bus312a/612a financial reporting i - goizueta business … 2014/h.10.22.1.00.pdf · ·...

TRANSCRIPT

BUS312A/612A

Financial Reporting I

Homework

Inventory

Chapter 8

Chapter 8

Inventory & Cost of

Sales

Objectives

Chapter 8

You should be able to

• Discuss the relevance of inventory methods

• Compare the periodic and perpetual inventory systems

• Identify the effects of inventory errors on financial statements

• Identify the items included as inventory costs

• Compare FIFO, LIFO, Average cost, specific identification, Dollar Value LIFO, and pooling methods)

• Extract inventory information from financial statements

• Convert COGS and inventory from LIFO to FIFO using information in the financial statements

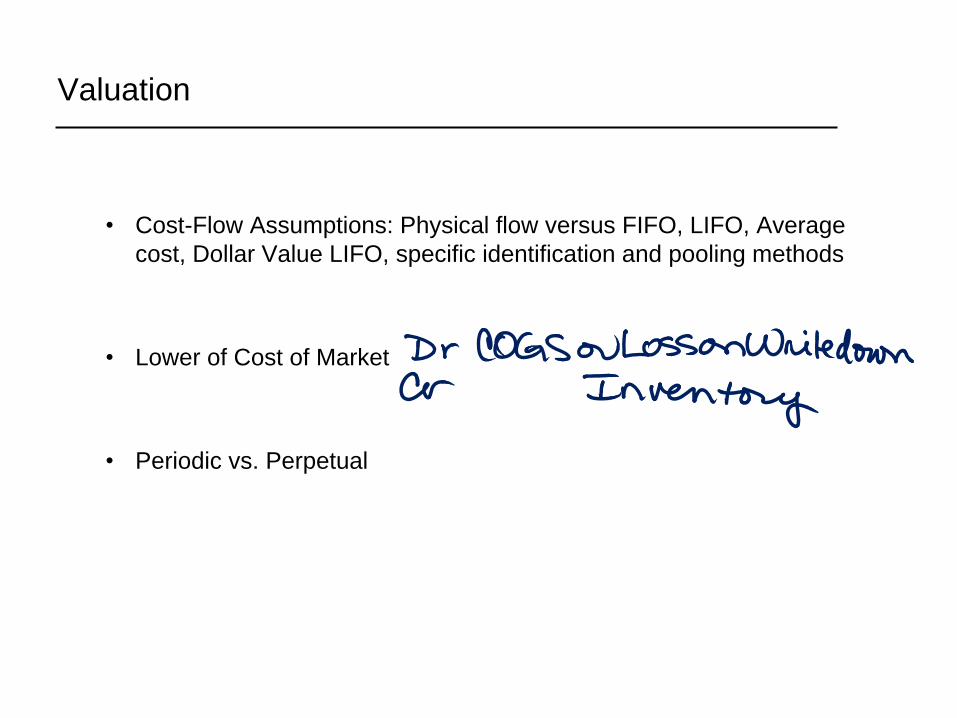

Valuation

• Cost-Flow Assumptions: Physical flow versus FIFO, LIFO, Average

cost, Dollar Value LIFO, specific identification and pooling methods

• Lower of Cost of Market

• Periodic vs. Perpetual

Inventory Valuation and Consequences

Same total $$ amount over the life of the company is allocated differently to

cost of goods sold and ending inventory.

• Is Cost of Goods Sold Correct?

• Is Ending Inventory Correct?

• Income and Asset Measurement

– How much does it cost?

