budget 2009 niki todd bertram todd no 5 oxford house oxford road wokingham berks rg41 2ye 0118...

Post on 20-Dec-2015

214 views

TRANSCRIPT

Budget 2009

Niki ToddBertram Todd

No 5 Oxford HouseOxford RoadWokingham

Berks RG41 2YE

0118 9770944 E - mail : [email protected]

Budget 2009

• This was the second time the Budget was delivered so late in its history.

• The first time was exactly 100 years ago on the 29th of April 1909 and the then chancellor of the exchequer was Lloyd George.

Budget 2009

• Lloyd George, called it “ the most significant politically ever”! His speech funnily enough started with “ No Chancellor of the Exchequer has ever had to raise so much money”! This referring to a Budget Deficit of £714K , in today's money £54 million. The money was needed to finance the commencement of old age pensions and he intended to raise it by taxing the property owners.

• Compare this to Darling’s deficit of £170 Billion!

Budget 2009

• Lloyd Georges Budget was blocked by the House of Lords who objected to the increased taxation being levied primarily at them.

• This, in turn, led directly to the Parliament Act of 1911 by which the Lords lost their power of veto.

Budget 2009

• Disclaimer• The information on this presentation is based

on the Budget Notes, Press Notices and the HM Treasury Budget Report all issued on 22 April 2009.

• The final version of most of the measures will only be known once the Finance Bill has been enacted in the Summer.

Budget 2009

• General• Personal• Business• Employees• Capital• Tax Administration• Comment

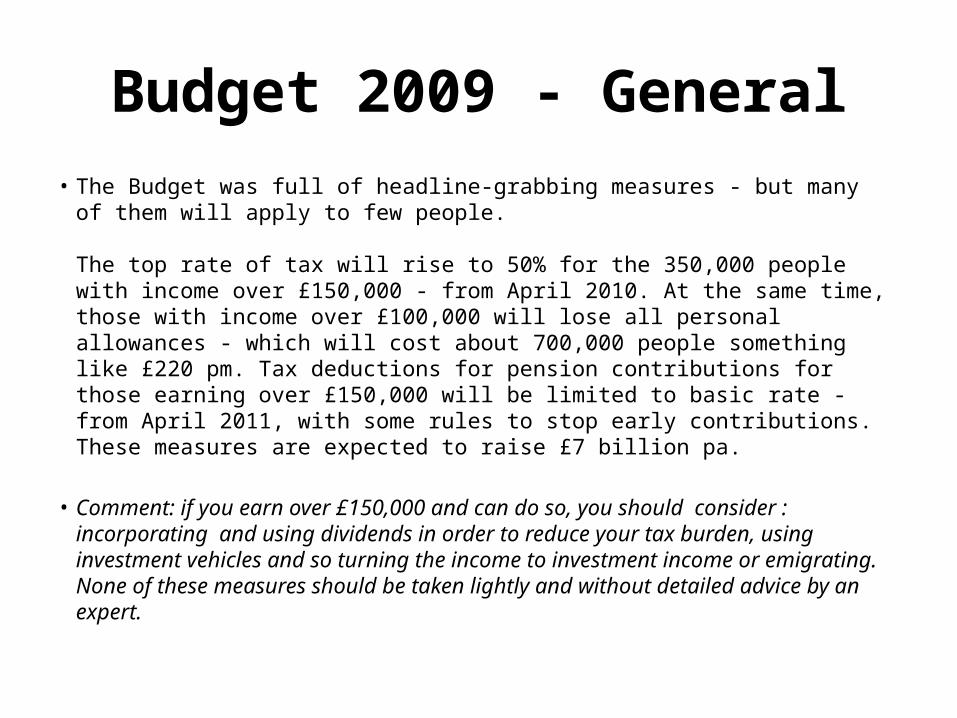

Budget 2009 - General• The Budget was full of headline-grabbing measures - but many of them will apply

to few people.

The top rate of tax will rise to 50% for the 350,000 people with income over £150,000 - from April 2010. At the same time, those with income over £100,000 will lose all personal allowances - which will cost about 700,000 people something like £220 pm. Tax deductions for pension contributions for those earning over £150,000 will be limited to basic rate - from April 2011, with some rules to stop early contributions. These measures are expected to raise £7 billion pa.

• Comment: if you earn over £150,000 and can do so, you should consider : incorporating and using dividends in order to reduce your tax burden, using investment vehicles and so turning the income to investment income or emigrating. None of these measures should be taken lightly and without detailed advice by an expert.

Budget 2009 - General

• From 2011/12 we will also see the 0.5p National Insurance Contribution (NICs) increases for high earners (as previously announced) representing an overall tax/NIC increase of 10.5p in the pound for a higher earner.

Budget 2009

• Personal

Budget 2009 – 2009/ 10 Changes

• Personal allowance up to £6,475

• 10% band ( savings income only)Up to £2440

• Basic rate band Up to £37400A taxpayer with income of £50000 would

save £696 or more compared to 2008/09 depending on whether his income is earned or savings income.

Budget 2009 – Personal Allowance 2010/11

• Personal Allowance to be withdrawn if “Net Adjusted Income” above £100,000.

