bumrungrad hospital public company...

TRANSCRIPT

PG.1

Bumrungrad Hospital Public Company Limited

6 March 2015

Analyst Meeting No.1/2015 (4Q14 and 2014 Results Update)

PG.2

Disclaimer • The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or

the solicitation of an offer or invitation to purchase or subscribe for any securities of Bumrungrad Hospital Public Company Limited (the

"Company") in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in connection with, any contract or

commitment whatsoever.

• This presentation is being communicated only to persons who have professional experience in matters relating to investments and/or

to persons to whom it is lawful to communicate it under the laws of applicable jurisdictions. Other persons should not rely or act upon

this presentation or any of its contents.

• Certain information and statements made in this presentation contain the Company's forward-looking statements. All forward-looking

statements are the Company's current expectation of future events and are subject to a number of factors that could cause actual

results to differ materially from those described in the forward-looking statements. Prospective investors should take care with respect

to such statements and should not place undue reliance on any such forward-looking statements.

• This presentation has been prepared by the Company solely for the use at this presentation. The information in this presentation has

not been independently verified. No representation, warranty, express or implied, is made as to, and no reliance should be placed on,

the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the Company, any of

its affiliates or any of their respective agents, advisors or representatives, shall have any liability (in negligence or otherwise) for any

loss or damage howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this

presentation. The information presented or contained in this presentation is current as of the date hereof and is subject to change

without notice and its accuracy is not guaranteed. None of the Company, any of its affiliates or any of their respective agents, advisors

or representatives, makes any undertaking to update any such information subsequent to the date hereof.

• This presentation should not be construed as legal, tax, investment or other advice. No part of this presentation shall be relied upon

directly or indirectly for any investment decision-making or for any other purposes. Prospective investors should undertake their own

assessment with regard to any investment and should obtain independent advice on any such investment’s suitability, inherent risks

and merits and any tax, legal and accounting implications which it may have for them.

• Certain data in this presentation were obtained from various external data sources, and none of the Company, any of its affiliates or

any of their respective agents, advisors or representatives have verified such data with independent sources. Accordingly, the Company

makes no representation as to the accuracy or completeness of those data, and such data involve risks and uncertainties and are

subject to change based on various factors.

PG.3

Overview

• Outpatient and inpatient volumes advanced 14.9% and 19.8%, respectively, in 4Q14 compared with 4Q13, with most of the increase due to volumes contributed by the UBSD acquisition, and strong growth in international volumes. Excluding UBSD, outpatient and inpatient volumes grew 3.7% and 7.4%, respectively. International outpatient volumes increased 8.2%, while inpatient volumes jumped 12.7%. Impacted by the significantly lower intensity services provided by UBSD compared to those provided by the Company, revenue intensity declined 7.0% and 11.3% for outpatient and inpatient services, respectively. Revenue intensity, excluding UBSD, declined 0.3% for inpatient services and rose 2.1% for outpatient services. The combined results of the above resulted in outpatient service revenues advancing 14.4% while inpatient service revenues grew 13.9%.

Operational Update

Financial Performance

• Bangkok - Obtained EIA Approval for Petchburi project

• Thailand - Continuing Bumrungrad network development

• International - Mongolia, developing and improving the capability of UBSD

Updates and Ongoing

Focus

4Q14 growth 2014 growth

Total revenues 13.8% 8.6%

EBITDA 16.9% 12.4%

Net profit 9.9% 8.3%

PG.4

Agenda

Strategy

Operational Update

Financial Performance

PG.5

Strategy

• Campus expansion

• Doctor recruitment in subspecialties

• Advanced technology

• Skilled work force

Bumrungrad International

Hospital

• Development of the Bumrungrad Network • Expand into a new market segment – 2nd Brand

Thailand

• Evolve UB Songdo into a regional referral hospital

• Review of selective opportunities in existing referral markets

International

PG.6

Strategy (Detail)

• Opened 5 floors in Bumrungrad International Clinic

• Renovate and expand clinics in Bumrungrad International Hospital

Clinics

• Added 18 ICU beds and 58 ward beds in Bumrungrad International Hospital building

• Renovate and expand ancillary services Inpatient

• Bought 8,200 sq. meters of land on Petchburi Road.

