business and taxation guide - praxity guides/tax guide - austria.pdf · 10 business and taxation...

TRANSCRIPT

1 Business and Taxation Guide

Business and Taxation

Guide to

Austria

2 Business and Taxation Guide

Preface This guide was prepared by LeitnerLeitner in Austria in 2012. LeitnerLeitner has offices in: Vienna Linz Salzburg Sarajevo Zagreb Budapest Bucharest Bratislava Belgrade Ljubljana.

Austrian participating firm: LeitnerLeitner GmbH, Wirtschaftsprüfer und Steuerberater, Am Heumarkt 7, 1030 Vienna Tel.: 0043-1-7189890 and Ottensheimerstraße 32, 4040 Linz and Hellbrunner Straße 7 5020 Salzburg Partner – Andreas Damböck [email protected]

Director – Harald Galla - [email protected]

© Praxity 2011 This guide is intended as a general guide only and should not be acted upon without further advice.

3 Business and Taxation Guide

Contents Page 1. General information 6

1.1 Opportunities and possible obstacles for foreign investors 1.2 Area and population 1.3 Government and law 1.4 Key economic indicators 1.5 Currency

2. Regulation of foreign investment 8 3. Government incentives 9 4. Business organisations available to foreigners 10 5. Setting up and running business organisations 11

5.1 Process for incorporation 5.1.1 Requirements for a joint stock company (AG) 5.1.2 Requirements for a limited liability company (GmbH)

5.2 Business related taxes 5.2.1 Capital duty 5.2.2 Stamp duties 5.2.3 Customs duties 5.2.4 Other excise duties 5.2.5 Environmental taxes

5.2.6 Advertising duty 6. Corporate taxes and social charges 14

6.1 Corporations 6.1.1 Taxpayers and residence 6.1.2. Principles for determining the tax base

6.2. Non-resident corporations 6.3 Reorganisations 6.4 Holding structures

6.4.1. Domestic participation exemption 6.4.2. Participation exemption (dividend income from portfolio shareholdings) 6.4.3. International holding participations exemption (dividend income from qualified shareholdings and capital gains) 6.4.4. Anti-abuse rules 6.4.5. Interest deduction and thin capitalisation 6.4.6. Non-resident shareholders 6.4.7 Tax group

7. Personal taxation 21 7.1 Individual taxation

7.1.1 Rates 7.2. Sole entrepreneurs and partnerships

7.2.1. Unlimited tax liability and income 7.2.2. Principles for determining business income tax base

7.3. Non-resident sole entrepreneurs and partners of partnerships

4 Business and Taxation Guide

7.4. Employees and board members 7.4.1. Employees 7.4.2. Board Members 7.4.3. Municipal tax 7.4.4 Provisions for cross-border employments

8. Double taxation agreements 32 8.1 Withholding Tax – dividends

8.1.1 Resident corporate shareholders 8.1.2 Non-resident corporate shareholders

8.2. Withholding Tax - interest 9. Sales and use taxes 34

9.1. Value Added Tax (VAT) 9.1.1 Taxable persons 9.1.2 Taxable transactions 9.1.3 Place of supply 9.1.4 Taxable amount 9.1.5 Tax rates 9.1.6 Exemptions 9.1.7 Input VAT deduction 9.1.8 VAT liability 9.1.9 Tax assessment

10. Real estate and portfolio investment 39 10.1 Real estate investments

10.1.1. Individual resident investors 10.1.2 Corporate resident investors 10.1.3 Individual non-resident investors 10.1.4 Corporate non-resident investors 10.1.5 Real estate taxes 10.1.6 VAT on real estate 10.1.7 Real estate investment funds 10.1.8 Structuring of real estate investments

10.2. Portfolio/capital investments 10.2.1 Resident capital investors 10.2.2 Principles for determining the tax base 10.2.3 Tax rates and tax payments 10.2.4 Transitional rules 10.2.5 Non-resident capital investors 10.2.6 Withholding tax obligations 10.2.7 Tax treaty protection from Austrian withholding tax 10.2.8 Austrian banking secrecy 10.2.9 Investment funds

11. Trusts 55 11.1. Private foundations (PF)

11.1.1. Organisation of an Austrian private foundation 11.1.2. PF foundation tax 11.1.3 Income taxation of a PF 11.1.4 Taxation of beneficiaries of a PF 11.1.5 Dissolution of a PF

12. Practical information 58 12.1 Transport

5 Business and Taxation Guide

12.2 Language 12.3 Time relative to Greenwich Mean Time (GMT) 12.4 Business hours 12.5 Public holidays

6 Business and Taxation Guide

1. General information 1.1 Opportunities and possible obstacles for foreign investors Some of the key attractions for foreign investors in Austria include: Access to a market of approximately 8.4 million citizens Bordering the core European Union, and within a growing Eastern European market Investment incentives Skilled and competitive workforce Multilateral and bilateral conventions, significantly reducing or eliminating

export/import costs. Investing in Austria means investing in the economic core of the European Union. The single European market has the potential to reach 500 million consumers.

The following aspects may require careful consideration by a foreign investor and may, in some circumstances, be regarded as investment drawbacks or possible obstacles. 1.2 Area and population Austria lies in Central Europe. The territory of Austria covers approximately 84,000 square kilometres and is bordered by the Czech Republic and Germany to the north, Hungary and Slovakia to the east, Slovenia and Italy to the south, and Switzerland and Liechtenstein to the west. Austria’s terrain is highly mountainous due to the presence of the Alps. The nation’s population is approximately 8.4 million. 1.3 Government and law Austria, officially the Republic of Austria, is a federal republic, with nine federal states. Through the Federal Constitution of 1920 Austria became a federal, parliamentary, democratic republic. The Parliament of Austria comprises two chambers - the Nationalrat has 183 seats and is the dominant chamber in the formation of Austrian legislation. The head of state is the Federal President, who is directly elected by popular vote. The highest financial authority in Austria is the Ministry of Finance in Vienna. As well as the legislative and executive powers, the courts also hold state powers. The Constitutional Court (Verfassungsgerichtshof) has considerable influence on the political system by ruling on laws and ordinances not in compliance with the constitution. Since 1995, the European Court of Justice may overrule Austrian decisions in all matters defined in laws of the European Union. Austria also implements the decisions of the European Court of Human Rights, since the European Convention on Human Rights is part of the Austrian constitution.

7 Business and Taxation Guide

Since 1995, Austria has been a member of the European Union. 1.4 Key economic indicators

Austria is one of the richest countries in the world, with a nominal GDP per capita of $49,809 (2011 estimated). Austria has developed a high standard of living and in 2011 was ranked 19th in the world in the Human Development Index. In addition to a highly developed industry, international tourism is a large and critical part of the national economy, accounting for 9% of the country’s GDP. Trade with other EU countries accounts for almost 66% of Austrian imports and exports. Expanding trade and investment in the emerging markets of central and Eastern Europe is a major element of Austrian economic activity. Trade with these countries accounts for almost 14% of Austrian imports and exports. What’s more Austria has been a very active investor in Eastern Europe, with a diverse number of mergers and acquisitions valued at over €160 billion between 1995 and 2010. In addition, Austrian firms have sizable investments in and continue to move labour-intensive, low-tech production to Eastern European countries. (Source: http://en.wikipedia.org/wiki/Austria) 1.5 Currency The monetary unit used in Austria is the Euro (€). One Euro is divided into 100 cents. The International Standards Organization (ISO) currency code is EUR.

8 Business and Taxation Guide

2. Regulation of foreign investment In general, Austria is open to foreign investments. There is no limitation to foreign equity investment and the setting up of a company and establishing a business in Austria is relatively straightforward. In general, direct investment in Austria does not require approval from the Austrian government. However, the acquisition of residential or rural real estate may be restricted (depending of the region).

The eastward expansion of the European Union and the location of Austria in Central Europe provide an attractive hub for regional trade and a springboard for investors seeking opportunities to access the growing Eastern Europe market.

Austria is also a good location for research & development (R&D), with several attractive incentives available (please see section 3 and section 7.2.2.).

9 Business and Taxation Guide

3. Government incentives Tax incentives

An investors’ tax base may be reduced by applying an investment incentive/s. The most important currently available in Austria include:

Transfer of hidden reserves Invention and research allowance Education allowance General allowance for profits.

For detailed information, see 7.2.2 (tax incentives).

