchmark price for purchases of oil worldwide.Wells Fargo Investment Institute forecasts. Forecasts are not guaranteed and are subject to change.Past performance is no guarantee of future results. An index is unmanaged and not available for direct investment.

182016 Midyear Outlook Eyes on the Horizon

DefinitionsIndexesAn index is unmanaged and not available for direct investment.

Barclays U.S. Aggregate Bond Index covers the U.S. dollar-denominated, investment-grade (rated Baa3 or above by Moody’s), fixed-rate, and taxable areas of the bond market. This is the broadest measure of the taxable U.S. bond market, including most Treasury, agency, corporate, mortgage-backed, asset-backed, and international dollar-denominated issues, all with maturities of one year or more.

BofA Merrill Lynch U.S. High-Yield Master II Index tracks the performance of below-investment-grade publically issued U.S. corporate bonds.

MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The Index consists of the following 21 developed market country indexes: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The Index consists of the following 23 emerging market country indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Russia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates.

Russell 2000® Index (small cap) measures the performance of the 2,000 smallest companies in the Russell 3000® Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index.

Russell Midcap® Index measures the performance of the 800 smallest companies in the Russell 1000® Index, which represent approximately 25% of the total market capitalization of the Russell 1000® Index.

S&P 500® Index consists of 500 industrial, financial, utility and transportation companies with market capitalizations of $4 billion or more.

Risk ConsiderationsAll investing involve risks, including the possible loss of principal. There can be no assurance that any investment strategy will be successful or will meet its investment objective. Investments fluctuate with changes in market and economic conditions and in different environments due to numerous factors some of which may be unpredictable. Each asset class has its own risks and return characteristics. The risks associated with the asset classes discussed in this report include:

Alternative Investments: The use of alternative investments, such as hedge funds and private capital funds, includes the risk of investment loss, including the loss of the entire amount invested. While investors may potentially benefit from the ability of alternative investments to potentially improve the risk-reward profiles of their portfolios, the investments themselves can carry significant risks. Government regulation and monitoring of these types of investments may be minimal or nonexistent. There may be no secondary market for alternative investment interests and transferability may be limited or even prohibited. Alternative investments employ aggressive investment techniques, including the use of short sales, leverage, swaps, futures contracts, options, forward contracts and other derivatives which can expose the investor to substantial risk. Short selling involves the potential for unlimited loss of the security sold short. The use of derivatives for other than hedging purposes is considered speculative and involves greater risks than those used for hedging. Investing in derivatives carries the risk of the underlying instrument as well as the derivative itself and may not be successful, resulting in losses to the fund, and the cost of such strategies may also reduce the fund’s returns.

Alternative Strategy Risk: Event Driven strategies involve investing in opportunities created by significant transactional events, such as spinoffs, mergers and acquisitions, bankruptcy reorganization, recapitalization and share buybacks. Managers who use such strategies may invest in, and might sell short, the securities of companies where the security’s price has been, or is expected to be, affected by a distressed situation. Event Driven-Distressed strategies involve a high degree of risk. Distressed companies could declare bankruptcy shortly, could currently be in bankruptcy proceedings or just emerging from bankruptcy. Because of their distressed situation, these securities may be illiquid, have low trading volumes, and be subject to substantial interest rate and credit risks. Equity Hedge strategies maintain positions both long and short in primarily equity and equity derivative securities. Macro managers trade a broad range of strategies in which the investment process is predicated on movements in underlying economic variables and the impact these have on equity, fixed income, hard currency and commodity markets. Relative Value strategies focus on exploiting perceived imbalances or valuation discrepancies between related markets or instruments. Structured credit strategies are not suitable for all investors. These strategies aim to generate returns via positions in the credit sensitive area of the fixed income markets. The strategy generally involves the purchase of corporate bonds, mortgages, suppliers’ claims and bank loans with hedging of the interest exposure. Such strategies involve taking advantage of mispriced credit exposure at certain points in the term structure of single name credits relative to other points in the same term structure. Positions may use, but are not limited to, traditional fixed income and credit securities, as well as other structured credit products and credit derivatives, such as credit default swaps. The use of these strategies may require a manager’s skill in assessing corporate events, the anticipation of future movements in securities prices, interest rates, or other economic factors. No assurance can be given that a manager’s view of the economy will be correct which may result in lower investment returns or higher return volatility. There can be no assurance that a manager that uses these strategies will be successful or that a manager will not deviate from its stated investment strategy and not employ other investment techniques in an effort to meet the fund’s investment objective.

