budget policies

DESCRIPTION

Budget 2014/15 - 2016/17TRANSCRIPT

!"## $!"!%$ &

TABLE OF CONTENTS

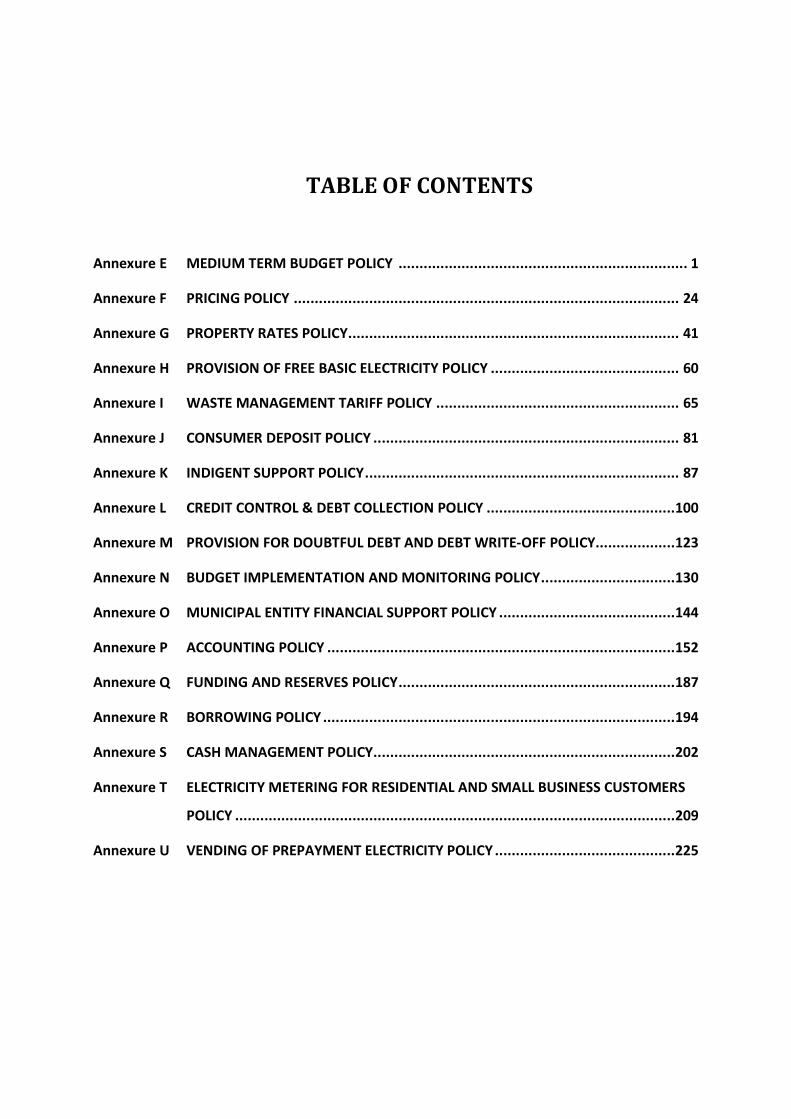

Annexure E MEDIUM TERM BUDGET POLICY ..................................................................... 1

Annexure F PRICING POLICY ............................................................................................ 24

Annexure G PROPERTY RATES POLICY............................................................................... 41

Annexure H PROVISION OF FREE BASIC ELECTRICITY POLICY ............................................. 60

Annexure I WASTE MANAGEMENT TARIFF POLICY .......................................................... 65

Annexure J CONSUMER DEPOSIT POLICY ......................................................................... 81

Annexure K INDIGENT SUPPORT POLICY........................................................................... 87

Annexure L CREDIT CONTROL & DEBT COLLECTION POLICY .............................................100

Annexure M PROVISION FOR DOUBTFUL DEBT AND DEBT WRITE-OFF POLICY...................123

Annexure N BUDGET IMPLEMENTATION AND MONITORING POLICY................................130

Annexure O MUNICIPAL ENTITY FINANCIAL SUPPORT POLICY ..........................................144

Annexure P ACCOUNTING POLICY ...................................................................................152

Annexure Q FUNDING AND RESERVES POLICY..................................................................187

Annexure R BORROWING POLICY ....................................................................................194

Annexure S CASH MANAGEMENT POLICY........................................................................202

Annexure T ELECTRICITY METERING FOR RESIDENTIAL AND SMALL BUSINESS CUSTOMERS

POLICY .........................................................................................................209

Annexure U VENDING OF PREPAYMENT ELECTRICITY POLICY ...........................................225

Annexure E

EKURHULENI METROPOLITANMUNICIPALITY

MEDIUM TERMBUDGET POLICY

2014/152014/15

1

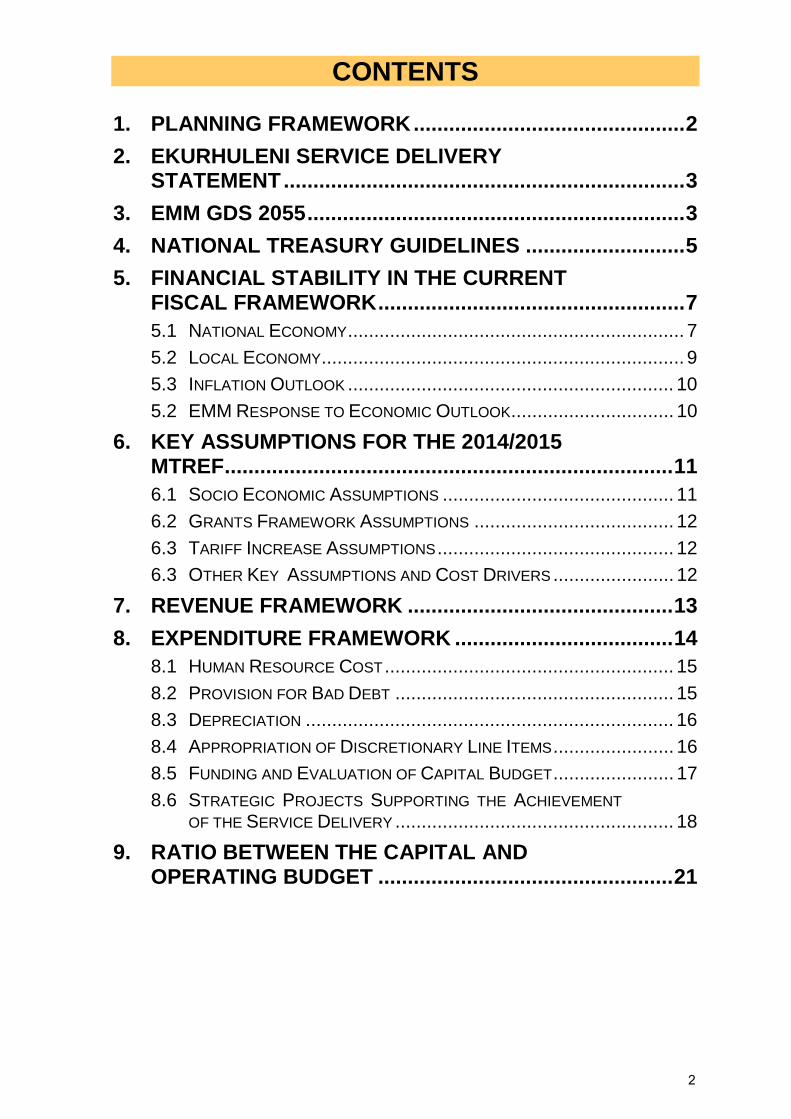

CONTENTS

1. PLANNING FRAMEWORK..............................................2

2. EKURHULENI SERVICE DELIVERYSTATEMENT....................................................................3

3. EMM GDS 2055................................................................3

4. NATIONAL TREASURY GUIDELINES ...........................5

5. FINANCIAL STABILITY IN THE CURRENTFISCAL FRAMEWORK....................................................7

5.1 NATIONAL ECONOMY................................................................ 7

5.2 LOCAL ECONOMY..................................................................... 9

5.3 INFLATION OUTLOOK .............................................................. 10

5.2 EMM RESPONSE TO ECONOMIC OUTLOOK............................... 10

6. KEY ASSUMPTIONS FOR THE 2014/2015MTREF............................................................................11

6.1 SOCIO ECONOMIC ASSUMPTIONS ............................................ 11

6.2 GRANTS FRAMEWORK ASSUMPTIONS ...................................... 12

6.3 TARIFF INCREASE ASSUMPTIONS ............................................. 12

6.3 OTHER KEY ASSUMPTIONS AND COST DRIVERS ....................... 12

7. REVENUE FRAMEWORK .............................................13

8. EXPENDITURE FRAMEWORK .....................................14

8.1 HUMAN RESOURCE COST ....................................................... 15

8.2 PROVISION FOR BAD DEBT ..................................................... 15

8.3 DEPRECIATION ...................................................................... 16

8.4 APPROPRIATION OF DISCRETIONARY LINE ITEMS....................... 16

8.5 FUNDING AND EVALUATION OF CAPITAL BUDGET....................... 17

8.6 STRATEGIC PROJECTS SUPPORTING THE ACHIEVEMENT

OF THE SERVICE DELIVERY ..................................................... 18

9. RATIO BETWEEN THE CAPITAL ANDOPERATING BUDGET ..................................................21

2

MEDIUM TERM BUDGET POLICY

1. PLANNING FRAMEWORK

The Constitution requires local government to relate its management, budgeting andplanning functions to its service delivery objectives. This gives a clear indication of theintended purposes of municipal integrated development planning. Legislation stipulatesclearly that a municipality must not only give effect to its IDP, but must also conduct itsaffairs in a manner which is consistent with its IDP. This includes the compilation of theMedium Term Revenue and Expenditure Framework.

The City’s GDS and IDP is its principal strategic planning instrument, which directly guidesand informs its planning, budget, management and development actions. This frameworkis rolled out into objectives, key performance indicators and targets for implementationwhich directly inform the Service Delivery and Budget Implementation Plan.

With the compilation of the 2014/15 Medium-Term Revenue and Expenditure Framework(MTREF), each department/function had to review its business planning processes takinginto their individual departmental strategies. Business planning links back to priority needsand master planning, and essentially inform the detail operating budget appropriationsand three-year capital programme.

