business opportunities in latam€¦ · •latam accounts for 16% of total global food and...

TRANSCRIPT

BUSINESS OPPORTUNITIES IN LATAM

Thessaloniki, April 6th 2017

Program funded by the

European Union

Implemented by the consortium led by AESA

Why LATAM?

• A US$5.3 trillion economy

• Approximately 600 million citizens

• Latin America is a rapidly-growing market• A fast growing middle class

And because diversifying export markets is alwaysa good idea…

Why Latin American?

US$ 5.3 trillion economy

GDP almost x3 in 15 years

Why Latin America?

Despite economic uncertainty…things are expected to improve

Why Latin America?

Fast growing middle-class

What does Latin America look like?

Population disparities

What does Latin America look like?

Fast-growing urbanization

What does Latin America looks like?

LATAM aging population +65 years %

What does Latin America look like?

Uneven economic growth across the region

What does Latin America look like?

GDP per capita disparity across the region

What does Latin America looks like?

Income inequalities within countries

What does Latin America looks like?

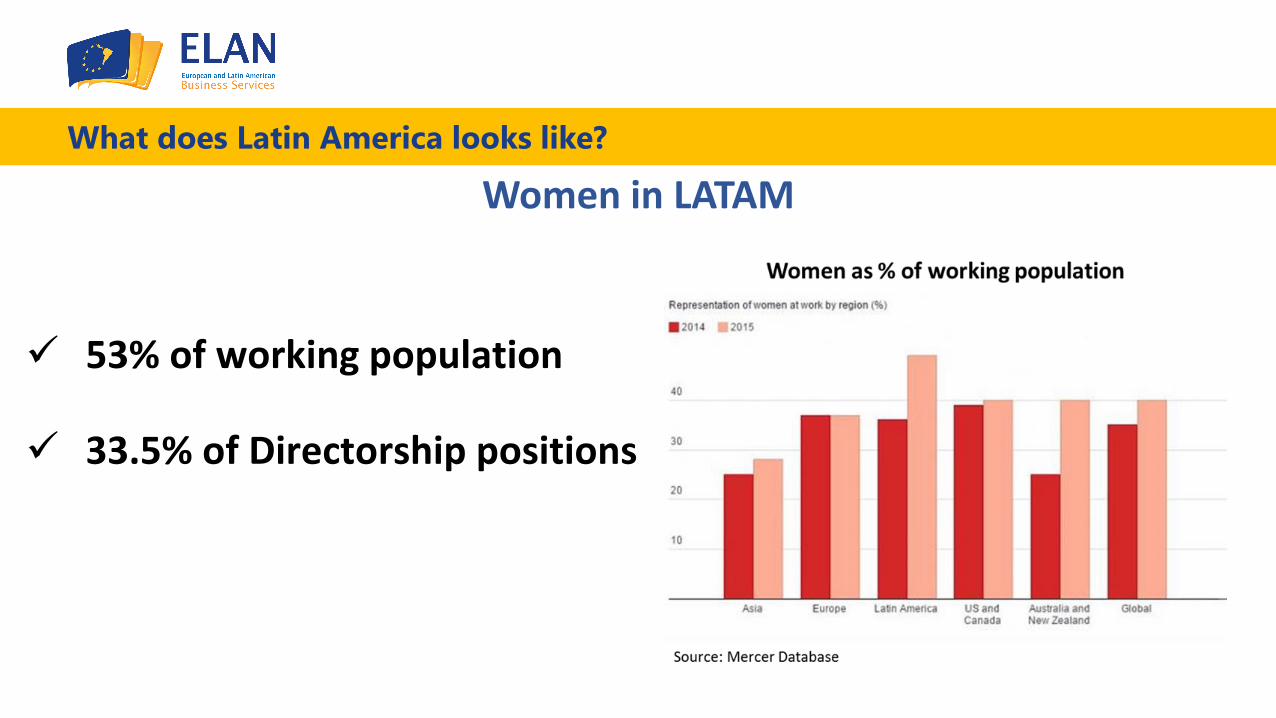

Women in LATAM

53% of working population

33.5% of Directorship positions

What does Latin America looks like?