10 Business and Taxation Guide

4. Business organisations available to foreigners

Business activities in Austria are conducted by sole entrepreneurs (individuals) or by companies (legal entities). Among others, Austrian law recognises these companies commonly used by foreign investors and residents when establishing a business in Austria:

1. General partnership - Offene Gesellschaft (OG) 2. Limited partnership - Kommanditgesellschaft (KG) 3. Limited liabilitycompany - Gesellschaft mit beschränkter Haftung (GmbH) 4. Joint stockcompany - Aktiengesellschaft (AG)

Outlined in this table are several of the key legal requirements and the basic tax framework for a sole entrepreneur (sEnt) and the different company types:

Forms Liability of shareholders

Minimum capital (EUR)

Minimum number of founders and shareholders

Registration in commercial register

Tax treatment Tax rates

sEnt No shares, personal liability of the sole entrepreneur

--------- 1 Obligatory, if turnover > EUR 700,000 per year

Tax liability of sole entrepreneur

0-50%1

OG Unlimited --------- 2 Obligatory Transparent, tax liability of partners

0-50%2or 25%3

KG Unlimited (general partner) Limited (limited partner)

--------- 2

Obligatory Transparent, tax liability of partners

0-50%3

or 25%4

GmbH Limited 35,000 1 Obligatory Non-transparent, dividend taxation at the level of the shareholders

25%4

AG Limited 70,000 1 Obligatory Non-transparent, dividend taxation at the level of the shareholders

25%4

1Personal income tax rate. 2 The rate of 0 – 50% applies, insofar as the partners are individuals. 3 The rate of 25% applies, insofar as the partners are corporations. 4 Corporate incometax rate.

11 Business and Taxation Guide

5. Setting up and running business organisations

5.1 Process for incorporation The formalities for setting up a company in Austria are as follows:

Companies (GmbH and AG) and certain partnerships (OG and KG) must be registered at the commercial court in the jurisdictional area where the company is domiciled.

5.1.1 Requirements for joint stock company (AG)

The minimum capital requirement for a joint stock company (AG) is EUR 70,000, and the minimum face value per share is EUR 1 (no par value shares are permitted). There must be at least one founding shareholder. A AG may be founded immediately by paying in the entire shareholder capital.

A AG is obliged to have a supervisory board. The board must have at least three members (supervisory board members must not sit on the management board or be employees of the company.)A AG must also have a management board, with at least one managing director.

5.1.2 Requirements for limited liability company (GmbH)

The minimum capital requirement for a limited liability company (GmbH) is EUR 35,000 (only EUR 17,500 must be paid in cash). The minimum share value amount is EUR 70 and one share per shareholder. There must be at least one founding shareholder.

Only in certain circumstances is a GmbH obliged to have a supervisory board (e.g. when registered capital exceeds EUR 70,000 and the company has more than 50 shareholders). Otherwise a supervisory board is voluntary. A GmbH has to have at least one managing director (no residency or nationality requirements). 5.2 Business-related taxes 5.2.1 Capital duty

Contributions of capital to Austrian companies (i.e. the AG, GmbH and a specific type of a partnership - the GmbH & Co KG) by the shareholder trigger a capital tax of 1%. The tax base is the amount of the contribution, or alternatively the value of shares being issued in exchange for the contribution. The following transactions are subject to capital tax: The initial acquisition of shares upon formation of the company, or a subsequent

increase in its capital contributions Mandatory contributions by shareholders Voluntary contributions by shareholders that increase the value of their shares Contributions made by a non-resident company to its Austrian branch or permanent

establishment, and

12 Business and Taxation Guide

The transfer of seat or place of management to Austria, except for transfers by companies that are resident in another EU Member State.

’Indirect’ capital contributions, e.g. contributions made by a person/company other than the direct shareholder, are basically tax-free, subject to limitations set by Austrian case law and decisions of the European Court of Justice.

Capital contributions in the course of a reorganisation within the scope of the Reorganisation Tax Act (RTA) may also be exempt from capital duty. In addition, the Capital Transfer Tax Act provides for a capital duty exemption of the contribution of (i) all assets and liabilities or (ii) a business or (iii) a part of a business incorporated into an Austrian company in exchange for shares. 5.2.2 Stamp duties Stamp duties are levied on selected legal transactions that are concluded in written form, for example: Protocols Official documents Lease and rental agreements Guarantee and assignment agreements.

The rates vary between 0.8% and 2% of the underlying value of the transaction. In some cases the stamp duties are levied at flat amounts. As of1 January 2011 the provisions of the Stamp Duties Act, which levies a stamp duty on loan and credit agreements, has been abolished. Surety agreements closely linked to the loan and credit agreements according to Sec. 20 of the Stamp Duties Act are tax exempt. 5.2.3 Customs duties

In general, all goods crossing the Austrian border are subject to customs duties. As an EU Member State, Austria does not levy customs duties on the import of goods from other Member States. The customs tariffs for imports from countries outside of the EU are determined by the EU. In addition to the EU regulations, Austria has concluded various international agreements that provide for customs exemptions or preferential customs tariffs. 5.2.4 Other excise duties

Excise duties are levied on tobacco, alcoholic beverages and mineral oils. These duties are non-recurring and are payable by the seller, who passes these costs onto the consumer.

13 Business and Taxation Guide

5.2.5 Environmental taxes

Austrian law provides for various environmental taxes. Suppliers or users of energy are subject to electricity, natural gas or coal contributions. A residual waste contribution is levied on landfills of garbage (waste). 5.2.6 Advertising duty

Advertising duty is levied at a rate of 5% on the consideration for advertising activities performed in Austria, in addition to advertising broadcasts in Austria from another country. The advertising duty law defines advertising activities as advertising insertions in newspapers or journals, commercials on radio or TV and the leasing of billboards and banners.

14 Business and Taxation Guide

6. Corporate taxes and social charges 6.1 Corporations

6.1.1 Taxpayers and residence

Corporate entities, for instance the AG and the GmbH, are regarded as non-transparent under Austrian tax law. This means that the income derived by the corporation is taxable at the level of the corporation. Austrian tax law does not have a ’check-the-box regime’. A corporation with its statutory seat or place of management in Austria is subject to unlimited corporate income tax liability, which provides for taxation of income on a worldwide basis (subject to applicable tax treaties).

6.1.2 Principles for determining the tax base

Income of a GmbH or an AG must be regarded as ’business income’ in any event, regardless of the nature of the income. The tax base is determined using the net equity comparison method, according to Sec. 5 of the Austrian Income Tax Act (ITA). Special tax provisions apply to holding structures (participation exemption).

Carry-forward of losses

Basically, losses of corporations, for tax purposes, are treated similar to losses of sole entrepreneurs and partnerships. Also, corporate income tax law provides for loss trafficking rules – this means the loss carry-forward may no longer be applied when the company has lost its identity within the meaning of Sec. 8 para. 4 CITA. This is to be assumed if the ownership, as well as the organisational and business structure, has substantially changed. Apart from that, the Austrian Reorganization Tax Act (RTA) outlines further loss-trafficking rules that are applicable to certain types of reorganisations (e.g. mergers).

Tax rates and tax payments

Any profit derived by a corporation is subject to corporate income tax at a flat rate of 25%. This is regardless of whether the profit is distributed to shareholders or retained.

A corporation has to make quarterly pre-payments based upon the taxable income of the preceding year, and must file annual tax returns with the competent tax office. The tax office determines the final tax liability for the year by issuing a yearly tax assessment notice. The pre-payment is credited against the final corporate income tax liability. Resident companies are subject to a minimum corporate income tax, even in the case of losses (EUR 1,750 for a GmbH and EUR 3,500 for an AG). The minimum tax is credited against the future tax liability.

15 Business and Taxation Guide

6.2 Non-resident corporations

A non-resident corporation (i.e. with neither the place of management or legal seat in Austria), which is comparable to an Austrian corporation, is subject to limited corporate tax liability if it conducts business in Austria through an Austrian permanent establishment or an Austrian partnership. In this case, tax liability is limited to the income attributed to that permanent establishment (PE) or partnership.

In addition, income derived from Austrian real estate is subject to limited tax liability if it belongs to the business of a foreign corporation.

The corporate income tax rate applied to non-resident corporations is 25%.

6.3 Reorganisations

Under general income tax principles, a reorganisation of companies normally constitutes a taxable event and triggers the realisation of hidden reserves of the assets transferred during the reorganisation. However, the Reorganization Tax Act (RTA) - which is based on the EC Merger Directive (90/434/EEC) - provides for a special tax regime applicable to the following types of reorganisations:

Mergers Conversions Contributions of assets Formation of partnerships Divisions of partnerships Demerger of corporations.