The main objectives of the City include:

Provision of quality basic services and infrastructure;

Economic growth and development that leads to sustainable job creation;

Fighting poverty and building clean, healthy, safe and sustainablecommunities;

Provision of integrated social services for empowered and sustainablecommunities;

Fostering participatory democracy and Batho Pele principles through a caring,accessible and accountable service;

Ensuring financial sustainability; and

Optimal institutional transformation to ensure capacity to achieve setobjectives.

In order to ensure integrated and focused service delivery between all spheres ofgovernment it is important for the City to align its budget priorities with that of national andprovincial government. All spheres of government place a high priority on infrastructuredevelopment, economic development and job creation, efficient service delivery, povertyalleviation and building sound institutional arrangements.

The 2014/15 MTREF will, in particular, be based on the following strategic documents:

EMM GDS 2055;

Ekurhuleni Service Delivery Statement;

Addressing the National Outcomes set by Parliament; and

National Treasury guidance.

3

2. EKURHULENI SERVICE DELIVERY STATEMENT

Reduce unemployment, poverty and inequality and produce decent jobs andsustainable livelihoods.

Adequate education and training to enable people to participate productively inthe economy and society.

Health care in a system that is accessible to more South Africans.

Rural communities benefiting from investments in basic services (water,electricity, sanitation and roads), and

Safer communities as serious and priority crimes are reduced, corruptiondefeated, and the criminal justice system is radically changed.

3. EMM GDS 2055

EMM Gauteng City Regional Integration

Regional accessible public transport network development.

Regional broadband infrastructure networks development.

Regionally integrated Ekurhuleni Aerotropolis redevelopment.

Integrated regional air, rail and road logistics network development.

Sustainable Settlements and Infrastructure

Invest in off grid long term infrastructure.

Investment in on grid long term infrastructure.

Develop long-term formal settlements plan.

Develop long term informal settlements plan.

Connected working and living spaces

Establish integrated urban core.

Break through and re-connecting townships.

Creating new civic identity and connections.

Revalorise historic sites and redundant land assets.

Strengthened Industrial Competiveness

Establish industrial development pricing mechanisms.

Institutionalise industry clusters.

Integrate industrial policy and government supply chain.

Industrial Systems and Infrastructure

Establish a centre of excellence for sustainable industrial production.

Establish an incentive framework for sustainable production.

Establish an industrial skills hub.

New Value Chains Development

Establish business development infrastructure for SMMEs.

Integrated SMME development and urban development.

4

Facilitate the development of new value chains in the green industry.

Market and Product Development

Integrate industrial and urban development policy.

Facilitate sustainable product development.

Facilitate development and access to new markets.

Greenhouse gas emissions policy development and implementation.

Sustainable Agriculture

Integrated environmental and urban development policy.

Integrated greening and food production.

Conversion of wasted urban spaces for urban agriculture.

Sustainable Natural Resources Use

Deployment of renewable energy regimes.

Promote re-use of waste.

Incentivise water harvesting and re-use.

Increase usage of sustainable storm water.

Biodiversity and Ecosystems Management

Conserving existing ecosystem and biodiversity.

Acid mine water rehabilitation.

Rehabilitate damage ecosystems and biodiversity.

Waste lands rehabilitation.

Improved Environmental Governance

Increase air pollution control measures.

Develop, implement and enforce by-laws of carbon reduction.

Incentives carbon efficient business and community measures.

Social care supply chains management

Integrate social care policy and family development.

Implement life cycle management.

Integrate administrative and social structures.

Social care chains development.

Capabilities Development

Increase investment in economic and social skills.

Promote multiple livelihood approaches.

Increase support to primary and secondary education.

Integrated family and early childhood development.

Responsive and Active Citizenry

5

Integrate service delivery and citizen responsibility.

Digitise municipal interactions with communities.

Strengthen existing community structures.

Building a Capable Local City State

Develop integrated urban development programme.

Modernise and capacitate the institution.

Effective and responsive area based management.

Strengthen Developmental Governance

Establish partnerships for service delivery.

Establish long term partnership for growth.

Strengthen inter-governmental partnerships accords.

Establish Gauteng City Region based development partnership.

Establish Long Term Fiscal Strength

Galvanise state and private sector investment.

Strengthen tax base and income streams.

Balanced subsidy burdens and financial viability.

Strategic Acquisition and Management of Assets and Operations

Strategic acquisition and management of HR assets.

Strategic acquisition and management of key assets.

Strategy aligned human resource management.

Strategy aligned operations management.

4. NATIONAL TREASURY GUIDELINES

National Treasury guidelines are issued during the latter part of the year. The 2014/15MTREF was based on the following key focus areas highlighted in National TreasuryCircular No 70 dated 4 December 2013 and Circular 72 dated 17 March 2014, which areas follows:

Key focus areas for the 2014/15 budget process

The Medium Term Budget Policy Statement (MTBPS) 2014The MTBPS notes that over the past four-and-a-half years government has steered thecountry through the worst global recession in 70 years, and that the South Africaneconomy is projected to grow by 1.8% in 2013/14 while the GDP growth is expected to be2.1% in 2014/15 increasing to 3.5% by 2016/17.

Specific strategies and interventions required by local government in achieving economicstability and higher levels of growth as outlined in the MTBPS include, among others:

Expanding public sector investment in infrastructure through ensuring the budgetsand MTREFs acknowledge that capital programmes need a balanced funding structureaddressing not only backlogs in services but also investment in new infrastructure, as wellas renewing current infrastructure.

6

Sustainable job creation remains a national priority and municipalities must ensure thatin drafting their 2014/15 budgets and MTREFs, they continue to explore opportunities topromote labour intensive approaches to delivering services, and more particularly toparticipate fully in the Expanded Public Works Programme. Municipalities, however,should not carelessly employ more people without any reference and consideration to thelevel of staffing required delivering effective services. Remuneration increases associatedwith bargaining council decisions and affordability must be considered over the mediumterm. Municipalities should focus on maximising job creation by:

Ensuring that service delivery and capital projects use labour intensive methodswherever appropriate;

Ensuring that service providers use labour intensive approaches; Supporting labour intensive LED projects; Participating fully in the Expanded Public Works Programme; and Implementing internship programmes to provide young people with on-the-job

training.

Municipalities must act as catalysts for economic growth through creating anenabling environment for investment and other activities that foster job creation. It isimportant for municipalities to pay particular attention to:

Joint planning by a municipality, its community and business sectors. This meansthat all economic forces in the local situation have to be brought on board toidentify resources, understand needs and work out plans to find the best ways ofmaking the local economy fully functional, investor friendly and competitivelyproductive;

Ensuring the timely delivery of their capital programmes and to review all by-lawsand development approval processes with a view to removing any regulatorybottlenecks to investment and job creation; and

Act as a catalyst for local economic development by appropriately structuringcapital programmes to address backlog eradication, asset renewal anddevelopment of new infrastructure; this will require carefully formulating thefunding mix to include grants, borrowing and own funding (internally generatedfunding).

Securing inclusive growth through investing in strategic infrastructure programmes suchas electricity generation. An example is the partnership between the public and the privatesectors on the Renewable Energy Independent Power Producer Programme.

Implementing the National Development Plan through expanding electricity, transport,communications capacity and promoting industrial competitiveness. Municipalities need tosupport special economic zones, broadening rural development and strengthening publicservice delivery while combating waste and corruption.

Building an efficient developmental state through increasing the levels of delivery byensuring improvements to policy formulation, procurement, management systems,developing mechanisms for sharing skilled personnel in critical delivery areas andminimising waste.

Furthermore, the NDP recognises capable municipalities as the core of a capable state.National Treasury will continue to closely monitor and engage – and if need be intervene –in those municipalities that fail to live up to the standards of public service established inthe Constitution.

In supporting municipalities over the MTEF period, a strong focus on economicdevelopment is proposed by:

Ensuring that value for money and long term impact/sustainability are keyconsiderations;

7

Having an economic development /growth support strategy in place, but not just asan end in itself but rather as an opportunity to understand and respond to theunderlying economic dynamics, networks and dynamic systems of interactions of amuch wider range of stakeholders that shape the economic fabric of each locality;

Pursue initiatives that:Stimulate growth required to create jobs and to reduce poverty;Provide a competitive local business environment;Encourage and support networking and collaboration between businesses and

public/private and community partnerships;Facilitate workforce development and education;Focuse inward investment to support cluster growth; andSupport quality of life improvements.

Considering that public expenditure growth has remained well within the limits set bygovernment over the past two years, further efforts to find savings, eliminate waste andreprioritise spending toward key social and development objectives must be pursued byall government spheres.

The notion of ‘doing more with less’ can further be supported by municipal approachesthat ensure:

Spatial strategies align public spending and unlock public and private investment;

Focus on catalytic interventions that also promote inclusion and desegregation;and

Provide clear signals to private sector.

Consequently, municipal revenues and cash flows are expected to remain under pressurein 2014/15 and so municipalities must adopt a conservative approach whenprojecting their expected revenues and cash receipts.

Municipalities should carefully consider affordability of tariff increases; especially as itrelates to domestic consumers while considering the level of services versus theassociated cost. Municipalities should also pay particular attention to managing revenueeffectively and carefully evaluate all spending decisions. Municipalities must implementcost containing measures as approved by Cabinet to eliminate non-priorityspending.

5. FINANCIAL STABILITY IN THE CURRENT FISCALFRAMEWORK

5.1 NATIONAL ECONOMY

The Minister of Finance, in his budget speech of 26 February 2014, indicated that SouthAfrica’s economy has continued to grow, but at a slower rate than projected a year ago. Aweaker exchange rate is a risk to the inflation outlook, but it supports exporters. Sustainedimprovements in competitiveness require further investment in infrastructure and a rangeof microeconomic reforms.

GDP growth reached 1.8% in 2013 and is expected to grow at 2.1% in 2014, rising to3.5% in 2015.

Inflation has remained moderate, with consumer prices rising by 5.7% in 2013 andprojected to increase to 6.2% in 2014 and hopefully decrease to 5.5% in 2016.

In his speech, the Minister of Finance referred to a number of aspects and initiatives thatinfluenced the local economy, namely:

Boosting growth

8

Government will continue to provide an enabling environment for businesses to grow andcreate employment.