Women in LATAM – MERCER Research 2015

What does Latin America looks like?

Latin America trading blocs

Doing business in Latin America

World Bank ease οf doing business index

Doing business in Latin America

Corruption perceptions

Doing business in Latin America

161.000 million US$ will be invested in the next 5 years

• Transportation and logistics90.417 million US$

• Oil and gas infrastructures35.500 millions US$

• Energy26.226 MUS$ In 2030 50% to be covered withrenewable energies

Doing business in Latin America

Fastest growing consumers markets 2010-2015

Doing business in Latin America

EU-LATAM trade

Doing business in Latin America

EU-LATAM trade

Doing business in Latin America

FDI in LATAM

Doing business in Latin America

FDI in LATAM

Doing business in Latin America

EU FDI in LATAM

EUR 2.260 billion= 40.2%

EUR 591.1 billion= 10.5%

EUR 490.6 billion= 8.77 %

EUR 651.4 billion= 11.6%

EUR 168.7 billion= 3%

EUR 1.157 billion= 20.6%

Doing business in Latin America

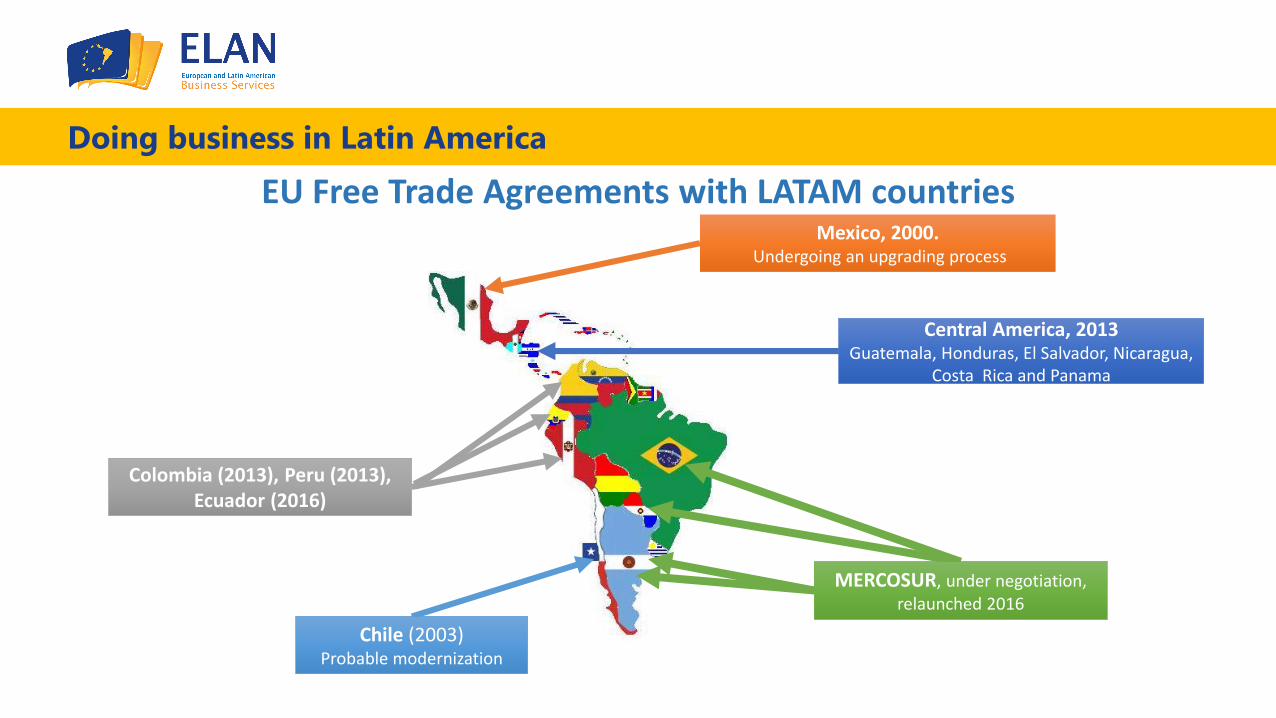

EU Free Trade Agreements with LATAM countries

Colombia (2013), Peru (2013), Ecuador (2016)