– Valuation: Cost-original or replacement, Lower of Cost or Market

• Economic Consequences

– Income Taxes and Liquidity

– Bookkeeping Costs

– LIFO Liquidation and Inventory Purchasing Practices

– Debt and Compensation Practices

– The Capital Market- Current ratio, Profit margin ratio

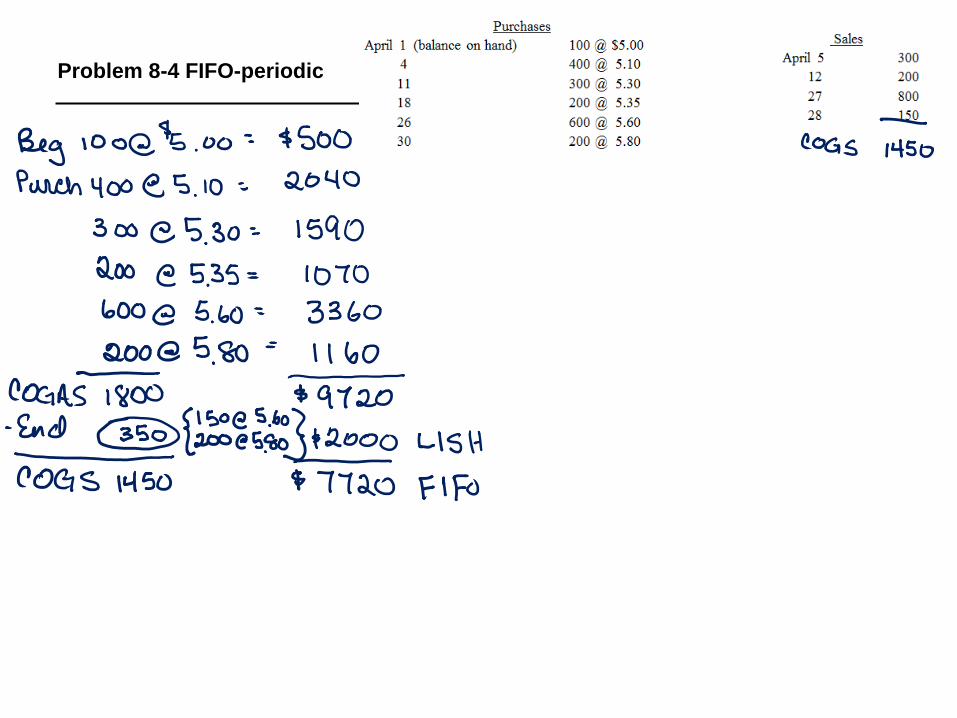

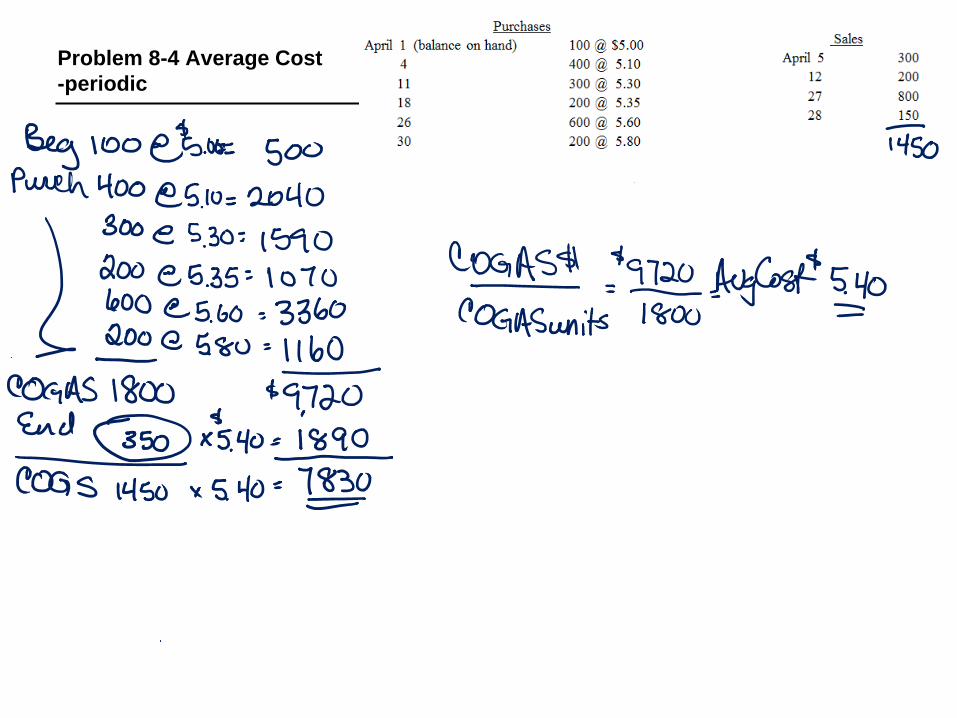

P8-4 (FIFO, LIFO, and Average Cost-Periodic and Perpetual)

Purchases

April 1 (balance on hand) 100 @ $5.00

4 400 @ 5.10

11 300 @ 5.30

18 200 @ 5.35

26 600 @ 5.60

30 200 @ 5.80

Sales

April 5 300

12 200

27 800

28 150

(a) Compute the inventory (kept in units only) at 04/30.