Removing constraintsOver the medium term government will:

Add to electricity supply to improve the balance between: available energy and the amounts required by businesses; and households to thrive.

Increase investment in economic infrastructure, including rail, water, roads andports;

Pursue the exploration of shale gas to provide an additional energy source for theeconomy; and

Provide business support programmes and special economic zones thatencourage industrialisation and improve local competitiveness.

Regulatory improvementsGovernment has been engaging business on specific steps that can be taken to make iteasier to do business in our country. This includes the streamlining of regulatory andlicensing approvals for environmental impact assessments, water and mining licenses.

There is further work in progress on lowering the cost structure of the economy, forexample through improved efficiencies in freight logistics.

Government published a new policy on broadband which will, in due course, lead tomodernisation of our communications capabilities. Several cities are bringing Wi-Ficonnectivity to their environs.

SARS is taking further steps to lower the cost of tax compliance in South Africa.

AfricaInvestment into Africa has reached R36 billion a year, in a range of industries. SouthAfrica is the second largest developing country investor on the continent. In 2013, a figureof 29% of our exports was destined for Africa. In 2012, 12% of our dividends came fromAfrica, up from just 2% a decade earlier. Increasing these inflows will be crucial for closingthe current account deficit.

The Minister of Finance announced further steps in his budget speech to simplify tradeand investment with Africa.

Promoting InvestmentIncreased investment in the economy by both the private and public sector is at the heartof creating jobs and growth.

Government is committed to providing policy certainty for domestic and foreign investors.A holistic framework for investment is being finalised by National Government. Thisframework flows from the National Development Plan, which places investment at thecentre of our economic growth plan.

A number of incentives have been put in place, which will provide substantial benefits toboth foreign and domestic investors. Moreover, a new Promotion and Protection ofInvestment Bill has been released for public comment. This entrenches the rights of allinvestors, ensuring that property rights are protected, in line with the Constitution.

Unlocking city development and municipal service delivery

The Minister of Finance also addressed the unlocking of city development and municipalservice delivery in his budget speech.

9

He, inter alia, indicated that development plans must focus on overcoming the spatialfragmentation of South Africa’s built environment, improved public transport andaccelerated investment in human settlements.

An integrated city development grant has been introduced by National Government tostrengthen long-term city planning and encourage private investment in urbandevelopment. It will amount to R814 million over the medium term. In this regard EMMreceived an allocation of R40.3 million in 2014/15.

The assignment this year of the human settlements function to metropolitan municipalitiesis a vital intervention in accelerating housing investment and integrated urbandevelopment. A new grant of R52.3 million per financial year has been allocated to EMMto assist in managing the human settlements function.

Over the next three years, National Government will allocate R105 billion to municipalitiesfor free basic water, sanitation, electricity and refuse removal services. This allocation inthe form of an Equitable Share amounts to R2.043 billion in 2014/15.

5.2 LOCAL ECONOMY

As global economic growth recovers there will be opportunities and risks for the economy.These developments have the potential to increase exports. Among our emerging marketpartners, growth remains strong but demand for mineral products has moderated and isunlikely to pick up soon. The prices of our largest sources of foreign earnings remaindepressed.

The rand, however, remains an effective shock absorber against global volatility. Recentmovements of the currency have been supportive of export growth while reducing thecountry’s reliance on capital inflows.

South Africa must ensure that its fiscal and monetary choices keep inflation low andmaintain the recent gains in competitiveness. While significant progress has been made inaccumulating reserves, there is scope for further improvement. This will support thestability of the currency.

The local economy has the challenge of unemployment confronting the City. Attempts aremade to invest in short-term employment solutions which include, among other, thecommunity works and the expanded public works programme (EPWP). These solutions,while important, are not sustainable in the long run and Ekurhuleni will need to find long-term job creating solutions that will guarantee growth in employment opportunities in orderto absorb the growing number of unemployed residents of the City. Secondly, the City willhave to balance continuing to attract the services sector developments which are notnecessarily good for jobs but for economic growth.

Skills development, in line with what industry needs, continues to confront the City inaddressing the challenge of employment creation as indicated above. In making thenecessary strides in skills development the national government established Skills,Education and Training Authorities (SETAs) to undertake this project. The lack ofeffectiveness during the implementation of this initiative has raised the need for industryled skills development approaches. The City’s development status as a manufacturinghub has its connections to steel/metal and plastic as key sectors, and these havemaintained their resilience.

However, with the shift that is being undertaken globally and nationally towards a greeneconomy the City will have to balance making more investments and structuringincentives that promote its traditional manufacturing base, and making investment andstructuring incentives in line with the changing demands from emerging markets and therequirements of the green economy.

10

There have been major strides taken by the City in this regard, these includeestablishment of tender advice centres, cooperatives and other SMME supportmechanisms. Underpinning these mechanisms has been massive reliance on PreferentialProcurement framework and BEE frameworks as development systems. These systemshave made some gains; however, it is also noticeable that SMMEs continue to bedislocated from the main economic value chains defining the structure of the SouthAfrican economy.

On 1 October 2012, Moody’s Investor Service downgraded the long term ratings of 13South African sub-sovereign issuers, including the Ekurhuleni and its entity ERWAT. Theaction was prompted by the recent Moody’s downgrade of South Africa’s governmentbond rating to Baa1 from A3.

Despite the ratings downgrade to Aa3.za, Ekurhuleni maintains a credit rating that is atthe high end of all municipalities rated by Moody’s in South Africa.

The downgrade may increase investors’ risk in investing in EMM’s bond market. It couldresult that EMM has to borrow funds at a higher interest rate than previously. This couldincrease the Interest on Loans as provided in the Operational Budget. Subsequently itcould result in a higher increase of rates and taxes. However, the Metro remains confidentthat the downgrade will not have a negative impact on the interest rates at which itborrows as the Metro is still in the high grade category.

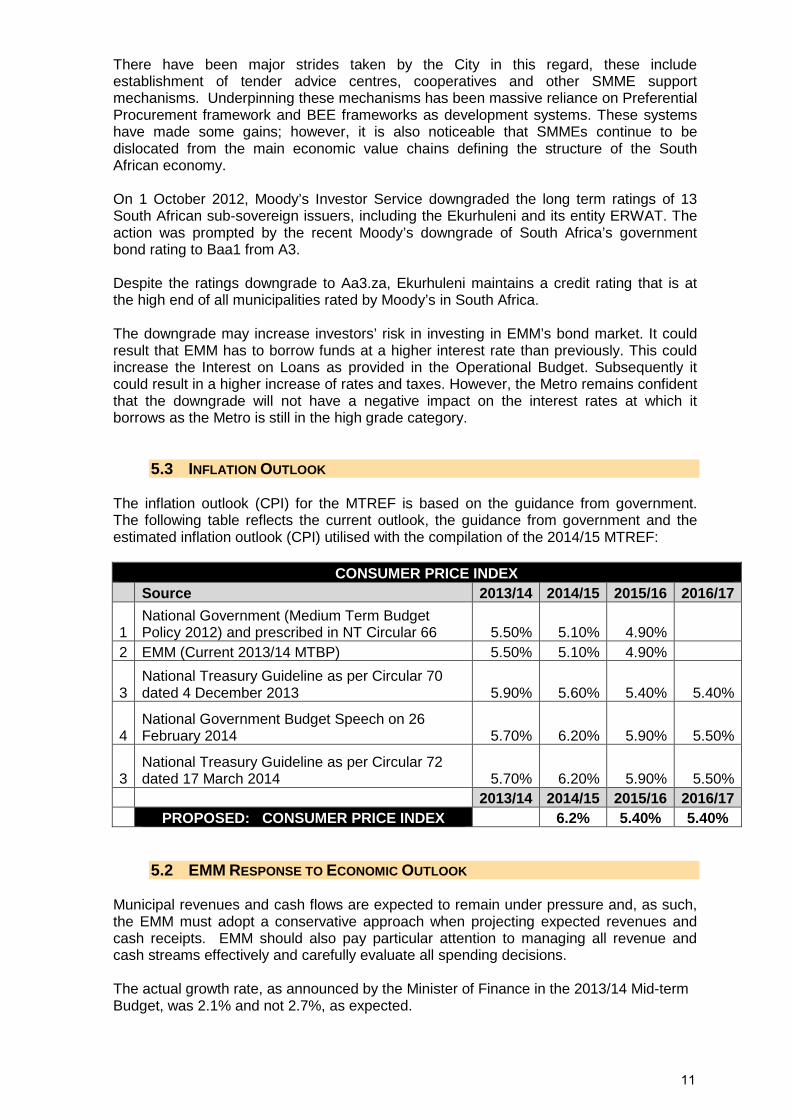

5.3 INFLATION OUTLOOK

The inflation outlook (CPI) for the MTREF is based on the guidance from government.The following table reflects the current outlook, the guidance from government and theestimated inflation outlook (CPI) utilised with the compilation of the 2014/15 MTREF:

CONSUMER PRICE INDEX

Source 2013/14 2014/15 2015/16 2016/17

1National Government (Medium Term BudgetPolicy 2012) and prescribed in NT Circular 66 5.50% 5.10% 4.90%

2 EMM (Current 2013/14 MTBP) 5.50% 5.10% 4.90%

3National Treasury Guideline as per Circular 70dated 4 December 2013 5.90% 5.60% 5.40% 5.40%

4National Government Budget Speech on 26February 2014 5.70% 6.20% 5.90% 5.50%

3National Treasury Guideline as per Circular 72dated 17 March 2014 5.70% 6.20% 5.90% 5.50%

2013/14 2014/15 2015/16 2016/17

PROPOSED: CONSUMER PRICE INDEX 6.2% 5.40% 5.40%

5.2 EMM RESPONSE TO ECONOMIC OUTLOOK

Municipal revenues and cash flows are expected to remain under pressure and, as such,the EMM must adopt a conservative approach when projecting expected revenues andcash receipts. EMM should also pay particular attention to managing all revenue andcash streams effectively and carefully evaluate all spending decisions.

The actual growth rate, as announced by the Minister of Finance in the 2013/14 Mid-termBudget, was 2.1% and not 2.7%, as expected.

