briefing seoul office sector q3 2015 -...

TRANSCRIPT

savills.co.kr/research 01

BriefingSeoul office sector Q3 2015

Savills World Research Korea

In Q3 the net absorption of Seoul prime office space was 72,300sqm. The CBD and YBD posted demand increases while the GBD saw demand decrease.

The Seoul prime office market posted a 0.4% YoY increase in face rents, which is below CPI (0.6% in Q3/2015).

“Total employment increased slightly and demand for office space rebounded despite recent international financial market uncertainty.” Savills Research

Image : CBD, Seoul

In September 2015 international rating agency Standards & Poor’s raised Korea’s credit rating back to its pre-foreign exchange crisis level of AA-.

The total volume of office transactions executed in Q3 was KRW 283.2 billion; with small and medium sized buildings in secondary markets accounting for the majority of transactions.

SUMMARYThe growing demand for office relocations arising from the remodeling of existing buildings and strategic repositioning led to a net demand increase. However, rental rates showed no significant change.

savills.co.kr/research 02

Briefing | Seoul office sector Q3 2015

SupplyNo new prime office buildings were supplied in Q3 2015.

Demand and vacancy rateThe IMF recently adjusted its outlook for Korea’s economic growth for 2015 from 3.1% to 2.7%, whilst the BOK also lowered its GDP forecasts from 2.8% to 2.7%. On a more positive note S&P raised Korea’s credit rating from A+ to AA-, its highest level since the foreign exchange crisis. The number of employees in the financial and insurance sectors inched up again in September, after declining since May 2015.

In Q3/2015, the total net absorption of the Seoul prime office market was 72,300sqm. By district, the CBD posted a net absorption of 63,560sqm and the YBD 10,400sqm, while the GBD showed a net absorption of -1,670sqm.

The overall vacancy rate of the Seoul prime office market declined by 1.2% ppt from the previous quarter to 14.1%, as the vacancy rates in both the CBD and YBD fell.

The vacancy absorption in Q3/2015 was mainly attributable to office upgrades involving secondary to prime relocations, which accounted for 36% of total absorption. However, our survey shows that many of these relocations were temporary moves. Prime to prime office relocations represented 26% of vacancy absorption, office expansion 23% and new office establishment 15%.

The CBD witnessed a 2.3% ppt QoQ decrease in vacancy to 15.7%. Of all the CBD sub-markets (Jongno/Gwanghwamun, City Hall/Euljiro, Seoul station/Namdaemun), the Seoul station area showed the most significant decline. As large vacancies in STX Namsan Tower and Twin City Namsan were filled by tenants, the vacancy rate of this area dropped from 32.6%, posted in the previous quarter, to 28.3%. STX

TABLE 1

Montly rent and vacany rate by district, Q3/2015

DistrictAverage rent

(KRW per 3.3058 sq m GLA)

Average rent(KRW per 3.3058

sq m NLA)

YoY rental increase rate (%)

Net absorption (sq m) Vacancy rate (%)

CBD 100,900 180,100 0.7% 63,560 15.7

GBD 85,400 166,500 0.1% -1,670 10.4

YBD 78,100 160,600 0.1% 10,400 16.5

Overall Seoul Average

91,400 171,800 0.4% 72,300* 14.1

Source: Savills Korea *Net absorption of Seoul prime office buildings.

GRAPH 1

Growth rate of real GDP and real exports, 2006 - 2016 (E)

Source: Bank of Korea

5.2% 5.5%

2.8%0.7%

6.5%

3.7%

2.3%2.9%

3.3% 2.7% 3.2%

13.4%12.4%

6.0%

0.4%

13.5%

17.1%

4.4% 4.5%

2.3%0.2% 2.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016F

Economic Growth (GDP, annual variance in %) Export Growth (annual variance in %)

GRAPH 2

The number of employees in the financial and insurance sectors, Sep 2006 – Sep 2015

15,000

17,000

19,000

21,000

23,000

25,000

27,000

600

700

800

900

1,000

1,100

1,200

Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15

Unit : Number Employed (thousands)Financial Institutions & Insurance Employment (LHS)Total Employment (RHS)

Source: Korean Statistical Information Service

savills.co.kr/research 03

Briefing | Seoul office sector Q3 2015

Namsan Tower’s vacancy declined as Dongbu Steel and Daewoo Shipbuilding & Marine Engineering took occupation, while Seoul Square saw its vacancy decline as LG Electronics expanded.

