bulgaria: economic performance, prospects and risks craig otter, economist intelligence unit may 11...

TRANSCRIPT

Bulgaria: Economic Performance, Prospects and Risks

Craig Otter, Economist Intelligence Unit

May 11th 2007

Outline

Economic performance 1996-2006

Economic prospects 2007-2008

Key challenges

Conclusion

Growth robust and stable

-15

-10

-5

0

5

10

15

1996 1998 2000 2002 2004 2006

Net trade

Investment

Public exp

Private exp

Actual growth

Real GDP growth, % and contributions, pp

Falling unemployment

02468

101214161820

1996 1998 2000 2002 2004 2006

Unemployed persons, % of labour force

Moderating price and wage inflation

02468

101214161820

CPI

Wages

Consumer price index and wages, average % change

Supportive fiscal policy

-12

-10

-8

-6

-4

-2

0

2

4

1996 1998 2000 2002 2004 2006

Government budget balance, % GDP

Credit expanding fast, but level low

-10

-5

0

5

10

15

20

25

30

35

1996 1998 2000 2002 2004 2006

0

20

40

60

80

100

120

Growth (Left axis)

% GDP (Right axis)

Growth in domestic credit stock

External weakness growing

-25

-20

-15

-10

-5

0

5

10

15

1996 1998 2000 2002 2004 2006

CA balance

Trade balance

External balances, % of GDP

Overall debt dynamics favourable

0

20

40

60

80

100

120

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Private sector

Public sector

External debt, % GDP

Foreign capital inflows booming

0

1000

2000

3000

4000

5000

6000

1996 1998 2000 2002 2004 2006

Foreign Direct Investment, US$mn

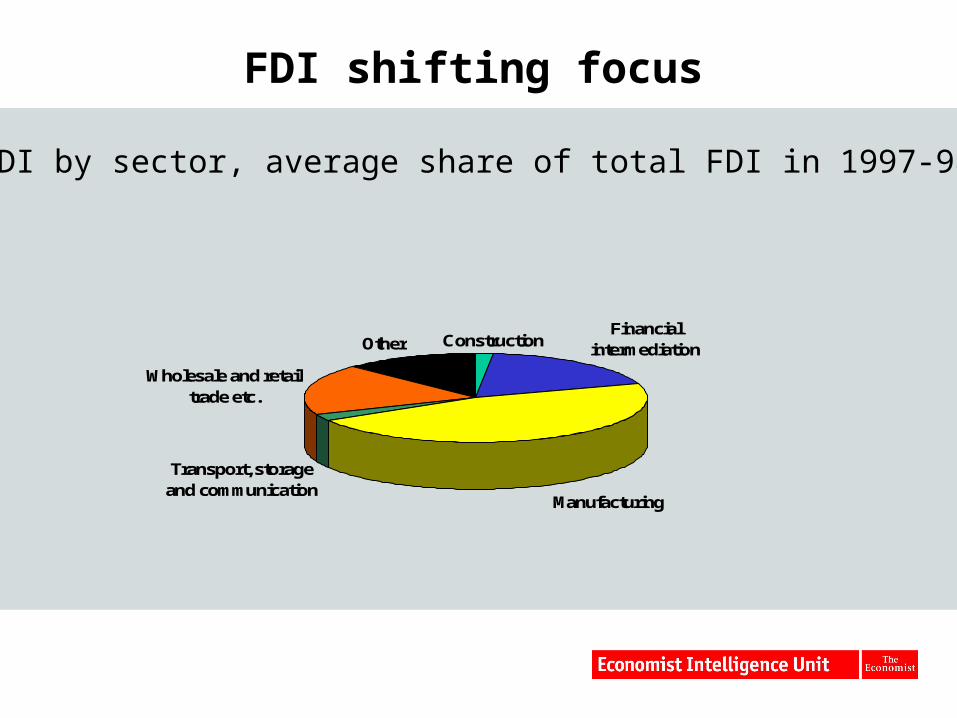

FDI shifting focus

ConstructionFinancial

intermediation

Manufacturing

Transport, storage and communication

Wholesale and retail trade etc.