11

The Electricity, Water and Sanitation income, which is demand-driven, appears to shownegative/very slow growth from the previous financial year. The electricity income reflectseven a negative result of 4.96% in the 1st Quarter report. The fact that bulk purchasesshow a similar below budget results is proof that actual sales were reduced in the firstquarter.

Population growth in EMM, as reflected in the 2011 statistics, does not necessarily implythey are economically active, which puts a huge demand on existing income sources.

The proposed growth rate per service is as follows:

- Assessment Rates Income: 2.0%- Electricity Sales: -1.0%- Water Sales: 2.0%- Sanitation Sales: 2.0%- Refuse Removal / Solid Waste: 2.0%

6. KEY ASSUMPTIONS FOR THE 2014/15 MTREF

6.1 SOCIO ECONOMIC ASSUMPTIONS

Despite various campaigns launched to increase the number of EMMregistered indigents the number remains in the region of 30 000. This is alsofar below par if compared to neighbouring metros where is ranges between100 000 and 130 000 indigents.

This situation has a direct impact on the current collection levels and theincrease in outstanding debts, and subsequently wasteful credit control costs.One of the biggest reasons for the low number of residents applying forindigent-status is the relative large number of residents living in Eskomelectricity supply areas.

EMM will continue with the maintenance of a formal indigents register, but it isproposed to implement the targeted approach for the identification of deemedindigents. All land owners of properties below R150 000, as reflected inCouncil’s general valuation roll, will be deemed as indigent and benefit on thesocial grants available to indigents. The policy on indigents has beenamended to accommodate registered as well as deemed indigents. Thenumber of indigents will increase to approximately 115 000.

Social support will be provided to indigents in the form of additional rebatesand free basic services.

It is further assumed that consumption management will be applied to ALLindigent households and no excess consumption will be written off.

EMM will continue to supply 6Kl water as a free basic service to ALLresidential properties.

The first 6Kl charged for sanitation will also be supplied as a free basic serviceto ALL residential properties.

Registered and deemed indigents will receive an additional 3Kl of water andsanitation as a free basic service.

The current tariff schedule for assessment rates makes provision for aresidential rebate of R150 000 for all residential properties, which is also beingregarded as a free basic service and it will remain in the 2014/15 MTREF.

The limited resources for the supply of electricity nationally have an impact oneconomic development in Ekurhuleni. As part of the national campaign toreduce energy demand EMM will continue to supply 100kWh electricity units.These will benefit from the targeted approach on making free basic servicesavailable to consumers who manage their consumption to be within prescribed

12

limits. This will benefit indigents both by reducing the cost of their accounts,but also by providing a greener environment which would ultimately lead toincreased investment and additional jobs (additional electricity capacity willattract businesses that require additional electricity capacity).

The job creation projects will yield jobs during the MTREF period but as aresult of in-migration of additional poor people seeking employment in the City,the number of poor households will remain stable.

The medium term goal of Council to ensure financial stability is to increasecollection rates closer to 95% of the billed income. The low collection level ofresidents in Eskom supply areas remains a huge burden in achieving thedesired collection levels.

6.2 GRANTS FRAMEWORK ASSUMPTIONS

Grants included in the MTREF as per the Division of Revenue Bill, 2014 - Billpublished in Government Gazette No 37337, dated 21 February 2014.

National Treasury will continue to use the Stats SA data to determine povertyin municipalities and use this data as the basis for the calculation of theEquitable Share Grant, and that the increased number of indigents registeredin the EMM will not have any impact on the grant.

The provincial grants are based on Provincial Gazette Extraordinary publishedon 3 March 2014.

The EMM will continue to receive a portion of the Fuel Levy.

Ekurhuleni will benefit from Public Transport Infrastructure (PTIS) grants forthe amount of R970 million over the MTREF period as per the IntegratedRapid Public Transport Network (IRPTN) business plan, and funding requestsubmitted to National Treasury. An amount of R750.4 million over the MTREFhas also been provided from the USDG.

6.3 TARIFF INCREASE ASSUMPTIONS

Projected revenue for the MTREF period is based on an 8.02% electricity bulkpurchases and a 7.39% sales price increase.

Projected revenue for the MTREF period is based on bulk water purchases of8.1% and similar sales price increase of 8.1%.

ERWAT tariff increases are indicatively set at 8% based on their capital andoperating requirements. A sanitation charges increase of 8% is proposed.

An assessment rate tariff increase of 7.5% is proposed. This increase remainsin line with the previous year’s MTREF estimates.

Solid Waste will increase with 10% for residential properties and 6% tobusinesses and industries. In addition to this, the levying of the R5 cleansinglevy per property per month has been removed. This, in effect, resulted in anaverage of 4.5% reduction for residential owners. The net impact of the solidwaste tariff for residential properties is therefore approximately 5.5%.

The increase for businesses and industries serves as a catalyst for economicgrowth as one of the key aspects mentioned in the NT circular mentionedearlier.

All other services are assumed to increase by the CPI rate.

6.3 OTHER KEY ASSUMPTIONS AND COST DRIVERS

Standard Chart of Accounts implementation – EMM systems to be adjustedwithin the MTREF period.

13

Introduction of NERSA system of Tariff approvals based on Return on Assets– this is assumed to be introduced in the outer years and not in 2013/14.

On-going fuel increases – higher than inflation increases expected for MTREFperiod.

Rand/Dollar exchange rate: ongoing pressure on the rand expected over themedium term.

Ongoing instability in the labour market – higher than inflation increasesexpected. It is assumed in this budget policy statement that the SALGABargaining Council agreement signed between the employer and employeerepresentatives on 27 July 2012 will prevail and that wage negotiations will notbe re-opened.

7. REVENUE FRAMEWORK

The municipality’s revenue strategy is built around the following key components:

National Treasury’s guidelines and macro-economic policy.

Growth in the City and continued economic development.

Efficient revenue management, which aims to ensure a 93% annual collectionrate for property rates and other key service charges. As a result of therevised indigent management methodology, there may be a movementbetween the provision for bad debt and the grants: indigent’s line items but netrevenue collected will remain stable.

Revenue targets to be set for each department and, in particular, monthlyrevenue targets for:

Assessment rates;

Electricity;

Water and Sanitation (based on water loss eradication programme);

Refuse Removal;

Real Estate Commercial Leases;

SRAC Leases;

Housing Rentals;

Building Control Revenue;

Outdoor Advertising; and

Revenue from Data services provided.

Electricity tariff increases as approved by the National Energy Regulator ofSouth Africa (NERSA) – this does not exclude the application of tariffs higherthan NERSA guidelines.

Achievement of full cost recovery of specific user charges especially in relationto trading services – this could lead to higher than inflation tariff increases.

Determining the tariff escalation rate by establishing/calculating the revenuerequirement of each service.

The municipality’s Property Rates Policy approved in terms of the MunicipalProperty Rates Act, 2004 (Act 6 of 2004) (MPRA).

Increase ability to extend new services and recover costs.

The municipality’s Indigent Policy and rendering of free basic services, whichmay include the phasing out of certain components of the free basic servicesover the MTREF period.

Tariff policies of the City.

14

In summary, the following sources of revenue (cash inflows) will be available to the Metro(excluding entities) during the next financial year:

Assessment Rates and User Charges for Services: R20.9 billion.

Operating Grants - R2.7 billion

Fuel Levy – R1.5 billion

All other Revenue excluding the above listed income – R1.2 billion

A total of R26.3 billion is thus projected as revenue for the 2014/2015 financial yearas reflected in Table 4 of Annexure C.

Capital grants amounting to R2.0 billion has been excluded in the above amount.The capital grant as reflected in Table 39 in Annexure C.

8. EXPENDITURE FRAMEWORK

The City’s expenditure framework for the 2014/15 budget and MTREF is informed by thefollowing:

Institutional Review and Human Resources Strategy.

The asset renewal and the repairs and maintenance requirements asidentified in the asset condition assessment.

Balanced budget constraint (operating expenditure should not exceedoperating revenue) unless there are existing uncommitted cash-backedreserves to fund any deficit, of which there is none.

Funding of the budget over the medium-term as informed by Section 18 and19 of the MFMA.

Intensified cost reduction strategy to be implemented.

Expenditure is categorised as being either committed (top-slice) or discretionary based onthe level of discretion that the municipality has in amending the cost in the medium term.The greatest portion of the operating budget is committed expenditure which is highlypredictable based on contractual commitments. Committed costs can generally only beavoided/amended after the contractual period has expired.

Discretionary budget allocations will only be made based on Results Based Projectsubmissions made by departments.

The following line items will be considered for budget allocations as the “Top Slice” andincreases will be based on the appropriate index (be it CPI or other appropriate economicindex):

Salaries;

Councillors’ allowances;

Provision for bad debt (based on a 93% collection rate);

Depreciation;

Interest expense;

Committed contracts as per register;

Bulk purchases (Eskom, Rand Water, ERWAT); and

Accounting provisions.

15

8.1 HUMAN RESOURCE COST

Insofar as Human Resources costs are concerned, the current profile of the salary bill isas follows:

Employeecategory

No. ofPositions

% ofPositions

Salary Budget % of Budget

Top management 197 1% R 312,791,936.54 6%

SeniorManagement

170 1% R 124,447,646.78 3%

Professionals 1,153 6% R 641,718,962.82 13%

Unskilled 1,995 11% R 276,845,728.28 6%

Skilled 4,706 26% R1,621,045,443.91 33%

Semi-Skilled 10,022 55% R1,946,000,246.81 40%

Grand Total 18,243 100% R4,922,849,965.14 100%

Top Management (City Manager, Heads of Departments, Directors).

Senior Management (Executive Managers, Senior Managers, SeniorProfessional Engineers, Regional Managers).

Professionals (Managers, Legal Advisors, Environmental Health Practitioners,Chief Accountants/ Engineers).

Skilled (Accountants, Artisans, Building Inspectors, Examiners - driving).

Semi-Skilled (Administrative Assistants, Artisan Assistants, Enrolled Nurses,Supervisors).

Unskilled (General Workers, Cleaners, Messengers, Office Assistants).

During this MTREF, focus will be in ensuring more professionals and skilled positions arebrought into the structure. The vast majority of staff members are in the semi-skilled andunskilled category. The low percentages of skilled and professional staff are one of thecontributing factors of the significant present use of consultants.

