building a better company - corporate-ir.net · products/distribution network key brands/ markets...

TRANSCRIPT

Terex Equipment Limited Unit Rig Payhauler Fermecaques O&K Mining Powerscreen International Powerng Standard Havens American Crane Comedil Terex Ler PPM SAS Telelect Terex Aerials Limited Terex HandleWaverly Operations Terex RO Amida Industries Bartell

ica-Jaques Cedarapids Terex Equipment Limited Unit Rascreens Limited Jaques O&K Mining Powerscreen

dustries Simplicity Engineering Standard Havens Ameerexlift Terex Lifting UK Peiner PPM SAS Telelect Terexway Operations Terex Lifting Waverly Operations Tereenford Limited B.L. Pegson Canica-Jaques Cedarapids Tcturing Limited Finlay Hydrascreens Limited Jaques Oech Royer Industries Simplicity Engineering Standarand Lift Terexlift Terex Lifting UK Peiner PPM SAS Teleng Conway Operations Terex Lifting Waverly OperationeerinG Benford Limited B.L. Pegson Canica-Jaques Cedanufacturing Limited Finlay Hydrascreens Limited Jated Re-Tech Royer Industries Simplicity Engineering ia Holland Lift Terexlift Terex Lifting UK Peiner PPM

alia Terex Lifting Conway Operations Terex Lifting Wa

BUILDING A BETTER COMPANY

ANNUAL REPORT 2000

▼

P R O F I T A B L E G R O W T H

Q U A L I T Y P R O D U C T S

C U S T O M E R S A T I S F A C T I O N

B R A N D R E C O G N I T I O N

O R G A N I Z A T I O N A L E F F E C T I V E N E S S

CONTENTS

1 Financial Highlights

2 Terex Corporation At-A-Glance

4 Letter to Shareholders and Stakeholders

BUILDING A BETTER COMPANY

8 Profitable Growth

10 Quality Products

12 Customer Satisfaction

14 Brand Recognition

16 Organizational Effectiveness

18 Shareholder Information

— Annual Report on Form 10-K

IBC Terex Corporation World Wide Web Site

A B O U T T E R E X▼

Terex Corporation is a diversified global

manufacturer of a broad range of lifting, earth-

moving, and light construction equipment for

the construction, infrastructure development,

quarrying, recycling, and surface mining indus-

tries. Terex has achieved a significant opera-

tional transformation over the past several years

due to a unique business model of outsourcing,

low overhead, and acquisitions leading to prod-

uct and geographic diversity.

We are driven by our mission statement of

manufacturing and marketing high quality capital

equipment designed to improve our customers'

productivity and return on invested capital. Our

products are manufactured in 39 facilities in

North America, Europe, Asia, and Australia and

are marketed in more than 100 countries. They

are sold primarily through a worldwide network

of dealers in over 1000 locations.

1

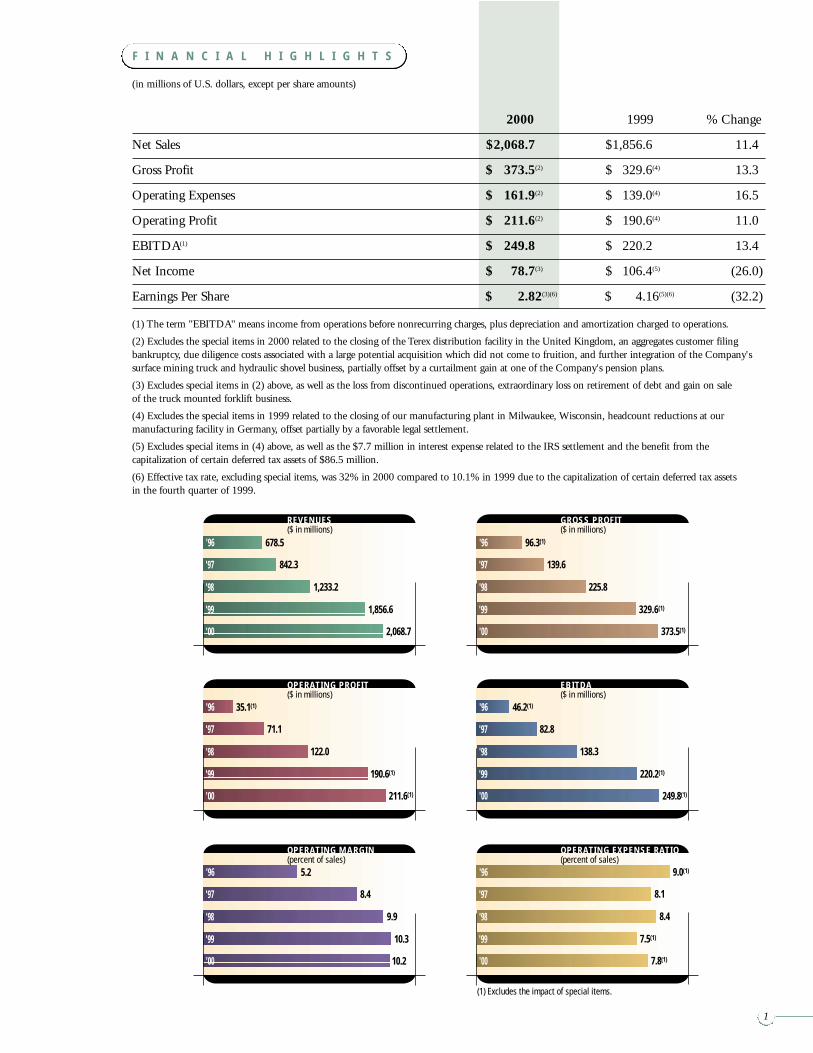

F I N A N C I A L H I G H L I G H T S

2000 1999 % Change

Net Sales $2,068.7 $1,856.6 11.4

Gross Profit $ 373.5(2) $ 329.6(4) 13.3

Operating Expenses $ 161.9(2) $ 139.0(4) 16.5

Operating Profit $ 211.6(2) $ 190.6(4) 11.0

EBITDA(1) $ 249.8 $ 220.2 13.4

Net Income $ 78.7(3) $ 106.4(5) (26.0)

Earnings Per Share $ 2.82(3)(6) $ 4.16(5)(6) (32.2)

(in millions of U.S. dollars, except per share amounts)

OPERATING EXPENSE RATIO(percent of sales)

(1) Excludes the impact of special items.

EBITDA($ in millions)

GROSS PROFIT($ in millions)

OPERATING MARGIN(percent of sales)

OPERATING PROFIT($ in millions)

REVENUES($ in millions)

'97

'98

'99

'00

'96

1,856.6

1,233.2

842.3

678.5

2,068.7

'97

'98

'99

'00

'96

329.6(1)

225.8

139.6

96.3(1)

373.5(1)

'97

'98

'99

'00

'96

220.2(1)

138.3

82.8

46.2(1)

249.8(1)

'97

'98

'99

'00

'96

7.5(1)

8.4

8.1

9.0(1)

7.8(1)

'97

'98

'99

'00

'96

190.6(1)

122.0

71.1

35.1(1)

211.6(1)

'97

'98

'99

'00

'96

10.3

9.9

8.4

5.2

10.2

(1) The term "EBITDA" means income from operations before nonrecurring charges, plus depreciation and amortization charged to operations.

(2) Excludes the special items in 2000 related to the closing of the Terex distribution facility in the United Kingdom, an aggregates customer filing bankruptcy, due diligence costs associated with a large potential acquisition which did not come to fruition, and further integration of the Company'ssurface mining truck and hydraulic shovel business, partially offset by a curtailment gain at one of the Company's pension plans.

(3) Excludes special items in (2) above, as well as the loss from discontinued operations, extraordinary loss on retirement of debt and gain on sale of the truck mounted forklift business.

(4) Excludes the special items in 1999 related to the closing of our manufacturing plant in Milwaukee, Wisconsin, headcount reductions at our manufacturing facility in Germany, offset partially by a favorable legal settlement.

(5) Excludes special items in (4) above, as well as the $7.7 million in interest expense related to the IRS settlement and the benefit from the capitalization of certain deferred tax assets of $86.5 million.

(6) Effective tax rate, excluding special items, was 32% in 2000 compared to 10.1% in 1999 due to the capitalization of certain deferred tax assets in the fourth quarter of 1999.

(1) Excludes the impact of special items.

OPERATING PROFIT($ in millions)

'97

'98

'99

'00

'96

90(1)

42

25

16

115(1)

(1) Excludes the impact of special items.

