budgeting & financial management basics for living within our means and staying out of debt

TRANSCRIPT

Budgeting & Financial Management

Basics for living within our means and staying out of debt.

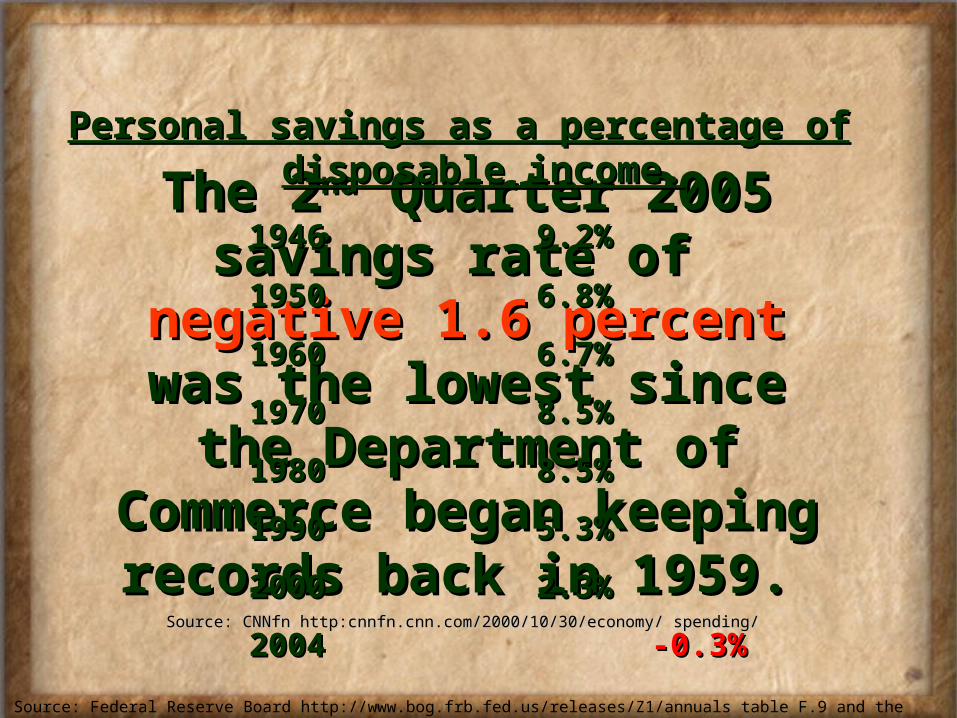

The 2The 2ndnd Quarter 2005 Quarter 2005 savings rate of savings rate of

negative 1.6 percentnegative 1.6 percent was the lowest since was the lowest since the Department of the Department of Commerce began Commerce began

keeping records back in keeping records back in 1959.1959.

Personal savings as a percentage of Personal savings as a percentage of disposable income.disposable income.

19461946 9.2%9.2%

19501950 6.8%6.8%

19601960 6.7%6.7%

19701970 8.5%8.5%

19801980 8.5%8.5%

19901990 5.3%5.3%

20002000 2.3%2.3%

20042004 -0.3%-0.3%

Source: Federal Reserve Board http://www.bog.frb.fed.us/releases/Z1/annuals table F.9 and the U.S. Department of Commerce http://www.bea.doc.gov/bra/newsrel/pi0800.htm

Source: CNNfn http:cnnfn.cnn.com/2000/10/30/economy/ spending/Source: CNNfn http:cnnfn.cnn.com/2000/10/30/economy/ spending/

Pres. Ezra Taft BensonPres. Ezra Taft Benson

The Lord desires His Saints to be free and independent in the critical days ahead. But no man is truly free who is in financial bondage…Get out of debt if it is at all humanly possible.

President Gordon B Hinckley

The problem: • “So many of our people are living on the very edge of their

incomes. In fact, some are living on borrowings”.• “I repeat, I hope we will never again see such a depression.

But I am troubled by the huge consumer installment debt which hangs over the people of the nation, including our own people.”

• “In December of 1997, 55 to 60 million households in the United States carried credit card balances. These balances averaged more than $7,000 and cost $1,000 per year in interest and fees. Consumer Debt as a percentage of disposable income rose from 16.3 percent in 1993 to 19.3 percent in 1996…We are beguiled by seductive advertising.”

