bsbfia303_certiii_business_master presentation 1

TRANSCRIPT

BSBFIA303PROCESS ACCOUNTS PAYABLE AND RECEIVABLEPRESENTATION 1

PRESENTATION OBJECTIVES

At the end of this presentation you will be able to:

• Maintain financial journals

• Verify and work with sources documents

• Resolve errors in compliance with organisational requirements

• Enter transactions in cash and credit journal system

• Total credit journals

MAINTAINING DAILY RECORDS

The processes of maintaining daily financial records starts with an

organisation’s financial transactions.

Transactions are recorded into source documents, then summarised

into journals.

Journals are then posted to the general ledger, and subsidiary ledgers

- accounts payable and accounts receivable ledger.

Whether you decide to manage your own financial records, or obtain

the services of a professional bookkeeper or accountant, it is

beneficial to have a general knowledge of basic bookkeeping so you

understand where the information comes from and how best you can

use this information.

BOOKKEEPING BASICS TO STARTDouble entry bookkeeping

• Means to record each transaction twice

• The first entry records what comes into the business (a debit), the second entry

records what goes out of the business (a credit)

• Every debit must have a credit of the same value

• Debits display on the left of the line for the transaction and credits on the right

• Each transaction reflects the basic accounting equation:

Assets = liabilities + capital

If each entry is recorded accurately the ‘books of account’ will balance, think of

your books looking like this, one side has to equal the other.Debit Credit

What comes into the business What goes out of the business

Example: Stock (inventory) Example: Account payable (owe money to supplier to pay for stock)

DEBIT AND CREDITTransactions affect two accounts - total debit amounts must equal total credit

amounts. They are one of the most important tools in an accounting system.

In accounting, debits are balanced by credits, which operate in the opposite way.

When a debit is made to one account, a corresponding credit must occur on an

opposing account.

• One account is debited and another is credited

• The amount of debit and credit must be equal

• Transactions affect two accounts

What’s the difference between credit and debit?A credit is an accounting entry that either increases a liability or equity account, or decreases an asset or expense account. It is positioned to the right in an accounting entry. The reverse of a credit is a debit.

A debit is an accounting entry that either increases an asset or expense account, or decreases a liability or equity account. It is positioned to the left in an accounting entry. The reverse of a debit is a credit.

DEBIT DR AND CREDIT CR

What’s the difference between credit and debit?

These rules help you make decisions as to the effect on each account. The rules are very strict, refer to this table at all times.

Example If your bank balance is $300 and you deposit $100(debit), your asset account will increase to $400.

If your bank balance is $300 and you make a payment (credit) for $100, your asset account will decrease to $200.

Asset accountsTo increase an asset account, record amount in debit column

To decrease an asset account, record amount in credit column

Liability accounts

To increase a liability account, record amount in credit column

To decrease a liability account, record amount in debit column

Owner’s equity accounts

To increase an equity account, record amount in credit column

To decrease an equity account, record amount in debit column

Revenue accounts

To increase a revenue account, record amount in credit column

To decrease a revenue account, record amount in debit column

Expense accounts

To increase an expense account, record amount in debit column

To decrease an expense account, record amount in credit column

BOOKKEEPING BASICS TO STARTChart of accounts

• This is a foundation of the double entry bookkeeping system

• Lists all accounts found in the general ledger, and is used to code each

transaction

• The chart of accounts consists of accounts for assets, liabilities, owners’

equity, income and expenses

• Needs to be appropriate to your business

• You will be responsible to work from the chart of accounts allocating

transactions to their relevant accounts

• The chart of accounts is normally broken into accounting groups and

subgroups for reporting and depends on the type of business you operate

and the needs of that business

• See your eBook for an example

BOOKKEEPING BASICSDaily recording involves working with:

• Income and expenses incurred through the operation of the business

• Dealing with debtors and creditors of the business

The customer/supplier relationship is often referred to as the debtor/creditor

relationship within accounting. Monitoring debtors and creditors systems is an

important part of daily financial management process - managing the flow of

money into the organisation with payments from debtors and payments to

creditors.