OPERATING PROFIT($ in millions)

'97

'98

'99

'00

'96

100(1)

82

47

23

95(1)

T E R E X E A R T H M O V I N G

T E R E X L I F T I N G

T E R E X L I G H T C O N S T R U C T I O N

2

Operating Units Manufacturing Facilities

B.L. Pegson Coalville, EnglandBenford Limited Warwick, EnglandCanica-Jaques Vancouver, Washington, USACedarapids Cedar Rapids, Iowa, USAFermec Manufacturing Limited Manchester, EnglandFinlay Hydrascreens Limited Omagh, Northern IrelandJaques Subang Jaya, Malaysia; Melbourne, Australia;

Chomburi, ThailandO&K Mining Dortmund, GermanyPowerscreen International Dungannon, Northern IrelandPowerscreen Limited Kilbeggan, IrelandRe-Tech and Royer Industries Lebanon, Pennsylvania, USASimplicity Engineering Durand, Michigan, USAStandard Havens Glasgow, Missouri, USATerex Equipment Limited Motherwell, ScotlandUnit Rig and Payhauler Tulsa, Oklahoma, USA

American Crane Wilmington, North Carolina, USAComedil Fontanafredda, ItalyHolland Lift Hoorn, The NetherlandsPPM SAS Montceau-les-Mines, FrancePeiner Trier, GermanyTelelect Watertown, South Dakota, USATerex Aerials Limited Cork, IrelandTerex Handlers Baraga, Michigan, USATerex Italia Crespellano, ItalyTerex Lifting Australia Brisbane, AustraliaTerex Lifting – Conway Operations Conway, South Carolina, USATerex Lifting UK Tetbury, EnglandTerex Lifting – Waverly Operations Waverly, Iowa, USATerex – RO Olathe, Kansas, USATerexlift Perugia, Italy

Amida Industries Rock Hill, South Carolina, USA

Coleman Engineering Holly Springs, Mississippi, USA; Memphis, Tennessee, USATerex Bartell Ltd. Brampton, Ontario, Canada

T E R E X C O R P O R A T I O N A T - A - G L A N C E

Products/Distribution Network Key Brands/ Markets

Crushers B.L. PegsonPower buggies, rollers, soil compactors, vibratory plate compactors BenfordCrushers Canica-JaquesCrushers, asphalt pavers, screens Cedarapids, GrayhoundLoader backhoes FermecCrushers, washing systems, trommels, screens FinlayScreens, feeders, crushers Jaques

Large hydraulic excavators O&KWashing systems, screens, trommels PowerscreenWashing systems, screens, trommels PowerscreenTrommels, recycling systems Re-Tech, Royer, TerexHeavy duty screens and feeders SimplicityAsphalt mixing plants Cedarapids, Standard HavensOff-highway rigid and articulated haulers, scrapers TerexElectric rear and bottom dump haulers, all wheel drive rigid off-highway trucks Unit Rig, Payhauler, Lectra Haul, TerexOver 212 independent dealers and over 77 distributor/agents. Broad array of worldwide customers

in the construction, mining, quarrying, recycling, and infrastructure industries.

Lattice boom cranes, tower cranes American, TerexTower cranes ComedilAerial work platforms Holland LiftAll terrain hydraulic mobile cranes, container stackers PPM, TerexTower cranes PeinerUtility aerial devices, digger derricks Telelect, Hi-RangerAerial work platforms TerexRough terrain telescopic material handlers Square Shooter, TerexRough terrain hydraulic mobile cranes Terex, Bendini, PPMAll terrain mobile cranes FrannaRough terrain hydraulic mobile cranes, truck cranes P&H, TerexMaterial handlers MatbroRough terrain hydraulic mobile cranes, truck cranes, aerial work platforms Terex, Lorain, Terex AerialsTruck mounted cranes RO-StingerRough terrain telescopic material handlers, cement mixers, concrete pumps Italmacchine, TerexOver 700 independent distributors worldwide. Crane and aerial lift rental customers in the construction,

recycling, shipping, transportation, refining, and utility industries.

Portable floodlighting systems, concrete power trowels, Amida, Benford, Morrison, Terex, Mullerconcrete placement systems, traffic control productsGenerators, light towers Coleman EngineeringPower trowels, concrete finishing systems Bartell, TerexGlobal network of dealers, distributors, and national accounts. Rental customers in the construction

and maintenance industries.

3

The year 2000 was a year of both accomplishments and

challenges at Terex. We posted record sales, operating income,

and operating cash flow for the fourth consecutive year, despite

an economic environment that grew increasingly more challeng-

ing as the year progressed. Over the past several years, we have

taken many steps to transform Terex into a Company that

not only thrives and prospers in good times, but also remains

profitable during downturns. I am gratified to say that the Terex

model of variabilizing our cost structure and minimizing our

overhead costs has proven itself during 2000. We were able to

maintain and, in some cases, increase our margins in the face

of declining volumes in several of our product lines, especially

in North America. The strategic actions we took in 1999 to

diversify and strengthen the Company with the acquisitions

of both Powerscreen and Cedarapids are paying off. We believe

we have positioned ourselves for more consistent growth and

profitability by becoming a leading player in the growing

aggregate equipment industry.

In last year’s letter, I made a commitment to generate a

substantial amount of free cash flow, to pay down debt and

to slow down acquisitions. We exceeded these commitments,

and I am happy to say that our financial structure has improved

markedly. I also commented that we would use the Internet to

help our customers and challenge the way we conduct business

in this industry. We delivered on that commitment too, and in

mid-January 2001, we announced the launching of EarthKing

(Terex is Latin for EarthKing), an independent and unbiased

Internet marketplace for owners and operators of construction

and mining equipment to manage their fleet. Our vision was to

create a new company that would reduce the life cycle costs on

all types of capital equipment and allow owners and operators

of capital equipment to maximize their return on investment.

And I believe we are on our way to realizing this goal.

For the fifth year in a row, we created a material amount of

economic value as our after-tax return on invested capital was

greater than our weighted average cost of capital. However, we

continue to be disappointed by the performance of our stock price.

Having said that, despite the fact that equity markets for capital

goods companies have been in turmoil for the past couple of

years, Terex’s equity value has outperformed both the S&P 500

and the S&P Diversified Machinery indices over the past five

T O O U R S H A R E H O L D E R S A N D S T A K E H O L D E R S :

years. The Terex operating model is designed to offer to current

and prospective stakeholders a company with a lower operating

risk, which in a cyclical industry should be rewarded with a

higher valuation than the current one. I remain committed to

look for ways to create shareholder value, and I am convinced

that ultimately Terex will prove to be a solid investment for

all our stakeholders.

Financial Performance

Over the past five years, we have quadrupled the size of our

Company, growing from $501 million in revenue in 1995

to $2.1 billion in revenue in 2000. We continue to build a

growing franchise under the Terex brand name and remain

very focused on our mission of delivering products that are

reliable, productive, and cost-effective and that improve our

customers’ return on invested capital. Sales in 2000 increased

11 percent to a new record of $2.1 billion. Operating profit

rose 11 percent to $212 million, driven almost entirely by the

impact of the 1999 acquisitions of Cedarapids and Powerscreen.

Operating margin remained essentially flat at 10.2 percent of

sales, despite the fact that we faced declining volumes in several

of our North American product lines.

The Terex operating model successfully passed a very impor-

tant test this past year, especially in the mining business, where

we saw volume decline almost 50 percent. Many in the capital

goods sector reported operating losses in this type of environment.

Terex did not! EBITDA of $250 million for the year was also

a record and was up $30 million, or 13.4 percent, versus the

prior year. EBITDA margin has also increased for the sixth con-

secutive year, increasing from 11.9 percent of sales in 1999 to

12.1 percent in 2000. Operating expenses as a percentage of sales,

which had fallen for the past four years, increased slightly from

7.5 percent in 1999 to 7.8 percent in 2000. Our objective in

this area is to continue to eliminate non-value added functions

throughout the organization and at the same time strengthen

our franchise by investing in operating control systems, after-

market service and support, and e-commerce capabilities. One

of our stated objectives for 2000 was to reach an 11 percent

operating margin for the entire Company. We did not reach

that objective, mainly because we faced a number of issues in

the mining business including the absence of the 1999 Coal

4

Over the past two years alone, we have

increased our revenues by more than

65 percent and at the same time reduced

our net debt-to-capital ratio by 25

percentage points from 86.1 percent

in 1998 to 61.5 percent in 2000.

next two years will be to further reduce our working capital as a

percentage of sales down to 25 percent.

