budget review fy19-saad · budget positive for stock market corporatetaxreducedby 1%; supertax...

TRANSCRIPT

April 28, 2018 REP‐057

Pakistan Equity| Economy

20182018 2019201920182018‐‐20192019

FY19 Budget ReviewAmbitious Budget Ahead of The Elections

Topline Researchh@t li k

Best Local Brokerage HouseBrokers Poll 2011 14 2016 [email protected]

Tel: +9221‐3530‐3338‐40Topline Securities, Pakistan www.jamapunji.pk

Brokers Poll 2011-14, 2016-17

Best Local Brokerage House 2015-16

Table of Contents

Key Highlights of FY19 Budget -------------------------------------- 3

Budget Positive for Stock Market -------------------------------------- 4

Sector Impact and Analysis -------------------------------------- 8

Stock Market Outlook -------------------------------------- 15

Topline Universe - Top Picks -------------------------------------- 16Topline Universe Top Picks 16

Budget Highlights -------------------------------------- 17

Key Measures For Real State -------------------------------------- 21

Other Relief Measures -------------------------------------- 22

Honda Atlas Cars (HCAR) 2

Other Tax Measures -------------------------------------- 23

Pakistan Budget Review

Key Highlights of FY19 Budget

PML‐N Govt. proudly unveiled its 6th budget yesterday with total outlay of Rs5.9tn (+11% YoY over revised estimate of

Rs5.3tn) for FY19. We are of the view that FY19 Federal budget seems highly populist with a series of relief measures,

which will likely bode well for the stock market in the short run.

The Govt. announced major tax relief for salaried class in‐line with the recently announced tax relief package, exempting

income tax to individuals with annual salary of up to Rs1.2mn. The Govt. also announced that corporate tax rate to be

gradually reduced by 1% to 25% (from 30%) during the next 5 years, which would result in reduced corporate tax rate of

29% for FY19 from 30%.

The Govt. also reiterated its stance on Amnesty Scheme as undeclared asset can be regularized till Jun 30, 2018. In a big

policy change, state is also given the power to purchase land & property at 100% of the declared value within six‐months

of its registration. Other contours of the Amnesty Scheme including regularization of domestic and foreign assets have

also been made part of the finance bill. Regularization of unaccounted for wealth will be positive for stock market.

Other key highlights of the budget include: 1) super tax to be reduced by 1% every year (currently it is 3% for non‐

banking companies & 4% for banks), 2) removal of tax on bonus shares and 3) reduction of GST on all Fertilizer products

among others.

Sector wise Consumer, Textile and Fertilizer are expected beneficiaries of budgetary measures.

Honda Atlas Cars (HCAR) 3Pakistan Budget Review

d d d

Budget Positive for Stock Market

Tax removed on Bonus Dividends ‐ PositiveThe govt. has announced removal of tax on bonus shares issue, which is now currently at 5% of market value.This is positive as ever since the imposition of this tax in FY15 budget, there has been a major decline in

f b h b li d fi I Y16 d Y1 l ll d d l 89announcement of bonus shares by listed firms. In FY16 and FY17 total tax collected amounted to only Rs589mnand Rs1bn respectively, as per PSX calculations. PSX further estimates that total bonus issues in terms of valuereduced to Rs4.4bn during Jan’17‐Jan’18 from Rs19bn in FY14. Similarly, number of companies issuing bonush d li d t 35 d i J ’17 J ’18 f 71 i FY14 lt f th th kishares declined to 35 during Jan’17‐Jan’18 from 71 in FY14 as a result of the same measure, as per the workingsmade by PSX.

Select Companies that used to pay high Bonus DividendsCompany Name Symbol Company Name SymbolCompany Name Symbol Company Name SymbolAllied Bank ABL IGI Holdings IGILArif Habib Corp AHCL Mari Petroleum MARIAskari Bank AKBL MCB Bank MCBAtlas Honda ATLH Meezan Bank MEBAttock Cement ACPL National Bank of Pakistan NBPBank Al Habib BAHL Pakistan Petroleum PPLEngro Corp. ENGRO Pakistan State Oil PSOFauji Fertilizer FFC Sui North SNGPGlaxoSmithKline GLAXO Thal Limited THALL

Honda Atlas Cars (HCAR) 4

GlaxoSmithKline GLAXO Thal Limited THALLHabib Bank HBLSource: Topline Research

Pakistan Budget Review

Budget Positive for Stock Market

Corporate Tax reduced by 1%; Super Tax will end gradually ‐ PositiveThe Govt. has proposed to reduce the corporate tax rate to 25% (from current 30%) during the next 5 years. For

FY19, corporate tax rate would be reduced by 1% to 29%. Further, Super Tax is proposed to be reduced by 1%

every year. Currently, it is 3% for non‐banking companies and 4% for banking companies.

The above is positive as we had assumed corporate tax rate of 30% in our forecasts. However, we had not

incorporated super tax in our estimates. Given the above, non‐banking companies in our coverage will face a

negative impact on earnings of around 1% while banking companies will be negatively impacted by 2% for FY19.

Rationalization of tax on Brokers ‐ PositivePreviously, Advance Withholding tax (WHT) collected from stock brokers was 0.02% and was a final tax liability.

The WHT is now being made adjustable, which would lead to lower taxes for brokers and is positive for the

market.

Real Estate Investment Trusts (REITs) dividends subject to lower tax rate ‐ PositiveReal Estate Investment Trusts (REITs) shareholders have been provided tax relief as REIT dividends are nowsubject to tax of 7.5% as compared to previous 12.5%. However, profit and gains accruing on sale of immovableproperties to REIT (Development & Rental) remain taxable.

