british technology programme - ffg.at · british technology programme ... • aircraft and...

TRANSCRIPT

British Technology ProgrammeTuesday 3 June 2008, Palais Strudlhof - Vienna

Business Relations: Aerospace, Marine & DefenceDepartment for Business, Enterprise & Regulatory Reform1 Victoria StreetLondon SW1H 0ETwww.berr.gov.uk

Peter Joyce Richard PitmanAssistant Director, Policy Assistant Director, TechnologyTel: 00 44 (0)20 7215 1165 Tel: 00 44 (0)20 7215 [email protected] [email protected]

British Technology Programme

• UK Aerospace Industry

• National strategy

• What has been achieved so far

• Technology Programme

• Conclusions

UK Aerospace Industry

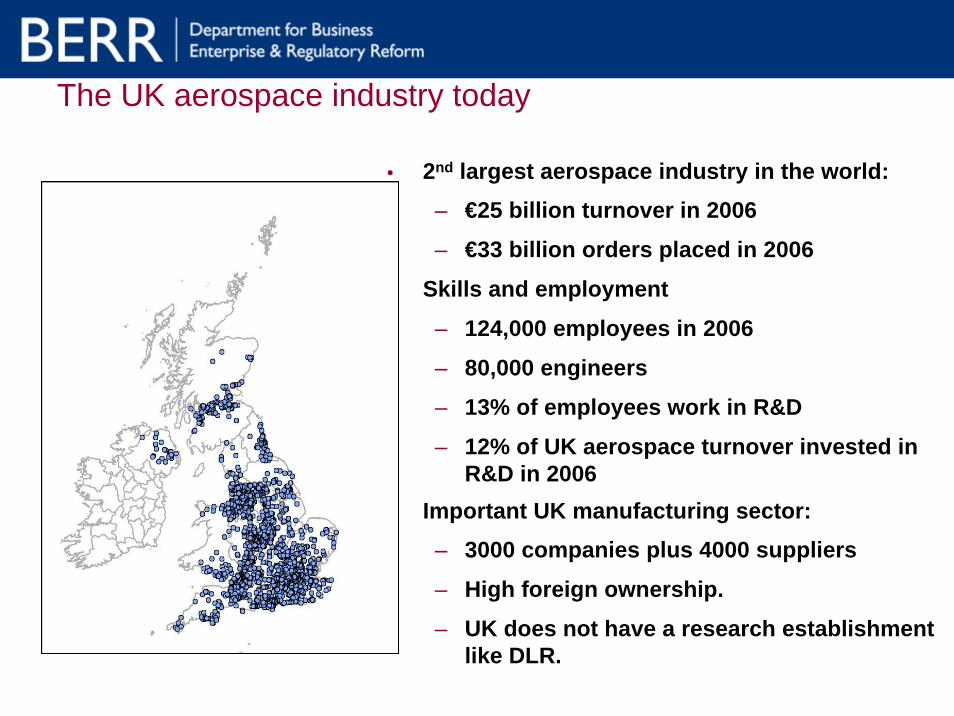

The UK aerospace industry today

• 2nd largest aerospace industry in the world: – €25 billion turnover in 2006

– €33 billion orders placed in 2006

• Skills and employment

– 124,000 employees in 2006

– 80,000 engineers

– 13% of employees work in R&D

– 12% of UK aerospace turnover invested in R&D in 2006

• Important UK manufacturing sector:– 3000 companies plus 4000 suppliers

– High foreign ownership.

– UK does not have a research establishment like DLR.