192016 Midyear Outlook Eyes on the Horizon

Risk ConsiderationsCommodities: In addition to the risks of investing in commodities generally, investing in gold carries special risk considerations such as potentially severe price fluctuations over short periods of time and storage costs that exceed the custodial and/or brokerage costs associated with a portfolio’s other holdings.

Currency: Currency risk is the risk that foreign currencies will decline in value relative to that of the U.S. dollar. Exchange rate risk between the U.S. dollar and foreign currencies may cause a portfolio to decline.

Equity investments are subject to market risk which means their value may fluctuate in response to general economic and market conditions, the prospects of individual companies, and industry sectors. Technology and Internet-related stocks: Technology and Internet-related stocks, especially of smaller, less-seasoned companies, tend to be more volatile than the overall market.

Master limited partnerships (MLPs): MLPs involve certain risks which differ from an investment in the securities of a corporation. MLPs may be sensitive to price changes in oil, natural gas, etc., regulatory risk, and rising interest rates. A change in the current tax law regarding MLPs could result in the MLP being treated as a corporation for federal income tax purposes, which would reduce the amount of cash flows distributed by the MLP. Other risks include the volatility associated with the use of leverage, volatility of the commodities markets, market risks, supply and demand, natural and man-made catastrophes, competition, liquidity, market price discount from Net Asset Value, and other material risks.

Fixed-income securities: Investments in fixed-income securities are subject to market, interest rate, credit and other risks. Bond prices fluctuate inversely to changes in interest rates. Therefore, a general rise in interest rates can result in the decline in the bond’s price. Credit risk is the risk that an issuer will default on payments of interest and/or principal. This risk is heightened in lower rated bonds. High yield fixed income securities (junk bonds) are considered speculative, involve greater risk of default, and tend to be more volatile than investment grade fixed income securities. If sold prior to maturity, fixed income securities are subject to market risk. All fixed income investments may be worth less than their original cost upon redemption or maturity.

Foreign securities: Investing in foreign securities presents certain risks not associated with domestic investments, such as currency fluctuations, political and economic instability, and different accounting standards. This may result in greater share price volatility. These risks are heightened in emerging markets.

Mortgage-related securities: Investments in mortgage and asset-backed securities are subject to prepayment risk. Changes in prepayments may significantly affect yield, average life and expected maturity. Commercial Mortgage Backed Securities (CMBS) are a type of mortgage-backed security backed by commercial mortgages rather than residential real estate. CMBS tend to be more complex and volatile than residential mortgage-backed securities due to the unique nature of the underlying property assets.

Municipal bonds offer interest payments exempt from federal taxes, and potentially state and local income taxes. These bonds are subject to credit risk and potentially the Alternative Minimum Tax. Quality varies widely depending on the specific issuer.

Real estate: There are special risks associated with an investment in real estate, including the illiquidity of underlying properties, credit risk, interest rate fluctuations and the impact of varied economic conditions.

Small- and mid-capitalization stocks: The prices of small- and mid-cap company stocks are generally more volatile than large-company stocks. They often involve higher risks because smaller companies may lack the management expertise, financial resources, product diversification and competitive strengths to endure adverse economic conditions.

Sovereign Debt: In addition to the risks associated with investing in international and emerging markets, sovereign debt involves the risk that the issuing entity may not be able or willing to repay principal and/or interest when due in accordance with the terms of the debt agreement.

Treasury Inflation-Protected Securities (TIPS): TIPs are subject to interest rate risk, especially when real interest rates rise. This may cause the underlying value of the bond in the portfolio to fluctuate more than other fixed income securities.