Mexico, 2000.Undergoing an upgrading process

Chile (2003)Probable modernization

MERCOSUR, under negotiation, relaunched 2016

Central America, 2013Guatemala, Honduras, El Salvador, Nicaragua,

Costa Rica and Panama

Agroindustry

Food sector in LATAM

• LATAM is the largest net exporter of food in the world

• LATAM accounts for 16% of total global food and agriculture exports and 4% of total food and agriculture imports.

• 43% of imported foods are correspond to intrarregional trade

• The region is one of the few parts of the world with significant resources of unexploited agricultural land (concentrated in Brazil and Argentina)

• Raising productivity will be essential to meet domestic food needs or to maintain or enhance export competitiveness.

Food sector in LATAM

Food sector in LATAM

• Global influences: health, urbanization, sustainability, food safety,

• Increased demand for high-quality foodstuffs

• Convenience foods, organic products and functional foodstuffs impressive growth rates, albeit starting from a relatively low level.

• Dual economy within each individual country: market niches vsmass market

• Opportunities for smaller and medium-sized EU businesses in niche markets

Agroindustry

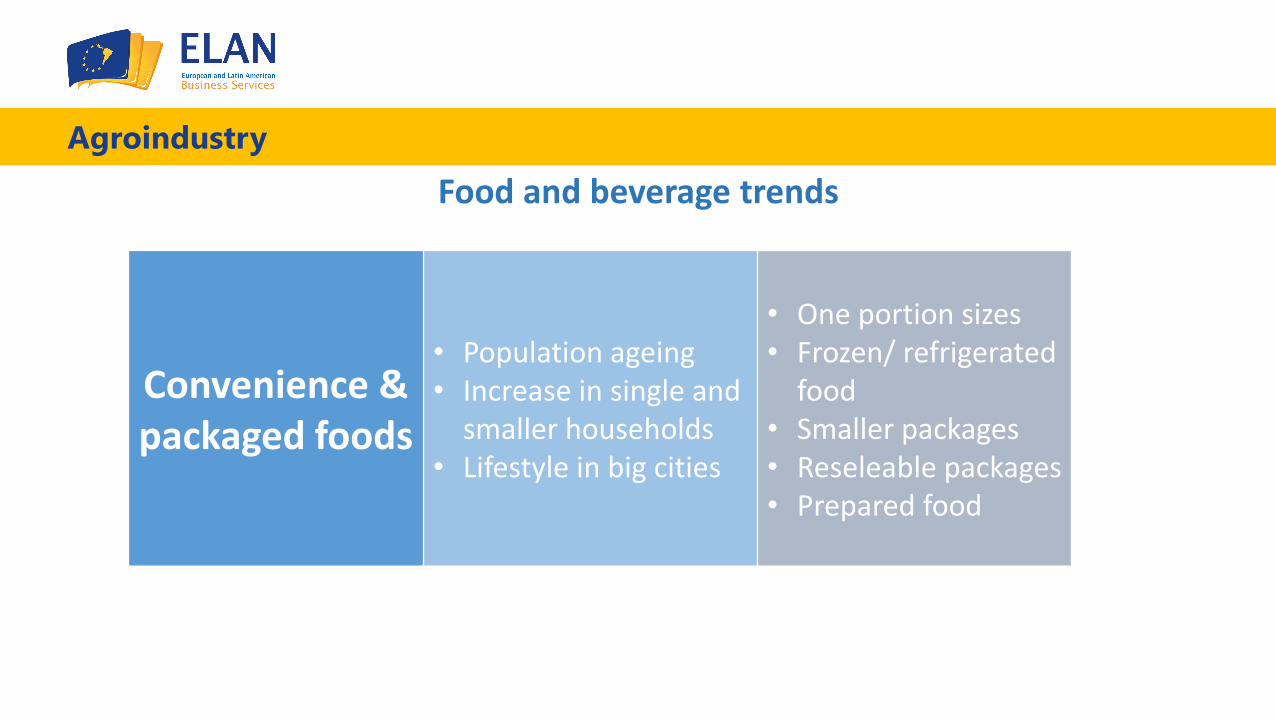

Food and beverage trends

Convenience & packaged foods

• Population ageing• Increase in single and

smaller households• Lifestyle in big cities

• One portion sizes• Frozen/ refrigerated

food• Smaller packages• Reseleable packages• Prepared food

Agroindustry

Food and beverage trends

Indulgence& pleasure

• Income growth• Higher educational

level

• Gourmet and premium products

• Use of ingredients: chocolate, cheese, milk

• Food service

Agroindustry

Food and beverage trends

Health

• Population ageing• Higher education

level• Lifestyle in large cities• Obesity and general

health concerns

• “Healthy” foods• Organic / ecological

certifications• Functional foods• Light and diet foods• Label information

Agroindustry

Food and beverage trends

Safety

• Increase in income• Higher education

level• Health consciousness

• Traceability• Brand reliability• Label information

Agroindustry

Food and beverage trends

Sustainability& ethics

• Increase in income• Higher educational

level• Tourism and travel• Environment

