bulent eris model development for planning and forecasting in diagnostic and treatment systems...

TRANSCRIPT

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 1/182

T.C.MARMARA UNIVERSITY

INSTITUTE FOR GRADUATE STUDIES INPURE AND APPLIED SCIENCES

MODEL DEVELOPMENT FOR PLANNING ANDFORECASTING IN DIAGNOSTIC AND TREATMENT

SYSTEMS

Salih Bülent ER ŞMSc.(Management Engineering)

THESISFOR THE DEGREE OF DOCTOR OF PHILOSOPHY

ININDUSTRIAL ENGINEERING

SUPERVISOR

Prof.Dr. Erkan TÜRE

STANBUL 2004

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 2/182

T.C.MARMARA UNIVERSITY

INSTITUTE FOR GRADUATE STUDIES INPURE AND APPLIED SCIENCES

MODEL DEVELOPMENT FOR PLANNING ANDFORECASTING IN DIAGNOSTIC AND TREATMENT

SYSTEMS

Salih Bülent ER ŞMSc.(1412009 19920009)

THESISFOR THE DEGREE OF DOCTOR OF PHILOSOPHY

ININDUSTRIAL ENGINEERING

SUPERVISOR

Prof.Dr. Erkan TÜRE

STANBUL 2004

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 3/182

ACKNOWLEDGEMENTS

I would like to express my sincere gratitude to my thesis advisor, Prof. Dr. ErkanTüre, for his supervision, guidance, continued support and motivation throughout this study.

I wish to extend my thanks and Prof Dr. Sevil Ünal, Prof Dr. Sami Ercan, Prof. Dr.

Taylan Ula and Asst. Prof. Dr Güldal Büyükdamgacı for serving on my thesis committee and

for their valuable advices and comments.

Special appreciation is due to my General Manager Asst. Prof. Dr. Giray Velioğlu,

and Asst. General Manager Umur Çullu and my colleagues Burak Sayın, Deniz Sümengen,Esra Güler, Ulas Öncül, Ercan Tekin, Utku Birdal and Ali Özmen for their valuable technical

advice.

Finally, I would like to thank to my wife Nalan and son Onat for their patience,

encouragement and support

Eylül, 2003 Salih Bülent Eriş

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 4/182

TABLE OF CONTENTS

ACKNOWLEDGEMENTS.................................................I

TABLE OF CONTENTS....................................................II

ÖZET ..........................................................................................V

ABSTRACT .....................................................................................VI

ORIGINALITY CLAIM..................................................VII

LIST OF SYMBOLS............................................................. X

ABBREVATIONS..................................................................XI

LIST OF FIGURES............................................................XII

LIST OF TABLES..............................................................XIV

PART.I. INTRODUCTION AND OBJECTIVES ......................1

PART.II. GENERAL BACKGROUND ........................................4

II.1 PRIVATE HEALTH INSURANCE IN THE WORLD .......................4

II.2 TURKEY PRIVATE HEALTH INSURANCE BACKGROUND.......7

II.3 HEALTH RISK MODELS IN LITERATURE..................................11

II.3.1 Demographic Models .......................................................12

II.3.2 Prior Year Expenditures ...................................................14II.3.3 Diagnosis-Based Risk Adjustment....................................15

II.3.4 Information Derived from Prescription Drugs...................17

II.3.5 Self-Reported Health Information.....................................17

II.3.6 Mortality..........................................................................18

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 5/182

II.3.7 Other Models ...................................................................18

II.4 PRIVATE HEALTH INSURANCE PRICING .................................18

II.4.1 Practice of Pricing in the World........................................18

II.4.2 Theory of Health Insurance Pricing ..................................23

PART.III. ANALYSIS OF THE DATA........................................26

III.1 DIAGNOSIS AND TREATMENT SERVICES CATEGORIES.......27

III.1.1 Out- patient Treatment (without hospitalization) ............27

III.1.2 In-patient Treatment.............. ..........................................28

III.2 ESTIMATION OF PARAMETERS .................................................29

III.2.1 Prior year stats ................................................................30

III.2.2 Group size.......................................................................33

III.2.3 Parameters .............................................. ........................37

III.3 MOMENTS OF USAGE ..................................................................43

III.3.1 Comparison of the Data from Other Sources ...................50

PART.IV. THE MODEL................................................................52

IV.1 ALTERNATIVE MODELS..............................................................52

IV.1.1 Moments Based Approach ..............................................52

IV.1.2 Recursive Algorithm.......................................................55

IV.1.3 Inversion -Methods Fast Fourier- ....................................55

IV.2 SIMULATION MODEL STRUCTURE...........................................57

IV.2.1 Individual Expenses Module...........................................58IV.2.1.1 Pc, n, X 61 IV.2.1.2 Age and Gender 61 IV.2.1.3 Distribution Assumptions 61 IV.2.1.4 Limits and Deductibles 63 IV.2.1.5 Dependency 66 IV.2.1.6 Short Term Monthly Analysis 68

IV.2.2 Experience - Credibility Module .....................................75IV.2.2.1 Experience Rating with monthly and Quarter Yearly Periods 80

IV.2.3 Individual to Group Module............................................81

IV.2.4 Characteristics of the Model Output and Sensitivity........83IV.2.4.1 The Effect of Dependency 84 IV.2.4.2 The Effect of Group Size and Uncertainty on Individual to Group Module 87 IV.2.4.3 Sensitivity 90

PART.V. IMPLEMENTATION AND MODELVALIDATION ..........................................................95

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 6/182

V.1 IMPLEMENTATION.......................................................................95

V.1.1 Characteristic of the Sample Data ....................................95V.1.1.1 Age and Gender Profiles 95 V.1.1.2 Profile of Group 1 97 V.1.1.3 Profile of Group 2 97 V.1.1.4 Profile of Group 3 97

V.1.2 Scenarios .........................................................................97V.1.2.1 Output Analysis 99

PART.VI. CONCLUSION ...........................................................139

REFERENCES..............................................................................143

APPENDIX 1..........................................................................146

Definiton of the Actuary.............................................................146

Extreme Cases............................................................................148

APPENDIX 2..........................................................................150

APPENDIX 3..........................................................................157

CURRICULUM VITAE...............................................................161

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 7/182

ÖZET

TEŞH S VE TEDAV S STEMLER NDE PLANLAMA AMAÇLITAHM NE YÖNELK MODEL GEL ŞT R LMES

Bu çalışmanın amacı ülkemizdeki gerek özel sağlık sigortalarında gerekse sağlık

sandıklarındaki grupların kullanılmak üzere gelecekteki sağlık hizmetlerinden faydalanma

adetleri-miktarları ve maliyetlerini kısa ve orta vadede tahminde kullanılacak dinamik bir

model geliştirilmesidir. Bu çalışma simülasyon modelinin kurulması, duyarlılık analizi ve

7436 kişilik örnekli pilot uygulamalarla sınanmasıyla amaca ulaşmıştır. Güvenilir sonuçlara

ulaşabilmek amacıyla eldeki gerçek verilerden faydalanılarak çeşitli değişkenler

kullanılmıştır.

Geleneksel modellerde sadece grup büyüklüğüne dayanarak limit ve muafiyetinetkilerini göz ardı ettiğinden karşılaşılan risk ve dolayısıyla maliyetlerle ilgili yeterince bilgi

sağlamamaktadır. Bu çalışmada üç modül kullanılmıştır. Bireysel Harcamalar Modülü’nde

değişik yaş cinsiyet dağılımlarından oluşan gruplarda, değişik limit ve muafiyet sonucu ortaya

çıkacak maliyet tahminleri yapılmıştır. Bireysel’den Gruba Modülünde gerçek yaşamda

incelenmesi zor olan değişkenler arası bağımlılığın etkisi, tahmin üzerinde istatistiksel

dalgalanma ve bunların dışındaki, parametre hataları veya verinin uygunluğu gibi

belirsizliklerin etkilerinin nasıl incelenebileceği gösterilmiştir. Grubun önceki harcamalarının

değerlendirilmesi Deneyim-Kredibilite Modülü’nde kullanılmıştır.

Bu çalışmada ayrıca Türkiye’deki Sağlık hizmetleri konusunda ekonomi, ekonometri,

aktüerya ve yöneylem araştırması/endüstri mühendisliği konularında çok az sayıda araştırma

olduğundan tahmin konusundaki araştırmalara geniş olarak yer verilmiştir.

Eylül, 2003 Salih Bülent Eriş

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 8/182

ABSTRACT

MODEL DEVELOPMENT FOR PLANNING AND FORECASTING INDIAGNOSTIC AND TREATMENT SYSTEMS

In this study we intended to build a dynamic forecasting model for future health care

service costs and utilizations of the groups in the short and mid term ranges in private health

insurance and health funds. This study covers its scope by developing and testing validity of a

simulation model together with the sensitivity analysis and pilot applications on a sample of

7436 people. Real data have been used to describe a model with a number of variables so that

reliable forecasts can be made.

Traditional models that rely on just group size and ignore the effect of limit and

deductibles do not furnish adequate information on the potential risk and therefore the cost

involved. Three different modules have been used. In Individual Expenses Module cost

forecasts for the groups with different age and gender distributions where different limits and

deductibles are done. Factors which can not be tested in real life like interrelational

dependency between variables, statistical fluctuations due to group size, uncertainty due to

credibility and suitability of the data are examined in Individual to Group Module. Group

prior statistics are used in the Experience Rating – Credibility Module.

As there are very few academic or non-academic research studies on economics,econometrics, actuarial or operations research/industrial engineering fields concerning health

care services in Turkey we provided a wide range of literature for forecasting research on

health systems on different disciplines.

September, 2003 Salih Bülent Eriş

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 9/182

ORIGINALITY CLAIM

MODEL DEVELOPMENT FOR PLANNING AND FORECASTING INDIAGNOSTIC AND TREATMENT SYSTEMS

Health is a dynamic and relative concept both on individual and national base. The

objective of health care systems, their structures, functions, their effectiveness largely differ at

local, regional and national levels. Relations between the elements of the health care systems

and the interaction of these elements with the other elements like cultural behaviors of the

people in the society, environmental conditions etc have complex and dynamic

characteristics.

Strategic health care decision problems including medical, behavioral, socio-economic,

managerial and technical variables can be solved only by integrated and inter disciplinaryapproach. Quantitative techniques and methods have been applied with success for more than

30 years now in finding solutions to the health care decision problems of developed countries.