The HR strategy will be developed and resourced in the MTREF period and the followingpriorities will be dealt with:

Finalisation of the Institutional Review;

HR ICT Systems;

Workforce Planning;

Remuneration Framework;

Scarce and Critical Skills;

Health and Wellness – disease profiling;

Scoping of the EMM Institute.

8.2 PROVISION FOR BAD DEBT

The provision for bad debt is a quantification of the billed amounts not collected.

An amount equalling the amounts billed and not collected is shown as an expenditure itemand as a contribution to the provision for bad debt. This is called “impairing” the debtor inaccounting terms. In other words, the debtor is valued at less than the billed amount as itis expected that a lessor amount will be collected. This does not mean that the debt isactually written off. Only once Council approves debt write-offs, is the debt actually

16

written off. These write offs are then not processed as an expenditure item but the write-off is effected against the provision for bad debt.

8.3 DEPRECIATION

Depreciation is the systematic expensing of the value of an asset as it is used up anddoes not relate to any cash payment made (nor is the money owed to anyone for thatmatter). A road can last for 40 years and every year 1/40th of the road is “used up” andthat must be shown as an expenditure item called depreciation. The intention is to setthese funds aside so that there is cash available at the end of the useful life of the asset toreplace the asset.

The projected depreciation cost is based on the existing asset register, the remaininguseful life of the assets, the condition of the assets as well as the new assets to beacquired as per the draft MTREF for the 2014/15 – 2016/17 financial periods.

Phasing in of the inclusion of depreciation as cost in the setting of tariffs: 2014/15 will bethe seventh year of a 10-year implementation plan - with 2017/18 as the last year. A 57%of the depreciation charge is now included and will increase to 70% in 2014/2015.

8.4 APPROPRIATION OF DISCRETIONARY LINE ITEMS

An overheads cost allocation will be given to departments – these items will be dealt withas incremental budgets as it is not cost effective to embark on a zero based budget forthese typical administrative costs:

Audit Fees;

Bank Charges;

Corporate Gifts;

Fuel and Lubricants;

General Consumables;

Insurance;

Materials;

Postage;

Printing and Stationery;

Refunds of developers contributions in terms of approved servicesagreements;

Stock Adjustments;

Telephone Costs; and

Rental of existing leased buildings (where agreements are in place).

Costs that are classified as being “top-slice” and administrative will not be automaticallyincreased without scrutiny. These cost items will be subjected to cost reductionprocesses. As a result, inflationary increases will be given to some departments, lowerthan inflationary increases will be allocated in certain cases, and even reductions inothers.

Departments will then be given an opportunity to submit proposals for service deliveryprojects, which must include the outputs to be achieved. The allocation of funding will bebased on the outputs to be achieved, and not based on actual expenditure of previousyears.

17

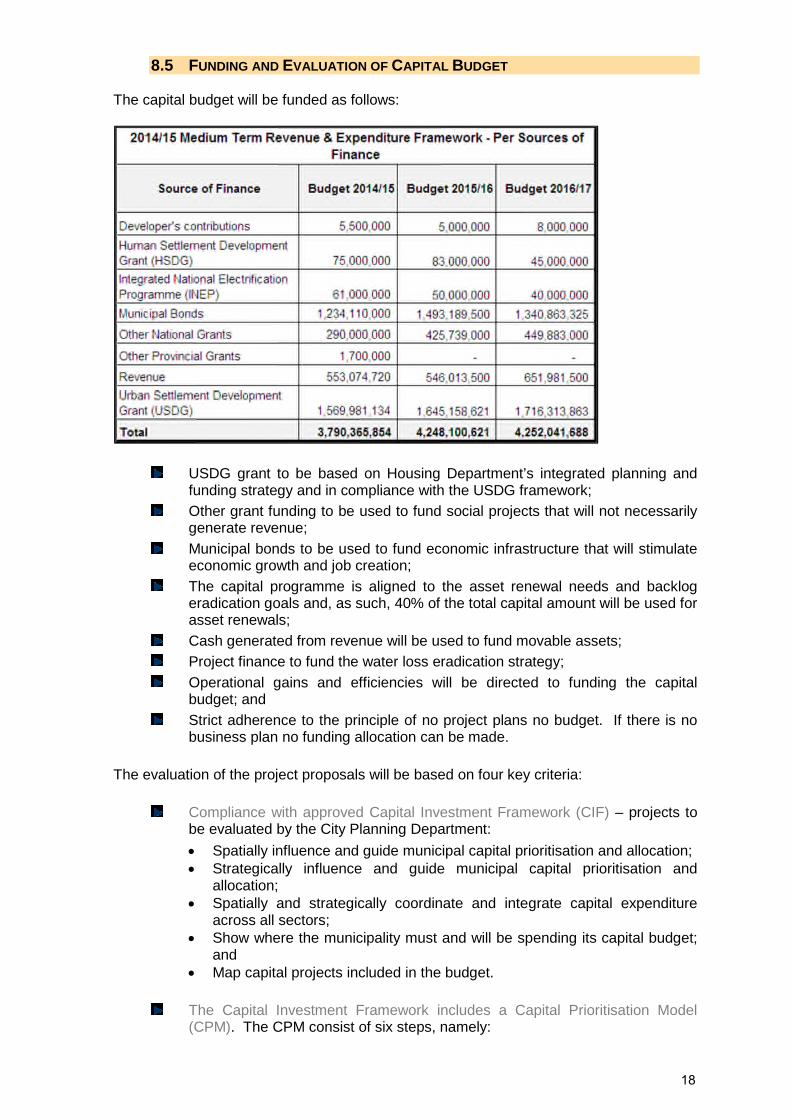

8.5 FUNDING AND EVALUATION OF CAPITAL BUDGET

The capital budget will be funded as follows:

USDG grant to be based on Housing Department’s integrated planning andfunding strategy and in compliance with the USDG framework;

Other grant funding to be used to fund social projects that will not necessarilygenerate revenue;

Municipal bonds to be used to fund economic infrastructure that will stimulateeconomic growth and job creation;

The capital programme is aligned to the asset renewal needs and backlogeradication goals and, as such, 40% of the total capital amount will be used forasset renewals;

Cash generated from revenue will be used to fund movable assets;

Project finance to fund the water loss eradication strategy;

Operational gains and efficiencies will be directed to funding the capitalbudget; and

Strict adherence to the principle of no project plans no budget. If there is nobusiness plan no funding allocation can be made.

The evaluation of the project proposals will be based on four key criteria:

Compliance with approved Capital Investment Framework (CIF) – projects tobe evaluated by the City Planning Department:

Spatially influence and guide municipal capital prioritisation and allocation; Strategically influence and guide municipal capital prioritisation and

allocation; Spatially and strategically coordinate and integrate capital expenditure

across all sectors; Show where the municipality must and will be spending its capital budget;

and Map capital projects included in the budget.

The Capital Investment Framework includes a Capital Prioritisation Model(CPM). The CPM consist of six steps, namely:

18

Describe the capital budget in four project categories (Backlog Eradication,Upgrading and Renewal; Economic Development; Political Prerogative);

Allocate a budget percentage to each of the four project categories; Allocate each budget category per geographic focus area (in the CIF); Screen all submitted projects for IDP, SDBIP and PMO compliance; Allocate individual capital projects as submitted by departments into

project categories and CIF geographic priority areas; and Score individual capital projects to determine ranking per project category

and CIF geographic priority areas.

Compliance with the USDG Framework and Housing Strategy - projects to beevaluated by the Human Settlements and City Planning departments:

Allocation towards the outcomes as identified in the USDG Framework:o Access to basic services and infrastructure.o Incremental improvements in security of tenure.o Access to social services and economic opportunities.o Improved rates of employment through skills development in the

delivery of infrastructure.o Bridging the bankability gap for infrastructure provisions within mixed

income and mixed use developments. Allocation in respect of land release; Development of human settlements and achievement of the outcomes of

sustainable human settlements and improved quality of household life asmeasured against the following indicators:o Additional households in informal settlements receiving basic municipal

services per annum, including water and sanitation, solid waste andarea lighting.

o Inset upgraded households in informal settlements.o Households relocated from informal settlements.o Hectares of land identified, procured and proclaimed for informal

settlements upgrading and/or mixed use development.o Title deeds transferred to eligible households.o Work opportunities created through the overall capital programme of

the municipality.o Households served by schools and clinics within upgrade settlements.

Alignment of municipal planning on human settlements with nationalpriorities and provincial human settlements plans.

Economic impact of projects - projects to be evaluated by the EconomicDevelopment Department:

Impact on job creation and skills development. Key industrial and cluster development. Key regional economic catalytic projects. Local production and procurement. Community economic empowerment.

8.6 STRATEGIC PROJECTS SUPPORTING THE ACHIEVEMENT OF THE SERVICE

DELIVERY

Infrastructure Delivery (Municipal and Social)

Council’s backlogs were determined in June 2009 as part of the first asset managementevaluation process. The original figures were reviewed in June 2011 as part of thecompilation of the asset management plan. Backlogs mainly resulted from formation ofinformal settlements, historical services backlogs and ageing infrastructure. Accessbacklogs were directly advised by the Housing Development Plan and level of services. At

19

present, the availability of land is the biggest constraint due to dolomite and shallowundermining.

Composite capital and maintenance funding requirements up to 2028

Some R85.81 billion is needed to address existing service access backlog, technicalbacklogs, and to meet the demand of growth and on-going renewals until 2028. This willrequire an average of R5.72 billion per annum, which means an increase in the assetbase of 79% (asset replacement value). In addition, an amount of R41.27 billion would berequired for maintenance over the 15-year reporting period, representing an increase of87% per year over current levels of expenditure by 2028.

The following categories have been identified in the backlog study and represent thefunding requirements for the next 15 years:

Access backlog: Total infrastructure backlog of existing customers (informalsettlements and previously disadvantaged areas) – R14.5 billion;

Technical backlog – R9.9 billion;

Condition Backlog: Total renewal needs (due to aged infrastructure); Capacity Backlog: Total upgrading needs (due to under capacity of existing

infrastructure);

Growth: Demand for new infrastructure due to expected growth – R42.6billion; and

Renewal: Future renewal demand due to ageing infrastructure – R18.8 billion.

Asset Maintenance and Renewals

Asset maintenance is critical to the sustainability of the Metro. National Treasury advisesthat 8% of the carrying value of assets must be used towards the maintenance of thoseassets.