concerns

• Recyclablepackaging

• Reduction of packaging

• Fair tradecertification

• Label information

Agroindustry

Food and beverage trends

Imported foods

• Increase in income• Higher educational

level• Tourism and travel

• Packaged foods• Packaging• Food service, hotels

and restaurants• Chocolate, cheeses,

premium olive oil, snacks, premiumwines and spirits

Agroindustry

Health concerns

• Functional food and beverages market in LATAM will value US$ 21 billion in 2020• Change in lifestyle and increasing of disorders such as diabetes and cardiovascular

diseases create opportunities for stevia, amino acids, antioxidants, enzymes, fibers, proteins, probiotics, prebiotics, phytosterols and polyphenols

Agroindustry

Health concerns

Agroindustry

Health concerns

Agroindustry

Health concerns

Agroindustry

Sustainability & ethics

• LATAM accounts for almost 20% of global organic food trade.

• 2.2 million organic producers worldwide, 400.000 in LATAM

• Mutual recognition and equivalence systems: Chile (2016), Colombia (in progress)

• Consumer awareness of sustainability issues is rising; however awareness is translating slowly into demand

• Many Latin American perceive organic, fair trade and other eco-labeled products as luxuries.

Agroindustry

Favorite Snacks

Agroindustry

Yogurt

• With rising population demand for yogurt and other dairy products are also increasing in LATAM• Probiotic curd, frozen yogurt, soy yogurt, low fat variety, flavored yogurt are some of the most

popular varieties in the market. • Since increasing obesity is serious threat in LATAM, people are demanding variety of low fat

yogurt for meal replacement. • Demand for drinking yogurt is soaring in Latin America.• Demand for flavored yogurt with low sugar content is increasing.• Because veganism is increasing in Caribbean Nations, people are looking for dairy free

alternatives: demand for soy yogurt is increasing substantially.• Since gourmet food items are gaining admiration throughout the Latin American region,

demand for yogurt with expensive berries and nuts, yogurts with exotic flavors is rising.

Agroindustry

Alcoholic drinks

• LATAM is the second highest per capita consumer of alcohol worldwide

• Huge surge in demand for alcoholic drink products.