Debtors

Customers

Accounts

receivable

Money owed to us

Creditors

Suppliers

Accounts

Payable

Money we owe

BOOKKEEPING BASICS

Cash accounting

•Usually for smaller less complicated businesses that often handle cash payments eg: hairdresser•Tracks the actual money coming in and out of your business•Doesn't capture money owed by you or to you•When you send an invoice to a customer, don't record the sale in your books until you receive the money from the customer•Eg: if you send an invoice on Tuesday, and don't receive the payment in your account until Thursday, record the income on Thursday's date•Records involve income and expenses, any wage records

Accrual accounting

•More complicated and better suited for businesses that charge by invoice and don't get paid immediately eg: builders

•The performance and position of a company can be measured by recognising economic events regardless of when cash transactions occur

•Record expenses and sales when they take place, instead of when cash changes hands

•Eg: if you're a builder and send an invoice for a project completed, record the sale in your books even though you haven't received payment yet

•Captures money owed by you or to you so provides an true picture of your financial position

•Records required involve all source documents, journals and ledgers

Accounting for your businessThere are two main methods for accounting for your business. The main choice depends on the size of your business and how complicated your business is.

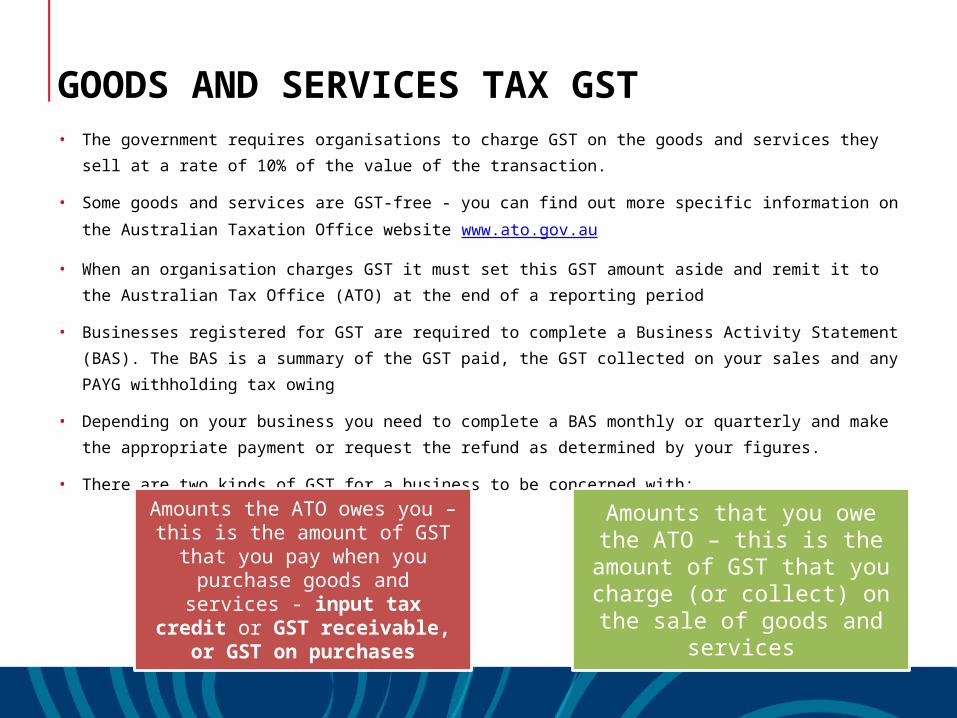

GOODS AND SERVICES TAX GST• The government requires organisations to charge GST on the goods and services they sell at

a rate of 10% of the value of the transaction.

• Some goods and services are GST-free - you can find out more specific information on the

Australian Taxation Office website www.ato.gov.au

• When an organisation charges GST it must set this GST amount aside and remit it to the

Australian Tax Office (ATO) at the end of a reporting period

• Businesses registered for GST are required to complete a Business Activity Statement (BAS).

The BAS is a summary of the GST paid, the GST collected on your sales and any PAYG

withholding tax owing

• Depending on your business you need to complete a BAS monthly or quarterly and make the

appropriate payment or request the refund as determined by your figures.

