business development issues in latin...

TRANSCRIPT

1Julio 2007

Iberdrola Renovables SA

BUSINESS DEVELOPMENT ISSUES IN LATIN AMERICA

February 2008

2

Contents

I. Iberdrola Group NumbersII. Iberdrola Renewables Growth StrategyIII. “Renewable” countriesIV. Some Data about Latin AmericaV. One Example: The Case of ColombiaVI. Conclusions

Iberdrola Group Numbers

Energy Production (GWh) 86.800

Energy Sales (GWh) 115.508

Nº of Customers (Gas & Electricity) (millions) 24

Installed capacity (MW) 41.001

11.38

Stock Market Value

(30 October 2007)

51.44

Net Profit(Profit year 2006: 1.660 M euros)

Total Assets 68.13

Operational Data Nine months of 2007

Financial Data Nine months 2007

(Billion euros)

Income

1.61 Nº of Employees 26.375

4

Iberdrola focusses in the Atlantic Region: Four strategic markets

North America:2º Wind energy producer (in US)

3º Gas storing (in US)

Latin America: 1º Private generation Co Mexico

1º Distribution Co Brazil

United Kindom:3rd Distribution Co

Among the5 major retailers1ª Wind energy producer

Spain:1 º Utility

Iberdrola Group Strategic Markets

ProductionProduction MixMix 20062006

NuclearNuclear27%27%

CombComb. . CycleCycle40%40%

CoalCoal6%6%

OilOil2%2% HydroHydro

14%14%

WindWind9%9%

Cogeneration Cogeneration 2%2%

Iberdrola Group Production Numbers

2005 2006

CombinedCombinedCycleCycle

EmissionEmissionFreeFree

91.99191.99183.00983.009

Production GrowthProduction Growth

+15%+15%+15%

+18%+18%+18%

+10,8%+10,8%

Driven by Low Emission TechnologiesDriven by Low Emission Technologies

-32%--32%32% Coal + OilCoal + Oil

* Hidráulica + Nuclear + Eólica

GWhGWh

6

Iberdrola Renovables Evolution

1.070 MW

2001

2003

2004-05

2007

2006

2001

Startegic Plan2001-2006

Leader in Spain CORE

Getting into European market

Getting intoUS market

Acquisition ofScottish Power

4.434 MW

2006

7.342 MW

2007

Stock market

Iberdrola Renovables Near Future

Pipeline42.000 MW

Rest

USA

Spain

18% 16%

51%

Installed Wind Capacity 7.704 MW

Spain

USA

United Kindom

Res

4.214 MW(62%)

507 MW(7%)

1,741 MW(26%)

364 MW(5%)

United Kindom

15%

World Leader in Wind Energy

13.500 MW by 201013.500 MW by 2010

8

Iberdrola Renovables: Growth Strategy

Regulating frame / Infrastructures

Growth

Potential

+

+_

_

Asia

Latin America

Medit. S- E Canada

Spain

USA

FranceU.K.

Poland

Greece

Portugal

GermanyEast Europe

Short termMedium Term

Case-by- case oportunities

Low Interest

9

Installed Capacity (MW) Mechanism

Countries In 2006 Ac Dec 2006

Feed-In Certifictes

Germany 1.773 20.200 Spain 1.572 11.600 Danmark 9 3.136 Italy 224 1.941 Netherlands 345 1.553 U.K. 616 1.958 Portugal 529 1.553 France 708 1.478 Sweden 27 519 Austria 146 965 Greece 173 746 Belgium 28 188 Total 6.150 45.837

Renewable Countries: Clues for success

Feed-In tarif: key for success

More than 90% installed wind capacity in countries with feed-in tarif.