President Gordon B Hinckley

“The Solution:• “Pay the debt thou has contracted…Release thyself from

bondage” (D&C 19:35).• “If there is any one thing that will bring peace and

contentment into the human heart, and into the family, it is to live within our means. And if there is any one thing that is grinding and discouraging and disheartening, it is to have debts and obligations that one cannot meet” (Heber J. Grant).

• “We are carrying a message of self-reliance throughout the Church. Self-reliance cannot (be) obtain(ed) when there is a serious debt hanging over a household.”

President Gordon B Hinckley

• “In managing the affairs of the Church, we have tried to set an example. We have, as a matter of policy, stringently followed the practice of setting aside each year a percentage of the income of the Church against a possible day of need.”

• “…the Church in all its operations…is able to function without borrowed money. If we cannot get along, we will curtail our programs. We will shrink expenditures to fit the income. We will not borrow (emphasis added)”.

• “What a wonderful feeling it is to be free of debt, to have a little money against a day of emergency put away where it can be retrieved when necessary.”

President Gordon B Hinckley

• Prophetic admonition: “I urge you, brethren, to look to the condition of your finances. I urge you to be modest in your expenditures; discipline yourselves in your purchases to avoid debt to the extent possible. Pay off debt as quickly as you can, and free yourselves from bondage.”

• God’s promise to the obedient: “May the Lord bless you,

my beloved brethren, to set your houses in order. If you have paid your debts, if you have a reserve, even though it be small, then should storms howl about your head, you will have shelter for your wives and children and peace in your hearts. That’s all I have to say about it, but I wish to say it with all the emphasis of which I am capable.”

Steps to financial self-reliance and freedom from debt

Four Steps

1. Pay an honest tithing and other offerings.

2. Pay yourself.

3. Live on the rest. (Budgeting and Provident Living)

4. Eliminate debt.

1. Pay an honest tithing and other offerings

• Malachi 3:10 …prove me now…saith the Lord of host, if I will not open you the windows of Heaven, and pour you out a blessing, that there shall not be room enough to receive it.

• Successful financial management in every LDS home begins with the payment of an honest tithe. Elder Marvin J Ashton “One for the Money”

2. Pay Yourself

• Retirement Savings

• Personal Savings

Two Approaches: 1. Pay all expenses first and save whatever is left.

2. Save a certain amount first and then pay expenses on what is left.

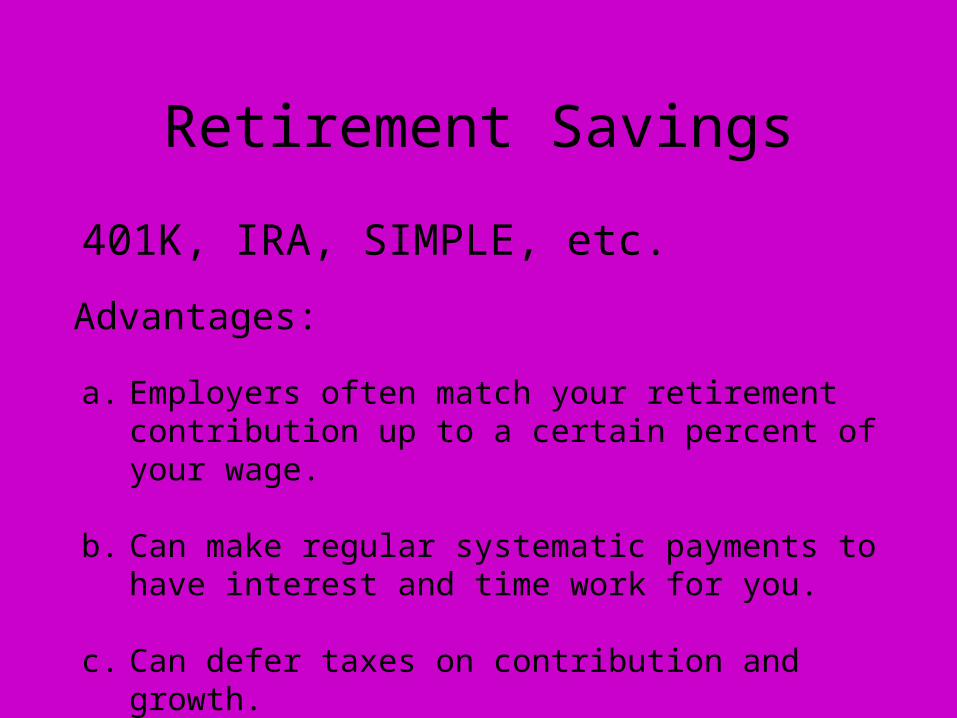

Retirement Savings

401K, IRA, SIMPLE, etc.

a. Employers often match your retirement contribution up to a certain percent of your wage.

b. Can make regular systematic payments to have interest and time work for you.

c. Can defer taxes on contribution and growth.