We used cash to reduce debt, and at the end of 2000 our

debt net of cash stood at approximately $721 million and the

net debt-to-capital ratio was 61.5 percent. This is the first time

in the past decade that Terex’s net debt-to-capital ratio dropped

to approximately 60 percent. Over the past two years alone,

we have increased our sales by more than 65 percent and at the

same time reduced our net debt-to-capital ratio by approximately

25 percentage points from 86.1 percent in 1998 to 61.5 percent

in 2000. There is no question in my mind that today, Terex is

in a much better position to continue to grow and create value

for our shareholders.

Strategic Intent

We remain committed to a low cost provider strategy, selling to

multiple channels of distribution with a very flexible cost and

pricing structure. This is the same internal strategy that we out-

lined last year. During 1998 and 1999, we invested over $800

million in several acquisitions with the objective of diversifying

our portfolio and creating long-term value for our shareholders.

However, we did take a pause last year in our acquisition pro-

gram and concentrated on reducing our leverage and increasing

our financial flexibility. This does not alter the fact that both

our customers and suppliers are rapidly consolidating, and in

order to grow and prosper in the capital goods industry, manu-

facturers need to do the same. Our process regarding acquisitions

is very disciplined and is one of our core competencies. First,

the target company must provide substantial opportunity for

revenue growth or for implementing the Terex operating model

or both. Second, the transaction must generate a return on

invested capital substantially in excess of our weighted average

cost of capital of approximately 10 percent. Third, the acquisition

must be accretive to earnings within the first year of ownership.

India order, the slowdown in anticipated orders, and the finan-

cial impact of the introduction of the new MT5500 mining

truck, which needed to prove itself to our customers. In addi-

tion, in the North American hydraulic mobile crane market,

we had to manage through a 13 percent decline in industry

orders and a more aggressive competitor trying to reestablish

itself in the marketplace. We did find out in the process, however,

that the hydraulic crane market is a lot less price-sensitive in a

downturn than we had anticipated. We will continue to raise

the bar and challenge the organization, even if we know that

the business outlook will make it very difficult to increase our

operating margin in 2001.

Cash Flow and Capital Structure

In last year’s letter, I committed to increase our financial flexibility

and to generate over $200 million of free cash flow and pay

down debt. I believe we delivered on all those fronts. In total

for 2000, we generated over $300 million of free cash flow -

a very satisfying performance. During 2000, we generated $201

million of operating cash, a $196 million increase from 1999.

We also made a concerted effort to improve our working capital

management. By focusing more aggressively on our supply chain,

we were able to reduce our net inventories by approximately

10 percent from $666 million in 1999 to $598 million in 2000.

Furthermore, we brought our trade receivables and payables in

better balance, freeing additional cash flow. Overall, we reduced

our working capital by approximately $120 million. As a result,

our working capital as a percentage of sales declined from 37

percent in 1999 to 31 percent in 2000. There is no question that

we have more work to do in this area and our objective over the

Ronald M. DeFeo, Chairman, President and Chief Executive Officer, center

Ernest R. Verebelyi, President, Terex Earthmoving, left

Fil Filipov, President, Terex Lifting, right

5

EBITDA, were sold approximately one year later for 9 times

EBITDA to Partek of Finland. We also continued to reduce

our exposure to the aerial work platform business because we

believe that this industry suffers from over-capacity and that

the rental companies will continue to exert downward pressure

on manufacturers’ margins.

Going forward, you should expect us to remain disciplined

in our capital allocation whether we choose to pay down debt,

buy back stock, or acquire assets.

Internal Developments

The Terex franchise continues to grow across the construction,

infrastructure, recycling, mining, and rental markets. The

Lifting segment faced a difficult year, as the U.S. hydraulic

crane market fell approximately 13 percent and a major com-

petitor tried to reestablish itself with a revitalized product line.

Several of our hydraulic mobile crane customers were also

affected by a lack of capital and substantially reduced their

equipment purchases. We held our own very well and our mar-

ket share of U.S. commercial hydraulic cranes stayed above 40

percent in 2000. Besides the weakness in hydraulic mobile

cranes and aerial work platforms, we had a very successful year,

highlighted by the strong performance of our lattice boom crane

operation and our continued market penetration in boom

trucks and utility aerial devices. The European Lifting business

delivered a good performance, driven by the impact of the 1999

acquisitions and our strong performance in France, Italy, and

Spain, with container stackers, tower cranes, and material

handlers. We initiated a new aftermarket program designed to

provide faster and better service to our customers. This brand

new Product Support Plus Program was designed to create 30

service centers in both North America and Europe, all of them

connected to a central location with global positioning systems

capability. These red vans are providing a product support

link between customers, distributors, and the respective Terex

Lifting factories.

The Earthmoving segment had a mixed year, as the strong

performance of our aggregates business was partially offset by

the very soft performance of our mining business. Powerscreen

posted record results, led by the introduction of new track-

mounted machines, cost savings from leveraging our material

purchases, and more efficient production. Cedarapids benefited

from a full year of restructuring actions as overhead expenses

We did make two small acquisitions during the second half

of 2000. In October, we closed on the acquisition of Coleman

Engineering, a $15 million manufacturer of portable light

towers and generators for the rental industry. This transaction

strengthens our position in the light construction equipment

area, particularly in the large generator product line, which we

believe is a growth segment. In late December, we closed on

the acquisition of Fermec, a leading European manufacturer

of loader backhoes based in England, with $80 million in rev-

enues. This acquisition gives us the opportunity to implement

our low-cost operating model in a new product line that

increasingly sells through rental fleets and therefore requires a

lower cost design. The Fermec brand provides an excellent plat-

form from which to develop a cost-effective line under Terex

ownership that represents a compelling value to these customers.

While you know us for the many acquisitions we have made

over the past several years, we would like to be known for the

many we walked away from because they did not meet our criteria.

We were also busy during the past year assessing our portfolio

of assets, and during the third quarter of 2000, we divested the

truck-mounted forklift businesses. Those businesses, which we

acquired in the second half of 1999 for approximately 6 times

T O O U R S H A R E H O L D E R S A N D S T A K E H O L D E R S :

6

Front row, left to right, Jack Lascar, Vice President, Investor Relations

and Corporate Communications, Murray Scott, Vice President and General

Manager, Terex Light Construction / Terex Worldwide Parts Distribution Center,

Brian J. Henry, Vice President, Finance, Business Development

Back row, left to right, Eric I Cohen, Senior Vice President, Secretary and

General Counsel, Kevin A. Barr, Vice President, Human Resources,

Ronald M. DeFeo, Chairman, President and Chief Executive Officer,

Joseph F. Apuzzo, Chief Financial Officer

(continued)

were reduced by 50 percent from 1999 levels and company-

wide cost reduction efforts yielded in excess of $10 million

annualized in the second half of the year.

The construction business, which includes our off-highway

trucks, compaction and dumper equipment, set another record

year in terms of sales, operating profit, and market penetration.

Our off-highway truck volumes increased 23 percent as we

continue to successfully expand our presence in Europe, North

America, South Africa, and Indonesia. We are in the process of

upgrading our articulated truck product line, barely two years

after we went through a total redesign, in order to continue to

provide our customers with the lowest cost per ton moved.

The mining business faced a difficult environment in 2000,

with revenues down approximately 30 percent. The continued

weakness in commodity prices has driven the customer base into

postponing new equipment purchases. Despite the lack of new

orders, our mining revenues were up 8 percent compared to

1999, excluding the Coal India order, and we believe we main-

tained our number one market share position for the second year

in a row. During the third quarter of 2000, we finalized plans

to integrate our surface mining truck and hydraulic shovel busi-

nesses. This integration effort will position our mining business

to become more profitable, while improving our customer service.

We had a vision in early 2000 to create an independent

e-commerce company that will change the way business is

conducted in the capital goods industry and will provide new

tools for equipment owners and operators to maximize their

return on investment. In early 2001, this vision became reality.

We named it EarthKing. Our objective is for EarthKing to use

the Internet and available technology to provide real savings to

their customers in the selection, acquisition, management, and

disposition of their equipment and parts. Since EarthKing is

supplier, vendor, and channel-neutral, they can provide a

complete and unbiased solution to their customers’ equipment

and parts needs. We believe that EarthKing is currently the

only e-commerce company with the ability to provide a full menu

of services for equipment throughout the product life cycle.