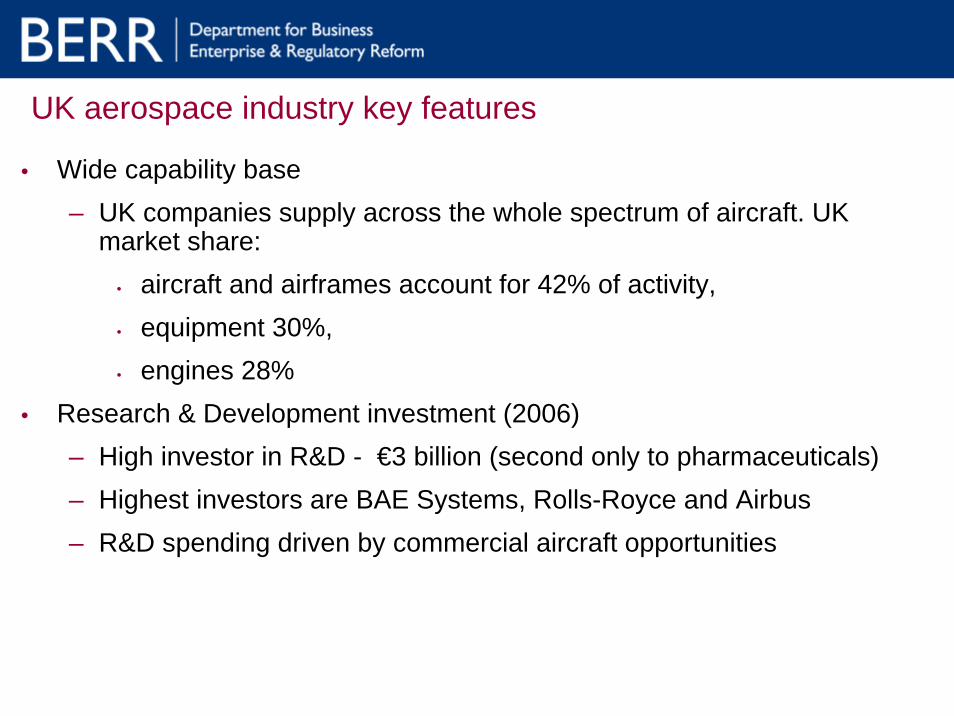

UK aerospace industry key features

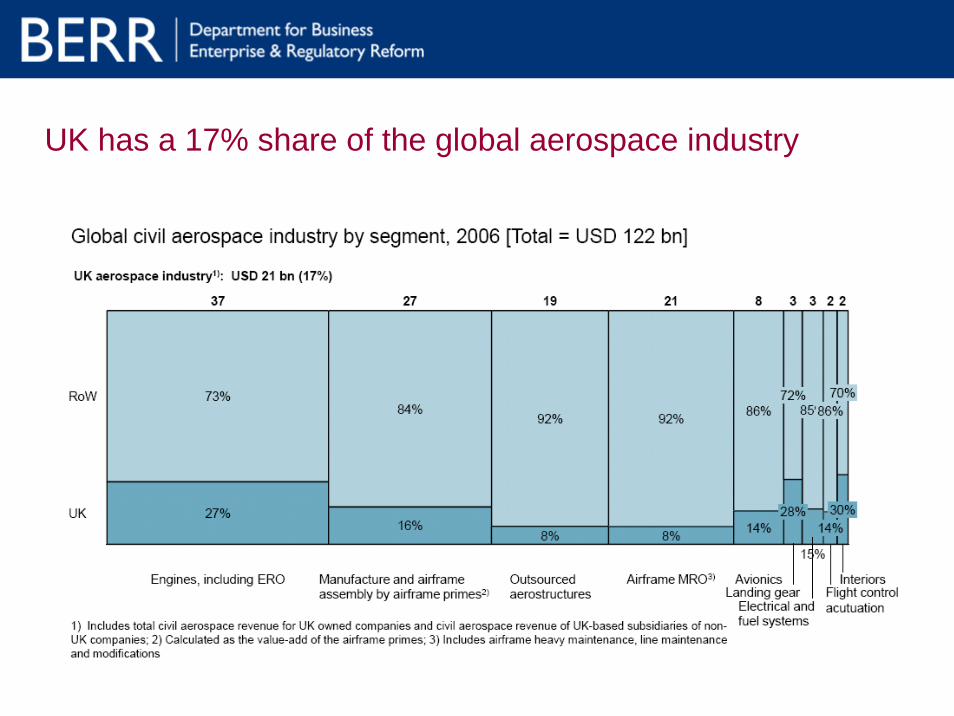

• Wide capability base– UK companies supply across the whole spectrum of aircraft. UK

market share:• aircraft and airframes account for 42% of activity, • equipment 30%, • engines 28%

• Research & Development investment (2006)– High investor in R&D - €3 billion (second only to pharmaceuticals)– Highest investors are BAE Systems, Rolls-Royce and Airbus– R&D spending driven by commercial aircraft opportunities

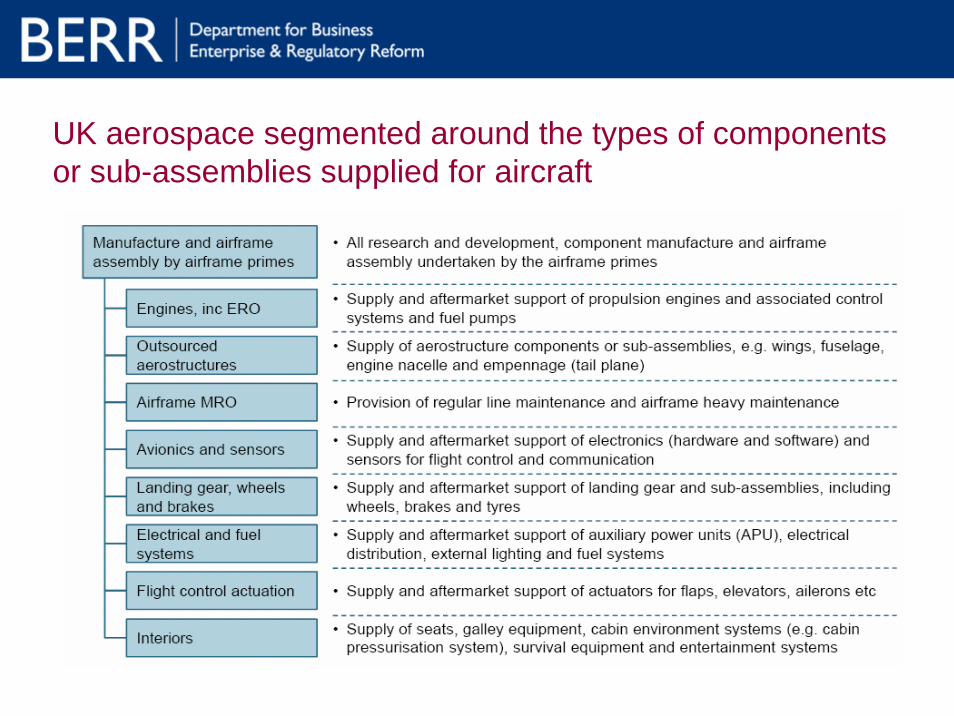

UK aerospace segmented around the types of components or sub-assemblies supplied for aircraft

UK has a 17% share of the global aerospace industry

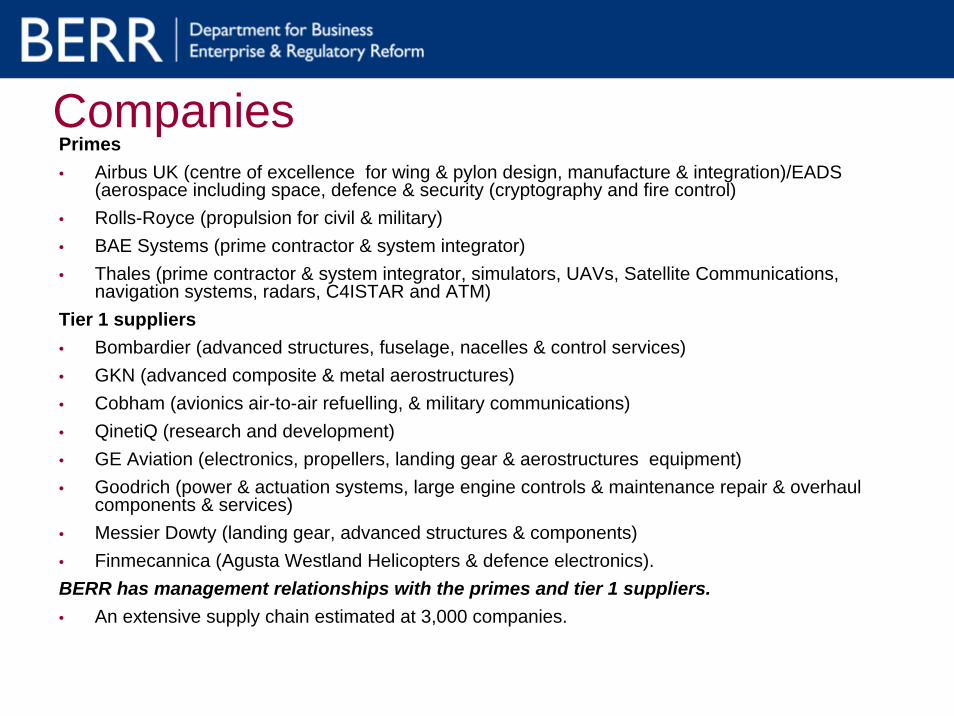

CompaniesPrimes• Airbus UK (centre of excellence for wing & pylon design, manufacture & integration)/EADS

