broad brush 1 private bkg 08 11 18

TRANSCRIPT

15 Abchurch Lane, London EC4N 7BW UK

+44 20 7112 2131

www.spencejohnson.com

Welcome to our first edition of The Broad Brush. In each

we will aim briefly to describe a selection of the issues in

a one area of the investment landscape across which we roam

in our varied strategic research assignments.

We are very grateful to SEI, a leading global provider of

outsourced asset management, investment processing and

investment operations

solutions, for making the

findings in this edition

possible. SEI’s mission is to help firms in this space excel in the

delivery of advice, investment mangement and other wealth

management services while growing revenue, allocating capital

effectively, and managing risk.

This Summer our help was requested by SEI to explore the

changing landscape of wealth management in Europe. In order

to help it position itself for greatest success in these markets,

SEI asked us to add to its understanding of the strategic trends

and relevant issues in onshore and offshore private banking

and wealth management. Some outputs of this project are

shared with you in the following pages.

Please look out for further editions of The Broad Brush on

topics such as: Developments in DC Pensions, The Shift from

Products to Solutions in Asset Management, and Distribution of

Offshore Life Insurance Products.

As the dust eventually settles on the financial landscape,

there will be two businesses less damaged than most:

Private Banking and Wealth Management.

Asset management groups will seek out these firms more than

ever as potential buyers of their funds. The more resilient large

financial institutions will seek to acquire them for their ‘sticky’

assets. And investment bankers requiring fresh challenges

will set up new boutiques to compete in this market - always

assuming they have grasped that ‘product pushing’ is no longer

the name of the game here as it was in their old territory.

The first of our four sections focuses on the simple but

important point that the market is not homogenous. Existing

classifications give little clue to the underlying patterns. We

suggest a new Segmentation into ‘Factories’, ‘Cottages’ and

‘Homes’ (Stately- or Retirement-, take your pick).

This segmentation in turn unlocks new insights into the way

that private banks and wealth managers relate to their clients,

how and where they operate, and how they seek to grow.

These themes are explored in three further sections on

Offshore and Onshore, Discretionary and Advisory, and

the Hunt for Scale.

Please do give us your feedback.

Nils Johnson and Magnus Spence

Spence Johnson is a specialist provider of marketing intelligence. Our research products and consulting assignments support marketing, sales, and strategic planners across the investment business - in asset management, life & pensions and wealth management.

Factories, Homes & Cottages

A regular analysis of strategic marketing issues in the European investment business

Number 111 • 2008

The Broad Brush

A new look at the architecture of Private Banking in Europe

2

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

Segmentation

Private banks and wealth management firms are not a homogenous group. There are a wide variety of

business models. But the existing and conventional segment categories do not fully explain the distinct

behaviours which exist.

Research which we have recently carried out for SEI suggests that among the many available indicators,

that there are three key measures which provide the clues – the net worth of clients, the number of

clients, and type of mandate (discretionary/advisory).

Using these we have found coherent patterns. There are three main groups which emerge: Factories,

Cottages and Homes. No doubt further sub-categories can be developed, but these are the main ones.

This categorisation unlocks insights into the way that banks relate to their clients, how and where they

operate, and how they seek to grow. These themes are explored in the following sections.

Offshore and Onshore

Most banks service both onshore and offshore clients, although most specialise in one direction or the

other. The desire for offshore services is tax and privacy driven – the desire for secrecy is not the same

as desire to avoid tax. The Factories have the highest proportion of offshore clients. Some say offshore

is growing fastest, others the reverse.

Discretionary and Advisory

If we were to select one single feature which was most important for understanding the behaviour of any

Private bank or wealth management firm, it would be the proportions of its clients’ assets which are

Discretionary and Advisory.

Most banks are a mixture, but most focus on one or the other. Only one of our three segments, Homes,

is focused on discretionary business. Most Factories and Cottages are heavily weighted towards advisory

business.

Firms which have predominantly advisory clients reveal quite different economics and drivers to firms

with predominantly discretionary clients. For example discretionary clients are said to be much more

profitable, and many banks have been trying to increase their discretionary books. But very wealthy

clients are seldom discretionary.

Advisory clients offer the advantage of providing a lower ‘market exposure’ risk, which means that in any

market downturn advisory clients are less likely to blame their bank. Which in turn may explain why

advisory bankers in the current climate seem slightly less agitated than their discretionary focused

competitors.

Hunt for Scale

There is a big hunt for scale going on among Private banks and wealth management firms. In an

environment where growth may no longer come through stock markets, the need to maximise efficiency

is paramount. The industry is clearly being ‘industrialised’. But it is the Homes who need to see the

benefits of scale most, since they seek client volume in a way that Cottages, in particular, do not. One

measure in particular reveals most clearly the variety of attitudes towards scale – the number of

advisers per client.

Summary

Section 1

Page 3

Section 2

Page 7

Section 3

Page 11

Section 4

Page 16

3

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

We are one of only fourteen ‘real’ private banks in Switzerland – unlimited liability partnerships.

We’re a private bank, but we’re much closer to a multi-family office style business than we are to a private bank.

We are part PRIVATE Bank, part INVESTMENT Manager, part Family OFFICE. So we call ourselves a PRIVATE INVESTMENT OFFICE.

We are an integrated broad wealth management service, becoming trusted advisors to very high end families

Our model can be described as customer intimacy with holistic premium service.

The term private bank is very poorly defined. Most private banks, like us, just want to manage assets.

Our Swiss model: primarily advisory brokerage, and very traditional Swiss private banking

We offer what we call integrated wealth management - some people call this holistic wealth management

We are a global bank serving upper high net worth, international, commercial and lifestyle clients.

We offer all the Private Banking core services: banking, advisory, investment, and credit.

We are not an investment bank, we are not an asset manager. We are not a distributor. We are an aggregator.

There is an endless variety of business models

Partnership

Multi family office

Private Investment Office

Integrated and broad

Intimate, holistic

Asset management only

Swiss model

Holistic

Global lifestyle

Core services

Aggregation

Examples Descriptions given in interviews

There is an endless variety of business models in wealth management. This is not a homogenous group, it is highly varied. A sample of the variety is shown below. This prompted us to develop a more meaningful categorisation.

This variety is not a bad thing. Far from it, it shows a lively landscape. But it does make it difficult to analyse. As observers of the industry we must attempt to compare groups of firms, and this grouping is problematic.

One thing we found above all was that the conventional descriptions for grouping firms are not adequate. So for this project we have developed our own which more accurately (in our view) reflect the way firms actually behave.