Council has PPE to the value of R50 billion, meaning that a Repairs and Maintenancebudget of R4 billion must be set aside. The budget for Repair and Maintenance for2014/15 amounts to R2.36 billion, which is still below the required level. However, theimpact to increase the repair and maintenance budget to be 8% of PPE value would havea severe impact on the expenditure budget with consequential huge tariff increases. EMMwill prioritise the annual allocation for repair and maintenance over the medium-term.

In terms of the Asset Condition Assessment done, assets were required that have aremaining useful lives of less than five years and must be renewed to avoid asset failure.Cognisance must be taken of these assets when the capital renewal and repairs andmaintenance budgets are compiled.

Transport, Freight and Logistics

The Ekurhuleni Aerotropolis project includes, inter alia, development of land uses thatfacilitate the movement of people and goods by air. Initiatives include activities related toconsolidating Ekurhuleni as a ‘Gateway to Africa and the world’. This should includebusiness tourism, head office facilities, and the like. In this financial year the focus will beon developing the strategic road map and the master plan for the aerotropolis.

The Integrated Rapid Public Transport Network (IRPTN) project involves establishment ofinfrastructure, operations and modes of transport that will result in accessible reliable, safeand affordable public transport system. The project is mainly funded from the PublicTransport Infrastructure Grant (PTIS), but it is proposed that EMM provides for additionalfunding from its own sources.

20

Based on the revised plan submitted to the National Department of Transport (DoT), themunicipality is ready to proceed with the implementation of the subsequent phases of theproject namely, preliminary and detailed design, construction of road infrastructure,construction of the transport control center and depots, rolling out of IT infrastructure,implementation of the public transport industry transition programme and the acquisition ofappropriate fleet for the operations of the system.

A PTIS grant of R970 million has been allocated to EMM over the medium term period.

Institutional Mobilisation and Capabilities

The Institutional Review and Development is a project with the ultimate aim of ensuringintegration of the institutional configuration and capacity of the EMM. For some time, theEMM has been using the combination of two structures, both of which are not fullyimplemented. This has had a negative impact on service delivery, given the limitedcapacity in many departments. The institutional review process now under way will helpcreate a single, integrated organisation with the requisite skills and competencies to giveeffect to better service delivery.

City Modernisation

The Digital City project aims to ensure innovative use of technology to create a smartEkurhuleni. This project is divided into four streams of work, namely (1) Broadbandinfrastructure; (2) Setting up EMM as an internet service provider; (3) EnterpriseOperation Centre/Unified Command Centre, and (4) Digital City Services and products.Phase 1 of the project is under way and incorporates the setting up of a Digital City unit toprovide effective broadband infrastructure capable of supporting business services,commercialisation of the available optic fibre and connectivity for the Ekurhulenicommunity.

The City of Ekurhuleni is home to a significant number of manufacturing companies byany global comparative means. Global events such as the recessions across continentsare also impacting upon the growth, both positive and negative, of the companiesoperating within Ekurhuleni municipal boundaries. These events and conditions affectdecision making by senior managers, owners or investors in companies globally, inclusiveof those in Ekurhuleni municipality. As such, negative decisions, disinvestments orreduction of production capacities could be engaged by these senior managers which willultimately affect the competitiveness of Ekurhuleni as a region, liquidity of the city, andother socio-economic issues such as unemployment. The City, therefore, embarked on aprogramme of revitalising the manufacturing sector with the aim of contributing to thecompetitiveness of the manufacturing sector in its geography and contributes to thenational agenda of job creation.

Urban Acupuncture

The utilisation of our water bodies to support the building of local economies, sportdevelopment, recreation and tourism has been started in the 2012/13 financial year.Ekurhuleni is rich with lakes and dams which have the potential to enhance economicactivity in the City in the context of the Aerotropolis. The South African Maritime SafetyAuthority (SAMSA) and Ekurhuleni Metropolitan Municipality have started a process ofassessing the development potential of these water bodies, and to determine theirdevelopment and utilisation potential. To set the process in motion, some lakes and damswill be upgraded to appropriate standards. The Boksburg Lake, for example, is one waterbody that has been identified as contaminated with hazardous sludge. Here the mainfocus of the project is the dredging of the lake and restoration of its water quality toconform to recreational standards. In the past, the Brakpan Dam has had poor waterquality resulting in an intolerable smell during the rainy season. In its case, the aim will beto ensure that its water quality is addressed through aeration as well as installation of litterand silt traps.

21

The Germiston Urban Renewal and Township Revitalisation and Renewal Strategyprocesses will help give direction and guidance in terms of investment and developmentof the township to achieve economic growth, social cohesion and facelift of townships.This process has started with the facilitating and developing townships economies throughprogrammes of Township Hubs, which include Township Services Hubs, TownshipShared Industrial Production Facilities, Township Business Parks, Recycling Buy BackCenters, Fabrication Laboratory and the provision of street trading facilities. In addition,the City is facilitating development and investment projects in townships such as shoppingmalls.

A funding model based on a percentage of the programme management cost of theproject will be developed. The funding model will comprise funds from NationalGovernment as well as PPPs.

The township economies project aims to revive, revitalise and grow the collapsed state ofthe township economy that is as a result of the previous developmental trajectory thatexcluded previous black townships, resulting in poverty, unemployment, illiteracy and lowskills base with the resultant current social ills such as social crime, teenage pregnancy,and substance abuse.

This project includes several paradigms that include economic transformation (supplierdevelopment and BBBEEE), agriculture, and enterprise development, skilling for theeconomy, graduate placement programme, support for the formal and informal economythrough infrastructure provision (Township Hubs) and poverty alleviation.

Job Creation

The Revitalisation of the Manufacturing Sector programme aims to unlock investmentsinto strategic, underdeveloped and marginalised areas to stimulate industrial investmentsthat will drive efficiencies and competitiveness through sector development and support,industrial park regeneration and development, development facilitation, localisation ofproduction, local procurement practices, and the provision of economic infrastructure inorder to generate short, medium and long-term jobs.

The Ekurhuleni Community Skills Development, Job Creation and EconomicEmpowerment is a deliberate intervention to leverage its operational and capitalexpenditure budget for skills development, job creation and community empowermentthrough the following interventions:

Type A: By setting aside a percentage of Capex on infrastructure (eg EPWPand Vukuphile) and Opex to develop and mainstream PDI-owned businesses.

Type B: By setting aside a percentage of Opex to activate trade-in-services forcommunity (ie indigents) according to work packages.

Type C: By setting aside a percentage of Opex to activate a graduatedevelopment programme and experiential learning in partnership with localindustries.

Type D: By utilising the “Lungile Mtshali Poverty Alleviation Programme” toactivate neighbourhood development and job creation initiatives; and

Type E: By setting aside a percentage of Opex to activate youth developmentinitiatives for unemployed youth to gain work readiness and experience.

9. RATIO BETWEEN THE CAPITAL AND OPERATING BUDGET

The proportion between the Capital and Operating budgets is an issue that will bereceiving attention during the MTREF period with the aim of increasing the CapitalBudget.

22

In determining the ideal split between the two, a number of factors are considered:

The extent of flexibility in the budget (ie how much of the current budget canbe changed in the medium term);

Extent of grant funding received for the Capital Budget; and

Benchmarking with other metros.

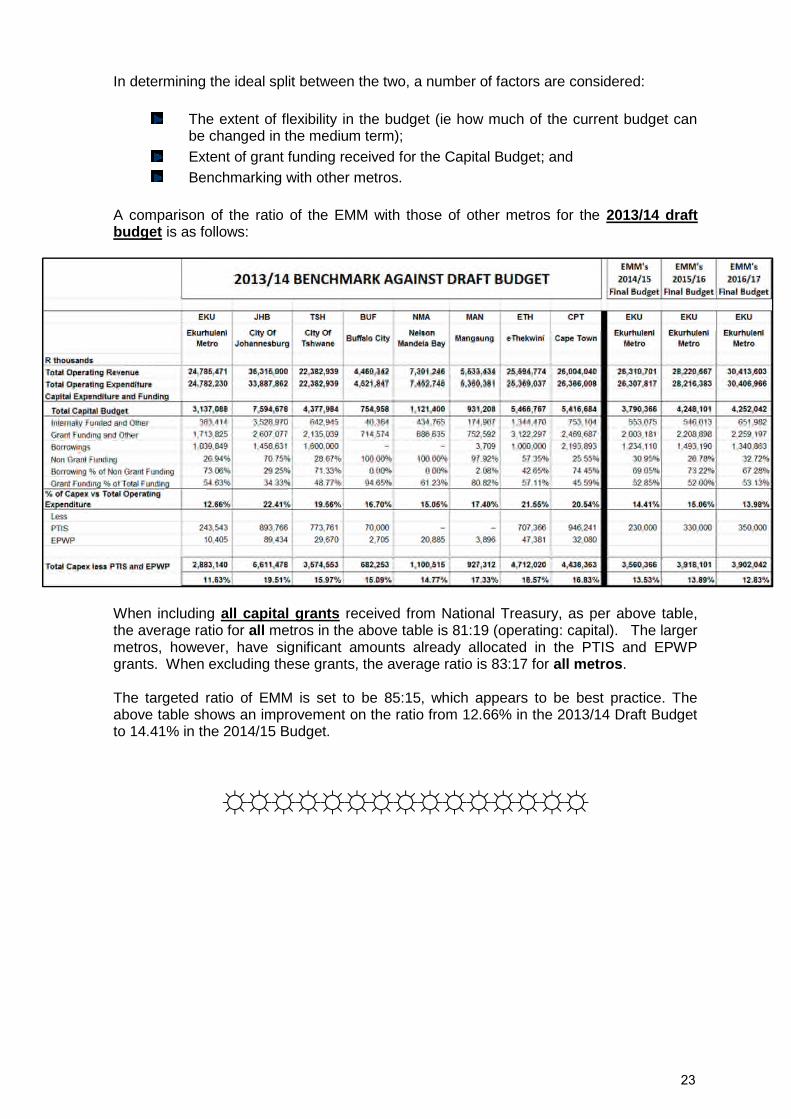

A comparison of the ratio of the EMM with those of other metros for the 2013/14 draftbudget is as follows:

When including all capital grants received from National Treasury, as per above table,the average ratio for all metros in the above table is 81:19 (operating: capital). The largermetros, however, have significant amounts already allocated in the PTIS and EPWPgrants. When excluding these grants, the average ratio is 83:17 for all metros.