• Unregulated marketing, policies and low taxes are contributing to the growth of alcohol consumption

• Packaging has played an important role, with a wide range of offerings by alcoholic drink manufacturers contributing to the market growth.

• Even though, glass is the major material used for packaging, plastic packaging for alcoholic beverages is also available in some of the developing countries. Apart from these, metal cans and PET bottles are also being used for alcoholic drinks packaging.

Agroindustry

Most common errors made by exporters

Agroindustry

Strategies for EU exporters• A niche market

– Gourmet, specialized food,…

– Healthy, low sugar, functional

– Tourism and food service channel

• Differentiated products, innovation

• Brand protection

• Opportunities for food technology and food production (weakdomestic supply)

Building materials

Building materials

• Fast-growing populations and middle class• Rapid urbanization process• Increasing demand for commercial, retail, and industrial properties has

greatly boosted building construction and related product sales.• Government investment in public infrastructure has stimulated

construction spending and generated a considerable product demand.• Small construction sectors and underdeveloped public infrastructures.

Overview

Building materials

Overview

Building materials

Homebuilding

Building materials

The outlook for the construction, homebuilding and building materials sector in Latin America will be stable for the region as a whole in 2017

• Improvements in Mexico's homebuilding industry offset ongoing weakness in Brazilian construction

• Revenues for Mexican homebuilders will grow between 5% and 15% next year, largest growth will happen in the low-income housing market.

• The sector faces a more challenging outlook in Brazil, where the homebuilding contraction began in 2012 and the recession worsened it in 2015. Inventories remain high and while a gradual, partial recovery is likely next year,

a complete turnaround won't come until mid-2018

Homebuilding

Building materials

• Latin America currently spends approximately 1.7% of gross domestic product (GDP) on infrastructure development. This is less than any other region of the world except Africa.

• It is estimated that the regional infrastructure market will grow to $114 billion by 2018.

Infrastructure

Building materials

Infrastructure Growth PotentialThe top 100 Latin American infrastructure projects total US$138.7 billion• Airports• Electricity – Generation• Electricity – Transmission• Highways and Bridges• Internet Communications Technology• Oil and Gas• Ports and Logistics• Rail• Urban Mass Transit• Water and Wastewater

Infrastructure

Building materials

Infrastructure Growth PotentialThe top 100 Latin American infrastructure projects total US$138.7 billion

• 21 projects valued at $48 billion are in Brazil• 15 projects at $17 billion are in Colombia• 8 projects at $20 billion are in Chile• 7 projects at $12 billion are in Mexico

Infrastructure

Building materials

• Strong national industry: Until 2007, the Brazilian trade balance surplus – exports less imports – of the construction sector was more then 1 billion BRL.

• Domestic industry is not competitive: since 2008, the expansion of the civil construction and the appreciation of the real the import/export situation in the country has been changing with imports surpassing exports by 1.1 billion BRL.

• Products with high added value, such as ceramics, fittings and metals, which have high prices in Brazil have preference for importers.

• Cranes, freight elevators, racks and machines for construction of foundations, because of the shortage of domestic supply, can be added to the list of the most sought-after items to be imported to Brazil.

• Currently, Brazil's biggest partners in the marketing of construction materials are China and Turkey focusing on steel pipes and finishing products. While Poland is very competitive in glass.

Brazil

Building materials

• The National Association of Construction Materials Retailers (ANAMACO) estimated an overall growth of 6% in 2016, after a 5.8% dip in 2015.

• Its monthly survey of sales found that, while the South and South-East had contracted slightly in February, there was growth of 18% and 10% in the Centre-West and the North.

Brazil

Building materials

• According to a 2015 study by the São Paulo Federation of Industries (FIESP), and the Brazilian Equipment and Maintenance Technology Association (Sobratema), the infrastructure and construction industries are expected to receive about US$1 trillion in investment through 2022.