• There are two kinds of GST for a business to be concerned with:Amounts the ATO owes you – this is the amount of GST that you pay when you purchase goods and services - input

tax credit or GST receivable, or GST on

purchases

Amounts that you owe the ATO – this is the

amount of GST that you charge (or collect) on the

sale of goods and services

MAINTAIN DAILY FINANCIAL RECORDS

• Accounting and financial management activities in an organisation

are mainly based around these areas:

• Financial record keeping is accomplished through tracking financial

events (transactions – eg. expenses and income)

• Your organisation will use a system that suits their size and needs

• Managing daily financial transactions can be done by using

software or manual bookkeeping. Whichever system your business

uses, the following steps make up the flow of information:

Transactions

Journals

Accounts

Ledgers

Financial reports

MAINTAIN DAILY FINANCIAL RECORDS

The early stages of daily financial record keeping involves monitoring

the flow of money in and out.

Daily recording involves working with:

• Income and expenses incurred through the business

• Debtors and creditors of the business

The customer/supplier relationship is often referred to as the

debtor/creditor relationship within accounting and involves managing

the flow of money into the organisation with payments from debtors

and payments to creditors.

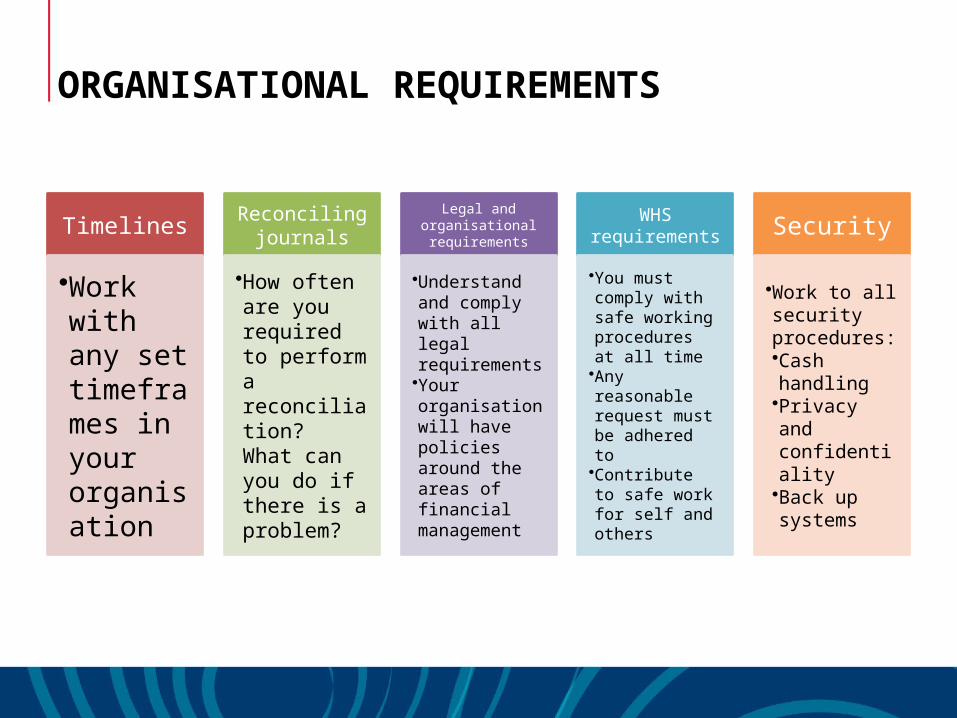

ORGANISATIONAL REQUIREMENTSEach organisation has strict guidelines and requirements for maintaining

their financial records.

Standards are set down for various business activities and legislated by

various government regulations.

Example The (ATO) requires compliance with taxation legislation i.e.

paying GST on time and completing the Business Activity Statement (BAS)

by the due date.

The organisation you work for will have specific requirements for their

operation. They may involve these guidelines, on the following slide:

ORGANISATIONAL REQUIREMENTS

Timelines

•Work with any set timeframes in your organisation

Reconciling journals

•How often are you required to perform a reconciliation? What can you do if there is a problem?