• Reduce Allowance by £1 for every £2 of NAI• At 2009/10 rate would loose PA at £112,950.

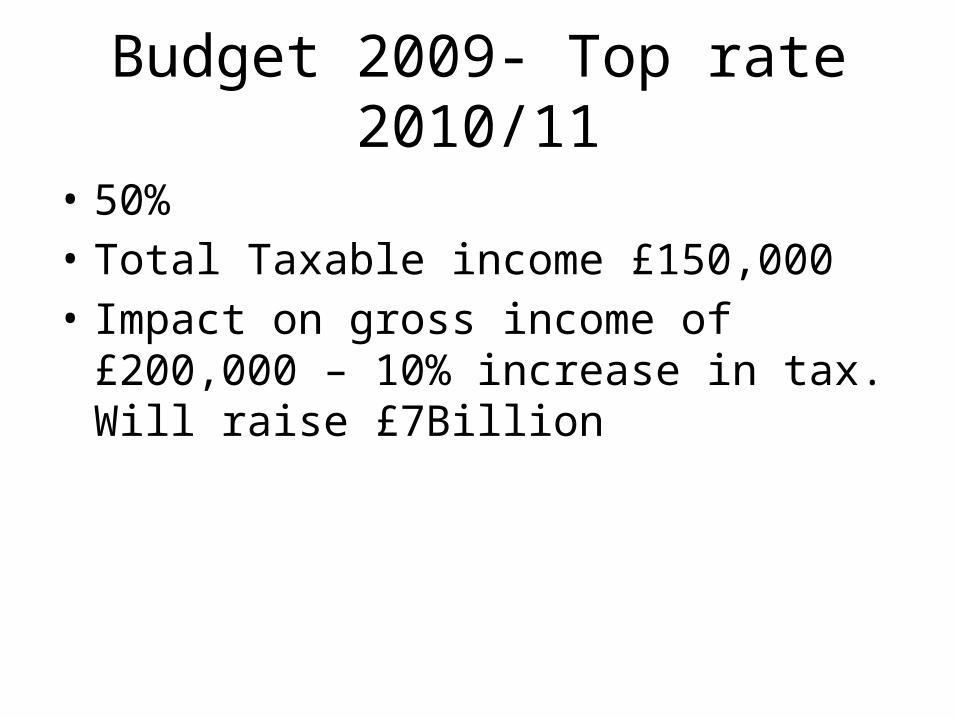

Budget 2009- Top rate 2010/11

• 50%• Total Taxable income £150,000• Impact on gross income of £200,000 – 10%

increase in tax. Will raise £7Billion

Budget 2009 – Dividend Income 2010/11

• Basic dividend rate 10%

• Upper Dividend rate32.5%

• Additional dividend rate42.5%

Budget 2009 – Trust income tax 2010/11

• Trust rate50%

on all income• Trust Dividend rate

42.5%• No de minimis limit

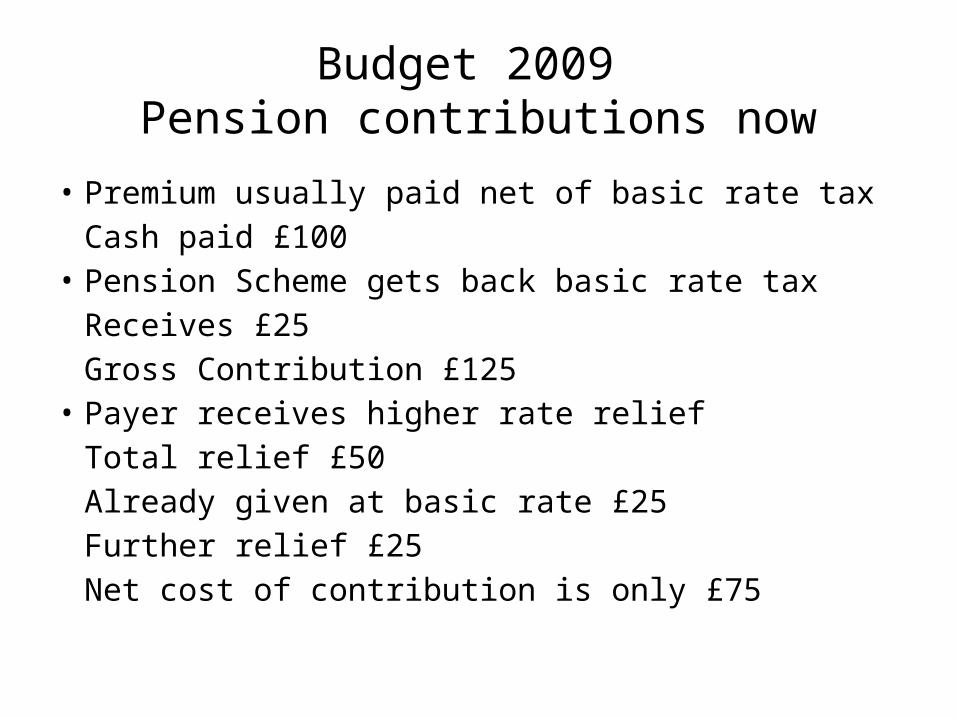

Budget 2009 Pension contributions now

• Premium usually paid net of basic rate tax Cash paid £100

• Pension Scheme gets back basic rate tax Receives £25Gross Contribution £125

• Payer receives higher rate reliefTotal relief £50Already given at basic rate £25Further relief £25Net cost of contribution is only £75

