business interruption values & exposures dempsey, myers & company quinnipiac university june...

TRANSCRIPT

Business Interruption Values & Exposures

Business Interruption Values & Exposures

Dempsey, Myers & CompanyQuinnipiac University

June 14, 2006

Today’s PresentationToday’s Presentation

BI Basics BI Values Explained Values v. Exposures Hypothetical Claims

A Business Interruption PrimerA Business Interruption Primer

The purpose of BI coverage is to do for the business what it would have done for itself had there been no loss.

Coverage generally triggered by physical damage.

Reimburses net profits, continuing expenses and expenses incurred to reduce loss

Optional coverage for extra expenses to continue operations

Duty to mitigate

Coverage Triggered by Direct Damage to Insured Property

Coverage Triggered by Direct Damage to Insured Property

Underlying Form: ISO/Proprietary/Manuscript

Extended Period of Indemnity Research and Development E-Commerce Extra Expense

Coverage Triggered by Damage to Other Property

Coverage Triggered by Damage to Other Property

Contingent Business Interruption Contingent Extra Expense Interdependent Properties Civil Authorities Ingress/Egress Service Interruption Leasehold Interest Royalties

Business InterruptionBusiness Interruption

Three Essential Variables:– Time– Revenue– Costs

Business InterruptionBusiness Interruption

Key Revenue Streams - 2006 ($2.95b)