Legal and organisational requirements

•Understand and comply with all legal requirements •Your organisation will have policies around the areas of financial management

WHS requirements

•You must comply with safe working procedures at all time•Any reasonable request must be adhered to •Contribute to safe work for self and others

Security

•Work to all security procedures:•Cash handling•Privacy and confidentiality•Back up systems

VERIFY SOURCE DOCUMENTS

All organisations should make sure transactions are recorded as soon

as possible. The transaction record is referred to as a source

document.

It not only provides evidence of the transaction but contains

important details for accounts payable and receivable records and

allows for accuracy and completeness to be verified.

Common source documents can include:

Receipts / Tax invoices / Invoices / Statements from suppliers

Credit Notes / Adjustment Notes / Cheque butts/

Statements to customers

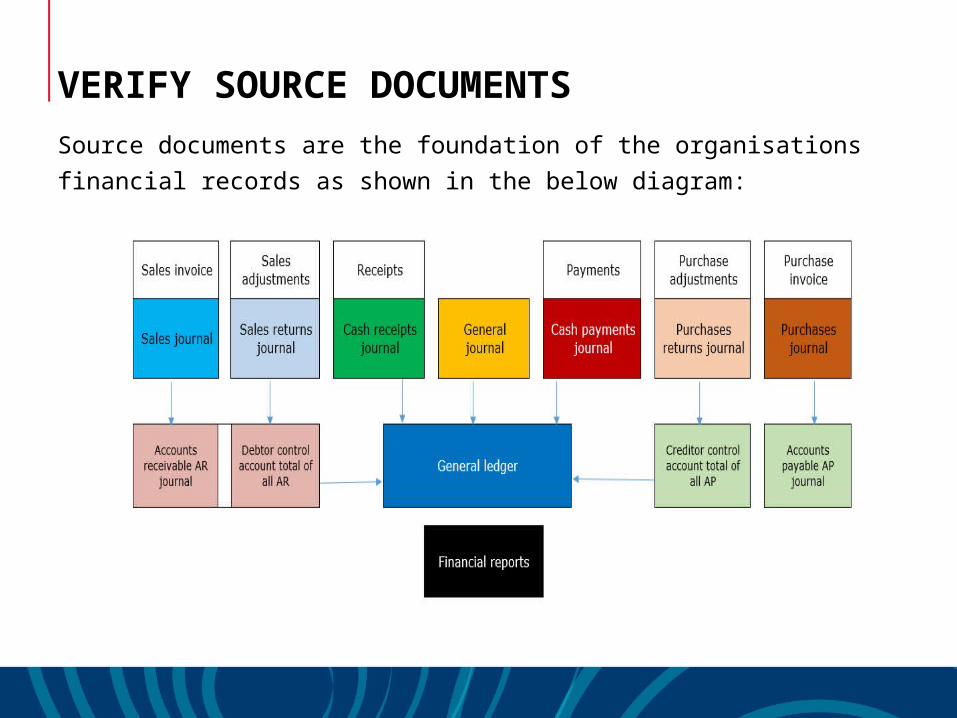

VERIFY SOURCE DOCUMENTS

Source documents are the foundation of the organisations financial

records as shown in the below diagram:

MAINTAIN DAILY RECORDS

Your organisation may require you to perform certain activities within a

certain time, for example:

• Banking

• Reconciliations

• Posting transactions to the general ledger

• Performing trial balance

Why is this important?

Possibility for errors is minimised High standards of accountability

Ease of reporting Books are up to date

DISCREPANCIESAn unintentional error in financial records. Be careful and…

• Always take time and double check when issuing and receiving documents

• Staff will need training and procedures to detect and rectify errors

• More than one person may need to check documents for accuracy check invoices before issuing

• Your business must charge correctly and remain professional

Discrepancies may relate to any account in the business they can involve:

• Invoices entered incorrectly and payments in error

• Invoices in error from suppliers

• Bank charges or direct deposits not deposited to the business ledger yet - a timing error rather than a problem

• Dishonoured cheques or amounts transferred to wrong bank accounts

• Errors between source documents and journals

• Interest expenses and charges

DISCREPANCIESWhen checking invoices look at the following details:

• Does your invoice provide all essential details to meet organisational and legal

requirements?