Honda Atlas Cars (HCAR) 5Pakistan Budget Review

d d d d d f l

Budget Positive for Stock Market

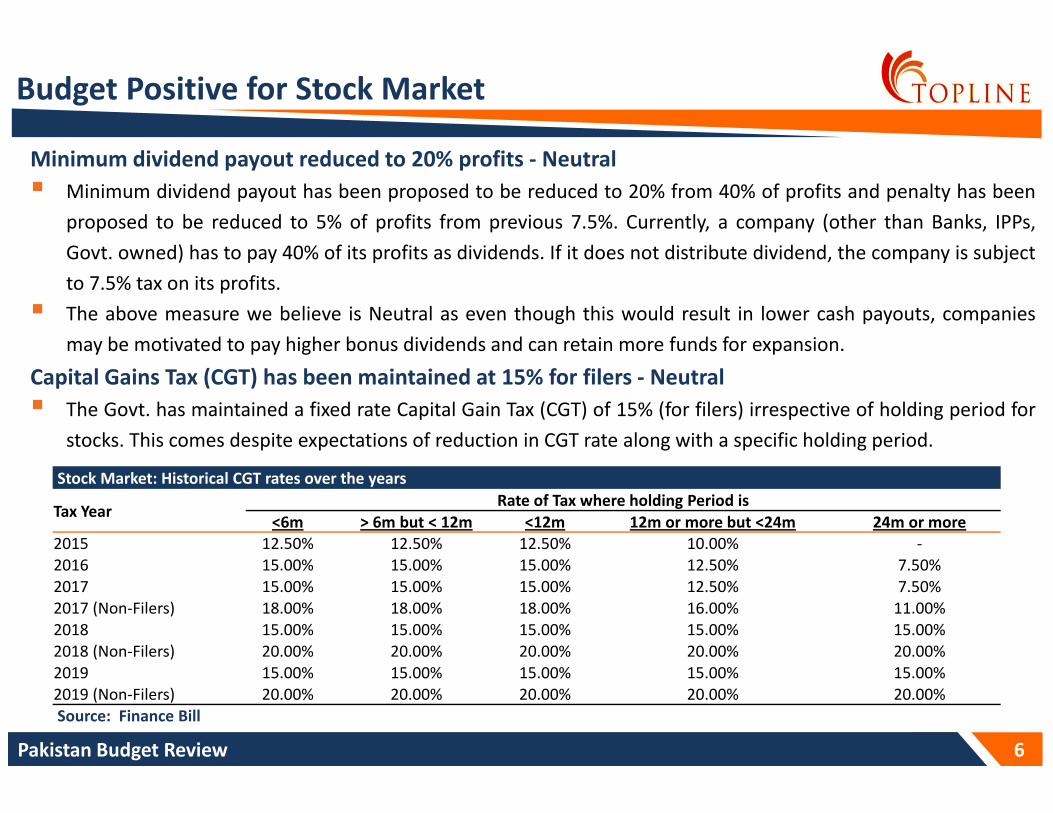

Minimum dividend payout reduced to 20% profits ‐ NeutralMinimum dividend payout has been proposed to be reduced to 20% from 40% of profits and penalty has beenproposed to be reduced to 5% of profits from previous 7.5%. Currently, a company (other than Banks, IPPs,Govt owned) has to pay 40% of its profits as dividends If it does not distribute dividend the company is subjectGovt. owned) has to pay 40% of its profits as dividends. If it does not distribute dividend, the company is subjectto 7.5% tax on its profits.The above measure we believe is Neutral as even though this would result in lower cash payouts, companiesmay be motivated to pay higher bonus dividends and can retain more funds for expansion.

Capital Gains Tax (CGT) has been maintained at 15% for filers ‐ NeutralThe Govt. has maintained a fixed rate Capital Gain Tax (CGT) of 15% (for filers) irrespective of holding period forstocks. This comes despite expectations of reduction in CGT rate along with a specific holding period.

Stock Market: Historical CGT rates over the years

Tax YearRate of Tax where holding Period is

<6m > 6m but < 12m <12m 12m or more but <24m 24m or more 2015 12.50% 12.50% 12.50% 10.00% ‐2016 15 00% 15 00% 15 00% 12 50% 7 50%2016 15.00% 15.00% 15.00% 12.50% 7.50%2017 15.00% 15.00% 15.00% 12.50% 7.50%2017 (Non‐Filers) 18.00% 18.00% 18.00% 16.00% 11.00%2018 15.00% 15.00% 15.00% 15.00% 15.00%2018 (Non‐Filers) 20.00% 20.00% 20.00% 20.00% 20.00%

Honda Atlas Cars (HCAR) 6Pakistan Budget Review

2019 15.00% 15.00% 15.00% 15.00% 15.00%2019 (Non‐Filers) 20.00% 20.00% 20.00% 20.00% 20.00%Source: Finance Bill

d d d ll

Budget Positive for Stock Market

Tax Credit on expansion activities extended till 2021 ‐ PositiveIn order to incentivize companies to make further investment/BMR, they are eligible for up to 10% tax credit on

amount invested up till 2021. This tax incentive was scheduled to expire in FY19. This will be positive for the

economy and listed companies and it will result in higher economic activity and industrialization, we believe.

Minimum turnover tax maintained at 1.25% ‐ NeutralFederation of Pakistan Chambers of Commerce & Industry (FPCCI) had urged that upcoming budget should

include reduction of turnover to 1% (from 1.25%) and that loss making enterprises be exempt from such a tax.