State of Michigan38%

Federal programs

12%

Local and private programs

7%

Student fees24%

Auxiliary activities 13%

Departmental activities

4%Investments/Other2%

Business InterruptionBusiness Interruption

Expenditures and Surplus - 2006

Services17%

Scholarships10%

Operating expense

18%

G&A expense6%

Fixed/other4%

Surplus5% Instruction/research

40%

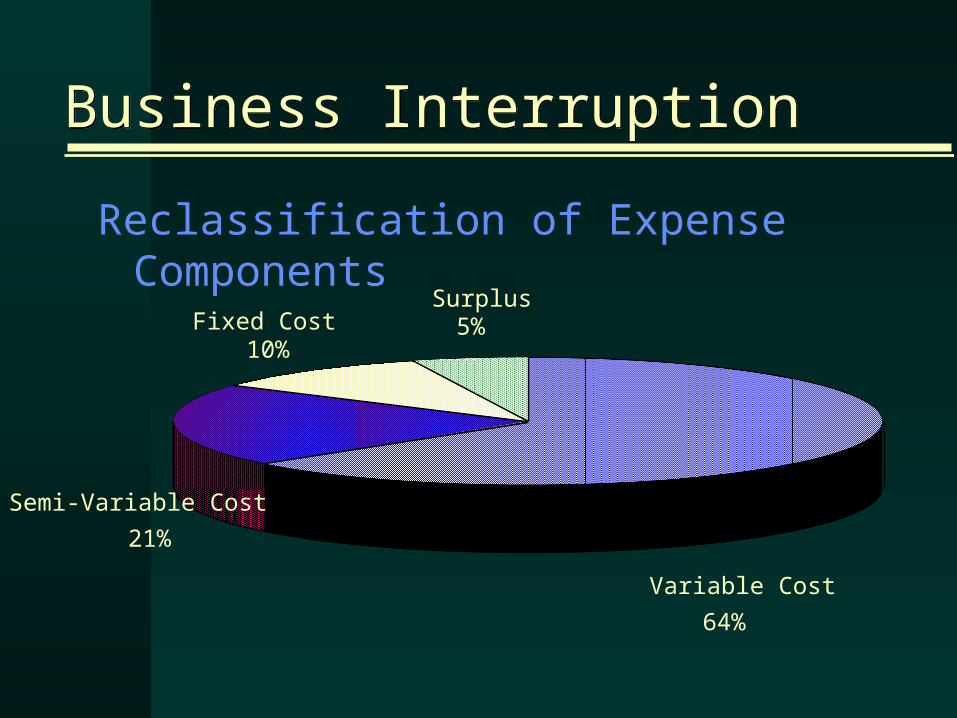

Business InterruptionBusiness Interruption

Reclassification of Expense Components

Variable Cost

64%

Semi-Variable Cost

21%

Fixed Cost10%

Surplus5%

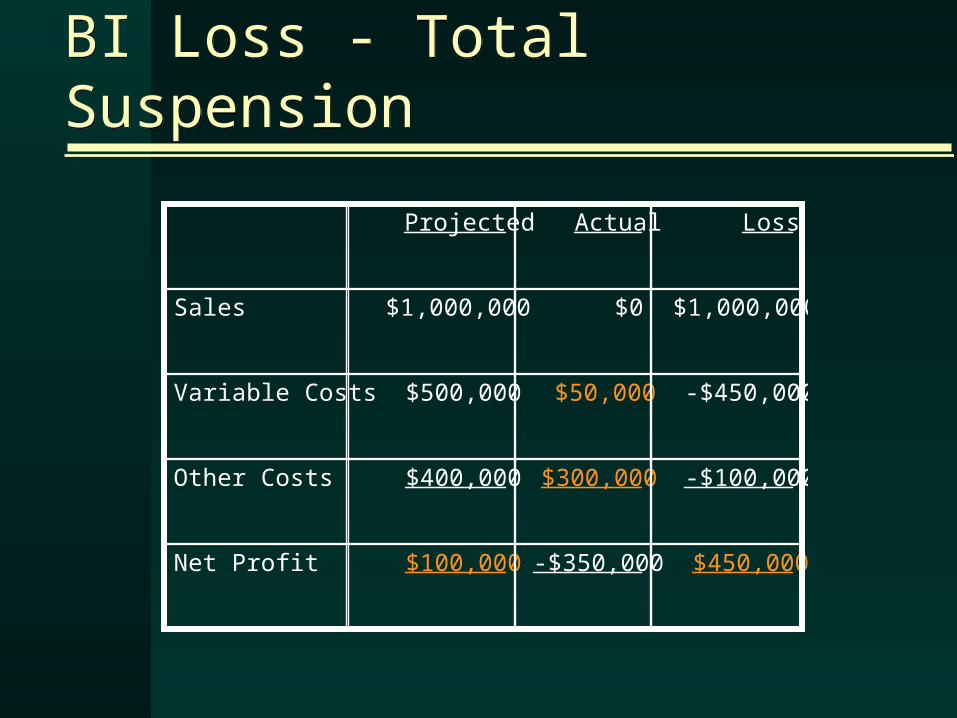

BI Loss - Total SuspensionBI Loss - Total Suspension

$450,000-$350,000$100,000Net Profit

-$100,000$300,000$400,000Other Costs

-$450,000$50,000$500,000Variable Costs

$1,000,000$0$1,000,000Sales

LossActualProjected

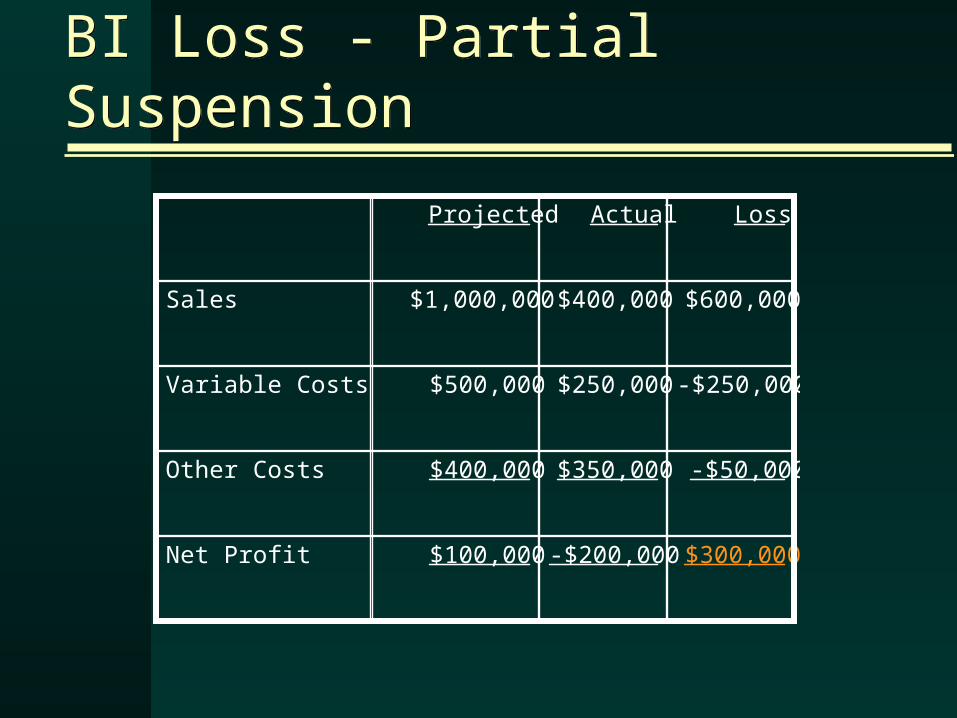

BI Loss - Partial SuspensionBI Loss - Partial Suspension

$300,000-$200,000$100,000Net Profit

-$50,000$350,000$400,000Other Costs

-$250,000$250,000$500,000Variable Costs