Advantages:

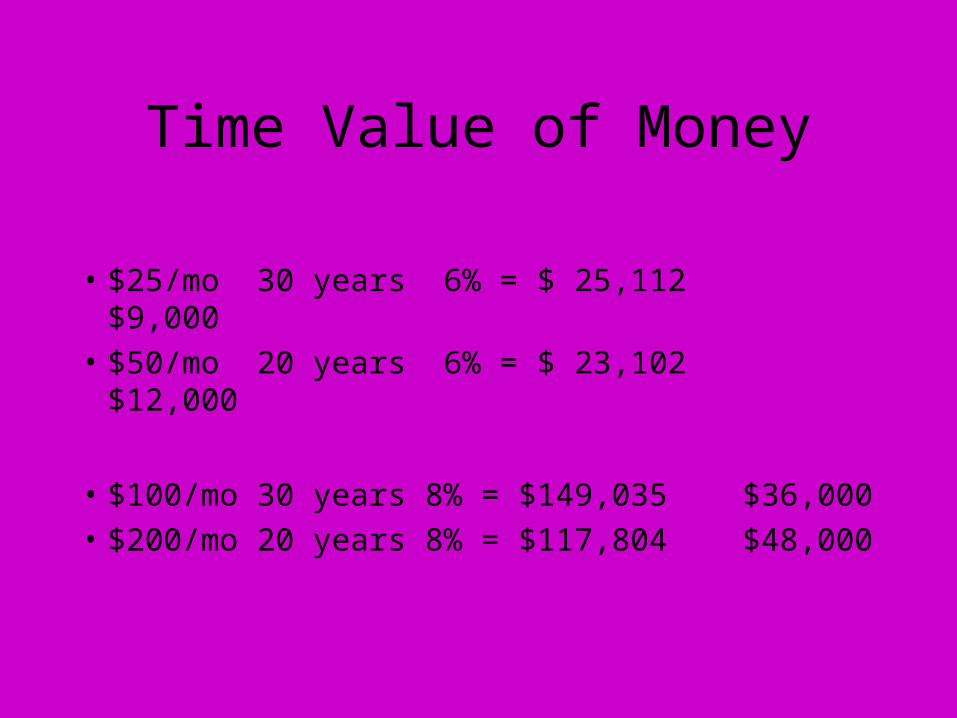

Time Value of Money

• $25/mo 30 years 6% = $ 25,112 $9,000

• $50/mo 20 years 6% = $ 23,102 $12,000

• $100/mo 30 years 8% = $149,035 $36,000

• $200/mo 20 years 8% = $117,804 $48,000

Personal Savings

Emergency savings

3 months salary …..Ideally 1 year

Spendable savings Vacations

Repairs Major Purchases

Elephant Theory of Savings

•One “Percent” Bite at a Time

Start With 1%, Then 2%, 3% Etc.

3. Live on the Rest

• Use a budget to allocate your remaining resources.• If your not committed, or your spouse is not

committed, then the budget will fail before you begin.

• You will need to discuss the budget at least weekly to know where you stand. Experience has shown the longer you wait to check yourself the more likely you will not stay within your budget.

3. Live on the Rest

• Start with your Income. How much do I make? (Bring Home)

• Subtract from that Tithing & Savings.• Budget/Plan your monthly expenditures: Mtge/Rent, Utilities, Food, Clothing, Gifts, Debt Pmts,

Insurance, Education, Transportation, Medical, Food Storage, etc.

• Monitor actual expenditures against budget.