(aerospace including space, defence & security (cryptography and fire control)• Rolls-Royce (propulsion for civil & military)• BAE Systems (prime contractor & system integrator)• Thales (prime contractor & system integrator, simulators, UAVs, Satellite Communications,

navigation systems, radars, C4ISTAR and ATM)Tier 1 suppliers• Bombardier (advanced structures, fuselage, nacelles & control services)• GKN (advanced composite & metal aerostructures)• Cobham (avionics air-to-air refuelling, & military communications)• QinetiQ (research and development)• GE Aviation (electronics, propellers, landing gear & aerostructures equipment)• Goodrich (power & actuation systems, large engine controls & maintenance repair & overhaul

components & services)• Messier Dowty (landing gear, advanced structures & components)• Finmecannica (Agusta Westland Helicopters & defence electronics).BERR has management relationships with the primes and tier 1 suppliers.• An extensive supply chain estimated at 3,000 companies.

The Funders

Regions and Devolved AdministrationsResearch Councils

Central Government

UK Industry

National strategy

BackgroundThe concept was first announced in a government “White Paper” in 2001.

ObjectivesInnovation & Growth Teams look strategically at a sector, with the top level commitment of industry and drawing on the expertise of all the major stakeholders. The aim is to identify the key issues which will shape the future of their industry and how the UK can best respond to the competitive challenges which it will face.

“Innovation and Growth Team”

National Strategy• In 2003, a 20 year vision and

strategy for the future success of the UK aerospace industry was set:

By 2022 “the UK will offer a global aerospace industry the world’s most innovative and productive location, leading to sustainable growth for all its stakeholders”

• The main actions were needed in the areas of technology, enterprise excellence, skills, and sustainable aviation to ensure the continued success of the industry.

• The Aerospace Innovation and Growth Team, a partnership of government, academia and industry recommended a jointly funded National Aerospace Technology Strategy.

• The National Aerospace Technology Strategy identified civil & military technology themes where the UK aerospace industry was an innovative global aerospace leader or could become such.

• The objective of National Aerospace Technology Strategy is to embed technology throughout the supply chain as a basis for future product development.

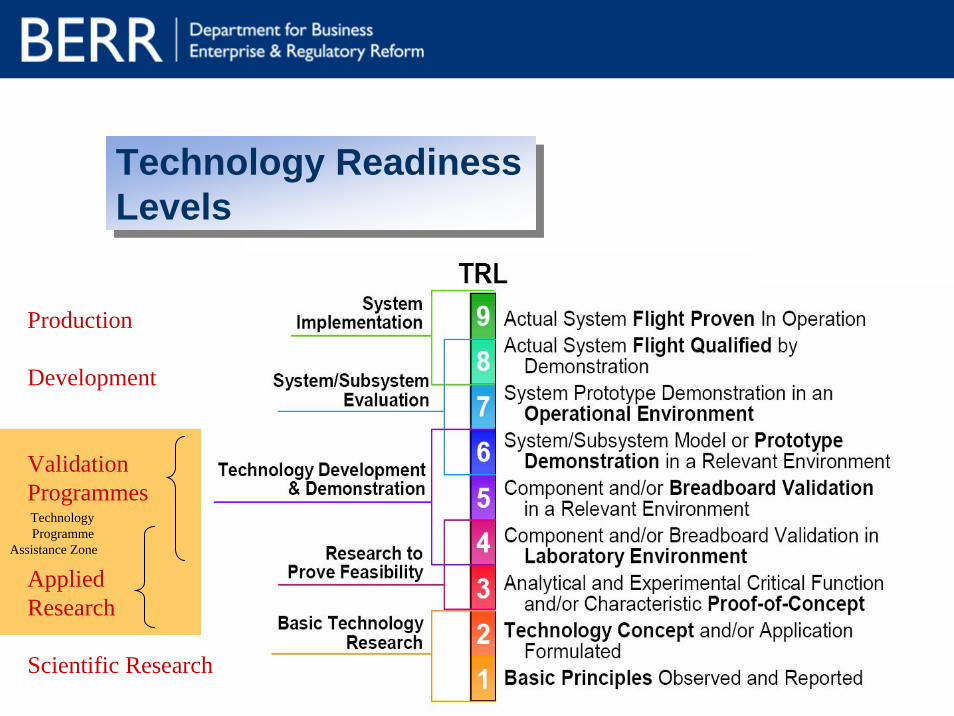

National Aerospace Technology Strategy

Integrated Wing

INFOAir

Production

Development

Validation Programmes

Applied Research

Scientific Research

Technology Programme

Assistance Zone

Technology Readiness LevelsTechnology Readiness Levels

What Has Been Achieved So Far

Achievements

• Aerospace & Defence Knowledge Transfer Network established that drives the sector forward through the challenges and opportunities it faces. The Network comprises of people and organisations including industry, universities, government and public sector bodies.

• Aerospace strategy implemented through projects supported by theTechnology Strategy Board and the regions in open cross-sector calls.

• Since 2004, the government has secured €291 million in aerospace research and technology programmes, including:– ASTRAEA Unmanned Air Vehicle programme– Centre for Fluid Mechanics Simulation– Integrated Wing– Environmentally Friendly Engine– Electronic Landing Gear Systems– Next Generation Composite Wingplus a range of underpinning research

• Government funding levels at around €69 million per year.

Environmentally Friendly Engine (EFE)• The programme is aimed at developing UK aerospace capabilities in the following fundamental

technologies:– High temperature materials. – High efficiency turbine components. – Low emissions combustion. – Advanced manufacturing technologies. – Engine controls and actuation technologies. – Nacelle aerodynamic technologies.

• A significant part of the programme will focus on the application of these technologies into specific components that then need to be integrated into a gas turbine engine. The core engine demonstrator vehicle will be tested at extremes of temperature and pressure, significantly in excess of current service design capability, in order to prove the technology and the improved efficiencies of the components and system. These improvements should lead to reduced fuel consumption, whist achieving significantly lower CO2 and NOX emissions at a lower engine-generated noise.