Budget 2009 Pension contributions 20011/12

• Higher rate relief removed• Taxable income £150,000 +• Removal tapered• All higher rate relief removed at £180,000

Budget 2009Impact

• Gross income £200,000• Net pension contributions £20,000• Tax payable• 2009/10 - £64,930• 2010/11 - £72,520• 2011/12 – £77,520• Various forestalling provisions to prevent

taxpayers from taking advantage of period 22 April 2009 to 6 April 2011.

Budget 2009ISAs

• Current limits £7,200Cash max £3,600

• From 6 October 2009Individuals aged 50 and overMax £10,200Cash element £5,100

• New limits available to all from 6 April 2010

Budget 2009Personal Dividends

• Dividends from non- UK companies • Non – payable tax credit 10%• Currently available where shareholding < 10%• From 22 April 2009 available irrespective of

shareholdingcompany must be in a country with

which UK has a DTA with non discrimination article

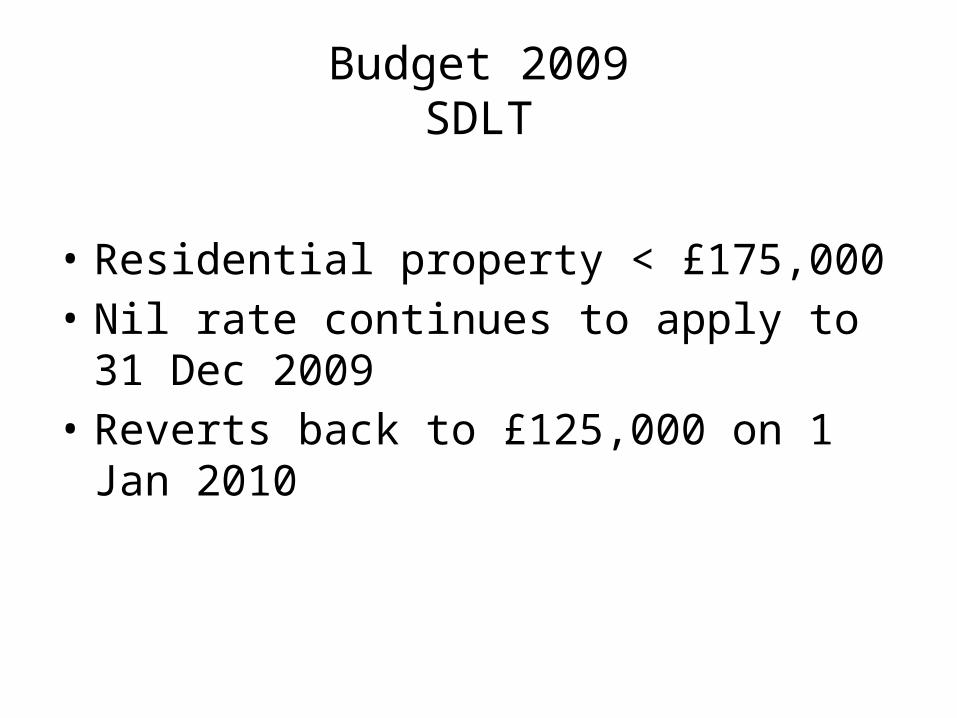

Budget 2009SDLT

• Residential property < £175,000• Nil rate continues to apply to 31 Dec 2009• Reverts back to £125,000 on 1 Jan 2010

Budget 2009Child Trust Fund

• Eligible children born on or after 22 Sep 2002• Government will make additional contributions

£100 pa for disabled children£200 pa for severely disabled

children• Does not affect annual contribution limit of

£1,200

Budget 2009car scrappage scheme

• £2,000 discount on purchase of new vehicle• Old car must be over 10 years old• Current owner must have had it for 1 year• Scheme will run to 31 March 2010

Budget 2009 - General

Personal Tax and Individuals Tax Rates and AllowancesThe Chancellor, has announced the following changes to tax rates and allowances for taxpayers with income over £100,000: from 2010-11, there will be an additional higher rate of 50 per cent for taxable income above £150,000;from 2010-11 the basic personal allowance for income tax will be gradually reduced to nil for individuals with “adjusted net incomes” above £100,000; from 2010-11 there will be increases to the trust rate and dividend trust rate to match those for income tax; andthe measure includes new powers to vary the income tax rates for the charges that apply to registered pension schemes.These changes replace the announcements made at the 2008 Pre-Budget Report. The reduction of personal allowances affects those with incomes over £100,000 and the new tax rate affects those with incomes over £150,000.