Demand arising from the need for office upgrades was most pronounced in the CBD, which recorded the greatest vacancy absorption. JR AMC and ABC Mart Korea, which had leased in secondary GBD buildings, upgraded by relocating to Pine Avenue B. Maersk Korea, with its affiliate Damco Logistics, relocated from Hana Tour’s building to Twin City Namsan. Temporary office upgrades included Hana Tour, which moved to Pine Avenue B. The tour agency signed a six-month lease in Pine Avenue B as it began remodeling its own building to include a duty-free shop, after it was granted a duty-free license in July.

The overall vacancy rate of the GBD remained at 10.4%. However, there were a number of relocations within the area. Amway Korea left Korea Textile Center for ASEM Tower and the resulting vacancy in Korea Textile Center was filled by law firm, Yulchon, expanded its existing space. SK Hynix relocated from Samsung Life Insurance’s Daechi Tower to Pangyo U Tower and the subsequent vacant space was absorbed by Samsung Life Insurance. The relocation of Samsung Life Insurance increased the vacancy in Samsung Finance Building and Glass Tower. On the other hand, KAIT Tower recorded vacancy rate declines due to office expansion by existing tenants and luring new tenants.

In the YBD the vacancy rate dropped by 0.8% ppt quarter-on-quarter to 16.5%. Hanwha Hotel & Resort relocated to Hanwha Life Insurance’s 63 Building as the remodeling of Hanwha Janggyo Building began. The vacancy rate of FKI Tower, which was 18% in the previous quarter, fell to 11% as the child day care

GRAPH 3

Net absorption, Q1/2008 – Q3/2015

Source: Savills Korea

-200,000

-150,000

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2008 2009 2010 2011 2012 2013 2014 2015

Unit: sq mCBD GBD YBD

GRAPH 4

Seoul prime office vacancy rate, Q1/2002 – Q3/2015

Source: Savills Korea

0%

5%

10%

15%

20%

25%

30%

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CBD GBD YBD

GRAPH 5

The CBD prime office vacancy rate, Q1/2010 – Q3/2015

Source: Savills Korea

0%

5%

10%

15%

20%

25%

30%

35%

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

2010 2011 2012 2013 2014 2015

Jongno-Gwanghwamun Euljiro-City Hall Seoul Station-Namdaemun

savills.co.kr/research 04

Briefing | Seoul office sector Q3 2015

center of Hyundai Card, the Startup Support Center of Hyundai Capital, Dongbu Fire & Marine Insurance and Dongbu Asset Management all took occupation.

OutlookIn Q4, the office market is expected to remain steady with no material changes from Q3.

By district, the CBD is likely to see the most change, with the vacancy rate expected to rise by approximately 0.3% ppt from Q3 to around 16%. Samsung Fire & Marine, located at YG Tower, plan to move to City Center Tower. CJ Korea Express will relocate from its own office building in Ssangnimdong to Pacific Tower. Yeonsei Building is

to see increased vacancy as Korea Scholarship Foundation will move to Daegu. Finally, Servico will lease two floors at Tower 8.

In the GBD, the vacancy rate will remain in the low-10% range, which is the same as Q3. Samsung Life Insurance’s organizations will complete their relocation to

TABLE 2

Major tenant relocations, Q3/2015

Source: Savills Korea

District Current building Tenant Area (sqm)Previous district

Previous building

CBD

D Tower S-Oil Project TFT 4,170 New Office Opening

Pine Avenue B

Hana Tour 13,440 CBD Hana Tour Building

Hanwha S&C 7,198 CBD Hanwha Janggyo

ABC Mart Korea 1,637 Others Gangnam Paragon S

STX Namsan TowerDSME 6,474 GBD El Crew Building

Dongbu Steel 5,346 GBD Dongbu Finance Centre

Twin City Namsan Maersk Korea 2,744 CBD Hana Tour Building

Twin Tree Embassy of Japan 6,508 CBD Embassy

WISE Tower (former YTN Tower) Polaris Shipping 2,561 CBD KCCI

Seoul Square LG Electronics 3,855 Office Expansion

Ferrum Tower SK 3,155 Office Expansion

Hanwha Sogong Hanwha Machinery 3,188 CBDHanwha Finance Plaza Taepyeongno Building