Other

FDI by sector, average share of total FDI in 1997-98

FDI shifting focus (continued)

Construction

Energy

Financial intermediation

Manufacturing

Real estate, renting and business

activities

Wholesale and retail trade etc.

Other

FDI by sector, average share of total FDI in 2005-06

Capital investment driving potential output

-30-25-20-15-10-505

10152025

1996 1998 2000 2002 2004 2006

Capital

TFP

Labour

Potential output

Growth in labour, capital and total factor productivity, %

Business environment improves

0

10

20

30

4050

60

70

80

90100

UK LT EE DE LV FR SK RO CZ BG SQ HU PL IT RU

2007

2006

World Bank Ease of Doing Business Rank (1 = highest)

Catch-up proceeding slowly

0

10

20

30

40

50

60

70

80

90

1989

1991

1993

1995

1997

1999

2001

2003

2005

EU-27

CEE

Ratio of Bulgarian to EU-27 and CEE GDP per head at PPP

Catch up: GDP per head, EU15=100

0

10

20

30

4050

60

70

80

90C

zech

Hu

ng

ary

Po

lan

d

Slo

vaki

a

Slo

ven

ia

Bu

lgar

ia

Ro

man

ia

Cro

atia

Ser

bia

Est

on

ia

Lat

via

Lit

hu

ania

2005

2025

EU15 growth at 2% pa

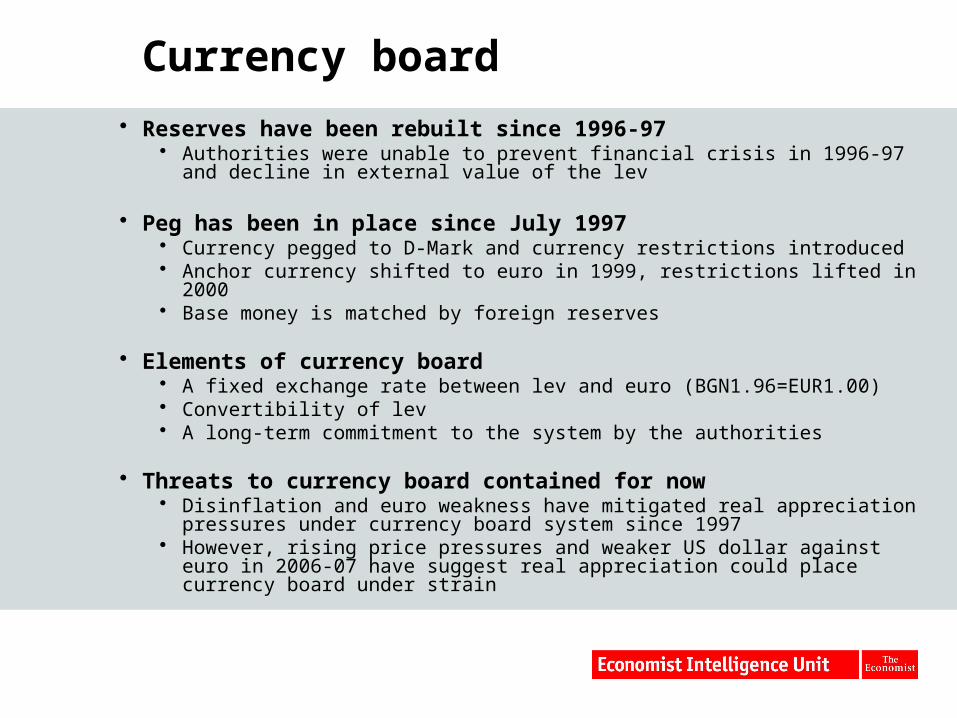

Currency board

Reserves have been rebuilt since 1996-97 Authorities were unable to prevent financial crisis in 1996-97 and decline in

external value of the lev

Peg has been in place since July 1997 Currency pegged to D-Mark and currency restrictions introduced Anchor currency shifted to euro in 1999, restrictions lifted in 2000 Base money is matched by foreign reserves