Looking Ahead

We expect to post another solid performance in 2001, despite

the challenges of the U.S. economy. It is clear to us that the

U.S. economy started to slow down in the second half of 2000

and this situation, which we expect to continue at least through

the first half of this year, has created a real hesitancy from our

customers in terms of capital equipment purchases. The speed

at which the Federal Reserve Board is reacting to the slowdown

in the U.S. economy may bode well for the second half of this

year. We expect the energy producing countries to grow fairly

strongly during 2001, helped by strong energy prices, which

should help us in terms of lifting equipment sales. We also

expect relatively higher commodity prices, which should

strengthen our mining equipment sales, and continued infra-

structure spending worldwide, which should have a positive

impact on our aggregate equipment sales. We will continue to

drive to higher levels of performance by leveraging our internal

strengths and by delivering faster and better value to our cus-

tomers. Regarding our capital structure, we will continue to

focus our efforts on reducing working capital, generating cash,

and paying down additional debt. Our fundamental business

strategy has not changed. We will continue to grow and

strengthen our franchise and create economic value for our

shareholders. Our determination to execute, coupled with an

effective management team and a proven operating model,

should allow us to generate more stable and more predictable

financial performance going forward. Our entire organization

joins me in thanking you for your continuing support.

Sincerely,

Ronald M. DeFeo

Chairman, President and Chief Executive Officer

7

Our fundamental business strategy has

not changed. We will continue to grow

and strengthen our franchise and create

economic value for our shareholders.

Board of Directors:

front row, left to right,

Marvin B. Rosenberg,

G. Chris Andersen,

Back row, left to right,

David A. Sachs,

Ronald M. DeFeo,

Donald P. Jacobs, Not

shown, William H. Fike,

Don DeFosset

profitable growth

BU

ILD

ING

A B

ET

TE

R C

OM

PA

NY

TH

RO

UG

H

8

T E R E X C O R P O R A T I O N

9

T E R E X P RO V I D E S I T S C U S TO M E R S W I T H A

VA LU E P RO P O S I T I O N S E C O N D TO N O N E .

As a result of a multi-year contract between construction giant Enka-Bechtel and the

Republic of Croatia, Cedarapids was awarded approximately a $3 million order for an entire

portable crushing and screening system to be used in the Croatia Motorway project. When

complete, the motorway will feature 74 miles of four-lane segments linking the Croatian

capital of Zagreb with important economic corridors in the region. Specifications for the

project included the ability to readily move the equipment from site to site and the production

of up to six products simultaneously. The relationship between Cedarapids and Enka-Bechtel

stretches back more than a decade to the construction of a 114-mile, four-lane superhighway

connecting the Turkish capital of Ankara and the city of Gerede, located near the Black Sea.

Cedarapids began shipping the order to Croatia in March 2001.

Terex Mining introduced its new 150-ton AC drive truck, the MT3300AC, at MinExpo

in Las Vegas, Nevada, in the fall of 2000. This new truck is materially different from the

traditional standard for off-highway haulage trucks that have either a mechanical or a DC

electric drive train powered by diesel engines developing about 1 horsepower per 350 pounds

of gross vehicle weight. The drive train used on this new truck is an AC electric drive and the

engine, while still a diesel, has more horsepower, with a rating of better than 1 horsepower per

300 pounds of gross vehicle weight. The new system’s major advantage is less maintenance

and, as a result, more uptime. English China Clay (ECC) became our first customer for this

new truck. ECC, a British division of French-based parent IMERYS, is the largest producer

of five North American limestone properties. ECC was interested in upgrading their existing

truck fleet, which included 100-ton trucks from a major competitor. Their objectives were

to upgrade the technology at the quarry, lower their operational cost per ton, and ultimately

double their limestone production from one million to two million tons per year. Thanks to

the support from key suppliers and the total team effort from the Tulsa, Oklahoma, facility,

Terex Mining got their first order for four MT3300AC trucks against two key competitors.

The 150-ton AC drive truck was chosen based on the expected lower maintenance profile of

the AC drive system and its productivity potential as the quarry continues to expand.

Above: The Cedarapids

portable crushing

and screening system

consisting of three

components - a single

impeller, a vertical

shaft impactor and

a horizontal shaft

impactor - is being

used in the Croatia

motorway project.

Below: The newly

introduced, highly

productive MT3300AC

150-ton off-highway

hauler.

quality products

BU

ILD

ING

A B

ET

TE

R C

OM

PA

NY

TH

RO

UG

H

10

T E R E X C O R P O R A T I O N

N E W P RO D U C T I N T RO D U C T I O N A N D Q UA L I T Y P RO D U C T S

R E M A I N K E Y FA C TO R S I N I M P RO V E D M A R K E T P E N E T R AT I O N .

11

The summer of 2000 saw the introduction of the new Terex 70-ton capacity TR70

quarry truck, a model size in which the Company did not participate previously. The TR70

follows the proven Terex rigid truck concept, but incorporates several new features and is

aimed at the quarry market, where trucks are expected to perform around the clock. The

TR70 has a 24-liter, 4-cycle, 12-cylinder turbocharged and aftercooled Detroit Diesel

engine, very conservatively rated at 760 horsepower. This engine has been designed for low

maintenance and low fuel consumption and has a mean time to major overhaul of 20,000

hours. The low maintenance cost and a load over height which is five inches lower than

the main competition provides this truck with a major advantage in the marketplace.

Powerscreen, based in Dungannon, Northern Ireland, was acquired by Terex in the

summer of 1999 and has been introducing some of the most innovative and popular models

in today’s crushing and screening markets. During the spring of 2000, Powerscreen intro-

duced the brand new Turbo Chieftain 1400 at Intermat in Paris, France. Mounted on a

heavy-duty crawler undercarriage and with hydraulically folding conveyors, the Turbo Chieftain

1400 is easily transportable, highly maneuverable on site, and designed for high volume

processing and stockpiling of aggregates, overburden, coal, crushed stone, and demolition

debris up to 500 tons per hour. With set-up time of 15 minutes and the ability to be reduced

to a compact size for road travel, the machine has been gaining market share since its introduction.

The acquisition of Terexlift, formerly Italmacchine, in the fall of 1998 brought to Terex a

solid manufacturer of telescopic material handlers for construction and agricultural applica-

tions. The cost and performance advantage of this product line manufactured near Perugia,

Italy, provided Terex with the opportunity to introduce a popular 5,100 pounds lifting capac-

ity, rough terrain unit to the United States. The TX51-19 is a compact and versatile machine

that is easily transportable. The unit’s ability to operate in many diverse work environments

such as drywall, masonry, landscape, and general contracting activities has made this unit very

popular in the U.S. since its introduction in early 2000. Terex Lifting is finding many new

applications for this unit mainly because it is larger than a skid steer loader, but smaller than

most average telescopic handlers.

Above: The Powerscreen

Turbo Chieftain 1400

provides three-way

separation and stockpiling

of material.

Below: The TX51-19

telescopic material

handler has 5,100

pounds of lifting capacity,

19 feet of reach and

weighs only 9,500

pounds, making it a

versatile and easily

transportable machine.

customer satisfaction

BU

ILD

ING

A B

ET

TE

R C

OM

PA

NY

TH

RO

UG

H

12

T E R E X C O R P O R A T I O N

A D E L I G H T E D C U S TO M E R A LWAY S R E T U R N S

W I T H R E P E AT B U S I N E S S .

13

In early 2000, Terex Lifting initiated a new aftermarket program, Support-Plus, designed

to provide faster and better service to its customers. The objective of Support-Plus is to strate-

gically locate field service technicians throughout North America and Europe to provide

on-site technical assistance to any customer of Terex Lifting. These technicians are equipped

with vans that have CD-ROMs for parts, service, and maintenance material, fax-capable

mobile phones, vehicle locator systems, and global positioning systems that provide voice

turn-by-turn directions to assist them in getting to the customers as quickly as possible.

Mr. Tony Sacco, Director of Product and Service Assurance at Maxim Crane Works said,

“Terex is now the most responsive company in the industry. Support-Plus is a very innovative

program that has significantly improved Terex’s aftermarket support.”

With sales in excess of $800 million, Joannou & Paraskevaides (J&P) based in Athens,

Greece, is ranked among the top 40 international contractors worldwide. J&P has been a

customer of Terex Italia, based near Bologna, Italy, for the past five years and has purchased

25 hydraulic mobile cranes since 1996. During 2000, J&P ordered six cranes. Two of these

particular units were initially used for the construction of a new polypropylene plant in

Salonica, Greece. Mr. Costas Timotheou of J&P stated, “Both units were delivered within

a week after they were ordered, and the machines were commissioned and the operators

trained in record time. Both units are performing very well, and we continue to be very

satisfied with the level of aftermarket support we receive from Terex.”

A Cedarapids customer based in Minneapolis, Minnesota, who previously contracted

out his crushing and screening work, chose to enter this field through the purchase of both

a jaw primary plant and a portable MVP 380 Rollercone crusher system as part of his

recycling operation. This portable closed circuit, dual crusher operation is being used to

recycle concrete for the expansion of the Minneapolis-St. Paul airport. The equipment

owner, Mr. Frank Frattalone, has found the Cedarapids system to be extremely forgiving, and

it has enabled the recycling operation at the airport to achieve tonnage rates unmatched by

competitive systems. Mr. Frattalone commented, “I looked at a lot of different crushers

before we bought this system. It is very productive and the Cedarapids dealer has been very

helpful. We really like the Cedarapids products because they are state-of-the-art.”