Budget 2009

• Personal• Business

Budget 2009 CT rates

• Small companies rate stays at 21% for 2009• Main rate 28%

will also apply for 2010

Budget 2009Company trading losses

• Current positioncarry forwardset against other company income in same

AP Carry back against profits in previous 12

monthscarry back terminal losses 3 years

• Proposals for additional carry back extended

Budget 2009Company loss relief

• AP ending between 24 Nov 2008 and 23 Nov 2010• Trading loss incurred• Extended carry back

One year no limitTwo further years limit ( combined)

£25,000Conditions apply

• Not quite as generous as 1991

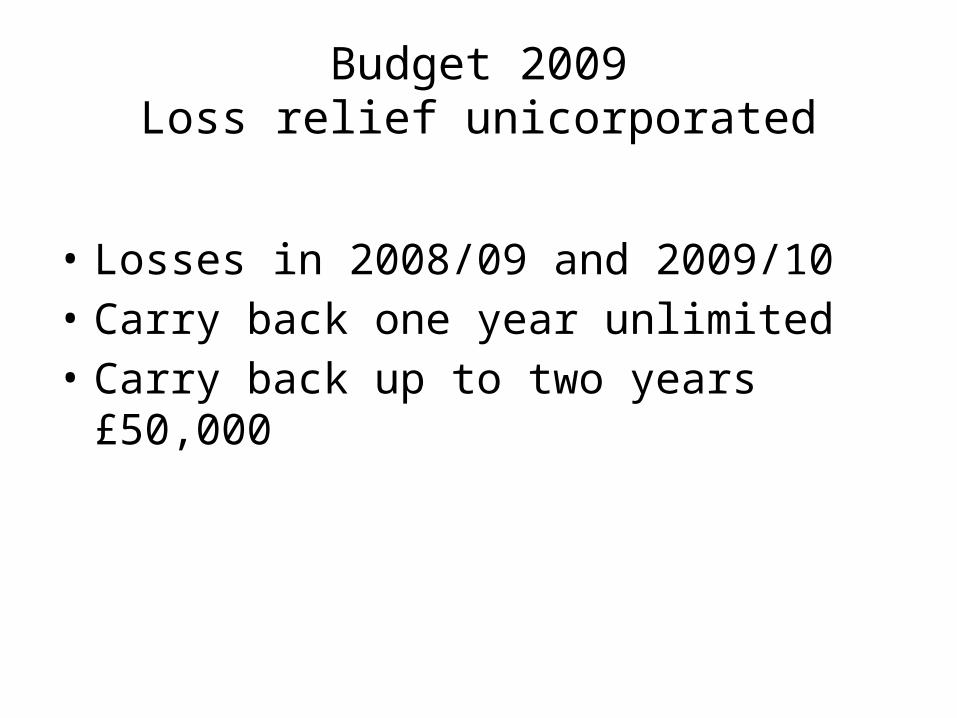

Budget 2009Loss relief unicorporated

• Losses in 2008/09 and 2009/10• Carry back one year unlimited• Carry back up to two years £50,000

Budget 2009Temporary First year allowances

• Remember Annual investment allowance £50,000 pa max

• Extra allowance of 40% on unlimited additional expenditure for main pool expenditure( not cars or assets for leasing)

Budget 2009Motor cycles

• No longer treated as cars• Qualify for AIA post April 2009

So if you fancy a Harley this is your chance and with the chancellors blessings!

Budget 2009Furnished Holiday lettings

• Currently special rules apply which the letting must meet.

• Benefit of this losses are treated as trade lossesCapital allowances are availableEntrepreneurs reliefRoll over relief

• Earnings considered as relevant earnings for pension

Budget 2009Good News

• Provisions to be extended to any qualifying property in EEA

• Can go back and pick up benefit of reliefs• HMRC will accept claims subject to normal