• EIA approval received 2nd Campus

• Bought 6,178 sq. meters of land on Sukhumvit Soi 1 to initially develop a parking structure

• Grand opening of Bumrungrad Tower on 6 March 2015 for employee houses and back office functions

Acquire Additional Capacity

• Acquired controlling interest in UB Songdo hospital International

Estimated Capital Investment (Million THB)

Y15 Y16 Y17 Y18 Total

1,598 3,231 4,550 392 9,771

PG.7

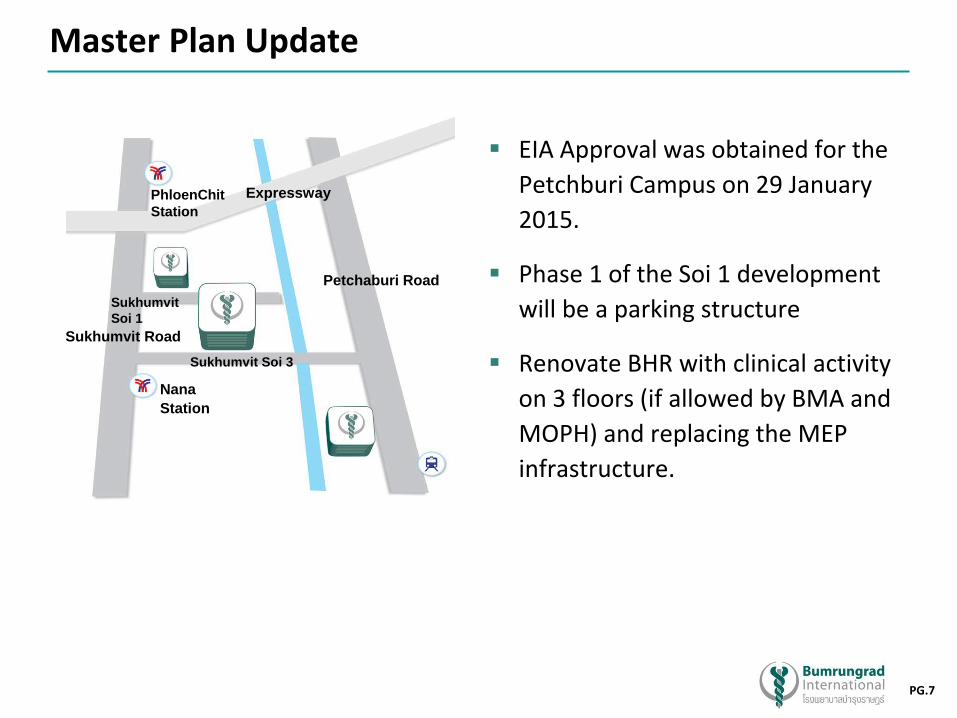

Master Plan Update

EIA Approval was obtained for the

Petchburi Campus on 29 January

2015.

Phase 1 of the Soi 1 development

will be a parking structure

Renovate BHR with clinical activity

on 3 floors (if allowed by BMA and

MOPH) and replacing the MEP

infrastructure.

Sukhumvit

Soi 1

Petchaburi Road

Sukhumvit Soi 3

Nana Station

Sukhumvit Road

Expressway PhloenChit

Station

PG.8

Current Status – Petchburi Project

• EIA Approval was obtained for the Petchburi Campus on 29 January 2015.

• The EIA Approval allows:

• 100% FAR: 8,204 x 8 = 65,632 m2

• 19.2% Bonus FAR = 12,601 m2

• Maximum FAR = 78,233 m2

• Construction Area is likely to be around 85,000 m2

• Construction expected to start in November 2015

PG.9

Strategy

Operational Update

Financial Performance

Agenda

PG.10

Outpatient Visits Volume Trend

4th Quarter: Outpatient volumes advanced 14.9% in 4Q14 compared with 4Q13, with most of the increase due to volumes contributed by the UBSD acquisition, and strong growth in international volumes. Excluding UBSD, outpatient volumes grew 3.7% in 4Q14.

YTD Dec: Outpatient volumes advanced 7.5% in 2014 compared with 2013 as a result of volumes added by the UBSD acquisition. Excluding UBSD volumes, outpatient volumes declined 1.5% in 2014.

Visits

Average Visits per Day

0.1% 7.5%

3,017 3,021 3,021 3,021

3,249

2,976

0

800

1,600

2,400

3,200

4,000

2012 2013 2014

(exc. HHE)

1.5%

3,004 2,958 3,069 3,022 3,038 2,958 2,958 2,820

3,348 3,424 3,397 3,068

0

1,000

2,000

3,000

4,000

4Q 1Q 2Q(inc. HHE)

3Q(inc. HHE)

4Q(inc. HHE)

4Q(exc.HHE)

2012 2013 2014

Visits

Average Visits per Day

8.1% 10.8% 1.5% 12.7% 3.7% 14.9%

PG.11

Admissions Volume Trend

Admissions

Average Admissions per Day

11.2%

85 84 84 84

94 86

0

20

40

60

80

100

2012 2013 2014

1.0%

4th Quarter: Inpatient volumes advanced 19.8% in 4Q14 compared with 4Q13, with most of the increase due to volumes contributed by the UBSD acquisition, and strong growth in international volumes. Excluding UBSD, inpatient volumes grew 7.4% in 4Q14.