$600,000$400,000$1,000,000Sales

LossActualProjected

Business Interruption LossBusiness Interruption Loss

Evaluate Nature of Revenue:– Will it abate in the event of loss?

State of Michigan appropriationsOther government aidStudent feesAuxiliary activitiesResearch grantsInterest

Business Interruption LossBusiness Interruption Loss

Evaluate Nature of Cost:– Will it abate in the event of loss?

Instructional costs (salaries, supplies)

Utilities and maintenanceAuxiliary expensesResearch costsGeneral & Administrative costsDepreciation and interest

What are BI Values?What are BI Values?

A projection of what the business

will do during a 12-month period

What are BI Values?What are BI Values?

Annualized estimates of net profit and “continuing” (fixed) expenses

May or may not include “ordinary payroll” (direct labor expense)

Computed for each insured location where earnings are produced

Policy requirement of most insurance markets

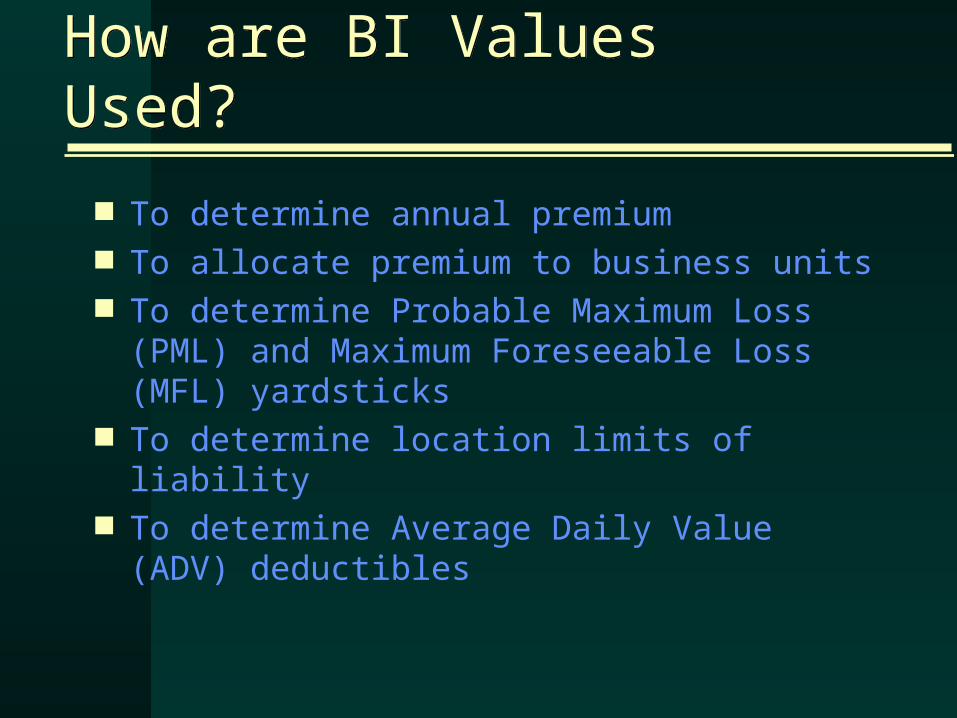

How are BI Values Used?How are BI Values Used?