time limits

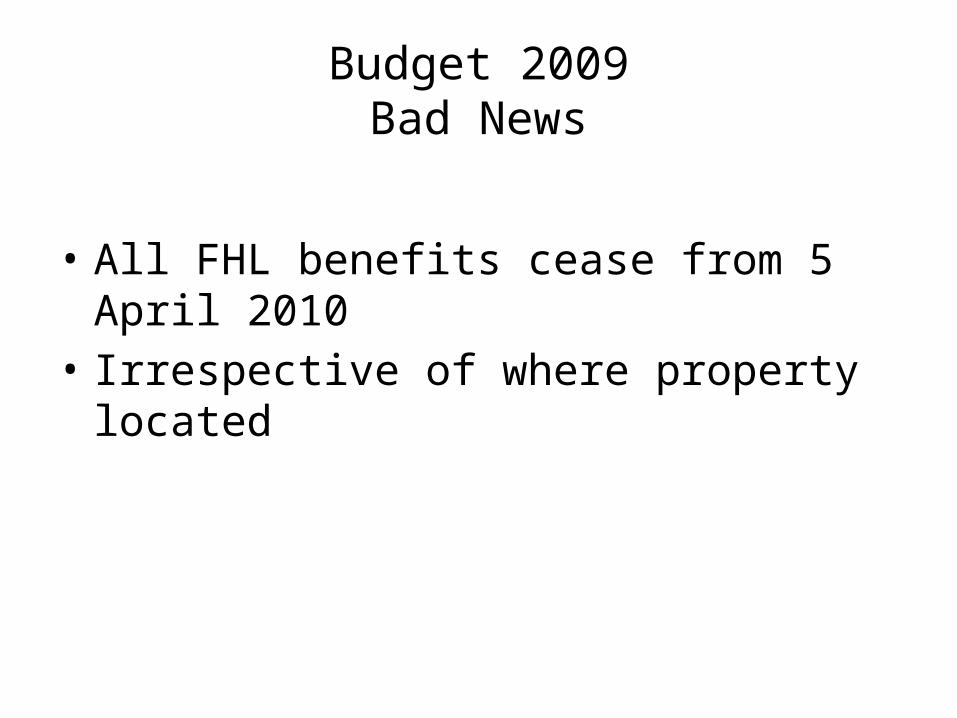

Budget 2009Bad News

• All FHL benefits cease from 5 April 2010• Irrespective of where property located

Budget 2009VAT

• Registration limits from 1 May 2009– Registration £ 68,000– De – registration £ 67,000

Vat rate15% until 31 Dec 200917.5 % on 1 Jan 2010

Good news : Reduced rate to apply to child car seat bases

Budget 2009

• Personal• Business• Employees

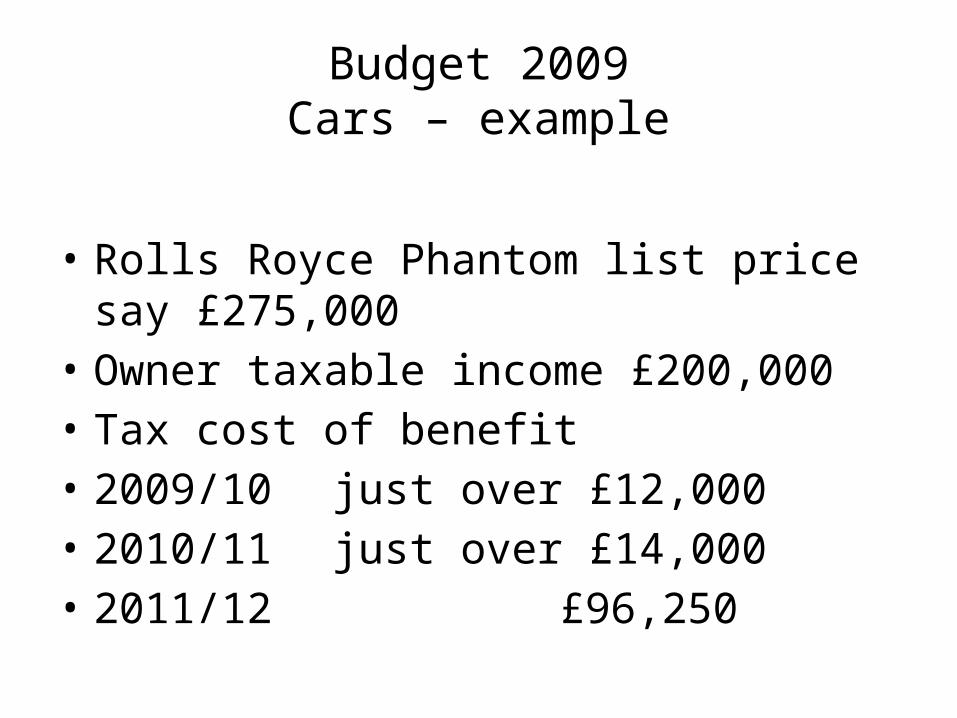

Budget 2009Car benefits from 2011

• Lower threshold drops to 125 gms/km• Reduction for hybrids and bi –fuel cars to be

abolished• Removal of £80,000 list price limit

Budget 2009Cars – example

• Rolls Royce Phantom list price say £275,000• Owner taxable income £200,000• Tax cost of benefit• 2009/10 just over £12,000• 2010/11 just over £14,000• 2011/12 £96,250