However, no such relief was provided in the budget.

Group taxation/Inter corporate dividend tax maintained ‐ NeutralIn order to promote group formation and consolidation in Pakistan, it was recommended by business

community to exempt group companies (provided the holding company holds 55% or more stake in one of the

listed companies or in case of no listed company in the group, the holding company shall hold 75% or more

stake) from paying tax on inter‐corporate dividend. However, the above measure was not proposed in this year’s

budget.

Honda Atlas Cars (HCAR) 7Pakistan Budget Review

Sector Impact and Analysis

Fertilizer | PositiveTextile | PositiveConsumer | Positive E&Ps | Neutral

OMCs | NeutralBanks | Neutral Gas Distribution | Neutral Power | Neutral

Cement | Neutral to Negative Steel | Neutral to NegativeTobacco | Neutral to Negative Auto | Negative

Honda Atlas Cars (HCAR) 8Pakistan Budget Review

Sector Impact and Analysis

R d ti f C t D t (CD) f 10% t 5% i t d ili l t i l t l h t PAEL b iPositiveConsumer Reduction of Customs Duty (CD) from 10% to 5% on imported silicon electrical steel sheets. PAEL beingthe leading transformer manufacturer will likely benefit from this.

10% Regulatory Duty (RD) imposed on Completely Knock Down (CKD) and Semi Knock Down (SKD) kitsfor home appliances. This will negatively impact PAEL as home appliances kits are being used for AC’s,

t di d i H th ill lik l th i t

PositiveConsumer

water dispenser and microwave ovens. However, the company will likely pass on the impact.

CD exemption on bovine semen and decline in tax on preparations for making animal feed to 5% from10% previously could bode well for dairy producers such as NESTLE, EFOODS, FFL etc.

CD on specified equipment used in the cinema industry reduced to 3%. Sales tax on import of 19 itemsof cinematographic equipment reduced to 5% for 5 years. This should bode well for production houseslike HUMNL, we believe.

The Govt. has decided to give tax relief to salaried class in the budget. We believe that lower incometax rates should increase consumers’ spending power, thereby leading to higher sales for consumerp g p y g gfirms.

PositiveTextile Continuation of zero rating regime, long term financing at 5% and export refinancing at 3% is positivefor textile sector. Additionally, new export package is also on cards.

G i hi b d h d l d hl b i l i iGovernment in this budget has assured to clear exports dues on monthly basis, resulting intoimproved cash flows of the companies.

Moreover, reduction of sales tax on LNG by 5% to 12% is likely to reduce cost of doing business of thecompanies.

Honda Atlas Cars (HCAR) 9

There was no development for removal of minimum turnover tax for loss making companies, keepingintact the taxation burden on textile companies, especially spinners.

Pakistan Budget Review

Sector Impact and Analysis (contd.)

f l d ll f l d f l dPositi eFertili er Uniform sales tax is imposed on all fertilizer products at 3% from earlier 5% on urea and 3.5%‐10% onothers (DAP, NP, NPK etc.). This is likely to reduce prices of all products (except urea) in range of Rs30‐150 per bag, resulting into higher volumetric sales, we believe.

Removal of cash subsidy on Urea (Rs100/bag) by the federal government is likely to bode well for the

PositiveFertilizer

y ( / g) y g yfertilizer manufacturers, as through this subsidy manufacturers were contributing Rs106/bag, whilegovernment was contributing Rs100 per bag (total cash: Rs206/bag). To maintain their currentprofitability, manufacturers have to increase urea prices by minimum of Rs75‐80/bag. To note, cashsubsidy created cash constraints for the manufacturers As per Dec 2017 subsidy receivables ofsubsidy created cash constraints for the manufacturers. As per Dec 2017, subsidy receivables ofmanufacturers stood at ~Rs19bn (EFERT Rs7bn, FFC Rs7bn, FFBL Rs3bn, and FATIMA Rs1.5bn).

Input sales tax on feed gas is reduced to 5% vs. 10% earlier. On the other hand output tax is reduced to3%. This will continue sales tax refunds problems for the manufactures. As of Dec 2017, sales taxrefunds of the fertilizer manufacturers stood at Rs10bn (FFC Rs5.2bn, FATIMA Rs1.7bn, EFERT Rs1.5bn,and FFBL Rs1.5bn).

Other developments, like higher agricultural credit, and reduction of GST on agri machinery are likelyt i h i f th f Whil ithd l f l t LNG i lik l t dto improve purchasing power of the farmers. While withdrawal of sales tax on LNG is likely to reducecost of doing business for LNG based manufacturers (Fatima Fert and Pak Arab).

NeutralE&Ps The Govt. has set dividend income target of Rs25bn (Rs8.6/share) from Oil & Gas DevelopmentCompany limited (OGDCL) Similarly it has set target Rs13bn (Rs9 8/share) from Pakistan Petroleum

Honda Atlas Cars (HCAR) 10

Company limited (OGDCL). Similarly, it has set target Rs13bn (Rs9.8/share) from Pakistan PetroleumLimited (PPL).

Pakistan Budget Review

Sector Impact and Analysis (contd.)

F 2019 G h i d f 3% B k hi h ill d b 1%Banks Neutral For tax year 2019, Govt. has imposed super tax of 3% on Banks which will come down by 1% everyyear and will eventually be removed. We had not assumed super tax in our models so imposition ofthe same could impact our bank’s earnings by 3%/2%/1% for 2018‐20.