The targeted ratio of EMM is set to be 85:15, which appears to be best practice. Theabove table shows an improvement on the ratio from 12.66% in the 2013/14 Draft Budgetto 14.41% in the 2014/15 Budget.

23

Page 0

Annexure F

EKURHULENI METROPOLITANMUNICIPALITY

PRICINGPOLICY

2014/1524

Page 1

CONTENTS

1. APPLICATION AND SCOPE ...........................................2

2. OBJECTIVES OF POLICY...............................................2

3. INTRODUCTION ..............................................................2

4. VARIOUS CATEGORIES OF PRICING...........................2

5. DETERMINATION OF POVERTY....................................3

5.1 PROPERTY RATES POLICY ........................................................ 4

5.2 INDIGENT SUPPORT POLICY ...................................................... 5

6. ASSESSMENT RATES PRICING....................................7

7. ENERGY PRICING.........................................................10

8. WATER AND SANITATION PRICING...........................12

8. SOLID WASTE PRICING...............................................14

25

Page 2

PRICING POLICY

1. APPLICATION AND SCOPE

The Pricing Policy is applicable to the Ekurhuleni Metropolitan Municipality as well as to allof the municipal entities of the Metro, being:

Brakpan Bus Company;

East Rand Water Care Company; and

Ekurhuleni Development Company, including Pharoe Park, Phase Two andLethabong Housing Institute.

The policy will be effective as from 1 July 2014.

2. OBJECTIVES OF POLICY

To ensure that pricing of services in the EMM is done in a financially sustainable andsocially responsible manner, and in doing so:

Determining cost reflective tariffs, as far as is possible;

Ensuring equitable pricing;

Ensuring affordability of basic services to the community;

To ensure compliance with the Municipal Systems Act; and

To ensure compliance with all tariff setting regulatory bodies.

3. INTRODUCTION

The municipality must have a balance between investments made in productive capacityversus investment made in social services. As such, a Pricing Policy Statement will beintroduced during the compilation of the 2013/14 – 2015/16 budget cycle. This policystatement must be read in conjunction with the following policy documents:

Budget Policy Statement;

Property Rates Policy;

Electricity Tariff Policy;

Free Basic Electricity Policy;

Water and Wastewater Tariff Policy; and

Solid Waste Tariff Policy.

4. VARIOUS CATEGORIES OF PRICING

The Ekurhuleni Metropolitan Municipality has a wide range of customers. The pricingpolicy is intended to derive at appropriate pricing and cross-subsidisation mechanisms tomeet the needs of the various customer groupings.

Whilst the categories of users guide pricing, the various tariff policies of the Metro willgovern the prices that will be payable for the various services and a person will not be

26

Page 3

entitled to a subsidy simply based on the category in which the person is deemed to fall.The exception will be the indigent category where a person will qualify for grants, rebatesand free basic services based on the indigent status as soon as the person has beenapproved as indigent and included in the formal indigents register of Council.

In terms of the approved Indigent Policy of Council, indigent relief will be granted to anapproved household where the:

a) combined household income of all occupants/ residents and/ or dependants residingon the property and are over the age of 18 years of age, is less than two (2) statemonthly pension grants, as amended by Minister of Finance from time to time;

b) account in respect of basic services and/or assessment rates, is held with Council inthe name of the applicant;

c) applicant is a South African citizen;d) the property is used for Residential purposes only; ande) owner of the property is an indigent applicant and municipal value of property does

not exceed maximum value as determined by Council’s assessment rates tariffpolicy.

In addition, residents of Ekurhuleni who do not have a formal municipal account but live inan informal settlement will also be registered as indigents. Whilst these residents will notbenefit from rebates related to assessment rates, free basic services will be extended tothese residents to the extent that infrastructure is available (ie provision of water toinformal settlements, collection of refuse from informal settlements, chemical toilets, etc).Other benefits that apply to registered indigents will also be extended to those in informalsettlements who are registered on the indigents register of Council.

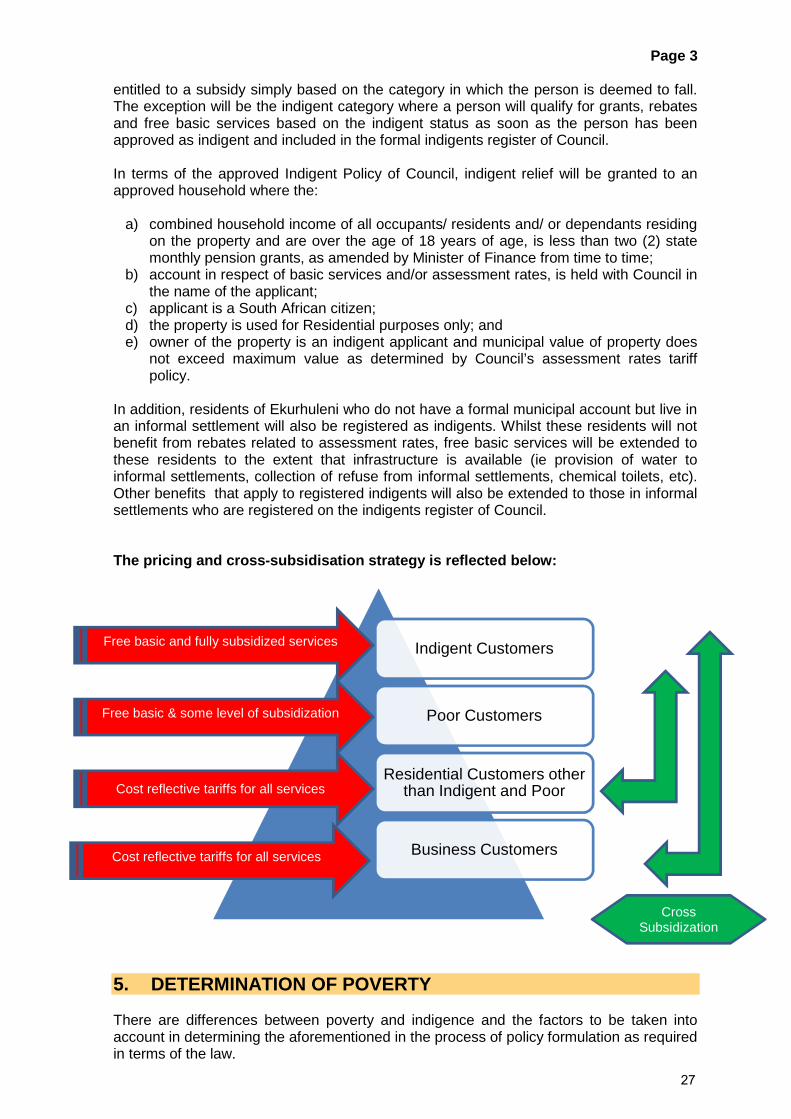

The pricing and cross-subsidisation strategy is reflected below:

5. DETERMINATION OF POVERTY

There are differences between poverty and indigence and the factors to be taken intoaccount in determining the aforementioned in the process of policy formulation as requiredin terms of the law.

Indigent Customers

Poor Customers

Residential Customers otherthan Indigent and Poor

Business Customers

Free basic and fully subsidized services

Free basic & some level of subsidization

Cost reflective tariffs for all services

Cost reflective tariffs for all services

CrossSubsidization

27

Page 4

How do we deal with scenarios where an individual is a beneficiary under the indigentpolicy of the municipality in circumstances where it is clear that the individual is above theset threshold to qualify for such benefits or discounts? For example, an individual wholives in a shack simply because it is his or her choice, or individuals with certain amenitieswhich ordinarily cannot be enjoyed by people falling within the threshold, as set out forqualification in the indigence scheme (such as DSTV in a shack or a flashy car etc).

The list below relates to legislative provisions, municipal policies and by-laws which arerelevant in dealing with this matter:

The Constitution of the Republic of South Africa Act 108 of 1996.

Water Services Act.

The Municipal Systems Act 32 of 2000.

The Municipal Property Rates Act 6 of 2004.

Framework for a Municipal Indigent Policy.

Electricity By-laws.

Water By-laws.

Policy on the Provision of Free Basic Services – water and wastewater.

Policy on the Provision of Free Basic Electricity.

Indigent Support Policy.

Property Rates Policy.

Section 229 of the Constitution authorises the municipality to impose rates on propertyand surcharges on fees for services provided by, or on behalf of, the municipality subjectto national legislation.

Section 3 of the Water Services Act states that everyone has a right of access to basicwater supply and basic sanitation.

Section 74 of the Municipal Systems Act provides that a municipal council must adopt andimplement a tariff policy on the levying of fees for municipal services, in accordance withprescribed principles in terms of the section.

Section 2(a) of the Municipal Property Rates Act says that a metropolitan or localmunicipality may levy a rate on property in its area.

Section 3(5) of the Municipal Property Rates Act states that any exemptions, rebates orreductions adopted by a municipality must comply and be implemented in accordancewith a national framework that may be prescribed after consultation with organised localgovernment.

It is worth mentioning at this stage that the above mentioned legislation does not definepoverty or indigent. Poverty is defined in Black’s Law Dictionary as “a condition wherepeople’s basic needs like food and shelter are not being met”. Indigent is defined in theaforementioned source as “a person who is needy and poor, or one who has no propertyto furnish him a living or anyone able to support him and to whom he is entitled to look forsupport”.

5.1 PROPERTY RATES POLICY

Paragraph 6 of the abovementioned policy provides for criteria for exemptions, reductionsand rebates in terms of which the following are to be taken into account:

28

Page 5

a) Indigent status of the owner of a property.b) Source of income of the owner of a property; andc) Social or economic conditions of the area where the owners of the property are

located.

Paragraph 7 lists the categories of owners of property for purposes of exclusions,exemptions, reductions, rebates and differential rating, namely, residential, indigentowners, child headed households, pensioners and disability grantees/medically boardedpersons and the like.

Paragraph 8.2 deals with indigent owners whereas 8.4 deals with pensioners and theconditions under which they may qualify for such reduction and a rebate.