YTD Dec: Inpatient volumes advanced 11.2% in 2014 compared with 2013 as a result of volumes added by the UBSD acquisition. Excluding UBSD volumes, inpatient volume grew 1.8% in 2014.

1.8%

(exc. HHE)

84 83 86 80

89 83 83

84 91

101 99 89

0

20

40

60

80

100

120

4Q 1Q 2Q(inc.HHE)

3Q(inc.HHE)

4Q(inc.HHE)

4Q(exc.HHE)

2012 2013 2014

Admissions

Average Admissions per Day

2.0% 1.9% 13.1% 13.7% 7.4% 19.8%

PG.12

Average Daily Census Volume Trend

ADC

Average Daily Census

12.2%

379

370 370 370

415

371

340

360

380

400

420

2012 2013 2014

(exc. HHE)

2.4%

4th Quarter: ADC advanced 19.7% in 4Q14 compared with 4Q13, with most of the increase due to volumes contributed by the UBSD acquisition, and strong growth in international volumes. Excluding UBSD, ADC grew 3.7% in 4Q14. YTD Dec: ADC advanced 12.2% in 2014 compared with 2013, with most of the increase due to volumes contributed by the UBSD acquisition. Excluding UBSD, ADC grew 0.3% in 2014.

ADC

Average Daily Census

378 368

381

356 374 368 368

374

406

438 440

381

300

320

340

360

380

400

420

440

460

4Q 1Q 2Q(inc.HHE)

3Q(inc.HHE)

4Q(inc.HHE)

4Q(exc.HHE)

2012 2013 2014

2.7% 1.9% 14.1% 17.3% 3.7% 19.7%

0.3%

PG.13

Revenue per episode reflects an increase from the

1st Jan 2014 price adjustment.

OPD Revenue intensity :

4th Quarter YTD Dec

Including HHE Consolidated FS -7.0% -8.9%

Excluding HHE Consolidated FS 2.1% -1.7%

OPD Revenue Intensity

Bt

Revenue per Visit

6,560

7,428 7,428 7,428 7,341

7,891

4,000

5,000

6,000

7,000

8,000

9,000

2012 2013 2014(exc. HHE) (inc. HHE)

Bt

Revenue per Visit

7,192

7,411 7,459 7,652 7,652 7,531

6,982 7,254

7,624

8,289

4,000

5,000

6,000

7,000

8,000

9,000

1Q 2Q(inc.HHE)

3Q(inc.HHE)

4Q(inc.HHE)

4Q(exc.HHE)

2012 2013 2014

5.8% 4.7% 8.3% 0.4%

6.2%

2.8%

13.2% 1.2%

PG.14

IPD Revenue Intensity

Revenue per episode reflects an increase from the

1st Jan 2014 price adjustment.

IPD Revenue intensity per admission:

4th Quarter YTD Dec

Including HHE Consolidated FS -11.3% -6.7%

Excluding HHE Consolidated FS -0.3% 1.7%

Bt

Revenue per Admission

220,001

241,340 241,340 241,340

242,410 262,366

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2012 2013 2014(exc. HHE) (inc. HHE)

Bt

Revenue per Admission

233,385 246,372 234,988 251,356 251,356

263,996

238,899 231,289

238,959 263,404

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1Q 2Q(inc.HHE)

3Q(inc.HHE)

4Q(inc.HHE)

4Q(exc.HHE)

2013 2014

3.0% 13.1% 4.8% 4.9%

8.7%

1.6%

9.7% 0.4%

PG.15

Volume Contribution by Nationality

Revenue Contribution by Nationality

International Breakdown

• For 4Q14: Revenues by market segment international patients

accounted for 63.2% of the total in 4Q14, with the remaining

36.8% from Thai patients, reflecting a decrease in the 39.1%

from Thai patients in 4Q13, and the noted improvement of the

international business.