• Were goods or services actually ordered? Are they accompanying this invoice?

• Are all the calculations are correct?

• Are the terms of invoice correct? Are payment terms in accordance with formal

arrangements in place?

• Has a credit account been established for the customer? Have all necessary credit

checks been completed? Has the customer signed a credit agreement? Credit

arrangements need to be clearly established before any goods or services are

provided

• Has the invoice generated a credit account balance? Or exceeded agreed credit limit

on the customer’s account?

• Invoices should never be validated by the person whom prepared them but rather a

supervisor or manager

HOW SHOULD A DISCREPANCY BE RECTIFIED?

Discrepancies need to be corrected regardless of the stage of the process.

You can identify issues when checking an account, when preparing a trial

balance, reconciling your accounts or at any time.

Consider the following questions:

• What type of discrepancy is it?

• How can it be fixed? Can you do it yourself?

• Do the financial records need to be revised?

After identifying the discrepancies within your organisation’s financial

records, it may be that you need to pass these on to the designated

persons in accordance with organisational requirements.

These people could include:

Line management or supervisor

Organisation’s authorisations department

RESOLVE ERRORS

Organisations must have policies and procedures that outline

creation, authorisation and processing of financial documents

To eliminate errors always check that the information in the source

document is correct such as:

Document title /

numberDate

Organisation information

Australian Business

Number (ABN)

ENTER TRANSACTIONS INTO JOURNALS – DEBIT AND CREDIT

After transactions have occurred they must be entered in the cash

and credit journal system while complying with organisational and

legislative requirements. Journals:

• Record transactions chronologically

• Show debit and credit effects for each transaction

Businesses generally work with the following journals:

• General journal

• Cash receipts journals

• Cash payments journals

• Purchases and purchase returns

• Sales and sales returns

JOURNALS

Cash payments journal

CPJ

Cash receipts journal

CRJ

Sales journalSJ

Purchases journal

PJ

General journalGJ

Daily recording involves working with journals and ledgers. Throughout this

unit we will work on a colour coded system to help you understand how this

works.

• All the journals listed above have coloured templates in your eBook

• Each journal will deal with transactions and debtors and creditors of the

business

.

GENERAL JOURNAL

Business entries Correction of posting errors

Interest expense Interest receivable

The general journal is an important part of the journal keeping system for a business.

It is a place to record transactions which do not fit into any of the other specialised journals. See your eBook for more explanation and examples.

They can include the following transactions:

GENERAL JOURNALExample

We have a situation where we need to adjust an account for a bad debt (a customer

who is not going to pay), one of the reasons for using the general journal to record a

transaction.

This transaction adjusts the amount to be paid out of the account for the creditor

office people (credit) and debits it to the bad debt account, we also need to adjust

GST for this example since the transactions affects GST.

Entries into the general journal may look like this one below, the format and

accounts will vary but the intention is the same regardless of your system:

General journalDate Particulars Account ref Debit Credit BalanceBank (asset)Xx/xx Bad debts