1.1 Segmentation ● Variety

4

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

1

2

3

4

5

6

7

8

9

10

Net Worth Clients Mandate Domicile AuM Ownership Employees Offices Urgency

Highest score

Lowest score

Scores for each firm interviewed

1

2

3

4

5

6

7

8

9

10

Net Worth Clients Mandate Domicile AuM Ownership Employees Offices Urgency

Highest score

Lowest score

Scores for each firm interviewed

We suggest new ways of segmentingBy scoring each firm in a sample of 25 banks on ten features, we could scan visually for similar patterns. Three groups emerge: Factories, Cottages and Homes. Each group has clear common behaviour.

Most of the ten features we scored were not helpful in assessing differences. The chart above appears to show just a jumble of differences.

But by isolating the first three in the chart – the net worth of clients, the number of clients, and type of mandate (discretionary/advisory) – we can see patterns emerge. We suggest there are in fact three groups, Factories, Cottages and Homes, each with the broad characteristics shown here.

Factories are the larger firms, but include a variety of models. Cottages align closely to Family and Multi- Family offices in terms of commonly used terms. Homes are mostly smaller, and tend to be more focused on discretionary clients than the other types. We are tempted to call them ‘retirement homes’ because their clients are often more elderly.

1.2 Segmentation ● New ways

1

2

3

4

5

6

7

8

9

10

Net Worth Clients Mandate

1

2

3

4

5

6

7

8

9

10

Net Worth Clients Mandate

1

2

3

4

5

6

7

8

9

10

Net Worth Clients Mandate

1. Factories

• High number of clients

• Usually high in advisory

• Example UBS

2. Cottages

High net worth clients

Low number of clients

Example Lord North Street

• Low in advisory

• Lower net worth clients

• Example Rathbones

1

2

3

4

5

6

7

8

9

10

Net Worth Clients Mandate

1

2

3

4

5

6

7

8

9

10

Net Worth Clients Mandate

1

2

3

4

5

6

7

8

9

10

Net Worth Clients Mandate

1. Factories

• High number of clients

• Usually high in advisory

• Example UBS

2. Cottages

High net worth clients

Low number of clients

Example Lord North Street

3. Stately or Retirement Homes (‘Homes’)

• Low in advisory

• Lower net worth clients

• Example Rathbones

5

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

Services offered

0%

25%

50%

75%

100%

Factory Cottage Home

Investment Trusts Tax advice Banking Lending Custody Other

Services offered

0%

25%

50%

75%

100%

Factory Cottage Home

Investment Trusts Tax advice Banking Lending Custody Other

Factories tend to offer the broadest range of servicesAs you might expect Factories distinguish themselves by offering a wide variety of services, while Cottages and Homes focus on investment.

This is the key to the success of the big banks who have gathered so much more assets in recent years. They have easy access to specialists and a credible and wide collection of offerings.

You have to offer a wide range. If you don’t offer credits, for example, then others can have a hook into your clients. If others have a hook into your clients it becomes that much more difficult to maintain the client relationship.

Generally very wealthy clients don't need input on Trusts and so on - they are already in place. If they do, we introduce them to legal experts. We don't pretend to have specialist legal knowledge.

Most of our clients, in the wealth profile we’ve talked about, have accountants and lawyers advising them.

Our major value offering is service. Not tax.

We try to give to a soup-to-nuts service. But we don’t do everything, for example credits.

Clients do not want a bank offering. That is not what they are interested in.

Banking is not an attractive proposition. Commodity services like credits, credit cards, and chequebooks do not make money, but are nonetheless high risk, because they can ruin your reputation overnight if you get it wrong.

Some Factories maintain you have to have a wide offering

But Cottages and Homes generally avoid trying to compete with lawyers, and don’t want to provide low margin services like Banking and Credits.

The chart shows how varied the factories are, offering their clients everything from investment to trust and tax advice, banking and lending (credits).

The smaller Cottages and Homes are much more focused. As one told us, “generally very wealthy clients don't need input on Trusts and so on - they are already in place”.

1.3 Segmentation ● Services

Comments given in interviews

6

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

Homes focus on discretionary, onshore and less wealthyA key factor distinguishing Homes is that their clients tend to be onshore, discretionary, and are less wealthy than those of the Factories and Cottages.

Homes are clearly much more focused on onshore assets, which in turn tend to be more discretionary. Factories and Cottages are the reverse.

Homes are also much more focused on less wealthy clients, as shown in the lower chart. This is again in contrast to Factories and Cottages who tend to have much higher average AuM per client. Very wealthy client base also tends to indicate a high proportion of Offshore activity.

1.4 Segmentation ● Homes

R2 = 0.1222

0

5

10

0 5 10

Advisory Mandate

Off

sho

re d

om

icile

Offshore

Onshore

Discretionary Advisory

We live in a sort of virtual, global world. Because we’re advice led, we ’re upper high; we ’re upper of the upper where we ’re pitching, we ’re international. (F -1)

The discretionary side of the business is the one that ’s growing. The demand coming from the 45 to 55 year age bracket onshore in the UK is a huge area. (F -17)

Factory HomeCottage

Client base by domicile and mandate scores

R2 = 0.1222

0

5

10

0 5 10

Advisory Mandate

Off

sho

re d

om

icile

Offshore

Onshore

Discretionary Advisory

We live in a sort of virtual, global world. Because we’re advice led, we ’re upper high; we ’re upper of the upper where we ’re pitching, we ’re international.

The discretionary side of the business is the one that ’s growing. The demand coming from the 45 to 55 year age bracket onshore in the UK is a huge area.

Factory HomeCottage

Client base by domicile and mandate scores

R2 = 0.3145

0

5

10

0 5 10

Client Net Worth

Off

sho

re d

om

icil

e

Offshore

Onshore

Lower Higher

Our client, being the upper wealth, international, by definition, they have an international lifestyle. These clients tend to be serviced offshore.

There are very few truly global clients. Below about £10m. most client ’s needs are for domestic onshore services.

Client base by domicile and net worth scores

Comments given in interviews

Factory HomeCottage

Factory HomeCottage Comments given

in interviews

7

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

The desire for offshore services is tax and privacy drivenThe days of tax avoidance are (most say) now gone – offshore is now mostly used by those seeking tax efficiency and privacy

Companies are increasingly using offshore centers' as a way of owning their businesses through what are called ‘tax blockers’. This is based on the principal that tax authorities never go up the whole chain

Offshore activities are nowadays particularly relevant, for those who want to be or who can successfully be taxed on a remittance basis. This means that they are taxed eventually when they bring the assets onshore, but in the meantime are able to postpone any tax.

In my view, offshore is still used to a large extent for hiding money. I have seen estimates which suggest that half of the money in Switzerland has never been declared to a tax authority anywhere.

Offshore clients are internationally mobile; working away from their home country or have business interests in several countries.

Our client, being the upper wealth & international, by definition, they have an international lifestyle so they tend to be serviced offshore. Clients come to us because, through us they can access the world. We live in a sort of virtual, global world. It’s on and offshore both.