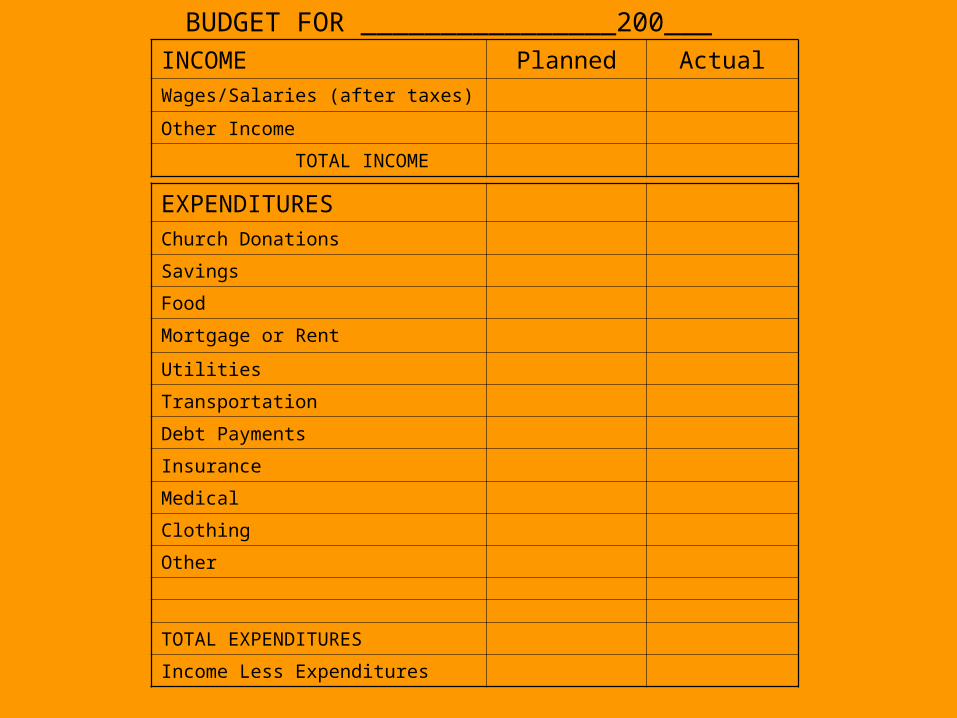

EXPENDITURES

Church Donations

Savings

Food

Mortgage or Rent

Utilities

Transportation

Debt Payments

Insurance

Medical

Clothing

Other

TOTAL EXPENDITURES

Income Less Expenditures

BUDGET FOR ________________200___

INCOME Planned Actual

Wages/Salaries (after taxes)

Other Income

TOTAL INCOME

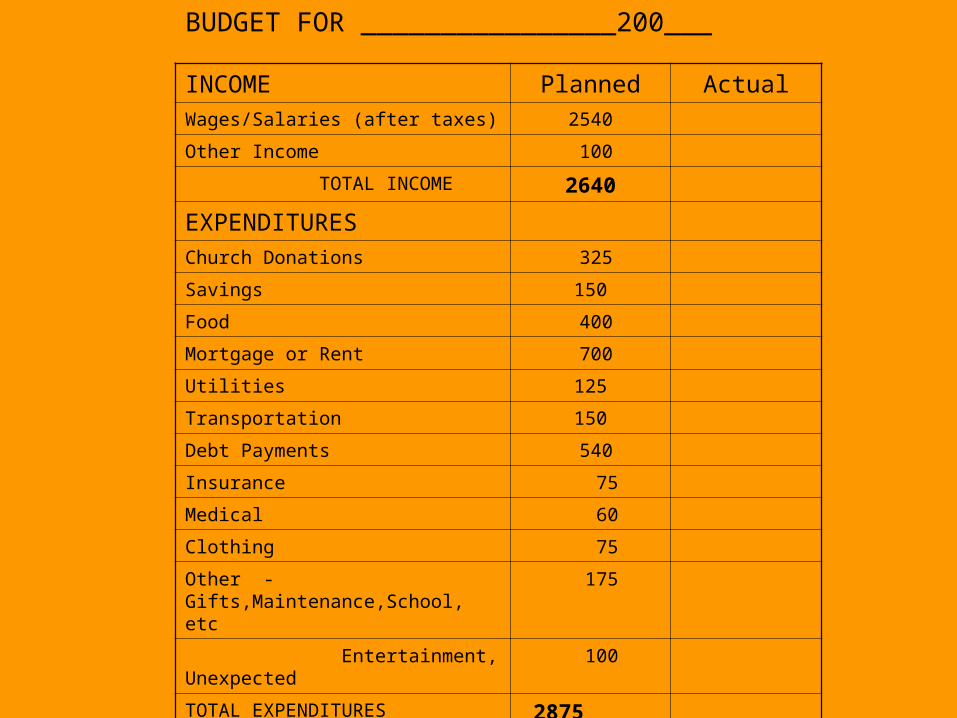

INCOME Planned Actual

Wages/Salaries (after taxes) 2540

Other Income 100

TOTAL INCOME 2640

EXPENDITURES

Church Donations 325

Savings 150

Food 400

Mortgage or Rent 700

Utilities 125

Transportation 150

Debt Payments 540

Insurance 75

Medical 60

Clothing 75

Other - Gifts,Maintenance,School, etc 175

Entertainment, Unexpected 100

TOTAL EXPENDITURES 2875

Excess (Deficiency) (235)