Elements of currency board A fixed exchange rate between lev and euro (BGN1.96=EUR1.00) Convertibility of lev A long-term commitment to the system by the authorities

Threats to currency board contained for now Disinflation and euro weakness have mitigated real appreciation pressures

under currency board system since 1997 However, rising price pressures and weaker US dollar against euro in 2006-

07 have suggest real appreciation could place currency board under strain

Currency board

0

2000

4000

6000

8000

10000

12000

1996 1998 2000 2002 2004 2006

Intl. reserves

M1

Reserves and the monetary base (US$ m)

M1 includes demand accounts

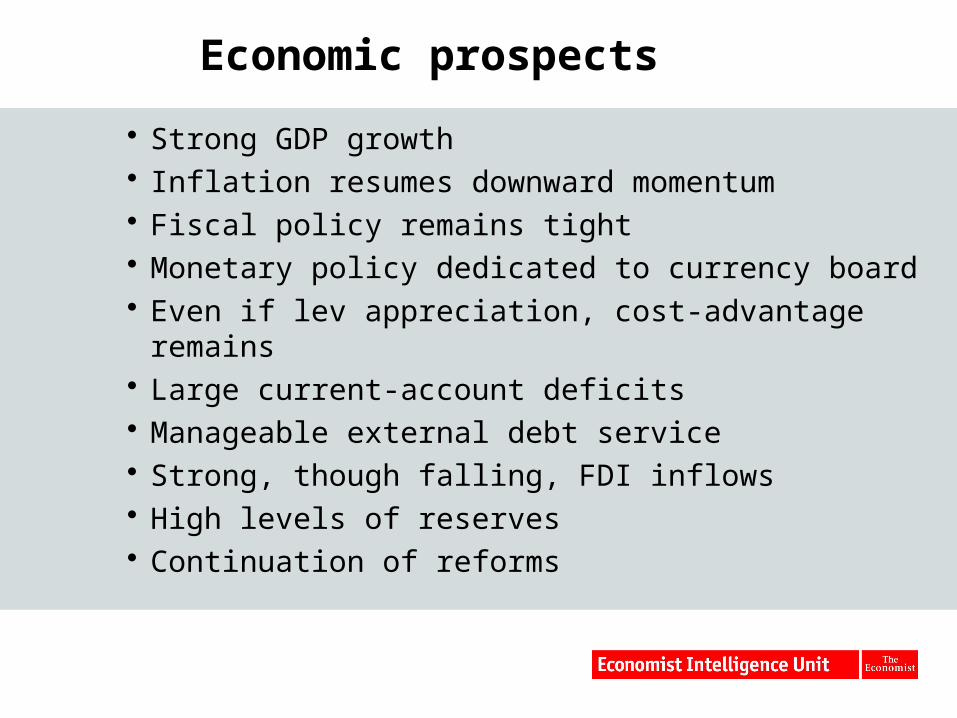

Economic prospects

Strong GDP growth Inflation resumes downward momentum Fiscal policy remains tight Monetary policy dedicated to currency board Even if lev appreciation, cost-advantage remains Large current-account deficits Manageable external debt service Strong, though falling, FDI inflows High levels of reserves Continuation of reforms