• Rolls-Royce as lead is partnering with, Bombardier Aerospace, Shorts (Northern Ireland), Goodrich Engine Control Systems (West Midlands), HS Marston (Wolverhampton) and Smiths (Burnley) as the industrial parties and the Universities of Oxford, Cambridge, Sheffield, Loughborough, Birminghamand Queens Belfast.

• EFE will address the engine technologies to deliver a 10% reduction in carbon dioxide emissions and a 60% reduction in nitrous oxides emissions. It will also provide the opportunity to validate other technologies to address other customer requirements such as the high temperature materials.

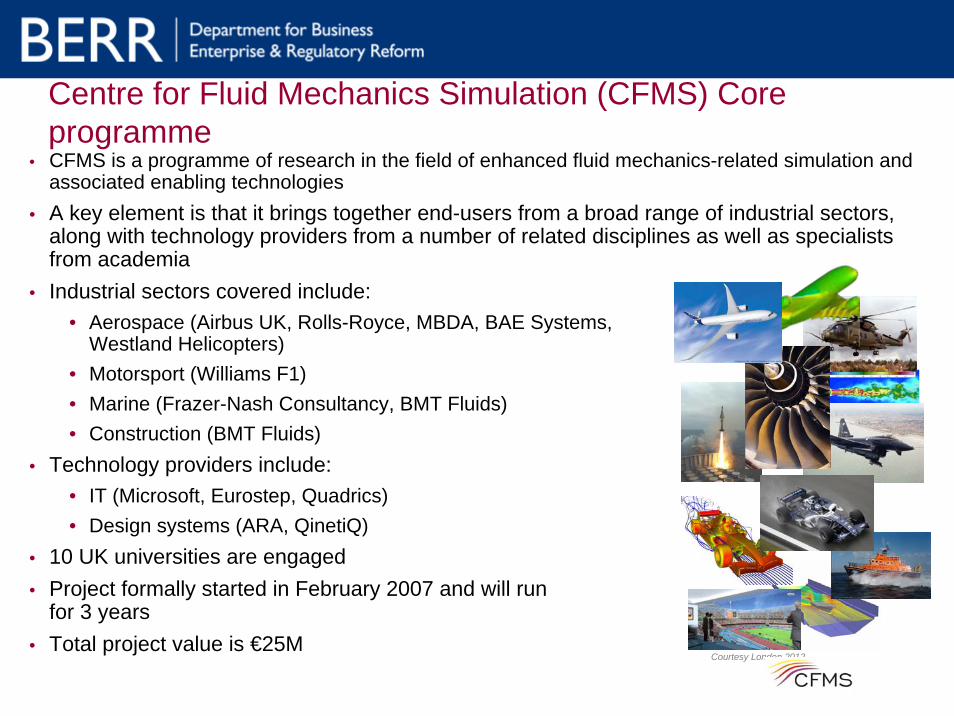

Centre for Fluid Mechanics Simulation (CFMS) Core programme

• CFMS is a programme of research in the field of enhanced fluid mechanics-related simulation and associated enabling technologies

• A key element is that it brings together end-users from a broad range of industrial sectors, along with technology providers from a number of related disciplines as well as specialists from academia

• Industrial sectors covered include:• Aerospace (Airbus UK, Rolls-Royce, MBDA, BAE Systems,

Westland Helicopters)• Motorsport (Williams F1)• Marine (Frazer-Nash Consultancy, BMT Fluids)• Construction (BMT Fluids)

• Technology providers include:• IT (Microsoft, Eurostep, Quadrics)• Design systems (ARA, QinetiQ)

• 10 UK universities are engaged• Project formally started in February 2007 and will run

for 3 years• Total project value is €25M

Courtesy London 2012

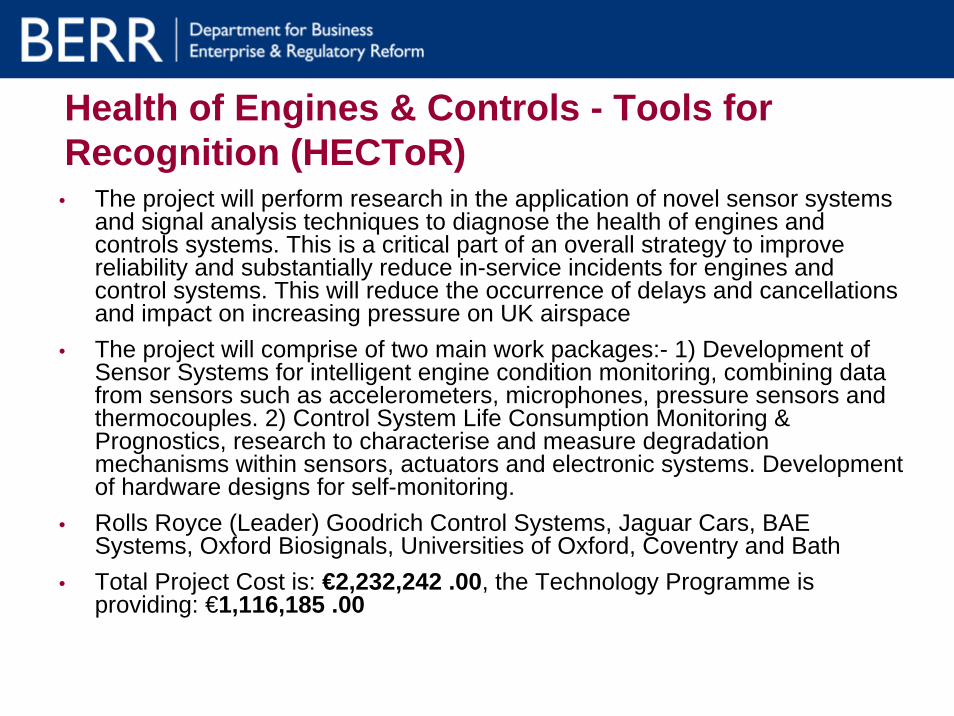

Health of Engines & Controls - Tools for Recognition (HECToR)

• The project will perform research in the application of novel sensor systems and signal analysis techniques to diagnose the health of engines and controls systems. This is a critical part of an overall strategy to improve reliability and substantially reduce in-service incidents for engines and control systems. This will reduce the occurrence of delays and cancellations and impact on increasing pressure on UK airspace

• The project will comprise of two main work packages:- 1) Development of Sensor Systems for intelligent engine condition monitoring, combining data from sensors such as accelerometers, microphones, pressure sensors and thermocouples. 2) Control System Life Consumption Monitoring & Prognostics, research to characterise and measure degradation mechanisms within sensors, actuators and electronic systems. Development of hardware designs for self-monitoring.