To determine annual premium To allocate premium to business units To determine Probable Maximum Loss (PML) and Maximum Foreseeable Loss (MFL) yardsticks

To determine location limits of liability

To determine Average Daily Value (ADV) deductibles

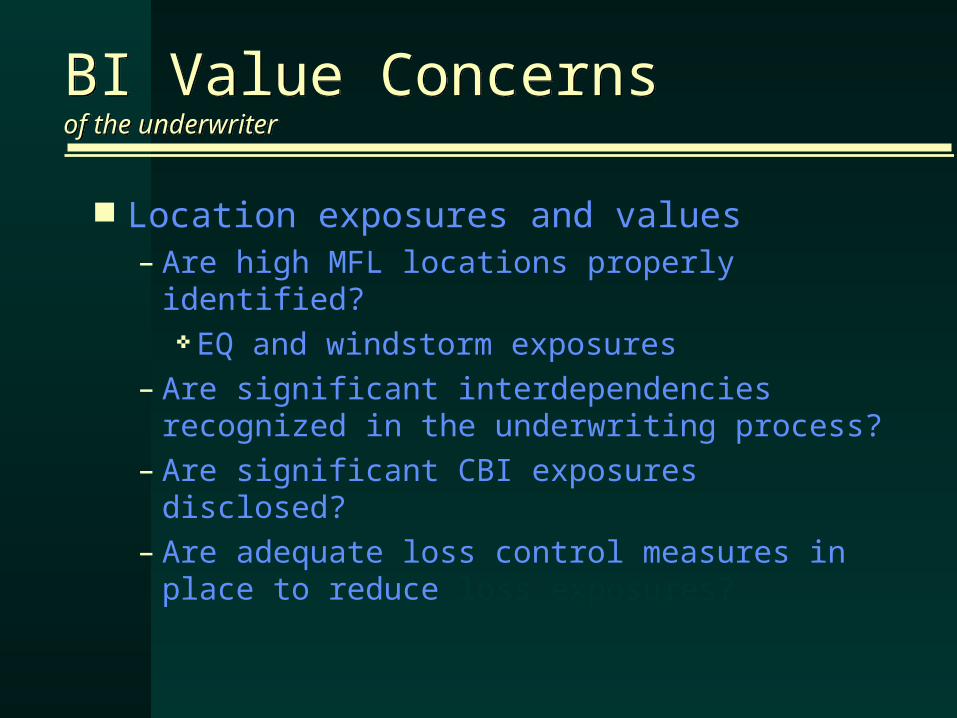

BI Value Concernsof the underwriter

BI Value Concernsof the underwriter

Location exposures and values– Are high MFL locations properly identified? EQ and windstorm exposures

– Are significant interdependencies recognized in the underwriting process?

– Are significant CBI exposures disclosed?

– Are adequate loss control measures in place to reduce loss exposures?

BI Value Concernsof the risk manager

BI Value Concernsof the risk manager

Conceptual framework and accuracy– Do business units understand the purpose and importance of accurate BI value reporting?

Premium allocation– Are reported values calculated consistently among business units and locations?

Process efficiency– Is the right amount of data reported?– Is the collection process rational and efficient?