• 2014 Top 5 revenue contribution by Non-Thai Nationalities

Myanmar 8%

UAE 7%

Oman 7%

USA 5%

Cambodia 3%

62% 61% 60% 61% 59% 62% 60% 63%

38% 39% 40% 39% 41% 38% 40% 37%

0%

20%

40%

60%

80%

100%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

International Thai

47% 47% 46% 47% 44% 52% 52% 53%

53% 53% 54% 53% 56% 48% 48% 47%

0%

20%

40%

60%

80%

100%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

International Thai

PG.16

Revenue Breakdown

Inpatient vs. Outpatient (% of revenue) Method of Payment (% of revenue)

Y2014

• 4Q14 Revenue growth:

Outpatient revenue increased by 14.4% y-o-y

Inpatient revenue increased by 13.9% y-o-y

• Self-pay remains the primary method of payment

48% 47% 48% 48% 51% 48% 48% 48%

52% 53% 52% 52% 49% 52% 52% 52%

0%

20%

40%

60%

80%

100%

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

Inpatient Outpatient

Corporate Contracts - Domestic

9%

Corporate Contracts -

Intl 8%

Self-pay 69%

Insurance 14%

PG.17

Agenda

Strategy

Operational Update

Financial Performance

PG.18

Revenue from Hospital Operations

Revenue from Hospital Operations (THB mm)

3,641

14,251

4,166

15,571

0

4,000

8,000

12,000

16,000

4th Quarter YTD Dec

Y2013 Y20149.3%

14.4%

• 2014: Revenues from hospital operations were Baht 15,571 million for

2014, a 9.3% improvement year-over-year from Baht 14,251 million in

2013. Outpatient and inpatient volumes advanced 7.5% and 11.2%,

respectively, in 2014 compared with 2013 as a result of volumes

added by the UBSD acquisition. Excluding UBSD volumes, outpatient

volumes declined 1.5% in 2014 while inpatient volume grew 1.8% in

2014, both impacted by the ongoing political environment in Thailand

that began in 1Q14 and continued to contribute to weak volumes and

lower revenue intensity, especially through 2Q14. Volumes from the

international market segment were significantly more impacted than

volumes from the Thai and expat market segments during this period,

although international volumes progressively recovered after 2Q14

and exhibited strong growth in 4Q14. Thai volumes ended 2014 with a

2.6% increase in admissions and a 1.2% decrease in outpatient visits,

while international volumes, excluding UBSD, slightly increased 0.9%

in admissions with a 1.9% decrease in outpatient visits year-over-year.

Impacted by the significantly lower intensity services provided by

UBSD compared to the Company’s, and to a lesser degree the drop in

international volumes and elective procedures caused by the unstable

Thailand political environment, revenue intensity decreased by 8.9%

and 6.7% for outpatient and inpatient services, respectively. Revenue

intensity, excluding UBSD, decreased 1.7% for outpatient services,

while inpatient services intensity improved 3.1% on a patient-day

basis and 1.7% on an admission basis. The combined results of the

above resulted in outpatient service revenues advancing 6.3% while

inpatient service revenues grew by 11.7%.

• 4Q14: The Company reported Revenues from hospital operations of Baht

4,166 million, a 14.4% improvement year-over-year from Baht 3,641

million in 4Q13. Outpatient and inpatient volumes advanced 14.9% and

19.8%, respectively, in 4Q14 compared with 4Q13, with most of the

increase due to volumes contributed by the UBSD acquisition, and strong

growth in international volumes. Excluding UBSD, outpatient and

inpatient volumes grew 3.7% and 7.4%, respectively. International

outpatient volumes increased 8.2%, while inpatient volumes jumped

12.7%. Impacted by the significantly lower intensity services provided by

UBSD compared to those provided by the Company, revenue intensity

declined 7.0% and 11.3% for outpatient and inpatient services,

respectively. Revenue intensity, excluding UBSD, declined 0.3% for

inpatient services and rose 2.1% for outpatient services. The combined

results of the above resulted in outpatient service revenues advancing

14.4% while inpatient service revenues grew 13.9%.

PG.19

EBITDA and EBITDA Margin

EBITDA (THB mm)

EBITDA Margin

27.4% 27.7% 28.0% 28.6%

20.0%

22.0%

24.0%

26.0%

28.0%

30.0%

32.0%

4th Quarter YTD Dec

Y2013 Y2014

16.9%

12.4%

1,011

4,016

1,182

4,516

0

600

1,200

1,800

2,400

3,000

3,600

4,200

4,800

4th Quarter YTD Dec

Y2013 Y2014

• 4Q14: Cost of hospital operations (including Depreciation and amortization) was Baht 2,574 million for 4Q14, or 14.2% more year-over-year from Baht 2,253 million in 4Q13, compared to the 14.4% growth in Revenues from hospital operations. Administrative expenses (including Depreciation and amortization) were Baht 757 million in 4Q14, or 3.5% more than Baht 732 million in 4Q13. The small percentage increase in Administrative expenses was mostly due to Baht 27 million increase in repairs and maintenance expense, Baht 26 million associated with a physical inventory adjustment, and Baht 19 million in additional software support and maintenance offset by a Baht 46 million reduction in Depreciation and amortization associated with the revised estimated useful lives of certain assets in 4Q13, and Baht 11 million decrease in Bad debt expense, as a result of additional reserves taken in 4Q13. EBITDA grew 16.9% year-over-year from Baht 1,011 million in 4Q13 to Baht 1,182 million in 4Q14, with an EBITDA margin of 28.0% in 4Q14 compared to 27.4% in 4Q13.