For the offshore clients, if you’re a Kazakh or a Russian or a Peruvian for instance, and you’ve put your money in Zurich, you’ve normally done it for a reason, and secrecy is part of that reason. It’s not necessarily about tax, but in some cases it’s about not wanting people or your government to know, because they might shoot you.

There are several other reasons, apart from plain fraud, why assets are moved offshore. General secrecy is definitely a factor. So also is secrecy from one’s own relatives.

There are still clients from less developed countries with high tax regimes who use offshore assets as ‘run to the airport’ money - a safety factor.

By moving assets offshore, clients can delay tax, and achieve other legal tax related advantages.

Tax avoidance may not have disappeared completely

Offshore clients are often said to be highly international, and in need of international financial services

Another frequently mentioned need was secrecy

Offshore clients are often said to be highly international, and in need of international financial services. This includes tax saving advice and services like Trusts.

While most insist that regulatory and anti-terrorist pressures have signalled the end of tax avoidance in most European offshore locations, some beg to differ and argue that “offshore is still used to a large extent for hiding money”.

2.1 Offshore and onshore ● Tax driven

Comments given in interviews

8

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

Desire for secrecy is not the same as desire to avoid taxMany in the industry now talk about the need for privacy or secrecy as a key driver of offshore business. They can quote many examples of how an individual might want secrecy whilst still not trying to avoid tax. We captured three short case studies:

2.2 Offshore and onshore ● Secrecy

Why German clients like Switzerland

There are several reasons why German clients like to use Swiss private banks.

They aren’t looking to hide their assets, and are quite willing to be completely open and transparent, and to pay all taxes. This also applies to clients from the Emirates.

What they are looking to achieve is to spread their assets by geography, so in many cases they will have some of their assets in Switzerland, and some elsewhere.

They are also looking to spread their risk by currency, and Switzerland is a natural home for some of their assets.

Switzerland also has a stable government, which is appealing to people from Germany who have memories of very unstable governments in the past.

Another factor is that many wealthy Germans and other Europeans are coming to live in Switzerland. A lot of Formula One drivers now live around Lake Geneva, for example.

Another factor is that they like the fact that Swiss bankers are more international and better educated.

Case Study A

Four legal reasons why assets are moved offshore

There are several other reasons, apart from plain fraud, why assets are moved offshore.

1. General secrecy from authorities is definitely a factor.

2. So also is secrecy from one’s own relatives. In many cases, it is easier for a family to keep its assets offshore to avoid disputes between family members.

3. Inheritance tax avoidance is another major factor.

4. I have heard of people living in less secure countries who keep their assets offshore to avoid kidnapping risks, which are prevalent, for example, in South America.

Case Study B

Why some people want money to be secret

If you’re a Kazakh or a Russian or a Peruvian for instance, and you’ve put your money in Zurich, you’ve normally done it for a reason, and secrecy is part of that reason.

It’s not necessarily about tax, but in some cases it’s about not wanting people or your government to know, because they might shoot you.

They are cultural reasons: local crime and local fiscal corruption. We have clients who don’t want statements mailed to them because they don’t want the postman to see it. They’re worried the kids will get kidnapped.

So it can be very simple.

Most UK clients are less worried about secrecy - leaving tax aside, there are less people who are going to abuse it. By and large the risks of being got at by your government or your local warlord or whatever are limited in most parts of London!

Case Study C

Why German clients like Switzerland

There are several reasons why German clients like to use Swiss private banks.

They aren’t looking to hide their assets, and are quite willing to be completely open and transparent, and to pay all taxes. This also applies to clients from the Emirates.

What they are looking to achieve is to spread their assets by geography, so in many cases they will have some of their assets in Switzerland, and some elsewhere.

They are also looking to spread their risk by currency, and Switzerland is a natural home for some of their assets.

Switzerland also has a stable government, which is appealing to people from Germany who have memories of very unstable governments in the past.

Another factor is that many wealthy Germans and other Europeans are coming to live in Switzerland. A lot of Formula One drivers now live around Lake Geneva, for example.

Another factor is that they like the fact that Swiss bankers are more international and better educated.

Case Study A

Four legal reasons why assets are moved offshore

There are several other reasons, apart from plain fraud, why assets are moved offshore.

1. General secrecy from authorities is definitely a factor.

2. So also is secrecy from one’s own relatives. In many cases, it is easier for a family to keep its assets offshore to avoid disputes between family members.

3. Inheritance tax avoidance is another major factor.

4. I have heard of people living in less secure countries who keep their assets offshore to avoid kidnapping risks, which are prevalent, for example, in South America.

Case Study B

Why some people want money to be secret

If you’re a Kazakh or a Russian or a Peruvian for instance, and you’ve put your money in Zurich, you’ve normally done it for a reason, and secrecy is part of that reason.

It’s not necessarily about tax, but in some cases it’s about not wanting people or your government to know, because they might shoot you.

They are cultural reasons: local crime and local fiscal corruption. We have clients who don’t want statements mailed to them because they don’t want the postman to see it. They’re worried the kids will get kidnapped.

So it can be very simple.

Most UK clients are less worried about secrecy - leaving tax aside, there are less people who are going to abuse it. By and large the risks of being got at by your government or your local warlord or whatever are limited in most parts of London!