• As a result, annual average investment should be approximately US$125 million, equivalent to 9.8% of GDP.

Brazil

Building materials

• Brazilian families will be expanding at an average annual rate of 2% over the next 23 years

• The country will need 11.5 million new homes over the next seven years, which means its needs to build around 1.4 million homes per year.

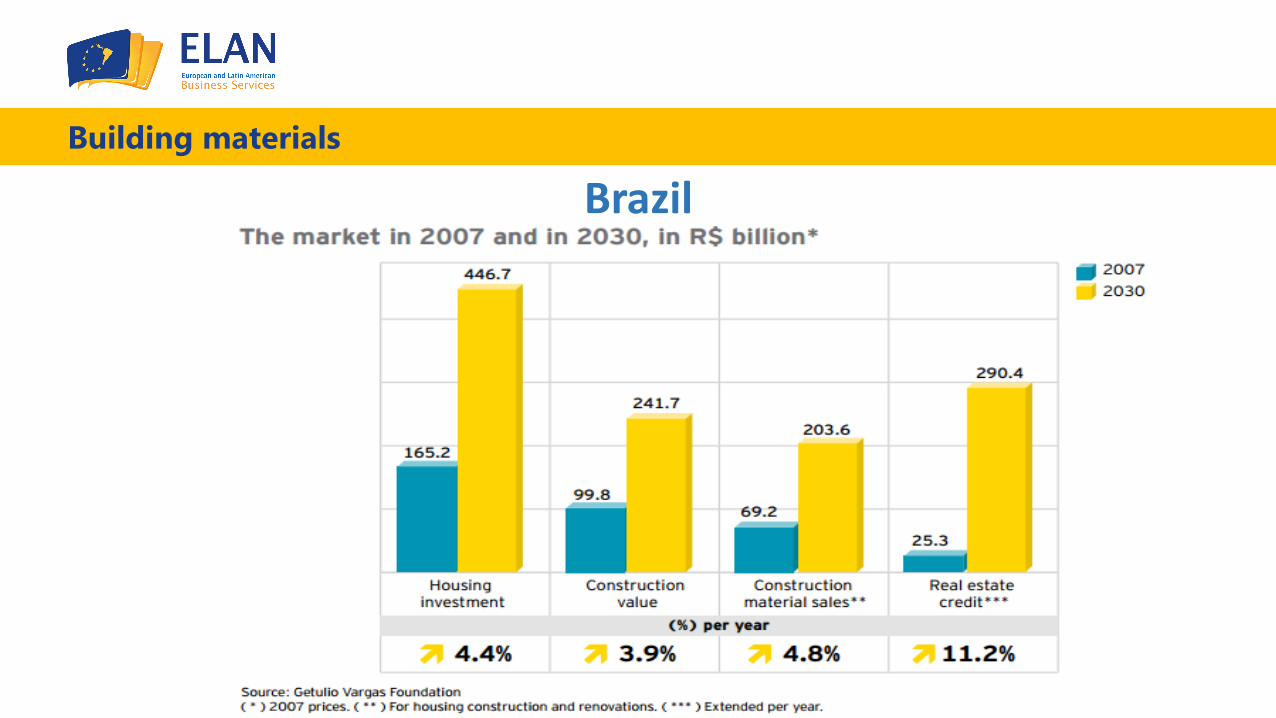

• Construction company turnover, for example, will jump from R$ 53.5 billion in 2007 to R$ 129.6 billion in 2030

Brazil

Building materials

• The Brazilian Federal Government is also providing tax incentives that will create opportunities for refurbishing, building, acquiring or operating hotels, as travel and tourism continues to grow.

• As a result, new hotel construction is underway in several cities, and several current hotels are being refurbished and upgraded.

Brazil

Building materials

• Spending for public works projects, including BUS Rapid Transport (BRT) and Vehicle on Light Tracks (VLT) systems, dedicated bus lanes, subway and commuter trains, and the implementation of integrated monitoring systems, projects to be around US$2.7 billion each year.