In Turkey, there is a multi provider health care system which is managed by the

Ministry of Health, social security organizations, armed forces, universities and private

organizations. This system has many problems like over utilization of health care services

leading to the huge health care expenses and budget deficits. Until now the government or the

other parties involved have offered solutions and approaches regarding the political medical,financial and organizational factors. But the approach of mathematical modeling and

prediction techniques that can be employed in health care systems to control the expenditures

and service utilization has been largely ignored .

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 10/182

The condition stated above is also valid for the insurance sector. When Turkish and big

European Health Insurance markets are observed, it is seen that there is enormous need for

development of forecasting models. It is nearly impossible to find neither detailed academic

studies nor application examples on decision-making and health insurance claims prediction

models. Models should be adaptive and should be suitable for all kinds of health insurance

products. Most of the common approaches in the market are far from supplying flexible

solutions for different health insurance products including various specifications. Simple

common assumptions, pricing and prediction approaches are believed to insufficient and so

they are criticized in this study

The problem in model building in health systems comes from the lack of data and the

uncertainty concerning the model structure, parameters and interrelations between variables.

The complexity (compound and mixed statistical nature of the health utilizations and costs)

makes it harder in addition to issues stated above.

The originality of this study is that it is the first example of a health care expenses

prediction simulation model in group health insurances in Turkish health insurance sector.

The model is purely constructed from the scratch using the actuarial, mathematical and

statistical techniques. The originality also lies in the real insurance claims data which was

derived from the health insurance expenses (claims) made by the insured population building

up the portfolio of a certain insurance company. In this context the data is unique andcontrollable since it is obtained through real observations and a well running IT system.

While building up the model, the stochastic nature of the process is examined and the

distribution characteristics of costs and utilizations in monthly and annual intervals are shown

depending on the real data.

The model has 3 different modules as follows;

A- Individual Expense Module: This module reduces the group medical expensesbehavior to individual and creates a representative individual expense form on an expense

type basis. The module variables are set as; probability of claiming (Pc), number of claims(n),

claim size(X) for demographical classes. Setting these variables is a new approach that allows

the usage of positively skewed or long tailed non-zero distributions, which are allocated to

severity and frequency of variables.

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 11/182

B-Experience and Credibility Module: This module combines the observed results of

the examined groups’ statistics with the standard portfolio values to improve the estimation.

This is done for the distributional characteristics of each utilization type (physician visit

prescribed drugs, etc) for each variable of the model (Pc, n and X). This is also another new

proposal to the actuarial study ground where the actuarial health studies are rarely

sophisticated.

C-Individual to Group Module: Taking into account the group size and the uncertainty

from other factors (trend, credibility and suitability of the data), this module examines the

possible variations on the empirical distribution output from the A and B modules to quantify

the stochastic nature. This prediction of uncertainty approach is also new to Turkish health

insurance sector.

The model presented in this study is a potentially useful tool for either private insurance

companies (which have approximately 700,000 insured) or health aid funds (which have more

than 270,000 members) in Turkey. The companies or health aid funds can determine the

distribution characteristics of health care needs for populations that are formed of people in

different age and gender groups. The suggested methods could also be used for social security

or governmental planning purposes when the data is based on a short-term period.

September, 2003 Prof.Dr. Erkan TÜRE Salih Bülent Eriş

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 12/182

LIST OF SYMBOLS

n :Claim Count(utilization of the observed health care service)

Pc :Probability of claimingX :Cost of the utilized health care service

αααα , λλλλ :Parameters of Gamma and Pareto distributions

σσσσ :Population STD

1 X φ :The characteristic functions of the input distributions

ω :The correlation matrix for two different benefits

γ γγ γ : Skewness

Z : Credibility

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 13/182

ABBREVATIONS

MSA : Medical Saving Accounts

MCO : Managed Care Organization

LER : Loss Elimination RatioLEV : Limited Expected Value

ACG : Ambulatory Care Group

DCG : Diagnostic Cost Group

DPS : Disability Payment System

HCC : Hierarchical Condition Categories.

ICD : International Classification of Diseases

CDS : Chronic Disease Score

NHE : National Health ExpenditureCPI : Consumer Price Increases

NCD: : No Claim Discount

RF: Rating Factors

PMPM: Per Member Per Month

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 14/182

LIST OF FIGURES

Figure II.1 Health Spending for Gender, Age Sample Netherlands........................................13

Figure II.2 Health Spending for Gender, Age Sample USA Privately Insureds......................13

Figure II.3 Health Spending for Gender, Age Sample USA Medicaid Eligibles ....................13Figure II.4 Distribution of population costs to the members for year one and two .................14

Figure II.5 Group and Individual Rating Structures ..............................................................19

Figure II.6 Distribution of Relative Costs Between Groups...................................................22

Figure III.1 Ratio of Users to the Population.........................................................................37

Figure III.2 Ratio of Physician Users in Age and Gender Band Population ...........................38

Figure III.3 Average Number of Visits for Different Age and Gender Bands ........................38

Figure III.4 Distribution of Number of Visits for Different Age and Gender Bands ..............39

Figure III.5 Average Cost Per Usage ....................................................................................39Figure III.6 Distribution of Visit Costs for Different Age and Gender Bands ........................40

Figure III.7 Gender and age effect on sample data ................................................................42

Figure IV.1 Output for Prescribed Drugs of a Group.............................................................56

Figure IV.2 Second Fourier Example....................................................................................57

Figure IV.3 Creation of the Input Parameters for Individual to Group Module + Experience-

Credibility Module........................................................................................................59

Figure IV.4 Iteration of the Individual Expense Module(fed with credibility if any) .............60

Figure IV.5 Hospital Claim Cost X graph produced with gamma and real data.....................62

Figure IV.6 Number of Physician Visits n graph produced with gamma and real data...........62

Figure IV.7 Limit and Deductible Application Process ................................. ........................64

Figure IV.8 Limit and Deductible Affect On Diagnostic Annual Costs.................................65

Figure IV.9 When various scenarios Applied Total Costs on Individual Basis ......................66

Figure IV.10 Development of Distributions..........................................................................69

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 15/182

Figure IV.11 Distribution of "n" in March and August..........................................................70

Figure IV.12 Flow Process for the Individual to Group Module............................................83

Figure IV.13 Std B coefficients for Total Costs Incurred ......................................................91

Figure IV.14 Std B coefficients for Total Costs After the Limits and Deductibles.................93

Figure V.1Graph of Group 1 Total Costs ............................................................................101

Figure V.2 Graph of Group 1 After First Scenario .............................................................104

Figure V.3 Graph of Group 1 After Second Scenario.........................................................108

Figure V.4 Graph of Group 2 Total Costs ...........................................................................110

Figure V.5 Graph of Group 2 After First Scenario .............................................................113

Figure V.6 Graph of Group 2 After Second Scenario.........................................................117

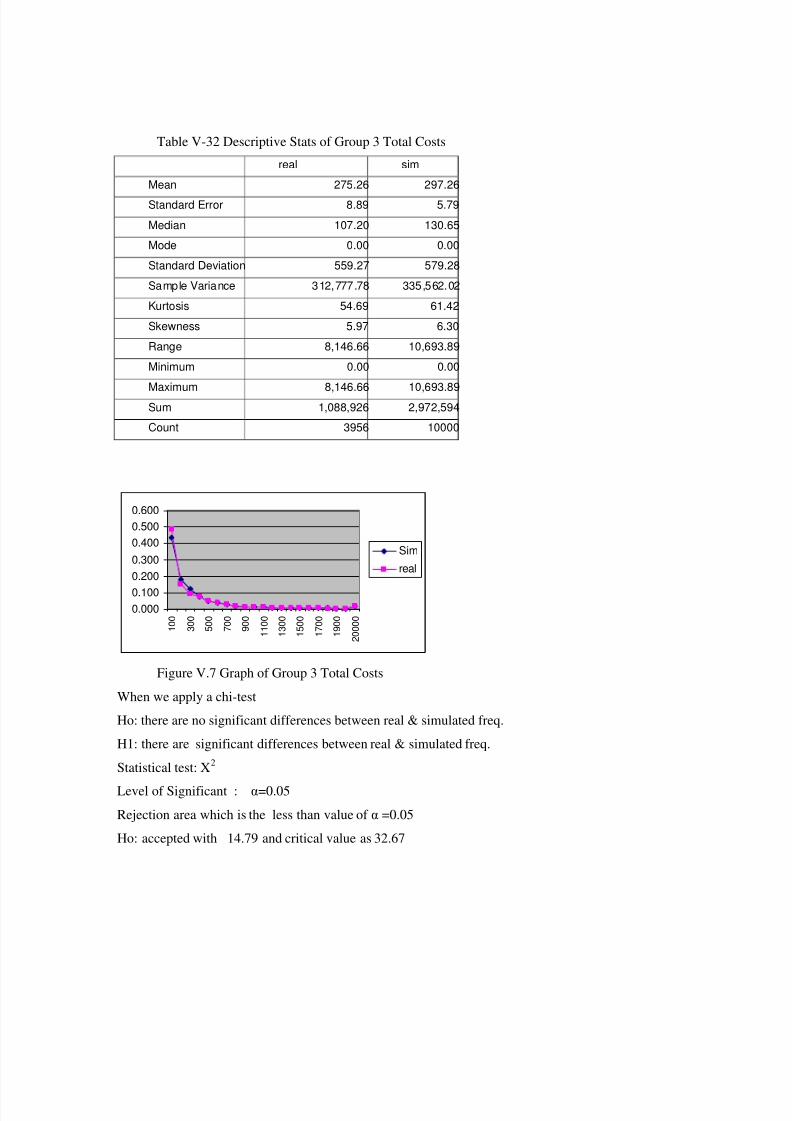

Figure V.7 Graph of Group 3 Total Costs ...........................................................................119