Budget 2009

• Personal• Business• Employees• Capital

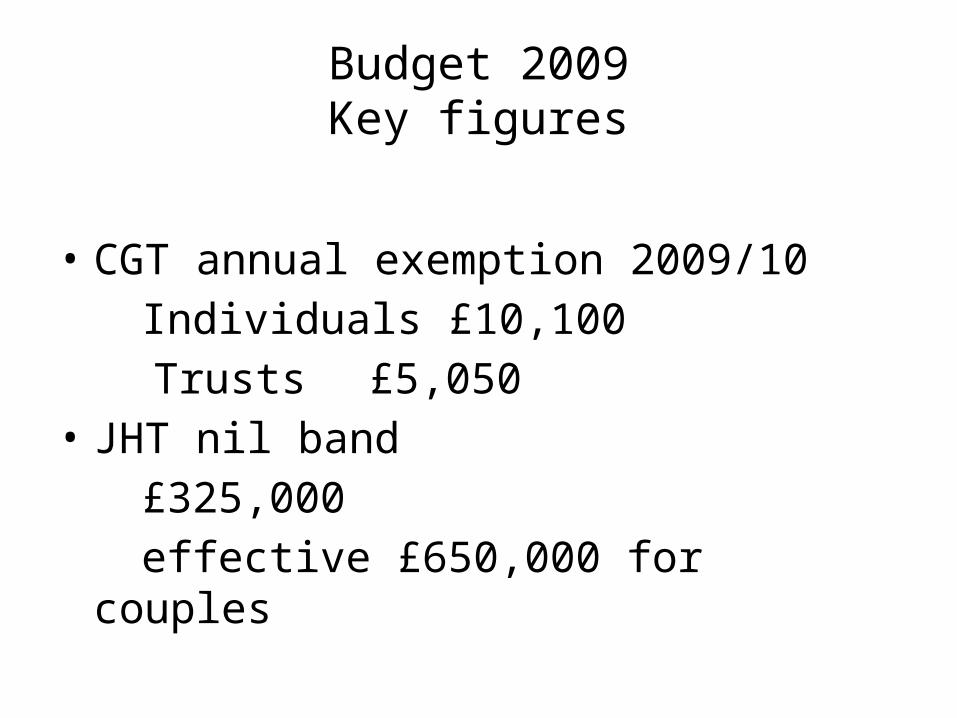

Budget 2009Key figures

• CGT annual exemption 2009/10Individuals £10,100

Trusts £5,050• JHT nil band

£325,000effective £650,000 for couples

Budget 2009

• Personal• Business• Employees• Capital• Administration

Budget 2009Changes to HMRC powers

• Revised penalties • New power to obtain information• New power to inspect business premises• New penalty structure for late filing and payment

from 1 April 2010• Interest harmonisation, but not of interest

charged and paid.• Tax defaulters to be named publically

Budget 2009 - General • Taxation of foreign dividends

The non-payable tax credit on dividends from foreign companies will be extended to certain large shareholdings in foreign companies.

• Furnished holiday lettingsFrom 2010/11 losses from furnished holiday accommodation will not be able to be set against other personal income. In the meantime it will be possible to set losses from furnished holiday accommodation situated in the European Economic Area against other personal income.

• Taxback on interestThere will be a new campaign to help low income pensioners claim any tax back which they have incorrectly paid.

• Cash ISA limitFrom 2009/10 the ISA limits for people aged 50 and over will be raised to £10,200, of which £5,100 can be held in cash. The ISA limits will be raised for all investors by the same amount from 6 April 2010.

Budget 2009- General• Tax Relief on Pension Contributions• The Chancellor has announced that, starting in 2011-12, tax relief on pension

contributions will be restricted to basic rate for individuals with an annual income of £150,000 or higher.

• Comment: It is worth remembering that this the minister who presided over the original reduction of all our pensions via the abolition of the tax credits in dividends which at that point represented a quarter of the annual income of most pension scheme. One wonders if re - elected what else he is hiding in his bag of goodies.

• In anticipation of this change, there will be special rules which will apply from Budget Day (22 April 2009) to prevent people from making large additional contributions to their pensions before then in order to benefit from higher rates of tax relief while it is still available.

• These changes do not affect the vast majority of individuals. They affect only those who have a total annual income of £150,000 or higher in the current tax year or in either of the preceding two tax years. More information is in Budget Note 47 and in the guidance notes.

Budget 2009 - General

• Business Payment Support Service• The Business Payment Support Service announced at

the Pre Budget Report in November 2008 is now being extended for those businesses which are genuinely unable to pay their outstanding liability immediately or enter into a reasonable time to pay arrangement.

• Where a viable business is due to pay tax on the previous year’s business profits and is likely to make a trading loss in the current year, those losses can be taken into account when agreeing the level of payments to be made.

Budget 2009

• Corporation Tax RatesThe main rate for Financial Year (FY) 2010 will be 28 per cent (unchanged from FY 2009). The small companies rate for FY 2009 will be 21 per cent. Details are in Budget Note 2 and Budget Note 3.

Budget 2009

• Capital Allowances - First Year AllowanceThe Chancellor has announced a new temporary 40 per cent first-year allowance (FYA) for expenditure on general plant and machinery will apply to qualifying spending incurred in the 12 month period beginning on 1 April 2009 for corporation tax, and on 6 April 2009 for income tax.

Budget 2009 - General• Compliance Proposals • Offshore Disclosure

The Chancellor has announced a New Disclosure Opportunity for UK residents with unpaid tax connected to an offshore account. The NDO will run from the autumn 2009 for a limited period to give the offshore account holders one final opportunity to disclose, and put their affairs in order. Customers taking up this opportunity will be expected to pay the duties they owe, interest and a penalty. The level of penalty will be publicised before the scheme opens and for those eligible to take part it is likely to be lower than the level they can expect to pay under normal rulers.

• Tax avoidance disclosure regime hallmarks These are to be revised and extended.

• Tax agent consultationThere will be consultation on working with tax agents, as part of HMRC’s work to modernise its powers, deterrents and the accompanying safeguards. The consultation focuses on the small number within the tax agent community whose work falls below a professional standard. The aim of this consultation is to raise issues and ask questions rather than propose definite solutions.