High growth rates in countries with feed-in tarif

No significant successes where certificates

* Data as of Dec 2006

10

Fuente: Communication from the Commission : “The support of electricity from renewable energy sources”, dic 2005

Bélgica

Italia

RUPrices for end user of wind energy are higher in countries with certificates

Feed-in results in less cost for end user

Due to higher risks, profitability required by investors under certificate schemes are higher. Final customer pays more at the end

Din

amar

ca

EspañaFi

nlan

dia

11

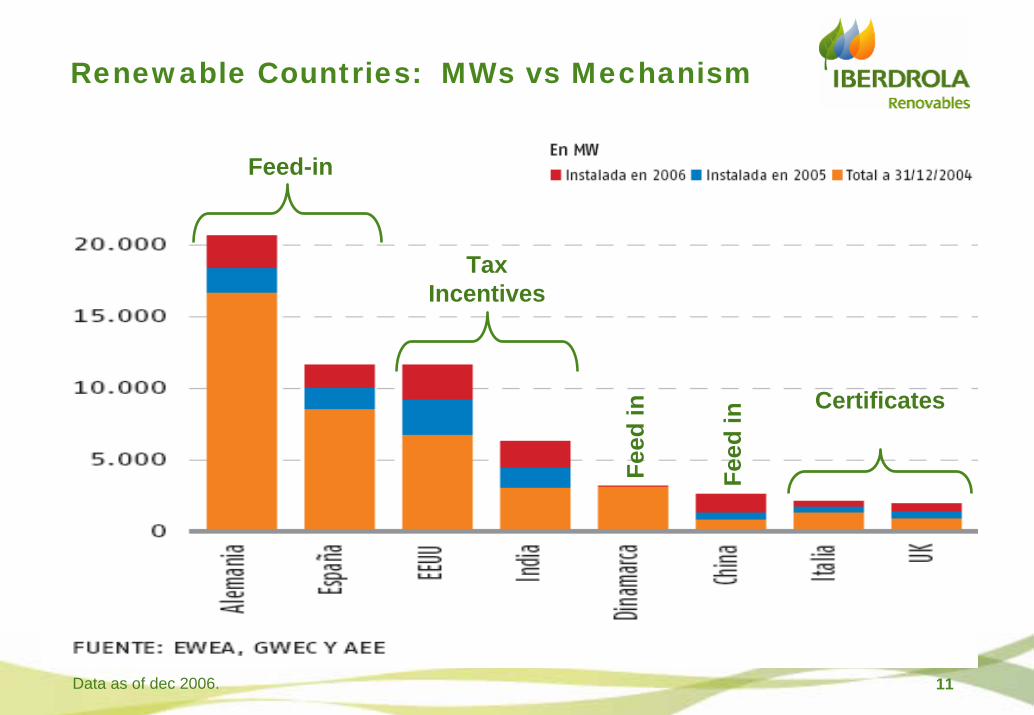

Renewable Countries: MWs vs Mechanism

Data as of dec 2006.

Feed-in

TaxIncentives

Feed

in

Feed

in

Certificates

12

Renewable countries: average prices of wind energy in 2007

PAIS REGULACION €/MWh - 2007

USA Certificates/Incentives 81Spain Feed In (RD 436) 79United Kindom Certificates 114Greece Feed in/ Investment subsidees 90Francia Feed in 82,5Polonia Certificates 74Brasil Feed in (PROINFA) 82

Latin America: some figures (aprox)

13

LATAM MEXICO BRASIL REP DOM CHILE COLOMBIA PANAMA PERU ECUADOR ARGENTINA GUATEMALA COSTA RICA

Installed (MW) 300.000 58.633 96.634 3.394 12.720 13.280 1.540 6.548 4.398 24.352 1.758 2.048

Generation mix 52%H 45%T21%H 72%T

7%O 76%H 21%T 3%O 14%H 83%T 3% G 39%H 61%T 66%H 33% T 1%O 44%H 56%T 50%H 50%T 50%H 50%T 42%H 54%T 4%N 38%H 60%T 2% G 63%H 19%T 17% G

Demand growth 5% 5,20% 4% 4,40% 5,50% 4,70% 5% 6,50% 6,20% 7% 7,00% 7%

Rating (S&P) BBB+ BB+ B+ A+ BB BB+ BB+ CCC+ B+ BB BB

Price range (Apr)75-85

$/MWh 65-80 $/MWh 70-75 $/MWh 55-60 $/MWh 45-55 $/MWh100-120 $/MWh

50-60 $/MWh

90-100 $/MWh 30-35 $/MWh110-120 $/MWh

Electric market Liberalized Generation Lib Liberalized Liberalized Liberalized Liberalized Liberalized Liberalized Liberalized Liberalized Monopoliy ICE