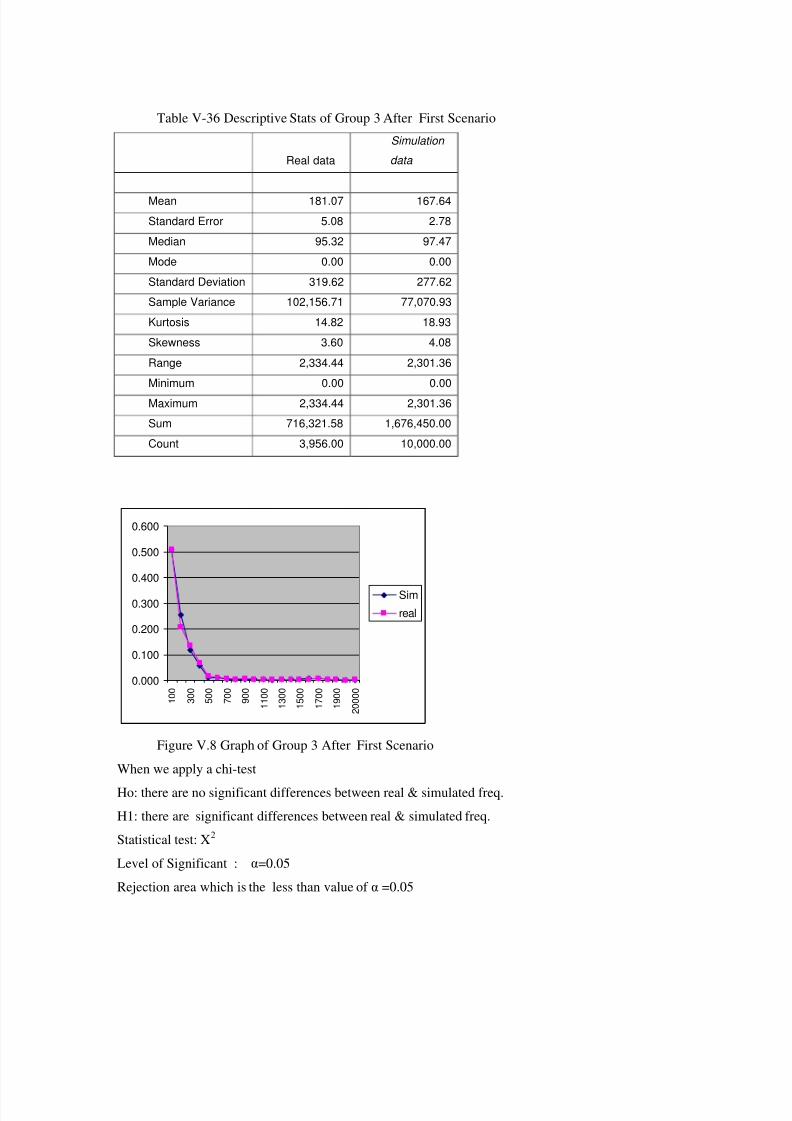

Figure V.8 Graph of Group 3 After First Scenario .............................................................122

Figure V.9 Graph of Group 3 After Second Scenario..........................................................126

Figure V.10 Physician Visit Comparison ............................................................................130

Figure V.11 Prescribed Drug Comparison ..........................................................................132

Figure V.12 Diagnostic procedure comparison ...................................................................134

Figure V.13 Minor treatment comparison ...........................................................................136

Figure V.14 Hospital benefit comparison............................................................................138

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 16/182

LIST OF TABLES

Table II-1 Types of VHI in the EU .........................................................................................5

Table II-2 VHI coverage in the EU in 1998 ................................ ............................................5

Table II-3 VHI expenditure as a percentage of total expenditure on health in the EU, 1980-

1998 ...............................................................................................................................6Table III-1 Out Patient Benefits............................................................................................27

Table III-2 In patient Benefits...............................................................................................28

Table III-3 Descriptive Stats for 2 year sample data in total expenditures .............................30

Table III-4 Regression for 2 year total expenditures..............................................................30

Table III-5 ANOVA for Regression for 2 year total expenditures ................. ........................31

Table III-6 Coefficients of Regression for 2 year total expenditures......................................31

Table III-7 Line Fit Plot For 2 Year Expenditures.................................................................31

Table III-8 Descriptive Stats for 2 year total number of utilizations ......................................32Table III-9 Regression Statistics for 2 year total number of utilizations ................................32

Table III-10 ANOVA for Regression Statistics for 2 year total number of utilizations ..........32

Table III-11 Coefficients for Regression Statistics for 2 year total number of utilizations .....32

Table III-12 Line Fit Plot For 2 Year Utilizations .................................................................33

Table III-13 Descriptive stats of the groups formed of males born between 1960 -1970........34

Table III-14 Different Group Size Characteristics.................................................................35

Table III-15 Single Factor ANOVA......................................................................................35

Table III-16 ANOVA table for different group sizes.............................................................36

Table III-17 Correlation of Average Physician Visits vs Group Size.....................................37

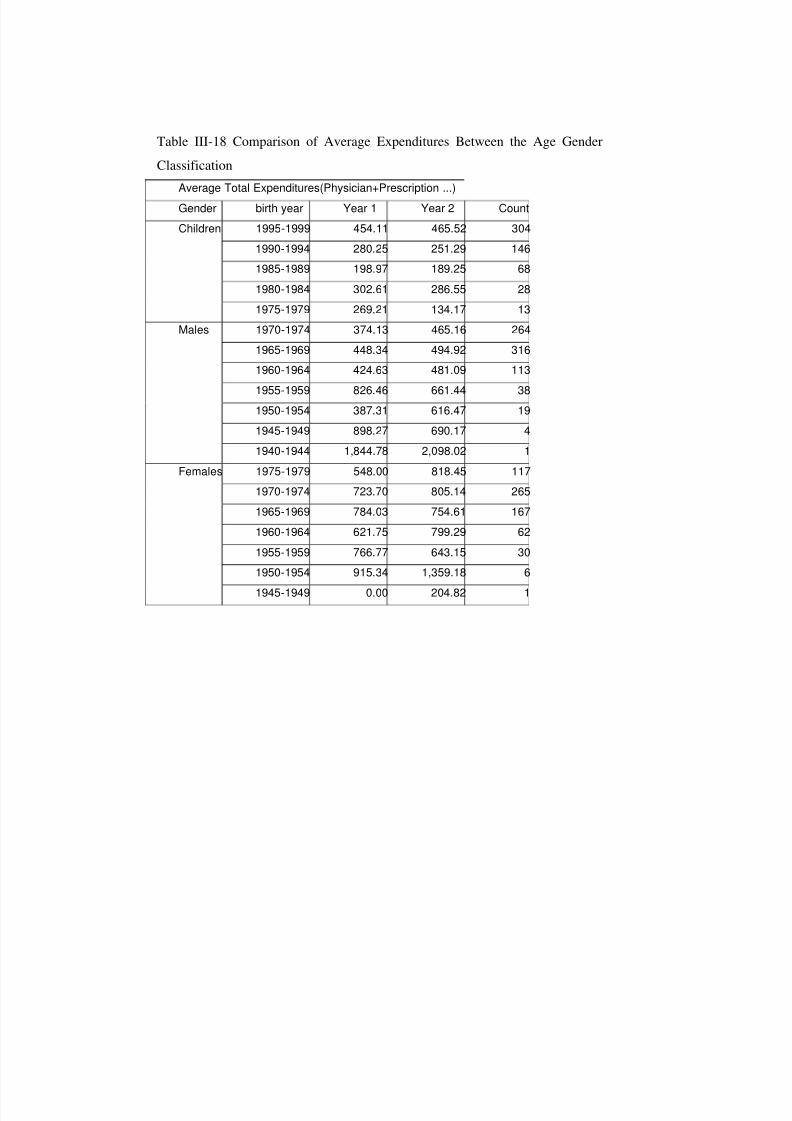

Table III-18 Comparison of Average Expenditures Between the Age Gender Classification.41

Table III-19 Correlation between the Average Figures..........................................................42

Table III-20Moments of Physician(Dr) Visits.......................................................................44

Table III-21 Moments of Prescribed Drugs...........................................................................45

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 17/182

Table III-22 Moments of Diagnostics ...................................................................................46

Table III-23 Moments of Minor Treatment ................................. ..........................................47

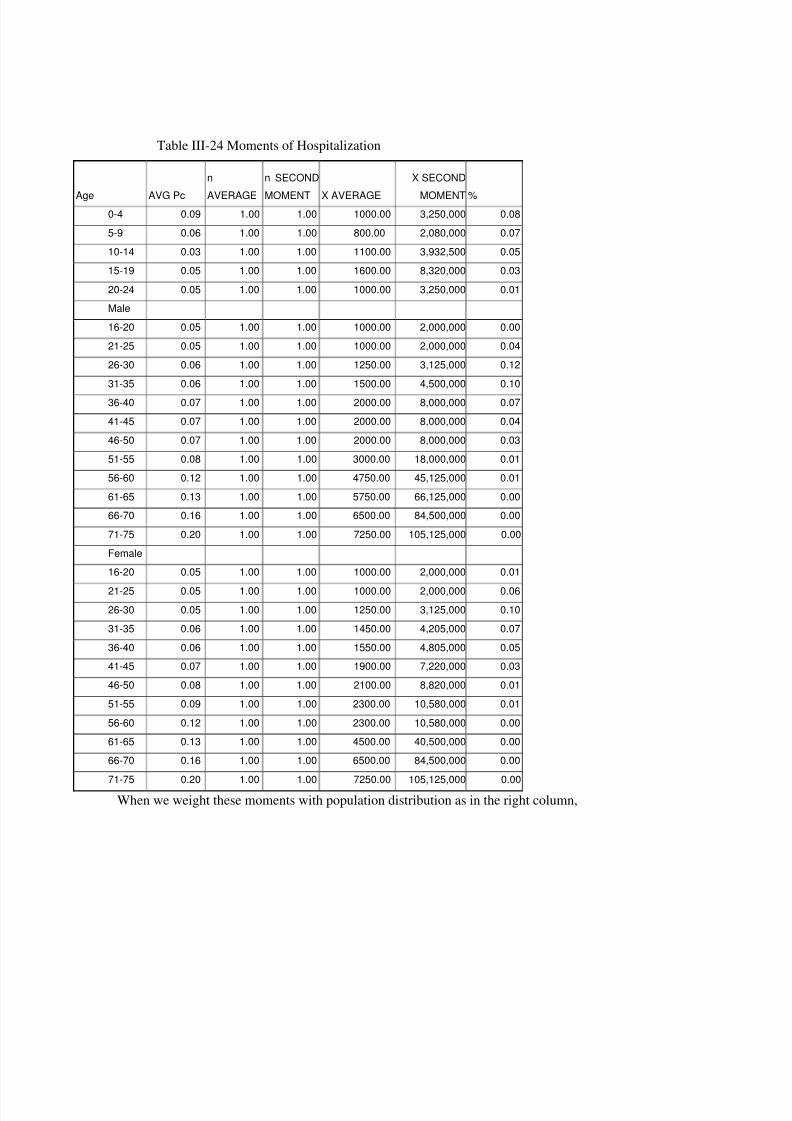

Table III-24 Moments of Hospitalization..............................................................................48