All non‐cash banking transactions of worth over Rs50,000 are being charged at 0.6% for non‐filers. This

Banks Neutral

rate is to be reduced 0.6% to 0.4%. This will have the positive impact for deposit mobilization of banks.

In order to promote microfinance banks, profit on debt derived by non‐profit organizations frommicro‐finance banks shall also qualify as income eligible for 100% credit under section 100C of theIncome Tax Ordinance 2001 This exemption is currently also available on profit on debt fromIncome Tax Ordinance, 2001. This exemption is currently also available on profit on debt fromscheduled banks.

Pakistan Mortgage Refinance Company (PMRC) is an initiative of the SBP and has been established forpromoting affordable housing finance for the middle and low income groups. PMRC has beenexempted from income tax and income derived from investors from PMRC bonds issued to refinancethe residential mortgage market. This bodes well for overall Mortgage Financing.

Removal of tax on bonus will lead to banks issuing a mix of bonus and cash dividend.

NeutralGas Distribution

Reduction in taxation on LNG also bodes well for cash flows of Gas distribution companies which aremandated to supply RLNG to industries.

Govt. expects to receive dividend income of Rs1.5bn (Rs7/share) from Sui Northern Gas Pipeline(SNGP) which is also in line with our estimate for FY19 From Sui Southern (SSGC) government

Honda Atlas Cars (HCAR) 11

(SNGP), which is also in line with our estimate for FY19. From Sui Southern (SSGC), governmentexpects to receive Rs500mn (Rs0.6/share). We do not expect SSGC to announce any cash dividends forFY19.

Pakistan Budget Review

Sector Impact and Analysis (contd.)

G t i th fi bill tifi d i if P t l L t ll t l d t fOMCs N t l Govt. in the finance bill notified maximum uniform Petroleum Levy rate on all petroleum products ofRs30/ltr. We believe this is notified just to increase the maximum limit of levy that can be imposed infuture instead of the fixed Rs8‐12/ltr on HSD/MOGAS, currently. We do not expect this to necessarilylead to higher pump prices & lower fuel demand as this is a government measure to adjust fuel prices

OMCs Neutral

in future using Petroleum levy.

With expected deregulation of diesel, tax on dealers margin shall now be collected on ex‐depot saleprice of HSD (excluding dealers margin) at the rate of 0.5% from a filer and 1% from a non‐filer. Thiscould have a marginal impact on OMC dealers but OMCs and end consumers are not anticipated tocou d a e a a g a pact o O C dea e s but O Cs a d e d co su e s a e ot a t c pated towitness any impact.

Govt. expects to receive Rs1.5bn (Rs22/share) in the form of dividend income from PSO in FY19.

Sales tax rate on import of LNG is proposed to be reduced from 17% to 12%. Furthermore, valueaddition tax of 3% chargeable on import of LNG will also be waived off. We believe this could lead to~6% drop in LNG notified prices which bodes well for the cash flows of PSO.

Govt. has given 20‐year tax holiday for setting up a deep conversion refinery with capacity of over100k barrels per day This will benefit PARCO refinery project however listed companies may not

Questions related to surging circular debt remains unanswered in this budget. However, subsidyamount to Wapda/PEPCO is increased to Rs134bn for FY19 budget vs. revised FY18 target of Rs82bn.

Power Nuetral

100k barrels per day. This will benefit PARCO refinery project however listed companies may notbenefit as other refineries may not be expanding at such scale.

Honda Atlas Cars (HCAR) 12

p g g

Pakistan Budget Review

Sector Impact and Analysis (contd.)

N t l tC t f l h b d d f h ll l k l fNeutral toNegative

Cement CD on import of coal has been decreased to 3% from present 5%. This will likely improve earnings ofcement companies by 2‐3%, we estimate.

WHT has been proposed to be reduced from 5.5% to 4%. This will have a cash flow impact on cementproducers.p

Tax credits under Sections 65B, 65D & 65E for setting up manufacturing unit and BMR has beenextended up to June 30, 2021 from present June 30, 2019. This will have positive implications forcement producers (LUCK, DGKC, POWER, CHCC, PIOC, GWCL, KOHC, MLCF and BWCL), which are goingi t iinto expansion.

Total size of Federal Public Sector Development Program (PSDP) has been proposed at around Rs1tn,up by 37% YoY against revised estimates of PKR 750bn in Budget FY18.

Sales tax on LNG import has been reduced from 17% to 12% This will be positive for North basedSales tax on LNG import has been reduced from 17% to 12%. This will be positive for North basedproducers with Captive Power Plant (CPP) like DGKC, MLCF and LUCK.

Federal Excise Duty (FED) has been increased to Rs1.5/kg, up 20% which will have impact of aroundRs15/bag (Rs13/bag FED impact and Rs2/bag sales tax impact as sales tax is levied on top of FED). Webelieve that producers will partially be able to pass on the impact as North cement prices are alreadyunder pressure while South manufacturers have also little room to increase prices due to upcomingcapacities. While this is negative in the short run, robust demand going forward might enablemanufacturers to fully pass on the impact.

Honda Atlas Cars (HCAR) 13Pakistan Budget Review

Tobacco FED on locally produced cigarettes has been proposed to be increased across all three tiers. This willnegatively affect the volumetric sales of listed tobacco producers like PAKT and KHTC, we believe.

Negative

Sector Impact and Analysis (contd.)