• In transportation and logistics, forecasts are for a total investment of US$95 billion, which includes 1,167 current projects country-wide, of which 99% should be completed by 2023.

Brazil

Building materials

Brazil

Building materials

Brazil

Building materials

• Mexican construction industry grew only 2.8 % in 2015 instead of the 6.5% initially forecasted

• Building and construction sector in Mexico is reliant on federal government programs.

• In 2014, the 2014-2018 National Infrastructure Program (NIP) was launched, with $586 billion investment

Mexico

Building materials

• The total value of federal government construction projects during 2015 was estimated at $107 billion:40 % was allocated to PEMEX (government-owned oil company)22 % to highway construction22 % to housing developments and multi-purpose buildings16 % to other infrastructure projects.

• The Mexican states that received the most funds were State of Mexico, 10 %; Mexico City, 9 %; Veracruz, 9 %; Chiapas, 7 %; and Queretaro, 7 %.

Mexico

Building materials

• The new housing initiatives announced in the NIP are intended: to address a shortfall of an estimated 8 million housing units to promote growth in the housing industry in the short and medium-

term; and to increase vertical housing developments in major cities across the

country. • These initiatives will offer opportunities to developers and suppliers focused

on the low-income market• Based on these initiatives, industry sources estimate that the housing

market will increase 5% percent from 2016 to 2018.

Mexico

Building materials

• Mexico is moving towards green, or environmentally-friendly, activities. • Mexico joined the World Green Building Council (WGBC) and is learning best

practices from Europe and the US• Policy efforts to promote green buildings are relatively new and generally focused on

the housing sector. • Although green construction growth in Mexico continues on a positive trend, the

numbers for sustainable construction remain small. According to the Mexican Green Building Council, Mexico has over 44 buildings with LEED certification. During 2014 and 2015, over 250 construction projects with an estimated investment of $37.5 million subscribed to the certification process.

• Projects include tourism real estate development, marine projects, thematic and recreational parks, residential, industrial and commercial.

Green building

Building materials

• Demand for cement, steel bars and glass is growing faster than local suppliers’ abilities to provide them

• There is also a high demand for plywood, another important raw material for the construction industry. o Potential niche markets exist in the furniture manufacturing sector

and the interior decoration sector, particularly in flooring, paneling and molding.

Mexico

Building materials

• Opportunities include: wooden windows, doors, flooring, and frames from sustainable woods; ecological paints, coverings and coatings; ecological concrete pipes for potable water and sewage; energy saving light bulbs; ecological pipes and fixtures for electrical applications; skylights; green-certified electrical devices and home appliances; permeable concrete; green roof systems and equipment; high-efficiency air conditioning systems and equipment; high-efficiency HVAC equipment for commercial buildings and hospitals; natural insulation materials; ecological blocks and bricks; and insulation, acoustics, and fire retardant thermal protection materials.

Mexico

Building materials

• For EU firms interested in entering Mexico’s housing industry, one of the best options is to partner with a Mexican distributor or housing developer or construction firm that is active in the housing industry.

• Mexican companies’ knowledge of the market, the labor and legal aspects involved in this industry is invaluable to EU firms.

In addition, it is important that manufacturers register as building materials suppliers with INFONAVIT, FOVISSSTE, FONHAPO, PEMEX, CEF, and State housing institutes.

Mexico

Introduction to business culture in Latin America

Communication and business culture

Overview

• 19 countries • 626 million people• Languages: Spanish is spoken as first language by about 60% of

the population Portuguese is spoken by about 34% of the population About 6% of the population speak other languages

• Religion: Christians (90%), Catholics about 70%

Communication and business culture

Ethnic diversityOne of the most diverse regions in the world. The specific composition varies from country to country:

People with European ancestry are the largest single group, and along with people of part-European ancestry, they combine to make up approximately 80% of the population.