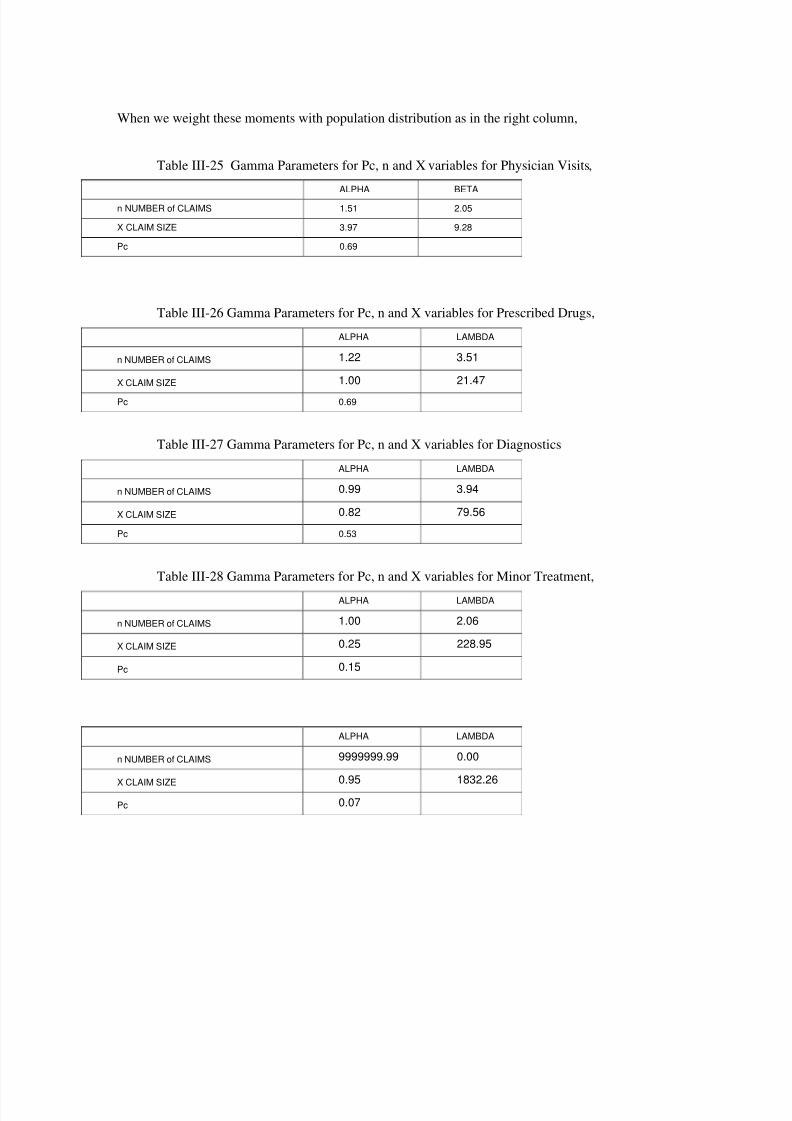

Table III-25 Gamma Parameters for Pc, n and X variables for Physician Visits,...................49

Table III-26 Gamma Parameters for Pc, n and X variables for Prescribed Drugs,..................49

Table III-27 Gamma Parameters for Pc, n and X variables for Diagnostics...........................49

Table III-28 Gamma Parameters for Pc, n and X variables for Minor Treatment,..................49

Table III-29 Annual Number Physician Contacts..................................................................50

Table III-30 Annual Number Hospitalizations .............................................. ........................51

Table III-31 Physician contacts with different level of income..............................................51

Table IV-1 Spearman Rank Correlations For Ratio of User Input Data(Pc)...........................67

Table IV-2 Spearman Rank Correlations For Number of Usage Input Data(n) ......................68

Table IV-3 Descriptive Statistics of Monthly Figures ...........................................................71

Table IV-4 Mann-Whitney U test (two-tailed test) for Monthly Incurred Costs.....................72

Table IV-5 Kolmogorov-Smirnov(two-tailed test) test for Monthly Incurred Costs...............72

Table IV-6 Mann-Whitney's U (two-tailed test) test for Monthly Number of Utilizations .....72

Table IV-7 Empirical Distribution for Number of Utilizations for Out Patient Benefits ........73

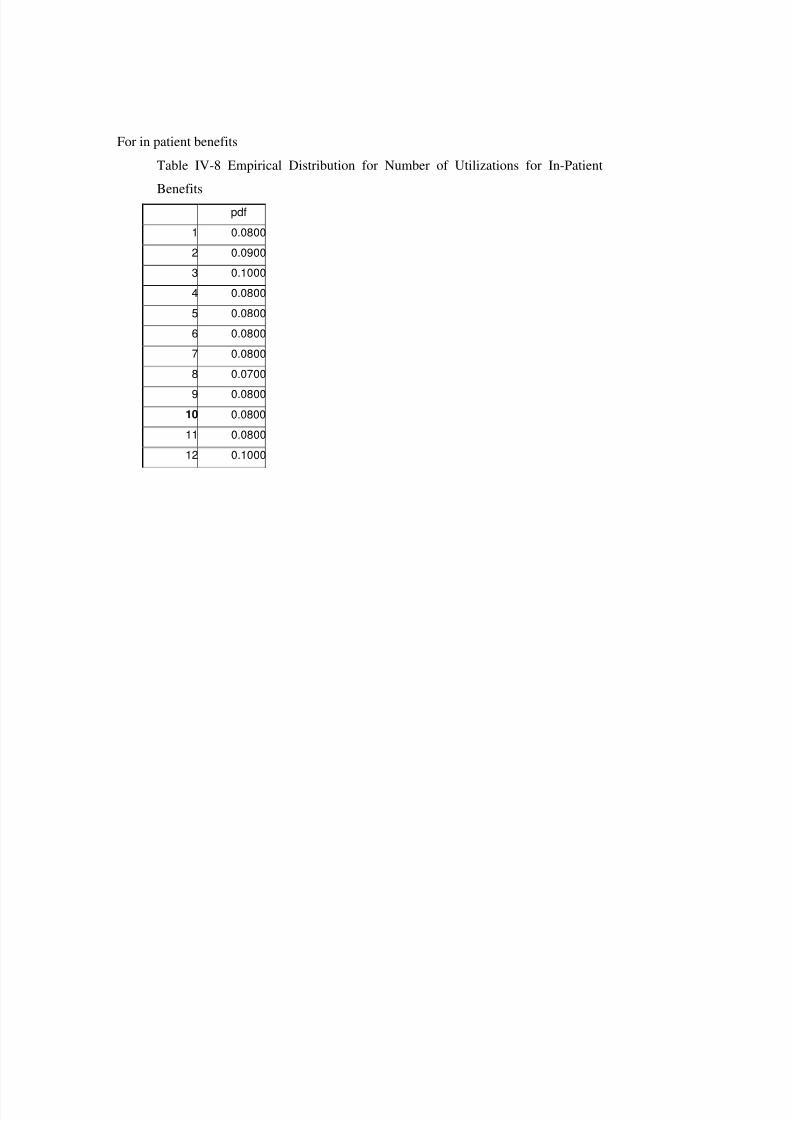

Table IV-8 Empirical Distribution for Number of Utilizations for In-Patient Benefits...........74

Table IV-9 Credibility ratings for groups with at least 3 year’s claims history ......................76

Table IV-10 Summary Statistic of the Total Costs Incurred(Independent of the limits) .........84

Table IV-11 Distribution of the Total Costs Incurred(Independent of the limits)...................85Table IV-12 Distribution of the Limit and Deductible Applied Costs With Scenario 2..........86

Table IV-13 Summary Statistics of the Limit and Deductible Applied Costs With Scenario 2

.....................................................................................................................................86

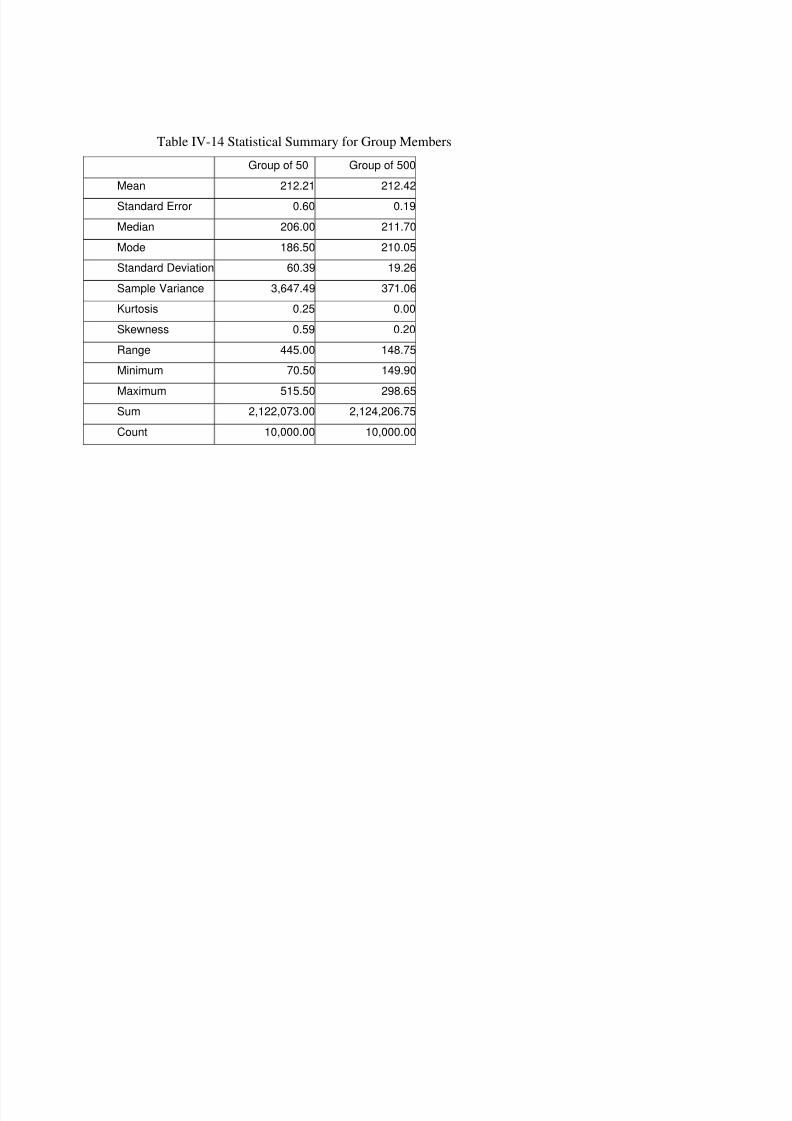

Table IV-14 Statistical Summary for Group Members..........................................................88