• Rolls Royce (Leader) Goodrich Control Systems, Jaguar Cars, BAE Systems, Oxford Biosignals, Universities of Oxford, Coventry and Bath

• Total Project Cost is: €2,232,242 .00, the Technology Programme is providing: €1,116,185 .00

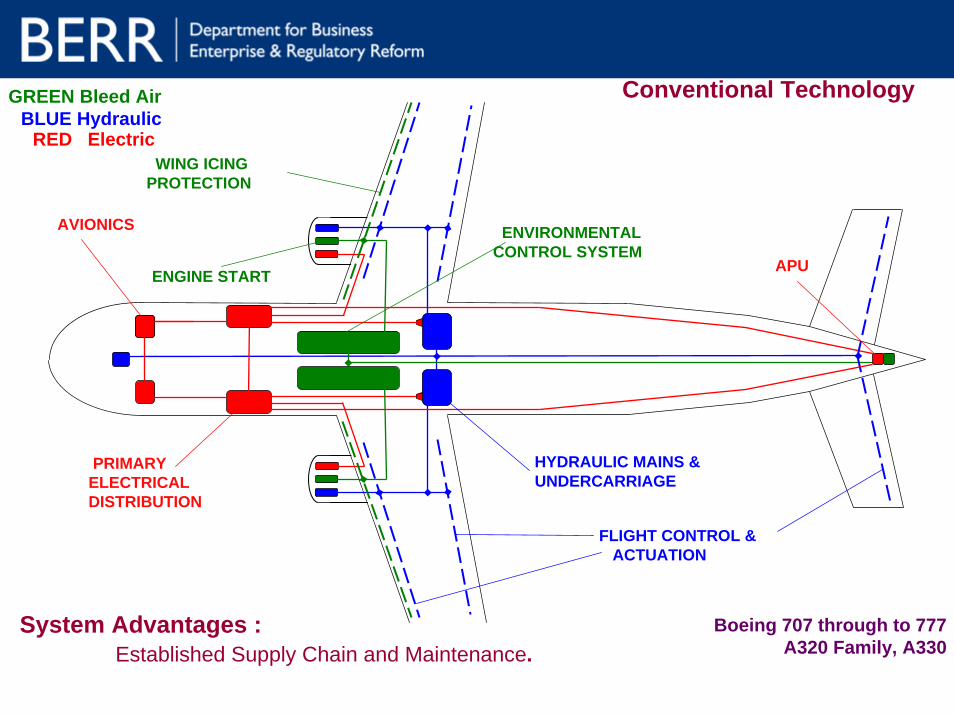

Conventional Technology

ENVIRONMENTAL CONTROL SYSTEM

PRIMARY ELECTRICAL DISTRIBUTION

AVIONICS

ENGINE START

WING ICING PROTECTION

APU

HYDRAULIC MAINS & UNDERCARRIAGE

FLIGHT CONTROL & ACTUATION

System Advantages : Established Supply Chain and Maintenance.

GREEN Bleed AirBLUE Hydraulic

RED Electric

Boeing 707 through to 777 A320 Family, A330

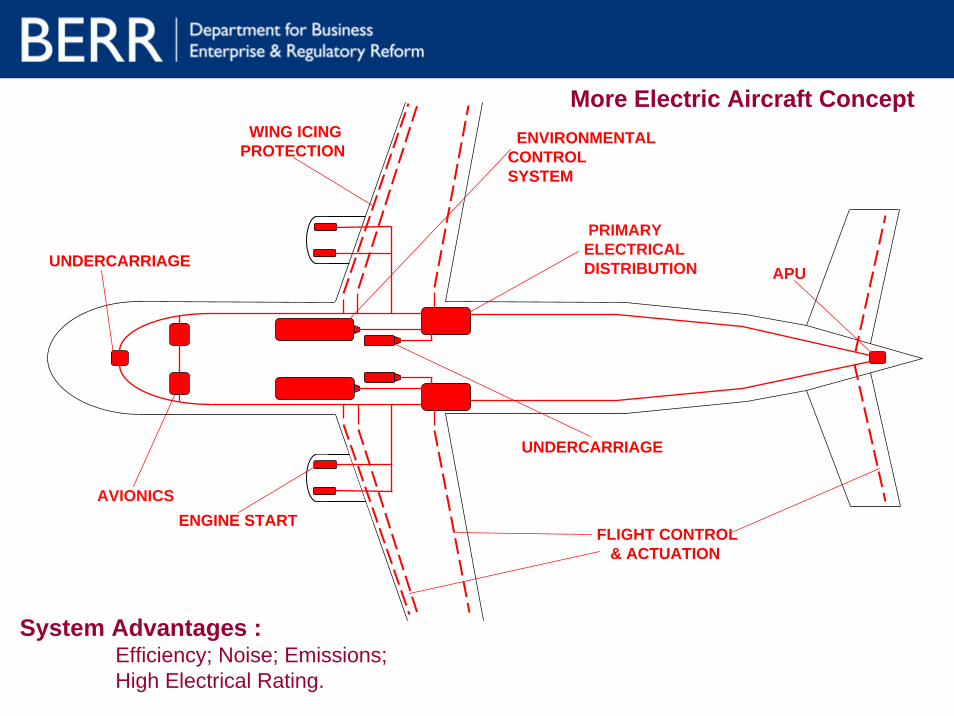

More Electric Aircraft Concept

System Advantages : Efficiency; Noise; Emissions; High Electrical Rating.

ENVIRONMENTAL CONTROL SYSTEM

PRIMARY ELECTRICAL DISTRIBUTION

AVIONICSENGINE START

WING ICING PROTECTION

APU

UNDERCARRIAGE

FLIGHT CONTROL & ACTUATION

UNDERCARRIAGE

Technology Programme

Technology Strategy Board• The Technology Strategy Board promotes innovation across all

business sectors through open competitions without sector budgets or sector calls.

• The Technology Strategy Board invests in projects involving business and researchers working together to deliver new technology-based products and services.

• Collaborative research and development assists business and researchers to work on projects in strategically important areas of science, engineering and technology which are the themes for thecalls - from which new products, processes and services can emerge.