The RTA provides for the following tax treatment, subject to certain conditions:

No liquidation taxation due to the reorganisation (neither on the level of the company/partnership or on the level of the shareholder/partner)

Tax-neutral transfer of assets Transfer of loss carry-forward to the receiving entity Beneficial rules to the tax base for real estate transfer tax purposes Exemption from capital tax Exemption from value added tax.

The RTA allows reorganisations with retroactive effect (basically within a nine-month period), as well as multiple reorganisations, with the same effective date.

As from 2011 binding rulings are available in reorganisation issues (costs amounting to between EUR 1,500 and EUR 20,000, depending on the turnover of the requesting taxpayer).

16 Business and Taxation Guide

6.4 Holding Structures

6.4.1 Domestic participation exemption Under the domestic participation exemption regime, any income (e.g. dividend distributions) derived by a resident GmbH or AG from a participation in another Austrian corporation is exempt from corporate income tax. This exemption is regardless of the capital ownership percentage and the holding period. However, the domestic participation exemption does not apply to capital gains of a GmbH or AG resulting from the alienation or liquidation of the domestic participation in another Austrian corporation.

6.4.2 Participation exemption (dividend income from portfolio shareholdings) Dividend income (but not capital gains) derived by a resident GmbH or AG from a participation of less than 10% in the capital of a foreign corporation is exempt, providing the following conditions apply: The subsidiary has a legal form listed in the Annex of the EC Parent-Subsidiary

Directive, or The subsidiary is situated in a third country, has a legal form comparable to domestic

corporations and the residence state of the subsidiary has concluded an agreement providing for a comprehensive administrative assistance.

No minimum shareholding or holding period has to be met. Under certain conditions, Austrian tax law provides for a switch–over from the tax exemption to the credit system. 6.4.3 International holding participations exemption (dividend income from qualified shareholdings and capital gains) In addition, tax law provides for a participation exemption regime for ’international holding participations’ requiring the fulfilment of the following conditions:

Direct or indirect (e.g. via an intermediate transparent partnership) equity

participation of at least 10% in a foreign corporation for a minimum uninterrupted period of one year, and

Comparability of the legal form of the foreign subsidiary corporation to Austrian corporations, or listing of the legal form in the Annex to the EC Parent-Subsidiary Directive.

The international participation exemption is also granted to Austrian PEs of companies resident in another EU Member State, providing these companies fulfil the requirements listed above.

17 Business and Taxation Guide

If the requirements are met, dividends from international holding participations are, in general, tax exempt. Dividend income from subsidiaries before the expiration of the one-year holding period are tax exempt under the rules set out in section6.4.2. This tax exemption also applies to capital gains from international holding participations. Capital losses (except losses in the event of insolvency or liquidation) and other write-downs of the participation are basically non-deductible. The parent company may, however, exercise an option to have capital gains and losses from the participation to be treated as taxable or tax-deductible. The option must be exercised in the year of acquisition and is binding on any group company holding or acquiring that participation. The tax exemption of dividend income and capital gains does not apply in cases of suspected tax avoidance or abuse of law, which is assumed in certain situations (see section 6.4.4). 6.4.4 Anti-abuse rules Switch-over clause regarding portfolio shareholdings Dividend income from portfolio shareholdings is not tax exempt if the conditions set out below are met. This means that the dividend income is taxable at the level of the Austrian parent company (corporate income tax 25%). However, any foreign corporate (and withholding) tax may be credited against the Austrian tax burden of the Austrian parent company. In practice, determining the creditable foreign tax can be quite complex.

Switch-over conditions:

o the subsidiary is not subject to a tax in the foreign country, which is comparable to the Austrian corporate income tax, or

o the level of taxation of the profits of the foreign subsidiary is not comparable to Austrian standards - this is fulfilled if the applicable foreign tax rate is lower by more than 10 percentage points than the Austrian corporate income tax rate (i.e. below 15% corporate income tax rate), or

o the subsidiary is exempt from taxation in the foreign country.

Switch-over clause regarding international holding participations In terms of international holding participations, Austrian tax law provides for a special anti-abuse rule, with conditions varying from the anti-abuse rule applicable to portfolio shareholdings. The anti-abuse rule also provides for a switch-over from the tax exemption to the credit system, i.e. the income derived from the participation (dividends and capital gains) will be fully taxable at the level of the Austrian parent company (corporate income tax 25%). Any foreign corporate (and withholding) tax may be credited against the Austrian tax burden of the Austrian parent company.

The anti-abuse provisions apply in cases of suspected tax avoidance or abuse of law. Tax avoidance or abuse of law is assumed if two tests, as described below, are cumulatively fulfilled:

o ’Passive-business test’: The business of the foreign subsidiary is focused on deriving (directly or indirectly) ’passive’ income, which covers interest income, royalty/lease income and capital gains on portfolio-investments.

18 Business and Taxation Guide

Rental income from immovable property, dividend income or capital gains resulting from qualified shareholdings that meet the criteria of an ’international holding participation’ are not regarded as passive income. This test is met if the majority of the company’s assets (or the company’s staff) is used for deriving passive income and the company’s income predominantly results from ’passive’ sources

o ’Low-taxation test’: The income of the foreign subsidiary is not liable to taxation comparable to Austrian tax law, i.e. the foreign average tax burden is not more than 15% of the tax base determined under Austrian tax law.

Exclusion for dividends from hybrid shareholdings As of2011, dividend income received from portfolio shareholdings and from international holding participations is not exempt from corporate income tax if the dividend is deductible as a business expense at the level of the foreign subsidiary. This could apply when a participation in a foreign company is characterised from an Austrian perspective as equity and from the foreign tax law perspective as debt (leading to a tax deduction at the level of the foreign subsidiary, as the dividends are regarded as deductible interest), i.e. a hybrid shareholding.

Investment fund legislation These participation exemption regimes do not apply if the foreign subsidiary qualifies as a foreign investment fund under the Investment Fund Act (IFA). A foreign investment fund is deemed to exist if a foreign entity by law, statute or on the basis of actual practice, structures its investments by applying risk diversification rules.

If the foreign subsidiary qualifies as an investment fund, the Austrian company is taxed on distributed and retained earnings of the foreign subsidiary, with the latter calculated on a lump-sum basis. The amount of retained earnings is assumed to be 90% of the difference between the last and the first redemption price fixed in the calendar year, or, in any case, 10% of the last redemption price fixed in the calendar year.

6.4.5 Interest deduction and thin capitalisation

Interest deduction Interest on the debt-financing of the acquisition of a participation in a corporation (resident or non-resident) is usually tax deductible, regardless of whether the participation exemption provides for a tax exemption on income from the acquired participation. However, interest on the debt financing is not tax deductible: When the participation is not part of the business assets of the shareholder When the participation is acquired directly or indirectly from

o a group company or o a shareholder exerting a dominant influence (intra-group acquisition)

When there’s a capital or contribution increase (in cash or in kind) to a company, in which the shareholding was acquired via an intra-group acquisition.

19 Business and Taxation Guide

Thin capitalisation Specific rules on thin capitalisation do not exist in Austria. The Austrian Administrative Court has established various principles to determine which conditions debt financing is not recognised for tax purposes. For instance, if the equity is inadequate, a loan may be (partly) regarded as hidden equity. However, there are no defined debt-equity ratios to comply with. Hidden equity may also be assumed if the loan agreement is not in line with the arm's length principle. Interest paid on loans regarded as hidden equity will be treated as a constructive dividend and may not be deducted from the taxable income.

6.4.6 Non-resident shareholders Interest and royalty payments to non-residents Interest income of a non-resident taxpayer (corporation and individuals) is not subject to tax in Austria unless the underlying loan is secured directly or indirectly by immovable property located in Austria. However, in the latter case tax treaties usually protect from Austrian taxation if the treaty contains an OECD Model-type of provision on interest. If the interest income is to be attributed to PE of the non-resident recipient, that income is taxable as business income in Austria. Royalties paid to a non-resident recipient are usually subject to a 20% withholding tax under Austrian law. Tax treaties, if applicable, usually reduce the withholding tax or even exempt the income from Austrian taxation. Interest and royalties that are paid to associated companies or to their PEs located in a Member State, other than Austria, are exempt from the withholding tax under Sec. 99a ITA, which has codified the EC Interest and Royalty Directive in Austrian law. The exemption is subject to the conditions that: The recipient qualifies as beneficial owner of such payments The parent company has a form listed in the Annex to the Interest and Royalty

Directive The parent company is subject to regular income tax in its residence state

(confirmation issued by the competent tax authority is necessary). A company is deemed to be associated if it directly holds at least 25% capital of the subsidiary for an uninterrupted period of one year. Also, the exemption requires a confirmation from the recipient that it qualifies as beneficial owner of the payments and that it fulfils the participation requirements. For tax avoidance, abuse of law and royalties exceeding the arm’s length amount, these are re-characterised as constructive dividends and are subject to withholding tax. Capital gains Capital gains of a non-resident corporation (or individual) resulting from the alienation of a participation in an Austrian corporation (such as a GmbH or a AG) are taxable in Austria if the shareholding is at least 1% of the capital of the GmbH or AG at any time during the five preceding years. Tax treaties usually prohibit Austria from taxing if they contain an OECD Model-type of capital gain provision.