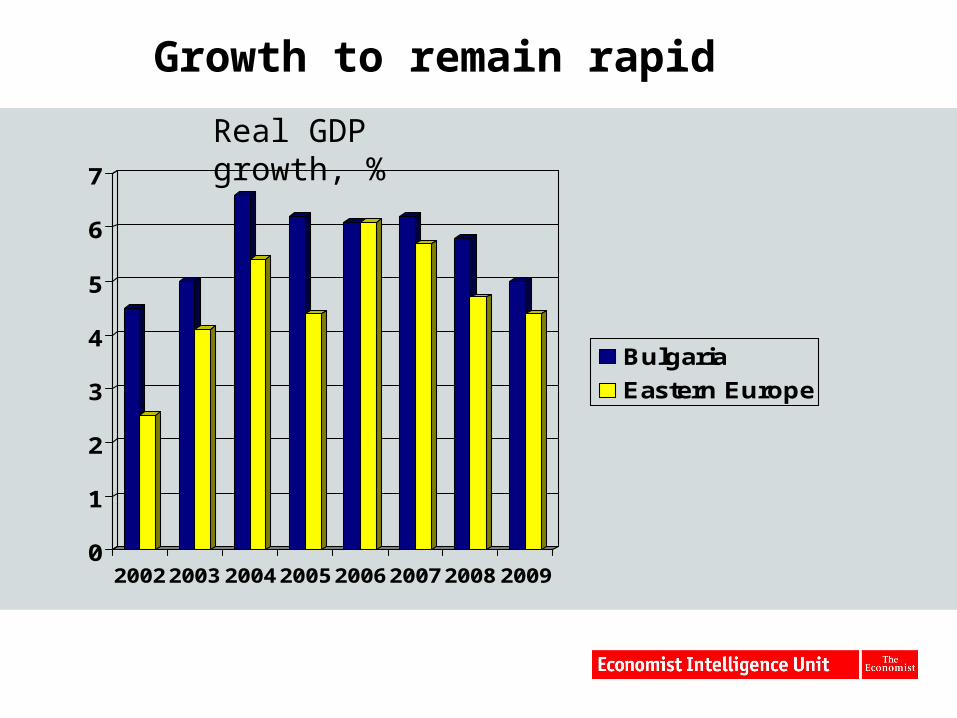

Real GDP growth, %

0

1

2

3

4

5

6

7

2002 2003 2004 2005 2006 2007 2008 2009

Bulgaria

Eastern Europe

Growth to remain rapid

Inflation, average annual %

0

1

2

3

4

5

6

7

8

2002 2003 2004 2005 2006 2007 2008 2009

Bulgaria

Euro zone

Disinflation to continue

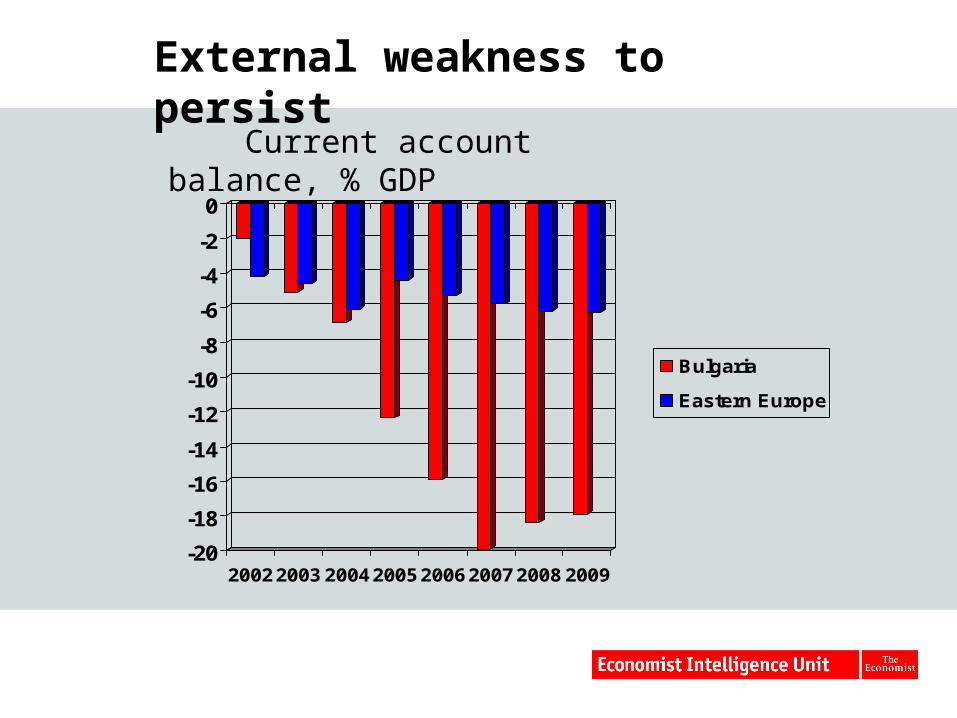

Current account balance, % GDP

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

2002 2003 2004 2005 2006 2007 2008 2009

Bulgaria

Eastern Europe

External weakness to persist

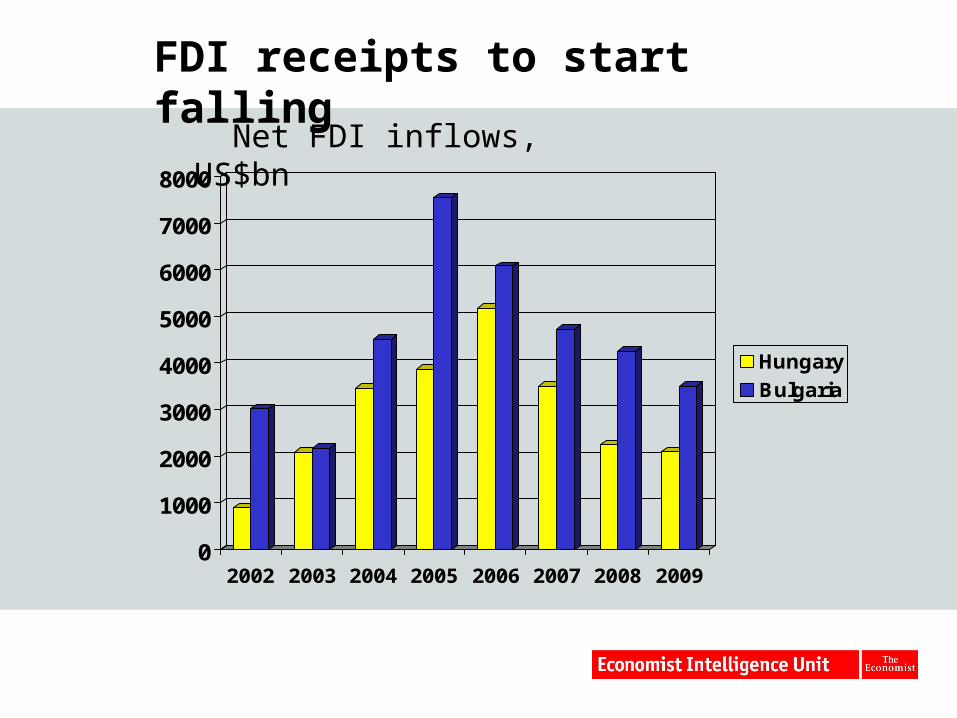

Net FDI inflows, US$bn

0

1000

2000

3000

4000

5000

6000

7000

8000

2002 2003 2004 2005 2006 2007 2008 2009

Hungary

Bulgaria

FDI receipts to start falling

Net FDI inflows, as % of GDP

0

2

4

6

8

10

12

14

16

2002 2003 2004 2005 2006 2007 2008 2009

Bulgaria

Hungary

FDI receipts to start falling (continued)

Economic risks

Managing underlying vulnerabilities External deficit

Continuing structural reform post-EU Maintaining reform momentum after EU accession

A very poor demographic outlook Need to review labour market incentives

Growth challengecan +5% pa growth be sustained?