• The new Technology Strategy Board strategy just announced with budget of €1.26 billion over 3 years including English regional and research council support. Two of the themes of this year’s calls have been announced “high value manufacturing” and “energy generation & supply”, but not the timing

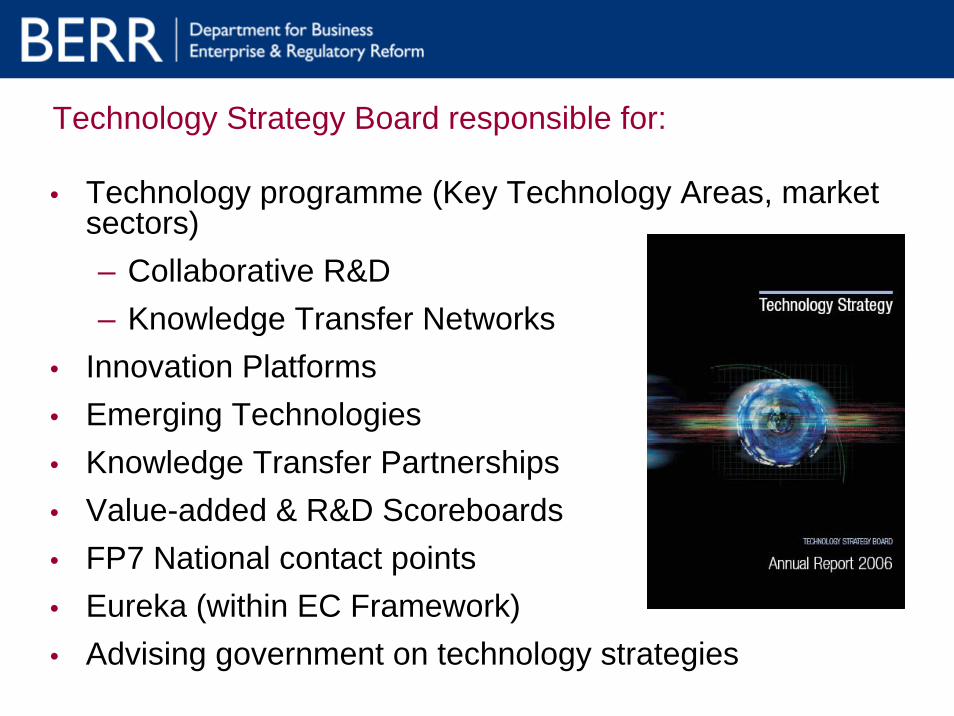

• Technology programme (Key Technology Areas, market sectors)– Collaborative R&D– Knowledge Transfer Networks

• Innovation Platforms• Emerging Technologies• Knowledge Transfer Partnerships• Value-added & R&D Scoreboards• FP7 National contact points• Eureka (within EC Framework) • Advising government on technology strategies

Technology Strategy Board responsible for:

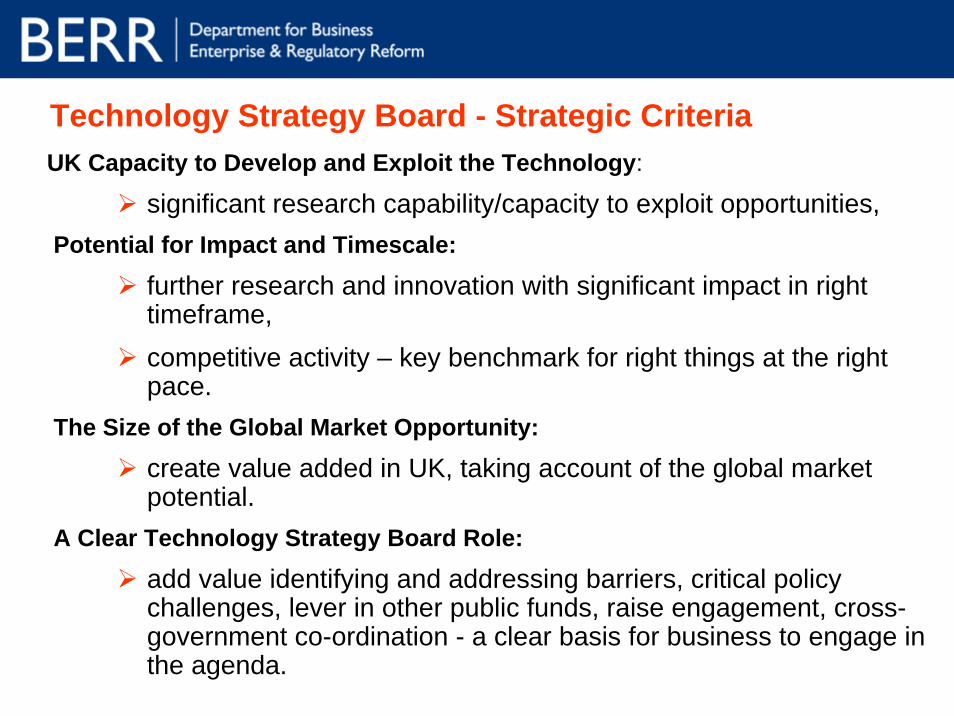

Technology Strategy Board - Strategic CriteriaUK Capacity to Develop and Exploit the Technology:

significant research capability/capacity to exploit opportunities,Potential for Impact and Timescale:

further research and innovation with significant impact in righttimeframe, competitive activity – key benchmark for right things at the right pace.

The Size of the Global Market Opportunity:

create value added in UK, taking account of the global market potential.

A Clear Technology Strategy Board Role:

add value identifying and addressing barriers, critical policy challenges, lever in other public funds, raise engagement, cross-government co-ordination - a clear basis for business to engage in the agenda.