20 Business and Taxation Guide

If the capital gain was realised by an Austrian PE of anon-resident seller, the gain is treated as business income of the PE and is subject to tax under the general rules.

6.4.7 Tax group If an Austrian corporation, or a PE of an EU corporation registered in Austria, holds a (direct or indirect) participation of more than 50% of the capital and the majority of the voting rights in a domestic or foreign corporation, a tax group may be established. The minimum holding requirement can also be met together with other companies, providing the shareholding of one corporation amounts to at least 40% and the shareholding of the other corporation’s amount to at least 15%. A tax group has the effect that all profits and losses of domestic group members (subsidiaries) will be allocated for tax purposes to the group leader. The group may also include foreign subsidiaries. Only losses of foreign group members may be deducted from the taxable income of the group. Deductions must be done in proportion to the amount of the direct shareholding of the group in the foreign entity. However, such losses are recaptured and taxed in Austria in subsequent years if, and to the extent, they can be offset against profits of the foreign entity under its domestic tax regime, or if the foreign entity drops out of the group (e.g. due to sale of the participation or if the foreign company is liquidated). Profits of foreign group members must not be included in the tax group. A write-down of participations in the share capital of group members is not deductible for tax purposes. A tax-deductible depreciation of goodwill over 15 years is applied to acquisitions of participations in domestic corporations running an operating business. The depreciation is limited to 50% of the purchase price of the shares - the acquisition costs of the participation are reduced accordingly. Providing that all requirements are fulfilled, the group leader may opt for group taxation simply by filing an application form with the tax authorities (subject to certain time constraints). The tax authorities approve the tax group by official notice. The tax group has to remain in existence for at least three years. If the tax group is terminated earlier, all benefits from the group taxation will be lost and each member of the group will be taxed as a separate entity with retroactive effect. As of2011, binding rulings are available in group taxation issues (costs amounting between EUR 1,500 and EUR 20,000, depending on the requesting taxpayer’s turnover).

21 Business and Taxation Guide

7. Personal taxation 7.1 Individual taxation Residents are liable for income tax on their worldwide income (i.e. income derived in Austria and abroad). Non-residents are liable only to certain Austrian-sources income. An individual is tax resident in Austria, if his/her home is in Austria or if he/she has an Austrian habitual place of abode for more than six months in a calendar year. The Austrian Income Tax Act distinguishes between seven categories of income: Income from agriculture and forestry Income from independent professional services and free professions Business income Income from employment Capital income Rental income Other income.

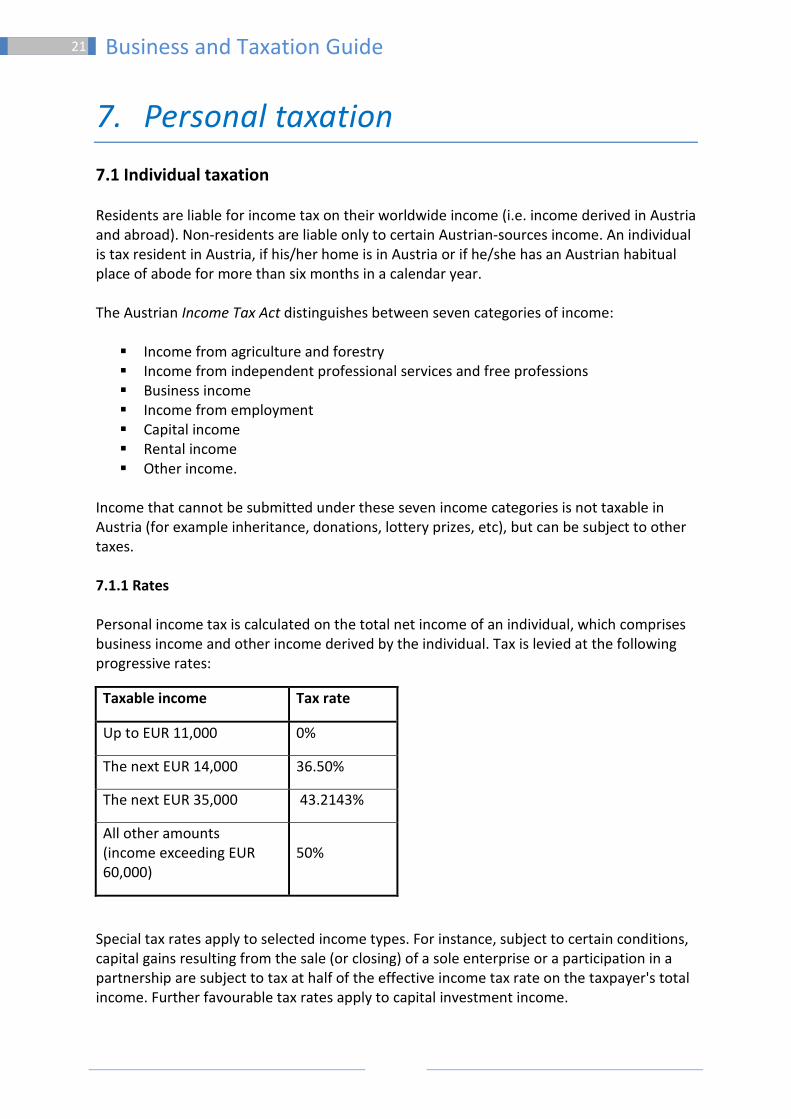

Income that cannot be submitted under these seven income categories is not taxable in Austria (for example inheritance, donations, lottery prizes, etc), but can be subject to other taxes. 7.1.1 Rates Personal income tax is calculated on the total net income of an individual, which comprises business income and other income derived by the individual. Tax is levied at the following progressive rates:

Taxable income Tax rate

Up to EUR 11,000 0%

The next EUR 14,000 36.50%

The next EUR 35,000 43.2143%

All other amounts (income exceeding EUR 60,000)

50%

Special tax rates apply to selected income types. For instance, subject to certain conditions, capital gains resulting from the sale (or closing) of a sole enterprise or a participation in a partnership are subject to tax at half of the effective income tax rate on the taxpayer's total income. Further favourable tax rates apply to capital investment income.

22 Business and Taxation Guide

Each taxpayer must declare his/her income in an annual tax return, which must be filed with the competent tax office. The tax office issues assessment notices for each tax year, whereby the annual tax liability is determined. During the year, the taxpayer has to make quarterly pre-payments based on the taxable income of the preceding year.

7.2 Sole entrepreneurs and partnerships

7.2.1 Unlimited tax liability and income

A sole entrepreneur domiciled or with a habitual place of abode in Austria is subject to unlimited personal income tax (i.e. resident taxation) on worldwide income (subject to tax treaties). This means, income from business activities conducted in Austria is subject to personal tax. An individual is deemed to domicile in Austria when occupying a house or an apartment (also vacation houses) which indicates a permanent stay. An individual has a habitual place of abode when physically present in circumstances indicating a permanent presence. For non-resident individuals, see section 7.3.

Taxpayer’s with a secondary residence, as defined by Sec. 26 (1) Federal Fiscal Code in Austria, is subject to unlimited tax liability. Consequently, the taxpayer is generally taxed in Austria on his worldwide income (subject to applicable tax treaties). However, if the conditions stipulated in the ‘Secondary Residence Regulation (Federal Law Gazette II 2003/528)’ are met, it is possible that the taxpayer will only be subject to limited tax liability for income tax purposes. In this case, only Austrian-source income is taxed in Austria.

The Secondary Residence Regulation provides for the following conditions:

The centre of vital interests for the taxpayer has to be abroad for more than five years

The domestic residence may not be used for more than 70 days in a calendar year - a record must be kept of the actual days spent in the domestic residence

The domestic residence must not be the residence of a spouse/partner who is subject to unlimited tax liability in Austria.