BUDGET FOR ________________200___

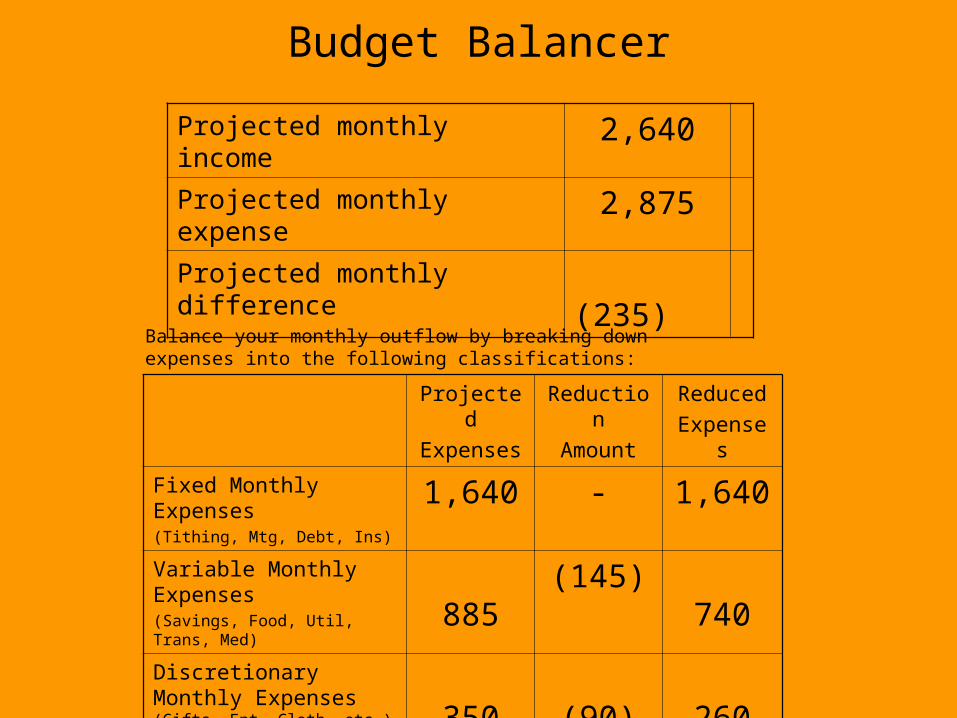

Budget Balancer

Projected monthly income 2,640

Projected monthly expense 2,875

Projected monthly difference (235)

Projected

Expenses

Reduction

Amount

Reduced

Expenses

Fixed Monthly Expenses(Tithing, Mtg, Debt, Ins)

1,640 - 1,640

Variable Monthly Expenses(Savings, Food, Util, Trans, Med)

885 (145) 740

Discretionary Monthly Expenses (Gifts, Ent, Cloth, etc.)

350 (90) 260

Totals 2,875 (235) 2,640

Balance your monthly outflow by breaking down expenses into the following classifications:

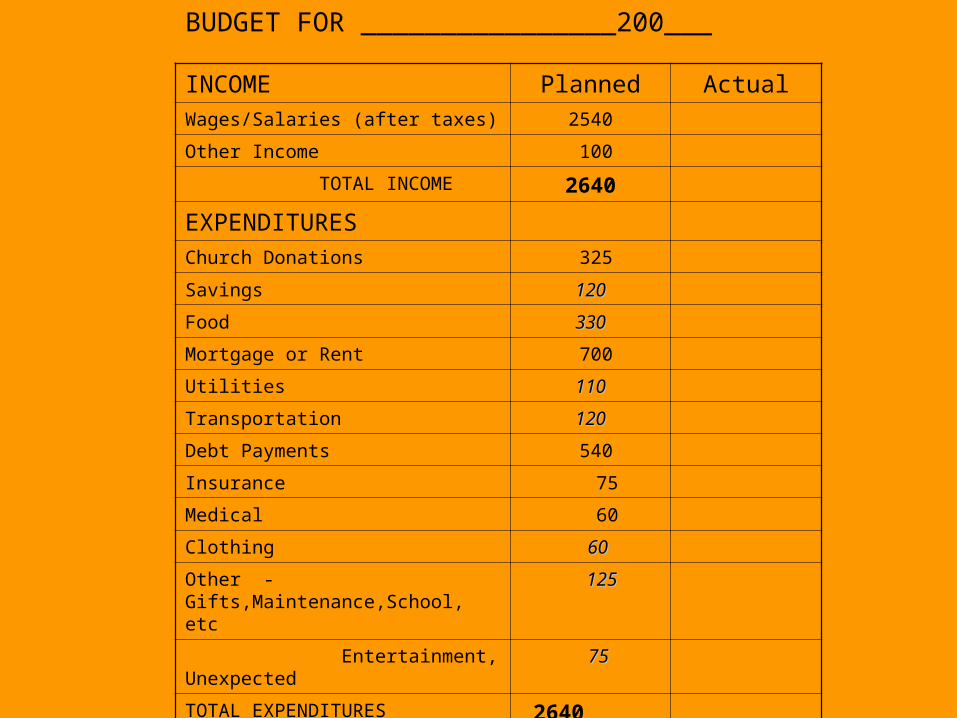

INCOME Planned Actual

Wages/Salaries (after taxes) 2540

Other Income 100

TOTAL INCOME 2640

EXPENDITURES

Church Donations 325

Savings 120120

Food 330330

Mortgage or Rent 700

Utilities 110110

Transportation 120120

Debt Payments 540

Insurance 75

Medical 60

Clothing 6060

Other - Gifts,Maintenance,School, etc 125125

Entertainment, Unexpected 7575

TOTAL EXPENDITURES 2640

Excess (Deficiency) -0-

BUDGET FOR ________________200___

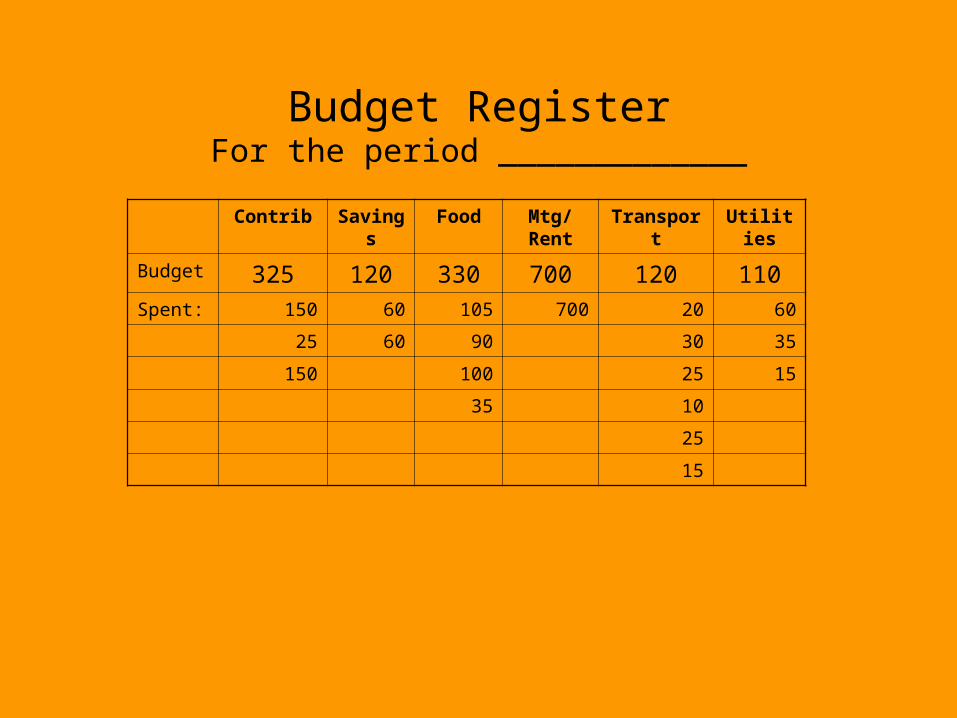