Case Study C

9

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

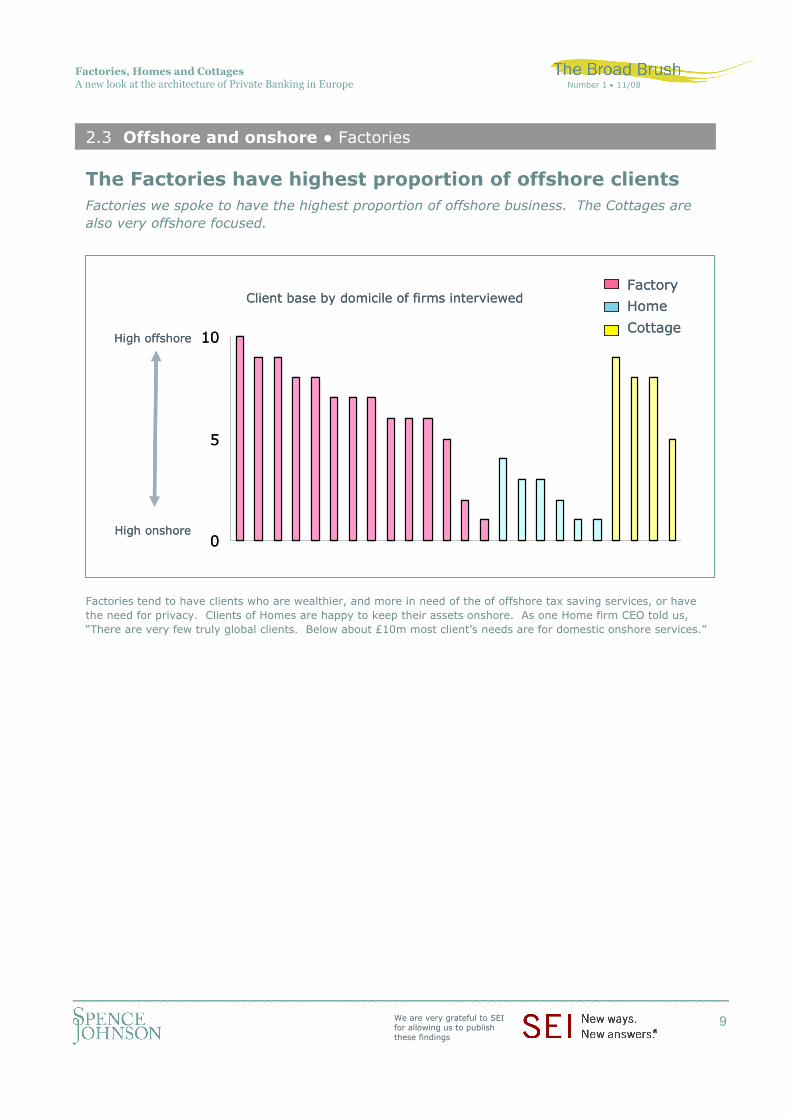

The Factories have highest proportion of offshore clientsFactories we spoke to have the highest proportion of offshore business. The Cottages are also very offshore focused.

Factories tend to have clients who are wealthier, and more in need of the of offshore tax saving services, or have the need for privacy. Clients of Homes are happy to keep their assets onshore. As one Home firm CEO told us, “There are very few truly global clients. Below about £10m most client’s needs are for domestic onshore services.”

0

5

10

Factory

Home

CottageHigh offshore

High onshore

Client base by domicile of firms interviewed

0

5

10

Factory

Home

CottageHigh offshore

High onshore

Client base by domicile of firms interviewed

2.3 Offshore and onshore ● Factories

10

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

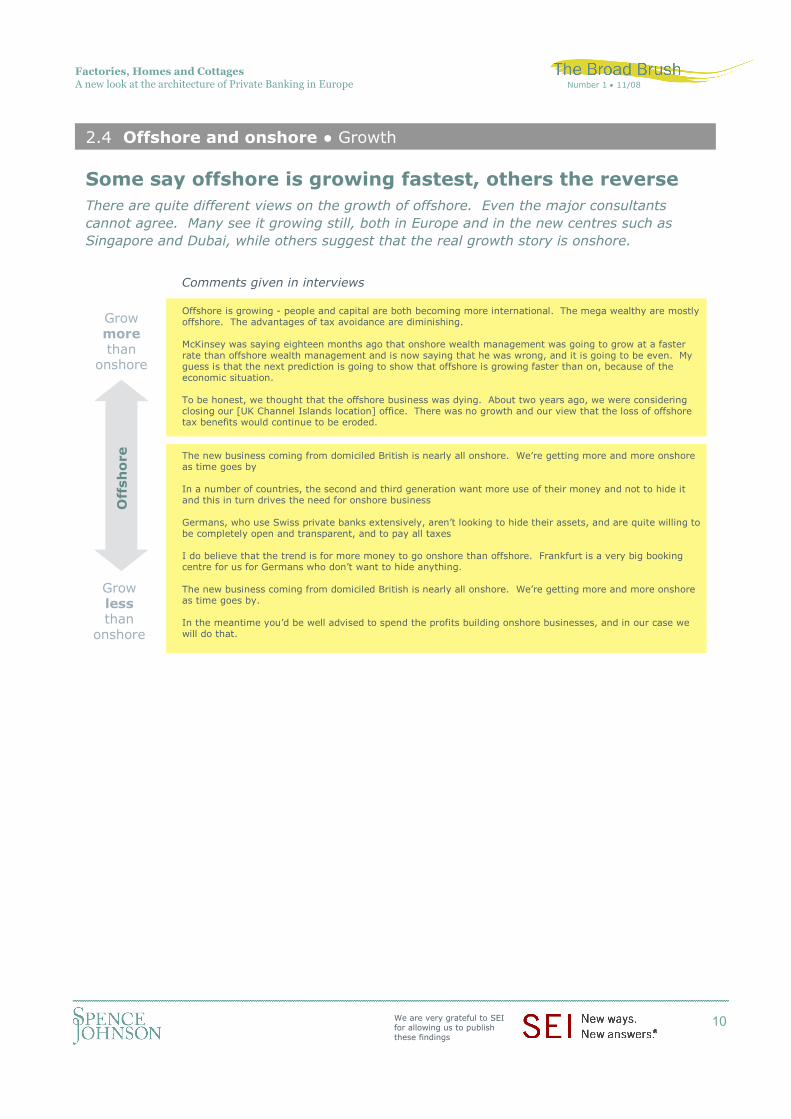

Some say offshore is growing fastest, others the reverseThere are quite different views on the growth of offshore. Even the major consultants cannot agree. Many see it growing still, both in Europe and in the new centres such as Singapore and Dubai, while others suggest that the real growth story is onshore.

Offshore is growing - people and capital are both becoming more international. The mega wealthy are mostly offshore. The advantages of tax avoidance are diminishing.

McKinsey was saying eighteen months ago that onshore wealth management was going to grow at a faster rate than offshore wealth management and is now saying that he was wrong, and it is going to be even. My guess is that the next prediction is going to show that offshore is growing faster than on, because of the economic situation.

To be honest, we thought that the offshore business was dying. About two years ago, we were considering closing our [UK Channel Islands location] office. There was no growth and our view that the loss of offshore tax benefits would continue to be eroded.

The new business coming from domiciled British is nearly all onshore. We’re getting more and more onshore as time goes by

In a number of countries, the second and third generation want more use of their money and not to hide it and this in turn drives the need for onshore business

Germans, who use Swiss private banks extensively, aren’t looking to hide their assets, and are quite willing to be completely open and transparent, and to pay all taxes

I do believe that the trend is for more money to go onshore than offshore. Frankfurt is a very big booking centre for us for Germans who don’t want to hide anything.

The new business coming from domiciled British is nearly all onshore. We’re getting more and more onshore as time goes by.

In the meantime you’d be well advised to spend the profits building onshore businesses, and in our case we will do that.