Partnerships are transparent entities for tax purposes. This means that the income of the partnership is not attributed to the partnership (OG or KG) but to the partners directly. Thus, the partners, if individuals, are subject to unlimited personal income tax liability on income derived from the partnership. If the partner of a partnership is a corporation (GmbH or AG), the income share of that partner is subject to corporate income tax liability. In this case the rules for corporations are applicable (see section 6.1).

Sole entrepreneurs and individual partners of an OG or KG running an operating business in Austria may derive income from:

Agriculture and forestry Independent (professional) services Business or trade.

23 Business and Taxation Guide

Income from business or trade (business income) is, in practice, the most common, so this category is used as subsequent examples. Please note that individuals, as well as partnerships, can also derive income from non-operating activities like real estate or capital investments.

7.2.2 Principles for determining business income tax base To determine the business income tax base, the same principles apply to sole entrepreneurs and partnerships. Austrian tax law provides for four different methods: Net equity comparison method under Sec. 5 ITA Sole entrepreneurs and partnerships deriving business income must apply the net equity comparison method if they are obliged to keep books (i.e. realising a turnover of more than EUR 700,000). With this method, ’profit’ is defined as the difference between the net equity at the end and at the beginning of the business year. The valuation and determination of net equity is based on the Austrian generally accepted accounting principles (GAAP) codified in the Commercial Code. In some cases, Austrian tax laws provide for adjustments of the valuation under Austrian GAAP.

Net equity comparison method under Sec. 4 (1) ITA This method only applies in rare cases, specifically in the area of agriculture and forestry. An essential difference between this method and the net equity comparison method under is gains or losses from the sale of land are disregarded when determining the taxable base.

Cash method The cash method applies to sole entrepreneurs and partnerships deriving a turnover of less than EUR 700,000. This method also applies to income from professional services. Average rates method For selected areas of business the tax base may be determined using a special average rates method.

In practice, the net equity comparison method under Sec. 5 ITA mostly applies, focused on below. The starting point is the Austrian GAAP, which are adjusted in some cases by special tax provisions for the purpose of determining the tax base. In terms of the valuation of assets and debts, the following principles apply:

Valuation of assets and debts

Depreciable fixed assets are reported in the accounts as acquisition or production costs, less depreciation. If the going-concern value is below the acquisition or production costs, the lower value may be recorded.

Non-depreciable assets and current assets must be reported at acquisition or production costs. If the going-concern value is below the acquisition or production costs, the lower value can be recorded.

Receivables are valued at acquisition costs (nominal value) or at market value, whichever is lower. Whereby the settlement of the receivable is doubtful, the

24 Business and Taxation Guide

receivables have to be written down accordingly. Lump-sum depreciation is not allowed for tax purposes.

Liabilities are valued at redemption value.

Withdrawals are valued at their going-concern value at the time of withdrawal.

Contributions are valued at their going-concern value at the time of the transfer.

Depreciation The acquisition or production costs of depreciable fixed assets are deducted proportionally over the useful life of the asset. Amortization starts when the asset is used first. If the asset is used for more than six months in the financial year, depreciation for 12 months will be allowed. Otherwise, depreciation is limited to 50% of the yearly depreciation amount. The useful life of fixed assets is determined as the total period of use. The taxpayer must prove the useful life (i.e. economic life) of each asset. Subject to alternative evidence of useful life, these provisions apply:

o 33.3 years minimum (i.e. depreciation of up to 3% per year) for buildings (except land) serving directly the purpose of the business; 50 years minimum (i.e. up to 2% per year) for other buildings;

o eight years (i.e. depreciation of 12.5% per year) for cars o 15 years for acquired goodwill (i.e. deprecation of 6.66% per year).

If the acquisition or production costs of a single asset do not exceed EUR 400 the total costs may be deducted in the year of acquisition or production.

In addition to ordinary depreciation, depreciation for extraordinary technical or economic wear and tear is allowed

Provisions For an anticipated claim, not yet certain in respect of its reason or its amount, a provision has to be entered in the books using general accounting principles. For tax purposes, only the following types of provisions may reduce the tax base:

o future severance payments o current pensions and future pension payments o other uncertain liabilities (e.g. warranty claims, legal charges) o potential losses from pending business transactions.

Provisions for uncertain liabilities and for potential losses from pending business transactions are only tax effective at 80% of their value if they are long term (more than 12 months).

Expenses

Basically, all expenses caused by a trade or business are tax deductible. However, the following restrictions apply:

o no deduction of expenses relating to the taxpayer’s personal life, income taxes, real estate transfer taxes and registration duties, if these resulted from

25 Business and Taxation Guide

the donation of real estate, or of the value added tax for self-supply and withdrawal of goods and services for private use

o expenses for social representation (includes entertainment expenditures and business meals); these expenses are tax deductible to 50% if the taxpayer can prove that the expenses were predominantly caused by business reasons

o grant or receipt of contributions in cash, or in kind, which is a punishable offence under fiscal criminal law and subject to company fines.

Tax incentives The tax base may only be affected by the application of investment incentives, the most important being:

o Transfer of hidden reserves Sole entrepreneurs and partnerships (partners are individuals) may transfer hidden reserves realised from the sale of an asset to a newly acquired asset, providing the asset sold has belonged to the enterprise for at least seven years (15 years for certain buildings and land).

o Invention and research expenditures Generally deductible for tax purposes. In addition, it is possible to claim a research premium of 10 %for research expenditures (credited to taxpayer).

o Education expenditures An allowance of 20% is granted for expenses connected to internal and external education. Alternatively, a premium of 6% may be claimed.

o General allowance for profits From the beginning of 2010, a general allowance for profits for all single entrepreneurs and partnerships was introduced. From 2010, a taxpayer may claim an allowance if acquiring or producing a depreciable tangible asset or securities to the lower of 13% of the profit or the maximum of EUR 100,000. An investment in assets or securities is not required if the profits do not exceed EUR 30,000.

Carry-forward of losses Generally, losses suffered in any of the ‘business income’ categories may be deducted in the same tax year from:

o profits of the same ’business income’ category o profits of any other ‘business income’ category o other positive income, subject to certain restrictions.

Losses from business activities that could not be deducted from other positive income in the same year may be carried forward without time limit, providing the loss was calculated using GAAP. If the tax base was determined on a cash basis, losses may be carried forward for a period of three years.

Loss deduction is limited to 75% of the positive yearly income of each year. If the unused losses are higher, the remaining losses may be carried forward.

26 Business and Taxation Guide

7.3 Non-resident sole entrepreneurs and partners of partnerships An individual with neither a domicile nor habitual place of abode in Austria (non-resident) is subject to limited tax liability. Tax liability is limited to Austrian-sourced income, as listed in Sec. 98 ITA. A non-resident individual may conduct business in Austria as sole entrepreneur through an Austrian PE or as a partner of an Austrian partnership (an Austrian partnership basically constitutes a PE of the partners to the partnership). Non-resident sole entrepreneurs and partners to Austrian partnerships are taxed accordingly on income from:

Domestic agriculture or forestry Independent professional services performed or utilised in Austria Other trade or business

o derived through an Austrian PE or o derived through a permanent agent in Austria or o resulting from Austrian real estate, if it belongs to a foreign trade or business.

Income derived from these activities is subject to income tax at the same rates applied to resident taxpayers. During an annual tax assessment, the income of non-resident individuals (and partners in Austrian partnerships) is increased by a deemed additional amount of EUR 9,000. In certain conditions, citizens of an EU Member State who are non-residents by Austrian tax law may also apply for treatment as a resident (Schumacker doctrine).

Non-resident individuals with Austrian-sourced business income must file tax returns, unless their income is levied by way of withholding (Sec. 99 ITA). A non-resident may opt for a regular assessment procedure by filing a tax return if the assessed tax would be lower than the tax withheld. The special withholding tax of 20% is levied on the gross amount on the following income:

Income from activities performed or utilised in Austria, including activities as author, lecturer, artist, architect, sportsperson, irrespective of to whom the salary for the performed activity is paid

Profit shares of an Austrian partnership if the partnership is owned by a foreign partnership, unless the Austrian partnership notifies (or the Austrian tax authorities otherwise get notice) who is the ultimate (individual or corporate) shareholder of the foreign partnership

Income from the licensing of intellectual property rights (Sec. 28 ITA) Remunerations for supervisory board members; Income from commercial and technical consultancy in Austria and income from the

supply of workers Specific income from real estate investment funds (private placements).