Budget RegisterFor the period _____________

Contrib Savings Food Mtg/Rent Transport Utilities

Budget 325 120 330 700 120 110

Spent: 150 60 105 700 20 60

25 60 90 30 35

150 100 25 15

35 10

25

15

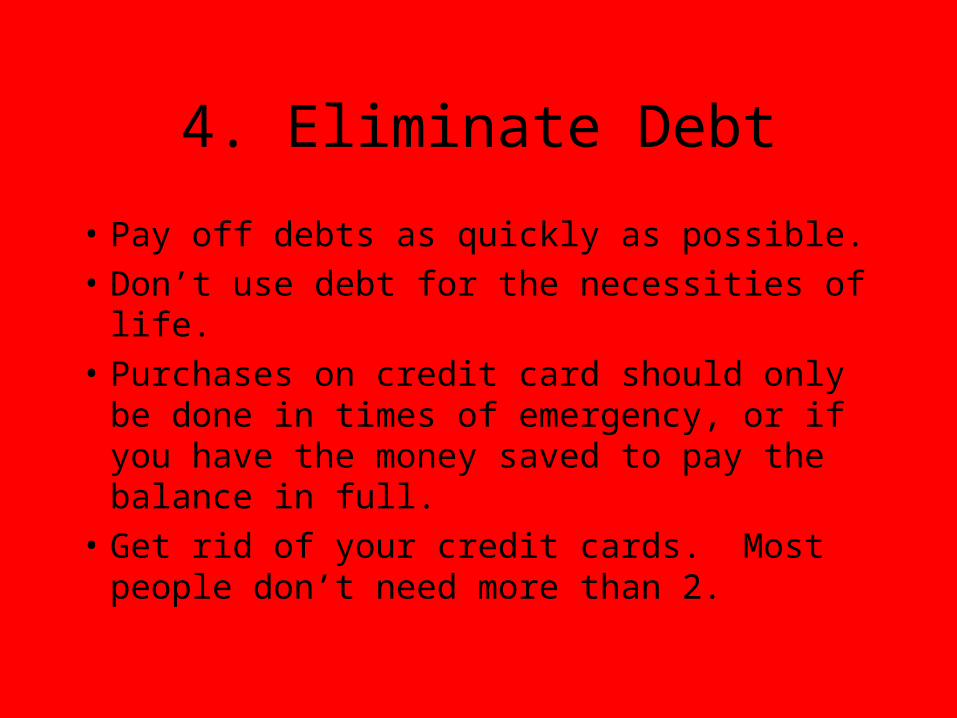

4. Eliminate Debt

• Pay off debts as quickly as possible.

• Don’t use debt for the necessities of life.

• Purchases on credit card should only be done in times of emergency, or if you have the money saved to pay the balance in full.

• Get rid of your credit cards. Most people don’t need more than 2.