• Close monitoring of serious tax defaultersThe Chancellor has announced that those who incur a penalty for deliberate evasion in respect of tax of £5,000 or more will be required to submit returns for up to the following 5 years showing more detailed business accounts information and detailing the nature and value of any balancing adjustments within the accounts.

• Publishing names of serious tax defaulters on HMRC InternetThe Chancellor has announced that the names and details of serious tax defaulters will be published in certain circumstances. More information is available in Budget Note 63

• Avoidance of living accommodation benefit chargeThis measure ensures that all employees pay the correct tax and national insurance where a new lease is entered into for living accommodation provided by reason of their employment. More information is available in Budget Note 56.

Budget 2009 - General• Review of Powers • Further changes are announced to modernise HMRC`s tax administration, including;• Simplifying and harmonising interest charged and paid, and aligning late filing /late payment penalties

The Chancellor has announced reform of the penalty regimes for late filing of tax returns and late payment of tax and to create a harmonised interest regime for the first time for all taxes and duties administered by HMRC with the exception of CT and PRT. More information are in Budget Note 90 and Budget Note 91.

• Launching a new Taxpayer Charter later in the yearLegislation will be introduced requiring HMRC to prepare and maintain a Charter. The Charter will set out standards of behaviour and values to which HMRC will aspire in dealing with taxpayers and others. More information is in Budget Note 92.

• Instalment schemes to help plan for future tax billsInstalment schemes will be available for individuals and companies who wish to spread their tax payments over time and who have met their obligations to pay what they owe on time. More information is in Budget Note 88.

• Applying taxpayer safeguards to all taxes where compliance checks are madeThis measure applies the new compliance checking framework to a number of taxes. It covers new, aligned, information and inspection powers, record-keeping rules and time limits for assessments and claims. More information is in Budget Note 89.

Budget 2009 - General• VAT Changes • VAT changes to modernise cross border trading will be introduced over a

3 year period from 1 January 2010 and will include;• Changes to the place of supply rules for cross border supplies of services.

More information is in Budget Note 74 and Budget Note 75. • Completion of quarterly EC Sales Lists. More information is in

Budget Note 76.• A new electronic VAT refund procedure for cross border supplies of

services. More information is in Budget Note 77. • The temporary rate of 15 per cent will cease on 31 December 2009, and

the standard rate of VAT will return to 17.5 per cent from 1 January 2010. Legislation will be introduced to counter schemes which purport to apply the temporary rate after 31 December 2009. More information is in Budget Note 71 and Budget Note 72.

Budget 2009 - General

• Excise Duties • Alcohol duty

Is increased by 2 per cent from 23rd April. • Tobacco duty

Is increased by 2 per cent from 6:00pm 22 April.

• Fuel dutyIs increased by 2 pence per litre from 1 September 2009.

Budget 2009 - General

• Stamp Duty Land Tax• The Chancellor announced an extended “holiday”

from stamp duty land tax (SDLT) which exempts any acquisitions of residential property of not more than £175,000. The holiday now applies to acquisitions between 3 September 2008 and 31 December 2009 inclusive.

• After that date the SDLT threshold for residential property will revert to £125,000. More information is in Budget Note 45.

Budget 2009 – Comment

• The budget and entrepreneurial business:• Entrepreneurial businesses will have been left slightly deflated by this Budget. The announcement of an

increase in the top rate of tax to 50% may dissuade entrepreneurs from basing themselves in the UK as it will make it much more costly to extract cash from the business.

It may also make it harder for serial entrepreneurs to start up new businesses. The funding for such enterprises may typically come by extracting funds from an existing successful venture.

The obvious method to do so from a tax perspective now would be to plan to ensure value is realised as a capital gain (the rate remains at 18%). But as very few deals are being done in the current environment this might be difficult. This raises the question whether the entrepreneur would be willing to take out money (and suffer rates in excess of 50%) to invest in new ventures?

Further, whilst there was an extension of the three year loss carry back scheme (to incorporate periods ending up to 23 November 2010), this is still capped at £50,000 of unused losses meaning the refund is likely to be quite small. This doesn’t go nearly as far as the loss carry back scheme announced during the 1991 recession which allowed for unlimited losses to be carried back against profits from previous years.

Budget 2009•

Business reliefs are modest. The £50,000 loss relief rule will be extended for a second year - allowing loss-making businesses to recover tax paid in the three previous years. However, the refund for a company is only £10,000 - so not a huge help. No further help for empty properties, though. There's an increase in Capital allowances for expenditure in the year to April 2010. However, the NPV is very small, so won't encourage extra investment.

The much heralded scrappage scheme will offer £2,000 to those who buy a new car; however, much of this money will end up financing cars manufactured overseas.

There are important new powers in relation to tax evasion and tax reporting. There will be a defaulters list, so that those who deliberately evade tax of £25,000 will be named. Finance directors will need to take personal responsibility for company tax filings.

Finally, the Foreign Profits measures will come in this year. The dividend exemption will apply from 1 July 2009 but the tax-raising interest restrictions will apply only from accounting periods starting on or after 1 January 2010 - a welcome delay.