Types of contracts PPAs - Licts PPAs - Licts PPAs - SPOT PPAs - SPOT PPAs - SPOT PPAs PPAs - SPOT PPAs - SPOT PPAs - SPOT PPAs - SPOT Licitaciones

Allowed parties CFE - Clients Distribution Cos Distribs - Clients Distribs - Clients Distribs - Clientes Distribution CoDistribs -Clientes Distribs - Clientes Gens-Dist-Clientes Distribs -- Grandes Cl ICE

Applicable laws X Law 5/07 -Regl 2008 law 2008 Law 08 Law 2004 Law 2003 / Reg 2005 NA

Types of support Incentive Feed in (-) Feed in Certificate Incentive Incentive Feed in Feed in Incentive Feed in (-)

Wind Potential

Capacity > 200.000 30.000 > 100.000 5.000 10.000 10.000 2.000 3.000 1.000 >100.000 3.000 5.000

Hours 2500-40004000 (Sur) 3000 (W) 3.000 (N) > 2.500 (S) 3000- (Norte-Este) 3.000 (C-N) 3.500 (Norte) 3.000 3.000 2.500 3.500 (S) 3.000© 2500 (Centro) 3500

Wind share > 15.000 5000 10.000 400 700 600 150 600 250 1000 150 200

Latin America: Some facts from figures

• Huge undeveloped wind potential• Generation mix base on Hydro + Thermal• High rates of growth: concerns about availability in the future• Wide ranges of prices. Some very low• Ratings below investment grade: higher requirements• Liberalized markets: energy competes per price• In many countries renewable cannot compete w/o support• Some interesting support initiatives but limited support, so far

14

Example of Colombia: Price history

Source: Empresa Operadora del Mercado ‐ XM S.A.‐

(1 Euro = 2.781 CO $ ------- 75 CO $ = 2,69 cents of euro)

Example of Colombia: Price forecast

Source : Estimates of generation costs, including the “cargo por confiabilidad”, under different generation mixes

30

35

40

45

50

55

60

65

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

Jan-

16

Jan-

17

Jan-

18

Jan-

19

Jan-

20

Jan-

21

Jan-

22

US$/M

Wh

Black = MIX 1 (H + G) Red = MIX 2 (H + G + C) BLUE= MIX 3 (H + G + C + R)

Example of Colombia: Present Situation

Profitability considering average investment and financing conditions together with Colombia electricity market conditions is in the range of 1% to 5%

Profitability considering average investment and financing conditions together with Colombia electricity market conditions is in the range of 1% to 5%

Commissioning : 2009

Investment : 2.200mUS$/MW

Capacity Factor: 35-40% (above normal, considering the best resources of the country: Guajira)

Electricity market price(*): 30 US$/MWh

Other Income (*) (“cargo por confiabilidad” , “certificates”…): 10-20$/MWh

Operational Inputs : Average market valuesOperational Inputs : Average market values

Depreciation: 20 years

Corporate tax: 33% of EBIT

Tax Incentives: Tax credit up to 40% of the total investment during life cycle

Financial InputsFinancial Inputs

(*) Crecimiento anual = Inflación

Example of Colombia: Effect of somepotential measures

Additional Income (Certificates, CDMs, extras to market price,…)Additional Income (Certificates, CDMs, extras to market price,…)

Mild financing schemes (effect on ROE) *Mild financing schemes (effect on ROE) *

1 year : + 50 bp above base case (equity)

Possible measures to increase profitability to a prospective investor can be of two types, orcombinations

Possible measures to increase profitability to a prospective investor can be of two types, orcombinations

Exemption periodExemption period Lower Interest RatesLower Interest Rates

18

Total increase above the assumptions: +10 US $/MWh ----------- +300 bp above base case +20 US $/MWh ----------- +450 bp above base case

+30 US $/MWh ----------- +630 bp above base case

Note: Base case Equity: 70% senior debt at an interest rate of 5%

2 years: +100 bp above base case (equity)

3 years : +170 bp above base case (equity)

2,5%: +260 bp above base case (equity)

4,0%: +90 bp above base case (equity)

0,0%: +653 bp above base case (equity)

* Return on equity has been calculated estimating no witholding tax and 100% of cash flows and reserves (after debt) converted to dividends