For other incomes, tax is levied by way of assessment.

For more details about income derived from employment or income from capital investments, see section 7.4.

27 Business and Taxation Guide

7.4 Employees and board members

7.4.1 Employees Resident employees

An employee is deemed resident in Austria if he/she has a domicile or habitual place of abode in Austria – occupying a house or apartment that indicates a permanent stay.

Employment income

General employment relationships

For purposes of the ITA, an employee receiving income under an employment contract is deemed to derive employment income. Employment income includes all remuneration, in cash or in kind, derived by an employed person and paid by the employer or by a third party.

Principles for determining the tax base

In general, employment income is calculated as the excess of taxable receipts over deductible expenses in respect of an employment. Cash expenditures reimbursed by the employer and certain payments rendered by the employer for various purposes, e.g. travel expenses, relocation, education and training, pension funds, etc. do not constitute taxable employment income.

Deductible expenses reduce the taxable employment income if incurred in earning, protecting or preserving the employment income and if they are not reimbursed by the employer. Deductible employment-related expenses include the employee's compulsory social security contributions, commuting expenses, technical literature, travel expenses, expenses for education and training borne by the employee, etc.

Tax rate, assessment and social security contributions

To calculate the income tax rate, see I.B.1.4. (0% - 50% income tax rate). It’s also important to note that in Austria an annual salary is not paid in 12 but, generally in 14 equal instalments - the 13th and 14th salary payments (holiday and Christmas pay) are taxed at a beneficial tax rate of 6%, instead of the progressive income tax rate (which may be up to 50%).

Attention should be paid to the fact that the ITA provides for the withholding of wage tax on the employment gross income at the time of the payment. Employers are obliged to withhold wage tax from gross salaries paid to their employees and to transfer the wage tax to the competent tax office. Wage tax laws and rules do not apply to salaries paid by an employer without an Austrian PE.

Wage tax is considered to be a pre-payment on the employee’s final income tax and is credited against its assessed income tax liability. If an individual only generates income under a single employment contract, no obligation exists to file an income tax return, but the employee may submit an application for an assessment after the end of the tax year if a repayment is expected. During a tax assessment, certain expenses

28 Business and Taxation Guide

and allowances can be considered that the employer was not allowed to consider for the purpose of the correct wage tax calculation. These include:

o deductible expenses o special allowances (e.g. premiums for personal insurance, expenses for home

construction and improvement, fees for tax advice, etc.) o extraordinary expenses (e.g. expenses to compensate shock losses, cost

related to the education of children away from home, etc.).

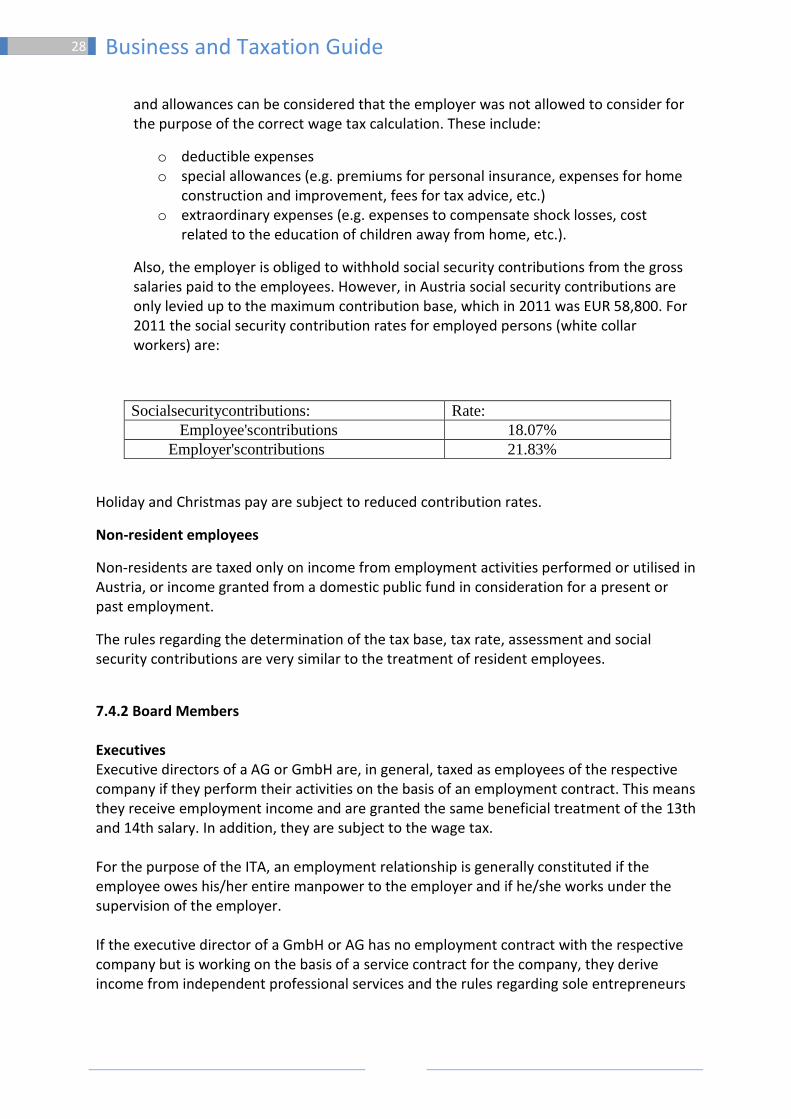

Also, the employer is obliged to withhold social security contributions from the gross salaries paid to the employees. However, in Austria social security contributions are only levied up to the maximum contribution base, which in 2011 was EUR 58,800. For 2011 the social security contribution rates for employed persons (white collar workers) are:

Socialsecuritycontributions: Rate: Employee'scontributions 18.07%

Employer'scontributions 21.83%

Holiday and Christmas pay are subject to reduced contribution rates.

Non-resident employees

Non-residents are taxed only on income from employment activities performed or utilised in Austria, or income granted from a domestic public fund in consideration for a present or past employment.

The rules regarding the determination of the tax base, tax rate, assessment and social security contributions are very similar to the treatment of resident employees.

7.4.2 Board Members Executives Executive directors of a AG or GmbH are, in general, taxed as employees of the respective company if they perform their activities on the basis of an employment contract. This means they receive employment income and are granted the same beneficial treatment of the 13th and 14th salary. In addition, they are subject to the wage tax. For the purpose of the ITA, an employment relationship is generally constituted if the employee owes his/her entire manpower to the employer and if he/she works under the supervision of the employer. If the executive director of a GmbH or AG has no employment contract with the respective company but is working on the basis of a service contract for the company, they derive income from independent professional services and the rules regarding sole entrepreneurs

29 Business and Taxation Guide

and business profits apply. In this situation, the beneficial treatment of the 13th and 14th salary payment is not granted and the director is not subject to wage tax.

Also, the ITA provides for special rules for directors being only employees of a GmbH or AG, as well as for directors additionally holding a participation of more than 25% in the same GmbH or AG (substantial shareholder and director). If the executive director of a GmbH or AG is a substantial shareholder of the GmbH or AG, remuneration is treated as ‘income from (other) professional services’ and the above-mentioned rules for directors working on a service contract basis would apply. The salaries should, in these cases, meet an arm's length standard; otherwise the income may be treated as a hidden distribution.

Non-executives

Usually, non-executive resident directors of a AG or GmbH are taxed in the same way as executive directors, working on the basis of a service contract or as a ‘substantial shareholder and director’. This means that they receive income from independent professional services and the rules regarding sole entrepreneurs and business profits are applied.

Non-resident board members

Non-resident executive directors are taxed only on income from employment activities performed or utilised in Austria if they have an employment relationship with the respective company. Otherwise, they are taxed on income from independent (professional) services performed or utilised in Austria. A non-resident ’substantial shareholder and director’ is taxed on income from independent services if the services were performed or utilised in Austria. The rules to determine the tax base, tax rate and assessment are very similar to the treatment of resident directors.

Non-resident non-executive directors are taxed on income from independent services if the services were performed or utilised in Austria. They are subject to a withholding tax of 20%, but they may opt for an assessment procedure.

7.4.3 Municipal tax Municipal tax is levied monthly at the rate of 3% on the wages and salaries paid by an enterprise to its employees, providing that they are part of an Austrian PE. For municipal tax purposes, a person is considered to be an employee if they derive income either from dependent work or certain kinds of independent activities (i.e. certain shareholder-managers). The rules apply also to employees seconded by non-resident personnel leasing companies to an Austrian lessee. For municipal tax purposes, the employee of the leasing company is, as a rule, treated as an employee of the Austrian PE, because the place of work is in Austria.