4. Eliminate Debt

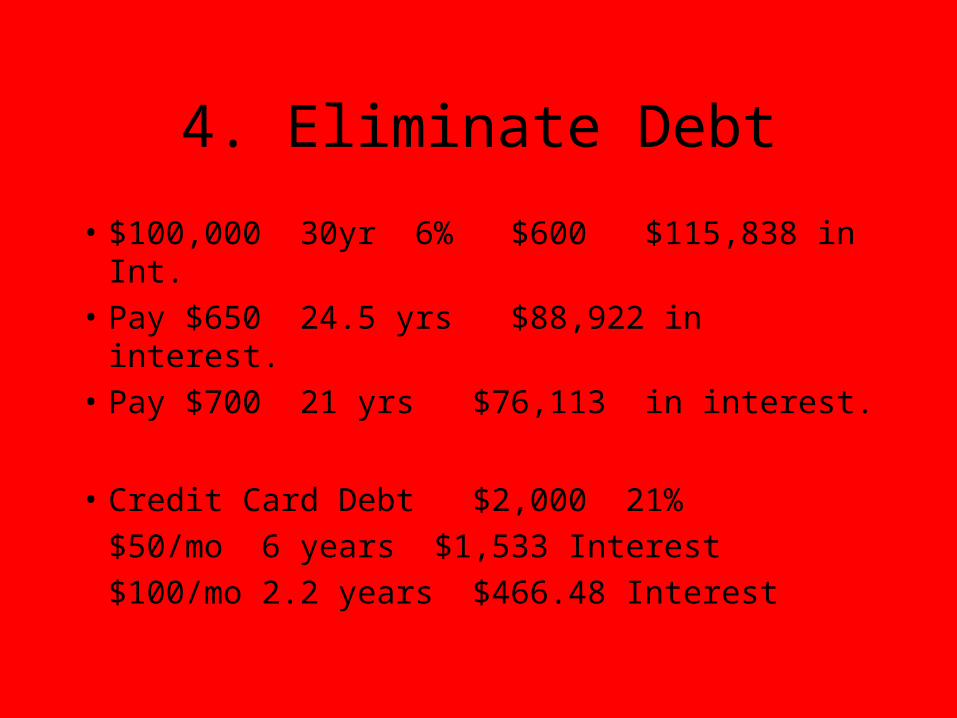

• $100,000 30yr 6% $600 $115,838 in Int.

• Pay $650 24.5 yrs $88,922 in interest.

• Pay $700 21 yrs $76,113 in interest.

• Credit Card Debt $2,000 21%

$50/mo 6 years $1,533 Interest

$100/mo 2.2 years $466.48 Interest

So Then...So Then...

Lost Lost Opportunity Opportunity Cost - Cost -

$1,192.51$1,192.51

Interest -Interest -$228.65$228.65

Dinner - Dinner - $84.12$84.12

Total - Total - $312.77$312.77

The credit card interest rate assumed is 21% with a minimum first payment of 1.8% and that same payment each month. The 7% rate of return used in calculating the lost opportunity cost is

for illustrative purposes only and does not represent any particular investment.

4. Eliminate Debt

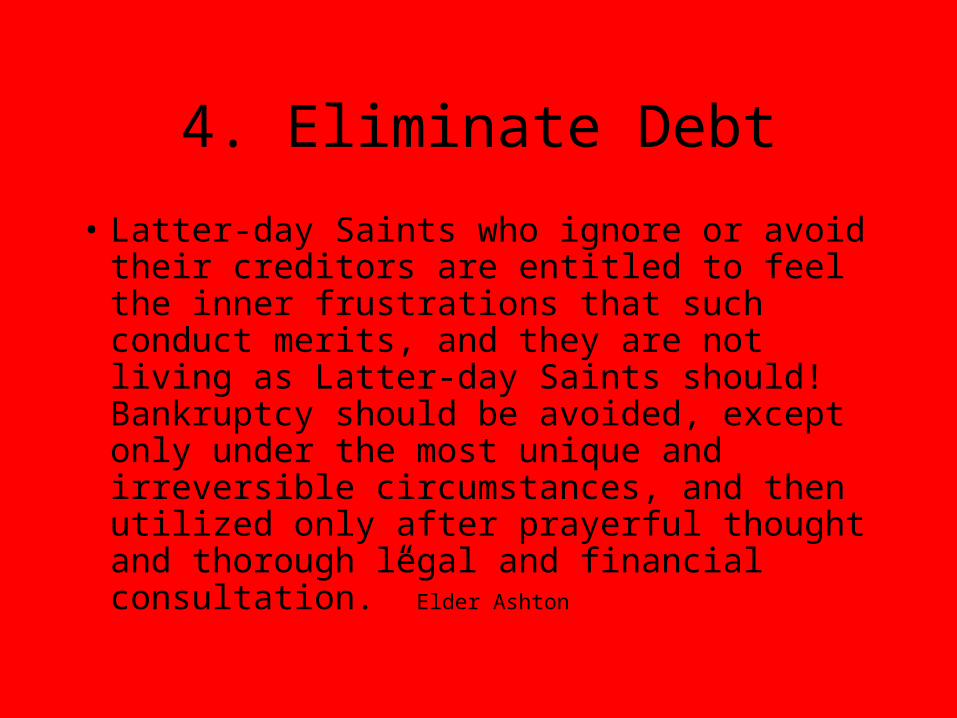

• Latter-day Saints who ignore or avoid their creditors are entitled to feel the inner frustrations that such conduct merits, and they are not living as Latter-day Saints should! Bankruptcy should be avoided, except only under the most unique and irreversible circumstances, and then utilized only after prayerful thought and thorough legal and financial consultation.” Elder Ashton

President Gordon B Hinckley

• God’s promise to the obedient: “May the Lord bless you, my beloved brethren, to set your houses in order. If you have paid your debts, if you have a reserve, even though it be small, then should storms howl about your head, you will have shelter for your wives and children and peace in your hearts.