Budget 2009- Comment• Although the £50,000 carry-back is nice, it's only worth around £10,000 in cash

tax for most, and so isn't nearly enough to make a difference. Many had hoped to see the amount of loss available for 3 year carry-back being increased, but will be disappointed.

The Chancellor also announced the doubling of tax allowances for capital assets to 40% for the current tax year. This will be of absolutely no benefit to those making losses, and worth very little to the profitable because the net present value increase is modest.

On the plus side, the Chancellor confirmed the Business Payment Support scheme will be extended. 100,000 taxpayers in financial difficulties, including many private business owners, have deferred £1.8 billion across all the taxes, and the extension beyond the current six month limit is welcomed.

Budget 2009 - CommentOverall this was a disappointing Budget for property

The extension of the stamp duty exemption will be welcome to first-time buyers, although it’s only for an extra 4 months. However, in an era where lenders want sizeable deposits from buyers, the stamp duty saving of up to £1,750 is important. Every little helps.

The value of the exemption depends on which part of the country buyers are looking. Land Registry figures show that the average house price is less than £175,000 in all parts of England & Wales - apart from the South East (£190,000) and London itself (£298,000).

The proposed REIT rules will make it easier for tenanted pub groups to become REITs, but will make it impossible for the managed pub sector.

Tenanted pub groups should be fine as their pubs are let on third party leases managed pubs are a different story.

“Otherwise this has been a disappointing Budget for property.

“The Government had an opportunity to do things for cash strapped REITs that would have cost very little. The REIT rules were conceived in a property boom and are not necessarily appropriate in a crash.

“They’ve also missed a trick for the residential sector. They should have done more to encourage institutional investment in residential property, which would have helped kick-start the house-building industry. They should also have seized the opportunity to improve the REIT rules to facilitate residential REITs.

“The changes to Empty Property Rate Relief were hatched in early 2007 when he had a booming economy. But they took effect last April when the property industry and businesses in general were on their knees. It’s a shame that Government hasn’t been able to do anything more.”

Budget 2009 – Comment • The announcement of a UK ‘scrappage’ scheme is a boost to the UK automotive industry.

This could jump-start new car sales which are at their lowest level for over a decade. Similar schemes have proved successful in both France and Germany. New car sales in Germany rose by 40 percent in March, bolstered partly due to the €2,500 subsidy for people who turn in their old car and buy a new one. Based on this evidence it would seem that a similar scheme could also have a beneficial affect in the UK and get car sales rising again.

It should also give automotive manufacturers greater confidence to increase production levels after the scaling back of production and reduction of working hours seen at plants right across the country.

Some have argued that such a scheme would have a limited impact in terms of boosting the UK economy since over 80% of cars sold here are manufactured overseas. However, this is to overlook the many automotive component manufacturers which make components for overseas manufacturers which will be buoyed by this news. It also forgets that over 500,000 people are employed in the UK automotive industry and any move to add greater confidence to consumers buying in this sector should be good news.”

Budget 200 – appendix 1

• Allowances 2009/10 2009/10 Change 2008/09 £ £ £

Personal allowance (age under 65) 6,475 440 6,035 Personal allowance (age 65-74) 9,490 460 9,030 Personal allowance (age 75 and over) 9,640 460 9,180 Married Couple’s allowance* 6,865 330 6,535 (age less than 75 and born before 6 April 1935) Married Couple’s allowance* (age 75 and over) 6,965 340 6,625 Married Couple’s allowance* - minimum amount 2,670 130 2,540 Income limit for age-related allowances 22,900 1,100 21,800 * Married Couple’s allowance is given at rate of 10%

The basic and higher income tax rates remain at 20% and 40% for 2009/10 and 2010/11. From 6 April 2010 the personal allowance will be restricted to half its value for those with incomes over £100,000 and to zero for those with incomes over £140,000. From 6 April 2011 incomes above £150,000 will be subject to a new 45% income tax rate.

Budget 2009 – appendix 2

Pensions 2009/10 Change

2008/09 £ £ £

Annual allowance 245,000 10,000 235,000 Lifetime allowance 1,750,000 100,000 1,650,000

Budget 2009 – appendix 3National Insurance Contributions

2009/10 Change 2008/09 £ £ £

Primary Class 1 contributions Lower earnings limit (per week) 95 5 90 Upper earnings limit (per week) 844 74 770 Primary threshold (per week) 110 5 105 Secondary threshold (per week) 110 5 105 Class 2 annual small earnings exception 5,075 250 4,825 Class 2 rate (per week) 2.40 0.10 2.30 Class 3 voluntary contribution rate (per week) 12.05 3.95 8.10

Class 4 contributions Lower annual earnings limit 5,715 280 5,435 Upper annual earnings limit 43,875 3,835 40,040

Budget 2009 – appendix 4

From 6 April 2011 a 0.5% increase in employer, employee and self-employed rates of national insurance contributions (both main and additional rates) will be introduced. At the same time the point at which individuals start to pay National Insurance will be aligned with the personal allowance.