1. FIFO

2. LIFO

3. Average Cost.

(b) If the perpetual inventory record is kept in dollars, and costs are computed at the time of each

withdrawal, what amount would be shown as ending inventory in 1, 2, and 3 above?

Problem 8-4 FIFO-periodic

Problem 8-4 FIFO-periodic

Problem 8-4 LIFO-periodic

Problem 8-4 LIFO-periodic

Problem 8-4 Average Cost

-periodic

Problem 8-4 Average Cost

-periodic

Perpetual

Inventory

Method

Cost of Goods Sold Balance Sheet Inventory

Weighted

Average

FIFO

LIFO

P8-4 Recap

Periodic

Inventory

Method

Cost of Goods Sold Balance Sheet Inventory

Weighted

Average

FIFO

LIFO

Problem 8-4 FIFO-perpetual

Problem 8-4 FIFO-perpetual

Problem 8-4 LIFO-perpetual

Problem 8-4 LIFO-perpetual

Problem 8-4 Average Cost

-perpetual

Problem 8-4 Average Cost

-perpetual

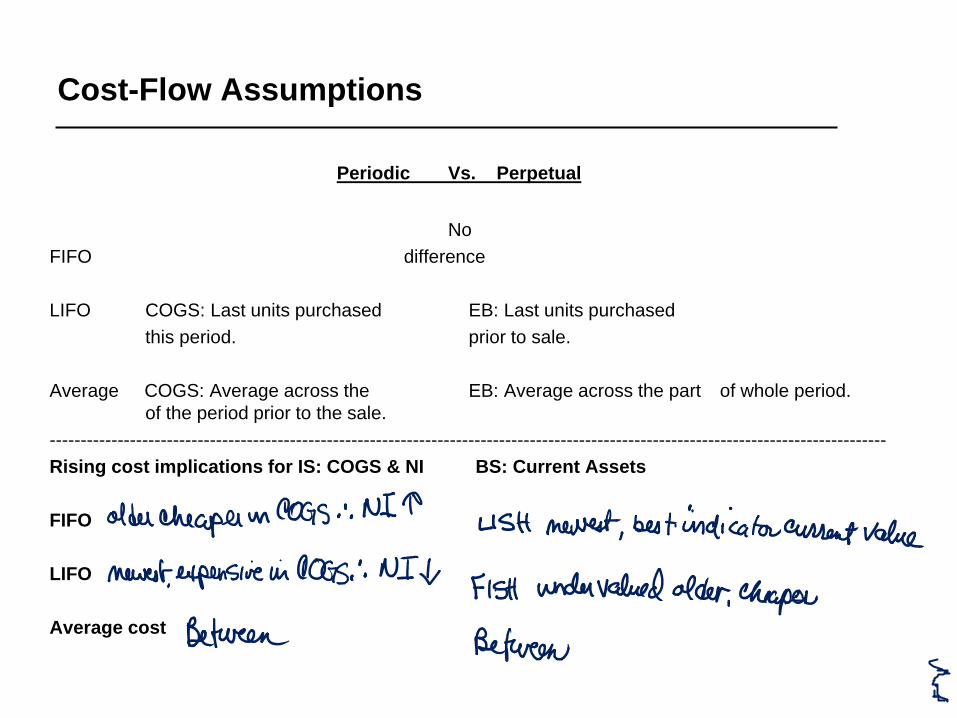

Cost-Flow Assumptions

Periodic Vs. Perpetual

No

FIFO difference

LIFO COGS: Last units purchased EB: Last units purchased

this period. prior to sale.

Average COGS: Average across the EB: Average across the part of whole period.

of the period prior to the sale.

----------------------------------------------------------------------------------------------------------------------------------------

Rising cost implications for IS: COGS & NI BS: Current Assets

FIFO

LIFO

Average cost

Summary of LIFO, FIFO, Average cost

• Managers have wide latitude in inventory cost flow decisions. Specific identification is generally considered appropriate where items of inventory are unique (low volume, high cost items) because of the potential for income manipulation.