Table IV-15 Distribution Output for Group Members...........................................................89

Table IV-1612 Std B coefficients for Total Costs Incurred....................................................92

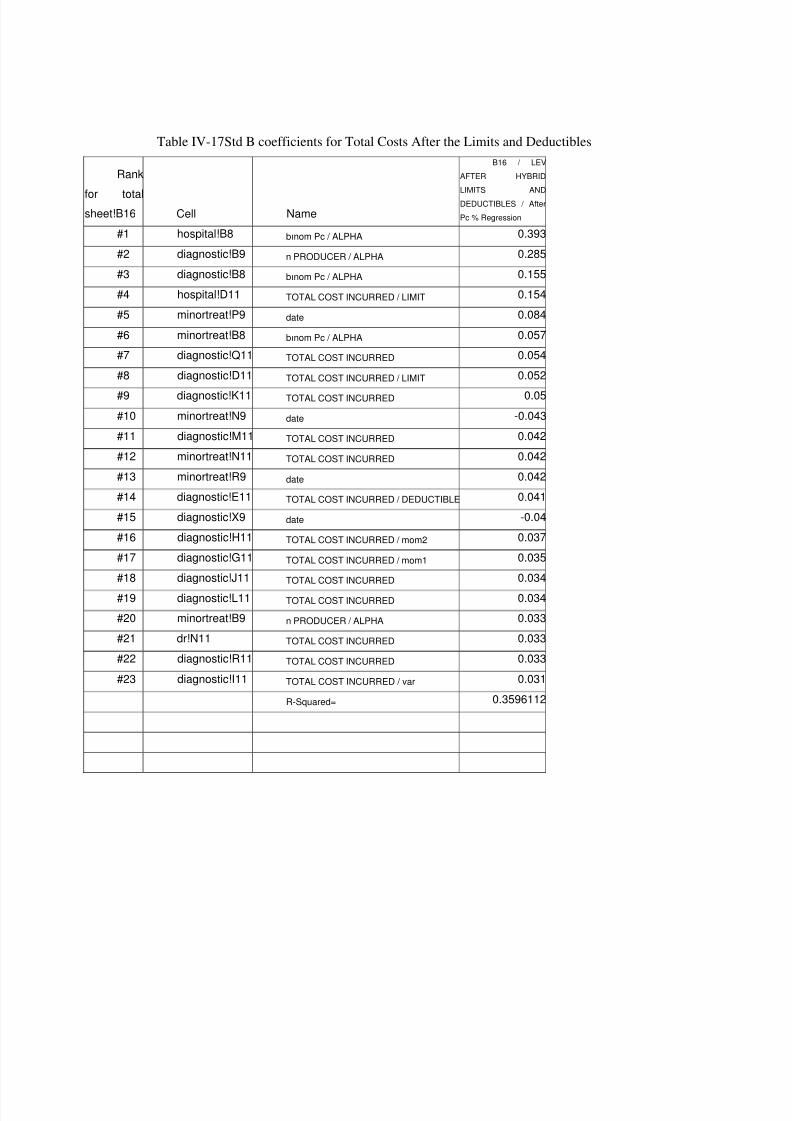

Table IV-17Std B coefficients for Total Costs After the Limits and Deductibles...................94

Table V-1 Age an Gender characteristics of the Sample Data ...............................................96Table V-2 Dr scenarios.........................................................................................................97

Table V-3 Prescription Scenarios..........................................................................................98

Table V-4 Diagnostic Scenarios............................................................................................98

Table V-5 Minor Treatment Scenarios..................................................................................98

Table V-6 Hospital Scenarios ...............................................................................................98

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 18/182

Table V-7 Distribution of Group 1 Total Costs ...................................................................100

Table V-8 Descriptive Stats of Group 1 Total Costs............................................................101

Table V-9 Mann-Whitney test for Gr1 Total Costs ............................................................102

Table V-10 Kolmogorov-Smirnov test for Gr1 Total Costs.................................................102

Table V-11 Distribution of Group 1 After First Scenario ...................................................103

Table V-12 Descriptive Stats of Group 1 After First Scenario...................... ......................104

Table V-13 Mann-Whitney test for Gr. 1 Scen.1.................................................................105

Table V-14 Kolmogorov-Smirnov test for Gr.1 and Scen. 1................................................105

Table V-15 Descriptive Stats of Group 1 After Second Scenario ................. ......................106

Table V-16 Distribution of Group 1 After Second Scenario ...............................................107

Table V-17 Mann-Whitney test for Gr. 1 Scen.2.................................................................108

Table V-18 Kolmogorov-Smirnov test for Gr.3 and Scen. 2................................................109

Table V-19 Distribution of Group 2 Total Costs .................................................................109

Table V-20 Descriptive Stats of Group 2 Total Costs..........................................................110

Table V-21 Mann-Whitney test for Gr2 Total Costs ..........................................................111

Table V-22 Kolmogorov-Smirnov test for Gr2 Total Costs.................................................111

Table V-23 Distribution of Group 2 After First Scenario ...................................................112

Table V-24 Descriptive Stats of Group 2 After First Scenario...................... ......................113

Table V-25 Mann-Whitney test for Gr. 2 Scen.1.................................................................114

Table V-26 Kolmogorov-Smirnov test for Gr.2 and Scen. 1................................................114

Table V-27 Descriptive Stats of Group 2 After Second Scenario ................. ......................115Table V-28 Distribution of Group 1 After Second Scenario ...............................................116

Table V-29 Mann-Whitney test for Gr. 1 Scen.2.................................................................117

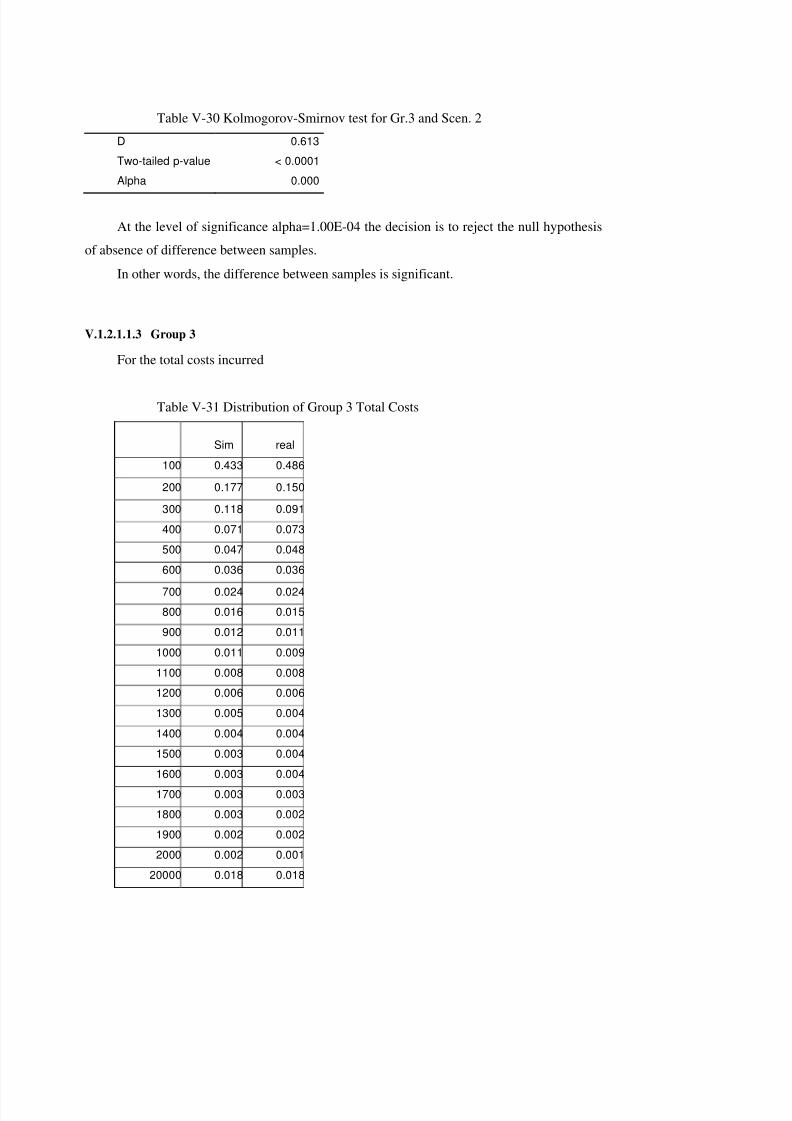

Table V-30 Kolmogorov-Smirnov test for Gr.3 and Scen. 2................................................118

Table V-31 Distribution of Group 3 Total Costs .................................................................118

Table V-32 Descriptive Stats of Group 3 Total Costs..........................................................119

Table V-33 Mann-Whitney test for Gr3 Total Costs ..........................................................120

Table V-34 Kolmogorov-Smirnov test for Gr3 Total Costs.................................................120

Table V-35 Distribution of Group 3 After First Scenario ...................................................121Table V-36 Descriptive Stats of Group 3 After First Scenario...................... ......................122

Table V-37 Mann-Whitney test for Gr. 3 Scen.1.................................................................123

Table V-38 Kolmogorov-Smirnov test for Gr.3 and Scen. 1................................................123

Table V-39 Descriptive Stats of Group 3 After Second Scenario ................. ......................124

Table V-40 Distribution of Group 3 After Second Scenario ...............................................125

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 19/182

Table V-41 Mann-Whitney test for Gr. 3 Scen.2.................................................................126

Table V-42 Kolmogorov-Smirnov test for Gr.3 and Scen. 2................................................127

Table V-43 F testf or Physician Simulation and real data comparison.................................128

Table V-44 t testf or Physician Simulation and real data comparison ..................................129

Table V-45 F testf or Prescribed Drugs Simulation and real data comparison .....................130

Table V-46 t testf or Prescribed Drugs Simulation and real data comparison ......................131

Table V-47 F testf or Diagnostic Simulation and real data comparison ...............................132

Table V-48 t testf or Diagnostic Simulation and real data comparison ................................133

Table V-49 F testf or Minor Treatment Simulation and real data comparison......................134

Table V-50 t test f or Diagnostic Simulation and real data comparison ...............................135

Table V-51 F testf or Hospital Simulation and real data comparison...................................136