• 2014: Cost of hospital operations (including Depreciation and amortization) was Baht 9,496 million for 2014, or 7.5% more year-over-year from Baht 8,836 million in 2013, compared to the 9.3% growth in Revenues from hospital operations. The percentage of Cost of hospital operations to Revenues from hospital operations improved from 62.0% in 2013 to 61.0% in 2014. Administrative expenses (including Depreciation and amortization) were Baht 2,806 million in 2014, increasing 11.0% from Baht 2,527 million in 2013. This change included Baht 74 million in additional repair and maintenance expense, Baht 69 million in donations to support nurse recruitment, Baht 43 million in inflationary increases in staff cost, Baht 29 million in Depreciation and amortization associated with the campus expansion and revised estimated useful lives of certain assets, and Baht 20 million more in software support and maintenance. EBITDA grew 12.4% year-over-year from Baht 4,016 million in 2013 to Baht 4,516 million in 2014, with the EBITDA margin advancing to 28.6% in 2014 compared with 27.7% in 2013.

PG.20

Net Profit (THB mm)

Diluted EPS (THB)

Net Profit Margin

Net Profit, Net Profit Margin and Diluted EPS

17.2%17.2%16.8%

16.2%

12.0%

14.0%

16.0%

18.0%

20.0%

4th Quarter YTD Dec

Y2013 Y2014

• 4Q14 : Net profit for 4Q14 grew 9.9% to Baht 689 million from Baht 626 million in 4Q13, with Net profit margin at 16.2% in 4Q14 compared to 16.8% in 4Q13.The change in Net profit margin was due to a decrease in capitalized interest expense associated with the campus expansion caused by the full Y2013 amount recorded in 4Q13, versus monthly recording in Y2014. Excluding this variance, Net profit margin for 2013 would have been 15.0%.Diluted EPS increased at the same rate as Net profit to Baht 0.79 from Baht 0.72 in 4Q13.

• 2014 : Net profit advanced 8.3% to Baht 2,730 million in 2014 from Baht 2,521 million in 2013, with Net profit margin at 17.2% for both 2014 and 2013. Diluted EPS increased at the same rate as Net profit to Baht 3.15 from Baht 2.91 in 2013.

626

2,521

689

2,730

0

500

1,000

1,500

2,000

2,500

3,000

4th Quarter YTD Dec

Y2013 Y2014

9.9%

8.3%

0.72

2.91

0.79

3.15

0.00

0.40

0.80

1.20

1.60

2.00

2.40

2.80

3.20

4th Quarter YTD Dec

2013 2014

9.9%

8.3%

PG.21

Leverage x Interest Coverage

x

Net Debt to EBITDA

x

Net Debt to Equity

x

** *

0.2

0.6

(0.1)

0.2

0.0

(0.25)

0.00

0.25

0.50

0.75

2010 20112012

2013 2014

0.4

1.3

(0.3)

0.5

0.1

(0.50)

0.00

0.50

1.00

1.50

2010 2011

2012

2013 2014

35.9

14.9 13.8 16.4

18.8

0

10

20

30

40

2010 2011 2012 2013 2014

• As a result of the increase in Cash and cash equivalents, Net debt to equity improved to 0.0x as at 31 December 2014 from 0.2x as at 31 December 2013.

• After adding back the 2014 and 2013 capitalized interest expense related to the campus expansion of Baht 55 million and Baht 97 million, respectively, the Company’s Interest coverage ratio improved to 18.8x in 2014 from 16.4x in 2013, due to higher EBITDA in 2014 compared to 2013.

**

*Interest expense related to the purchase of common shares of Bangkok Chain Hospital PCL (doing business as "Kasemrad Hospital Group") to calculate interest coverage ratio was Baht 111 million based on remaining days after the transaction settled. Assuming this interest expense was incurred for the full year, interest expense from this transaction would be Baht 140 million and interest coverage ratio will be 12.9x **After adding back the 2014 and 2013 capitalized interest expense related to the campus expansion.

Note: Net debt excludes fixed deposits with a maturity exceeding three months but not more than one year which are reported as Short-term investments of Baht 1,922 million in 2014 and Baht 2,718 million in 2013.

PG.22

Q & A