GST on sales

*Creditor Office People

6-2500

2-1100

2-1000

500.00

50.00

550.00

Write off debt from XYZ co. on advice from GM xx/xx

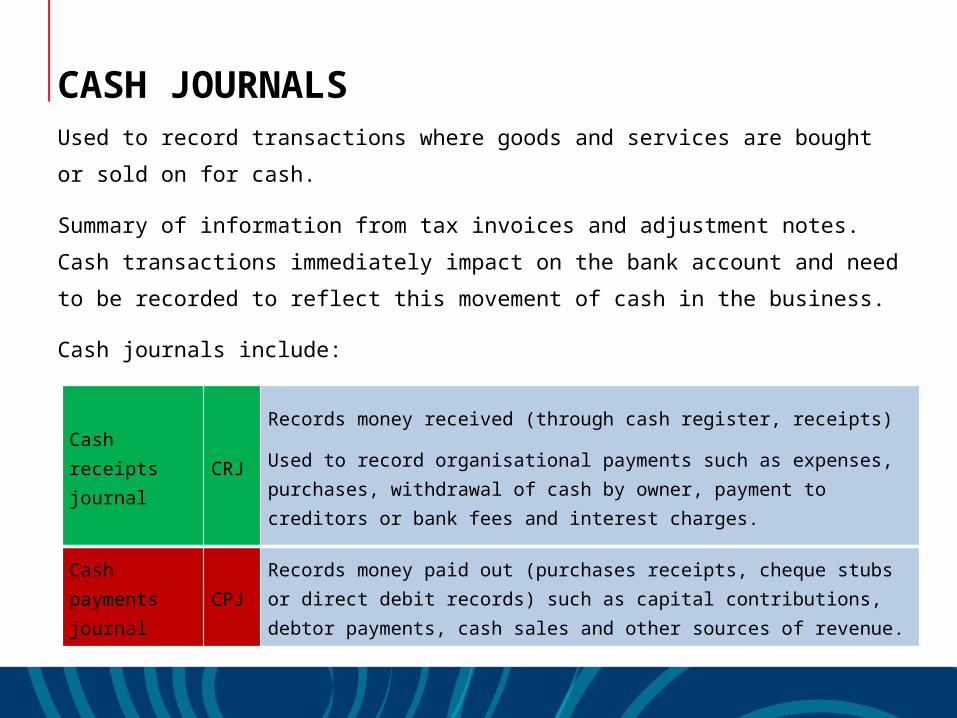

CASH JOURNALS

Cash receipts journal

CRJ

Records money received (through cash register, receipts)

Used to record organisational payments such as expenses, purchases, withdrawal of cash by owner, payment to creditors or bank fees and interest charges.

Cash payments journal

CPJRecords money paid out (purchases receipts, cheque stubs or direct debit records) such as capital contributions, debtor payments, cash sales and other sources of revenue.

Used to record transactions where goods and services are bought or sold on for cash.

Summary of information from tax invoices and adjustment notes. Cash transactions immediately impact on the bank account and need to be recorded to reflect this movement of cash in the business.

Cash journals include:

CREDIT JOURNALS

Used to record transactions where goods and services are bought or

sold on credit.

Summary of information from tax invoices and adjustment notes.

Credit transactions are contracted agreements between buyer and

seller. The buyer will receive goods in exchange for payment at a

time agreed in the contract. Credit journals include:

Sales journal SJ Records sales we have made on credit

Sales returns journal

SRJRecords sales we have made on credit but which were subsequently returned by our customers

Purchases journal

PJ Records purchases we have made on credit

Purchases returns journal

PRJRecords purchases we have made on credit but which were subsequently returned to our suppliers

TOTAL CREDIT JOURNALS

• When should you total your journals? This depends on your

organisation and their needs and expectations for you

• Totalling the journals is a way to verify and crosscheck details that

have been entered are correct

• When performing this task, keep in mind the ‘accounting equation’

and the standards of double-entry accounting

• Double-checking at this level can reduce frustrations when errors

are found further down the process

• A good practice is getting someone else to check information

TOTAL CREDIT JOURNALSWhen totalling journals, ensure organisational, legislative and

compliance requirements are met:Consumer• Privacy / Secrecy laws• Australian Consumer Credit Code• Codes of practice and ethical principles• Anti-discrimination legislation

Competition• Australian Competition and Consumer Commission• National Competition Policy

Prudential• Corporate Law• Credit Reference Association of Australia• Electronic Funds Transfer Code of Conduct• Financial Institutions Code• Commonwealth Bills of Exchange Act, Cheque and Payment Orders Act,

Financial Transaction Reports Act, Land Tax Assessment Act

PRESENTATION OBJECTIVES

Now that you have completed this presentation, you will be able to:

• Maintain financial journal systems

• Verify source documents

• Resolve errors in compliance with organisational requirements

• Enter transactions in cash and credit journal system

• Total credit journals