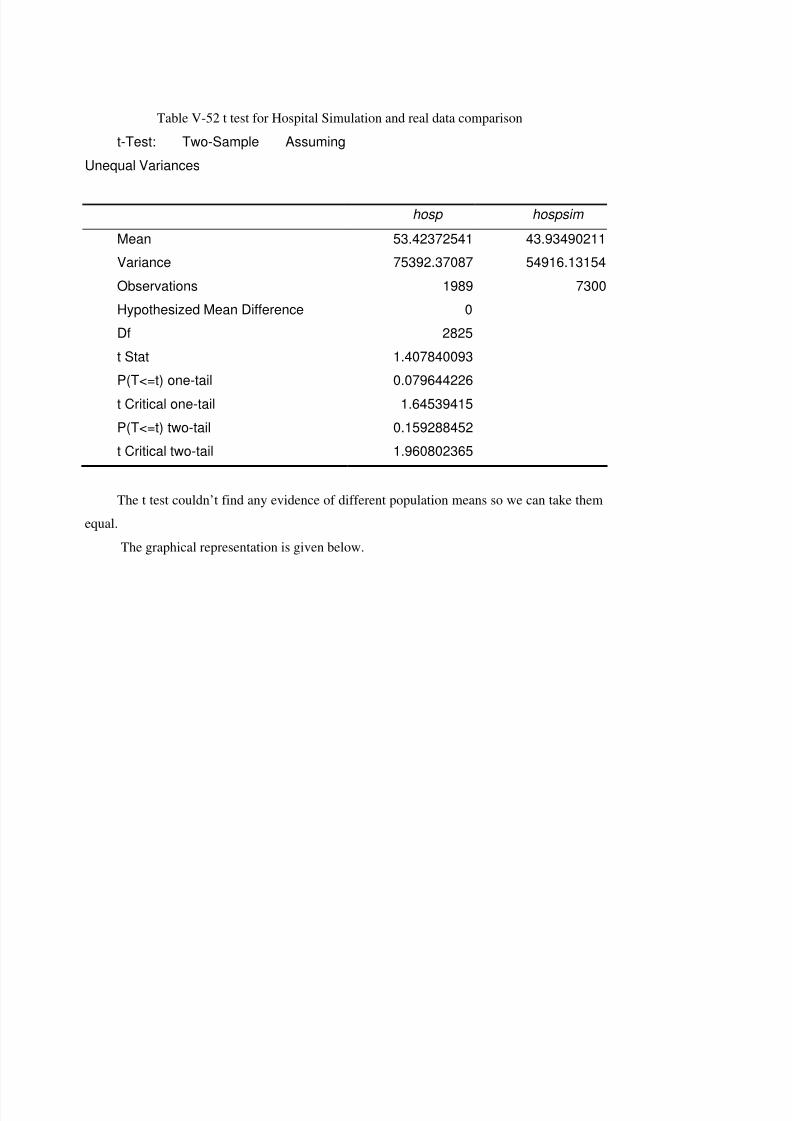

Table V-52 t testf or Hospital Simulation and real data comparison....................................137

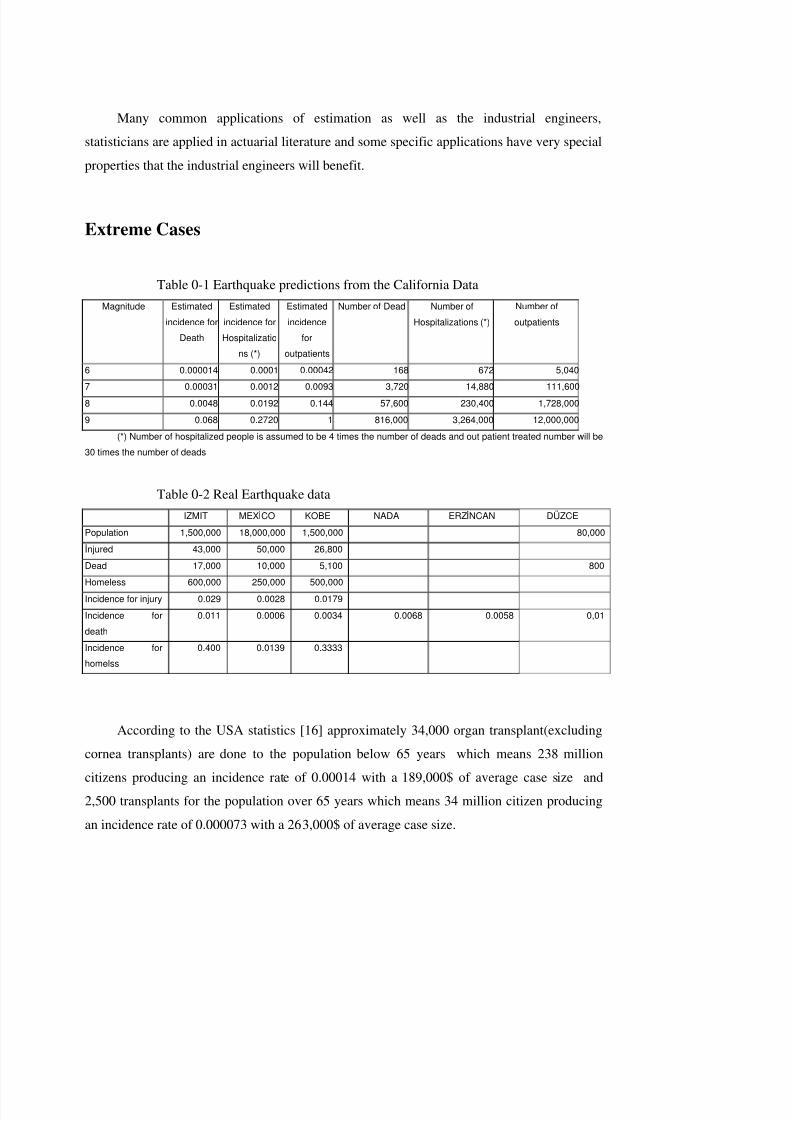

Table 0-1 Earthquake predictions from the California Data.................................................148

Table 0-2 Real Earthquake data ................................ ..........................................................148

Table 0-3 High costs incidence rates...................................................................................149

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 20/182

PART.I.

INTRODUCTION AND OBJECTIVES

Turkey is the third most populous country in World Health Organization’s European

Region, and its economy is among the ten largest in Europe. It has a high growth rate and ayoung population. Turkey is also a candidate for membership of the European Union.

However, the population’s health status and the quality of the health care system are far below

the country’s general level of development.

The last few years have seen a rapid expansion of the private health care sector in

Turkey. The expectations of those with high incomes (last decade has created a high-income

group of between six and eight million people) provide incentives for further expansion and

encourage the private sector to play a larger role in the health care system. Furthermore

patients prefer private to public health care, regardless of their income, due to a lack of

confidence in public health services and a belief that private health care is of better quality

It is difficult to make reliable estimates of the extent of out-of-pocket payments in

Turkey, as private spending on health care is not well documented. Official sources like the

World Health Organization’s European health for all database records, The Organization for

Economic Co-operation and Development (OECD), and reports of the Ministry of Health puts

the percentage of out of pocket expenses to be 28% of all health care expenditures which is 10

billion USD in official figures. This constitutes a total expenditure of 3 billion USD with out

of the record expenses. Taking into account differences in the relative purchasing power of

various currencies, Turkey’s GDP per capita (Intl $) is 6,455 where the total health

expenditure per capita (Intl $) is 323. ( in normal USD currency it is approximately GDP is

2000$ and expenditure is 110$) When we compare health care expenditures with other

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 21/182

comparable countries like Hungary (846$, 24.3 % of this is private expenditure), Greece

(1,390$, 44.5 % of this is private expenditure) we can say that private health care

expenditures are very low and will increase in the following years due to the technological

progress, the new expectations of consumers, population aging and the reluctance of

governments to devote an ever-growing proportion of State budget.

Private health insurance always plays a complementary role, which varies in

significance, in the majority of the countries all over the world. In some countries private

insurance even has partially taken the place of public services. Private insurance plays its role

at two different levels: the financing level, where the insurer reimburses the cost of care or

provides compensation, and the care providing level such as in the case of managed care. So

private health insurance covers a very extensive range of services, and also brings into play

many different operators. Its characteristics, and in particular the extent of its integration in

the various parts of the public systems, differ considerably from one country to another.

Considering the Private Health Care Expenditures covered by private health insurance

in Turkey, (257 Trillion TL which is 170 million USD) and covered population to be 700,000

which is 1% of population) if the system grows like in the western countries then the insured

population will grow to 10 million and will be covering privately insured expenses totaling

more than 2 Billion USD comparatively .

In private health insurance, contracts are done as a group or individually. In group

contracts employers or unions are contracting with the private health insurance company. But

for individual contracts, people are paying for their families. Because of the higher risk of

adverse selection for the insurance company, the conditions are much more stricter and

premium is higher for individual contract than group contracts.

To avoid major inequalities or excessive rise in premiums, group insurance contracts

have been favored by the regulation in the countries where private medical insurance is welldeveloped. And as a result of this group contracts are widespread in a number of countries. (In

US %70 of the population is covered under group business)

Only in a few countries health insurance statistics are published in sufficient volume to

be credible and meaningful. It is very hard to find the technical literature on private health

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 22/182

insurance. For example in UK where 11.5% of the population is under private health

insurance, there are no official published statistics as classified in this thesis. Though the

majority of the published actuarial literature is UK origin, first article on health insurance was

written in 1988 and few additional articles were published after that. Due to the lack of

information new articles written in UK still refer to the overseas articles like the ones that are

published in US or Australia.

The objective of this study is to prepare a dynamic forecasting model in private group

health insurance business and health funds. Real data have been used to describe the model

with a large number of variables so that reliable forecasts can be made. Structure of such a

model that aims to reflect a real life situation made up of various distributions with different

characteristics is very complex.

While developing this model, it is aimed to;

· Outline the approaches and adopt some general actuarial concepts to private health

insurance. (Since this is the first example of a health care expenses prediction simulation

model in group health insurances in Turkey.)

· Determine the structure of the model made up of various modules, taking into account

the age and gender differences on utilizations and unit costs, experience of the examined

group previous year statistics, uncertainty due to various factors such as trend, credibility and

suitability of the data.· Test the model due to interrelations and sensitivity of variables.

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 23/182

PART.II.

GENERAL BACKGROUND

II.1 PRIVATE HEALTH INSURANCE IN THE WORLD

In industrial States, health care financing has historically been inspired by three

competing “models”: the first one, implemented by Bismarck in Germany, relied on

professional enrolment through compulsory contributions from employers and employees;

more recently, Beveridge introduced in the after war UK a public health monopoly, ensuring

universal social protection. The last form of organization is a mix-system, which prevails in

the US, where health insurance is not compulsory [23].