G h d hik i l f l l f f R 10 5/K hN t l tSt l Government has proposed hike in sales tax for long steel manufacturers from Rs10.5/Kwh toRs13/Kwh. We believe, manufacturers will gradually pass on the impact of hike in sales tax by risingprices by Rs1800‐2200 per ton.

Moreover, allocated development expenditure of Rs1tn will bode well in terms of higher volumetric

Neutral toNegative

Steel

Non‐filers shall not be permitted to purchase new motor vehicles manufactured in Pakistan or newimported vehicles. This could be negative for local automobile assemblers as car sales could initially bei t d

NegativeAutos

demand of steel products used in construction/infrastructure development.

impacted.

Govt. has proposed exemption of 16% CD on charging stations for electric vehicles. Custom duty hasbeen reduced from 50% to 25% and RD of 15% on Electric Vehicles has been exempted. Furthermore,CD on kits of electric vehicle are reduced from 50% to 10%. This will not have any major impact onlocal automobile manufacturers.

Increase of CD on aluminum auto parts scrap from 30% to 35% is also proposed which could lead tohigher cost of production.

Carbon Black rubber grade is importable at 20% CD which is a raw material for manufacturing of tyres.It is proposed that CD may be reduced from 20% to 16% on import of Carbon Black rubber grade. Thisbodes well for the tyre Manufacturers.

Reduced rate of GST on Tractors has been continued for FY19 which bodes well for the tractor industry.

Honda Atlas Cars (HCAR) 14

Reduced rate of GST on Tractors has been continued for FY19 which bodes well for the tractor industry.

Pakistan Budget Review

Stock Market Outlook

Short term rally likely – Market on average has gained around 2-3% post budgetLower tax on bonus shares and reduction on tax on brokers may trigger a short term rally post Budget.

Historically, since 2012, the market has rallied on average by 2‐3% in the month after the budget (this excludes

last year that had one off MSCI upgrade).

After that, local politics (Former Prime Minister Nawaz Sharif’s court cases), success of recently announced

amnesty scheme and external account situation will likely dictate market trend.

We continue our liking for select Banks, E&Ps and Textile which will benefit from expected hike in interest rates,

currency devaluation and higher oil prices.

Sector wise Consumer, Textile and Fertilizer are expected beneficiaries of budgetary measures.

Market to trade in the range of 8.5-9.0x – 50,000pts target maintainedWe maintain our KSE‐100 index target of 50,000 pts by Dec 2018, which we had earlier forecasted (please refer

to our strategy report titled, ‘Pakistan Market Outlook’ dated Dec 20, 2018). Since our report, KSE‐100 index has

rallied 19% (14% in US$).

We believe that the market will likely trade in the PE range of 8.5‐9.0x, as mentioned in our above stated

strategy report. Market is currently trading at 2019F PE of 8.3x, based on our sample companies.

Honda Atlas Cars (HCAR) 15Pakistan Budget Review

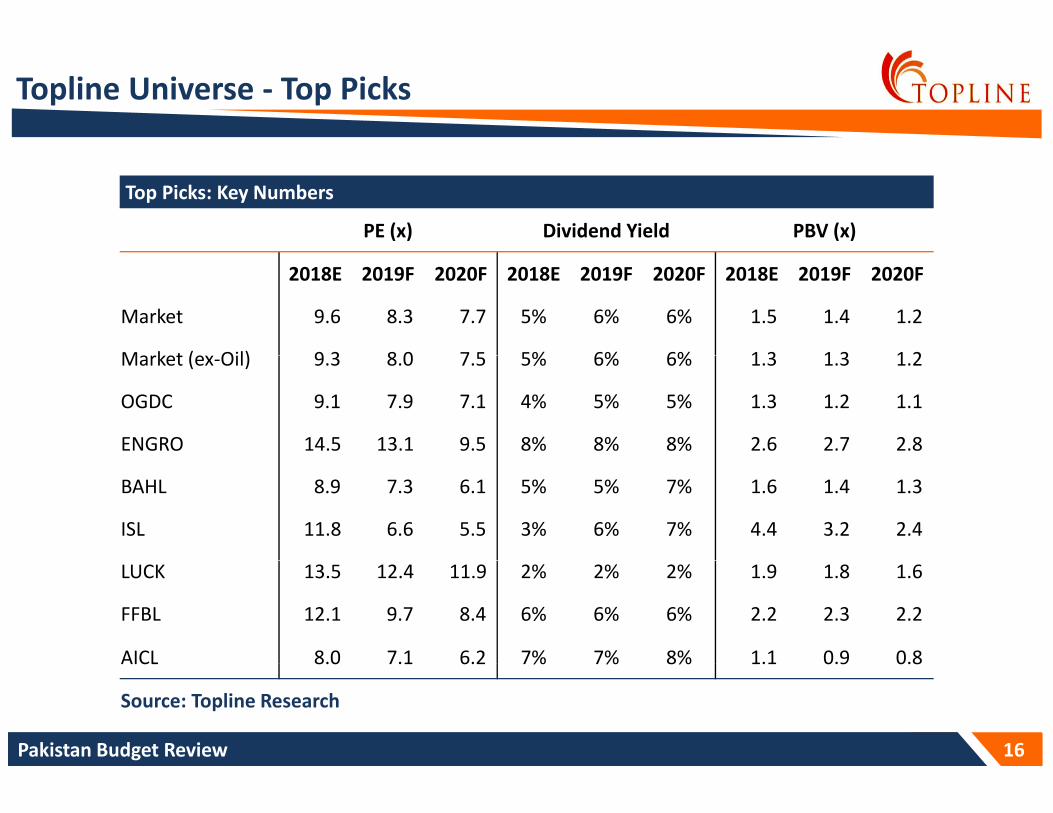

Topline Universe ‐ Top Picks

Top Picks: Key Numbers

PE (x) Dividend Yield PBV (x)