Municipal tax is levied on the employer. The tax base is the total amount of salaries paid to employees employed in an Austrian PE. Municipal tax is deductible for corporate income tax purposes. In certain cross-border cases (see section 7.4.4), no municipal tax is imposed.

30 Business and Taxation Guide

7.4.4 Provisions for cross-border employments General provisions

Tax treaty law

Foreign nationals carrying out their employment in Austria are basically subject to taxation in Austria, unless a tax treaty assigns the taxation right to the other contracting state.

In most cross-border employments, Art. 15 of the OECD Model Convention (OECD MC) provision is applied (most Austrian tax treaties are concluded on the lines of the OECD MC). Under Art. 15 OECD MC, the country in which the employment is performed (country of exercise) is assigned the taxation rights on the remuneration granted for this activity. However, the employment is taxable in the resident’s state only if the following cumulative criteria are met:

(i) the employee does not stay longer than 183 days during a calendar/tax year or a 12-month period in the country of exercise and

(ii) the employer is not resident in the country of exercise (iii) the remuneration is not borne by a PE which the employer has in the country

of exercise.

With regard to the cross-border employment of board members, only a few tax treaties concluded by Austria provide a separate provision (e.g. the tax treaty concluded with Germany). Depending on the individual situation (executive director; substantial shareholder and director; non-executive director) the provisions on independent services (Art. 14 OECD MC), employment income (Art. 15 OECD MC) or directors’ fees (Art. 16 OECD MC) may be applied.

Social security law

Foreign nationals coming to Austria to perform dependent activities in Austria are basically subject to the same social security scheme applicable to Austrian employees. However, a different treatment may be claimed under EC Regulation 883/2004 or 1408/71 or under a particular bilateral social security agreement that aims to prevent a person being subject to double social security schemes.

As of1 May 2010, persons resident in the EU are subject to the provisions of EC Regulation 883/2004. Under transitional rules, the provisions of EC Regulation 1408/71 remain applicable e.g. in cases where the underlying facts did not change after 1 May 2010. Both EC Regulations provide for the applicable social security scheme in the case of cross-border activities. Depending on a person's personal and professional circumstances, in many cases either the social security regulation of the home country or of the seconding country is applicable. The form A1 (under EC Regulation 1408/71: form E101) on the applicable social security provisions has to be requested in the competent country. Based on this form, no other country is entitled to levy local social security contributions.

31 Business and Taxation Guide

If non-EU residents work in Austria or Austrian nationals work in a third country, a bilateral social security agreement may provide for the applicable social security legislation. Austria currently has concluded social security agreements with 19 third countries/jurisdictions.

Specific provisions

Inward expatriates

Persons not resident in Austria during the past ten years who are employed in Austria temporarily and who keep their foreign residence during this period may benefit from the following tax exemption:

o If the employer refunds typical expatriate expenses borne by the employee (such as the keeping of two households or the costs of trips to visit the family, etc.) such refunds up to 35% of the entire salary are exempt from wage tax.

Outward expatriates

The ITA grants a few tax exemptions to employees working abroad, e.g. Austrian officials on duty in a foreign country or development aid workers. However, the most important wage tax exemption is granted to employees of domestic companies or PEs who perform particular activities abroad for an uninterrupted period exceeding one month. Such beneficial activities performed abroad include operations in connection with the construction, assembly, repair, maintenance, planning, instruction etc. of foreign plants and the hiring out of labour in connection with foreign constructions. 60% of income not exceeding maximum base of social security can be exempted based on domestic rules. For the year 2011 and 2012 a transitional rule applied. For2011 only 66 % (33% in 2012) of the previously tax-exempt income can be claimed as tax exempt.

32 Business and Taxation Guide

8. Double taxation agreements Austria has concluded approximately80 tax treaties in the area of personal and corporate income tax. In most of the agreed treaties the exemption method applies, except for dividends, interest and royalties. 8.1Withholding Tax - dividends

8.1.1 Resident corporate shareholders In general, dividends and other profit distributions made by Austrian GmbH or AG are subject to a withholding tax of 25%. If the recipient is a corporation, withholding tax is not levied, on the condition that the direct or indirect (via a tax-transparent partnership) shareholding is at least 10%. In all other cases, the withholding tax is credited against the final tax liability of the shareholder or refunded during the annual tax assessment. 8.1.2 Non-resident corporate shareholders EC Parent-Subsidiary Directive Having implemented the EC Parent-Subsidiary Directive into Austrian law, Sec. 94/2 ITA exempts outgoing dividends from any withholding tax if:

(i) the EU parent company has a legal form listed in the Annex to the Directive (ii) the EU parent company owns at least 10% of the capital of the subsidiary (iii) shares have been held directly or indirectly (via a tax-transparent partnership) for

an uninterrupted period of one year.

The exemption is not applicable to tax avoidance and abuse of law or in the case of constructive dividend distributions. As a rule, tax avoidance or abuse of law is not assumed if the EU parent company provides its Austrian subsidiary with a confirmation stating that it derives income from active business, employs its own personnel and maintains its own business facilities.

Tax treaties Beyond the scope of the EC Parent-Subsidiary Directive, relief from withholding tax on outbound dividends may be provided by the applicable tax treaties. Generally speaking, reduction (or even exemption) of withholding may be granted at source only if the receiving (foreign) corporation runs an operating business and has its own personnel and premises. Otherwise, treaty relief may be granted by way of a refund procedure.

According to Sec. 21/1/1a CITA (Amurta clause) a non-resident corporation may claim the total amount of the Austrian withholding tax in the following conditions:

o the foreign corporation is resident in the EU or Norway

33 Business and Taxation Guide

o under a tax treaty, the foreign corporation cannot – verifiably – wholly or partly, credit the Austrian withholding tax in its residence state.

8.2 Withholding Tax - interest

Interest paid to non-resident companies is typically not subject to withholding tax. Interest paid on bonds or paid by banks is subject to a 25% withholding tax. The EU Interest and Royalties Directive provides a special regime- there is no withholding tax on Austrian-sourced interest to an associated company, such as a direct parent or sister company, resident in another state of the EU or in Switzerland. However. tax treaties may provide lower rates for other countries.

34 Business and Taxation Guide

9. Sales and use taxes 9.1 Value Added Tax (VAT)

9.1.1 Taxable persons

Taxable transactions carried out by a taxable person in Austria are subject to Value Added Tax (VAT). A taxable person is defined as a person who independently conducts an economic activity, whatever the purpose or results of that activity are. Also, foreign taxable persons (persons without a seat or fixed establishment in Austria) may be subject to Austrian VAT if they carry out taxable transactions in Austria.

9.1.2 Taxable transactions Supply of goods and services Supply of goods means the transfer of the right to dispose of tangible property as owner. Supply of services means any transaction that does not constitute a supply of goods. Supply of services may result from a positive action (e.g. rendering of services) or tolerating actions of other persons (e.g. leasing of immovable property, use of rights and patents).

A supply is also the withdrawal of goods or the use of goods by a taxable person for private use, or for that of staff if the goods form part of the business assets of the taxable person and the VAT on those goods were totally or partly deductible.

Self-supply

Self-supply within the Austrian VAT Act (VATA) comprise non-deductible expenditures under the ITA or CITA for which input VAT was totally or partly deductible.

Import

The transfer of goods from a country outside of the Community to Austria is subject to import VAT.

Intra-Community acquisitions

An intra-Community acquisition is the acquisition of goods transported from an EU Member State to Austria, providing that both the supplier and the recipient are taxable persons for VAT purposes. On the one hand, the supplier carries out a tax-exempt intra-Community supply; on the other hand, the recipient effects an intra-Community acquisition, has to pay VAT and may deduct the VAT under the general conditions. A transfer of goods forming part of business assets by a taxable person from an EU Member State to Austria must also be treated as intra-Community acquisition of goods for consideration, unless the goods are only used temporarily in Austria.

35 Business and Taxation Guide

9.1.3 Place of supply

The supply of goods and services will only be taxed under the VATA if the place of supply is considered to be in Austria. Supply of goods

The place of supply of goods is deemed to be the place where the goods are located at the time the right to dispose of them as an owner is transferred to the recipient.