Above: The red Terex

van, a symbol of the new

Support-Plus aftermarket

program initiated in 2000.

Below: The combination

of a Cedarapids primary

plant with a Rollercone

crusher provides a high

capacity, low maintenance

recycling system.

brand recognition

BU

ILD

ING

A B

ET

TE

R C

OM

PA

NY

TH

RO

UG

H

14

T E R E X C O R P O R A T I O N

I N C R E A S E D P RO D U C T I V I T Y A N D T H E H I G H E S T R E T U R N

O N I N V E S T E D C A P I TA L A R E T H E H A L L M A R K S O F T E R E X P RO D U C T S .

15

For the past seven years, rigid trucks built in Motherwell, Scotland, have played a critical

role in fulfilling the international demand for some of the world’s lowest sulfur coal located

in the Pasir coal mine in Kalimantan, Indonesia, with annual production set to reach ten

million tons in 2001. The first order of Terex off-highway trucks, twenty-three 55-ton capacity

trucks, went into operation at Pasir in 1993, and, by now, each truck has logged between

27,000 and 33,000 operating hours. Another twenty-three 85-ton and 100-ton trucks

followed that order between 1998 and 2000. Due to the exceptional performance of these

trucks, the customer recently ordered eight newly redesigned 100-ton capacity trucks for its

fleet. Annual output at the Pasir coalfield is expected to increase to 12 million tons by the

end of 2002, aided in no small way by the reliability and performance of the Terex fleet.

In the spring of 1999, Terex Mining entered into a multi-year $100 million supply con-

tract agreement with one of the world’s leading international mining groups for the delivery

of 205-ton and 260-ton rear dump surface mining trucks. During the second half of 1999

alone, Unit Rig received a $46 million order under that agreement for the customer’s biggest

mine, located in Boron, California. The record productivity of these machines, coupled

with one of the lowest maintenance profiles in the industry, led to another multi-year supply

contract in the second half of 2000 with the same customer for the sale of Terex Mining’s

hydraulic mining shovels. The world’s largest mining companies are increasingly recognizing

the value proposition being delivered by Terex’s package of surface mining trucks and

hydraulic shovels.

For the past 56 years, Telelect, based in Watertown, South Dakota, has been manufacturing

world-class digger derricks and Hi-Ranger articulated aerial devices for their customers. Digger

derricks are used to set telephone poles, while articulated aerial devices are used to elevate

construction personnel to work areas at the top of utility poles or in trees. Since 1996,

Telelect has developed a growing business with the world’s largest tree-trimming company.

The relationship began with the first order of 100 units in 1996, and since that time, the

customer has been delighted with the performance of the machines. Because of the reliability

and excellent maneuverability of these machines, they have taken delivery of 2,200 units

over the past four years, making Telelect their primary supplier.

Above: The TR100, a

100-ton, rigid, off-high-

way truck is being used to

mine coal in Indonesia.

Below: The Telelect

digger derrick has sheave

heights exceeding 95 feet

and lifting capacities up

to 48,000 pounds.

organizational effectiveness

BU

ILD

ING

A B

ET

TE

R C

OM

PA

NY

TH

RO

UG

H

16

T E R E X C O R P O R A T I O N

T H E T E R E X M OT TO " FA S T E R A N D B E T T E R " I S R E A L I Z E D

T H RO U G H A B U S I N E S S M O D E L O F O U T S O U RC I N G A N D LOW O V E R H E A D .

17

Terex is proud of its ability to operate a very lean and cost-effective organization.

Over the past six years, we have managed to reduce our operating expenses as a percentage

of revenues from 11.5% to 7.8%. This level of operating expenses compares very favorably

with the rest of the capital goods industry and requires a continuing effort to streamline the

organization and to eliminate non value-added functions throughout the Company.

During the third quarter of 2000, the Company finalized plans to integrate its surface

mining truck and hydraulic shovel businesses. The integration of these businesses, which

should generate savings in excess of $6 million, strengthens its sales and marketing effective-

ness with the customer base, creates an improved and more uniform manufacturing model,

and better utilizes key aftermarket service and support, purchasing and financial resources.

Terex’s parts distribution center in Southaven, Mississippi, has been upgrading its

computer system in order to deliver better service to its customers. The center has reduced

cycle times for expediting purchase orders by using automatic e-mails. Automatic e-mails are

being sent to vendors requesting best delivery dates on open purchase orders as soon as an

item becomes backordered. This has increased productivity and reduced handling costs.

Parts are now also being set-up to order automatically upon customer order entry. Purchase

orders are system-generated and e-mailed directly to the vendor without human intervention

and are placed within 15 minutes of order entry, making same day shipment of non-stock

items possible. This system is being used to expand non-stock item sales and significantly

reduce inventory at the distribution center.

In the fall of 2000, Terex Lifting implemented a new program designed to reduce

warranty claim costs and improve the quality of its 2-axle rough terrain hydraulic mobile

cranes as part of the ongoing effort to improve the cost-effectiveness of their operation. The

objective of this program is to hold suppliers responsible for the costs incurred by Terex as

a result of quality problems encountered during the warranty period and to induce process

improvement and redesign at the supplier level. Over the past six months under this

program, total warranty costs have declined 30 percent due to supplier participation and

the performance of the supplier base has increased markedly.

Above: The powerful

combination of a Unit

Rig surface mining

truck teamed with an

O&K 800-ton hydraulic

excavator is the most

productive package in

the mining industry.

Below: The RT555 rough

terrain hydraulic mobile

crane, manufactured

in Waverly, Iowa, has

a maximum lifting

capacity of 55 tons and

a maximum tip height

of 170 feet.

18

Terex Corporation

Board of Directors

Ronald M. DeFeoChairman of the Board

G. Chris AndersenPartner, Andersen, Weinroth andCo., L.P.

Don DeFossetPresident and Chief OperatingOfficer, Walter Industries, Inc.

William H. FikePresident, Fike & Associates

Dr. Donald P. JacobsDean, J.L. Kellogg GraduateSchool of Management,Northwestern University

Marvin B. RosenbergSenior Vice President and GeneralCounsel, Terex (retired)

David A. SachsManaging Director, AresManagement, L.P.

Corporate Officers

Joseph F. ApuzzoChief Financial Officer

Kevin A. BarrVice President, Human Resources

Eric I CohenSenior Vice President, Secretary and General Counsel

Ronald M. DeFeoChairman, President and Chief Executive Officer

Brian J. HenryVice President, Finance, BusinessDevelopment

Jack LascarVice President, Investor Relationsand Corporate Communications

Kevin M. O'ReillyController

Susan K. SutherlandTreasurer

Transfer Agent and RegistrarAmerican Stock Transfer & Trust Company 40 Wall Street, 46th FloorNew York, New York 10005(800) 937-5449 or(212) 936-5100

Shareholders seeking information concerning stock transfers, change ofaddresses and lost certificatesshould contact the Company'sstock transfer agent directly.American Stock Transfer & TrustCompany may also be contacted atwww.amstock.com.

Stock InformationStock Symbol: TEX

Stock Exchange: New York StockExchange

The high and low quarterly salesprices for the past two years ofTerex Corporation are as follows:

Q1 Q2 Q3 Q4

2000High 287/8 171/4 191/2 173/16

Low 111/8 123/8 12 119/16

1999High 281/2 351/2 317/8 311/2

Low 221/8 231/4 241/4 2413/16

Annual Report/Form 10-KAdditional copies of the Annual Report/Form 10-K are available from Terex corporate headquarters by calling (203) 222-5942.

Annual MeetingThe Annual Meeting of Shareholderswill be held at 10:00 a.m. (EasternTime) on Tuesday, May 15, 2001at Terex Corporation, 500 PostRoad East, Suite 320, Westport,Connecticut.