2018E 2019F 2020F 2018E 2019F 2020F 2018E 2019F 2020F

Market 9.6 8.3 7.7 5% 6% 6% 1.5 1.4 1.2

Market (e Oil) 9 3 8 0 7 5 5% 6% 6% 1 3 1 3 1 2Market (ex‐Oil) 9.3 8.0 7.5 5% 6% 6% 1.3 1.3 1.2

OGDC 9.1 7.9 7.1 4% 5% 5% 1.3 1.2 1.1

ENGRO 14.5 13.1 9.5 8% 8% 8% 2.6 2.7 2.8

BAHL 8.9 7.3 6.1 5% 5% 7% 1.6 1.4 1.3

ISL 11.8 6.6 5.5 3% 6% 7% 4.4 3.2 2.4

LUCK 13.5 12.4 11.9 2% 2% 2% 1.9 1.8 1.6

FFBL 12.1 9.7 8.4 6% 6% 6% 2.2 2.3 2.2

AICL 8.0 7.1 6.2 7% 7% 8% 1.1 0.9 0.8

Honda Atlas Cars (HCAR) 16

AICL 8.0 7.1 6.2 7% 7% 8% 1.1 0.9 0.8

Source: Topline Research

Pakistan Budget Review

Budget Highlights

T l b d l f FY19 i i d R 5 9 (11% hi h h h l ’ b d l f R 5 3 ) hi hTotal budget outlay for FY19 is estimated at Rs5.9tn (11% higher than the last year’s budget outlay of Rs5.3tn), whichseems optimistic in light of the current macroeconomic situation.The Govt. is proposing Federal PSDP of Rs1tn for FY19, as compared to revised PSDP for FY18 of Rs750bn (as againstinitial target of Rs1tn). Out of the total Federal PSDP of Rs1tn, Rs230bn would be self financing by theg ) , g ycorporation/authorities and Rs800bn would be provided through budget FY19.The Tax Reform Package announced by PML‐N govt. in Apr 2018 included significant relief for the salaried class, whichhas been included in budget proposal. The govt. has proposed maximum tax rate of 15% for annual income in excess ofR 4 8 P i l i 30% H hi i d h i iRs4.8mn. Previously, maximum tax rate was up to 30%. However, this measure is expected to have negative impact onrevenues of Rs90‐100bn (~2% of total revenue).

Tax relief on salaried classRsRs

Monthly Income 150,000 300,000 500,000 Annual Income 1,800,000 3,600,000 6,000,000 Tax as per currently applicatble rates 137,000 497,000 1,147,000 T i d 30 000 180 000 360 000

Total Govt. revenue is projected at Rs5.7tn, which is up 13% over last year amount of Rs4.9tn. FBR Revenue for FY19 is

Tax as per revised rates 30,000 180,000 360,000 Savings 78% 64% 69%Source: Topline Research

Honda Atlas Cars (HCAR) 17

p j p yanticipated at Rs4.4tn, which will be 12.8% higher than Rs3.9tn expected for FY18. We believe that the govt. willpotentially struggle to achieve this target.

Pakistan Budget Review

Budget Highlights (contd.)

Additional tax revenues are expected to be collected from new tax measures to the tune of Rs93bn while the tax

relief is of Rs180bn, resulting in a revenue shortfall of Rs100bn, we estimate.

Current Expenditures for FY19 is expected to clock in at Rs4.8tn, which is 11.2% higher than the estimate of

Rs4.3tn for FY18.

Defense budget is estimated to increase by 10.1% at Rs1.1tn, whereas debt servicing is expected to increase by

6.2% to Rs1.6tn.

Govt. is proposing to set subsidy target of Rs175bn for FY19 as against Rs148bn for FY18 (up 18.2% over last

year). Subsidy for power sector has been increased to Rs149bn compared to Rs115bn last year, up 29.6%.

Key Economic IndicatorsKey Economic Indicators

FY14A FY15A FY16A FY17A FY18E FY19BE

Real GDP growth (%) 4.1% 4.0% 4.6% 5.4% 5.8% 6.2%Inflation (%) 8.6% 4.6% 2.9% 4.3% 4.5% 6.0%Fiscal Deficit (%) 5.5% 5.3% 4.6% 5.8% 5.5% 4.9%Current Account as % of GDP ‐1.3% ‐1.0% ‐0.6% ‐2.7% ‐4.9% ‐3.7%FX reserves (US$bn) 14.0 18.2 23.1 21.0 11.0 15.0

$

Honda Atlas Cars (HCAR) 18Pakistan Budget Review

Remittances (US$bn) 15.8 17.9 19.9 20.0 20.9 20.0Source: MoF, PBS, SBP

Budget Highlights (contd.)

Th t i t ti b d t d fi it f 4 9% f FY19 d t 5 5% t d f th t fi l Thi iThe govt. is targeting budget deficit of 4.9% for FY19 as compared to 5.5% expected for the current fiscal year. This isclose to our estimate of 5% and will likely be achieved by announcement of further tax measures post budget andcontainment of expenses.Other than tax measures, further currency devaluation and increase in interest rates are expected to slow down GDPgrowth to less than 5% during the next few years as against the govt. target of 6.2% for FY19 compared to 5.79% (13‐Year high) in FY18. We expect next year’s GDP growth to be at 4.6%.Inflation has been targeted at 6% for next fiscal year compared to our estimate of 7% due to further devaluation. ForFY18, inflation is expected to be around 4.25%. Current Account Deficit (CAD) is projected at US$12.5bn, which is in‐lineFY18, inflation is expected to be around 4.25%. Current Account Deficit (CAD) is projected at US$12.5bn, which is in linewith our estimates.