Off

sho

re

Growlessthan

onshore

Growmorethan

onshore

2.4 Offshore and onshore ● Growth

Comments given in interviews

11

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

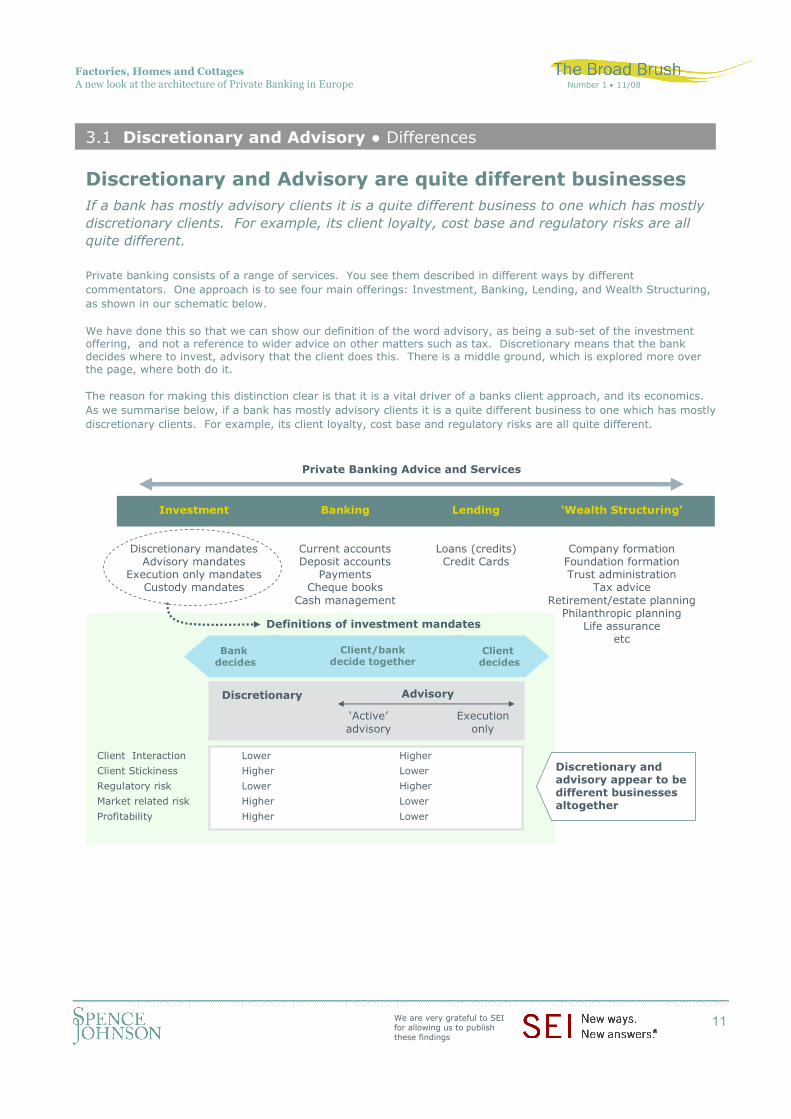

Discretionary and Advisory are quite different businessesIf a bank has mostly advisory clients it is a quite different business to one which has mostly discretionary clients. For example, its client loyalty, cost base and regulatory risks are all quite different.

Investment

Discretionary mandatesAdvisory mandates

Execution only mandatesCustody mandates

Banking

Current accountsDeposit accounts

PaymentsCheque books

Cash management

‘Wealth Structuring’

Company formationFoundation formationTrust administration

Tax adviceRetirement/estate planning

Philanthropic planningLife assurance

etc

Lending

Loans (credits)Credit Cards

Client decides

Bank decides

Discretionary Advisory

Execution only

‘Active’advisory

Definitions of investment mandates

Private Banking Advice and Services

Client Interaction Lower Higher

Client Stickiness Higher Lower

Regulatory risk Lower Higher

Market related risk Higher Lower

Profitability Higher Lower

Discretionary and advisory appear to be different businesses altogether

Client/bank decide together

Private banking consists of a range of services. You see them described in different ways by different commentators. One approach is to see four main offerings: Investment, Banking, Lending, and Wealth Structuring, as shown in our schematic below.

We have done this so that we can show our definition of the word advisory, as being a sub-set of the investment offering, and not a reference to wider advice on other matters such as tax. Discretionary means that the bank decides where to invest, advisory that the client does this. There is a middle ground, which is explored more over the page, where both do it.

The reason for making this distinction clear is that it is a vital driver of a banks client approach, and its economics. As we summarise below, if a bank has mostly advisory clients it is a quite different business to one which has mostly discretionary clients. For example, its client loyalty, cost base and regulatory risks are all quite different.

3.1 Discretionary and Advisory ● Differences

12

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

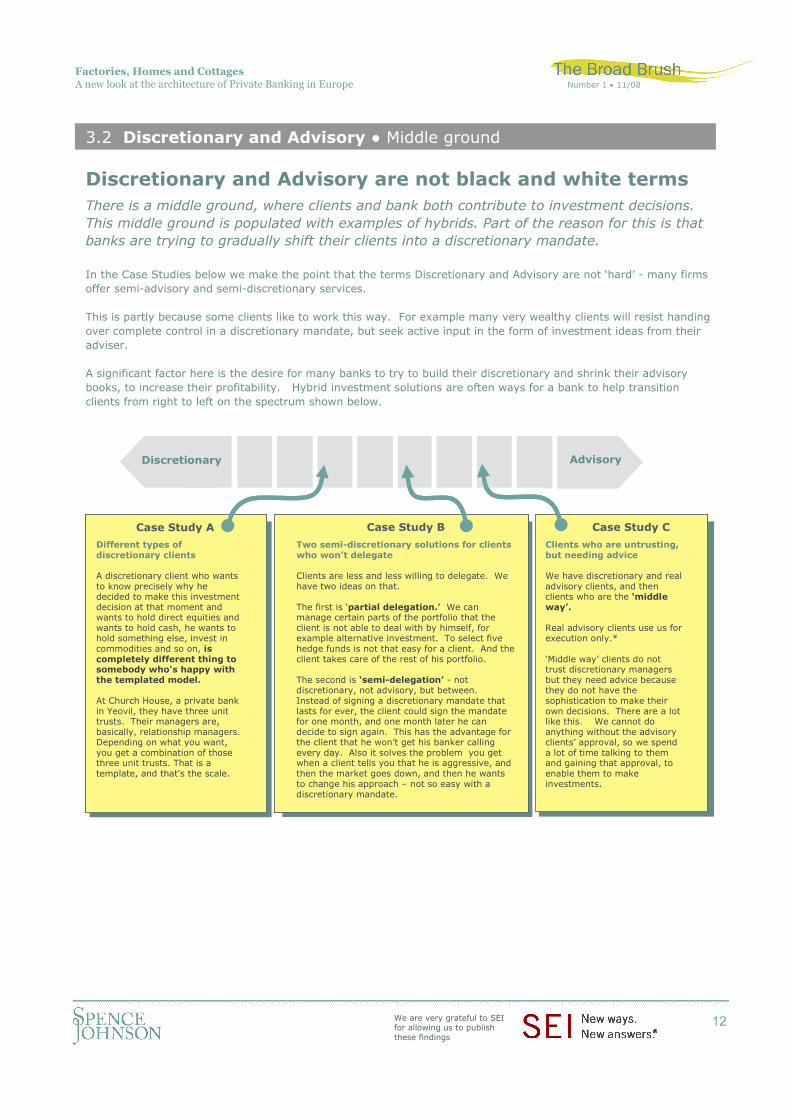

Discretionary and Advisory are not black and white termsThere is a middle ground, where clients and bank both contribute to investment decisions. This middle ground is populated with examples of hybrids. Part of the reason for this is that banks are trying to gradually shift their clients into a discretionary mandate.