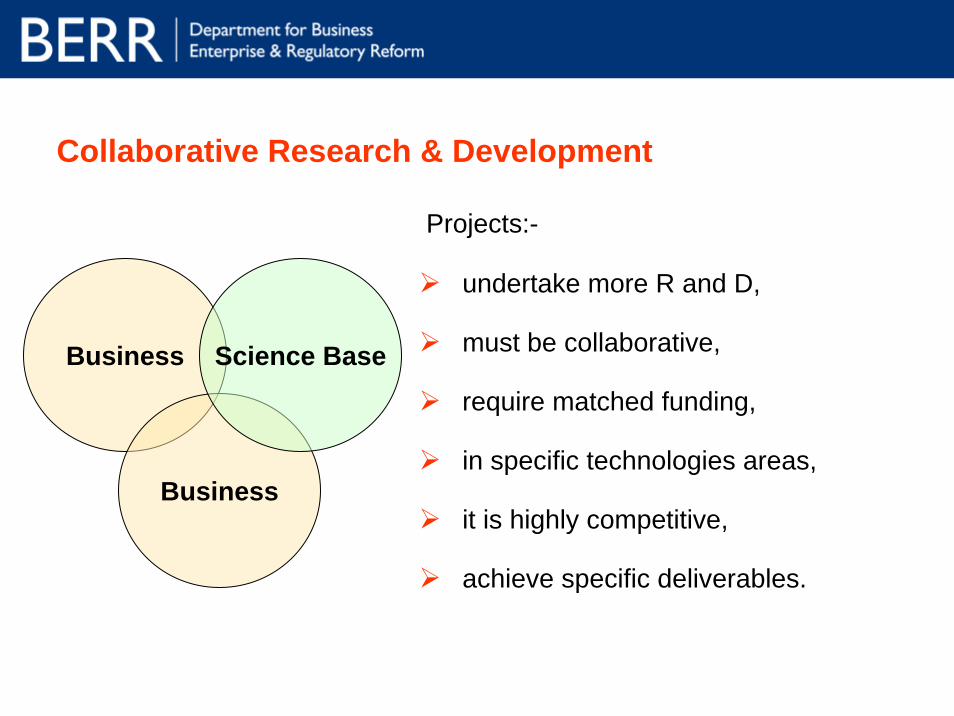

Collaborative Research & Development

Business

Business

Science Base

Projects:-

undertake more R and D,

must be collaborative,

require matched funding,

in specific technologies areas,

it is highly competitive,

achieve specific deliverables.

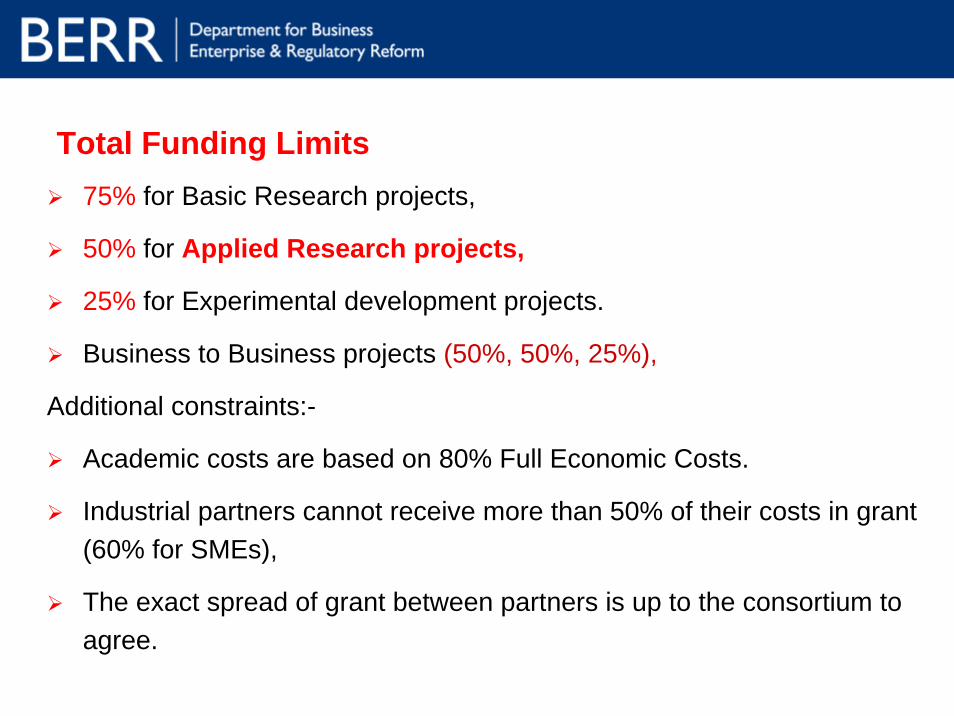

Total Funding Limits75% for Basic Research projects,

50% for Applied Research projects,

25% for Experimental development projects.

Business to Business projects (50%, 50%, 25%),

Additional constraints:-

Academic costs are based on 80% Full Economic Costs.

Industrial partners cannot receive more than 50% of their costs in grant (60% for SMEs),

The exact spread of grant between partners is up to the consortium to agree.

• Key enabling Technologies which underpin high value-added areas of UK economy.

Information and Communications TechnologiesBioscienceAdvanced Materials High Value ManufacturingElectronics, Photonics and Electrical TechnologiesHealthcare Technologies (including Pharmaceuticals)Energy Generation & TransmissionTransport (focus on aerospace & automotive)Environmental SustainabilityCreative Industries

Aerospace Interest

Key Technology/ Application Areas

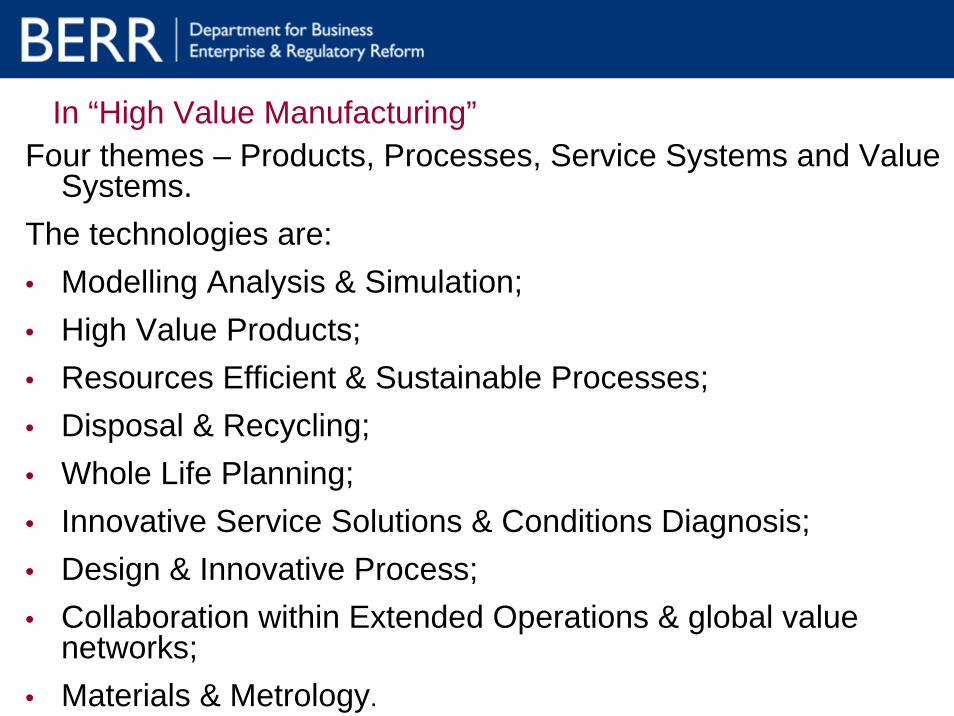

In “High Value Manufacturing”Four themes – Products, Processes, Service Systems and Value