Subsidy as % of GDP3.0%

1.5%

2.0%

2.5%

0.0%

0.5%

1.0%

11A

12A

13A

14A

15A

16A

17A

18E

9BE

Honda Atlas Cars (HCAR) 19Pakistan Budget Review

Source: Pakistan Economic Survey/Govt. Estimates

FY1

FY1

FY1

FY1

FY1

FY1

FY1

FY1

FY19

Budget Highlights (contd.)

Budget at a Glance

Rsbn FY17A FY18BE FY18E FY19BETax Revenue 3,969 4,331 4,147 4,889FBR Taxes 3,361 4,013 3,935 4,435Non Tax Revenue 967 980 845 772Gross Revenue Receipts 4 937 5 310 4 992 5 661Gross Revenue Receipts 4,937 5,310 4,992 5,661Less: Provincial Share 2,428 2,384 2,316 2,590Federal Revenue 2,508 2,926 2,676 3,070Current Expenditure 3 494 3 477 3 870 4 179Current Expenditure 3,494 3,477 3,870 4,179Development & Net Lending 867 1,276 1,063 1,068Federal PSDP 733 1,001 750 800Total Federal Expenditure 4,362 4,753 4,933 5,246Total Federal Expenditure 4,362 4,753 4,933 5,246Provincial Surplus & statistical discrepancy 10 347 365 286Overall Fiscal Deficit 1,843 1,479 1,891 1,890 Fiscal Deficit as % of GDP 5.8% 4.1% 5.5% 4.9%

Honda Atlas Cars (HCAR) 20Pakistan Budget Review

Source: Ministry of Finance

FY19 Budget – Key Measures For Real State

The measures for real estate announced in the Tax Relief Package by PML‐N earlier in the month have been

presented in the budget and made part of the Finance Bill. This will bode well for regularization of the real

estate where significant portion of value is unaccounted for.

Property transactions shall be recorded at the value declared by the buyer and the seller.

Property rates notified by FBR (for the purpose of collection of taxes on sale purchase of property) and DC rates

are to be abolished.

At the Federal level, 1% adjustable advance tax from the purchaser on the declared value shall be collected and

this tax shall replace the existing withholding tax on sellers and purchasers of property.

Non‐filers shall not be permitted to purchase property having declared value exceeding Rs4mn.

Provinces shall be requested to abolish the provincial rates for the collection of stamp duty (commonly known

as DC rates) and to collect a total of 1% tax under stamp duty and capital value tax on the value declared by the

buyer and the seller of property.

In order to deter under‐declaration and consequent loss of revenue, FBR shall have the right to purchase any

property within six months of registration by paying a certain amount over and above the declared value which

will be 100% in FY19, 75% in FY20 and 50% in FY21 and thereafter.

Pakistan Budget Review 21

FY19 Budget – Other Relief Measures

A 10% increase is being proposed for pensioners across the board. Minimum pension is being increased to

Rs.10,000 from the present Rs.6,000.

Reduction of custom duty on finished rooms (Pre‐fabricated structures) from 20% to 10% for setting up of new

hotels/motels is proposed.

To encourage local manufacturing of Optical Fiber Cables, custom duty on input materials i.e, Optical fiber

(20%), Cable filing compound (11%), Polybutylene (20%), Fiber reinforced plastic (20%) and Water blocking/

swellable tape (11%) reduced to 5% besides reduction of regulatory duty on Optical Fiber Cables from 20% to

10%.

Custom duty on specified equipment used in cinema industry reduced to 3%.

Exemption of 5% custom duty on specified LED parts and components for manufacturers of LED lights and Levy

of 2% regulatory duty on LED bulb & Tubes, Energy Saving Bulbs & Tube is proposed.

Reduced rate of sales tax @ 5% is being introduced on import of 19 items of cinematographic equipment for

revival of film industry for five years subject to limitations and conditions imposed under the Customs Act, 1969.

Zero rating is being restored on Stationery items.

Reduction of custom duty on growth promoters premix, vitamin premix, Vitamin B12 and Vitamin H2 for poultry

Honda Atlas Cars (HCAR) 22

sector from 10% to 5%.

Reduction of custom duty on Multi‐ply and Aluminum foil from 20% to 18% for Liquid Food Packaging Industry.

Pakistan Budget Review

FY19 Budget – Other Tax Measures

Additional customs duty to be increased from 1% to 2% with exception being provided for Plant and machinery,

imports by Privileged Personnel /Organizations, Relief goods, Export Promotion regimes etc.

WHT on sale of goods for non filers to be increased from 7% to 8% in the case of a company, and from existing

7.75% to 9.00% in non‐corporate cases.

Due to enhancement of the taxable limit of income to Rs.1.2 million, the number of filers will be substantially

reduced. This will also result in loss of revenue. A nominal income tax may be imposed @ of Rs.1000 for income

between Rs.400,000 to Rs.800,000 and @ of Rs.2000 for income between Rs.800,000 to Rs.1,200,000.

To enhance documentation and base of sales tax, further tax is proposed to be increased from existing 2% to

3%. This will not only discourage undocumented economy, but it will also result in revenue increase.