Net FDI inflows, % of Current account balance

0

50

100

150

200

250

300

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

CA deficit financing has deteriorated

External deficit

Has grown partly as a consequence of FDI inflows This has been shown to a be key factor in supporting income convergence … but economic vulnerability is higher nonetheless

Private sector foreign borrowing is more worrying Need to monitor risks allied to foreign borrowing

Export performance crucial Although non-trade elements of CA have also deteriorated, hopes for

improving external stability rest with a recovery of exports Data certainly no clear price- or wage-based competitiveness concerns But continuing structural reforms needed to ensure state enterprises are

restructured

Sustainability threat not obvious IMF research suggests that CA imbalance is broadly consistent with

Bulgaria’s stage of economic development

Price competitiveness

Gross monthly wages, US$

Predicted Actual Act/pr Predicted Actual Act/pr

Czech 685 701 1.02 Bulgaria 268 190 0.71

Hungary 725 719 0.99 Romania 242 253 1.04

Poland 619 627 1.01 Albania 206 236 1.14

Slovakia 661 491 0.74 B & H 372 475 1.28

Slovenia 1,398 1,478 1.06 Croatia 666 922 1.49

Estonia 636 573 0.90 Macedonia 345 421 1.22

Latvia 450 390 0.87 Serbia 257 350 1.36

Lithuania 570 472 0.83

“Equilibrium wages” estimated or predicted on the basis of a relationship between wages and productivity (output per employed, at PPP) and several other variables, across 70 economies.

EU membership and growth

Positive Reinforces political stability, reduces risksImpact on trade/FDI; removal of residual trade barriers Institutional development aided, albeit over long time frameEncourages macro policy disciplineEU funding for infrastructure development

Negatives Membership removes reform anchorMuch of acquis inappropriate for less developedHarmonisation pitfalls

- EU social and environment regulation

- Pressure for tax harmonisationStability or growth bias

• EU entry offers a possibility, not a guarantee of stimulating per-capita GDP convergence

• Key assumptions: trade integration; macro stability and price competitiveness; further deregulation; slow institutional improvement

• Modest pace of convergence. On baseline forecast, by 2025 Bulgaria reaches about 40% of EU-15 average income per head, from less than 30% at present

• Despite post-accession benchmarking, risk that Bulgaria’s commitment to EU-related reform weakens in line with greater political disunity

EU membership and growth

A declining and ageing population

0

1000

2000

3000

4000

5000

6000

7000

8000

2004 2025 2050

0

10

20

30

40

50

60

70

80

90

65+ (Left axis)

15-64 (Left axis)

0-14 (Left axis)

Ratio (Right axis)

Population by age group, thousandsand dependency ratio

• Bulgaria’s population has been declining for more than a decade

• It is projected to decline by another 24% by 2035 and the working-age population by 31%

• Policies needed to encourage higher labour market participation

• Incentives need to be reviewed to ensure that participation in the labour force is more effectively encouraged

• The IMF has called for a “release of excess staff from the public sector”, which it believes would lead to higher labour supply to the private sector

• Poor demographics shared by most CEE states, a produce of net migration and negative natural population increase

Adverse demographics

Assessment of currency board risks External deficit

Much of the external deficit is consistent with Bulgaria’s stage of economic catch-up Non-debt creating finance (FDI) has helped to finance current account deficit, but financing is expect to

deteriorate

Public finances Very restrictive (budget balance in surplus since 2004, primary balance in surplus since 1994). Fiscal overperformance has been used to build up a huge fiscal reserve, and has used this to make

early repayments of public sector external debt.

Private sector debt accumulation Perhaps most worrying aspect of recent economic developments rivate sector component has been rising rapidly, while public sector component has been coming down

because of the government's aggressive prepayments. Private sector credit growth a concern

Debt structure 75% of Bulgaria's external debt in euros. No large market of BGN-denominated instruments to serve as

a channel for forcing currency adjustment. Portfolio inflows (hot money flows) are relatively minor.

Banking sector

Overwhelmingly under foreign control and improving in terms of profitability and stability.

Summary of challenges

Nature of challenge

Growth Keep well-balanced

Inflation Emerging energy dependence could increase inflation

Fiscal policy Maintain tight fiscal policy

Monetary policy Preserve currency board despite large external deficit, manage credit growth and banking sector risk

External sector Manage and reduce vulnerability

FDI Ensure opportunities for greenfield investment when privatisation program comes to an end

Competitiveness Address problem of falling working-age population, invest in R&D to decrease reliance on labour-cost advantages

Business environment Need to further improve institutions and regulations