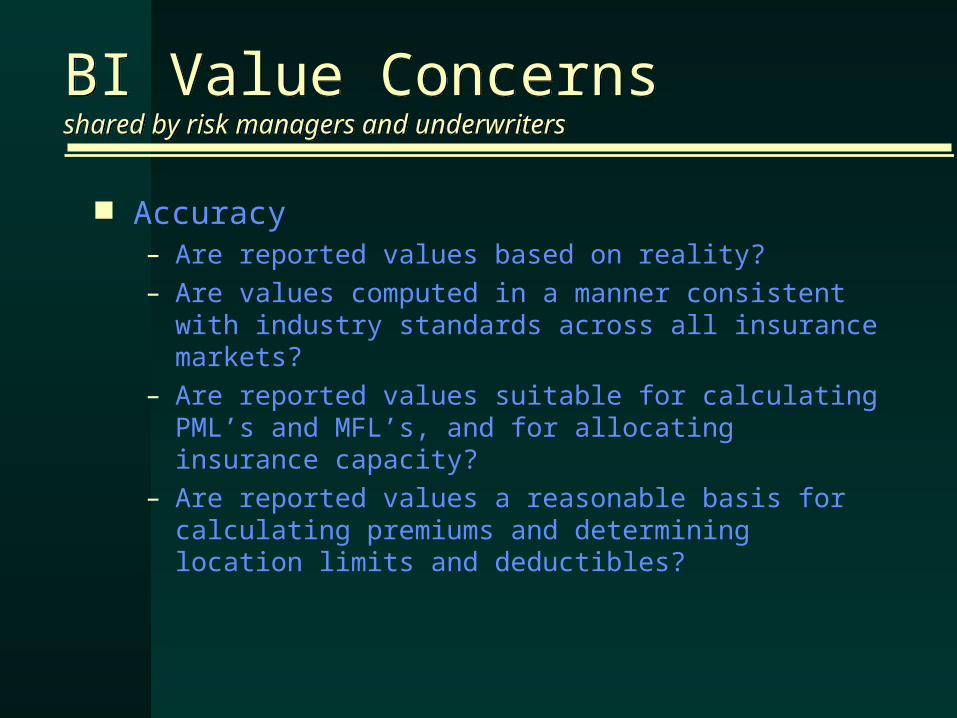

BI Value Concernsshared by risk managers and underwriters

BI Value Concernsshared by risk managers and underwriters

Accuracy– Are reported values based on reality?– Are values computed in a manner consistent with industry standards across all insurance markets?

– Are reported values suitable for calculating PML’s and MFL’s, and for allocating insurance capacity?

– Are reported values a reasonable basis for calculating premiums and determining location limits and deductibles?

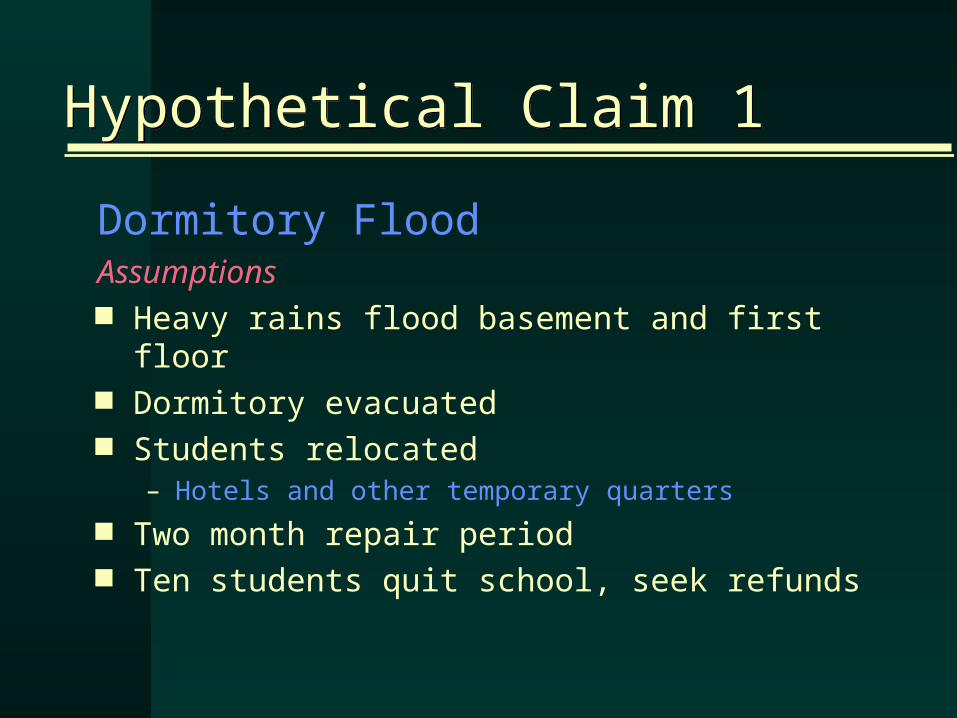

Hypothetical Claim 1Hypothetical Claim 1

Dormitory FloodAssumptions Heavy rains flood basement and first floor

Dormitory evacuated Students relocated

– Hotels and other temporary quarters Two month repair period Ten students quit school, seek refunds