To protect domestic manufacturers, customs duty on rickshaw tyres is increased from 11% to 20%.

Increase of custom duty on Soya bean oil from Rs9,050/ton & Rs10,200/ton to Rs.12,000/ton and Rs13,200/ton

respectively.

Levy of 30% regulatory duty on export of waste & scrap of copper has been imposed.

Levy of regulatory duty @ Rs.175/set on CKD/SKD kits of mobile phone has also been proposed.

23Pakistan Budget Review

Analyst Certification and DisclosuresThe research analyst(s), denoted by an “AC” on the cover of this report, primarily involved in the preparation of this report, certifies that (1) the views expressed in this report accurately reflect his/herThe research analyst(s), denoted by an AC on the cover of this report, primarily involved in the preparation of this report, certifies that (1) the views expressed in this report accurately reflect his/herpersonal views about all of the subject companies/securities/sectors and (2) no part of his/her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressedin this report.Furthermore, it is stated that the research analyst or its close relative have neither served as a director/officer in the past 3 years nor received any compensation from the subject company in the past 12months.Additionally, as per regulation 8(2)(i) of the Research Analyst Regulations, 2015, we currently do not have a financial interest in the securities of the subject company aggregating more than 1% of the value ofthe company.

Rating SystemTopline Securities employs three tier ratings system to rate a stock, as mentioned below, which is based upon the level of expected return for a specific stock. The rating is based on the following with timehorizon of 12‐months.Rating Expected Total ReturnBuy Stock will outperform the average total return of stocks in universe Neutral Stock will perform in line with the average total return of stocks in universeSell Stock will underperform the average total return of stocks in universeFor sector rating, Topline Securities employs three tier ratings system, depending upon the sector’s proposed weight in the portfolio as compared to sector’s weight in KSE‐100 Index:Rating Sector’s Proposed Weight in PortfolioOver Weight > Weight in KSE‐100 IndexMarket Weight = Weight in KSE‐100 IndexUnder Weight < Weight in KSE‐100 IndexRatings are updated daily to account for the latest developments in the economy/sector/company, changes in stock prices and changes in analyst’s assumptions or a combination of any of these factors.

Di l i

Valuation MethodologyTo arrive at our 12‐months Target Price, Topline Securities uses different valuation methods which include: 1). Present value methodology, 2). Multiplier methodology, and 3). Asset‐based methodology.

Research Dissemination PolicyTopline Securities endeavors to make all reasonable efforts to disseminate research to all eligible clients in a timely manner through either physical or electronic distribution such as email, fax mail etc.Nevertheless, all clients may not receive the material at the same time.

DisclaimerThis report has been prepared by Topline Securities and is provided for information purposes only. Under no circumstances this is to be used or considered as an offer to sell or solicitation of any offer to buy.While reasonable care has been taken to ensure that the information contained therein is not untrue or misleading at the time of publication, we make no representation as to its accuracy or completenessand it should not be relied upon as such. From time to time, Topline Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise be interested in anytransaction, in any securities directly or indirectly subject of this report. This report is provided only for the information of professional advisers who are expected to make their own investment decisionswithout undue reliance on this report. Investments in capital markets are subject to market risk and Topline Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arisingfrom any use of this report or its contents In particular the report takes no account of the investment objectives financial situation and particular needs of investors who should seek further professional

24Pakistan Budget Review

from any use of this report or its contents. In particular, the report takes no account of the investment objectives, financial situation and particular needs of investors, who should seek further professionaladvice or rely upon their own judgment and acumen before making any investment. The views expressed in this report are those of Topline Research Department and do not necessarily reflect those ofTopline or its directors. Topline as a firm may have business relationships, including investment‐banking relationships, with the companies referred to in this report.All rights reserved by Topline Securities. This report or any portion hereof may not be reproduced, distributed or published by any person for any purpose whatsoever. Nor can it be sent to a third party without prior consent of Topline Securities. Action could be taken for unauthorized reproduction, distribution or publication.

CONTACT US

Mr. Mohammed Sohail CEO Dir: +92 (21) 35303333-4 [email protected]

Research Team:

Mr. Saad Hashemy Chief Economist & Director Research Dir: +92 (21) 35303346 [email protected]

Mr. Umair Naseer Deputy Head of Research +92 (21) 35303330-2 [email protected]

Mr. Nabeel Khursheed Senior Research Analyst +92 (21) 35303330-2 [email protected]

Mr. Shankar Talreja Research Analyst +92 (21) 35303330-2 [email protected]

Mr. Fahad Qasim Manager Research +92 (21) 35303330-2 [email protected]

Mr. Asif Habib Database Officer +92 (21) 35303330-2 [email protected]

Equity Sales Team:

Mr. Muhammad Rizwan Head of Sales Dir: +92 (21) 35303337 [email protected]

Ms. Samar Iqbal Head of International Equity Sales Dir: +92 (21) 35370799 [email protected]

Mr. Muhammad Hammad Aman Senior Manager Equity Sales Dir: +92 (21) 353030297 [email protected]

M K il R S i M E it S l Di 92 (21) 353030297 k il@t li kMr. Kumail Raza Senior Manager Equity Sales Dir: +92 (21) 353030297 [email protected]

Mr. Haris Kunda Senior Manager Equity Sales Dir: +92 (21) 35303323 [email protected]

Corporate Office:508, Continental Trade Center,Block 8 Clifton Karachi Pakistan

25

Block-8, Clifton, Karachi, PakistanTel: +9221-35303330-2Fax: +9221-35303349

Pakistan Budget Review