business management. business management definitions management: directing of labor...

TRANSCRIPT

BUSINESS BUSINESS MANAGEMENTMANAGEMENT

Business ManagementBusiness Management

DefinitionsDefinitions Management:Management:

• Directing of labor resourcesDirecting of labor resources• utilization of resources/materialsutilization of resources/materials• production decisionsproduction decisions

Labor:Labor:• implementation implementation

of management of management decisions decisions

Departmentalization ExampleDepartmentalization Example

Owner(s) Owner(s) or board of or board of

directorsdirectors

General ManagerGeneral Manager

Engineering Engineering ManagerManager

Production Production ManagerManager

Marketing Marketing ManagerManager

Business Business affairs affairs

ManagerManager

Source:Source: Nelson, P.V. 1998. Greenhouse operations and management. 5th ed. Nelson, P.V. 1998. Greenhouse operations and management. 5th ed. Prentice-Hall Inc.Prentice-Hall Inc.

Production managerProduction manager• crop production/scheduling/recordscrop production/scheduling/records• production materials ordering/storingproduction materials ordering/storing• production labor schedulingproduction labor scheduling

Marketing managerMarketing manager• sales/promotions/recordssales/promotions/records• order “pulling”, packaging, and deliveryorder “pulling”, packaging, and delivery

Engineering managerEngineering manager• maintains physical plant, structures and equipmentmaintains physical plant, structures and equipment• may include shop for custom-building may include shop for custom-building

equipment/buildingequipment/building Business administration managerBusiness administration manager

• financial recordingsfinancial recordings• purchasing, billing, and payrollpurchasing, billing, and payroll

Greenhouse “Evolution”Greenhouse “Evolution” Up to about 60,000 ftUp to about 60,000 ft22

• owner/managerowner/manager• laborerslaborers• secretary/bookkeepersecretary/bookkeeper

Above 60,000 ftAbove 60,000 ft22

• owner/marketing manager? owner/marketing manager? engineering manager?engineering manager?

• production managerproduction manager• growersgrowers

• business officebusiness office

Business ManagementBusiness Management

Business ManagementBusiness Management

Business StructureBusiness Structure Survival tenets:Survival tenets:

• each employee answers to each employee answers to one person only one person only

• ownership = full ownership = full responsibilityresponsibility

• departmentalize logically departmentalize logically and as needed and as needed

• delegate responsibilitydelegate responsibility• complycomply• records rulerecords rule

Business ManagementBusiness Management

Labor ManagementLabor Management

Have clearly defined job descriptions and goals for Have clearly defined job descriptions and goals for labor forcelabor force

Establish effective evaluation and Establish effective evaluation and rewards systemrewards system

Create positive working conditions Create positive working conditions (physically and mentally)(physically and mentally)

COMMUNICATIONSCOMMUNICATIONS

Business ManagementBusiness Management

RecordsRecords Cultural records include timing (or treatments) and Cultural records include timing (or treatments) and

schedulesschedules Plant environment records include temperature/light Plant environment records include temperature/light

records, plant/substrate test results, insect & disease records, plant/substrate test results, insect & disease scoutingscouting

Production records are “timing Production records are “timing notes” and visual assessments (digital notes” and visual assessments (digital photographs!)photographs!)

Pesticide application records/ Pesticide application records/ WPS/govt. compliancesWPS/govt. compliances

A Typical Cultural Schedule

Record Placed at the End of a Bench in the Greenhouse

Greenhouse section Benches Crop Cultivar

Datescheduled

Dateaccomplished

Operation

Employee

3-7 Plant 7” x 8” 3-7 Fertilize, half strength 3-7 Start lighting at night

3-14 Fertilize and spray 3-21 Fertilize and spray 3-28 Pinch 3-28 Fertilize and spray 4-4 Fertilize and spray

4-11 Fertilize and spray 4-18 Fertilize and spray 4-18 Start shading 4-19 Prune plants back to 2 or 3 shoots 4-25 Fertilize and spray 5-2 Fertilize and spray 5-9 Fertilize and spray

5-16 Fertilize and spray 5-23 Fertilize and spray 5-30 Fertilize and spray 5-30 Disbud 6-6 Fertilize and spray

6-13 Spray 6-20 Spray 6-24 Harvest

Business ManagementBusiness Management

Financial RecordsFinancial Records IncomeIncome Expenses:Expenses:

• variable costs (fertilizer, pesticides, substrate, variable costs (fertilizer, pesticides, substrate, containers, labels, boxes/packaging, seed/cuttings, containers, labels, boxes/packaging, seed/cuttings, labor) labor)

• fixed costs (depreciation of equipment and buildings, fixed costs (depreciation of equipment and buildings, interest, repairs/maintenance, taxes, insurance, office interest, repairs/maintenance, taxes, insurance, office expenses, telephone, accounting/legal fees, travel and expenses, telephone, accounting/legal fees, travel and dues, management salaries, fuel, electricity)dues, management salaries, fuel, electricity)

LaborLabor• Potting, Watering, Spraying, Pinching, HarvestingPotting, Watering, Spraying, Pinching, Harvesting

Cost Analysis Sheet for an

Individual Crop Listing Expenses, Revenues, Profits

or Loss

Source:Source: Nelson, P.V. Nelson, P.V. 1998. Greenhouse 1998. Greenhouse operations and operations and management. 5th ed. management. 5th ed. Prentice-Hall Inc.Prentice-Hall Inc.

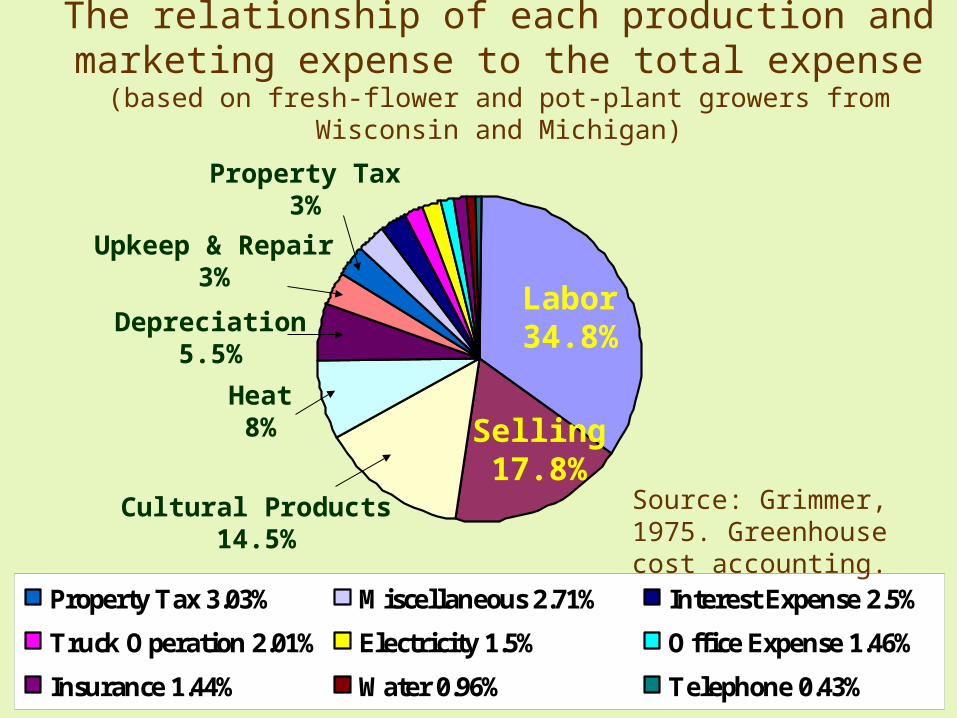

Property Tax 3.03% Miscellaneous 2.71% Interest Expense 2.5%

Truck Operation 2.01% Electricity 1.5% Office Expense 1.46%

Insurance 1.44% Water 0.96% Telephone 0.43%

Labor34.8%

Selling17.8%

Cultural Products14.5%

Heat8%

Depreciation5.5%

Upkeep & Repair3%

Property Tax3%

The relationship of each production and marketing expense to the total expense

(based on fresh-flower and pot-plant growers from Wisconsin and Michigan)

Source: Grimmer, 1975. Greenhouse cost accounting.

Business ManagementBusiness Management

Cost AnalysisCost Analysis Statement of cash flow (monthly)Statement of cash flow (monthly)

• day-to-day ability to pay debtsday-to-day ability to pay debts Balance sheet (annually)Balance sheet (annually)

• assets (cash, equipment, stock, etc.)assets (cash, equipment, stock, etc.)• liabilities (outstanding loans, interest, etc.)liabilities (outstanding loans, interest, etc.)