Corporate Headquarters

Terex Corporation500 Post Road East, Suite 320Westport, Connecticut 06880 Telephone: (203) 222-7170Fax: (203) 222-7976Website: www.terex.com

EarthKing, Inc.500 Post Road East, Suite 240Westport, Connecticut 06880Telephone: (203) 222-6100Fax: (203) 226-7100Website: www.earthking.com

Business Operations

Terex LiftingFil Filipov, President

Terex Lifting North AmericaBaraga, Michigan, USAConway, South Carolina, USAHuron, South Dakota, USAOlathe, Kansas, USAWatertown, South Dakota, USAWaverly, Iowa, USAWilmington, North Carolina, USA

Terex Lifting EuropeCork, IrelandCrespellano, ItalyFontanafredda, ItalyHoorn, The NetherlandsMontceau-les-Mines, FrancePerugia, ItalyTetbury, EnglandTrier, Germany

Terex Lifting AustraliaBrisbane, Australia

Terex EarthmovingErnest R. Verebelyi, President

Terex Construction/TerexPowerscreenColin Robertson, ManagingDirector

Benford LimitedWarwick, England

Fermec Manufacturing LimitedManchester, England

North Hauler LLC (Joint Venture)Baotou, Inner Mongolia, People'sRepublic of China

Terex Americas (North and South America) Tulsa, Oklahoma, USA

Terex Equipment LimitedMotherwell, Scotland

Terex U.K. Ltd. (U.K. Distributor)Watford Village, England

Terex PowerscreenB.L. PegsonCoalville, England

Finlay Hydrascreens LimitedOmagh, Northern Ireland

Powerscreen InternationalDungannon, Northern Ireland

Powerscreen LimitedKilbeggan, Ireland

Re-Tech and Royer Industries Lebanon, Pennsylvania, USA

Simplicity EngineeringDurand, Michigan, USA

Terex Mining InternationalPeter Rall, Managing Director

O & K MiningDortmund, Germany

Terex Mining AmericasBrian King, President

Payhauler Corp.Tulsa, Oklahoma, USA

Unit Rig DivisionTulsa, Oklahoma, USA

CedarapidsKerry O’Sullivan, General Manager

CedarapidsCedar Rapids, Iowa, USA

Canica-JaquesVancouver, Washington, USA

JaquesMelbourne, Australia

Standard HavensGlasgow, Missouri, USA

Terex Light Construction/Terex Worldwide PartsDistribution CenterMurray Scott, Vice President and General Manager

Amida IndustriesRock Hill, South Carolina, USA

Coleman EngineeringHolly Springs, Mississippi, USA

Terex Bartell Ltd.Brampton, Ontario, Canada

Terex Worldwide PartsDistribution CenterSouthaven, Mississippi, USA

Terex Employees Worldwide6,150 Full-time

S H A R E H O L D E R I N F O R M A T I O N

v i s i t o u r w e b s i t e : w w w . t e r e x . c o m

Corporate Divisions ProductsCompany Overview

Contact Us

Human Resources

Investor Relations

Over 50 Products

Listed by Division

Terex Distribution

Terex Earthmoving

Terex Financial

Terex Lifting

Terex Light Construction

Desig

ned

by: O

lsen

Graf

ix Gr

oup

Inc

NY P

rinte

d by

: San

dy A

lexa

nder

NJ

This Annual Report contains forward-looking information based on Terex's current expectations. Because forward-looking statements involve risks and uncertainties, actual results

could differ materially. For a more detailed description of such risks and uncertainties, see Terex's Annual Report on Form 10-K, included with this Annual Report, under the

heading "Management's Discussion and Analysis of Financial Condition and Results of Operations – Forward Looking Information." The forward-looking statements contained

herein speak only as of the date of this Annual Report. Terex expressly disclaims any obligation or undertaking to update or revise any forward-looking statement contained in this

Annual Report to reflect any change in its expectations.

Benford Limited B.L. Pegson Canica-Jaques CedarapidManufacturing Limited Finlay Hydrascreens LimitedLimited Re-Tech Royer Industries Simplicity EngineeAustralia Holland Lift Terexlift Terex Lifting UK PeiItalia Terex Lifting Conway Operations Terex LiftingColeman EngineerinG Benford Limited B.L. Pegson CaPayhauler Fermec Manufacturing Limited Finlay HydInternational Powerscreen Limited Re-Tech Royer InCrane Comedil Terex Lifting Australia Holland Lift Limited Terex Handlers Terex Italia Terex Lifting CoIndustries Bartell Industries Coleman EngineerinG Equipment Limited Unit Rig Payhauler Fermec ManufPowerscreen International Powerscreen Limited ReAmerican Crane Comedil Terex Lifting Australia HolAerials Limited Terex Handlers Terex Italia Terex LiftRO Amida Industries Bartell Industries Coleman EngTerex Equipment Limited Unit Rig Payhauler Fermec Mining Powerscreen International Powerscreen LiHavens American Crane Comedil Terex Lifting AustrTelelect Terex Aerials Limited Terex Handlers Terex

T E R E X C O R P O R A T I O N

5 0 0 P O S T R O A D E A S T , S U I T E 3 2 0

W E S T P O R T , C T 0 6 8 8 0

( 2 0 3 ) 2 2 2 - 7 1 7 0

W W W . T E R E X . C O M

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) ⌧ OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2000

or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) o OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from __________ to __________.

Commission File Number 1-10702

TEREX CORPORATION (Exact Name of Registrant as Specified in Charter)

Delaware 34-1531521 (State of incorporation) (I.R.S. Employer Identification No.) 500 Post Road East, Suite 320, Westport, Connecticut 06880 (Address of principal executive offices) (Zip Code) Registrant's Telephone Number, including area code: (203) 222-7170

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $.01 par value (Title of Class)

New York Stock Exchange

(Name of Exchange on which Registered)

Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90 days. YES X NO____

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ⌧

The aggregate market value of the voting and non-voting common equity stock held by non-affiliates of the Registrant was approximately $496.4 million based on the last sale price on March 13, 2001.

The number of shares of the Registrant's Common Stock outstanding was 26,810,105 as of March 13, 2001.

DOCUMENTS INCORPORATED BY REFERENCE: Portions of the Terex Corporation Proxy Statement to be filed with the Securities and Exchange Commission

within 120 days after the year covered by this Form 10-K with respect to the 2001 Annual Meeting of Stockholders are incorporated by reference into Part III hereof.

- 2 -

TEREX CORPORATION AND SUBSIDIARIES Index to Annual Report on Form 10-K For the Year Ended December 31, 2000

Page

PART I

Item 1 Business........................................................................................................................................................................ 3 Item 2 Properties ...................................................................................................................................................................... 17 Item 3 Legal Proceedings ....................................................................................................................................................... 19 Item 4 Submission of Matters to a Vote of Security Holders ........................................................................................... 19

PART II

Item 5 Market for Registrant's Common Stock and Related Stockholder Matters ........................................................ 19 Item 6 Selected Financial Data............................................................................................................................................... 20 Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations......................... 21 Item 7A Quantitative and Qualitative Disclosure about Market Risk................................................................................ 28 Item 8 Financial Statements and Supplementary Data....................................................................................................... 29 Item 9 Changes in and Disagreements with Accountants on Accounting and Financial Disclosures ..................... 30

PART III

Item 10 Directors and Executive Officers of the Registrant ................................................................................................ * Item 11 Executive Compensation ............................................................................................................................................ * Item 12 Security Ownership of Certain Beneficial Owners and Management.................................................................. * Item 13 Certain Relationships and Related Transactions.................................................................................................... *

PART IV Item 14 Exhibits, Financial Statement Schedules and Reports on Form 8-K .................................................................... 30 * Incorporated by reference from Terex Corporation Proxy Statement to be filed with the Securities and Exchange Commission with respect to the 2001 Annual Meeting of Stockholders.

- 3 -

As used in this Annual Report on Form 10-K, unless otherwise indicated, Terex Corporation, together with its consolidated subsidiaries, is hereinafter referred to as "Terex," the "Registrant," or the "Company."