Most of the earliest settlers were Spanish and Portuguese After independence, the most numerous immigrants have been Spanish and

Italians, followed by Germans, Levantine Arabs, Poles, Irish, British, French, Russians, Belgians, Dutch, Scandinavians, Ukrainians, Hungarians, Croats, Swiss, Greeks, and other Europeans

Communication and business culture

Context- vs. Content-Focus

In many EU business settings there is a strong emphasis on the content of communications: the data, facts and specific details.• Both verbal and written communications tend to be brief and to-the-point.In Latin America generally there is a broader focus that includes contextual factors such as relationship, circumstances, timing, and social appropriateness.• Consequently, the Latino may seem ambiguous or evasive to the some EU

counterparts.• At the same time, however, some EU cultures may be perceived as

impersonal and overly direct or blunt to a Latino person

Communication and business culture

“Molecular” vs “Atomic” social structure

• LATAM countries are usually rated low on the individualism scale.• The use of networks and connections, the exchange of information and

favors, reflect the “molecular” structure of LATAM societies.• This requires that one be more indirect, diplomatic, non-confrontational, and

cautious in communicating with others because there is a positive or negative multiplier effect in every social or business transaction.

• The EU counterpart may feel that the Latin American is being excessively diplomatic or “flowery,” which may be associated with insincerity.

• In contrast, the EU person’s individualism may be perceived as being selfish or egotistical

Communication and business culture

Transaction oriented vs. Relationship building

• In many EU cultures, people who work together may develop personal relationships over time but the task comes first.

• Latin Americans tend to feel that it is essential to invest in establishing a relationship before focusing on the task:

A warm-up period is typically required to create a good interpersonal environment in which the task can be accomplished most effectively.

An important clue in this regard is the high desirability of being considered simpático or likeable and accessible.

Communication and business culture

“Time is money”...vs “Time is precious”

The pace of life and work varies within Latin America. However, it is generally less intense than in the EU:• Building and maintaining relationships, attending to one’s “molecular” networks,

and managing the complex contextual dimensions of business simply takes more time.

Time is a guideline, but rarely a deadlineThe EU businessperson may appear hasty, rushed, and pushy, while the Latin American may seem to lack a sufficient sense of urgency.

Communication and business culture

Personal space

• The accepted amount of personal space that each person has or needs is muchsmaller in Latin America than in Europe.

• People will touch you more, stand closer when they talk to you and generally getup close and personal

• Latinos will usually stand closer together during conversations, so be preparedfor that plus casual touching

• You may even be startled to have a Latin businessman hold your elbow whileconversing, or walk down the street arm-in-arm

Communication and business culture

Negotiations according to polychronic cultures

Negotiations do not follow a linear logic

Negotiations stages are not neatly sequential:

a new stage may begin while the earlier stage is still beingdiscussed, and issues already agreed are open for subsequent discussion

Communication and business culture

Negotiations according to polychronic cultures

Negotiators from polychronic cultures tend to start and end meetings at flexible times take breaks when it seems appropriate be comfortable with a high flow of information expect to read each others' thoughts and minds sometimes overlap talk view start times as flexible and not take lateness personally.

Communication and business culture

Business conversations

• Good conversation topics include sports, art, history, and family.

• Avoid topics like politics, poverty, religion, or neighboring countries.

Communication and business culture

Eating

• Business lunches are common throughout Latin America, and they’re usually long.

• Dinner is a purely social event and can occur very late.

Communication and business culture

Become the friend of your business partner

• Latinos are very warm and friendly people and enjoy social conversationbefore getting down to business.

• This is a calculated process aimed at getting to know you personally.• Latinos tend to be more interested in you, the person, than you as a

representative of some faceless corporation.

www.elanbiz.org

Elanbiz

Elan Biz Social

Javier Sanchez

Program funded by the

European Union

Implemented by the consortium led by AESA