Systems.The technologies are: • Modelling Analysis & Simulation; • High Value Products; • Resources Efficient & Sustainable Processes; • Disposal & Recycling; • Whole Life Planning; • Innovative Service Solutions & Conditions Diagnosis;• Design & Innovative Process; • Collaboration within Extended Operations & global value

networks; • Materials & Metrology.

Conclusions

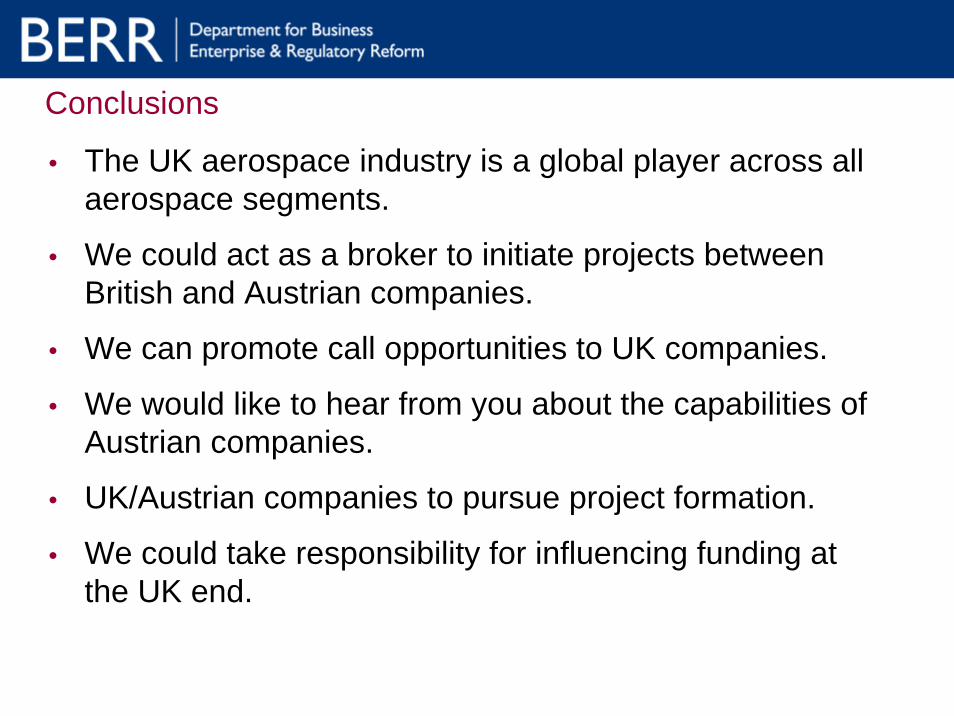

Conclusions

• The UK aerospace industry is a global player across all aerospace segments.

• We could act as a broker to initiate projects between British and Austrian companies.

• We can promote call opportunities to UK companies.

• We would like to hear from you about the capabilities of Austrian companies.

• UK/Austrian companies to pursue project formation.

• We could take responsibility for influencing funding at the UK end.

Questions ?

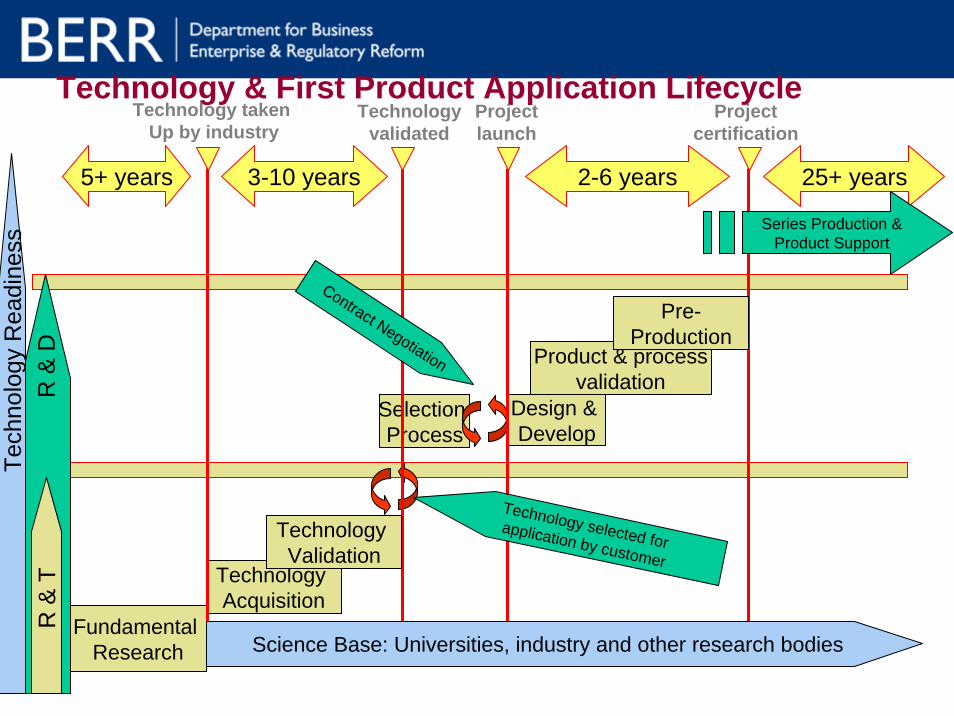

Technology & First Product Application LifecycleR

& D

R &

T

Fundamental Research

Technology Acquisition

Selection Process

Design & Develop

Product & processvalidation

Science Base: Universities, industry and other research bodies

5+ years

Tech

nolo

gy R

eadi

ness

3-10 years 2-6 years 25+ years

Pre-Production

Technology Validation

Technology selected for application by customer

Contract Negotiation

Series Production &Product Support

Technology taken Up by industry

Technologyvalidated

Projectlaunch

Projectcertification