Income statementIncome statement• revenuesrevenues• expensesexpenses

Planning for Profit IncreasePlanning for Profit Increase

Profit depends on management of expenses and Profit depends on management of expenses and the production of revenuethe production of revenue• revenue can be increased by:revenue can be increased by:

• higher productivity higher productivity • higher quality product (if not currently higher quality product (if not currently

meeting market standards)meeting market standards)• more profitable market channelsmore profitable market channels• rising prices (small increases and only if rising prices (small increases and only if

justified) justified) • lower expenseslower expenses

What Is the Economic Impact of What Is the Economic Impact of Rising Expenses on Profits?Rising Expenses on Profits?

Enterprise budgetsEnterprise budgets• determine profitsdetermine profits• analysis of breakevenanalysis of breakeven

If a factor of production was increased If a factor of production was increased one-percent, what is the anticipated percentage one-percent, what is the anticipated percentage change effect on profit?change effect on profit?

Study by Stegelin, F. 2001. Southeastern Floriculture 11(2)

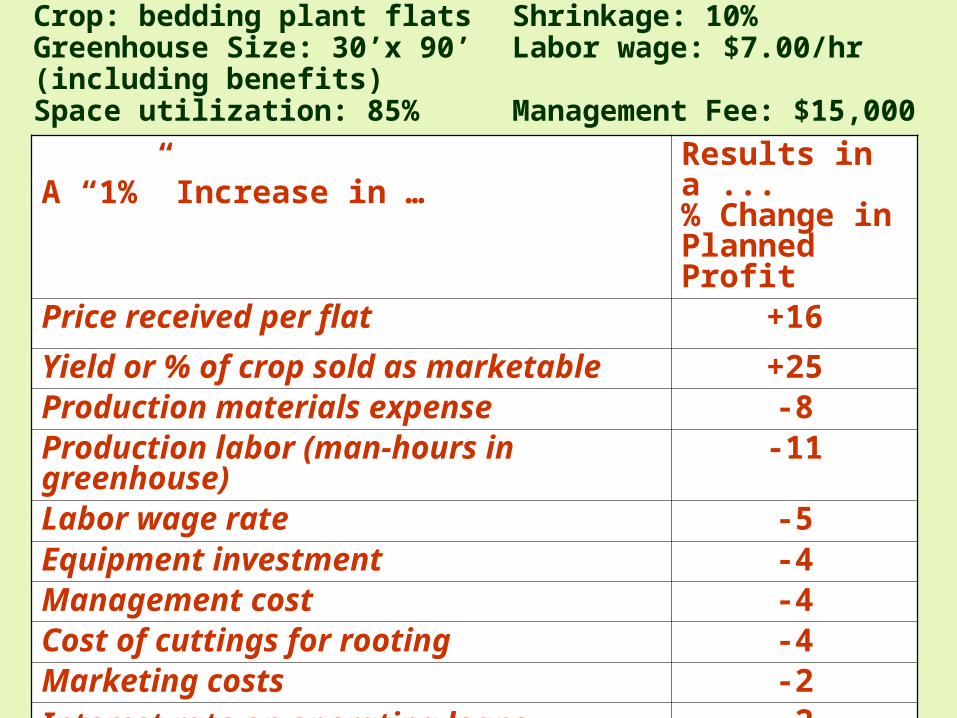

A “1%” Increase in …Results in a ...% Change in Planned Profit

Price received per flat +16Yield or % of crop sold as marketable +25Production materials expense -8Production labor (man-hours in greenhouse) -11Labor wage rate -5Equipment investment -4Management cost -4Cost of cuttings for rooting -4Marketing costs -2Interest rate on operating loans -2

Utility rate for heating (natural gas) -2

Crop: bedding plant flats Shrinkage: 10%Greenhouse Size: 30’x 90’ Labor wage: $7.00/hr (including benefits)Space utilization: 85% Management Fee: $15,000

Bodie Pennisi Bodie Pennisi

Paul Thomas Paul Thomas

Forrest StegelinForrest Stegelin

CopyrightCopyright, 2003, 2003The University of Georgia The University of Georgia

Department of Horticulture Department of Horticulture Department of Agricultural and Applied EconomicsDepartment of Agricultural and Applied Economics