GBD

KAIT TowerBullsone 3,134 GBD Dabong Tower

Tech Code 1,825 New Office Opening

Dongbu Finance Centre Dongbu's Affiliate 2,875 Office Expansion

Samsung Life InsuranceDaechi Tower

Samsung Life Insurance N/A GBD KAIT Tower

Samsung Life Insurance N/A GBD Glass Tower

Asia Tower Rockwell Automation Korea 3,742 GBD Golden Tower

ASEM Tower Amway Korea 7,164 GBD Korea Textile Center

Autoway TowerNokia Korea 2,999 GBD Meritz Tower

ST & Company 2,701 Office Expansion

Korea Textile Center Yulchon LLC 8,099 Office Expansion

YBDFKI Tower

Dongbu Fire 1,862 YBD Sinsong Center

Dongbu Asset Management 1,624 YBD Sinsong Center

the KIDS (Hyundai Card) 1,759 New Office Opening

Foundation Support Center (Hyundai Capital)

699 New Office Opening

Hanwha Life 63 Building Hanwha Hotels & Resorts 5,243 CBD Hanwha Janggyo

Pangyo U-Tower SK Hynix N/A GBD Samsung Life Insurance Daechi Tower

savills.co.kr/research 05

Briefing | Seoul office sector Q3 2015

Samsung Life Insurance Daechi Tower in October. Samsung Fine Chemicals will move to Glass Tower. Korea Western Power, currently a tenant of Gangnam Finance Building, will relocate to Taean. Samsung Electronics’ research and design units will leave Samsung Electronics’ office building in Seocho for the company’s R&D Campus in Umyeondong in November.

The vacancy rate of the YBD is projected to drop by 0.1% ppt from Q3 into the low 16% range. Bumhan Pantos’ relocation and upsizing within the district, moving from KTB Building to FKI Tower, demonstrates the potential for increased demand.

Rent ratesIn Q3/2015, the average face rent of Seoul prime offices rose 0.4% compared to the same period last year. By district, the CBD saw rental rates go up by 0.7%, while the GBD and YBD each recorded a 0.1% increase. In the case of Pine Avenue B, which adjusts rents in Q3 every year, its rent was raised by approximately 1%, which is similar to CPI. At Centre Point Gwanghwamun, where vacancies have been constantly absorbed, the rent increased by around 3%. Hanwha Financial Plaza, which recently saw its last vacancy filled, raised rents by 3%. Autoway Tower in the GBD, whose vacancy rate is now 5%, posted a rent increase rate of 3%.

Lease contract conditions differ depending on lease areas, tenants and lease periods but in the case of new prime office buildings which signed lease contracts recently, it is reported that extra rent-free periods for fit out are being provided in addition to four-month rent free periods, as well as interior costs. In some buildings with large vacancies, tenants signing a new lease are being granted as much as five months rent-free per year for a five-year lease. As such, according to our survey, some lease contracts are being signed with effective rents 30 to 40% lower than their marketed (face) rents.

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2008 2009 2010 2011 2012 2013 2014 2015

CBD GBD YBD CPI growth rate

GRAPH 6

YoY rental increase rate by district, Q1/2008 – Q3/2015

Source: Savills Korea, Bank of Korea

GRAPH 8

Prime office building cap rate trends, Q1/2005 – Q3/2015

Source: Savills Korea, Bank of Korea

0

100

200

300

400

500

600

700

800

900

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Spread (RHS) Cap rate (LHS) Five-year treasury bond yield (LHS)

GRAPH 7

Seoul office transaction volumes, Q1/2007 – Q3/2015

Source: Savills Korea

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014 2015

Unit: KRW (Trillion) Q1 Q2 Q3 Q4

savills.co.kr/research 06

Briefing | Seoul office sector Q3 2015

OutlookDuring 2H/2015, there will be limited rental adjustment for existing buildings and with no new buildings to be supplied, rental rates are forecast to remain steady.

Transactions and investment marketIn Q3 the BOK maintained the benchmark interest rate at 1.5%, the level set in Q2 to boost the economy. The average yield of the five-year government bond was 1.95% in the quarter and the cap. rate of prime offices remained around 5%.

Office transaction volumes have exceeded KRW 5 trillion per year over the last three years, but the volume posted for the first three quarters of 2015 has only been approximately KRW 2 trillion. However, there are transactions currently ongoing involving 15 buildings in the major office districts: eight in CBD, four in GBD and three in YBD. The investment volume for 2015 is projected to be similar to

GRAPH 9

Five-year treasury bond yield and benchmark interest rate trends, Jan. 2012 – Oct. 2015

Source: Bank of Korea

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2012

-01-

02

2012

-04-

02

2012

-07-

02

2012

-10-

02

2013

-01-

02

2013

-04-

02

2013

-07-

02

2013

-10-

02

2014

-01-

02

2014

-04-

02

2014

-07-

02

2014

-10-

02

2015

-01-

02

2015

-04-

02

2015

-07 -

02

2015

-10-

02

5yr Treasury bond yield The Bank of Korea Base Rate

recent levels, if the transactions of

these buildings complete.