PART I ITEM 1. BUSINESS General Terex is a diversified global manufacturer of a broad range of equipment for the construction, infrastructure and mining industries. The Company strives to build a growing franchise under the Terex brand name. The Company remains focused on its mission of delivering products that are reliable, productive and cost-effective, and of producing equipment that improves our customers’ return on invested capital. The Company primarily organizes itself into two business segments, Terex Lifting and Terex Earthmoving. The Company's products are manufactured at 39 plants in the United States, Europe, Australia and Asia, and are sold primarily through a worldwide distribution network with over 1,000 locations to the global construction, infrastructure and surface mining markets. Over the past several years, the Company has implemented a series of interrelated operational and strategic initiatives designed to create a competitive advantage in the marketplace. These include (i) increasing the variable portion of its manufacturing costs to over 80% of total costs; (ii) reducing operating expenses as a percentage of revenues substantially below the industry’s average and eliminating non value-added functions throughout the organization; (iii) providing our customers with a cost-effective product line; and (iv) diversifying the Company’s product line in order to maximize financial performance. For financial information about the Company's industry and geographic segments, see Note O --- "Business Segment Information" in the Notes to the Consolidated Financial Statements and "Management's Discussion and Analysis of Financial Condition and Results of Operations." Terex Lifting Terex Lifting manufactures and sells telescopic mobile cranes (including rough terrain, truck and all terrain mobile cranes), tower cranes, lattice boom cranes, utility aerial devices (including digger derricks and articulated aerial devices), telescopic material handlers (including container stackers and rough terrain), truck mounted cranes (boom trucks), aerial work platforms (including scissor, articulated boom and straight telescoping boom aerial work platforms)and related components and replacement parts. Construction and industrial customers, as well as utility companies, are the primary users of these products. Customers use these products to lift equipment, material or workers to various heights. Throughout the world market, mobile cranes are principally sold to rental companies and dealers with rental fleets. Terex Lifting's mobile crane market share varies by geographical area; however, the Company believes it is the leading manufacturer of mobile cranes in France, Italy and Spain and is the second largest manufacturer in the United States (and the Company believes it is the largest manufacturer of commercial hydraulic mobile cranes in the United States). The Company also believes that it is the second largest manufacturer in the United States of utility aerial devices and the third largest manufacturer of tower cranes worldwide. Terex Lifting has 15 significant manufacturing operations: (i) PPM S.A.S. located in Montceau-les-Mines, France, at which mobile cranes and container stackers under the brand names TEREX and PPM are manufactured; (ii) Terex Italia S.r.l., located in Crespellano, Italy, at which mobile cranes are manufactured under the TEREX, BENDINI and PPM brand names; (iii) PPM Cranes, Inc. (also known as Terex Cranes – Conway Operations), located in Conway, South Carolina, at which rough terrain hydraulic telescoping mobile cranes and truck cranes are manufactured under the P&H (a licensed trademark of Harnischfeger Corporation) and TEREX brand names; (iv) Terex Lifting - Waverly Operations (also known as Koehring Cranes, Inc.), located in Waverly, Iowa, at which rough terrain hydraulic telescoping mobile cranes and truck cranes are manufactured under the brand names TEREX and LORAIN, and aerial lift equipment is manufactured under the brand names TEREX AERIALS and TEREX; (v) Terex-Telelect, Inc. ("Telelect"), located in Watertown, South Dakota, at which utility aerial devices and digger derricks are manufactured under the TELELECT and HI-RANGER brand names; (vi) Terex Aerials Limited, located in Cork, Ireland, at which aerial platforms are manufactured under the TEREX brand name; (vii) Terex-RO Corporation ("Terex RO"), located in Olathe, Kansas, at which truck mounted cranes are manufactured under the RO-STINGER brand name; (viii) Terex Handlers, located in Baraga, Michigan, at which rough terrain telescopic boom material handlers are manufactured under the SQUARE SHOOTER and TEREX brand names; (ix) Holland Lift International B.V. (“Holland Lift”), located in Hoorn, The Netherlands, at which aerial platforms are manufactured under the HOLLAND LIFT brand name; (x) The American Crane Corporation ("American Crane") located in Wilmington, North Carolina, at which lattice boom cranes are manufactured under

- 4 -

the AMERICAN brand name; (xi) Terexlift S.r.l. ("Terexlift"), located near Perugia, Italy, at which rough terrain telescopic material handlers are manufactured under the ITALMACCHINE and TEREX brand names and cement mixers and concrete pumps are manufactured under the ITALMACCHINE brand name; (xii) Terex Peiner GmbH ("Peiner"), located in Trier, Germany, at which tower cranes are manufactured under the PEINER trade name; (xiii) Gru Comedil S.p.A. ("Comedil"), located in Fontanafredda, Italy, at which tower cranes are manufactured under the COMEDIL trade name; (xiv) Terex Lifting U.K. Limited ("Terex Lifting U.K."), located in Tetbury, England, at which material handlers are manufactured under the MATBRO trade name; and (xv) Terex Lifting Australia Pty. Ltd. ("Terex Lifting Australia"), located in Brisbane, Australia, at which all terrain mobile cranes are manufactured under the FRANNA trade name. The Company has been actively involved in both acquiring and disposing of operations with the Terex Lifting segment. In July 1999, as part of the acquisition of Powerscreen International plc, the Company acquired the material handling operations of Matbro Limited (now Terex Lifting U.K.) and Moffett Engineering Limited (“Moffett”). Moffett, located in Dundalk, Ireland, manufactures truck-mounted forklifts. On November 3, 1999, the Company completed the acquisition of the Material Handling Division of Teledyne, Inc., which included substantially all of the assets comprising the Princeton business and all of the capital stock of Teledyne GmbH, the owner of Kooi B.V. (collectively, “Princeton/Kooi”). Princeton/Kooi manufacture and market truck-mounted forklifts at facilities in Canal Winchester, Ohio and Vrouwenparochie, The Netherlands. On December 1, 1999, the Company comp leted the purchase of Terex Lifting Australia, formerly known as Franna Cranes Pty. Ltd., a manufacturer of all-terrain “pick and carry” cranes in Australia. See Note B – “Acquisitions” in the Notes to the Consolidated Financial Statements for further information. On September 30, 2000, the Company completed the sale of its truck-mounted forklift businesses, consisting of Moffett and Princeton/Kooi, to various subsidiaries of Partek Corporation of Finland for $144 million in cash, subject to adjustment. See Note C – “Sale of Businesses” in the Notes to the Consolidated Financial Statements for further information. Terex Earthmoving Terex Earthmoving manufactures and sells large hydraulic excavators, loader backhoes, articulated and rigid off-highway trucks, high capacity surface mining trucks, scrapers, crushing and screening equipment, asphalt pavers, asphalt mixing plants, and related components and replacement parts. These products are used primarily by construction, mining, quarrying and government customers. The Company believes that it has the leading market share for large hydraulic excavator models having machine weights in excess of 200 tons, that it is a significant competitor in the market for large capacity off highway haulers and scrapers and that it had the leading market share in high capacity surface mining trucks since 1999. Terex Earthmoving has 16 significant manufacturing operations: (i) Terex Equipment Limited ("TEL"), located in Motherwell, Scotland; (ii) Unit Rig ("Unit Rig") and Payhauler Corp. ("Payhauler"), located in Tulsa, Oklahoma; (iii) O&K Mining GmbH (“O&K Mining”), located in Dortmund, Germany; (iv) Powerscreen International Distribution Ltd. (“Powerscreen”), located in Dungannon, Northern Ireland and Kilbeggan, Ireland; (v) Finlay Hydrascreens (Omagh) Limited ("Finlay"), located in Omagh, Ireland; (vi) BL-Pegson Ltd. ("B.L. Pegson"), located in Coalville, England; (vii) Simplicity Engineering ("Simplicity"), located in Durand, Michigan; (viii) Royer Industries, Inc. and Re-Tech (collectively “Royer/Re-Tech”), located in Lebanon, Pennsylvania; (ix) Benford Limited ("Benford"), located in Warwick, England; (x) Cedarapids, Inc. (“Cedarapids”) located in Cedar Rapids, Iowa; (xi) Standard Havens, Inc. ("Standard Havens"), located in Glasgow, Missouri; (xii) Jaques International (“Jaques”), located in Melbourne, Australia; (xiii) Canica-Jaques, located in Vancouver, Washington; (xiv) Jaques International Sdn Bhd (“Jaques Malaysia”), located in Subang Jaya, Malaysia; (xv) Jaques (Thailand) Limited (“Jaques Thailand”), located in Chomburi, Thailand; and (xvi) Fermec Manufacturing Limited (“Fermec”) located in Manchester, England. TEL manufactures, sells and markets off-highway rigid haulers and articulated haulers, having capacities ranging from 25 to 100 tons, and scrapers that load, move and unload large quantities of soil for site preparations, including roadbeds. TEL's products are sold under the Company's TEREX brand name. Unit Rig and Payhauler manufacture, sell and market electric rear hauler trucks with payload capacities ranging from 50 to 360 tons and bottom dump haulers with capacities ranging from 180 to 270 tons, principally sold to copper, gold, iron ore, coal, borates and diamond mining industry customers, as well as all wheel drive rigid off-highway trucks. O&K Mining manufactures and sells large hydraulic mining shovels. Cedarapids, Finlay, Powerscreen, B.L. Pegson, Simplicity, Royer/Re-Tech, Jaques, Jaques Malaysia, Jaques Thailand and Canica-Jaques manufacture, sell and market crushing and screening equipment. Cedarapids also manufactures, sells and markets a line of asphalt pavers and associated equipment. Standard Havens manufactures, sells and markets asphalt plants. Benford manufactures, sells and markets dumpers and compactors. Fermec manufactures, sells and markets loader backhoes. These products are sold under the Company's TEREX, UNIT RIG, LECTRA HAUL, O&K, PAYHAULER, POWERSCREEN, FINLAY, SIMPLICITY, CEDARAPIDS, BENFORD, B.L. PEGSON, ROYER, RE-TECH, CEDARAPIDS/STANDARD HAVENS, JAQUES, CANICA-JAQUES and FERMEC brand names. TEL's North, Central and South American sales and distribution are managed