In the Case Studies below we make the point that the terms Discretionary and Advisory are not ‘hard’ - many firms offer semi-advisory and semi-discretionary services.

This is partly because some clients like to work this way. For example many very wealthy clients will resist handing over complete control in a discretionary mandate, but seek active input in the form of investment ideas from their adviser.

A significant factor here is the desire for many banks to try to build their discretionary and shrink their advisory books, to increase their profitability. Hybrid investment solutions are often ways for a bank to help transition clients from right to left on the spectrum shown below.

3.2 Discretionary and Advisory ● Middle ground

Clients who are untrusting, but needing advice

We have discretionary and real advisory clients, and then clients who are the ‘middle way’.

Real advisory clients use us for execution only.*

‘Middle way’ clients do not trust discretionary managers but they need advice because they do not have the sophistication to make their own decisions. There are a lot like this. We cannot do anything without the advisory clients’ approval, so we spend a lot of time talking to them and gaining that approval, to enable them to make investments.

Two semi-discretionary solutions for clients who won’t delegate

Clients are less and less willing to delegate. We have two ideas on that.

The first is ‘partial delegation.’ We can manage certain parts of the portfolio that the client is not able to deal with by himself, for example alternative investment. To select five hedge funds is not that easy for a client. And the client takes care of the rest of his portfolio.

The second is ‘semi-delegation’ - not discretionary, not advisory, but between. Instead of signing a discretionary mandate that lasts for ever, the client could sign the mandate for one month, and one month later he can decide to sign again. This has the advantage for the client that he won’t get his banker calling every day. Also it solves the problem you get when a client tells you that he is aggressive, and then the market goes down, and then he wants to change his approach – not so easy with a discretionary mandate.

Different types of discretionary clients

A discretionary client who wants to know precisely why he decided to make this investment decision at that moment and wants to hold direct equities and wants to hold cash, he wants to hold something else, invest in commodities and so on, is completely different thing to somebody who's happy with the templated model.

At Church House, a private bank in Yeovil, they have three unit trusts. Their managers are, basically, relationship managers. Depending on what you want, you get a combination of those three unit trusts. That is a template, and that's the scale.

AdvisoryDiscretionary

Case Study CCase Study BCase Study A

Clients who are untrusting, but needing advice

We have discretionary and real advisory clients, and then clients who are the ‘middle way’.

Real advisory clients use us for execution only.*

‘Middle way’ clients do not trust discretionary managers but they need advice because they do not have the sophistication to make their own decisions. There are a lot like this. We cannot do anything without the advisory clients’ approval, so we spend a lot of time talking to them and gaining that approval, to enable them to make investments.

Two semi-discretionary solutions for clients who won’t delegate

Clients are less and less willing to delegate. We have two ideas on that.

The first is ‘partial delegation.’ We can manage certain parts of the portfolio that the client is not able to deal with by himself, for example alternative investment. To select five hedge funds is not that easy for a client. And the client takes care of the rest of his portfolio.

The second is ‘semi-delegation’ - not discretionary, not advisory, but between. Instead of signing a discretionary mandate that lasts for ever, the client could sign the mandate for one month, and one month later he can decide to sign again. This has the advantage for the client that he won’t get his banker calling every day. Also it solves the problem you get when a client tells you that he is aggressive, and then the market goes down, and then he wants to change his approach – not so easy with a discretionary mandate.

Different types of discretionary clients

A discretionary client who wants to know precisely why he decided to make this investment decision at that moment and wants to hold direct equities and wants to hold cash, he wants to hold something else, invest in commodities and so on, is completely different thing to somebody who's happy with the templated model.

At Church House, a private bank in Yeovil, they have three unit trusts. Their managers are, basically, relationship managers. Depending on what you want, you get a combination of those three unit trusts. That is a template, and that's the scale.

AdvisoryDiscretionary

Case Study CCase Study BCase Study A

13

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

Mandate type is vital, but is often overlooked. Why?We have argued that the distinction between Discretionary and Advisory client mandates is a key factor in determining the character of a bank. But amazingly this distinction is not often made by industry observers, possibly because the measure is difficult to get or to predict.

The distinction between advisory and discretionary is a vital clue to the nature of any Private Bank, but it is very difficult measure to obtain. Possibly as a result many industry studies ignore it – a big mistake in our view.

Nor is this measure easy to predict from the outside. For example, as our two charts show, it is not correlated either to size of AuM, nor to the average net worth of clients.

* Top ten UK private client wealth managers. Source: Landsbanki Securities estimates. Private Client Wealth Management report, October 2007.

3.3 Discretionary and Advisory ● Unpredictable

*

100% Advisory

100% Discretionary

R2 = 0.2341

0

5

10

0 5 10

AuM

Man

date

R2 = 0.0901

£0 £20 £40

£m Aum

Other evidence

Mandate type vs AuM

100% Advisory

100% Discretionary

R2 = 0.2341

0

5

10

0 5 10

AuM

Man

date

R2 = 0.0901

£0 £20 £40

£m Aum

Evidence from this project

Mandate type vs AuM

R2 = 0.0014

£0 £3 £6

£m Minimum Assets

R2 = 0.0142

0

5

10

0 5 10

Net Worth

Man

date

Mandate type vs Net Worth of Clients

100% Advisory

100% Discretionary

R2 = 0.0014

£0 £3 £6

£m Minimum Assets

R2 = 0.0142

0

5

10

0 5 10

Net Worth

Man

date

Mandate type vs Net Worth of Clients

100% Advisory

100% Discretionary

*Other evidenceEvidence from this project

14

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

There is no consensus on growth of discretionary For every respondent who told us they thought their discretionary client base was growing the fastest, we were told by someone else that it was their advisory clients who are growing most.

Many Factories would like to have more discretionary business. They find advisory work to be demanding and less profitable. But despite the desire of many firms for this to happen, we saw no evidence of a shift taking place from advisory to discretionary. If anything the opposite was more prominent. For example, some Factories say that discretionary is risky and unattractive, particularly in the current market conditions, and is shrinking.