During the third quarter in 2015,

Transactions concluded in Q3 were

mostly led by small and medium-

sized companies, seeking asset

liquidation or office buildings for

their own occupation in secondary

markets. The total office transaction

volume for the quarter was

approximately KRW 283 billion.

Centreville Asterium in Yongsan was

sold to Hana Asset Management

by LS Networks for KRW 40 billion

under a sale and lease-back

structure to help them raise capital. STX Namsan Tower and DSME Building, which are currently under

TABLE 3

Office buildings in the sale process, Q3/2015

Source : Major daily newspapers

District Building Name Seller Area (sqm)

CBD

Jongno Place Tower Korea Investment Management 45,735

STX Namsan Tower KORAMCO 67,295

Sunhwa Tower Deutsche Asset & Wealth Management 21,772

Alpha Building Deutsche Asset & Wealth Management 13,519

Citi Bank Headquarter Citi Bank 39,624

Jongno Tower Samsung Life Insurance 60,653

Susong Tower Samsung Life Insurance 44,825

DSME Building DSME 24,854

GBD

Grace Tower KORAMCO 24,530

Nara Building M&G Real Estate 29,916

Capital Tower Mirae Asset Global Investments 62,747

Narae Building AON 13,973

YBD

Samsung Life Insurance East Yeouido Building Samsung Life Insurance 14,622

Hana Daetoo Building Hana Asset Management 69,826

NH Capital Building KORAMCO 20,700

savills.co.kr/research 07

Briefing | Seoul office sector Q3 2015

JoAnn HongDirectorKorea+82 2 2124 [email protected]

Savills Korea

Please contact us for further information

Savills plcSavills is a leading global real estate service provider listed on the London Stock Exchange. The company established in 1855, has a rich heritage with unrivalled growth. It is a company that leads rather than follows, and now has over 600 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

This report is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.

Savills Research

Simon SmithSenior DirectorAsia Pacific+852 2842 [email protected]

Seunghan LeeDirectorLeasing Services+82 2 2124 [email protected]

Sue LeeDirector, Worldwide Occupier Services+82 2 2124 [email protected]

Youngtaek KimVice PresidentKorea+82 2 2124 [email protected]

K.D. JeonHead of KoreaKorea+82 2 2124 [email protected]

Hyunseok JheeDirectorPM Services+82 2 2124 [email protected]

Crystal LeeSenior DirectorInvestment Advisory+82 2 2124 [email protected]

Grace KoDirector, Corporate Real Estate Services+82 2 2124 [email protected]

negotiation, are also expected to be transacted as some form of sale and lease-back. Samsung Life Insurance is proceeding to liquidate some of its non-core properties, including the sale of Samsung Life Insurance Building in Yeouido, Samsung Life Insurance Building in Donggyodong, Susong Tower and Jongno Tower.

The sale of the headquarters building of Citibank, which has been delayed for over a year, will be concluded shortly. Mastern Asset Management, the preferred bidder, applied for a business license for Mastern REIT 14 in September. Citibank is known to be considering a one year master lease option before relocating to IFC in Yeouido.

The sale of Samsung Life Insurance Building in East Yeouido was concluded as it was sold through Igis

Asset Management at the beginning of October, with the ultimate investor in the transaction being AEW Capital. The price of the building, with a 20% vacancy rate, was in the high KRW 13 million’s per pyeong and the entry cap rate was in the high-4%s with further reversion upon the lease up of vacant space.

Coupang recently relocated to Jongno Place, raising the occupancy rate of the building to 97% and further enhancing its sale prospects. The Korea Teachers Pension has decided to finance Ascendas Korea’s private office REIT 3, which will invest in Jongno Place Tower, with KRW 30 billion. The expected annual dividend yield is reported to be approximately 6.99%.