- 5 -

by Terex Americas, a division of the Company, located in Tulsa, Oklahoma. In addition, Terex Earthmoving has an interest in North Hauler Limited Liability Company (“North Hauler Limited”), a corporation incorporated under the laws of China, a joint venture with Second Inner Mongolia Machinery Company for the production of haulers in China. North Hauler Limited manufactures and sells heavy trucks, principally used in mining, at a facility in Baotou, Inner Mongolia, and the People’s Republic of China. The Company has made a number of significant acquisitions in the Terex Earthmoving segment in recent years as part of its continuing plan to diversify its product offerings and the geographic range of its customers. In January 2001, the Company acquired Jaques, Canica-Jaques, Jaques Malaysia and Jaques Thailand (collectively, the “Jaques Group”), manufacturers of crushing equipment in Australia, Asia and North America. On December 28, 2000, the Company acquired Fermec from CNH Global N.V., adding the loader backhoe product line to Terex Earthmoving’s offerings. The Company entered the aggregates industry with its acquisitions of Powerscreen International plc in July 1999 for a purchase price of approximately $294 million and Cedarapids on August 26, 1999 for approximately $170 million, subject to adjustment. The acquisitions of Powerscreen International plc and Cedarapids provided the Company with a significant market position in the crushing and screening equipment markets. On March 31, 1998, the Company acquired O&K Mining from O&K Orenstein & Koppel AG for net aggregate consideration of approximately $168 million, subject to adjustment. See Note B – “Acquisitions” in the Notes to the Consolidated Financial Statements for further information. Other Terex Light Construction manufactures and sells mobile and portable floodlighting systems, concrete power trowels, concrete placement systems, concrete finishing systems, concrete mixers, generators, traffic control products, and related components and replacement parts. These products are typically used for rental and construction applications. Terex Light Construction has three significant manufacturing operations: (i) Amida Industries, Inc. (“Amida”), located in Rock Hill, South Carolina, which manufactures and sells portable floodlighting systems, concrete power trowels, concrete placement systems, concrete finishing systems, concrete mixers and traffic control products under the AMIDA, BARTELL, MORRISON, BENFORD, MULLER and TEREX brand names; (ii) Terex Bartell, Ltd. (“Bartell”), located in Brampton, Ontario, Canada, which manufactures and sells concrete power trowels and concrete finishing systems under the BARTELL brand name and (iii) Coleman Engineering, Inc. (“Coleman”) located in Holly Springs, Mississippi, which manufactures and sells portable floodlighting systems and generators under the COLEMAN ENGINEERING brand name. Terex Light Construction also distributes products in North America that are manufactured in the Benford facility in Warwick, England, including dumpers and compaction equipment. These products are sold under the Company’s AMIDA, BENFORD, and TEREX brand names. Terex Light Construction is structured to capitalize on the rental segment of the construction equipment industry. The Company's strategy is to expand its product offerings to the national rental companies, while maintaining its business with independent rental stores. The Company's consolidation efforts are intended to create value for customers through the synergies of the Company's sales force and elimination of costly distribution steps, such as manufacturer’s representatives, thus lowering the cost of the Company's products to its customers. The light equipment concept originated in April 1999 with the acquisition of Amida. The Terex Light Construction product line was broadened by the addition of the Benford line of comp action equipment as part of the July 1999 acquisition of Powerscreen, the acquisition of Bartell in September 1999, the acquisition of the Muller Mixer product line in February 2000 and the acquisition of Coleman in October 2000. See Note B – “Acquisitions” in the Notes to the Consolidated Financial Statements for further information. In January 2001, the Company announced the launching of an Internet site by its subsidiary EarthKing, Inc. (“Earthking”). In 2001, EarthKing is introducing its e-commerce capabilities as an independent and unbiased Internet marketplace for the construction and mining equipment industry. EarthKing’s goal is to use the Internet and technology to provide savings to users of construction and mining equipment in the selection, acquisition, management and disposition of their equipment and parts. EarthKing has developed agreements with several strategic partners to participate within the EarthKing alliance to provide reliable delivery of cost-effective services to its customers.

- 6 -

Products Telescopic Mobile Cranes Telescopic mobile cranes are used primarily for industrial applications, in commercial and public works construction and in maintenance applications, to lift equipment or material to heights in excess of 50 feet. Terex Lifting manufactures the following types of telescopic mobile cranes:

Rough Terrain Cranes -- are designed to lift materials and equipment on rough or uneven terrain. Rough terrain cranes are most often located on a single construction or work site such as a building site, a highway or a utility project for long periods of time. Rough terrain cranes cannot be driven on highways and accordingly must be transported by truck to the work site. Rough terrain cranes manufactured by Terex Lifting have maximum lifting capacities of up to 100 tons and maximum tip heights of up to 225 feet. Terex Lifting manufactures its rough terrain cranes at its facilities located at Waverly, Iowa, Conway, South Carolina and Crespellano, Italy under the brand names TEREX, LORAIN, P&H, PPM and BENDINI.

Truck Cranes -- have two cabs and can travel rapidly from job site to job site at highway speeds. In contrast to rough terrain cranes, which are often located for extended periods at a single work site, truck cranes are often used for multiple local jobs, primarily in urban or suburban areas. Truck cranes manufactured by Terex Lifting have maximum lifting capacities of up to 75 tons and maximum tip heights of up to 193 feet. Terex Lifting manufactures truck cranes at its Waverly, Iowa and Conway, South Carolina facilities under the brand names TEREX, P&H and LORAIN.

All Terrain Cranes -- were developed in Europe as a cross between rough terrain and truck cranes in that they are designed to travel across both rough terrain and highways. All terrain cranes have two cabs and are versatile and highly maneuverable. All terrain cranes manufactured by Terex Lifting have lifting capacities of up to 130 tons and maximum tip heights of up to 246 feet. Terex Lifting manufactures its all terrain cranes at its Montceau-les-Mines, France and Brisbane, Australia facilities under the brand names TEREX, PPM and FRANNA.

Tower Cranes Tower cranes lift construction material to heights and place the material at the point where it is being used. They include a stationary vertical tower near the top of which is a horizontal jib with a counterweight. On the jib is a trolley through which runs a load carrying cable and which moves the load along the jib length. On larger cranes, the operator is located above the work site where the tower and jib meet, providing superior visibility. The jib also rotates 360 degrees, creating a large working area equal to twice the jib length. Luffing jib tower cranes have an angled jib with no trolley, and operate like a traditional lattice boom crane mounted on a tower. Luffing jib tower cranes are often used in urban areas where space is constrained. Tower cranes are currently produced by Terex under the PEINER, COMEDIL and TEREX brand names. Terex produces the following types of tower cranes:

Self-Erecting Tower Cranes -- are trailer mounted and unfold from four sections (two for the tower and two for the jib); certain larger models have a telescopic tower and folding jib. These cranes can be assembled on site in a few hours. Applications include residential and small commercial construction. Crane heights range from 50-75 feet and jib lengths from 60-100 feet.

Hammerhead Tower Cranes -- have a tower and a horizontal jib assembled from sections. The tower extends above the jib to which suspension cables supporting the jib are attached. These cranes are assembled on-site in one to three days depending on height, and can increase in height with the project; they have a maximum free-standing height of 200 feet and a maximum jib length of 240 feet.

- 7 -

Flat Top Tower Cranes -- have a tower and a horizontal jib assembled from sections. There is no tower extension above the jib, which reduces cost and facilitates assembly; the jib is self-supporting and consists of reinforced jib sections. These cranes are assembled on site in one to two days, and can increase in height with the project; they have a maximum freestanding height of 305 feet and a maximum jib length of 280 feet.

Luffing Jib Tower Cranes -- have a tower and an angled jib assembled from sections. The tower extends above the jib to which suspension cables supporting the jib are attached. Unlike other tower cranes, there is no trolley to control lateral movement of the load, which is accomplished by changing the jib angle. These cranes are assembled on site in two to three days, and can increase in height with the project; they have a maximum freestanding height of 185 feet and a maximum jib length of 200 feet.

Lattice Boom Cranes Terex Lifting produces crawler and truck mounted lattice boom cranes.