The extend and pace of the development of private health insurance in each country has

been very dependant on the original pattern of the national health care organization, even if

most countries tend to have now a rather hybrid health care system (mixing elements from the

three original models). Amongst OECD member countries, strong contrasts can now be

observed in the balance between private and public health insurance. Although, private sector

is mainly supplementary to public coverage, in some countries it can substitute to public

sector to cover even primary care for all or part of the population. Lastly private health

insurance may provide the same level of coverage than the existing public scheme, whilegiving access to private providers.

According to these regulations, if we would like to explain the systems in EU [23],

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 24/182

Table II-1 Types of VHI in the EU

Supplementary

increases choice / access

Faster access

increased choice of provider

own room in hospital

Complementary

services excluded / not fully covered

by the state

Dental care

‘alternative’ treatment

co-payments

Substitutive

the principle means of protection

Spain

Germany

Netherlands

Table II-2 VHI coverage in the EU in 1998

Country % populationsubstitutive

% populationcomplementary / supplementary

Austria (hospital expenses) 13

(hospital cash payments) 21

Belgium 30

Denmark 28

Finland (children) 33 / (adults) 10

France (co-payments) 85

(other types of VHI) 20

Germany 8.9

Greece 10

Ireland 42

Italy 5

Lux (active population) 75

Neth 31

Portugal 10

Spain 6.8 10.8

Sweden 0.5

UK 11.5

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 25/182

Table II-3 VHI expenditure as a percentage of total expenditure on health in the

EU, 1980-1998

Country 1980 1985 1990 1995 1998Austria 7.6 9.8 9.0 7.8 7.1

Belgium 0.8 1.2 1.6 1.9 *2.0

Denmark 0.8 0.8 1.3 1.2 1.5

Finland 1.4 1.8 2.2 2.4 2.7

France - 5.8 11.2 11.7 12.2

Germany 5.9 6.5 7.2 6.7 **6.9

Greece - - 0.9 - -

Ireland - - - - 9.4

Italy 0.2 0.5 0.9 1.3 **1.3

Luxembourg - 1.6 1.4 1.4 **1.6

Netherlands - 11.2 12.1 - 17.7

Portugal - 0.2 0.8 1.4 **1.7

Spain 3.2 3.7 3.7 5.2 **1.5

Sweden - - - - -

UK 1.3 2.5 3.3 3.2 3.5

Health care expenditures can be financed according to three basic models: risk-based

calculation of premium, community rating and funding.

Risk based calculation is the most common way for private insurers to provide health

products. Two different types of policies may be distinguished: individual and group

insurance. These models involve different kind of selectivity and premium calculations.

Individual policies are scarce in OECD countries (except in Italy and in Denmark). For

such policies, individual contract premiums are calculated on risk-based criteria such as age

or age at entry, sometimes gender (Luxembourg, Portugal, Switzerland) and often health

status. Therefore premiums are higher for older and weaker persons. Moreover, private

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 26/182

insurers are allowed in most case to deny the access to high-risked individuals or to impose

waiting period (such as in the US, Luxembourg or Switzerland). This is the case in nearly all

OECD countries except when policies are aimed at protecting specific categories of persons.

Group insurance policies are more common. They are widespread in a number of

countries such as:

The US, with more than 70% of the population covered by this type of scheme,

France, where two thirds of insured are covered by a global contracts through the

employer,

Germany,

The UK, where three quarters of the population have a supplementary health insurance

cover,

Canada,

And recently Portugal, in which 90% of contracts are group insurance policies.

Reasons for this development certainly lie on the particular financial and access

facilities of these policies. Actually, since risks are borne by more people, insured enjoy lower

premiums based on an experience-rated calculation. Insurers may therefore have fewer

incentives to have recourse to risk selection.

II.2 TURKEY PRIVATE HEALTH INSURANCE BACKGROUND

In essence, private health insurance started to develop circa 1990 by offering per event

limited out-patient based policies with a limited surgery, room and board benefits(Health

Insurance is defined to be a separate branch by 1990).

As many multinational companies started investing in Turkey and as a policy they

require Group Health Covers for their employees, private insurance companies have begun to

take part in the health market.

As a result of the lack of confidence to the social security system, the private insurance

companies have developed policies for individuals in addition to policies providing group

health coverage which are being spread out by the help of direct sales teams, and most

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 27/182

policyholders, although being at the same time contributors to the social security system,

more and more they stopped using the services provided by the social security institutions.

Between 1990 and 1993, as a consequence of the insufficient understanding of

principles of health insurance, health insurance policies were mostly out-patient oriented and

were insufficient for in-patient benefits. In 1994, the benefit structure of these policies was

changed to ones in which more comprehensive in-patient benefits were provided.

Between 1993 & 1995, a serious increase in the private health organizations was

observed. With these modern hospitals, there came a professional approach to private health

insurance. For example, Bayındır Hospital which was owned by a group who has also a life

insurance company, produced a Preferred Provider Organization (PPO) product to sell to the

upper and middle class markets in Ankara. This hospital has established contacts with the

health insurers of Istanbul in 1994.

PPO agreements were done with some of the well known hospitals in Istanbul and in

Ankara by Halk Yaşam and Koç-Allianz Hayat which were the first companies to initiate

PPO concept to the market through the end of 1994.

The leading companies in the market aim to expand this system gradually to the whole

country and thus create a private health service system. These products offer unlimitedbenefits with some exclusions and cost containment measures. Even though the policy is

unlimited, when the insured wants to get service from another provider (non-PPO) then, a

maximum limit, deductibles or coinsurance are applied. But for the emergency cases, when

someone could not reach a PPO, this condition is usually not enforced.

Due to the development in the private health insurance industry, Munich-Re, the most

known foreign reinsurance company in Turkish insurance market established Med-Net system

with foreign partners (a Third Party Administration) in 1994, which was a new concept for theinsurance sector. Small companies prefer this system because policy related services such as

underwriting, policy issuing, premium collections and claim settlements are done by Med-

Net. Med-Net offers a wide range of plans which are equipped with different geographical

scopes, limits, co-insurance and deductibles.

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 28/182

In 1994, affordable check-up benefits started to be offered by policies.

In 1993 and 1994, insurance companies began to provide air ambulance services which

are not unfortunately being able to be used efficiently. Air ambulances are employed

according to the distribution of the insureds within big cities. The air ambulance system is

supported by wide spread road ambulance system as well.

Since 1995, many different kinds of products have been introduced to the market, some

of which offer benefit limited products both per prescription, per visit limit and annual limit

per benefit whereas new models with annual maximum limits per person are being developed

as package options. In order to increase market penetration, more attractive policy options are

being developed in the market for the middle class people. As far as product designs are

concerned, the market has been moving from a fee for service model to annual limits and even

to unlimited benefit models. Halk Yaşam and Koç-Allianz Hayat have started a family

physician service including also free laboratory tests and keeping health condition records of

the insureds.

In late 1994 and 1995, guaranteed renewability rights were added to some of the

products of the leading companies in the market and Med-Net.

In 1997, companies which were not satisfied with the service quality and continuousincrease in prices started to quit from the market. Another Third Party Administration

Company named Med-Ex entered the market.

In 2001 Private pension law put the condition for life insurance companies who would

like to serve pension business, segregation of the health business is obliged.

As of 2002, there are approximately 700,000 policyholders in the health branch who are

either individually insured or members of group plans.

As a result of a number of factors including the following, there is an expectation of a

significant growth in health insurance business in Turkey in the coming years:

1. The poor quality of health services offered by the social security system.

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 29/182

2. The introduction of innovative health products which has already built public

confidence.

3. Increase in income levels.

4. Increased awareness.

5. Regulatory changes requiring separate life insurance companies, which

increased management's focus on health and life insurance.

6. Major developments in the financial sector in Turkey, including debt and

equity capital markets which have enabled diverse investment opportunities for individuals

and institutions for life savings (as opposed to bank deposits and real estate being the only

available investment tools pre-1980). Individuals are now more aware of the value added

provided by institutional fund management by investment professionals.

7. Private sector companies becoming more institutionalized as they transform

from family owned businesses into institutionally held corporations and offer better benefits

to their employees. The increased number of multinational companies establishing a presence

or expanding their existing operations in Turkey is resulting in better added benefits to

employees in the form of group health and life programs.

There is also a series of talks and preparations for a health reform, which include

special proposals to maintain the development in the health sector and health insurance

services. This can be outlined as following:

· to unify the 3 major Social Security Institutions ( SSK, BAG-KUR, Emekli Sandigi )

under a Social Security Finance Institution and to separate the concepts of health care

provision and financing;

· to include the non-insured ( almost 35% of the population ) in the new system;

· to expand the service of the Social Security System with the application of a "Green

Card" which provides free health services for people whose monthly income is equal to less

than 1/3 of the minimum wage;

· to separate the financial control of health and pension funds;· to use a modern accounting system throughout the health sector and to use efficient

financial & actuarial methods;

· to provide a modern information system;

· to encourage the establishment of private hospitals with efficient management and

financial systems in order to increase market competition and to decrease the prices;

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 30/182

· to enlarge the extent of support investments in the health sector;

Private health insurance companies are also allowed to participate in the

implementation of this program.

It is observed that 4/5 of the private insureds belongs to the upper income class and the

upper middle class. The rest are mainly members of group health insurance plans which are

offered as a fringe benefit by the employers in the private sector. The development of the

market with increasing number of insureds will reduce the risk of anti-selection which shall

lead to more affordable premiums for middle class people [29].

Private health insurance companies in Turkey compete with each other by their quality

of service, policy premiums and product differentiation. Preventive medicine, family

physician system and family planning are going to be popular benefits in order to make

policies more desirable. It is observed that the market tends to be more in oligopolistic

structure during the recent years because of the vast entrance into the market.

II.3 HEALTH RISK MODELS IN LITERATURE

Health care expenditures are characterized both by large random variation as well as

large predictable variation across individuals. Such differences create the potential for large

efficiency gains due to planning, risk reduction from social or private insurance, and raise

important concerns about fairness across individuals with different expected needs for

services. Although each population not only has unique demographic and socioeconomic

characteristics but also a distinct medical signature [35], it is indispensable to use experiences,

data and techniques of the other models.

Considerable research has been conducted on alternative forecasting models in many

countries, using a wide range of information.

Risk adjustment means the use of information to calculate the expected health

expenditures of individual consumers over a fixed interval of time (e.g., a month, quarter, or

year)

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 31/182

In the United States, actuaries have been slow to accept health-based risk adjustment,

despite its greater accuracy.

According to the demographics only, prior year expenditures, diagnoses, information

derived from prescription drugs, self-reported health and functional health status measures,

mortality, and approaches from the other discipline exist.