• LIFO is generally used when prices are rising because of the tax advantages and the requirement that it be used in the financial statements if it is used for tax purposes.

• The only theoretical defense for LIFO is that in times of extreme inflation, it minimizes the inflationary distortions in the income statement by matching current dollars of revenues and expenses. However, the LIFO method, over time, misrepresents the balance sheet by understating inventory values.

Summary of FIFO, LIFO, Average cost

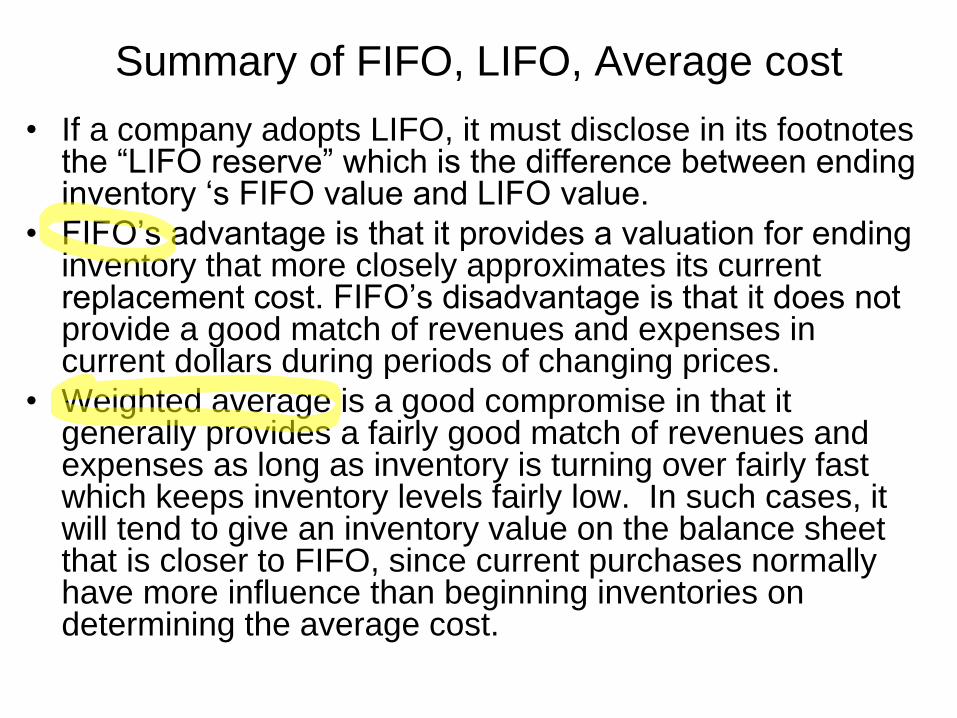

• If a company adopts LIFO, it must disclose in its footnotes the “LIFO reserve” which is the difference between ending inventory ‘s FIFO value and LIFO value.

• FIFO’s advantage is that it provides a valuation for ending inventory that more closely approximates its current replacement cost. FIFO’s disadvantage is that it does not provide a good match of revenues and expenses in current dollars during periods of changing prices.

• Weighted average is a good compromise in that it generally provides a fairly good match of revenues and expenses as long as inventory is turning over fairly fast which keeps inventory levels fairly low. In such cases, it will tend to give an inventory value on the balance sheet that is closer to FIFO, since current purchases normally have more influence than beginning inventories on determining the average cost.