The ownership transfer of the Kepco site, for which the sale contract

was executed last year, has now completed. The buyer was Hyundai Motor Company Consortium and the sale price was KRW 10.55 trillion. Hyundai Motor Company plans include developing part of the site for their new global headquarters.

savills.co.kr/research 08

Briefing | Seoul office sector Q3 2015

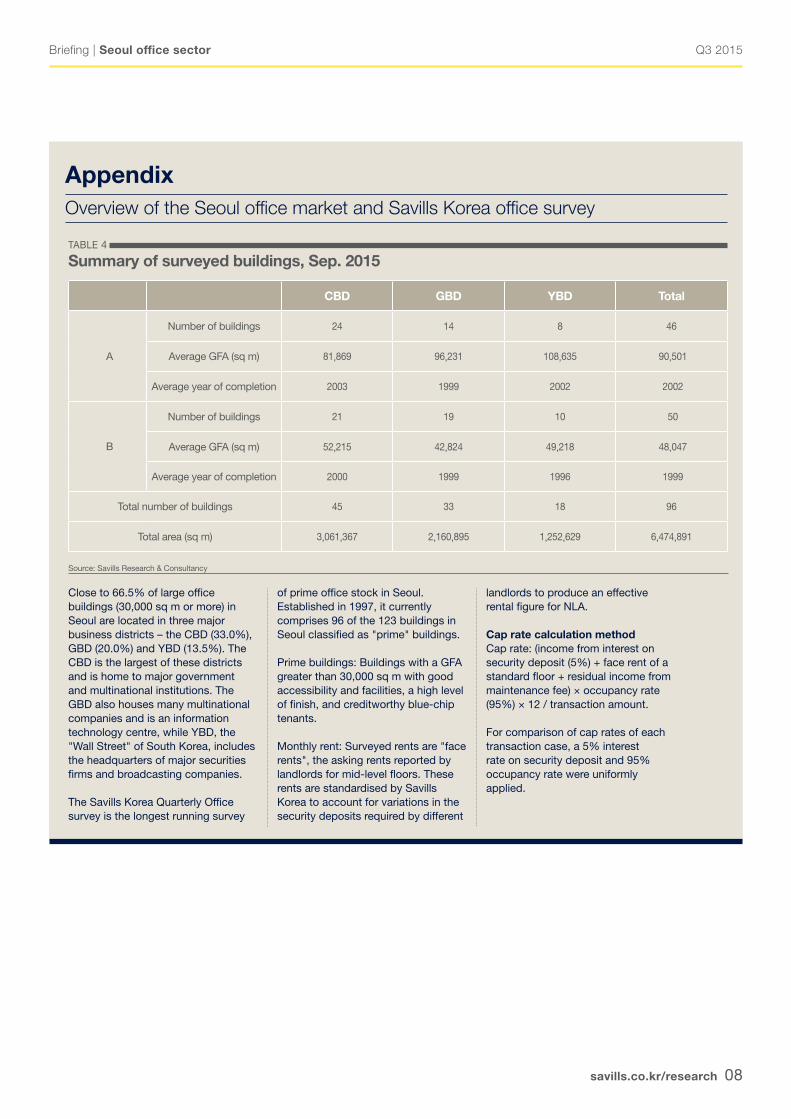

AppendixOverview of the Seoul office market and Savills Korea office survey

Close to 66.5% of large office buildings (30,000 sq m or more) in Seoul are located in three major business districts – the CBD (33.0%), GBD (20.0%) and YBD (13.5%). The CBD is the largest of these districts and is home to major government and multinational institutions. The GBD also houses many multinational companies and is an information technology centre, while YBD, the "Wall Street" of South Korea, includes the headquarters of major securities firms and broadcasting companies.

The Savills Korea Quarterly Office survey is the longest running survey

TABLE 4

Summary of surveyed buildings, Sep. 2015

Source: Savills Research & Consultancy

of prime office stock in Seoul. Established in 1997, it currently comprises 96 of the 123 buildings in Seoul classified as "prime" buildings.

Prime buildings: Buildings with a GFA greater than 30,000 sq m with good accessibility and facilities, a high level of finish, and creditworthy blue-chip tenants.

Monthly rent: Surveyed rents are "face rents", the asking rents reported by landlords for mid-level floors. These rents are standardised by Savills Korea to account for variations in the security deposits required by different

CBD GBD YBD Total

A

Number of buildings 24 14 8 46

Average GFA (sq m) 81,869 96,231 108,635 90,501

Average year of completion 2003 1999 2002 2002

B

Number of buildings 21 19 10 50

Average GFA (sq m) 52,215 42,824 49,218 48,047

Average year of completion 2000 1999 1996 1999

Total number of buildings 45 33 18 96

Total area (sq m) 3,061,367 2,160,895 1,252,629 6,474,891

landlords to produce an effective rental figure for NLA.

Cap rate calculation methodCap rate: (income from interest on security deposit (5%) + face rent of a standard floor + residual income from maintenance fee) × occupancy rate (95%) × 12 / transaction amount.

For comparison of cap rates of each transaction case, a 5% interest rate on security deposit and 95% occupancy rate were uniformly applied.