While examining these methods it should be noted that it very hard to estimate the

health care spending on individual basis. When the numbers reaches to sufficient size (in risk

adjustment literature it is considered to be more than 5000 members but this number is

defined by the characteristics of the health care system and population) than it becomes

possible to estimate the overall costs of the sample size.

II.3.1 Demographic Models

First data that is used in health estimations are age and sex. When we examine the

worldwide statistics and the Turkish data it is clearly seen that age and sex factors are the

primary factors concerning the health utilization and spending.

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 32/182

Figure II.1 Health Spending for Gender, Age Sample Netherlands

Figure II.2 Health Spending for Gender, Age Sample USA Privately Insureds

Figure II.3 Health Spending for Gender, Age Sample USA Medicaid Eligibles

Age and sex are easy to document and use for risk adjustment, are fair, and generally

accepted by all parties involved. Because the information is independent of medical care, and

not readily gamed, it appears attractive in terms of incentives. Most serious drawback of age

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 33/182

and sex as risk adjusters are simply that they are weak predictors of individual expenditures

[31].

II.3.2 Prior Year Expenditures

Because expenditures in one year are correlated with expenditure the following year -

the correlation coefficient for total health expenditures is on the order of .2 to .3 - a simple

proposal has often been made to regress expenditures in year two on year one expenditures

(together with other demographic variables) and use this model for calculating risk-adjusted

payments. Newhouse et. al. [24], Van de Ven and Van Vliet [32] and Ash et al. [5] have all

estimated such models and typically find that spending an extra dollar on health care in year

one "predicts" spending of $0.20 to $0.30 in year two. The R2 from a regression that includes

age, sex and prior year expenditures, is generally estimated to be in the range of .06 to .10. on

individual basis These measures are a substantial improvement over demographic only

models, and comparable to the predictive power achieved by diagnosis-based models or

models that use self-reported health status measures.

In the study that was done by Ash et al. [5]], by examining MED-STAT Market Scan

Research Database, the largest multi source private sector health care database in the United

States, 2.7 million individuals were selected and year 1997 and 1998 results were examined.Below figures were gathered,

Figure II.4 Distribution of population costs to the members for year one and two

This is the distributions of Year- One and Year- Two Cost by Year- one Cost Group,

which means in year one top (in term of health care costs occurred) 0,5% of the population

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 34/182

had spent %23 of the total population and next year in 1998 this group spent the 8% of the

total health care cost of all. And contrary to this bottom %80 of population had spent %13 of

total costs and next year they spent the %49 of costs. As can be seen top spenders tendency to

pay 2-3 times the average can be recognized easily where the bottom cost %80 has more

volatile nature. This shows us the large random component for the individual figures.

Van de Ven describes that the prior year expenditures or utilization appears to be the

best single predictor(where there is only one predictor in hand) of an individual’s future

health expenditures [31]. But Ash et al.(1998) mentions that prior cost, which was historically

superior to diagnostic information for the purpose of predicting future costs, is no longer

better than the current generation of diagnosis- based risk models for predicting future costs.

In her above-mentioned study diagnostic based methods were slightly superior at identifying

the top group with high costs [5].

II.3.3 Diagnosis-Based Risk Adjustment

Since the early 1980's a considerable amount of research has developed risk adjustment

models that use diagnoses from insurance claims to calculate risk-adjusted payments. In 1997,

the US Congress directed CMS to change the way it paid HMOs that contracted with the

federal government to provide Medicare covered services. [27]

The best-known methods are;

• Ambulatory Care Group (ACG)

• Diagnostic Cost Group (DCG)

• Disability Payment System (DPS)

The starting point for all diagnosis based risk adjustment models is the concept that

certain diagnoses predict of health care expenditures. Each of the three major diagnosis basedmodels begins by identifying a subset of all diagnoses that predict current or subsequent year

resource use. Although the three models differ in how they choose their subset of diagnoses,

each attempts to identify codes that are assigned only for encounters involving a

professionally trained clinician. In particular, diagnoses appearing on laboratory, diagnostic

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 35/182

testing, and medical supplies claims are uniformly not used in classifying individuals for

prediction, on the grounds that they are less reliable than those assigned by clinicians.

ACGs are based on aggregation of all ICD9-CM codes into 32 diagnostic groups using

ambulatory diagnoses only. These diagnostic groups can then be used in a number of

alternative combinations, providing up to 83 mutually exclusive ACGs into which any given

individual may be classified.

DCGs have received the most attention of all classification systems. Early versions of

this system were based on simple hierarchical models of diagnosis grouping, where modeling

was used to identify a large number of clinically homogenous groups, which were then

aggregated into between 9 and 20 Diagnosis Cost Groups. The DPS was developed for US

Medicaid disabled enrollees, and is based on similar principles to the DCG/HCC model. All

diagnoses from clinical encounters are used within a hierarchical system for conditions.

However, the DPS is more additive than the DCG/HCC system in its methods to account for

the number of conditions an individual has within certain body systems. The general disability

of the DPS is unclear, however, as its development and application has focused on people

with disabilities.

Also in USA, where medical infrastructure is said to be the technologically foremost

developed one in the world, the systems that combine diagnoses from patient - clinicianencounters across the spectrum of health care delivery sites with age and sex are now being

used by health care organizations to measure the health risk of populations. However, many

organizations have not implement ed “all encounter” diagnosis models because they require

timely, comprehensive, high- quality data from physician’s offices and other dispersed sites of

care.

In USA many author In patient models (diagnosis based) predict next year’s total costs

reasonably well in Medicare, where nearly 20 percent of the population is hospitalizedannually, of ten for chronic conditions. However, such models are less attractive for privately

insured under 65 populations, where fewer than 5 percent are hospitalized in a year and of ten

for acute conditions. Few previous studies have evaluated inpatient diagnosis models on

younger populations. So-called all encounter models that use both inpatient and out patient

diagnoses to predict cost have been developed for several types of populations: elderly

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 36/182

In Diagnosis based methods the data should be tracked for each member with the

following year costs and the diagnostic codes should be chosen, entered and kept correctly

which is not a very easy situation for Turkish private and social security systems.

II.3.4 Information Derived from Prescription Drugs

A second source of needs measures based on prior utilization is the use of prescription

drugs.

Early work focused on classifying drugs into different therapeutic classes and counting

drug orders in each class. This approach was extended to include clinician judgment of

severity to form weighted disease scores based on outpatient pharmacy utilization and

condition severity to develop the Chronic Disease Score (CDS)

II.3.5 Self-Reported Health Information

Health survey information can be obtained without contact with medical providers, no

prior medical or insurance history is required; reflects individual’s perceptions of their ownneeds and expected utilization, is uniform across health schemes and providers; and other

relevant data, such as socioeconomic measures etc., may also be collected. There are also

disadvantages to self-reported measures of health; surveys are costly to undertake; response

rates may be low and affect the robustness of empirical analysis, requiring large sample sizes;

responses may be correlated with medical risk; reporting may be inaccurate due to errors or

confidentiality issues. Furthermore, provider assistance in conducting surveys may be

required, which may lead to problems in follow up and non-random sampling. Van de Ven

(2000) presents information on the validity of regression models that have sought to explainvariations in health expenditure in terms of health status measures. These studies show that

adding self reported health status measures to demographic variables significantly increases

the predictive power of risk adjustment models. However, self reported health status measures

do not outperform prior diagnosis variables in explaining variations in health expenditure.

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 37/182

II.3.6 Mortality

In individual level analysis mortality has been proposed as a potential explanatory

variable in regressions on expenditure due to the excess costs incurred prior to death.

However, whether mortality is a useful predictor of variations in expenditure at the individual

level is not clear. One argument is that the costs associated with death are largely

unpredictable, and have been found to be 250% above. A more effective means of

reimbursing health schemes for the costs of death may be to control for deaths in the

regression model (through dummy variables for patients who died during the period, and

reimburse schemes retrospectively for those individuals. Van de Ven (2000) have questioned

the political and social acceptability of increasing payment rates to health schemes with

higher mortality rates. Mortality data may also be poorly coded and only partially available in

some contexts, and may raise some concerns about privacy.

II.3.7 Other Models

There is a considerable literature in statistics, econometrics, and health economics that

examines and assesses alternative functional forms for estimating models of health spending.For data source and applications we recommend [2,3,6,7,9,11,13,19,22,28 and 33]

II.4 PRIVATE HEALTH INSURANCE PRICING

II.4.1 Practice of Pricing in the World

Group business is defined as any collection of individuals who combine to make a

single proposal for uniform Insurance cover. Usually the collected individuals will beemployees in the same company and the employer will pay for the premiums either wholly or

in part. Generally the group will be a discrete definable unit of individuals and the insurer will

look for some minimum take-up rate of the terms offered, if the scheme is voluntary, in order

to limit and-selection.

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 38/182

Several kinds of product pricing mechanisms exists in health insurance market starting

from fixed price fully insured plans to experience rated plans with minimal stop loss

insurance protection. The options available to group policy holders increase together with the

increase of the employee within the company. Up to 10 employee groups are invariably

covered by fully insured contracts with no waivers on medical underwriting. Groups of more

than 1000 employees are almost invariably experience rated and all medical underwriting is

relinquished(UK, US) [12, 25,26].

The following chart illustrates the different pricing methods that are used in UK for

different sizes of policy [4]

Size of Policy Pricing methods available

Very large group scheme( > 5000 lives)

Large group scheme( > 500 lives)

Small group scheme( > 100-500 lives)

Very small group scheme

Individual Policyholder

C o s t

P l u s

E x p e r i e n c e

R a

t i n g

M i x o

f B o o

k a n

d

E x p e r i e n c e

R a

t i n g

B o o

k R a

t i n g

Figure II.5 Group and Individual Rating Structures

It should be noted that this chart is dependent on the type of cover offered. The chart is

appropriate for a cover including mainly hospital benefits. The size of scheme at which

Experience rating becomes appropriate would reduce for cover within higher frequency of

claiming (for example cover including primary and dental care) and would increase for cover

with a lower frequency of claiming (for example cover including a very large

excess/deductible).(smaller groups can be experience rated for higher frequency benefits like

8/8/2019 Bulent Eris Model Development for Planning and Forecasting in Diagnostic and Treatment Systems 9022004

http://slidepdf.com/reader/full/bulent-eris-model-development-for-planning-and-forecasting-in-diagnostic-and 39/182

for a 100 member group can be experience rated for physician visits while it is hard to give

credibility to the group data for hospital benefits )

The premium quoted by an insurer for new groups will be based on the following