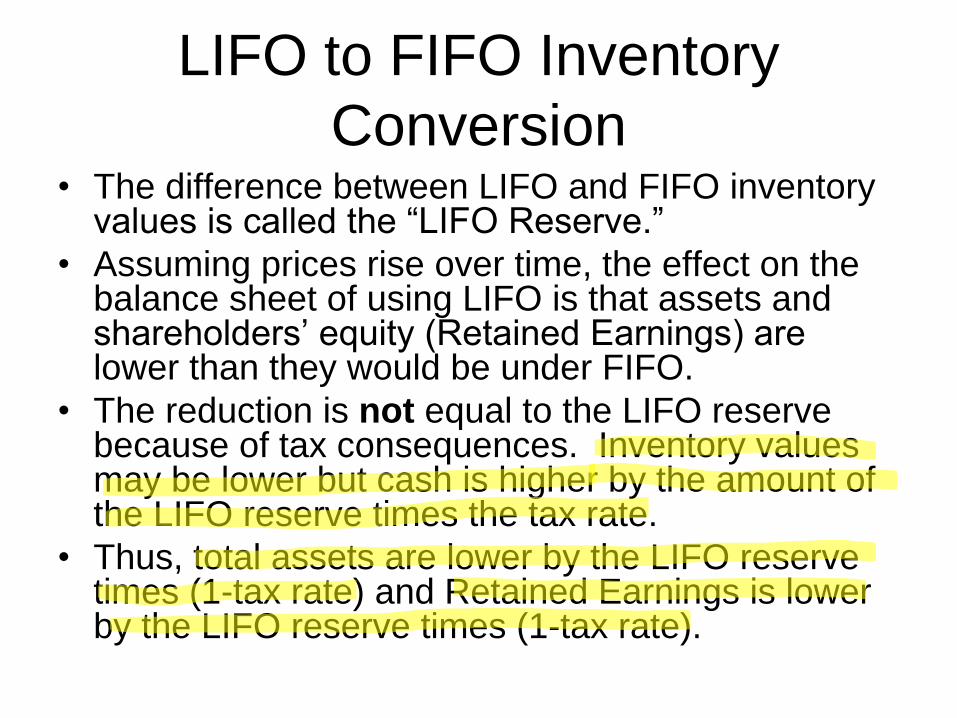

LIFO to FIFO Inventory

Conversion• The difference between LIFO and FIFO inventory

values is called the “LIFO Reserve.”

• Assuming prices rise over time, the effect on the balance sheet of using LIFO is that assets and shareholders’ equity (Retained Earnings) are lower than they would be under FIFO.

• The reduction is not equal to the LIFO reserve because of tax consequences. Inventory values may be lower but cash is higher by the amount of the LIFO reserve times the tax rate.

• Thus, total assets are lower by the LIFO reserve times (1-tax rate) and Retained Earnings is lower by the LIFO reserve times (1-tax rate).

FIFO V. LIFO

General Electric uses LIFO inventory cost

flow assumption, reporting inventories on its

2012 balance sheet of $15.4 billion and a

LIFO reserve of approximately $398 million.

What would be GE’s 2012 inventory balance

if it used FIFO assumption instead?

Why is disclosure of the LIFO reserve useful

to financial statement users?

International Perspective – Cost Flow

Assumptions

• Under IFRS the LIFO method is prohibited.

• This poses an important potential impediment to

the adoption of IFRS in the US. Most LIFO

users in the US have chosen LIFO because it

results in an income tax savings.

• DuPont, for example, has saved over $150

million in income taxes because it uses LIFO.

• A shift to IFRS could impose a huge and

immediate tax burden on LIFO users in the US.