If the goods are dispatched or transported by the supplier, the recipient, or by a third person (carrier), the place of supply is located where the dispatch or transport begins. Special rules are consequently applicable for ’distance selling’, whereby goods are supplied to private customers and are dispatched by the supplier from one EU Member State to another EU Member State. For distance selling, whereby the supplier exceeds the distance selling threshold of the destination country, the place of supply is not the place of departure of the goods, but the place where the goods are located at the end of transport. Intra-Community acquisitions are generally taxable where the dispatch or transport of the goods ends.

Supply of services

As a result of the EU VAT Directive (2008/8/EC), the regulations concerning the place of supply of services have been amended, with effect from 1 January 2010. Under the new regulations a distinction has to be made between supply of services to taxable persons (B2B transactions) and supply of services to non-taxable persons (B2C transactions).

B2B transaction In general, the supply of services is taxable at the place where the recipient has established his/her business or has a fixed establishment to which the service is supplied. Several regulations determine the place of supply of services in specific circumstances. For example:

o services in connection with immovable property are carried out where the immovable property is located

o passenger transport services are supplied at the place where the transport takes place.

B2C transactions

If the services are supplied to non-taxable persons, they are generally taxable at the place where the supplier has established his/her business. If the supplier has a fixed establishment from which the service is supplied, the service is taxable at the place where the fixed establishment is located. However, there are again several special regulations for determining the place of supply of services.

9.1.4 Taxable amount

The taxable amount is the full amount that the recipient has to pay in order to obtain the goods or services (without VAT). If the taxable person ultimately does not receive the agreed consideration, the chargeable and overpaid VAT has to be adjusted.

36 Business and Taxation Guide

9.1.5 Tax rates In Austria, the following VAT rates are applied: 20% standard VAT rate

10% reduced VAT rate, which applies, in particular, to foodstuffs, agricultural products, books, plants, supply of service by performing artists, transportation of persons, collection and disposal of waste and liquids, hospitals

12% reduced VAT rate for the supply of wine by the producer

19% reduced VAT rate for the customs exclusion zones of the local communities Jungholz and Mittelberg

9.1.6 Exemptions

Numerous exemptions from VAT can be classified in two categories, depending on whether they preclude the deduction of input VAT or not. The most important exemptions are:

Zero-rated supplies

The following supplies do not affect the right to deduct input VAT:

Export of goods (goods are transported outside the Community) Intra-Community supply of goods Cross-border transport of exported goods Cross-border transport of persons by vessels and aircraft Work on and the processing of goods to be exported outside of the Community.

Exempt supplies

VAT exemptions, which preclude the deduction of input VAT, include

Banking and financial transactions, and insurance transactions Transfer of immovable property including buildings (option for taxation connected

with the right to deduct input VAT is possible) Leasing or letting of immovable property for business purposes (option for taxation

connected with the right to deduct input VAT is possible) Services supplied by dentists, doctors or psychotherapists A special exemption scheme for small (domestic) businesses (yearly supplies below

EUR 30,000)

9.1.7 Input VAT deduction A taxable person is entitled to deduct input VAT issued in an invoice (Sec. 11 VATA) for the supply of goods or services carried out in Austria by another taxable person. Also, VAT due in connection with received supply of goods and services where the VAT liability is shifted to

37 Business and Taxation Guide

the recipient (reverse-charge transactions), importations and intra-Community acquisitions may be deducted as input VAT. However, the input VAT may not be deducted in case the received transaction is directly linked to a tax-exempt output supply.

Finally, the amount of the VAT liability in a taxable period comprises the VAT due on taxable transactions conducted by the taxable person less deductible input VAT in the same period. The taxable person must pay the balance due to or may claim a refund from the tax authority.

9.1.8 VAT liability Typically, a taxable person carrying out a taxable transaction is liable for the payment of VAT. The taxable person is obliged to pay the invoiced VAT to the tax authority. Exceptions apply, including for supply of goods with installation/assembly and for supply of services carried out by a foreign taxable person (no seat and no fixed establishment in Austria which is involved in the supply) to another (domestic or foreign) taxable person. In this instance the VAT liability shifts from the supplier to the recipient (reverse-charge mechanism) and the supplier may issue an invoice without VAT and a note that the reverse-charge mechanism is applicable.

9.1.9 Tax assessment Resident taxable persons Any taxable person who commences business activities in Austria must register for VAT purposes with the tax authority.

For VAT purposes, a taxable person carrying out taxable transactions has to file monthly (by the 15th day of the second calendar month following the calendar month for which the VAT is due) and annual (by the 30th of June of the following year) VAT returns electronically.

In addition, taxable persons carrying out intra-Community supply of goods and cross-border supplies of services to another Member State, which are subject to the general provision for B2B transactions and for which the reverse-charge mechanism is applicable, have to file recapitulative statements that show the VAT identification numbers of the recipient and the total value of all supplies made to them each month. The recapitulative statements must be filed, at the latest, by the end of the month that follows the month in which the supply was performed.

Foreign taxable persons

Foreign taxable persons (no seat or fixed establishment in Austria) carrying out taxable transactions in Austria have to register for VAT purposes at the tax office Graz Stadt and electronically submit monthly and annual VAT returns, unless they only perform supplies in Austria for which the reverse-charge mechanism applies. In their submissions, foreign taxable persons must declare the respective outgoing and incoming supplies in Austria.

If a foreign taxable person conducts a domestic supply of goods to a taxable person in Austria, for which the reverse-charge mechanism does not apply, the recipient has to

38 Business and Taxation Guide

withhold and pay the VAT in the name and on behalf of the supplier to the Austrian tax office of the supplier; otherwise the recipient is held liable for payment of VAT.

Also, foreign taxable persons who do not have their permanent residence, seat or fixed establishment in the European Community must have a fiscal representative if they carry out supplies subject to Austrian VAT.

Taxable persons established within the EU may reclaim Austrian VAT which was invoiced to them by filing a refund application with the competent tax authority in the Member State of residence. Subsequently, after verification the application is submitted to the Austrian tax authorities automatically. The following conditions must be fulfilled:

the taxable person has no seat and no fixed establishment in Austria, and the taxable person has neither effected supply of goods or services, self-supplies nor

carried out intra-Community acquisitions in Austria or has rendered only certain supplies (e.g., only supplies for which the reverse-charge mechanism is applicable).

Taxable persons from non-EU Member States may claim a refund of input VAT by filing an application with the tax office Graz-Stadt, using the official form. The following conditions must be fulfilled:

the taxable person has no seat and no fixed establishment in Austria/EU the taxable person has neither effected supply of goods or services, self-supplies nor

carried out intra-Community acquisitions in Austria or has rendered only certain supplies (e.g., only supplies for which the reverse-charge mechanism is applicable).

39 Business and Taxation Guide

10. Real estate and portfolio investments 10.1 Real estate investments

The general principles for taxation of Austrian resident or non-resident individual and corporate investors equally apply to real estate investments.

10.1.1. Individual resident investors

Income from real estate can include:

business income income from rentals and leasing short-term capital gains.

Business income

If real estate activity qualifies as business income, the general principles of business taxation apply. Rentals and leasing payments and capital gains from selling real estate are fully taxable. Expenses (e.g. ongoing expenses and maintenance) are, in general, tax deductible.

Acquisition costs must be capitalised. For buildings, these acquisition costs may be depreciated over the useful life. The same applies for manufacturing costs of real estate (costs incurred by the land owner for the construction of a building or major extensions of existing buildings). According to tax law, the maximum depreciation rates for real estate are:

half of a percentage for the year of acquisition or disposal if the utilisation of the real estate is less than six months

4% for buildings without a solid structure 3% per year if used by lessee for trade or farming/forestry activity 2.5% per year if used by lessee for bank or insurance business 2% per year for all other business activities higher depreciation rates if supported by appraisal.

A plot of land is not depreciable. Tax-effective write down to the lower market value is required if the market value is below the tax book value. For residential buildings rented out to individuals, other than own employees, a special rule applies: Some costs of maintenance, which may not be capitalised as manufacturing costs,

but which increase the value of the building significantly or increase the useful life significantly, must be allocated over a period of ten years.

Prepayments that refer to future periods have to be deferred and are in general tax effective in the future period.

The standard income tax rates (0% to50%) apply.

40 Business and Taxation Guide

Income from rentals and leasing

If the activity does not qualify as a business activity, rental and leasing payments are taxed as ’income from rentals and leasing’. Expenses related to this activity, including 1.5% depreciation for buildings, may be deducted as expense. A plot of land is not depreciable.