After all advisory business offers the advantage of providing a lower ‘market exposure’ risk, which means that in any market downturn advisory clients are less likely to blame their bank. Which in turn may explain why advisory bankers in the current climate seem slightly less agitated than their discretionary focused competitors.

We much prefer discretionary clients who are easier to manage. Advisory relationships are much more difficult to hold onto.

Advisory are the clients who take up most of our time, and who cost us the most.

No one wants the headache of dealing with advisory clients. Most of us want discretionary clients.

Discretionary is only about a third of the market today, and probably growing.

Some of the smarter banks (like EFG) actually try to avoid discretionary altogether - recognising that there are quite big risks for the bank when markets turn down.

The proportion of our AuM in discretionary is going down. Clients are less and less willing to delegate. We don’t aim to develop discretionary portfolio management as a priority.

I think there’s a little less demand for discretionary investment today, the new money wants to be a bit more hands on.

We needed a more diversified business mix, so we started to build a transaction based book.

I think we should build an advisory desk. A lot of people have a very transactional attitude to their money.

Many Factories would like to have more discretionary business

They find advisory work to be demanding and less profitable

Discretionary firms agree – they prefer discretionary mandates

The Discretionary firms see continued growth in this business

Some Factories think the opposite –discretionary is risky and unattractive, and is shrinking

We saw no evidence of a shift taking place from advisory to discretionary – if anything the opposite

Some Cottage firms agree – they think most new money is Advisory

Some Cottages have seen benefits in actively growing their advisory side

Now some Discretionary firms are thinking the same way

Dis

creti

on

ary

Shrink

Grow

We much prefer discretionary clients who are easier to manage. Advisory relationships are much more difficult to hold onto.

Advisory are the clients who take up most of our time, and who cost us the most.

No one wants the headache of dealing with advisory clients. Most of us want discretionary clients.

Discretionary is only about a third of the market today, and probably growing.

Some of the smarter banks (like EFG) actually try to avoid discretionary altogether - recognising that there are quite big risks for the bank when markets turn down.

The proportion of our AuM in discretionary is going down. Clients are less and less willing to delegate. We don’t aim to develop discretionary portfolio management as a priority.

I think there’s a little less demand for discretionary investment today, the new money wants to be a bit more hands on.

We needed a more diversified business mix, so we started to build a transaction based book.

I think we should build an advisory desk. A lot of people have a very transactional attitude to their money.

Many Factories would like to have more discretionary business

They find advisory work to be demanding and less profitable

Discretionary firms agree – they prefer discretionary mandates

The Discretionary firms see continued growth in this business

Some Factories think the opposite –discretionary is risky and unattractive, and is shrinking

We saw no evidence of a shift taking place from advisory to discretionary – if anything the opposite

Some Cottage firms agree – they think most new money is Advisory

Some Cottages have seen benefits in actively growing their advisory side

Now some Discretionary firms are thinking the same way

Dis

creti

on

ary

Shrink

Grow

3.4 Discretionary and Advisory ● Growth

Comments given in interviews

15

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

Discretionary may be particularly high in the UKWhy is it that UK banks seem to be so much more reliant on discretionary business than those in Switzerland? Rather backing up our point that not enough analysis is being done on the discretionary/advisory distinction, no one seems to know the answer to this question.

No one seems able to tell us why discretionary business is apparently so much higher among UK Private Banks than Swiss ones.

Some say that this is because UK money is ‘lazy’, although others disagree, vehemently, on this point.

Our sample included many Homes in the UK, but few in Switzerland, and this may have distorted the measure. Discretionary may be abundant among smaller Home-type banks focused on onshore clients in Switzerland, and elsewhere, especially in Germany.

0

5

10 Sample by location of HQAdvisory

Discr.

Within our sample a high proportion of the UK firms had low exposure to advisory, high to discretionary, unlike other nationalities.

Swiss

UK

Other

0

5

10 Sample by location of HQAdvisory

Discr.

Within our sample a high proportion of the UK firms had low exposure to advisory, high to discretionary, unlike other nationalities.

Swiss

UK

Other

In Switzerland we are primarily advisory but here in London we are 100% discretionary.

We have looked at taking our UK-style model to Europe, but the actual culture of the type of investment we do is not as prevalent as it is here.

UK onshore discretionary money is often old, ‘lazy’ money – unique to the UK.

The US clients tend to want more advisory services. Whereas I think the UK guys, they’re all time deprived, and don’t seem as interested.

If anything, UK money is more sophisticated, on average. Plenty of quite financially aggressive, far from lazy, entrepreneurs use discretionary for a portion of their assets - because they're time poor and/or want their money managed in a customised or specialist discretionary mandates.

The average for discretionary assets in Switzerland is about 50% in the firms I know.

I do believe that the trend is for more money to go onshore than offshore. Frankfurt is a very big booking centre for us for Germans who don’t want to hide anything. There is more and more onshore business from Germany. UBS has done very well there.

It is possible that the UK is quite unique in being heavy in discretionary business

Others disagree. They say UK discretionary assets are not ‘lazy’. It is also likely that discretionary is also in abundance in other countries, we just haven’t seen it in this project