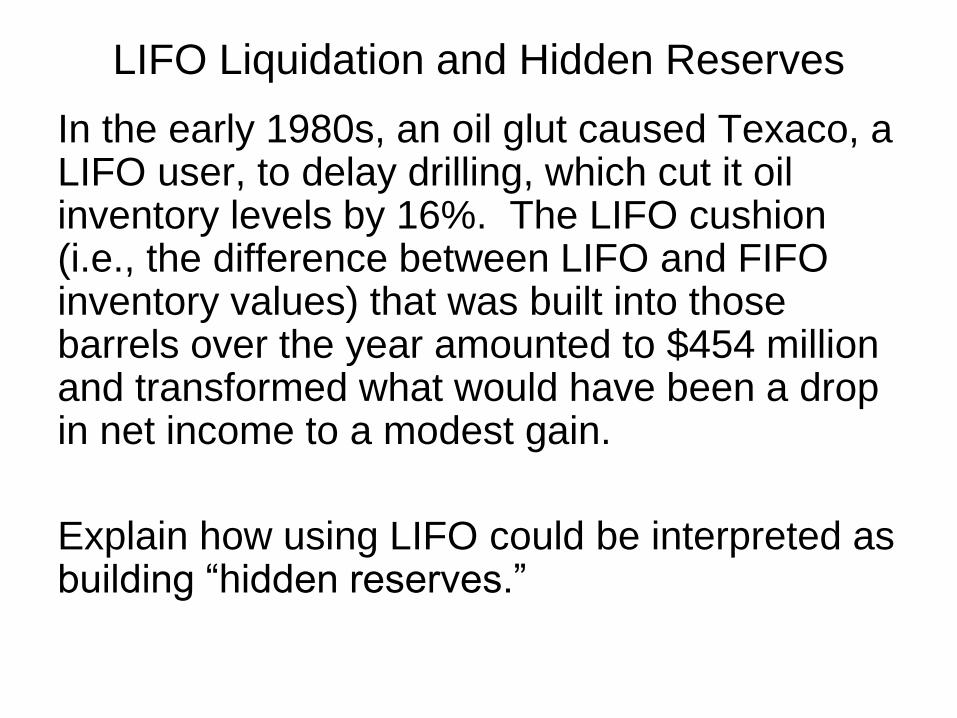

LIFO Liquidation and Hidden Reserves

In the early 1980s, an oil glut caused Texaco, a LIFO user, to delay drilling, which cut it oil inventory levels by 16%. The LIFO cushion (i.e., the difference between LIFO and FIFO inventory values) that was built into those barrels over the year amounted to $454 million and transformed what would have been a drop in net income to a modest gain.

Explain how using LIFO could be interpreted as building “hidden reserves.”

Disclosure

Method(s) used

If using LIFO, LIFO reserve information

(LIFO reserve=difference between LIFO inventory balances and balances if

either FIFO or current costs had been used)

Coca Cola Inventory

DisclosuresIncome Statement:

Balance Sheet:

Coca Cola Inventory Disclosures continued

Footnotes:

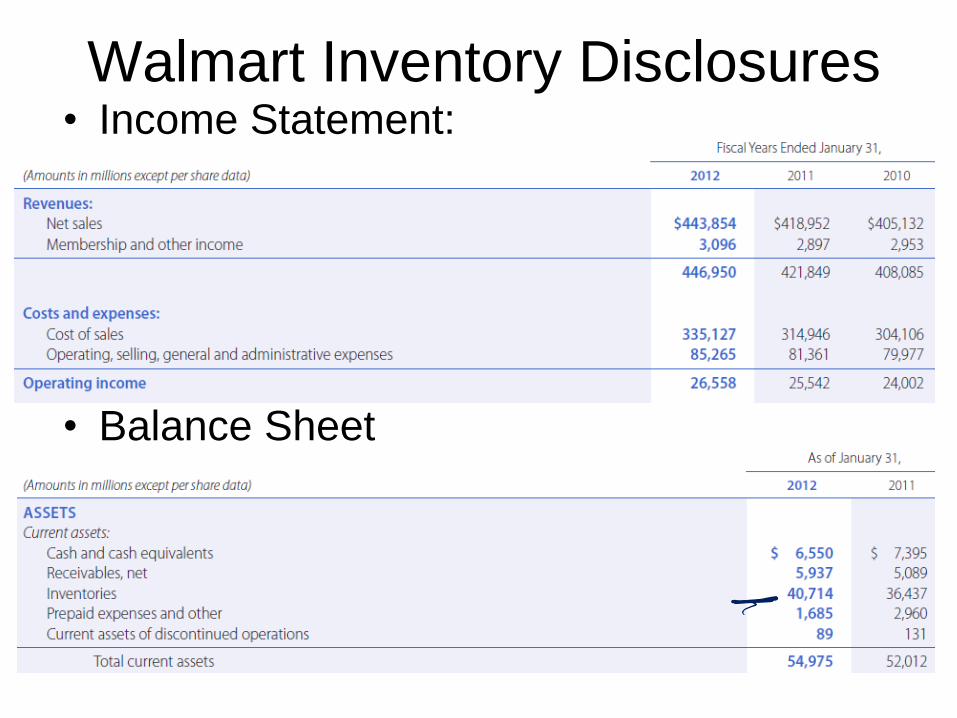

Walmart Inventory Disclosures • Income Statement:

• Balance Sheet

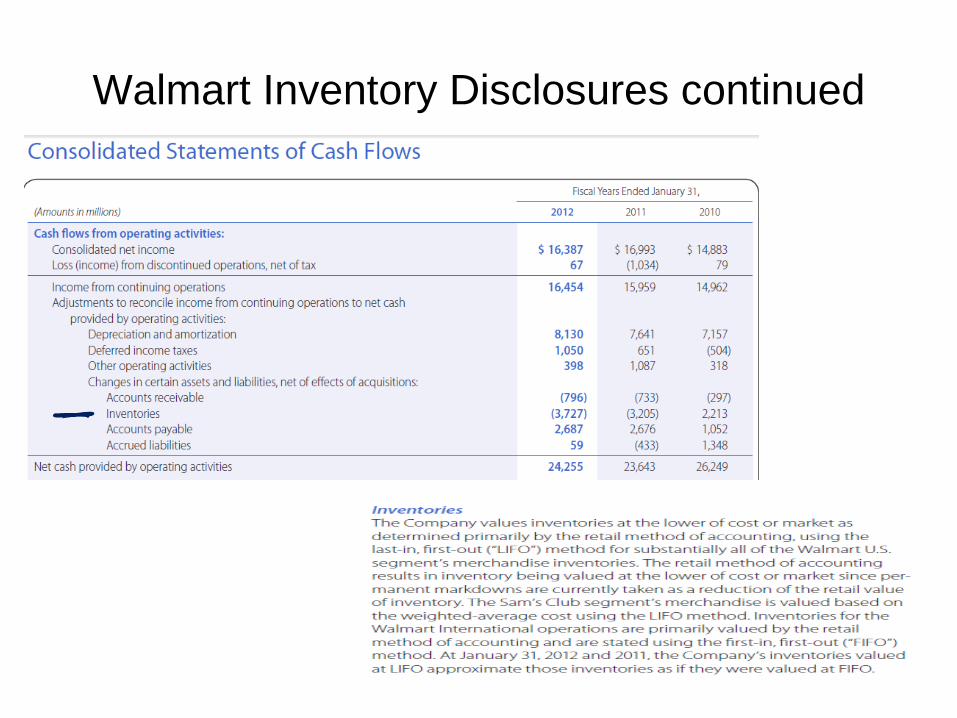

Walmart Inventory Disclosures continued

Footnotes:

Dollar-value LIFO

Lose verifiability

• BUT

Reduce cost of measurement

Dollar-value LIFO

Periodic

• Determine ending inventory (EI)

• Use EI to determine COGS

Ending Inventory

• Need ‘units’

Inventory in base-year dollars

• Need ‘cost’ per ‘unit’

Price index

P8-8 (Dollar-Value LIFO) Norman’s Televisions produces television sets in three categories: portable,

midsize, and flat screen. On January 1, 2014, Norman adopted dollar-value LIFO and decided to use a

single inventory pool. The company’s January 1 inventory consists of:

Category Quantity Cost per Unit Total Cost

Portable 6,000 $100 $ 600,000

Midsize 8,000 250 2,000,000

Flat screen 3,000 400 1,200,000

17,000 $3,800,000

During 2014, the company had the following purchases and sales:

Category No. Purchased Cost per Unit No. Sold Sales Price/Unit

Portable 15,000 $110 14,000 $150

Midsized 20,000 300 24,000 405

Flat screen 10,000 500 6,000 600

45,000 44,000

(a) Compute ending inventory, cost of goods sold, and gross profit.

P8-8 (Dollar-Value LIFO) Norman’s Televisions produces television sets in three categories: portable,

midsize, and flat screen. On January 1, 2014, Norman adopted dollar-value LIFO and decided to use a

single inventory pool. The company’s January 1 inventory consists of:

Category Quantity Cost per Unit Total Cost

Portable 6,000 $100 $ 600,000

Midsize 8,000 250 2,000,000

Flat screen 3,000 400 1,200,000

17,000 $3,800,000

During 2014, the company had the following purchases and sales:

Category No. Purchased Cost per Unit No. Sold Sales Price/Unit

Portable 15,000 $110 14,000 $150

Midsized 20,000 300 24,000 405

Flat screen 10,000 500 6,000 600

45,000 44,000

(b) Assume the company uses three inventory pools instead of one. Compute ending inventory, cost of

goods sold, and gross profit.