5.2 INDIGENT SUPPORT POLICY

Paragraph 1 describes this policy as a legal imperative designed to ensure that aspects ofthe Constitution of South Africa relating to service delivery and access to basic servicesare realised. The policy arose as a result of continuous prevalence of indigence andpoverty within communities.

Paragraph 5 deals with the guiding principles for the formulation of the policy which, interalia, includes joint income of all household occupants in assessing the validity of indigentsupport application, punitive action to be taken in cases misuse of any support or grantand verification of information provided by the applicants.

This policy defines an “indigent person” as a person lacking the basic necessities of lifesuch as insufficient water, basic sanitation, refuse removal, health care, housing,environmental health, and supply of basic energy, food and clothing.

Paragraph 9 deals with the criteria for qualification for indigent support and under 9.1,indigent relief will be granted to an approved household where the:

a) Combined household income of all occupants/residents and/or dependentsresiding on the property and are over the age of 18 years, are less than two statemonthly pension grants.

b) Account in respect of basic services and/ or assessment rates, is held with Councilin the name of the applicant.

c) Applicant is a South African citizen.d) The property is used for residential purposes only, ande) Owner of the property is an indigent applicant and municipal value of the property

does not exceed the maximum value as determined by council’s assessment ratestariff policy.

Paragraph 9.1.3 states that indigent relief will not be granted where the applicant,household, occupants/residents and/or dependents residing on the property, as thecase may be, -a) Receive significant benefits or regular monetary income (own emphasis) that is

above the indigent qualification threshold.b) Applicant is not registered as consumer of services in the records of council, andc) Applicant owns more than one property, registered individually or jointly.

Paragraph 9.2 states that households will be deemed indigent if the property is used forResidential purposes only and municipal value of the property does not exceed R150000.

Paragraph 12(b), after the application form has been completed, an effective andefficient evaluation system must be used in order to verify the information furnished by

29

Page 6

the applicant (own emphasis) and to reach a decision within 21 days after the date onwhich the application was lodged.

In Paragraph 12(d), the onus is on the recipient of relief in terms of the policy to informthe Council of any change in his/her status or personal household circumstances.

Paragraph 12(f) states that all indigents should be re-evaluated after 36 months form thedate on which relief was authorized in order to assess the need for the continuation ofrelief in terms of the policy.

Paragraph 12(g) says appropriate disciplinary measures as prescribed, shall beimposed on people who misuse the system and provide incorrect information, R5000.00 penalty.

An attempt was made, unsuccessfully, to source case law specifically relevant to theissue at hand as a result of the fact that the courts seem to adopt the stance thatcommunities are indeed entitled to provision basic services, however, the determinationof same is left to the legislators to deal with, they also emphasise that the municipalitymust have policies in place to address these issues. (Leon Joseph & others vs. City ofJHB 2009 ZA CC 30).

It has now become clear that the municipality has in place requisite policies as requiredby the national legislation in order to comply with Constitutional imperatives. Theauthorities (legislation and policies) as stated above do not attempt to distinguishbetween indigence and poverty, however, it can be said that the circumstances statedtherein are all encompassing for as long as there compliance with the requirements.

The indigent support policy(Para 9) clearly states the circumstances under whichindividuals may qualify for the support programme and also deals with exemptions ofindividuals who would ordinarily qualify for inclusion in such programme under certaincircumstances. The focus of the policy appears to be on individual households in that itallows for applications to be evaluated based on individual circumstances of individualhousehold, this means that the mere fact that individuals are residents of the samecommunity does not automatically entitle all of them to benefit from the indigent supportscheme.

On closer scrutiny of the policy, it is discernible that the municipality must have in placeeffective and efficient evaluation systems to enable it to verify the information assubmitted by the applicants.

The policy (Para 12) also provides for punitive measures in instances where individualsare misusing the support programme to their undue benefit.

A view is held that, if the municipality has adequate measures in place to monitor theimplementation of this policy (from evaluating application to timeous review of theapplicants circumstances/compliance monitoring and /or changes thereof), the riskexposure due to misuse and malpractices in the implementation of this policy could besuccessfully curbed.

30

Page 7

6. ASSESSMENT RATES PRICING

The following principles will ensure that the municipality treats persons liable forassessment rates equitably in terms of the act:

Ratepayers with similar categories of properties will pay similar levels ofassessment rates.

The ability of specific categories of properties and/or categories of owners topay their assessment rates will be taken into account by the Council throughapplicable rebate policies.

In terms of section 229(2)(a) of the Constitution, a municipality may notexercise its power to levy rates on property in a way that would materially andunreasonably prejudice -

(a) national economic policies;(b) economic activities across its boundaries; or

(c) the national mobility of goods, services, capital or labour.

The determination of the tariffs and the levying of rates must allow the Councilto promote local, social and economic development.

Property rates are determined based on the categories of rateable properties which aredetermined according to actual use of the property irrespective of the permitted use interms of the Town Planning Scheme.

The Council has determined the following categories of property for purposes of rating:

residential properties:

industrial properties:

business and commercial properties:

farm properties used for:

agricultural purposes;

other business and commercial purpose;

residential purposes; or

purposes other than those specified above.

smallholdings used for:

agricultural purposes;

residential purposes;

industrial purposes;

business and commercial purposes; or

purposes other than those specified above.

state-owned properties;

municipal properties;

public service infrastructure;

privately owned towns serviced by the owner;

informal settlements;

mining and quarries;

vacant land;

protected areas;

properties on which national monuments are proclaimed;

31

Page 8

properties used for multiple purposes; and

places of worship.

The applicable tariffs relevant to various categories of properties will be influenced in twoways:

Pricing ratio of the category – Residential category forms the basis of ratiodetermination with differentiated ratios being applied to different categories ofproperties. As an example, industrial ratio is 2.5, meaning that the rate ofindustrial properties will be 2.5 times higher than the residential rate.Similarly, the ratio of farms is 0.25 meaning that the rate of farms will be aquarter of that of residential properties. The various ratios are contained in theproperty rates policy.

Rebates and exemptions granted in respect of category – various categorieshave rebates associated with the use of the property. Churches, as anexample, receive a 100% rebate, indigents receive a 100% rebate, andpensioners receive rebates based in first instance on pensioner status withadditional rebate of up to 100% depending on their household income. Inaddition, all residential properties have a legally compulsory exemption of atleast R15 000. This exemption can be increased to the discretion of Councilas part of its pricing policy.

In addition, the existing rebates offered in terms of Section 15(1) (b) of the Property RatesAct read with Council’s Property Rates Policy will remain in place for the 2014/15 financialyear.

The rebates are as follows:

Indigent Households – Owner of residential property, registered in terms ofcouncils approved Indigent Policy, be exempted from paying of property rates.

Child headed households – That a child headed household registered in termsof councils approved Indigent Policy, be exempted from paying of PropertyRates.

Age/Pensioners reduction, disability grantees and medically boarded persons– That in addition to the reduction in 4.1 above and subject to requirements asset out in councils Rates Policy, an additional reduction of R150 000 on themarket value of residential property owned by person older than 60 years ofage or registered as “Life right use” tenant in deeds office (Age/Pensionerreduction), disability grantees and medically boarded persons be granted.

Aged/Pensioners rebate, disability grantees and medically boarded persons –That in addition to the reduction in 4.1 and 4.4 above, an additional rebate begranted respect of sliding scale based on average monthly earnings.

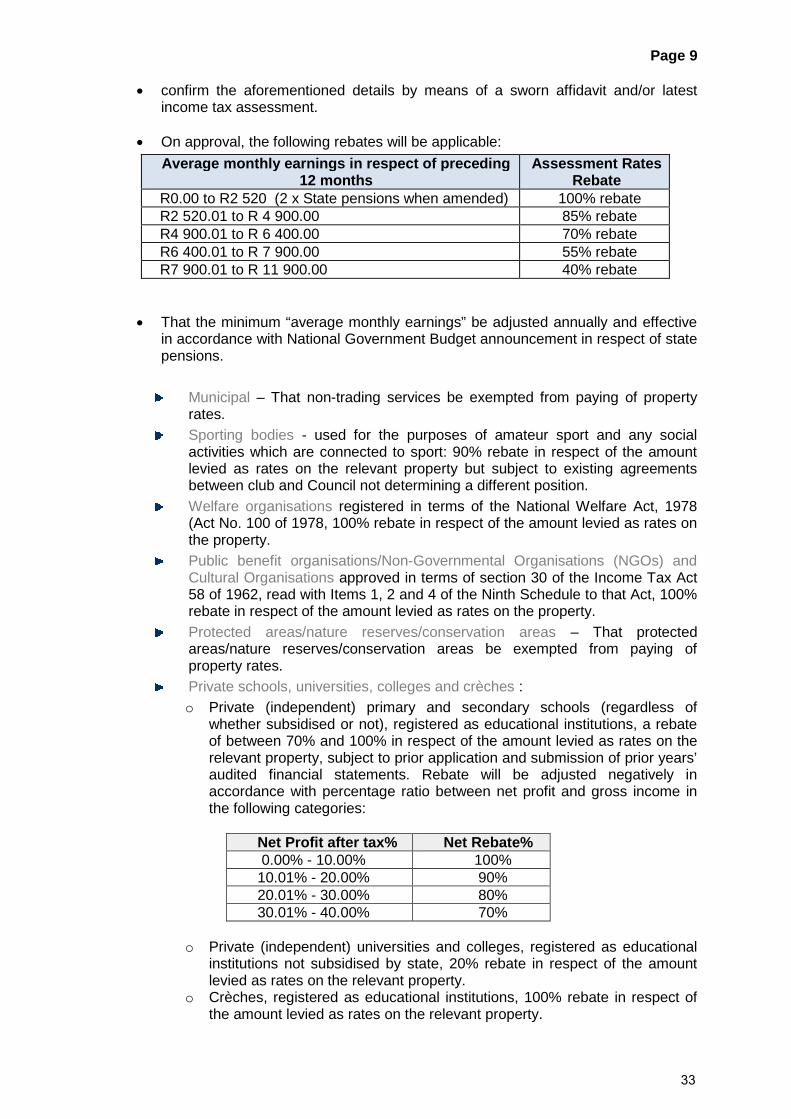

The applicant must: be the registered owner of the property or registered as “Life right use” tenant in