3.5 Discretionary and Advisory ● UK differences

Comments given in interviews

16

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

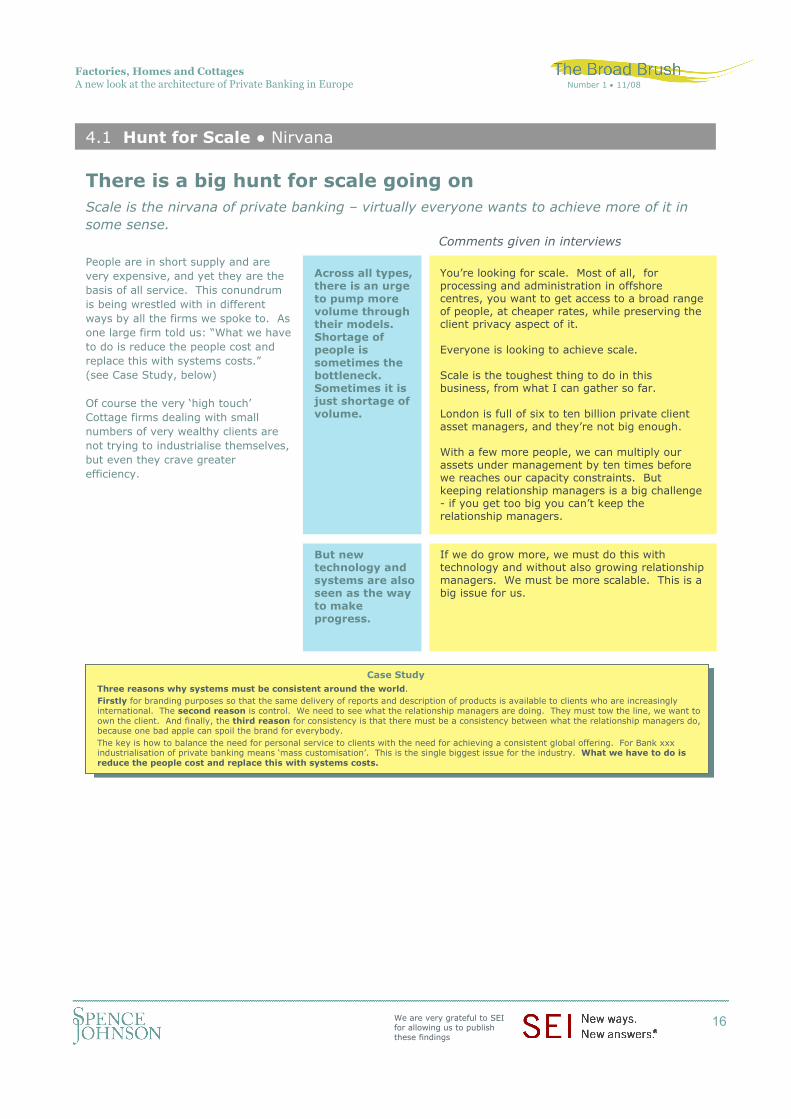

There is a big hunt for scale going onScale is the nirvana of private banking – virtually everyone wants to achieve more of it in some sense.

You’re looking for scale. Most of all, for processing and administration in offshore centres, you want to get access to a broad range of people, at cheaper rates, while preserving the client privacy aspect of it.

Everyone is looking to achieve scale.

Scale is the toughest thing to do in this business, from what I can gather so far.

London is full of six to ten billion private client asset managers, and they’re not big enough.

With a few more people, we can multiply our assets under management by ten times before we reaches our capacity constraints. But keeping relationship managers is a big challenge - if you get too big you can’t keep the relationship managers.

If we do grow more, we must do this with technology and without also growing relationship managers. We must be more scalable. This is a big issue for us.

Across all types, there is an urge to pump more volume through their models. Shortage of people is sometimes the bottleneck. Sometimes it is just shortage of volume.

But new technology and systems are also seen as the way to make progress.

People are in short supply and are very expensive, and yet they are the basis of all service. This conundrum is being wrestled with in different ways by all the firms we spoke to. As one large firm told us: “What we have to do is reduce the people cost and replace this with systems costs.”(see Case Study, below)

Of course the very ‘high touch’Cottage firms dealing with small numbers of very wealthy clients are not trying to industrialise themselves, but even they crave greater efficiency.

4.1 Hunt for Scale ● Nirvana

Comments given in interviews

Case Study Three reasons why systems must be consistent around the world. Firstly for branding purposes so that the same delivery of reports and description of products is available to clients who are increasingly international. The second reason is control. We need to see what the relationship managers are doing. They must tow the line, we want to own the client. And finally, the third reason for consistency is that there must be a consistency between what the relationship managers do, because one bad apple can spoil the brand for everybody. The key is how to balance the need for personal service to clients with the need for achieving a consistent global offering. For Bank xxx industrialisation of private banking means ‘mass customisation’. This is the single biggest issue for the industry. What we have to do is reduce the people cost and replace this with systems costs.

Case Study Three reasons why systems must be consistent around the world. Firstly for branding purposes so that the same delivery of reports and description of products is available to clients who are increasingly international. The second reason is control. We need to see what the relationship managers are doing. They must tow the line, we want to own the client. And finally, the third reason for consistency is that there must be a consistency between what the relationship managers do, because one bad apple can spoil the brand for everybody. The key is how to balance the need for personal service to clients with the need for achieving a consistent global offering. For Bank xxx industrialisation of private banking means ‘mass customisation’. This is the single biggest issue for the industry. What we have to do is reduce the people cost and replace this with systems costs.

17

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

Homes are most obsessed with scaleWe were told about the drive for scale in virtually all the interviews we conducted. The industry is clearly being ‘industrialised’. But it is the Homes who need to see the benefits of most, since they seek client volume in a way that Cottages, in particular, do not.

Homes gave us evidence that they are focused on using technology to try to increase the number of clients per relationship manager, without reducing service levels. Some talked to us about having as many as 300 to 400 clients per relationship manager. Some factories would love to achieve this, but many others are less concerned with measuring scale this way, and say they cannot conceive of having more than 20 or 50 clients per relationship manager before it would harm their service.

400 1

Well, each RM probably looks after about £40-£50m, and that’s probably three to four hundred clients, but it varies.

We once had 10 clients per manager, now its 100, and clients still get great service. Maybe in future we can achieve 200 with technology.

I am amazed at how many clients some private banks have per relationship manager. In our teams of two relationship managers we are aiming to have one billion under management spread across just twenty clients.

If we had one hundred clients per relationship manager, we would be very happy, and in fact we are nowhere near that yet but we are working on it

I think a private banker will never be effective if they are serving more than fifty clients at any time. Obviously technology helps, but it can only help so far.

We have twenty clients, and we have a team of twenty people to do this.

3-400 100 <100 50 7 1

Number of clients per Relationship Manager

In some Banking models you could have 300 clients per relationship manager, but in others you would be limited to 20.

Among Homes the trend is clearly to try to increase this number to 100 and above

Among some Factories and Cottages with very HNW clients, there is less concern with this number

400 1

Well, each RM probably looks after about £40-£50m, and that’s probably three to four hundred clients, but it varies.

We once had 10 clients per manager, now its 100, and clients still get great service. Maybe in future we can achieve 200 with technology.

I am amazed at how many clients some private banks have per relationship manager. In our teams of two relationship managers we are aiming to have one billion under management spread across just twenty clients.

If we had one hundred clients per relationship manager, we would be very happy, and in fact we are nowhere near that yet but we are working on it

I think a private banker will never be effective if they are serving more than fifty clients at any time. Obviously technology helps, but it can only help so far.

We have twenty clients, and we have a team of twenty people to do this.

3-400 100 <100 50 7 1

Number of clients per Relationship Manager

In some Banking models you could have 300 clients per relationship manager, but in others you would be limited to 20.

Among Homes the trend is clearly to try to increase this number to 100 and above

Among some Factories and Cottages with very HNW clients, there is less concern with this number

4.2 Hunt for Scale ● Homes

18

Factories, Homes and CottagesA new look at the architecture of Private Banking in Europe Number 1 • 11/08

We are very grateful to SEI for allowing us to publish these findings

15 Abchurch Lane London EC4N 7BW UK

Telephone +44 (0) 20 7112 2131

www.spencejohnson.com