Hypothetical Claim 1Hypothetical Claim 1

Dormitory FloodAssumptions Heavy rains flood basement and first floor

Dormitory evacuated Students relocated

– Hotels and other temporary quarters Two month repair period Ten students quit school, seek refunds

Hypothetical Claim 1Hypothetical Claim 1

Dormitory FloodIssues Presented Value of extra expense loss

– Living expenses– Transportation

Value of business interruption loss– Lost room revenue– Lost vending profits

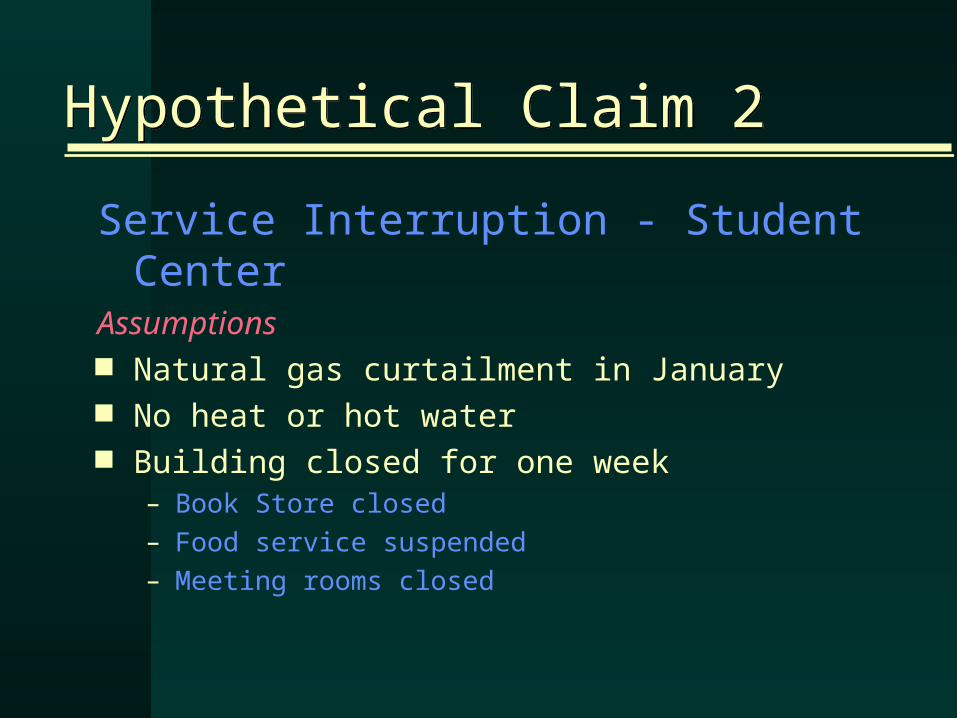

Hypothetical Claim 2Hypothetical Claim 2

Service Interruption - Student Center

Assumptions Natural gas curtailment in January No heat or hot water Building closed for one week

– Book Store closed– Food service suspended– Meeting rooms closed

Hypothetical Claim 2Hypothetical Claim 2

Service Interruption - Student Center

Issues Presented Value of business interruption loss

– Lost Book Store Profits– Lost Food Service Profits– Loss Mitigation

Value of extra expense loss– Meeting relocation costs

Hypothetical Claim 3Hypothetical Claim 3

Laboratory Fire - R&D LossAssumptions Biochemical experimentation US Government funded for fiscal 1997 Three-fourths completed at time of fire Entire experiment lost; nine months to replace Grant revenue $1 million; fixed cost $83,000/month

One month total suspension to repair fire damage Risk of losing future grants if fail to complete

Hypothetical Claim 3Hypothetical Claim 3

Laboratory Fire - R&D LossIssues Presented Value of business interruption loss

– Total suspension period - 30 days– Remainder of period - 9 months– Lost opportunities

Other potential losses– Expediting costs– Extra expenses

Q&AQ&A

Contact DetailsContact DetailsSharon Pisko Wolfe, CPADempsey, Myers & Company LLP426 Danbury RoadWilton, CT [email protected]

Karen Henricksen, CPA, CFEDempsey, Myers & Company LLP127 East 56th Street, 4th FloorNew York, NY [email protected]